Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 491.40 Million |

| Market Size (2026) | USD 511.16 Million |

| Market Size (2031) | USD 622.84 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

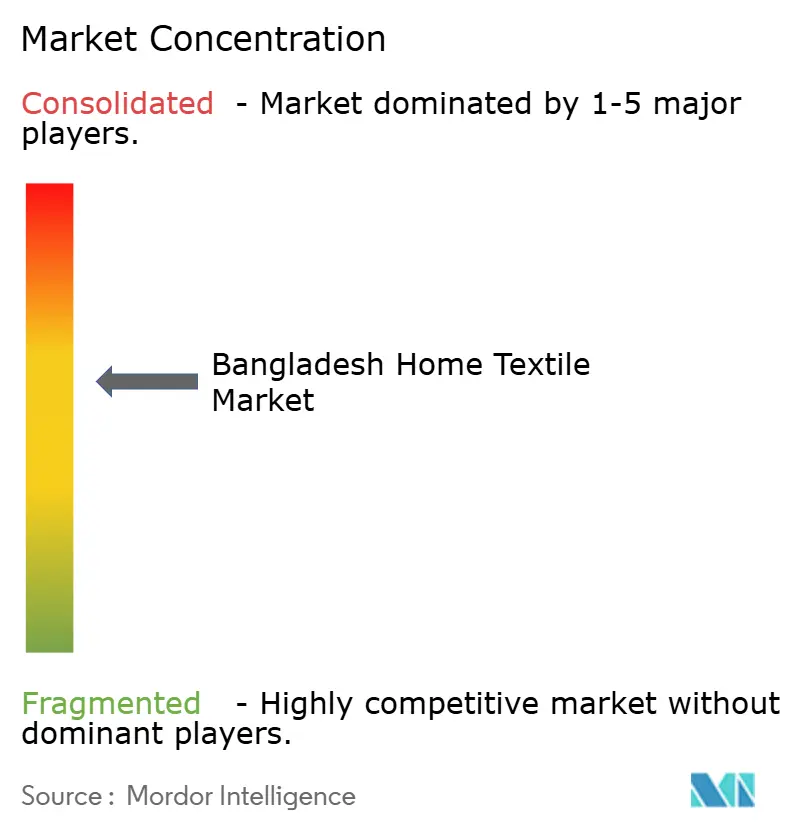

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Home Textile Market Analysis by Mordor Intelligence

The Bangladesh home textiles market size was valued at USD 491.40 million in 2025 and estimated to grow from USD 511.16 million in 2026 to reach USD 622.84 million by 2031, at a CAGR of 4.02% during the forecast period (2026-2031). Robust export linkages, low-cost manufacturing, and duty-free access to the EU, Canada, and Japan sustain a steady order pipeline for bedding, towels, curtains, and rugs, while rising domestic disposable income deepens urban demand for branded décor products. Greater adoption of African cotton, eco-preferred fibers, and digital design tools boosts product quality and value addition for international buyers. Meanwhile, e-commerce acceleration widens direct-to-consumer channels, allowing producers to bypass traditional intermediaries and capture healthier margins. These tailwinds are tempered by chronic gas outages, wage inflation, and the looming loss of LDC-linked tariff preferences, which collectively squeeze margins and complicate forward capacity planning.

Key Report Takeaways

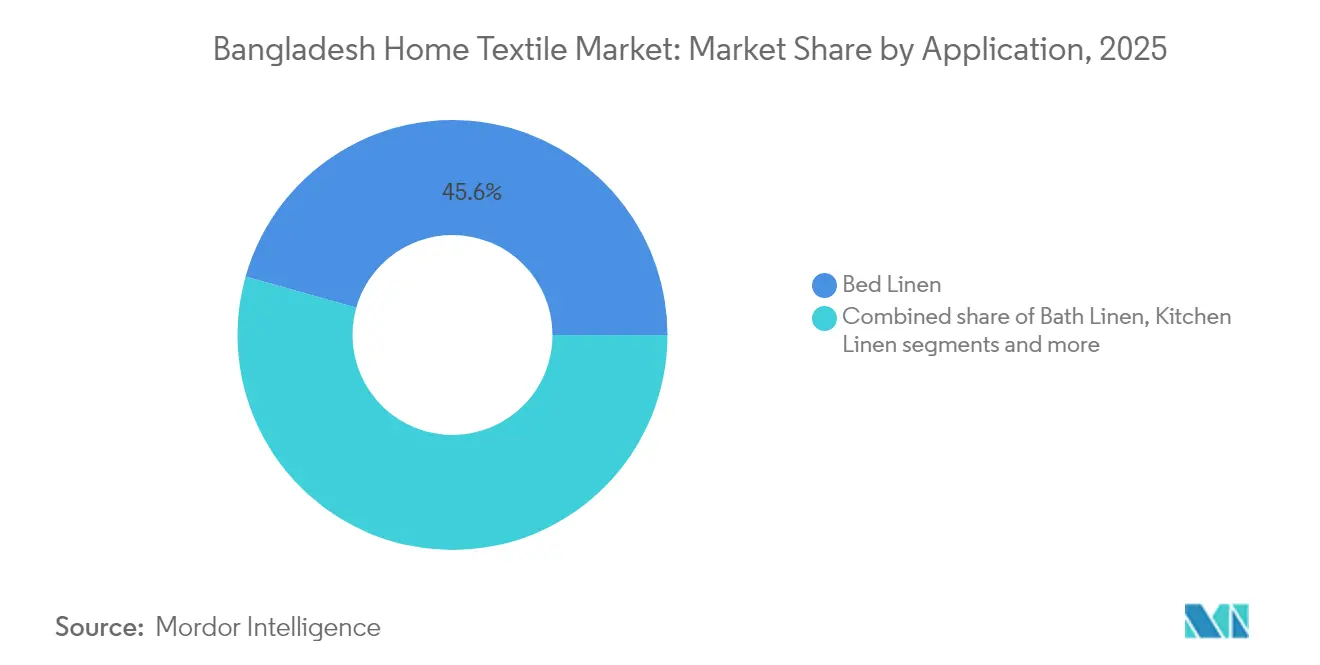

- By application, bed linen led with 45.62% of the Bangladesh home textiles market share in 2025. carpets & area rugs are forecast to expand at a 4.63% CAGR through 2031, the fastest among all applications.

- By material, cotton captured a 67.75% share of the Bangladesh home textiles market size in 2025. Synthetic Fibres are projected to register the highest 4.86% CAGR between 2026-2031.

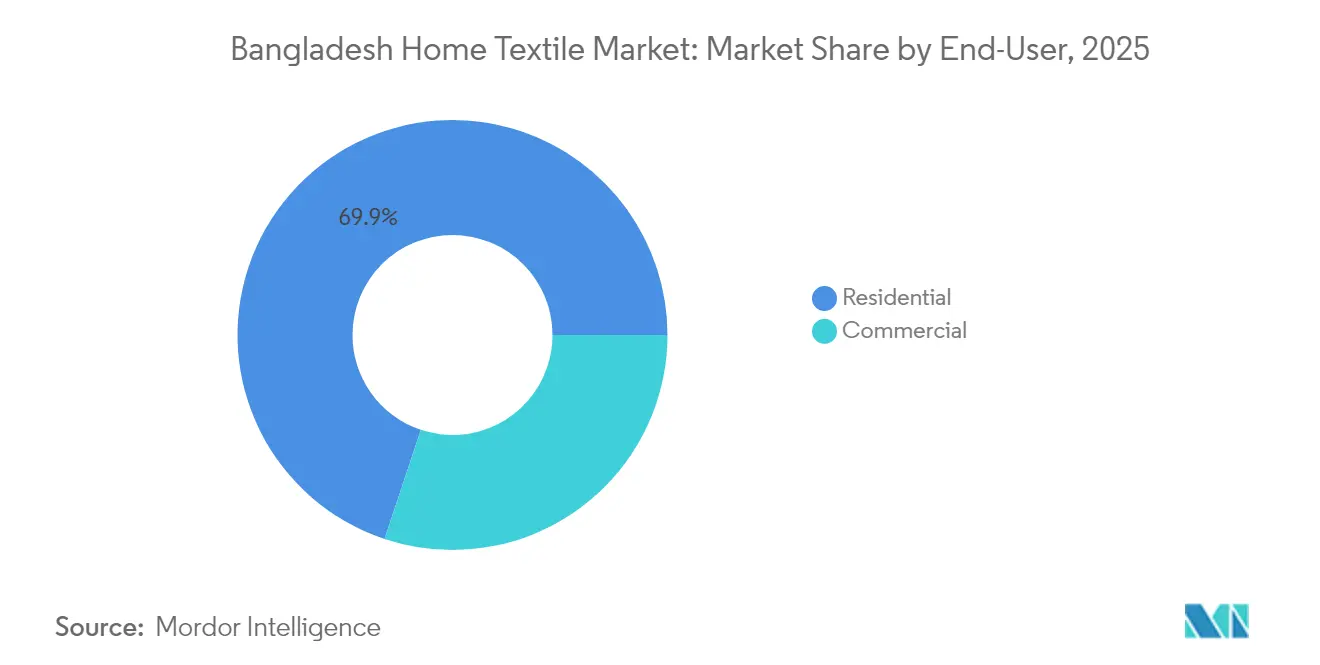

- By end-user, the residential segment accounted for 69.88% of the Bangladesh home textiles market size in 2025. Commercial applications are advancing at a 4.41% CAGR to 2031.

- By distribution channel, B2C/retail commanded 82.05% revenue share in 2025 and was advancing at a 4.74% CAGR to 2031.

- Geographically, the Dhaka division held 36.35% of the Bangladesh home textiles market share in 2025; the Sylhet Division is set to post a 4.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes | +0.8% | Dhaka, Chattogram, Sylhet; spillover nationwide | Medium term (2-4 years) |

| Duty-free EU/Canada/Japan access | +1.2% | Major EU destinations, Canada, Japan | Long term (≥4 years) |

| E-commerce boom | +0.6% | Domestic Bangladesh, regional export hubs | Short term (≤2 years) |

| Shift to higher-grade African cotton | +0.4% | Global quality-sensitive buyers | Medium term (2-4 years) |

| Adoption of eco-friendly fibers | +0.5% | EU and North America sustainability-focused markets | Long term (≥4 years) |

| “China-plus-one” sourcing diversion | +1.1% | The United States and EU buyer networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes Spurring Spending on Branded Home Décor

An expanding middle class of nearly 30 million consumers is moving beyond utilitarian linens toward branded aesthetics, lifting domestic value per purchase, especially in premium bed sheets and decorative pillow covers. Urban GDP growth of 3.8-4.5% in 2025 underpins this trend, strengthening discretionary budgets in Dhaka and Chattogram. Retailers note that brand recognition increasingly outweighs price as a deciding factor in household textile purchases, prompting manufacturers to invest in distinctive designs and stronger packaging. Bangladesh Standards and Testing Institution reinforces this shift by enforcing labeling and colorfastness norms that align with global requirements. Collectively, these factors lift the perceived quality ceiling and encourage local producers to target higher price points in the Bangladesh home textiles market.

Duty-Free EU/Canada/Japan Access Sustaining Export Demand

Preferential schemes such as the EU’s Everything but Arms program grant quota- and duty-free entry for Bangladeshi linens, towels, and curtains, securing roughly 60% of annual shipments to Europe. Exports under EBA currently amount to about USD 25 billion and shield producers from 9-12% ad-valorem tariffs levied on rivals[1]Staff Correspondent, “EU Everything But Arms scheme explained,” thefinancialexpress.com.bd.. Although Least Developed Country graduation in 2026 threatens this edge, the United Kingdom’s decision to extend GSP access through 2027 offers a near-term buffer. Producers are therefore accelerating capacity expansion and line certifications to lock in contracts ahead of tariff changes. Simultaneously, government negotiators are pursuing bilateral agreements to cushion the Bangladesh home textiles market against a sudden duty shock.

E-Commerce Boom Enabling Direct-to-Consumer Home-Textile Brands

Domestic platforms such as Fabric Lagbe and global-facing start-ups like Sourcewiz enable small and mid-sized factories to publish live catalogs, generate automated quotations, and transact with overseas buyers, reportedly boosting revenue by three-tenths in the first operational year[2]M. Islam, “Fabric Lagbe connects mills with buyers,” unb.com.bd.. Lower digital onboarding costs let producers sell batches as small as 300 units, democratizing export participation. Local shoppers also gravitate toward mobile marketplaces integrated with same-day delivery within Dhaka, widening consumer reach for novelty bedsheets and embroidered cushion covers. As a result, inventory cycles shorten, data analytics refine style assortments, and dependence on brick-and-mortar wholesalers declines. The channel, therefore, underwrites incremental volume and pricing power across the Bangladesh home textiles market.

Shift to Higher-Grade African Cotton Ensuring Better Yarn Quality

Large spinning mills are diversifying raw-cotton procurement towards premium West African grades that deliver higher strength-to-nep ratios, reducing fabric rejections and dye variability. While import costs edge up, mills recapture value through lower waste and stronger buyer quality scores. International retailers have responded by grading Bangladeshi bedding at par with Vietnamese and Turkish suppliers, opening avenues for higher-margin orders. The Cotton Development Board’s support for cultivar trials further signals long-run improvements in domestic agronomy. Elevated yarn consistency ultimately positions the Bangladesh home textiles market to climb the price ladder instead of competing solely on labor arbitrage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic gas & power outages | -1.4% | Nationwide, acute in industrial hubs | Short term (≤2 years) |

| Rising wage & compliance costs | -0.8% | Labor-intensive clusters | Medium term (2-4 years) |

| Loss of GSP benefits post-LDC graduation | -1.2% | EU, Canada, Japan export corridors | Long term (≥4 years) |

| High tariffs on specialty MMF fabrics | -0.6% | Synthetic fiber subsectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Gas & Power Outages Cutting Mill Utilization

Daily load-shedding of 7-9 hours forces roughly 19% of mills to run at just 40-50% capacity, while captive generators lie idle because pipeline pressure covers only 67% of national demand[3]Staff Reporter, “Power crisis slashes mill capacity,” newagebd.net.. Industrial gas prices have jumped from BDT 30 to BDT 42 per m³ since 2023, eroding contribution margins on energy-intensive bleaching and finishing processes. Exporters risk shipping delays and chargebacks when production stops mid-cycle, and some small operators have temporarily shut down weaving sheds in Narayanganj and Gazipur. Emergency allocations by the Power Division prioritize fertilizer plants over textiles, leaving little short-term relief. Consequently, buyer confidence wavers, and the Bangladesh home textiles market confronts systemic supply volatility.

Margin Squeeze from Rising Wage & Compliance Costs

Minimum wage revisions, fire-safety retrofits, and heightened social-audit frequency add cumulative pressure of 5-7% on FOB pricing, narrowing the competitiveness advantage Bangladesh once held over Pakistan and India. Factories aiming for BetterWork or SLCP conformity must allocate capital to worker well-being programs, cafeteria upgrades, and digitized payroll systems. Buyers rarely absorb these cost increments, compelling producers to search for efficiency in changeover times and material yields. The resultant capex outlays deter smaller mills from upgrading, potentially accelerating consolidation. This dynamic slows reinvestment cycles and affects volume growth for the Bangladesh home textiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Dominance Drives Volume Growth

Bed Linen anchors the Bangladesh home textiles market size, accounting for 45.62% of value in 2025. Vertically integrated leaders such as Zaber & Zubair run looms capable of weaving 400,000 meters of sheeting per day, guaranteeing large-lot consistency for European big-box retailers. Premium thread-count products shipped under OEKO-TEX labels command healthy unit economics even after energy surcharges. In contrast, the Bath and Kitchen Linen segments benefit from sustained hospitality procurement as global hotel chains refurbish room inventories post-pandemic. Upholstery textiles for sofas and drapery gain moderate traction from property development in Dhaka and Chattogram, although order volumes remain lower than bedding.

Carpets & Area Rugs constitute the fastest-expanding application, projected at a 4.63% CAGR. Heritage crafts like Nakshi Kantha stitchery and fine Jamdani motifs give Bangladeshi jute rugs a distinct artisanal appeal recognized by UNESCO. Export incentives of 8% on handicrafts help offset raw-material price volatility, yet weaver attrition and financing gaps limit scale. Government support under the National Handicraft Policy adds training and marketing grants, positioning artisan clusters in Tangail and Cumilla for higher foreign exchange earnings. Collectively, these forces elevate the rugs segment’s profile within the Bangladesh home textiles market.

By Material: Cotton Leadership Faces Synthetic Competition

Cotton contributes 67.75% of the Bangladesh home textiles market share in 2025, reflecting mills’ long-standing competency in carding, ring spinning, and finishing of staple-length fibers. Annual cotton imports run 8.5 million bales, equivalent to USD 8.67 billion, exposing mills to global price swings and shipping-route disruptions. The Cotton Development Board aims to raise local cultivation to 200,000 hectares by 2041, a move that could supply a fifth of demand and mitigate forex risk. Bangladesh home textiles market size for cotton products should therefore remain resilient, provided ginning infrastructure and Bt-cotton approvals materialize on schedule.

Synthetic Fibres, though smaller today, deliver the highest 4.86% forecast CAGR. Buyers value moisture-wicking, wrinkle-resistant, and quick-dry properties in polyester-rich bedsheets and microfiber comforters. High tariff walls on specialty MMF inputs currently dampen cost competitiveness, yet large groups are piloting recycled-ready PET yarn lines and exploring fabric recycling. Linen, jute, bamboo, and silk remain niche but command premium placements in eco-focused collections. Envoy Textiles’ waste-fabric recycling venture is a notable step toward circularity, aligning with EU requirements for traceability and low carbon intensity. Together, diversification beyond cotton broadens the Bangladesh home textiles market’s product mix.

By End-User: Commercial Segment Drives Premium Growth

The Residential segment captured 69.88% of the Bangladesh home textiles market share in 2025, driven by urban condominium growth and a preference for coordinated bed-and-bath ensembles. Retailers bundle bedsheets with cushion covers, pushing average ticket size higher. Traditional handloom goods such as Nakshi Kantha bedcovers still feature in gift purchases, but production constraints and skill shortages limit scale.

Commercial buyers, hotels, hospitals, and corporate guest houses register the stronger 4.41% CAGR through 2031. Hospitality chains stipulate chlorine-fast whites for institutional laundering and durability over 150 wash cycles, enabling factories to fetch a higher margin per yard. Sustainability certifications like GOTS and OEKO-TEX have become prerequisites for long-term supply. Compliance with fire-retardant specifications under U.S. NFPA 701 further distinguishes certified mills. Consequently, commercial sub-segments propel both value expansion and reputational lift for the Bangladesh home textiles market size.

By Distribution Channel: B2C Retail Transformation

B2C/Retail networks control 82.05% of the Bangladesh home textiles market size in 2025. Supermarkets such as Shwapno and Agora allocate dedicated shelf space to linens, while branded showrooms of ACS Textiles and Classical HomeTex flourish in high-income neighborhoods. Organized retail remains under-penetrated versus regional peers, implying headroom for floor-space growth.

Online channels enjoy double-digit expansion as mobile penetration hits 66% nationwide. Flash-sale events around Eid and Pahela Baishakh push spikes in bedsheet sales, and social commerce influencers increasingly endorse local brands. Mass Merchandisers capitalize on private-label programs to boost margins, whereas Mom-and-Pop stores retain relevance in rural districts by selling low-count cotton pillowcases. B2B/direct supply to institutional importers holds steady but cedes growth momentum to consumer outlets. This retail evolution deepens product assortment and price visibility throughout the Bangladesh home textiles market.

Geography Analysis

Dhaka Division commanded 36.35% of the Bangladesh home textiles market share in 2025, leveraging dense industrial estates, skilled labor pools, and seamless connectivity along the Dhaka-Chattogram corridor. Anchor projects such as the Beximco Industrial Park house spinning, weaving, dyeing, and finishing units within integrated campuses, streamlining lead times. Financial clusters in Motijheel and Uttara facilitate working-capital access, while Hazrat Shahjalal International Airport aids urgent sample dispatches. However, road congestion and gas rationing pose persistent logistical costs, prompting firms to explore satellite campuses in Gazipur and Manikganj.

Chattogram Division serves as the principal export gateway. The seaport handles over 90% of the country’s container trade, making its vessel berth queuing time a critical determinant of FOB competitiveness. Port-centric manufacturing enjoys customs-bond advantages, yet limited inland container depot capacity constrains off-dock efficiency. Planned Payra deep-sea port could alleviate some congestion, but until operational, exporters factor extra buffer days into shipment schedules. Proximity to the port nevertheless lowers internal freight for towel and bathrobe consignments compared with Dhaka-based suppliers.

Sylhet Division is forecast to post the fastest 4.97% CAGR through 2031. Government grants under the Bangladesh Economic Zones Authority are catalyzing light-manufacturing estates near the newly upgraded Sylhet airport. Diaspora remittances fuel retail spending on home upgrades, lifting local demand for premium bedding. Clusters in Rajshahi, Rangpur, Barishal, Khulna, and Mymensingh remain smaller but offer specialization opportunities in jute wall hangings and block-printed table linen. Infrastructure gaps, particularly gas pipelines and four-lane highways, must be closed to unlock production scalability across these secondary divisions. Together, regional diversification mitigates concentration risk for the Bangladesh home textiles market.

Competitive Landscape

The Bangladesh home textiles market exhibits moderate concentration anchored by vertically integrated groups such as Zaber & Zubair Fabrics, ACS Textiles, Apex Weaving & Finishing, and Mom Tex. Zaber & Zubair has invested more than USD 600 million in compaction, digital printing, and automated cutting lines, enabling daily output of 400,000 meters of fabric and 100,000 finished pieces destined mainly for Europe. ACS Textiles employs 5,000-plus staff across weaving, dyeing, and finishing, and exports OEKO-TEX-certified goods to Australia, North America, and the EU.

Strategic positioning revolves around cost leadership, compliance breadth, and buyer intimacy. Leading mills allocate up to 3% of revenue for sustainability capex, solar rooftops, and ZDHC-approved effluent treatment plants to secure long-term contracts. Smaller factories often serve as subcontractors but risk disintermediation as e-commerce and compliance demands escalate. Digital disruptors like Sourcewiz and Fabric Lagbe democratize export marketing for mid-tier suppliers yet require working-capital discipline to fulfill chunkier overseas orders. Financial distress at a few conglomerates, such as Beximco Group’s request for a BDT 4 billion bridge facility, highlights concentration risk and underscores the need for prudent liquidity management.

Emerging whitespace lies in eco-labeled collections, quick response drops for online retailers, and technical textiles such as fire-retardant drapery. Players armed with automated color kitchens and computerized jacquard looms can iterate designs rapidly, winning seasonal programs from Western retailers. Conversely, mills are slow to digitalize risk marginalization. Overall, scale, sustainability, and speed constitute the competitive triad shaping the Bangladesh home textiles market.

Bangladesh Home Textile Industry Leaders

Zaber & Zubair Fabrics Ltd. (Noman Group)

ACS Textiles (Bangladesh) Ltd.

Apex Weaving & Finishing Mills Ltd.

Noman Terry Towel Mills Ltd. (NTTML)

Momtex Expo Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Beximco Group’s Textiles and Apparel Division requested Tk 4.0 billion government support to keep 31 exporting factories running and settle wage arrears, averaging USD 32 million monthly exports over six years.

- November 2024: Ha-Meem Group initiated a digital productivity upgrade in partnership with Coats Digital.

- September 2024: Envoy Textiles unveiled a waste-fabric recycling plant to bolster circular production capacity.

- February 2024: Alif Industries moved to acquire Royal Denim and Diamond Dredging, aiming for 90% value addition in denim with 750,000-yard monthly capacity.

Bangladesh Home Textile Market Report Scope

Home textiles are fabrics and clothes used specifically for furnishing a residence. The materials and design of each are defined by the functional and aesthetic uses of each. Bangladesh Home Textile Market is segmented by product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and Floor Covering) and by distribution channel (Supermarkets & Hypermarkets, Specialty Stores, Online, and other distribution channels). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Local Mom and Pop Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct from the Manufacturers |

By Region

| Dhaka Division |

| Chattogram Division |

| Khulna Division |

| Rajshahi Division |

| Rangpur Division |

| Barishal Division |

| Sylhet Division |

| Mymensingh Division |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Local Mom and Pop Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct from the Manufacturers | ||

| By Region | Dhaka Division | |

| Chattogram Division | ||

| Khulna Division | ||

| Rajshahi Division | ||

| Rangpur Division | ||

| Barishal Division | ||

| Sylhet Division | ||

| Mymensingh Division | ||

Key Questions Answered in the Report

Which region is growing the fastest for home-textile production?

Sylhet Division is forecast to record a 4.97% CAGR through 2031 on the back of new economic zones and rising consumer spending.

What is the main challenge facing manufacturers now?

Chronic gas and power shortages are curbing mill utilization to as low as 40-50%, raising production costs and delaying shipments.

How will LDC graduation affect exports?

Loss of GSP duties from 2026 could cut export earnings by 7-14% unless new bilateral agreements or diversified product strategies offset the tariff hike.

Which material segment is gaining momentum beyond cotton?

Synthetic fibres, particularly recycled polyester, are projected to grow at a 4.86% CAGR because buyers seek performance fabrics and eco-friendly credentials.

What is the current value of the Bangladesh home textiles market?

The market is valued at USD 511.16 million in 2026 and is projected to rise to USD 622.84 million by 2031.

Which application drives the highest revenue?

Bed Linen holds 45.62% of total revenue, benefiting from scale production and strong European demand.

Page last updated on: