Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.18 Billion |

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 4.89 Billion |

| Growth Rate (2026 - 2031) | 2.65% CAGR |

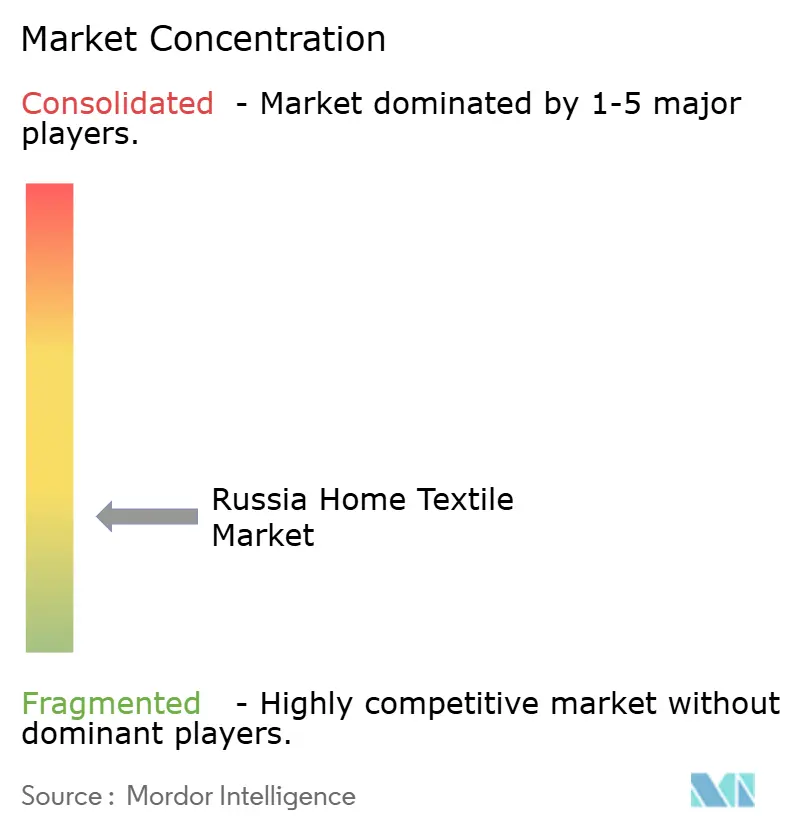

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Home Textile Market Analysis by Mordor Intelligence

The Russia home textile market size is expected to increase from USD 4.18 billion in 2025 to USD 4.29 billion in 2026 and reach USD 4.89 billion by 2031, growing at a CAGR of 2.65% over 2026-2031. A steady policy push toward localization and tighter compliance is supporting the Russia home textile market as domestic mills reduce exposure to imported inputs, stabilize lead times, and capture formalized demand. Mandatory data-matrix labeling under the Chestny ZNAK program is curbing grey channels, improving shelf discipline, and lifting realized prices as compliance becomes embedded in ex-factory rates. Marketplace consolidation remains a powerful force, with Wildberries and Ozon surpassing 72% combined share of consumer e-commerce spend in 2025, broadening distribution options for small- and mid-sized mills that meet listing and labeling standards. Mortgage-backed renovation activity is shifting more premium fabrics, such as cotton-sateen and jacquard upholstery, into mass channels, expanding average order values as curated room sets and bundled assortments gain traction[1]Editorial Team, “Wildberries, Ozon Maintain Leadership in Russia E-commerce,” Xinhua, news.cn.

Key Report Takeaways

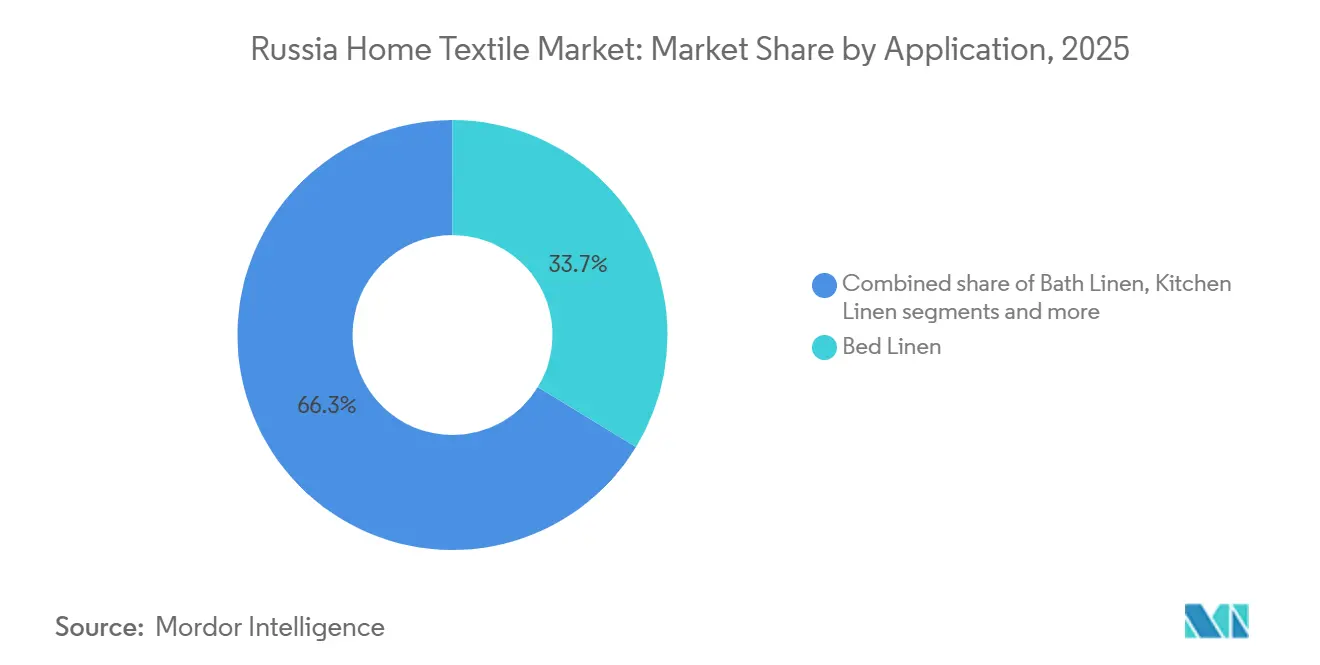

- By application, bed linen led with 33.72% revenue share in 2025 in the Russia home textile market and is expanding at a 2.95% CAGR through 2031.

- By material, cotton commanded a 51.05% share in 2025 in the Russia ome textile market, while other natural fibers registered the highest projected CAGR at 3.03% through 2031.

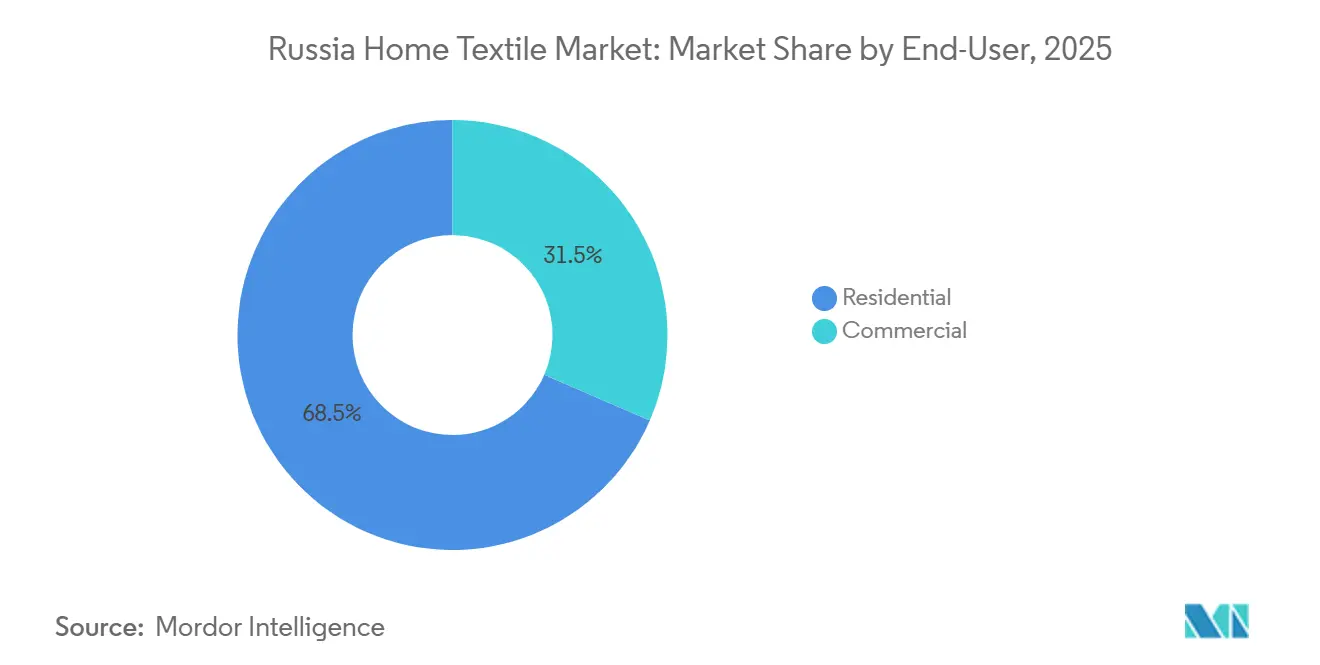

- By end-user, residential accounted for 68.45% of the value in 2025 in the Russia Home textile market and is advancing at a 3.28% CAGR through 2031.

- By distribution channel, offline retail held 66.00% of value in 2025 in the Russia home textile market, and online is growing at a 3.92% CAGR through 2031.

- By geography, Central Russia captured a 23.35% share in 2025 in the Russia home textile market, while Northwest Russia is the fastest-growing at a 4.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce marketplaces scale up, lifting online share of home textiles | +0.7% | Global, particularly Moscow, Saint Petersburg, and Central Russia | Medium term (2-4 years) |

| Domestic tourism and hospitality linen replacement accelerates | +0.2% | Central Russia, Northwest Russia, South & North Caucasus | Medium term (2-4 years) |

| Import substitution and localization support domestic manufacturing | +0.6% | Central Russia (Ivanovo cluster), Volga Region | Long term (≥ 4 years) |

| Home renovation and decor refresh cycles sustain demand | +0.5% | National, with early gains in Moscow, Saint Petersburg | Short term (≤ 2 years) |

| Mandatory product labeling (Chestny ZNAK) formalizes market and premiumizes assortments | +0.4% | National | Short term (≤ 2 years) |

| Ivanovo cluster on-demand digital printing shortens design-to-shelf lead times | +0.3% | Central Russia, with spill-over to the Volga Region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Marketplaces Scale Up, Lifting Online Share of Home Textiles

E-commerce scale continues to reshape the Russia home textile market as Wildberries and Ozon expand logistics coverage and simplify seller operations tied to compliance and inventory health. Next-day fulfillment now covers much of Moscow Oblast and Saint Petersburg, and new pickup points in Tatarstan and Bashkortostan reduce last-mile costs and widen access in Tier-2 and Tier-3 cities. Platform changes that removed punitive inventory indexing and automated the removal of low-performing goods improved margins and seller agility, enabling regional mills to rotate assortments into trending designs faster. As marketplaces prioritize listings with valid Chestny ZNAK codes and local fulfillment, discoverability improves for compliant domestic manufacturers, lifting click-through and conversion on core bed and bath lines. Stricter listing checks under TR CU 017/2011 keep home textiles aligned with product safety norms before sale, thereby supporting buyer confidence. Together, these marketplace changes are increasing the share of online-driven demand in the Russia home textile market by lowering friction for SMEs that meet compliance and logistics benchmarks.

Domestic Tourism and Hospitality Linen Replacement Accelerates

Domestic travel has remained resilient, and occupancy improvements in secondary cities are pulling forward replacement cycles for hospitality-grade bedding and terry. Buyers are standardizing 250-thread-count cotton-sateen blends and antimicrobial pillow protectors in line with infection-control priorities, creating steady batch orders that emphasize repeatability and color consistency. Multi-year framework contracts with chain hotels and healthcare networks support predictable volumes for vertically integrated mills that control spinning through sewing. Sanatoriums and resort operators adopted higher-spec towels and bathrobes with bamboo-cotton blends as hygiene and durability targets moved closer to four-star benchmarks. This institutional pull strengthens the commercial end of the Russia home textile market while reinforcing premium specifications that later diffuse into residential assortments.

Import Substitution and Localization Support Domestic Manufacturing

A December 2024 federal decree set a 90% domestic sourcing threshold for textiles in public procurement, channeling tenders to mills with local value addition and proven certifications. Low-interest loans from the Federal Industrial Development Fund supported upgrades to looms and finishing across Ivanovo, Vladimir, and Yaroslavl, improving throughput and consistency on prioritized lines. Ivanovo’s membrane-fabric cluster initiated domestic production, shortening lead times from months to weeks and reducing exposure to overseas supply chains. A planned Liocel line positions a leading mill to substitute imported viscose and modal with locally produced wood-pulp-based fiber, advancing medium-term supply independence[2]Press Office, “Membrane Fabric Production Launch in Ivanovo,” Ivanovo Gazette, ivgazeta.ru. Dye localization via a planned reactive-dye plant in Tatarstan is set to temper spot-purchase volatility and elevate color consistency once it ramps, touching a wide array of mill operations in Central Russia and the Volga Region.

Home Renovation and Decor Refresh Cycles Sustain Demand

Preferential mortgages issued in 2024 catalyzed remodels that included bed, bath, and window treatments, and this momentum is sustaining replenishment in 2026 as new homeowners continue to tailor interiors. Retail sales are tilting toward higher-ticket bedding sets as consumers allocate more discretionary spending to coordinated cotton-sateen sheets and jacquard throws. Design studios and digital mood-board tools are proliferating colorways and motifs, aided by Ivanovo’s digital printing, which compresses design-to-shelf cycles. Licensed character lines in nursery textiles now represent a visible slice of volume and maintain consistent premiums over generics, which elevates margins for compliant brands. Collaboration between mills and interior designers, including curated room kits that bundle bedding and décor, increases basket size without adding shopper friction. Seasonal micro-collections for towels and table linens mirror apparel calendars, preserving freshness and improving sell-through for mills that can plan short cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Input cost and FX volatility pressure pricing and margins | -0.6% | National | Short term (≤ 2 years) |

| Sanctions and logistics constraints limit access to fibers, dyes, and machinery | -0.9% | Central Russia, Volga Region, Northwest Russia | Long term (≥ 4 years) |

| Marketplace returns/discounting squeeze SME profitability | -0.3% | National, particularly Central Russia (Ivanovo SMEs) | Medium term (2-4 years) |

| Compliance testing and labeling raise time-to-market for small producers | -0.2% | National, with acute impact in Tatarstan, the Volga Region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Input Cost and FX Volatility Pressure Pricing and Margins

Exchange-rate swings have raised landed costs for cotton lint and polyester filament, creating persistent pressure on converter margins where hedging tools are limited. Inflation and high benchmark rates tightened financing conditions, compressing working capital and shortening payment terms in distribution. Reactive dye lead times lengthened, prompting mills to carry additional buffer stocks and tie up liquidity[3]Editorial Team, “Country and Currency Risk Insights,” Lloyds Bank Trade Portal, lloydsbanktrade.com. Wage arrears rose in early 2025, indicating broader fiscal stress that often spills into light-industry supply chains. Consumer price sensitivity remains pronounced at specific retail thresholds for bed-linen sets, which limits pass-through and delays purchases when inflation peaks, adding volatility to near-term sell-through.

Sanctions and Logistics Constraints Limit Access to Fibers, Dyes, and Machinery

United Kingdom rules introduced in April 2025 banned select technical-textile exports, while United States export controls kept most advanced textile machinery under license denial, stalling modernization cycles. Tighter European restrictions severed access to preferred European looms and components, extending equipment replacement timelines and raising maintenance burdens on older assets. Synthetic-fiber imports fell, and domestic producers have not fully replaced prior consumption, raising reliance on a narrower local base. Payment hurdles with foreign counterparties persist, which encouraged the rollout of local payment options that still carry conversion fees. Grey-channel goods in border regions undercut compliant pricing and add localized pressure on share, where customs enforcement remains a moving target.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Residential Replacement and Hospitality Upgrade Converge

Bed linen held 33.72% of the Russia home textile market in 2025 and is advancing at a 2.95% CAGR through 2031 as replacement cycles in homes and institutions remain steady. Consumers are upgrading to higher thread counts and smoother hand-feel fabrics, supported by mortgage-enabled remodels that shift more sales into curated room kits and coordinated sets. Upholstery fabrics, including curtains and cushion covers, accounted for 18% and benefited from stronger 2024 orders for textured drapes that align with refreshed interior palettes. Jacquard and chenille demand accelerated as interior design briefs favored tactile finishes across living and bedroom environments. Carpets and rugs, consolidated under “Others,” saw production growth in 2024, aided by competition among domestic and foreign suppliers and improved labeling compliance.

Digital tools and seasonal planning are lifting sell-through across the Russia home textile market. Bed-linen producers are adopting a short-cycle calendar that rolls out four micro-collections per year, keeping assortments fresh and lowering end-of-season carryover. Licensed character prints secured a notable slice of children’s lines and commanded price premiums that reward brand-safe production with verified labeling. E-commerce bundling of bath kits raised average basket sizes as shoppers pair towels, mats, and curtains during a single checkout. Compliance with TR CU 017/2011 and associated EAC requirements standardizes quality and safety across applications, which supports confidence in higher-priced selections. These combined shifts keep the Russia home textile market centered on bed and bath while pulling incremental demand into décor add-ons.

By Material: Cotton Anchors, Alternative Fibers, Pivot Sustainability

Cotton accounted for 51.05% of material usage in 2025, though its growth rate lags synthetics and specialty fibers as buyers weigh durability and cost-in-use. Exchange-rate volatility increased cotton input costs in 2024, which pressured margins for converters operating on fixed-price retail shelves. Linen maintained a niche anchored in eco-premium positioning, aided by expanded flax cultivation that broadens traceable supply for regional mills. Synthetic fibers, led by polyester blends, are capturing institutional orders, where shrink resistance and quick-dry performance reduce laundry costs, while domestic output rose in 2026 to meet this need. Polyester-cotton blends are the workhorse for hospitality bed linens, aligning fabric behavior with commercial laundering constraints while protecting hand feel.

Other natural fibers, including hemp and bamboo-based blends, are poised for 3.03% CAGR through 2031 growth, buoyed by green labeling and local cultivation initiatives. The Green Thread recycling cluster feeds regenerated cotton yarn into early towel and bathrobe runs, linking circular inputs to commercially viable products. A planned Liocel line will shift dependence away from imported viscose and modal, offering mills a domestic alternative with consistent fiber properties. Membrane fabric launched in Ivanovo supports technical and outdoor applications and is now appearing in water-resistant décor such as outdoor drapes and cushion covers. Tightening of Chestny ZNAK requirements reduces mislabeling risk and narrows arbitrage on imported fabrics, which favors mills that invest in verified fiber-content labeling across the Russia home textile market.

By End-User: Residential Leads, Commercial Consolidates Supplier Base

Residential customers accounted for 68.45% of the 2025 value and are forecast to grow at a 3.28% CAGR through 2031 as mortgage-enabled renovations and online shopping drive more frequent refreshes. Online mood boards and influencer-led curation are supporting higher average order values and smoother selection experiences for first-time buyers. Marketplace AR tools reduced return rates for window and décor categories, improving logistics efficiency and buyer satisfaction. Residential buyers are also adopting hospitality-grade specifications at home, narrowing the gap in sheet quality and towel GSM between the two end-user groups. This dynamic keeps the Russia home textile market anchored in household demand while borrowing design and performance cues from contract buyers.

Commercial end-users accounted for 31.55% and benefited from institutional batch purchasing and framework agreements that ensure volumes and repeatability. Hotels and healthcare operators have standardized higher-thread-count bed linens and antimicrobial pillow protectors as a hygiene baseline, which secures predictable orders for full-cycle mills. Sanatoriums in the North Caucasus upgraded terry goods to four-star standards, with bamboo-cotton blends gaining traction for their tactile and drying performance. Public procurement rules that mandate domestic content consolidate demand with vertically integrated suppliers that can prove local value addition and compliance. EAC certification and TR CU 017/2011 compliance apply uniformly across the residential and commercial segments, leveling the playing field for quality and safety in the Russian home textile market.

By Distribution Channel: E-commerce Algorithms Favor Local Mills

In 2025, offline channels, led by hypermarkets, home centers, and specialty stores, remain dominant as shoppers value hands-on fabric checks, immediate pickups, and familiar routines. Specialty stores in Moscow and Saint Petersburg attract Millennials with designer collaborations, exclusive patterns, OEKO-TEX labels, and in-store consultations. Premium bedding buyers prefer in-store validation for softness and weave density, keeping showrooms relevant.

Online channels grow at 3.92% through 2031. Next-day delivery expanded to Moscow Oblast and Saint Petersburg, while new pickup points in Tatarstan and Bashkortostan reduced costs and extended Tier-2 city reach. Wildberries removed its inventory index, and Ozon introduced automated goods removal, improving margins for regional mills and enabling faster inventory pivots. Augmented-reality tools reduced return rates for curtains and upholstery, attracting first-time buyers in underserved regions. Mobile orders dominated Wildberries' sales, supported by high smartphone penetration and mobile payment adoption. Commission tiers compressed prices compared to specialty stores while increasing unit volumes. Domestic mills avoided cross-border fees, benefiting from a majority of platform listings. Federal Antimonopoly Service scrutiny improved marketplace practices, enhancing SME access and Tier-2 consumer adoption.

Geography Analysis

Central Russia accounted for 23.35% of 2025 revenue, with Ivanovo, Vladimir, and Yaroslavl oblasts capitalizing on vertically integrated clusters that compress sourcing and production within short radii. Ivanovo introduced a textile recycling hub in July 2024 that processes post-consumer waste into regenerated yarn and quickly scaled from 200 to 400 tons per month by year-end, adding a circular input stream to local output. Digital printing capacity added between mid-2024 and early 2025 shortened pattern-to-production time from weeks to days and lowered minimums, enabling testing of niche motifs. Entrepreneurs in the region recorded one of the nation’s highest volumes of online sales in 2024, underscoring the region’s e-commerce fluency within the Russia home textile market. Local membrane-fabric production reduced lead times for technical applications, and Moscow’s light-industry output rose in early 2025 on the back of synthetic fibers. The area’s growth pace is moderate through 2031 due to capacity constraints in finishing, but strong proximity to Moscow’s retail ecosystem protects profitability.

Northwest Russia is the fastest-growing sub-region, tracking a 4.08% CAGR through 2031, driven by Saint Petersburg’s port access, rising local incomes, and trade links that favor linen and specialty inputs. Flax cultivation increased in early 2025 to supply eco-premium linen positions, supporting Northwest mills that market traceable fibers. Border dynamics have led to grey-channel competition in some areas, but stricter enforcement against suspicious EAC declarations has tightened customs controls and improved conditions for compliant mills. Modernization programs boosted linen throughput in select facilities and complemented Ivanovo’s cotton leadership, creating a broader material base for the Russia home textile market. While logistics in Kaliningrad remain complex, the region leverages its proximity to neighbors to target exports outside the strictest sanction scopes.

The South and North Caucasus together benefit from domestic tourism and upgrades to sanatoriums, which raise demand for hospitality linens and higher-GSM terry. Marketplaces added pickup points in regional capitals, lowering last-mile costs and aiding B2C penetration across Volga cities. Elsewhere, the Urals and Siberia exhibit mixed retail fabric trends tied to sector-specific wage cycles, yet e-commerce expansion and infrastructure investment in Far Eastern centers are lifting home-textile sales. Vladivostok’s port access and tighter labeling checks are curbing grey flows and supporting compliant domestic sellers that move standardized SKUs into hospitality projects ahead of 2030.

Competitive Landscape

The Russia home textile market remains moderately fragmented, leaving room for agile converters to compete in regional pockets and specialty niches. Vertical integration is a differentiator as mills that operate spinning, weaving, dyeing, and sewing in proximity deliver repeatable batches and color consistency valued by institutional buyers. Brands that commit to steady design refreshes and curated collections have cultivated loyal urban segments willing to pay for premium satin-jacquard sets showcased in omnichannel displays. Certifications such as OEKO-TEX and ISO unlock financing for equipment upgrades and signal quality across both marketplaces and specialty retail.

Mills aligned with public procurement rules are consolidating commercial demand, and labeling compliance now enables targeted action against counterfeiters using trace data to protect brands. Mattress-led retailers expanding into bedding are pairing sleep systems with coordinated linens to grow transaction values, while white-label partnerships with hypermarkets add volume for major converters. Sustainability narratives are strengthening as larger mills invest in recycled inputs and circular processes, aided by recycling capacity that turns post-consumer waste into regenerated yarn for bath and bed. Ivanovo’s new digital-printing base reduces design-to-shelf timing to about a week for select runs, enabling faster motif testing and reducing the first-mover advantage held by legacy catalogs.

Marketplace policy changes that reward verified labeling and local fulfillment raise the visibility of compliant SMEs, while regulatory oversight has trimmed controversial practices that once penalized smaller sellers. Direct-to-consumer webstores are yielding margin gains for established brands that can absorb logistics and customer care, and marketplaces remain critical for long-tail discovery across the Russia home textile market. Uniform enforcement of TR CU 017/2011 and EAC declarations creates barriers for unverified importers, supporting domestic mills with accredited lab ties and strong compliance teams[4].Editorial Team, “Technical Regulation TR CU 017/2011,” GOST Russia, gostrussia.com

Russia Home Textile Industry Leaders

Shuyskie Sitsy

Togas

Kariguz

TDL Textile

Nordtex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Government Decree No. 1875 mandated 90% domestic sourcing for textiles in public procurement, concentrating tenders with mills that can verify local value addition.

- November 2024: “Fotoprint-Ivanovo” delivered Russia’s first million linear meters of domestically produced membrane fabric and secured subsidies and preferential loans to accelerate production. This breakthrough substituted imports for home textile.

Russia Home Textile Market Report Scope

Home textiles are the textiles used for home furnishing. It consists of a range of functional as well as decorative products mainly used in decorating houses.

The Russian home textile market is segmented by product (bed linen, bath linen, kitchen linen, upholstery, and floor covering) and distribution channel (supermarkets and hypermarkets, specialty stores, online stores, and other distribution channels). The report offers market sizes and forecasts in terms of revenue (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets & Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Region (Russia)

| Central Russia (Central FD) |

| Northwest Russia (Northwestern FD) |

| South & North Caucasus (Southern + North Caucasian FD) |

| Volga Region (Volga FD) |

| Rest of Russia |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Others (Carpets & Area Rugs) | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Region (Russia) | Central Russia (Central FD) | |

| Northwest Russia (Northwestern FD) | ||

| South & North Caucasus (Southern + North Caucasian FD) | ||

| Volga Region (Volga FD) | ||

| Rest of Russia | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the Russia home textile market?

The Russia home textile market size was USD 4.18 billion in 2025 and is projected to reach USD 4.89 billion by 2031 at a 2.65% CAGR.

Which applications lead demand within Russia’s home textiles?

Bed linen leads by value with a 33.72% share in 2025, supported by steady residential replacement and institutional upgrades, and it is growing at a 2.95% CAGR through 2031.

How is e-commerce shaping the Russia home textile market?

Marketplaces like Wildberries and Ozon account for more than 72% of online consumer spend and favor compliant domestic sellers through algorithmic ranking and logistics coverage.

Which regions are most important for production and growth?

Central Russia, anchored by Ivanovo, accounts for 23.35% of revenue, while Northwest Russia is the fastest-growing region at a 4.08% CAGR through 2031, driven by port access and rising incomes.

What regulations most affect market participation?

TR CU 017/2011 and EAC declarations govern safety and labeling, and Chestny ZNAK data-matrix codes are mandatory for light-industry goods, which formalize supply and reduce counterfeit risk.

Page last updated on: