Genetic Toxicology Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

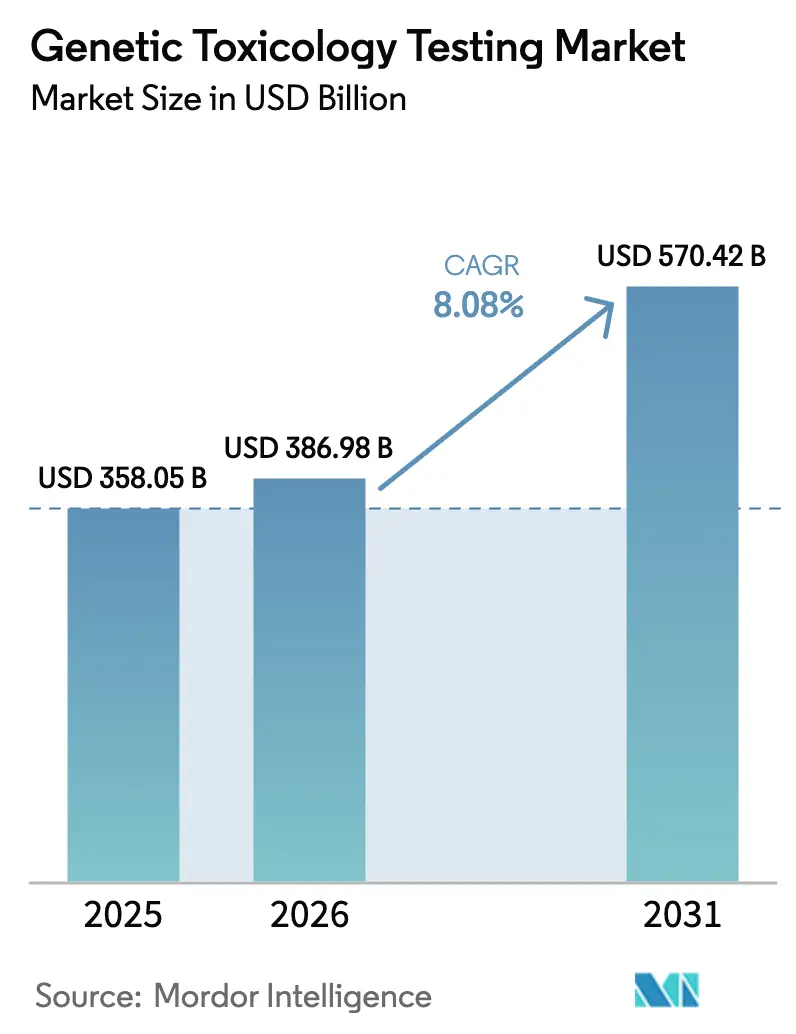

| Market Size (2026) | USD 386.98 Billion |

| Market Size (2031) | USD 570.42 Billion |

| Growth Rate (2026 - 2031) | 8.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genetic Toxicology Testing Market Analysis by Mordor Intelligence

The genetic toxicology testing market size is expected to grow from USD 358.05 million in 2025 to USD 386.98 million in 2026 and is forecast to reach USD 570.42 million by 2031 at 8.08% CAGR over 2026-2031. This solid expansion stems from three converging forces. First, global pharmaceutical R&D expenditure surpassed USD 288 billion in 2024, with oncology and biologics commanding the largest budgets, and each investigational asset must pass increasingly stringent mutagenicity screens before entering the clinic. Second, the United States Food and Drug Administration’s (FDA) Modernization Act 2.0 removed statutory language requiring animal studies for new drugs, creating an immediate pull for in vitro and in silico alternatives. Third, new-generation platforms—3-D spheroid cultures, organ-on-chip devices and transformer-based predictive models—improve assay predictivity and cut study cycle time, prompting both upgrade and green-field investments news-medical.net.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing regulatory push for non-animal (in-vitro & in-silico) assays | +2.1% | Global, with strongest impact in EU & North America | Medium term (2-4 years) |

| Increasing R&D spend in oncology & biologics pipelines | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of high-throughput & 3-D cell-culture platforms | +1.4% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-enabled predictive genotoxicity analytics | +1.2% | Global, led by North America & Europe | Medium term (2-4 years) |

| Standardisation of DNA-damage reference materials | +0.9% | Global, coordinated through OECD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Key Report Takeaways

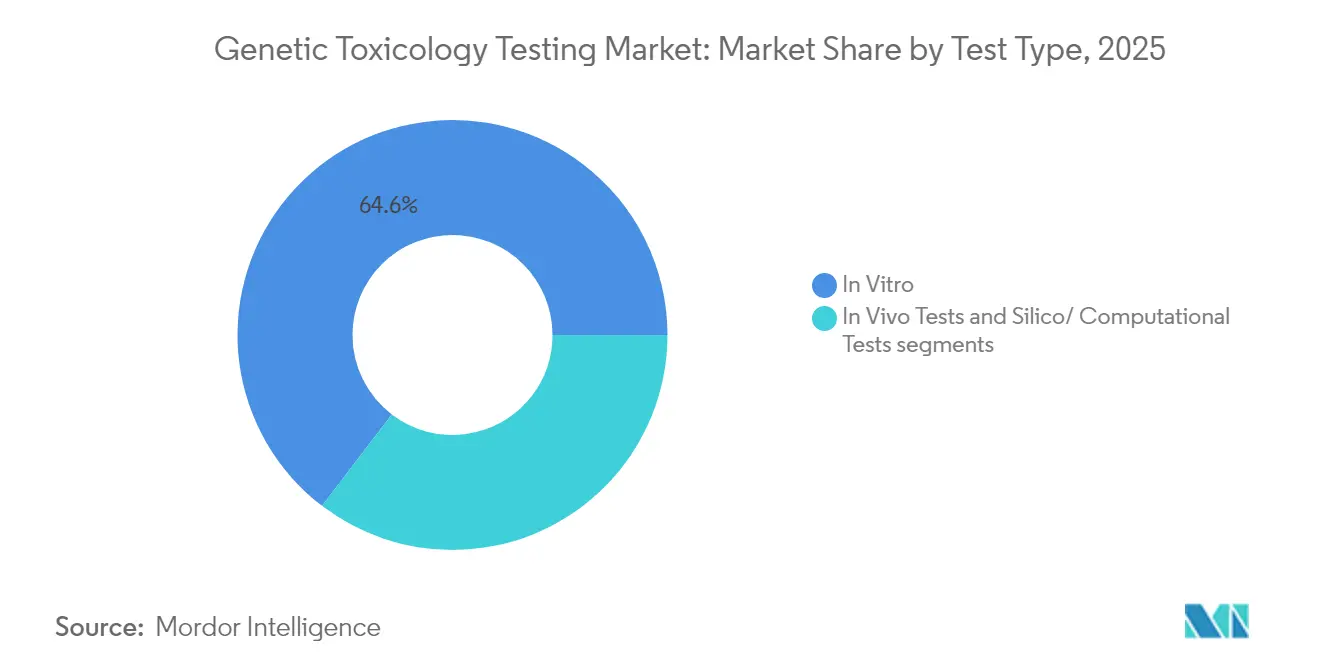

- By test type, in vitro methods captured 64.62% of the genetic toxicology testing market share in 2025, while in silico assays are forecast to post the fastest 8.83% CAGR through 2031.

- By component, reagents and kits held 39.62% of the genetic toxicology testing market size in 2025; the services segment is projected to expand at a 9.21% CAGR between 2026-2031.

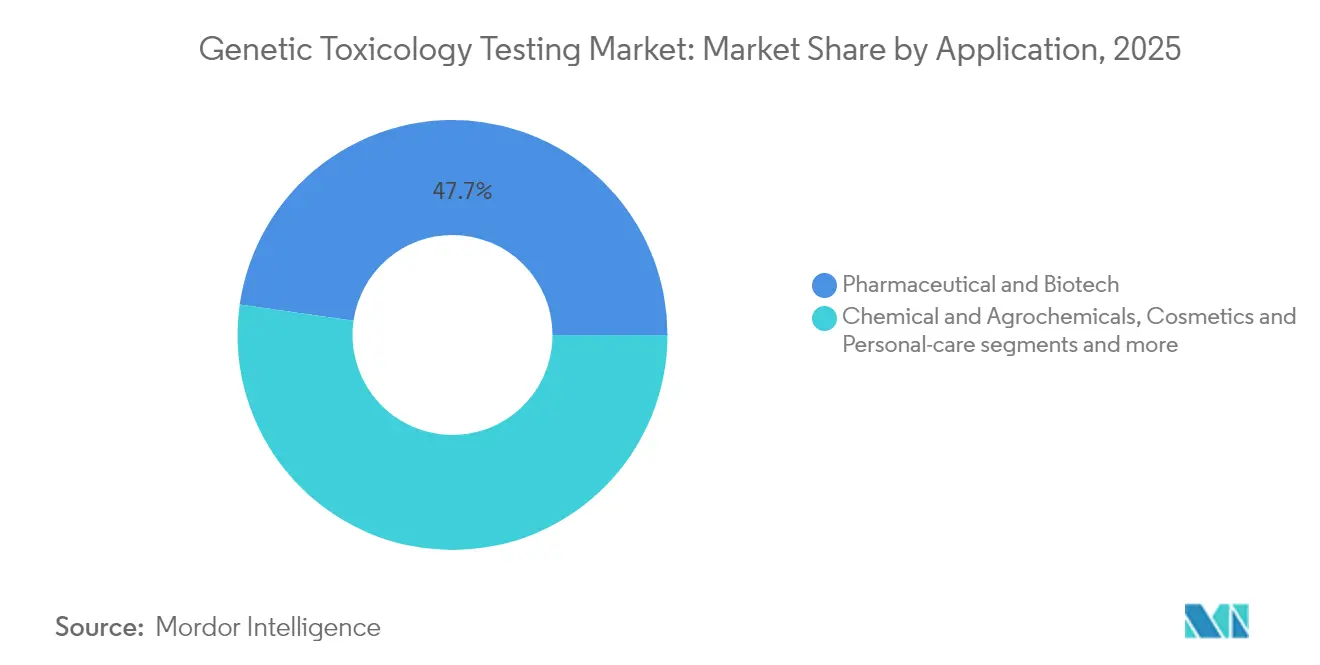

- By application, pharmaceutical and biotechnology testing accounted for 47.74% of the genetic toxicology testing market size in 2025, whereas cosmetics and personal-care testing is advancing at a 9.64% CAGR to 2031.

- By geography, North America commanded 46.05% revenue share in 2025; Asia-Pacific is expected to register the highest 10.05% CAGR over the forecast horizon

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Genetic Toxicology Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing regulatory push for non-animal (in-vitro & in-silico) assays | +2.1% | Global, with strongest impact in EU & North America | Medium term (2-4 years) |

| Increasing R&D spend in oncology & biologics pipelines | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of high-throughput & 3-D cell-culture platforms | +1.4% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-enabled predictive genotoxicity analytics | +1.2% | Global, led by North America & Europe | Medium term (2-4 years) |

| Standardisation of DNA-damage reference materials | +0.9% | Global, coordinated through OECD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory shift to non-animal genotoxicity assays

The FDA Modernization Act 2.0, enacted in late 2024, formally permits in vitro or in silico data to support Investigational New Drug submissions, effectively eliminating the default requirement for rodent studies. The European Union’s REACH program simultaneously broadened animal-testing restrictions by adding 20 new CMR substances to its Annex II and III cosmetics lists, effective February 2025. OECD Guideline Section 4 updates now include organoid-based micronucleus tests, establishing a harmonized path for cross-border data acceptance. Collectively, these moves expand the genetic toxicology testing market by forcing both legacy and pipeline products to re-validate safety using modern, human-relevant methods.

Rising oncology & biologics R&D spend

Total oncology R&D spending surpassed USD 161 billion in 2024, and biologics captured the highest per-asset investment as companies pursue cell- and gene-based therapies. Each modality requires a layered battery of Ames, micronucleus and γH2AX assays because genetic damage can arise through multiple, mechanism-specific pathways. The FDA-endorsed myeloMATCH precision-medicine trial integrates next-generation sequencing with genotoxic endpoints, demonstrating regulatory appetite for complex, multi-readout designs. Elevated spend assures long-cycle throughput for CROs and sustains premium pricing for reagents and automated imaging instrumentation, reinforcing the upward trajectory of the genetic toxicology testing market.

Adoption of high-throughput 3-D cell culture and organ-on-chip

Drug attrition linked to poor translational fidelity has prompted industry-wide migration from 2-D monolayers to 3-D spheroids and microfluidic organ-chips. Molecular Devices’ CellXpress.ai platform automates seeding, feeding and high-content imaging of thousands of spheroids per week, reducing technician time by 80% and boosting detection sensitivity. Kidney-on-chip systems now achieve 85% sensitivity for nephrotoxicity, eclipsing rodent assays and accelerating regulatory acceptance. Such platforms underpin much of the 1.4-percentage-point CAGR uplift expected for the genetic toxicology testing market.

AI-enabled predictive toxicology platforms

Transformer-based neural networks have broken accuracy barriers once thought unattainable by conventional QSAR. A 2024 Science Advances study logged AUROC gains of 14 points versus earlier baselines, reaching 0.88 on Tox21 data. Merck KGaA reduced liver-injury false negatives by 28% through its Quris-AI pilot, trimming screening cycles from weeks to days. The European Food Safety Authority’s AI4NAMS sandbox—which tests language-model extraction of toxicology dossiers—signals future regulatory endorsement. These developments heighten demand for in silico licenses and cloud compute subscriptions, reinforcing expansion of the genetic toxicology testing market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited metabolic activation fidelity of in-vitro systems | -1.3% | Global, particularly impacting EU & North America | Medium term (2-4 years) |

| Variability & reproducibility challenges across labs | -0.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| High capital cost of automated HTS instruments | -0.6% | Global, strongest impact in emerging markets & smaller CROs | Medium term (2-4 years) |

| IP & data-sharing barriers for AI toxicology models | -0.4% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited metabolic activation fidelity of in vitro systems

Most regulatory-accepted assays still rely on rat-liver S9 fractions that only partially mimic human Phase I and Phase II metabolism. OECD Technical Series papers cite inconsistent bioactivation of aromatic amines as a leading false-negative source. Although microfluidic liver-on-chip modules demonstrate improved xenobiotic processing, cross-lab validation remains thin and no consensus reference compound set yet exists. Until metabolic competency is standardized, regulators may still require confirmatory in vivo genotoxicity endpoints, trimming near-term upside for the genetic toxicology testing.

Inter-laboratory reproducibility gaps

Environmental Mutagen Society reviewers report coefficient-of-variation levels up to 30% for enhanced Ames fluctuation tests across different CROs. Divergent cell-culture conditions, inconsistent reagent batches, and variable imaging algorithms all erode confidence in regulatory submissions. Vendors such as MilliporeSigma attempt to mitigate the issue with bundled Aptegra™ CHO genetic stability kits that fold five assays into a single validated workflow, trimming timelines by 66%. Nonetheless, until ISO-style proficiency programs scale globally, reproducibility concerns will temper the overall growth rate of the genetic toxicology testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Computational Momentum Builds on Established In Vitro Base

In vitro assays retained 64.62% of 2025 revenue, underpinning the largest slice of the genetic toxicology testing market. Bacterial reverse-mutation, mammalian micronucleus, and Comet tests remain regulatory staples, generating steady reagent re-orders and high-content imaging demand. Yet the in silico branch is charting a 8.83% CAGR, the fastest of all modalities, as machine-learning models achieve 87.8% predictivity on public ToxCast sets. The genetic toxicology testing market size for in silico platforms is still modest, but expansions in cloud compute and curated chemical libraries point to compounding uptake across early discovery screens.

Predictive algorithms increasingly guide wet-lab priorities, cutting unproductive cell-based iterations and freeing budgets for confirmatory in vitro endpoints. The FDA’s draft guidance on follow-up to Ames-positive findings explicitly references computational weight-of-evidence use cases, clearing a regulatory path for broader deployment. Hybrid workflows integrating transformer-predicted mutagenicity with 3-D spheroid γH2AX readouts have trimmed candidate attrition times by up to three months, an efficiency directly fueling contract research uptake.

By Component: Services Race Ahead as Outsourcing Deepens

Reagents and kits represented 39.62% of 2025 spending, anchored by consumable-heavy micronucleus and Comet assays as well as liver S9 activation cocktails. However, services are advancing at a 9.21% pace through 2031, mirroring biopharma’s broader pivot to outsourced research models. Scantox Group’s acquisition of Gentronix added over 120 genetic toxicology employees and raised the combined lab footprint to more than 400 staff across Europe. The genetic toxicology testing market size for outsourced studies is projected to reach USD 288.6 million by 2031, backed by expanding Good Laboratory Practice (GLP) capacity in North America and Asia.

Instrument manufacturers are repositioning accordingly. Molecular Devices bundles its CellXpress.ai™ hardware with per-sample analytic subscriptions, ensuring continued revenue once capital placement peaks. MilliporeSigma’s Aptegra™ kit strategy likewise converts one-off instrument sales into repeat reagent demand. These combined moves deepen recurring revenue streams and enhance vendor stickiness across the broader genetic toxicology testing market.

By Application: Pharmaceuticals Dominate, Cosmetics Climb Fast

Pharmaceutical and biotechnology developers generated 47.74% of 2025 turnover, retaining top rank within the genetic toxicology testing market. Oncology pipelines alone account for roughly half of all genotoxic workload, spurred by precision gene-editing modalities that demand extra margin-of-safety data. Meanwhile, the cosmetics and personal-care segment is charting a 9.64% CAGR as EU animal-testing bans spread globally and consumer labeling shifts to “cruelty-free” claims. The genetic toxicology testing market share for cosmetics is still under 15%, but pipeline ingredient innovation in Asia and Latin America suggests rising contribution by decade end.

Food and beverage makers now face heightened scrutiny after the January 2025 FDA ban on Red Dye No. 3, scheduled for full enforcement in 2027. As more additives migrate to the Delaney Clause list, demand from flavor houses and ingredient suppliers is expected to broaden, partially offsetting slower chemical-sector growth hurt by recessionary downstream demand.

Geography Analysis

North America generated 46.05% of 2025 revenue, solidifying its position as the largest regional block in the genetic toxicology testing market. The FDA’s November 2024 draft guidance on Ames-positive follow-ups obliges deeper mechanistic investigations, lifting test volumes among US-based contract research organizations (CROs). Large biopharma firms, led by Merck and Bristol Myers Squibb, expanded 2025 R&D budgets by a combined USD 4 billion, guaranteeing throughput for regional laboratories.

Europe maintains second-place revenue status, propelled by its policy leadership in new approach methodologies. The region’s updated Annex II & III cosmetics bans along with REACH micro-update packages continue to add compounds to genotoxicity priority lists cirs-group.com. The OECD Paris secretariat, funded largely by EU commissions, is fast-tracking organoid and high-throughput screening protocols for Mutual Acceptance of Data, reinforcing local CRO competitiveness.

Asia-Pacific is the fastest-growing territory, posting a 10.05% CAGR to 2031 and targeting USD 152.8 million revenue by the end of the forecast window. China’s push to align NMPA safety dossiers with ICH requirements by 2027 mandates genotoxicity packages consistent with Western standards. WuXi AppTec alone maintained a RMB 43.10 billion (USD 6.0 billion) backlog in H1 2024, underscoring regional demand resilience. India is following suit: Syngene International is expanding “China-free” supply chains and deploying Genedata Screener across its Bangalore hub to standardize in vitro analysis for global clients prweb.com.

South America and the Middle East & Africa collectively contribute a mid-single-digit share but show rising inquiry volumes as Brazil’s ANVISA and Saudi Arabia’s SFDA draft new genotoxicity annexes to their respective pharmacopoeias. Multilateral funding agencies are earmarking capacity-building grants that could improve local GLP accreditation rates, providing longer-term upside for the genetic toxicology testing market.

Competitive Landscape

The genetic toxicology testing market remains moderately fragmented: the top five providers control about 45% of global revenue, leaving room for specialist disruptors. Charles River Laboratories introduced a viral-vector tech-transfer program in February 2025, enhancing its gene-therapy assay depth and positioning to cross-sell genetic stability testing.

Regional consolidation continues. Scantox Group’s Gentronix buyout raised its European market share north of 7%, creating a one-stop shop for in vitro, in vivo and computational toxicology. Agilent, historically an instrument supplier, opened a CLIA-certified Biopharma CDx services lab, blending hardware sales with turnkey assay development.

Tech-first entrants are penetrating from the software side. Axiom Bio secured USD 15 million seed funding to scale transformer-based mutagenicity algorithms, claiming 80% reduction in required wet-lab screens. Venture funding is also targeting organ-on-chip consumables, an un-dominated sub-sector where intellectual-property barriers remain low. Vendors that master regulatory validation and establish harmonized protocols will set de-facto standards and capture premium pricing within the genetic toxicology testing market.

Genetic Toxicology Testing Industry Leaders

Eurofins Scientific

WuXi AppTec

Charles River Laboratories

Frontage Labs

Laboratory Corporation of America Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Scantox Group acquired Gentronix, adding specialized genetic toxicology to its CRO portfolio

- September 2024: Agilent Technologies opened a CLIA-certified Biopharma CDx Services Lab in California

Global Genetic Toxicology Testing Market Report Scope

As per the scope of the report, genetic toxicology testing refers to evaluates the potential of chemicals, pharmaceuticals, or environmental substances to cause genetic damage. It is a key component of safety assessments, particularly in drug development, environmental monitoring, and regulatory compliance. This testing focuses on identifying substances that can cause mutations, chromosomal aberrations, or other alterations in genetic material, which may lead to cancer, heritable diseases, or other adverse effects.

The genetic toxicology testing market is segmented as products into reagents & consumables, assay kits, and services. By test type, the genetic toxicology testing market is segmented into in vitro genetic toxicology tests and in vivo genetic toxicology tests. In terms of end user, the market is segment into pharmaceuticals & biotechnology companies, food industry, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| In Vitro Tests |

| In Vivo Tests |

| In Silico / Computational Tests |

| Instruments & Software |

| Reagents & Consumables |

| Services (CRO) |

| Pharmaceutical & Biotech |

| Chemical & Agrochemicals |

| Cosmetics & Personal-care |

| Food & Beverages |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Test Type | In Vitro Tests | |

| In Vivo Tests | ||

| In Silico / Computational Tests | ||

| By Component | Instruments & Software | |

| Reagents & Consumables | ||

| Services (CRO) | ||

| By Application | Pharmaceutical & Biotech | |

| Chemical & Agrochemicals | ||

| Cosmetics & Personal-care | ||

| Food & Beverages | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the genotoxicity testing market?

The genotoxicity testing market stands at USD 386.98 million in 2026 and is forecast to reach USD 570.42 million by 2031.

Which test type is growing the fastest?

In silico computational assays exhibit the highest 8.83% CAGR as AI models gain regulatory traction through 2031.

Why is Asia-Pacific the fastest-growing region?

Regulatory harmonization with ICH guidelines and expanding biopharma manufacturing capacity push Asia-Pacific toward a 10.05% CAGR through 2031.

How are regulations shaping market demand?

The FDA Modernization Act 2.0 and EU cosmetics bans are phasing out animal studies, prompting companies to adopt validated in vitro and in silico alternatives.

Page last updated on: