Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.06 Billion |

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 4.33 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Ceramic Tiles Market Analysis by Mordor Intelligence

The Egypt ceramic tiles market size is expected to grow from USD 3.06 billion in 2025 to USD 3.24 billion in 2026 and is forecast to reach USD 4.33 billion by 2031 at 5.94% CAGR over 2026-2031. Ongoing government-backed mega-projects, a tourism rebound, and the phase-out of natural-gas subsidies have reinforced demand while lowering unit production costs for large domestic manufacturers.[1]Housing and Building National Research Center, “Annual Construction Materials Review 2025,” hbrc.gov.eg Population growth that requires 300,000-400,000 new housing units each year, coupled with LE 3.5 trillion (USD 72.9 billion) earmarked for FY 2025/2026 public-sector investment, ensures a sustained construction pipeline. Greater Cairo & Giza remain the primary consumption centers, yet coastal tourism districts and Upper Egypt are registering faster incremental gains as infrastructure spreads inland. Intensifying competition from the Russian Industrial Zone and other foreign entrants is accelerating technology upgrades across the value chain to defend domestic share and capture new African export opportunities.

Key Report Takeaways

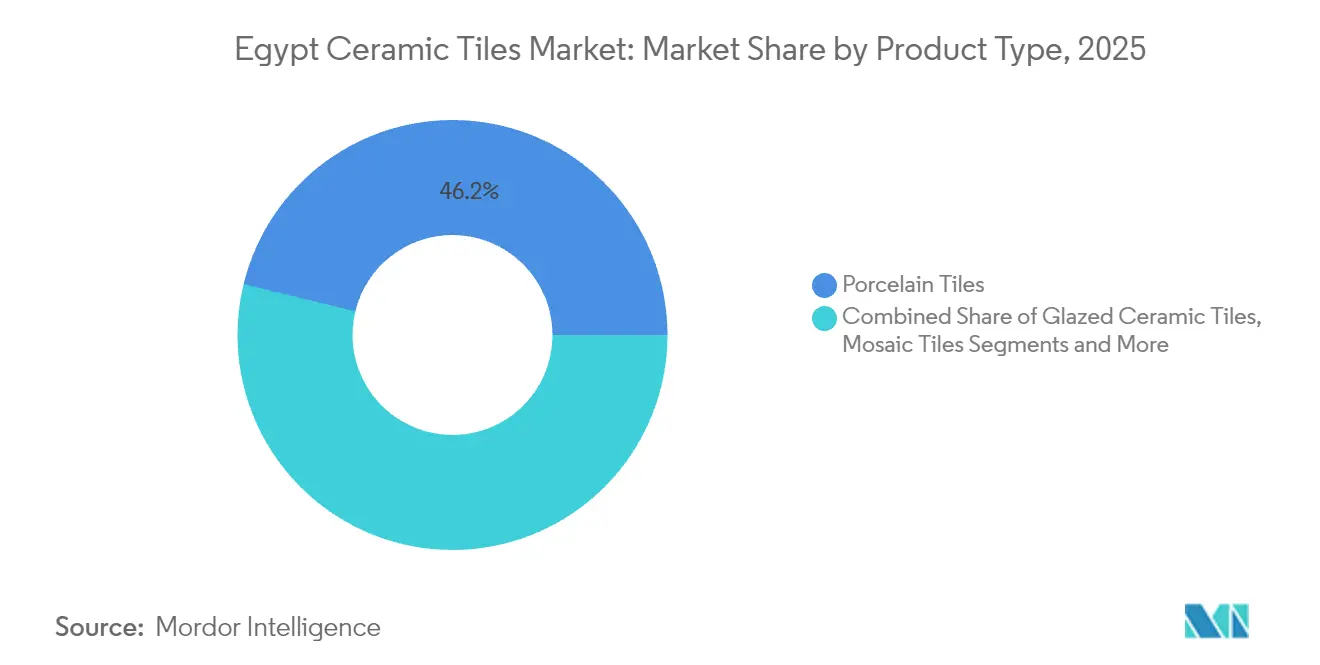

- By product type, porcelain tiles led with 46.20% of Egypt ceramic tiles market share in 2025; mosaic tiles are forecast to expand at a 6.25% CAGR through 2031.

- By application, floor coverings commanded 66.70% share of the Egypt ceramic tiles market size in 2025, while wall applications are advancing at a 5.65% CAGR to 2031.

- By end-user, residential construction accounted for 67.45% of demand in 2025; commercial projects are projected to rise at a 5.96% CAGR between 2026-2031.

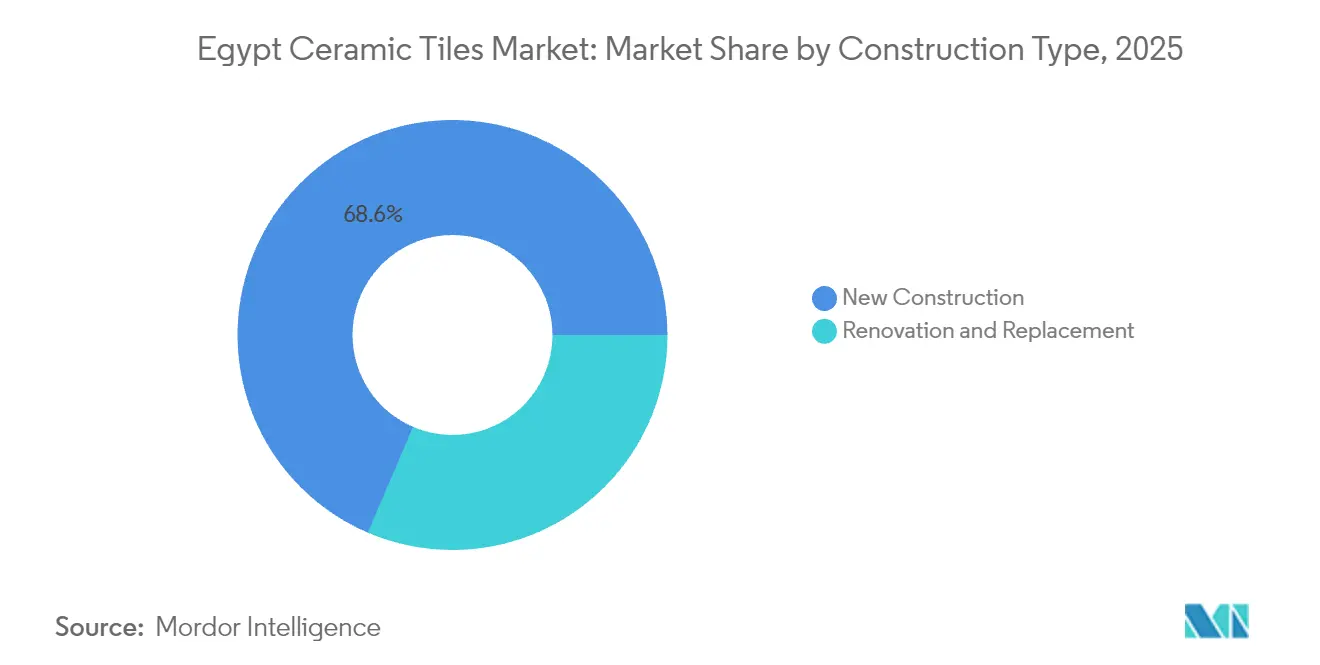

- By construction type, new builds contributed 68.55% share of the Egypt ceramic tiles market size in 2025, whereas renovation is poised for 7.28% CAGR growth over the same horizon.

- By distribution channel, specialty tile stores maintained a 43.70% share in 2025; online platforms are growing fastest at a 6.78% CAGR to 2031.

- By geography, Greater Cairo & Giza held 40.95% of Egypt ceramic tiles market share in 2025, while Red Sea Governorates represent the fastest-rising region with a 6.52% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led Housing Mega-Projects | +1.8% | Greater Cairo & Giza, New Administrative Capital | Medium term (2-4 years) |

| Rising Urban Population & Residential Construction Surge | +1.5% | National, concentrated in Greater Cairo & Alexandria | Long term (≥ 4 years) |

| Tourism Sector Revival Driving Hospitality Construction | +1.2% | Red Sea Governorates, Alexandria & Mediterranean Coast | Short term (≤ 2 years) |

| Shift Toward Porcelain Tiles For Superior Durability | +0.9% | National, premium segments in urban centers | Medium term (2-4 years) |

| Natural-Gas Subsidy Reforms Lowering Production Costs | +0.7% | National, manufacturing hubs | Short term (≤ 2 years) |

| AfCFTA-Enabled Export Opportunities To Sub-Saharan Africa | +0.6% | National, export-oriented facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led Housing Mega-Projects

Egypt’s flagship New Administrative Capital alone needs ceramic finishes for more than 300,000 housing units each year, securing long-run demand visibility for both mass-market and premium formats[2]World Bank Group, “Urban Development Strategy for Egypt,” worldbank.org. The LE 3.5 trillion (USD 72.9 billion) public-investment target for FY 2025/2026 allocates large parcels to social housing, roads, and public facilities that embed tile procurement in every tender.[3]World Bank Group, “Urban Development Strategy for Egypt,” worldbank.org Public-private partnership structures invite domestic producers to lock in multiyear supply contracts that mitigate volume risk. Ras El Hekma’s USD 35 billion mixed-use coastal project further boosts institutional and leisure demand. These mega-projects allow manufacturers to scale kilns at optimal utilization, spreading fixed costs and accelerating return on new digital printing lines.

Rising Urban Population & Residential Construction Surge

Egypt’s cities must add 300,000-400,000 new dwellings annually simply to avoid a housing shortfall, channeling sustained volumes into the Egypt ceramic tiles market. The government’s modern-methods-of-construction framework mandates quality façade and flooring materials, nudging developers toward durable tile solutions. Satellite towns encircling Cairo and Alexandria disperse future demand, prompting distributors to widen last-mile logistics networks. Rising middle-class incomes are shifting purchases from basic glazed tiles to larger format porcelain and decorative mosaics that carry higher margins. Urban densification policies simultaneously raise renovation activity in legacy districts, injecting counter-cyclical resilience.

Tourism Sector Revival Driving Hospitality Construction

International arrivals rebounded sharply in 2024, reigniting hotel and resort construction that requires high-performance, salt-resistant tile surfaces in Red Sea governorates[4]Ministry of Tourism & Antiquities, “Visitor Statistics & Hotel Pipeline—Red Sea Governorates 2024,” mota.gov.eg. Five-star properties specify large-format porcelain panels for lobbies, pools, and spas, supporting premium unit value in the Egypt ceramic tiles market. Co-investments by global chains enforce stringent technical standards, pushing domestic producers to certify slip-resistance and lifecycle durability. Airport expansions, marina upgrades, and ancillary retail clusters surrounding resort corridors add breadth to commercial tile uptake. Seasonal spikes enable factories to smooth production cycles by allocating kiln capacity away from lower-margin contracts during peak tourism procurement windows.

Shift Toward Porcelain Tiles for Superior Durability

Porcelain accounted for 46.5% of total shipments in 2024 because local producers now achieve sub-0.1% water-absorption rates at 1,220 °C firing, matching European benchmarks. High mechanical strength and compatibility with large-format pressing meet the needs of corporate offices, transport hubs, and luxury residences. Research confirms that up to 95% local raw materials suffice, insulating firms from currency swings on imported inputs. Developers view porcelain’s lifecycle cost advantage as a hedge against future maintenance outlays, justifying premium positioning. As African neighbors adopt stricter building codes, Egyptian porcelain is poised for export share gains under AfCFTA tariff concessions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Depreciation Inflating Imported Equipment Costs | -0.8% | National, manufacturing centers | Short term (≤ 2 years) |

| Volatile Prices Of Feldspar, Kaolin & Other Raw Materials | -0.6% | National, raw material dependent facilities | Medium term (2-4 years) |

| Intermittent Electricity Shortages Impacting Kilns | -0.5% | National, concentrated in industrial zones | Short term (≤ 2 years) |

| Stricter Emissions Regulations On Gas-Fired Kilns | -0.4% | National, gas-dependent manufacturing facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Depreciation Inflating Imported Equipment Costs

Successive pound devaluations raised landed prices of Italian presses, Spanish glazers, and German digital printers by more than 30% between 2024-2025, stretching capital budgets at mid-tier firms. Spare-part inventories denominated in euros further erode working-capital buffers, forcing leaner maintenance cycles that risk unplanned outages. Smaller plants lack the scale to hedge FX exposure, delaying essential upgrades that underpin product diversification. While devaluation supports exports, only large producers with established African channels can offset equipment cost spikes through foreign-currency receipts. Consequently, industry consolidation may accelerate as under-capitalized entrants exit or pursue joint ventures.

Volatile Prices of Feldspar, Kaolin & Other Raw Materials

Domestic feldspar output of 400,000 metric tons covers basic needs but quality variance demands beneficiation steps that add cost and complexity. Imported specialty clays are subject to freight rate volatility, with Red Sea shipping premiums swelling after regional security disruptions. Research on substituting Egyptian syenite and trachyte shows promise but requires recalibrated firing curves and glaze formulations, delaying commercialization. Price instability obliges firms to hold larger safety stocks, tying up cash and warehouse space. Producers investing in captive beneficiation plants and supply-chain digitalization can mitigate volatility, creating a performance gap with smaller rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Premium Shift

Porcelain tiles contributed 46.20% of total shipments in 2025 as local lines achieved European-grade absorption rates and flexural strength benchmarks. This technological leap positions porcelain as the volume and value anchor of the Egypt ceramic tiles market, allowing manufacturers to target high-end domestic projects and AfCFTA export orders simultaneously. Mosaic tiles, while niche, are tracking a 6.25% CAGR as architects revive artisanal aesthetics for boutique hotels and upscale residences. Glazed ceramic remains entrenched in price-sensitive housing programs whose budgets dictate cost efficiency over premium performance. Unglazed formats sustain industrial demand where slip resistance outweighs decorative appeal; however, line automation is enhancing texture options to capture incremental value.

Locally sourced syenite now substitutes up to 35% of imported feldspathic flux in porcelain bodies, curbing forex outflow while maintaining surface whiteness after iron-oxide mitigation. Optimal pressing at 45 MPa and firing at 1,220 °C for 20 minutes enables thinner, larger slabs that command higher margins in commercial halls and airport terminals. The Egypt ceramic tiles market size for porcelain alone is projected to top USD 2.01 billion by 2031, underscoring its strategic relevance. Producers integrating ink-jet lines with 400-dpi heads can replicate natural stone veining, enhancing differentiation versus imported Spanish designs. Decorative and hand-made tiles serve luxury villas and heritage restorations, reinforcing Egypt’s contribution to cultural tourism experiences.

By Application: Floor Segment Leads Despite Wall Growth

Floor coverings captured 66.70% of sales in 2025 due to standardized specifications in mass housing and retail chains that streamline procurement. Project contractors prefer 60 × 60 cm glazed porcelain for speed of installation and lower breakage risk, sustaining bulk volumes in the Egypt ceramic tiles market. Wall applications are gaining traction at a 5.65% CAGR as homeowners seek statement feature walls and moisture-resistant kitchen backsplashes. Large-format ventilated façades are emerging in commercial towers, but local codes are still evolving to codify fixative and anchoring requirements. Roofing tiles form a smaller niche yet benefit from Egypt’s hot-dry climate where ceramic’s thermal inertia moderates indoor temperatures relative to metal sheets.

In coastal resorts, salt-spray exposure makes porcelain the default for pool decks and walkways, raising average selling prices under hospitality tenders. Recycling initiatives that replace 20% of quarry aggregates with fired-tile waste reduce raw-material costs and support LEED certification points. Antimicrobial glazes developed for healthcare projects now permeate upscale home kitchens, widening their addressable client base. Floor-tile demand is seasonally synchronized with delivery schedules for social-housing tranches, while wall tiles experience steadier replacement cycles in the renovation market. As property developers market turnkey interiors, coordinated floor-wall color palettes drive bundle purchasing, lifting basket sizes per household unit.

By End-User: Residential Strength, Commercial Acceleration

Residential customers absorbed 67.45% of tile output in 2025, anchored by state-subsidized mortgage programs that boost first-home accessibility. Average apartment footprints between 85-110 m² translate into per-unit tile volumes of 125-150 m² for floors and bathrooms, shaping baseline demand in the Egypt ceramic tiles market. Commercial demand is expanding at a 5.96% CAGR, propelled by hospitality upgrades, mall refurbishments, and a new wave of Grade-A office towers in Egypt’s financial districts. Shopping-center operators select high-gloss, abrasion-resistant formats to prolong replacement intervals under heavy footfall. Hospitals specify antimicrobial porcelain with 24-hour silver-ion activity to meet infection-control protocols.

Educational projects drive sustained volumes as the government targets classroom density reduction goals, standardizing slip-resistant floor patterns across regional school builds. Airports and railway stations require thick-body porcelain capable of 3,600 N breaking strength, adding to premium-mix uplift. Residential renovation demand intensifies in mature urban blocks where owners upscale interiors as disposable income rises. Developers of gated communities bundle tiles with turnkey fixture packages, simplifying supply contracts for large manufacturers. The Egypt ceramic tiles industry is responding with modular concept collections that align floor, wall, and outdoor paver aesthetics for cohesive design language.

By Construction Type: Renovation Gains Momentum

New construction sustained 68.55% of turnover in 2025, underpinned by landmark undertakings such as the Green River Park and monorail corridors that punctuate Egypt’s urban transformation. Contractors prioritize reliability and volume discounts, prompting strategic alliances with top three local producers. Renovation work, although smaller in project value, is forecast to outperform at 7.28% CAGR thanks to aging building stocks in Cairo’s 1990s tower clusters. Homeowners opt for contemporary textures and larger tiles to create a perception of space, driving higher price-per-square-meter trends. Insurance-funded building remediation after infrastructure upgrades also channels discretionary budgets toward premium interior finishes.

ISO 13006 adherence is increasingly mandated by municipal permitting offices for structural retrofits, raising the technical threshold for imported low-cost tiles. Renovation cycles are shorter in coastal second homes where salt and humidity expedite surface wear, creating recurring demand. The Egypt ceramic tiles market size linked to renovation is estimated at USD 963 million for 2025 and expected to top USD 1.49 billion by 2031. Digital-platform retailers woo DIY remodelers through augmented-reality room planners and same-day delivery across the Cairo ring road. Manufacturers launch quick-cut formats and adhesive-backed sheets that reduce installation time by 30%, appealing to weekend remodel projects.

By Distribution Channel: Digital Transformation Accelerates

Specialty tile showrooms retained 43.70% of revenue in 2025 by curating extensive design libraries and providing accredited installer networks that guarantee finish quality. Architects prefer these venues for sample reviews and project mock-ups, ensuring their dominant role in the Egypt ceramic tiles market. Online platforms are growing fastest at a 6.78% CAGR as logistics providers roll out metropolitan fulfillment hubs enabling 48-hour delivery. Price transparency and real-time inventory checks resonate with both contractors and retail customers, lifting digital share particularly in wall and mosaic categories. Big-box DIY stores attract budget-conscious homeowners who value one-stop shopping for grout, tools, and plumbing fixtures.

Direct-to-contractor sales streamline bulk deliveries to mega-projects, with remote-sensing trackers providing proof of delivery and GPS-tagged unloading photos for dispute resolution. Manufacturers integrate e-catalog APIs into B2B procurement portals, reducing quotation cycles from days to hours. The Egypt ceramic tiles industry pilots blockchain smart contracts that release payments automatically upon sensor-verified delivery milestones, trimming working-capital lockups. Omnichannel strategies are converging: showrooms leverage virtual-reality visualization to complement in-store samples, while e-commerce brands host pop-up experience centers during peak renovation seasons. Insurance-backed warranties sold online further differentiate digital propositions from traditional cash-and-carry outlets.

Geography Analysis

Greater Cairo & Giza delivered 40.95% of 2025 revenue, a concentration driven by mega-projects such as the Administrative Capital and metro expansions that aggregate high-volume tile procurements. Dense population clusters, an extensive wholesale network, and proximity to major kiln complexes in 10th Ramadan City simplify final-mile logistics. Developers specify large-format porcelain for the capital’s Grade-A offices to signal international quality standards, sustaining premium segment turnover. Residential micro-units often use 60 × 60 cm matte-finish porcelain to balance price and aesthetics, underpinning baseline volumes. Infrastructure upgrades such as ring-road flyovers incorporate anti-skid pavers, broadening industrial and civic applications.

Alexandria & the Mediterranean Coast hold an entrenched customer base owing to resilient tourism traffic and port-linked industrial estates. Sea-spray corrosion risk pushes demand toward porcelain bodies with <0.5% porosity, and port warehouse expansion projects consume unglazed heavy-duty tiles. The Egypt ceramic tiles market gains seasonal uplift each summer as seaside hotels refurbish lobbies to meet peak occupancy expectations. Nile Delta towns like Mansoura and Tanta exhibit fragmented yet steady growth as agribusiness incomes filter into home improvement spending. Improved rail links cut lead times from kiln clusters, enabling same-week replenishment for regional distributors.

Red Sea Governorates—Sharm el-Sheikh, Hurghada, and Marsa Alam—represent the fastest-growing corridor, poised for a 6.52% CAGR to 2031 on the back of yacht marinas, boutique resorts, and expanded cruise terminals. Hotel developers prioritize slip-resistant, UV-stable exterior tiles, pushing average selling prices above national norms. Local showrooms partner with European brands on exclusive collections, intensifying design competition. Suez Canal & Sinai see strategic uplift as the Russian Industrial Zone injects USD 7 billion over the next five years, spawning ancillary tile demand for worker housing and logistics yards. Upper Egypt cities, historically under-served, benefit from rural-urban migration and road upgrades, yet logistics costs keep prices 8-12% higher than in Cairo, capping penetration. Collectively, geographic diversification cushions overall market volatility and broadens the base of design requirements manufacturers must satisfy.

Competitive Landscape

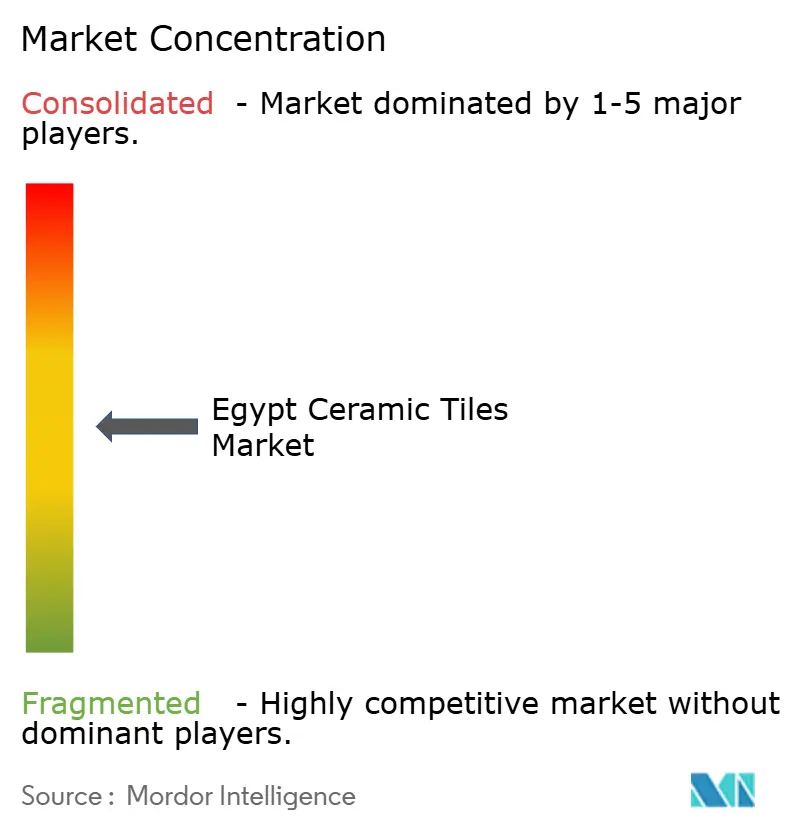

Egypt’s tile sector shows moderate concentration: the top five players hold major market share in 2024, placing the market at a mid-scale consolidation stage. Ceramica Cleopatra Group leads but faces labor-union disputes that triggered temporary line shutdowns in 2024, nudging distributors toward alternative suppliers. Al-Omaraa and Royal Ceramics invested in Italian digital printers that lift print resolution to 1,000 dpi, differentiating marble-look lines targeting premium shopping-mall floors. RAK Ceramics is finalizing a joint venture within the new Ras El Hekma industrial hub, promising annual capacity of 18 million m² and technology spillover on kiln fuel efficiency. EL-Arabi Group piloted hydrogen-enriched firing that cuts CO₂ by 9%, aligning with pending emissions caps.

Strategically, vertical integration into feldspar quarries gives some incumbents cost insulation against raw-material price swings. Others emphasize downstream showrooms and franchised installation teams to capture higher margins and lock in brand loyalty. Online-native entrant Tiles360 leverages algorithmic pricing and same-day Cairo delivery, gaining traction with independent contractors who prize speed over brand heritage. Foreign competition intensifies as Russian, Turkish, and Chinese firms eye the Egypt ceramic tiles market’s AfCFTA export springboard; yet importers face 10-day customs dwell times that erode lead-time advantages. Innovation cycles are shortening: antibacterial surfaces, slip-rating labeling, and 6 mm ultra-thin panels enter portfolios to pre-empt specification shifts among architects.

M&A appetite is rising: two mid-sized family outfits are rumored to be in talks with Gulf funds keen on downstream African distribution rights. Financing costs remain elevated, but export-backed receivables provide hard-currency collateral for kiln upgrades. The Egypt ceramic tiles industry is converging on a technology race where energy efficiency, digital print versatility, and ESG credentials dictate sustainable competitive advantage. Producers that fail to embrace data-driven kiln analytics risk falling behind on quality consistency, a critical factor as high-end developers enforce stricter acceptance criteria. By 2030, capacity additions clustered in Suez and Upper Egypt are projected to shift the supply map, tilting bargaining power toward distributors closer to new growth nodes.

Egypt Ceramic Tiles Industry Leaders

-

Ceramica Cleopatra

-

Lecico Egypt

-

Gemma Ceramics

-

Alfa Ceramic

-

Gloria Ceramic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Ceramica Market 2025 show at Cairo International Convention Center showcased large-format porcelain slabs, matte metallic glazes, and recyclable packaging innovations across 350 exhibitors.

- March 2025: Modon Holding and Elsewedy Industrial Development agreed to co-develop a 10 million m² industrial zone in Ras El Hekma, earmarking clusters for ceramic tile production that could create more than 20,000 jobs.

- September 2024: Ceramic World Review profiled Egypt’s adoption of digital printing and kiln heat-recovery systems, citing export orders to East Africa and the Levant.

Egypt Ceramic Tiles Market Report Scope

This report aims to provide a detailed analysis of the Egyptian ceramic tiles market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights on various product and application types. Also, it analyzes the key players and the competitive landscape in the Turkish ceramic tiles market.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Greater Cairo & Giza |

| Alexandria & Mediterranean Coast |

| Nile Delta |

| Upper Egypt |

| Suez Canal & Sinai |

| Red Sea Governorates |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Greater Cairo & Giza | |

| Alexandria & Mediterranean Coast | ||

| Nile Delta | ||

| Upper Egypt | ||

| Suez Canal & Sinai | ||

| Red Sea Governorates | ||

Key Questions Answered in the Report

What is the current value of the Egypt ceramic tiles market?

The market is valued at USD 3.24 billion in 2026 and is forecast to reach USD 4.33 billion by 2031.

Which product type leads sales in Egypt?

Porcelain tiles hold the lead, accounting for 46.20% of 2025 shipments due to their superior durability and low water absorption.

Which region is growing fastest for ceramic tile demand?

Red Sea Governorates show the highest growth, projected at a 6.52% CAGR through 2031 on the back of tourism-driven construction.

How are online channels affecting tile distribution?

E-commerce platforms are the fastest-growing channel with a 6.78% CAGR, offering real-time stock visibility and rapid delivery.

What key factor is pressuring manufacturers' margins?

Currency depreciation is inflating the cost of imported equipment and spare parts, squeezing margins especially for smaller plants.

Are Egyptian tiles competitive in export markets?

Yes, AfCFTA tariff reductions and proximity to Sub-Saharan markets enhance Egypt’s export position, especially for porcelain formats.

Page last updated on: