Mycoplasma Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

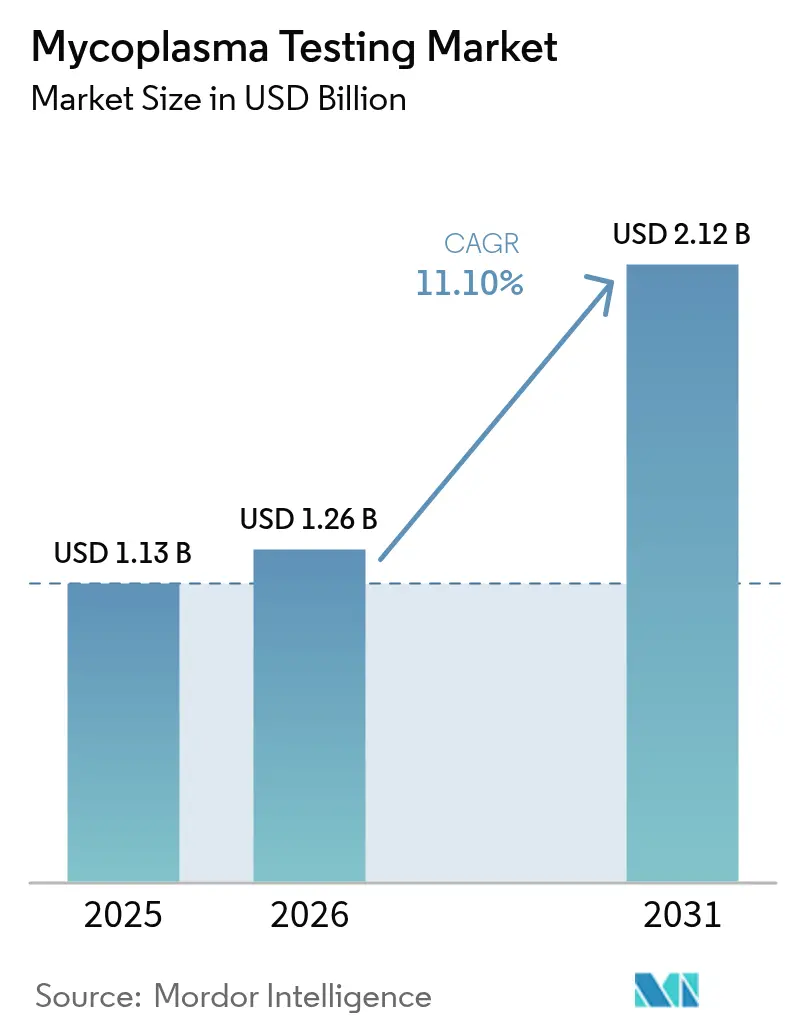

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 11.10% CAGR |

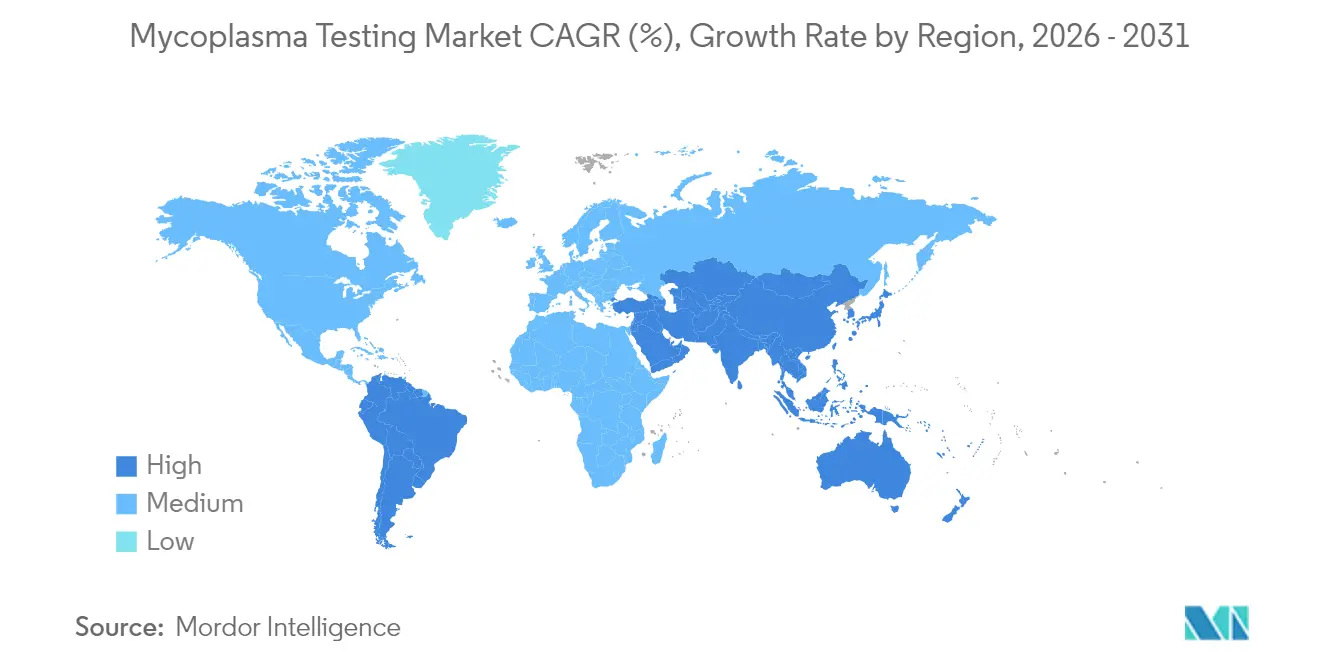

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

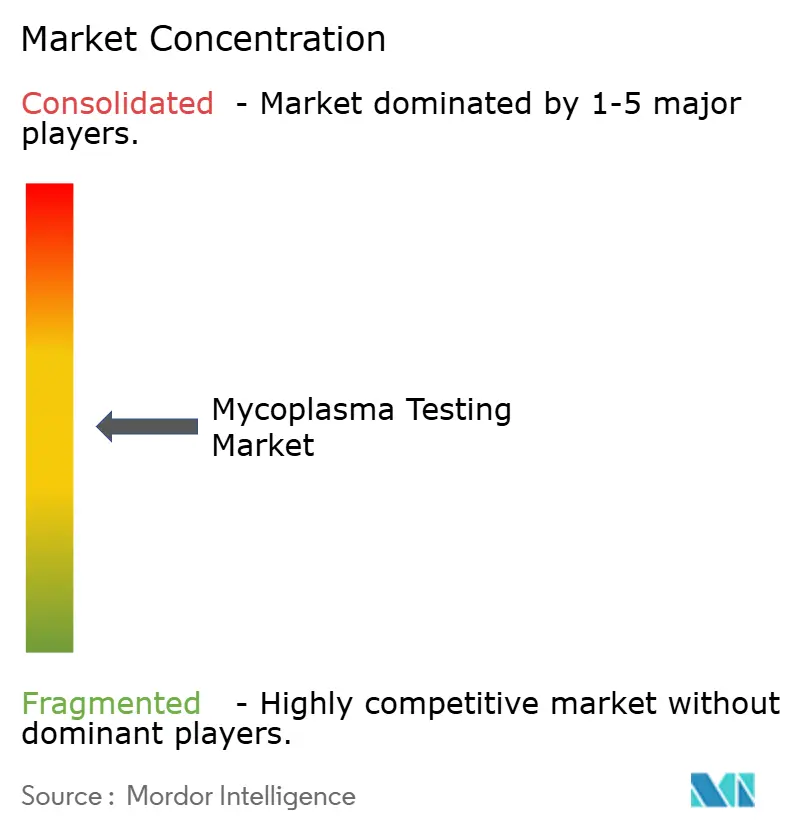

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mycoplasma Testing Market Analysis by Mordor Intelligence

Mycoplasma Testing Market size in 2026 is estimated at USD 1.26 billion, growing from 2025 value of USD 1.13 billion with 2031 projections showing USD 2.12 billion, growing at 11.10% CAGR over 2026-2031.

Heightened regulatory scrutiny on biologics manufacturing, expanding cell- and gene-therapy production, and growing preference for rapid nucleic-acid methods underpin this trajectory. Regulatory agencies, led by the FDA and EMA, require validated mycoplasma detection at multiple points in the product lifecycle, turning compliance into a non-discretionary spend for biomanufacturers fda.gov. Digital PCR and automated sample-to-answer platforms accelerate lot-release timelines, while the outsourcing trend transfers testing workloads to contract organizations that can scale capacity quickly. Regional manufacturing expansions in China, India, and Singapore combine with tax incentives to spur laboratory build-outs, yet shortages of skilled molecular QA personnel and high automation costs temper adoption rates in smaller facilities. Competitive dynamics favor vendors able to bundle instruments, kits, and services, boosting cross-selling potential and consolidating customer relationships.

Key Report Takeaways

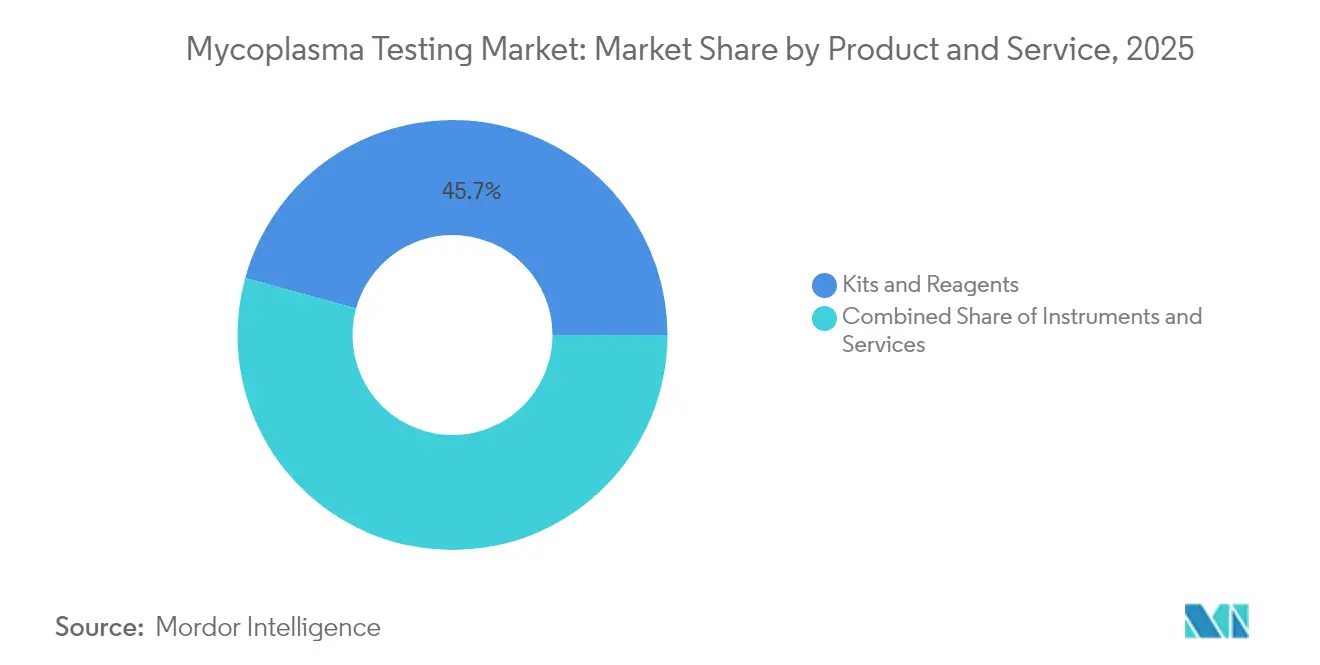

- By product and service, kits and reagents held a 45.72% revenue share in 2025, whereas services are projected to expand at a 14.15% CAGR to 2031.

- By technology, qPCR led with 63.85% of the mycoplasma testing market share in 2025, while digital PCR is forecast to grow at 15.75% through 2031.

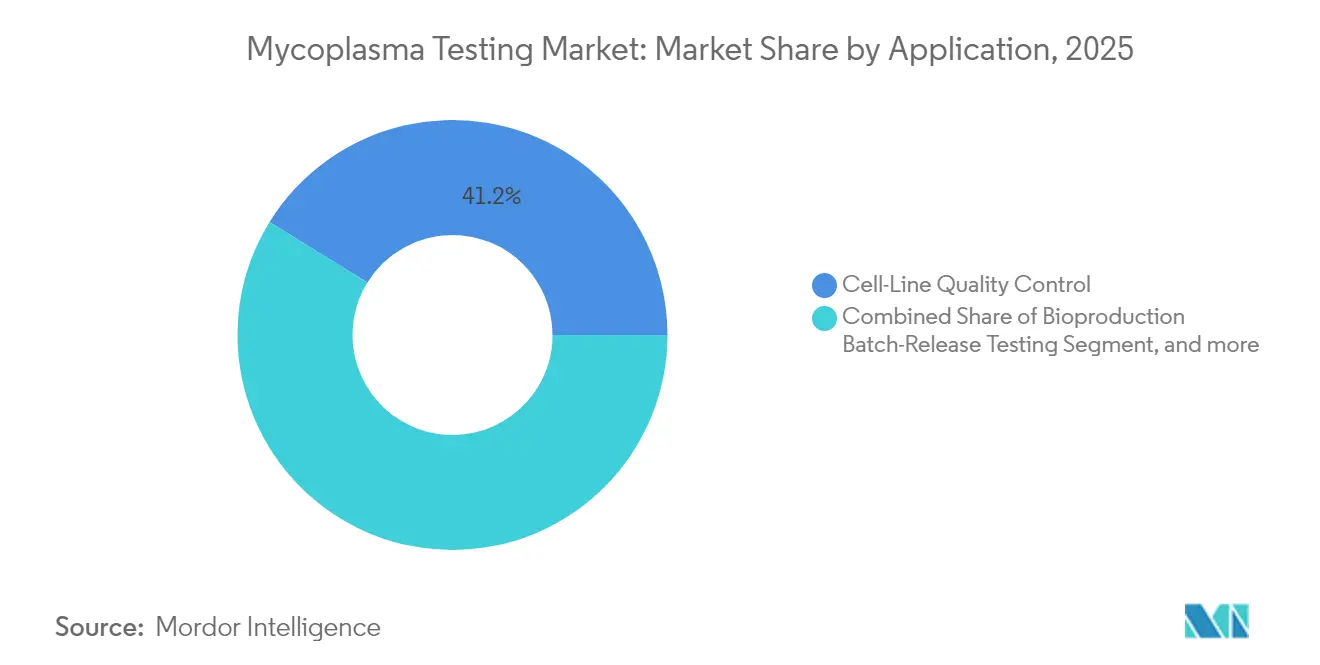

- By application, cell-line quality control accounted for 41.20% of the mycoplasma testing market size in 2025; gene and cell therapy manufacturing will rise at a 17.10% CAGR between 2026 and 2031.

- By end user, biopharma & biotechnology companies accounted for 64.70% of the mycoplasma testing market size in 2025; contract manufacturing organizations recorded the fastest growth, progressing at 14.98% CAGR to 2031.

- By geography, North America commanded 40.25% share of the mycoplasma testing market in 2025, yet Asia-Pacific is advancing at an 18.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mycoplasma Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of biopharma and cell & gene therapy facilities | +2.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Regulatory mandates require mycoplasma release testing | +2.1% | Global, led by FDA/EMA jurisdictions | Short term (≤ 2 years) |

| Increasing incidents of cell-culture contamination | +1.9% | Global, high-volume manufacturing hubs | Short term (≤ 2 years) |

| Rising demand for rapid, high-sensitivity PCR assays | +1.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Decentralised QC labs in emerging biotech hubs | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| VC-backed growth of synthetic biology start-ups | +0.9% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Biopharma and Cell & Gene Therapy Manufacturing Facilities

Capacity ramp-ups in autologous and allogeneic therapy plants have multiplied sample volumes that require 100% batch testing. Contamination prevalence in cell cultures ranges between 15% and 35%, and FDA guidance now mandates mycoplasma testing after pooling and prior to washing, increasing sampling frequency.[1]American Type Culture Collection, “Cell Culture Contamination Studies,” atcc.org Continuous perfusion bioreactors raise real-time monitoring needs, pushing demand for automated analyzers that handle higher throughputs with minimal human intervention. Facility roll-outs in emerging markets must complete qualification studies, creating greenfield demand for third-party test services. Together, these trends add 2.8 percentage points to the forecast CAGR.

Regulatory Mandates Require Mycoplasma Release Testing for Biologics

The FDA’s laboratory developed tests rule and EMA guidance for advanced therapy medicinal Products require validated assays from a master cell bank to a finished drug.[2]Federal Register Editorial Team, “Laboratory Developed Tests; Final Rule,” federalregister.gov The European Medicines Agency's guidelines for Advanced Therapy Medicinal Products mandate comprehensive mycoplasma testing throughout the manufacturing process, from master cell banks to final product release. These regulatory changes create non-discretionary demand for testing services, as manufacturers cannot release products without demonstrating mycoplasma absence through validated methods. Compliance spending accelerates through 2027 as phased LDT oversight takes effect.The phased implementation of new LDT regulations over four years creates predictable demand growth as laboratories upgrade their testing capabilities to maintain compliance.

Increasing Incidents of Cell-Culture Contamination

Industry case studies document filtration bypass, DNA persistence, and charge-variant shifts in monoclonal antibodies following undetected contamination.[3]Wiley Editors, “Charge Variants in Contaminated mAbs,” onlinelibrary.wiley.com Economic fallout includes batch destruction, facility shutdowns, and regulatory inspections, prompting proactive screening policies. High-density cultures and longer residence times in intensified processes further elevate risk, translating into more frequent interim tests.

Rising Demand for Rapid, High-Sensitivity PCR-Based Assays

Digital PCR detects ≤10 CFU/mL without reference curves, providing absolute quantification that meets release-testing precision needs. Platforms such as the BIOFIRE Mycoplasma system report results in 60 minutes, condensing lot-release cycles. AI-driven analytics streamline interpretation and cut false positives. Regulatory nods, e.g., Health Canada’s clearance of Roche MycoTOOL, validate these technologies for commercial adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for automated systems | -1.8% | Global, smaller labs affected | Short term (≤ 2 years) |

| False-positive/-negative retest delays | -1.4% | Global, high-volume sites | Medium term (2-4 years) |

| Skilled molecular-QA workforce shortages | -1.1% | North America & EU, rising in APAC | Long term (≥ 4 years) |

| Regulatory lag on microfluidic and next-gen assays | -0.8% | Global, jurisdiction-specific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Implementing Automated Detection Systems

Entry-level automated analyzers cost USD 100,000–500,000, with annual service contracts topping USD 50,000. Smaller CTLs and academic labs struggle to justify such outlays, prolonging reliance on manual culture methods. FDA LDT compliance adds validation costs and strains capital budgets, curbing near-term uptake. Smaller contract testing laboratories face particular challenges in justifying automation investments given their limited sample volumes and diverse testing requirements. The complexity of validating automated systems for regulatory compliance adds significant time and cost burdens, with validation studies typically requiring 6-12 months and specialized expertise.

False-Positive/-Negative Retest Delays

DNA carry-over and cross-contamination trigger confirmatory workflows that erode the speed advantage of PCR, while false negatives threaten patient safety and invite regulatory scrutiny. Discordant results between culture and molecular assays extend release timelines by weeks, especially when investigation protocols lack standardisation. Regulatory agencies' requirements for investigation of atypical results can delay product releases by weeks or months, particularly when multiple testing methods yield conflicting outcomes. The industry's transition from culture-based to molecular methods introduces new sources of variability that require extensive method validation and comparison studies to establish confidence in results.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Outsourced Services Gain Momentum

Kits and reagents maintained a 45.72% share in 2025, underlining their consumable nature within the Mycoplasma testing market. The Services segment is set to expand at 14.15% CAGR as biomanufacturers delegate method validation and routine screening to accredited laboratories. High regulatory hurdles and evolving assay formats encourage companies to buy expert capacity instead of building it. Eurofins’ network of 45+ global sites illustrates how scale produces cost-efficiencies that individual firms cannot replicate.

Automation-ready instruments show steady but slower growth because purchasers often tie them to long-term reagent contracts. The BIOFIRE platform and Rapid Micro Biosystems’ vial-reader appeal by blending speed with pharmacopeial compliance. As services grow, kit vendors align with third-party labs under reagent-rental models that lock in supply revenues. This synergy consolidates buyer–supplier dependencies and drives volume in both categories.

By Technology: Digital PCR Disrupts Legacy Workflows

qPCR holds 63.85% of the 2025 Mycoplasma testing market share thanks to entrenched protocols and broad instrument availability. Digital PCR, with a 15.75% growth rate, mitigates standard-curve errors and detects rare events vital for gene-therapy lots. Sensitivity gains resonate with regulatory auditors seeking robust quantification. Conventional PCR remains a budget choice for legacy facilities, while ELISA and DNA staining stay relevant in niche academic applications. Next-generation sequencing promises multiplex pathogen screens but awaits regulatory consensus.

Regulatory bodies now accept nucleic-acid methods equivalent to culture for release testing, catalysing digital PCR uptake. Instrument makers invest in microfluidic chip formats that slice reaction mixes into thousands of partitions, lowering detection thresholds. AI augmentation further lessens operator skill barriers, unlocking broader lab adoption.

By Application: Gene Therapy Drives Highest Upside

Cell-line quality control dominated the mycoplasma testing market in 2025, with a 41.20% share. Yet gene and cell therapy manufacturing will outpace all other uses at a 17.10% CAGR. Extended culture durations, autologous workflows, and multi-step manipulations amplify contamination risk, compelling frequent in-process checks. Regulatory guidance treats each manufacturing step as a potential contamination window, swelling sample numbers.

Bioproduction batch-release testing remains a staple, while raw-material & media testing gains share as firms recognise upstream vectors such as animal-origin components. Vaccine and virus manufacturers broaden surveillance alongside rising viral-vector therapeutics pipelines. Academic discovery work sits outside stringent release rules but still demands periodic screening to protect research integrity.

By End User: CMOs Capture Outsourcing Wave

Biopharma and biotechnology Companies accounted for 64.70% of the end-user segment in 2025, yet CMOs will grow the fastest at 14.98% CAGR as virtual biotech firms rely on third parties from plasmid prep through fill-finish. The Mycoplasma testing market size for contract labs widens when projects scale from pre-clinical to commercial runs.

Diagnostic and reference labs diversify into biologics support, chasing higher-margin industry work. Cell banks guard against line cross-contamination because a single tainted master cell bank can invalidate years of submissions. Workforce shortages push even large pharma to outsource surge testing during tech-transfer or facility shutdown periods, reinforcing the CMO growth curve.

Geography Analysis

North America led with 40.25% of 2025 revenue as FDA oversight, mature bioprocessing infrastructure, and early technology adoption underpin stable demand. The region’s biocluster density and capital availability encourage rapid replacement of culture methods with automated PCR systems. Service providers leverage proximity to innovators, enabling just-in-time sample logistics and compliance audits.

Europe follows with a cohesive regulatory framework from the EMA and harmonised pharmacopoeias that facilitate multi-country lot release. The Mycoplasma testing market size tied to EU gene-therapy trials rises as Germany, Spain, and the United Kingdom host GMP facilities. Vendors cater to multi-language documentation and serialization demands, spurring informatics-enabled assay platforms.

Asia-Pacific represents the fastest-growing arena, expanding at 18.10% CAGR. China’s cell-therapy sector benefits from government priority listings, while India’s production-linked incentive schemes attract vaccine exporters. Singapore’s decentralized QC labs shorten turnaround times for regional biologics plants. Fragmented regulations necessitate local validation, favouring global companies that co-locate service hubs.

South America and the Middle East & Africa trail in absolute revenue but offer untapped upside as domestic vaccine programs and biosimilar plants proliferate. Logistics hurdles and limited cold-chain infrastructure slow penetration of rapid PCR devices, yet public-health investments could unlock future orders once training and service networks mature.

Regulatory Landscape

Regulatory requirements for mycoplasma control in biopharmaceutical production are grounded in compendial standards and regulator expectations. In the United States, USP general chapters 63 (Mycoplasma Tests) and 77 (Mycoplasma Nucleic Acid Amplification Tests) are key references for cell-based manufacturing, alongside regulator guidance for biologics and related expectations covering viral safety and contamination control.

In Europe, the European Pharmacopoeia Commission and EDQM updated Ph. Eur. general chapter 2.6.7, which entered into force on April 1, 2026. The revision reinforces acceptance of NAT as standalone methods when product-specific suitability and performance are demonstrated, including sensitivity targets such as LOD <= 10 CFU/mL or < 100 genomic copies/mL for NAT-based approaches that replace culture. It also tightens execution controls, including adding external controls prior to nucleic acid extraction and checking for inhibition, which increases the focus on validated workflows, reference standards, and documentation for inspections and batch disposition.

Competitive Landscape

The mycoplasma testing market is moderately fragmented. Thermo Fisher Scientific, Charles River Laboratories, and Merck KGaA combine broad reagent portfolios with global technical-service teams, anchoring them atop instrument and kit sales. Danaher’s 2024 merger of Cytiva and Pall created a USD 7.5 billion bioprocess powerhouse that unifies filtration, culture media, and testing under one umbrella.

Specialised laboratories such as Eurofins Scientific and SGS scale through multi-site GMP accreditations, capturing outsourced workloads that require geographic proximity to filling lines. Their competitive edge lies in turnkey validation packages that compress client timelines. Smaller innovators like Minerva Biolabs focus on reagent-only niches, while Rapid Micro Biosystems targets high-throughput QC labs with automated reader systems.

Acquisition activity intensifies as firms chase end-to-end platform breadth. bioMérieux’s 2025 buyout of SpinChip Diagnostics adds ultra-fast immunoassay capability to complement its BIOFIRE molecular suite, positioning the company for sample-to-answer dominance. AI partnerships aim to trim interpretation errors and reduce retest frequency, providing another lever for differentiation.

Mycoplasma Testing Industry Leaders

-

Bionique Testing Laboratories Inc.

-

Thermo Fisher Scientific Inc.

-

Eurofins Scientific

-

Merck KGaA

-

ATCC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The revised EP 2.6.7 alignment supports an upgrade path from culture workflows to NAT-based assays used as standalone release tests, provided product-specific suitability and inhibition controls are demonstrated. This expands demand for end-to-end solutions that include extraction controls, inhibition testing, and reference standards tied to the stated LOD requirements (<=10 CFU/mL or <100 genomic copies/mL). Vendors that package assays with genomic copy-based controls and validation support can benefit as QC organizations standardize documentation and acceptance criteria across multi-site manufacturing networks.

Separately, activity around rapid, closed-system testing points to whitespace in faster lot disposition and outsourced validation capacity, particularly for cell and gene therapy operations with frequent in-process testing needs. In April 2026, bioMerieux introduced the BIOFIRE SPOTFIRE molecular testing system for pharmaceutical quality control, with rapid mycoplasma detection in less than 1 hour. In May 2026, Minaris Advanced Therapies expanded rapid mycoplasma detection services by implementing the BIOFIRE platform in GMP workflows. In parallel, Minerva Biolabs updated Venor Mycoplasma PCR, extraction kits, and GC/CFU reference standards to align with the revised EP 2.6.7 requirements, highlighting opportunities for labs to transition methods, run comparability studies, and manage matrix-specific inhibition risks without extending release timelines.

Recent Industry Developments

- May 2026: Minaris Advanced Therapies expanded rapid mycoplasma detection services by implementing the BIOFIRE Mycoplasma platform within its GMP manufacturing and testing workflows. This enhances outsourced, rapid PCR-based release and in-process testing capacity for cell and gene therapy programs, where turnaround time and validated workflows directly affect manufacturing cadence.

- May 2025: Bionique Testing Laboratories and Cellipont BioServices announced a partnership focused on accelerating adoption of rapid mycoplasma testing in cell and gene therapy manufacturing. The collaboration links specialized testing capabilities with CDMO operations, supporting faster method deployment and product-specific validation demands as programs transition from development into GMP production.

- September 2024: bioMerieux announced the availability of method validation services for BIOFIRE Mycoplasma. By packaging validation support with a rapid testing platform, the company reduced barriers for regulated labs adopting newer molecular approaches, reinforcing the trend toward standardized, inspection-ready rapid methods.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues from mycoplasma contamination testing used to screen and release cell cultures and biologics workflows. This includes instruments, kits, and reagents, plus outsourced testing services used by life science labs and manufacturers.

Scope exclusions: clinical mycoplasma diagnostic tests run in hospital or routine patient-care labs (for example, respiratory or urogenital panels) are excluded.

Segmentation Overview

-

By Product & Service

-

Instruments

- Real-time PCR Systems

- Rapid Microfluidic Analyzers

- Automated Detection Platforms

- Other Instruments

-

Kits & Reagents

- PCR Assay Kits

- ELISA Kits

- Enzymatic Assay Kits

- Fluorescent‐Staining Reagents

- Others

- Services

-

Instruments

-

By Technology

- Conventional PCR

- qPCR

- Digital PCR

- ELISA

- Enzymatic Methods

- DNA Staining

- Next-Generation Sequencing

- Other NAATs

-

By Application

- Cell-Line Quality Control

- Bioproduction Batch-Release Testing

- Raw-Material & Media Testing

- Gene & Cell Therapy Manufacturing

- Vaccine & Virus Testing

- Other Applications

-

By End User

- Biopharma & Biotechnology Companies

- Contract Manufacturing Organizations (CMOs)

- Academic & Research Institutes

- Cell Banks & Repositories

- Diagnostic & Reference Laboratories

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping where testing demand comes from, and how much lab activity is tied to cell culture and biologics production. Public sources were used to anchor the demand pool and context, including the US FDA, the European Medicines Agency, the World Health Organization, and the US National Institutes of Health (including PubMed articles on contamination control and test methods).

Supporting secondary material was also reviewed, including company filings, investor presentations, product documentation, association websites, and reputable press coverage on biologics manufacturing expansions and quality testing expectations. Where reported numbers were fragmented, paid subscriptions for company financials and news, patent lookups, and shipment-level trade data were used to cross-check product availability and pricing direction. The sources listed here are illustrative only, and many other public references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with test kit and instrument suppliers, contract testing providers, bioprocess and quality teams, and lab managers who run routine contamination screening. Since the market is global, discussions covered major demand centers across APAC, EMEA, and the Americas, which helped confirm assumptions on testing frequency, method mix (culture-based versus rapid molecular), and average selling prices.

In particular, respondent input clarified where labs separate in-house screening from outsourced service use, and how often teams run confirmatory steps after initial mycoplasma signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 40% |

| Mid tier: 48% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 22% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction that links biologics and cell-culture activity to expected mycoplasma testing frequency, then converts that into spend using method-level pricing and service share. To keep the estimate grounded, totals were corroborated with selective bottom-up approximations, such as sampling kit and reagent price bands, checking typical tests per batch or per cell line program, and rolling up a limited set of supplier and service revenues where disclosure allowed it.

Inputs in the model were driven by market variables that influence contamination screening spend, including growth in biologics and vaccine manufacturing capacity, the number of active cell culture programs, regulatory quality expectations for sterility and contamination control, adoption rates for rapid PCR-based workflows versus traditional culture methods, and the split between in-house testing and outsourced services. When a bottom-up check had gaps, conservative fill rates were used based on interview ranges, and then the impact was stress-tested by region and end-user type.

Forecasts were produced using scenario analysis supported by a small set of leading indicators, followed by expert-based adjustments to reflect realistic adoption timing. The final outlook was kept repeatable so each assumption can be traced back to either a public signal or a primary validation point.

Data Validation & Update Cycle

Outputs were triangulated using independent checks, including consistency versus biologics capacity additions, assay adoption shifts reported by labs, and year-over-year pricing movement for kits, reagents, and services. Variances were reviewed in more than one pass, and outliers were challenged until the assumption trail became clear and internally consistent.

If a material mismatch appeared, such as an unrealistic testing frequency or an abrupt pricing jump, the team re-contacted relevant participants and re-ran sensitivities before sign-off. Reports are refreshed annually, with interim updates when major events occur, and a final pre-release review is completed so clients receive the most current view.

Mordor Intelligence's Mycoplasma Testing Market Size Measured Against Other Published Estimates

Different market sizes for mycoplasma testing are common because firms do not always count the same activities, the same years, or the same pricing logic. Differences also come from how services are included, how method mix is handled, and whether the model is tied back to real testing frequency in biomanufacturing.

By tracking testing volume drivers and refreshing method mix assumptions with primary checks, Mordor Intelligence keeps the scope centered on contamination screening for cell culture and biologics workflows. This avoids clinical patient diagnostics that can inflate totals under broader definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.26 B (2026) | |

| Global Consultancy A | USD 1.03 B (2024) | Uses a 2024 base year and may reflect a narrower near-term spend capture, and the scope statement does not clearly separate bioprocess contamination screening from adjacent clinical diagnostic testing categories. |

| Industry Research Group B | USD 1.36 B (2025) | Applies a higher near-term growth step between 2024 and 2025 and can widen totals if broader service bundles or aggressive adoption of rapid molecular tests are assumed without matching those assumptions to observed testing cadence. |

Across the table, the spread is mainly explained by timing and boundaries, especially whether clinical diagnostics or broader service bundles are blended into the same bucket. A model that links demand to cell-culture and biologics activity, then tests pricing and mix assumptions with interview checks, tends to land on a steadier and more traceable number.

Key Questions Answered in the Report

What is the current size of the mycoplasma testing market?

The market is valued at USD 1.26 billion in 2026 and is forecast to reach USD 2.12 billion by 2031.

Which segment is growing the fastest?

Gene & Cell Therapy Manufacturing is projected to grow at 17.10% CAGR due to strict contamination-control requirements.

Why are CMOs gaining share in mycoplasma testing?

Biotech firms are outsourcing manufacturing and quality control to CMOs to access validated laboratories without large capital outlays, pushing CMO demand up at 14.98% CAGR.

How do regulatory mandates influence market growth?

FDA and EMA rules make mycoplasma testing mandatory before product release, creating non-discretionary spending that raises overall market CAGR.

Which technology is disrupting traditional methods?

Digital PCR offers absolute quantification with detection limits around 10 CFU/mL, expanding at 15.75% CAGR as labs replace culture-based assays.

What restrains rapid adoption of automated platforms?

High upfront costs of USD 100,000–500,000 and shortages of trained molecular-QA staff delay automation, particularly in smaller labs.

Page last updated on: