Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

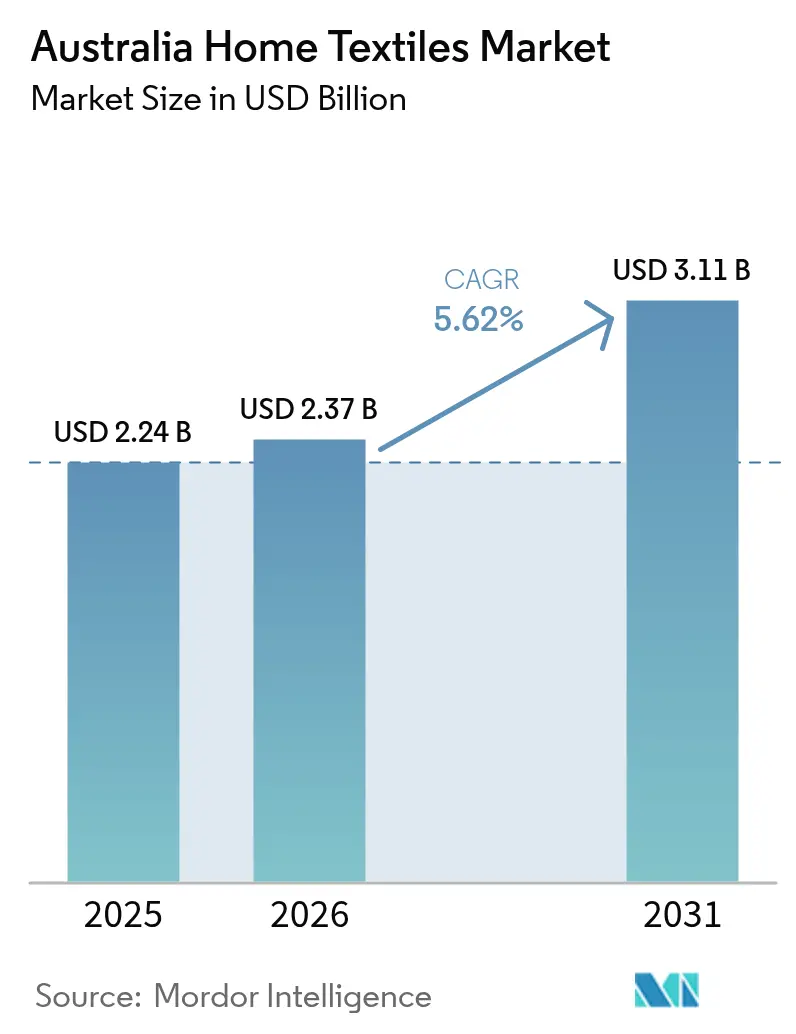

| Base Year Market Size (2025) | USD 2.24 Billion |

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

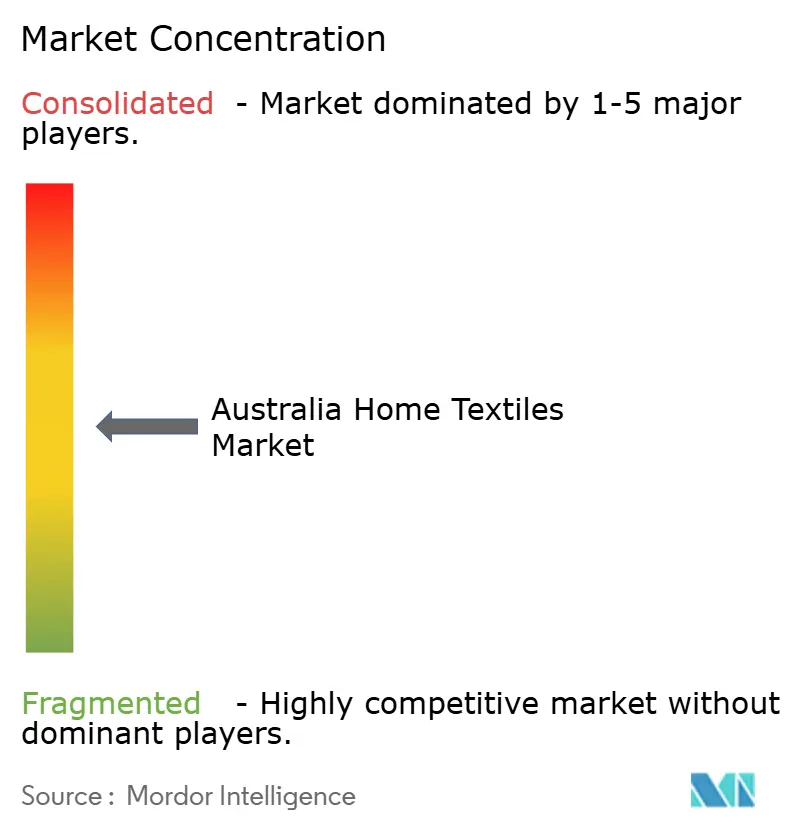

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Home Textiles Market Analysis by Mordor Intelligence

Australia home textile market size in 2026 is estimated at USD 2.37 billion, growing from 2025 value of USD 2.24 billion with 2031 projections showing USD 3.11 billion, growing at 5.62% CAGR over 2026-2031. Sustained renovation activity, premium natural-fiber adoption, and government support for domestic sourcing keep momentum strong even as overall discretionary spending normalizes. Millennials and Gen Z households continue to re-allocate travel and entertainment budgets toward home upgrades, bolstering demand for coordinated bed, bath, and upholstery collections. Climate-adaptive innovations such as nanodiamond cooling fabrics enhance product differentiation, while omnichannel fulfillment models convert online interest into in-store or locker pickups with minimal friction. Domestic mills benefit from tighter circular-economy rules that encourage longer product life cycles and higher recycled content, yet they must still navigate raw-material price swings and labor shortages.

Key Report Takeaways

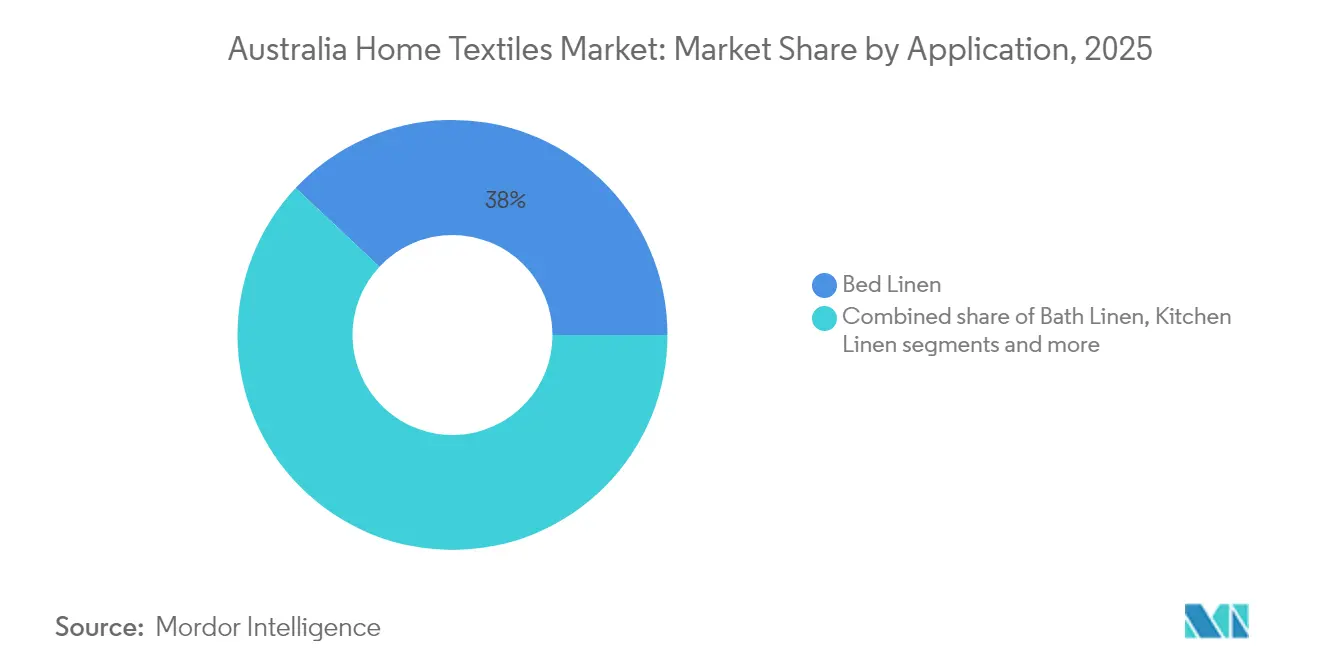

- By application, bed linen led with 38.02% revenue share of the Australia home textile market in 2025; upholstery is forecast to expand at a 5.82% CAGR through 2031.

- By material, cotton accounted for 40.78% of the Australia home textile market size in 2025, while alternative natural fibers are projected to grow at 5.63% through 2031.

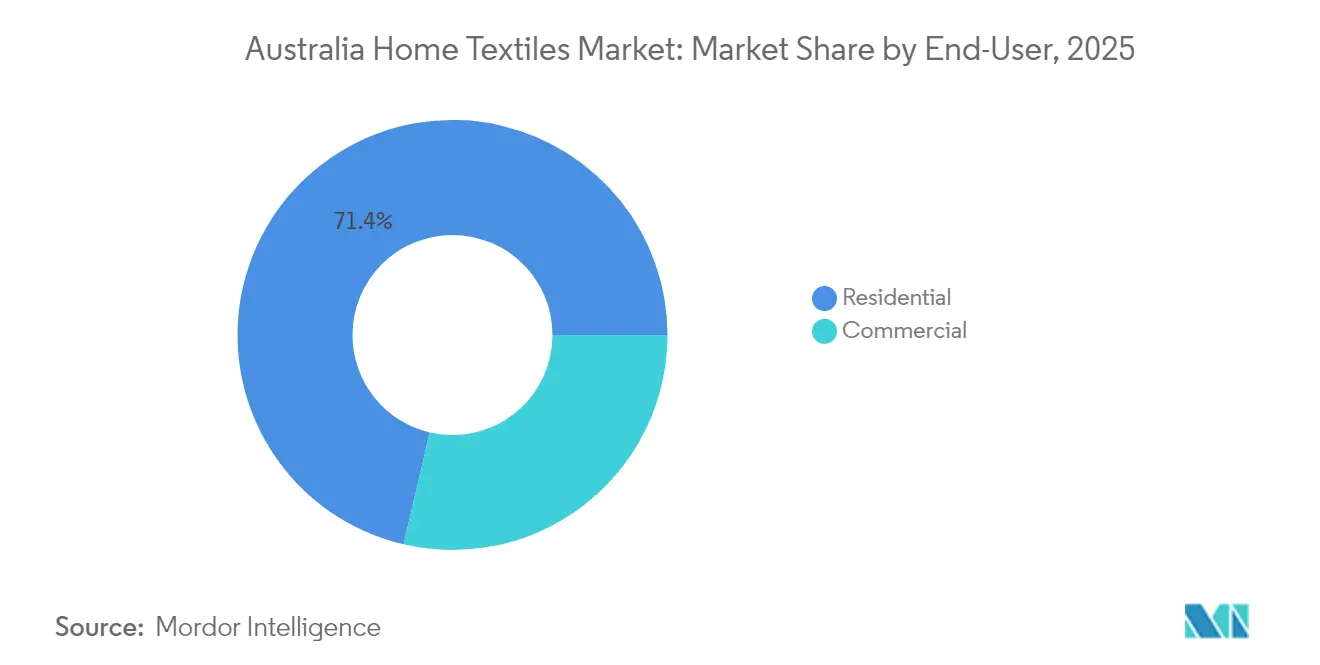

- By end-user, residential purchases represented 71.35% of the Australia home textile market share in 2025 and the commercial segment is advancing at a 5.78% CAGR to 2031.

- By distribution channel, B2C retail captured 65.12% of the Australia home textile market in 2025; B2B direct sales post the highest projected CAGR at 5.66% through 2031.

- By region, New South Wales held 23.22% of the Australia home textile market size in 2025; Queensland is on track for a 6.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Home Textiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation spending momentum | +1.2% | Capital-city corridors in NSW, VIC, QLD | Medium term (2-4 years) |

| Premium shift to natural fibers | +0.9% | Sydney, Melbourne, Gold Coast | Long term (≥ 4 years) |

| E-commerce and click-and-collect | +0.8% | Metropolitan and emerging regional hubs | Short term (≤ 2 years) |

| Local-content procurement mandates | +0.6% | Canberra and state capitals | Medium term (2-4 years) |

| Circular-economy regulations | +0.5% | NSW leadership; VIC and QLD adoption | Long term (≥ 4 years) |

| Climate-adaptive smart textiles | +0.4% | Tropical and arid states: QLD, NT, WA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renovation Spending Momentum

Home-improvement outlays now account for roughly 40% of total residential construction activity, and permit valuations in Brisbane, Sydney’s Northern Beaches, and Melbourne’s eastern suburbs keep rising. Consumers who accrued excess household savings during pandemic lockdowns continue to invest in soft-furnishing upgrades that create hotel-style comfort at home. Re-zoning incentives promoting secondary dwellings also stimulate fresh textile purchases when homeowners add granny flats or studios. National banks report that home-equity withdrawals increasingly fund interior refresh projects, further supporting high-ticket bedding sets and custom curtains. Large-format retailers quickly rotate seasonal color palettes to capture repeat purchases prompted by these ongoing makeovers.

Premium Shift to Natural Fibers

Heightened wellness awareness pushes shoppers toward breathable, hypoallergenic bedding made from organic cotton, linen, hemp, and bamboo. Domestic labels highlight certifications such as Global Organic Textile Standard and Oeko-Tex to establish trust and command 20-30% price premiums. Retail analytics show attach rates rising for accessories like quilt covers and throws when shoppers begin with an organic-fiber sheet set, lifting basket values. The shift also aligns with state government waste-reduction targets that favor biodegradable inputs over synthetics. Mills capable of blending lesser-known fibers such as jute or kapok earn early-mover advantages as retailers curate “new naturals” collections.

E-Commerce and Click-and-Collect

Online home-textile revenue topped USD 45.9 billion equivalent in 2024, and checkout data indicates that click-and-collect now accounts for 70% of digital orders. Locker networks at high-traffic stores, pioneered by IKEA Rhodes, shorten the last mile for bulky quilts and pillows while keeping freight emissions low. Search-driven discovery funnels shoppers into virtual swatch tools, and subsequent store pickup drives incremental spending on décor accents. Marketplace expansions at BIG W and MyDeal are widening SKU counts for niche fibers and bespoke sizes that physical shelves cannot hold. Yet return logistics remain a cost center, prompting investments in AI-guided size and fabric advisors to minimize fit-and-feel surprises.

Local-Content Procurement Mandates

The Future Made in Australia Act 2024 requires federal departments to evaluate domestic value-added ratios when awarding textile contracts exceeding USD 0.62 million (AUD 1 million). Similar criteria cascade to state and defense projects, channeling linen, towel, and curtain orders toward compliant suppliers. Mid-sized mills in regional hubs collaborate with social enterprises to secure workforce pipelines, ensuring they meet the act’s job-creation benchmarks. Preferred-supplier status brings longer contract tenures that justify capital spending on energy-efficient dyeing lines. For retailers, provenance labeling becomes a marketing tool that resonates with consumers seeking to support local manufacturing ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cotton-price volatility | -0.8% | Major cotton-processing corridors in NSW and QLD | Short term (≤ 2 years) |

| Import-led price pressure | -1.1% | Nationwide, acute in mass-market channels | Medium term (2-4 years) |

| Manufacturing-skills shortage | -0.6% | Industrial clusters in NSW, VIC, SA | Medium term (2-4 years) |

| Rising water & energy compliance costs | -0.4% | Regions with water-intensive processing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cotton-Price Volatility

Global benchmark prices have swung between USD 0.80 and USD 1.20 per pound over the past 18 months, compressing mill margins and complicating hedging strategies. Floods along the Macquarie and Namoi rivers curtailed harvests, causing sudden fiber shortages even as export commitments remained in place. Spinning facilities rely on multi-origin blends to smooth supply, yet freight bottlenecks continue to inflate landed costs. Retailers respond by staggering promotional calendars and adjusting fabric GSM to protect entry-price points. Wool production at century-low levels eliminates a traditional substitute, leaving mills exposed to synthetic fiber substitution risks that may dilute sustainability narratives.

Import-Led Price Pressure

Domestic factories compete against Pakistan and China, whose combined bed-linen exports exceed USD 1.3 billion. Favorable trade agreements and lower utility tariffs allow offshore producers to land finished goods at prices that often undercut Australian cut-and-sew operations by 25%. Private-label buyers for discount chains leverage this gap to maintain aggressive price ladders, reinforcing consumer expectations of perpetual markdowns. Local brands counter with limited-edition artistry and traceability features but must still cover higher wages and compliance expenses. The widening cost delta threatens to cap unit growth for made-in-Australia lines in the mid-market tier[1]Australian Bureau of Agricultural and Resource Economics and Sciences, “Agricultural Commodity Statistics,” agriculture.gov.au .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Anchors Revenue, Upholstery Gains Speed

Bed linen generated 38.02% of 2025 revenue within the Australia home textile market, solidifying its role as the category gateway for repeat household purchases. The segment benefits from high SKU refresh rates driven by seasonal color forecasts and queen-size mattress dominance, which simplifies inventory planning. Growth also stems from bundled value packs that pair sheets with pillowcases and duvet covers, elevating per-transaction revenue. Upholstery textiles, although starting from a smaller base, record a brisk 5.82% CAGR as commercial renovators specify climate-adaptive fabrics to meet updated fire and indoor-air-quality codes. Within residential settings, work-from-home arrangements fuel sofa and office-chair re-upholstering, supporting demand for durable yet tactile weaves.

In carpet and area rugs, ongoing preference for hard surfaces such as engineered timber and polished concrete tempers volume growth, yet acoustic and thermal considerations keep premium wool-blend rugs in architectural project specifications. Bath linen maintains steady momentum tied to hotel refurbishment cycles and bathroom renovation grants offered under state housing-energy-efficiency schemes. Kitchen-linen uptake stabilizes at pre-pandemic levels after the cooking surge of 2021-22, but niche items like beeswax-coated reusable food clothes emerge in zero-waste households. Overall, category diversification protects retailers from demand shocks, enabling balanced stock turnover across seasons.

By Material: Cotton Dominates, New Naturals Diversify

Cotton retained 40.78% of sales in the Australia home textile market in 2025, yet its share continues to dilute incrementally as hemp, bamboo, and linen blends capture environmentally minded consumers. Brands utilize Australian-grown cotton to meet local-content rules, often mixing it with imported long-staple varieties to elevate softness metrics. Alternative fiber adoption, growing at 5.63%, rides on consumer education campaigns that highlight breathability and lower pesticide requirements. Wool, despite heritage appeal, faces constrained supply and rising prices, spurring interest in superfine Merino-cotton hybrids that balance cost and performance. Chemical recycling breakthroughs promise to add post-consumer polyester back into cushion inserts, closing material loops without compromising loft.

Certification logos act as shorthand for quality and sustainability, with Oeko-Tex Standard 100 and GOTS labels prominently displayed on packaging and e-commerce listings. Retailers' blockchain traceability pilots that detail farm-to-finish journeys, enabling premium mark-ups. As supply chains localize, mills in Geelong and Albury trial short-run hemp-spinning lines, positioning Australia as a potential exporter of niche natural-fiber yarns. Innovation grants under the National Reconstruction Fund subsidize equipment imports, accelerating technology transfer.

By End-User: Residential Leads, Commercial Accelerates

Residential buyers accounted for 71.35% of 2025 revenue, reflecting the sheer volume of households and the replacement cadence for everyday linens. The prolonged shift to hybrid work keeps household occupancy high, heightening wear rates for bedding and upholstery and driving more frequent upgrades. Real estate turnover sparks starter-bundle purchases for first-time homeowners, capturing demand for coordinated bedroom and bathroom sets. In contrast, the commercial segment’s 5.78% CAGR is propelled by hotel reopening, healthcare bed capacity expansions, and office refurbishments that prioritize employee wellness through acoustic and antimicrobial fabrics. Bulk-order economics and long-term supply contracts underpin stable margins for suppliers serving business clients.

Hospitality chains increasingly favor linen rental services that convert capex into opex and guarantee consistent aesthetics across properties. Hospitals and aged-care facilities adopt copper-infused and silver-ion fabrics to mitigate infection risks, illustrating how functional attributes secure price premiums. Co-working operators commission customized drapery with integrated sound-dampening layers, broadening the application scope for higher-margin technical textiles. Collectively, commercial uptake diversifies revenue streams and cushions macroeconomic volatility that may affect discretionary residential spending.

By Distribution Channel: Omnichannel Retail Matures

B2C retail, encompassing department stores, specialty chains, and e-commerce, captured 65.12% of 2025 sales, while B2B direct contracts gain ground amid public-sector procurement reforms. Brick-and-mortar chains refine experiential layouts, installing digital kiosks that let shoppers visualize fabric drape on 3D room renders before placing click-and-collect orders. Specialty stores leverage loyalty programs offering birthday linens and design consultations, deepening lifetime customer value. Marketplaces add long-tail SKUs and facilitate cross-border sales into New Zealand, broadening exporter reach.

Direct-to-consumer start-ups like Bed Threads open showrooms to reduce online return rates linked to color variances and hand-feel expectations. B2B portals integrate with government e-procurement platforms, automating compliance documentation and easing vendor-registration hurdles. The dual-channel approach allows mills to segment production runs, dedicating small-batch collections to boutiques while allocating high-volume SKUs to institutional contracts. Logistics providers roll out reusable shipper totes, aligning with circular-economy mandates and cutting last-mile cardboard waste.

Geography Analysis

Greater Sydney’s affluent catchment areas, combined with its robust logistics backbone, secure New South Wales’ 23.22% leadership position. The Port Botany container terminal supports rapid import clearance for specialty fabrics destined for flagship stores, and proximity to design schools feeds a creative talent pipeline. State grants fund pilot fiber-recycling plants that convert post-consumer linens into insulation panels, reinforcing circular-economy credentials.

Victoria remains the cultural hub for textile design despite operating-cost pressures. Collaborative clusters in Collingwood fuse digital printing studios with heritage mills, shortening prototype lead times for fashion-forward duvet covers. The state’s Creative Industries Strategy earmarks USD 6.22 million (AUD 10 million) for export mentoring, enabling boutique brands to penetrate Asian luxury resort accounts.

Queensland’s population gains and climate realities underwrite its fastest-growing status. Tropical humidity drives demand for moisture-wicking sheets and mildew-resistant curtains, areas where the Australia home textile market sees higher ASPs. The Gold Coast Health and Knowledge Precinct specifies antimicrobial textiles, creating anchor orders that de-risk capacity expansions for local converters.

Western Australia’s geographic distance encourages retailers to maintain larger safety stocks, translating into sizeable forward orders that smooth factory utilization. Mining-town housing-investment subsidies stimulate purchases of durable blackout drapes that conserve interior cooling. South Australia leverages green-hydrogen availability to position itself as a low-carbon dyeing hub, appealing to brands chasing scope-3 emission cuts.

Tasmania and the ACT together punch above their population weight via tourism and government procurement, respectively. Boutique lodges along the Tasman Peninsula specify artisanal wool throws woven at Launceston’s mills, while Canberra’s departmental tenders include stringent sustainability scorecards favoring recycled-content textiles. The Northern Territory’s extreme UV index accelerates trials of UPF50+ window sheers, positioning the region as a reference site for sun-protective innovations.

Competitive Landscape

Competition in the Australia home textile market is moderate, with established domestic chains jostling against global mass merchants and digitally native newcomers. Adairs reduced SKU complexity by 12% after its Manhattan SCALE WMS rollout, unlocking USD 3.11 million (AUD 5 million) in annual savings that fund boutique-look store refurbishments. Sheridan deploys RFID tags across core bed-linen lines to tighten inventory accuracy and enable real-time click-and-collect allotment. Bed Bath Beyond leverages design collaborations with local artists, refreshing prints quarterly to avoid markdown fatigue.

Amart’s 2025 acquisition of Freedom Furniture yields purchasing power that compresses supplier lead times and enhances private-label penetration. IKEA experiments with subscription bedding that swaps seasonal colorways every six months, targeting younger renters craving novelty without large upfront spend. Pillow Talk positions as an everyday-premium alternative, offering free interior-style sessions that convert high-margin accessory sales. Smaller disruptors like Ettitude pioneer CleanBamboo lyocell sheets, securing eco-awards that drive influencer-led marketing.

Companies now routinely publish annual sustainability scorecards, highlighting metrics like water usage, energy consumption, and wage standards. These scorecards aim to enhance supply chain transparency, which has become a critical expectation in the current market. However, those without third-party verification are increasingly met with skepticism, particularly from urban millennials who prioritize accountability and ethical practices.

Australia Home Textiles Industry Leaders

Adairs

Sheridan

Bed Bath N’ Table

Pillow Talk

Linen House

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Bed Threads diversified into cotton bedding and confirmed plans for a Melbourne concept store to augment its online franchise, signaling a pivot toward omnichannel engagement.

- June 2025: Amart Furniture finalized the takeover of Freedom Furniture, forming a combined entity exceeding USD 1 billion in revenue and bolstering private-label leverage across linens and upholstery ranges.

- July 2024: Adairs completed a nationwide rollout of the Manhattan SCALE warehouse platform, achieving USD 3.11 million (AUD 5 million) annual savings and cutting order-to-ship lead time by 18%.

- March 2024: Researchers at RMIT University have pioneered a nanodiamond cooling textile technology, achieving a notable 2-3°C reduction in surface temperatures. This breakthrough positions Australia at the forefront of innovative, climate-adaptive textile solutions, tailored for extreme weather conditions.

Australia Home Textiles Market Report Scope

Home textile is a segment of technical textiles comprising components used in a domestic environment which includes upholstery, interior decoration, furnishing, carpeting, floor and wall covering, etc. The home textile consists of functional as well as decorative products used in a home with the fabric being used consisting of both natural and man-made fibre. Generally, home textiles are produced by weaving, knitting, crocheting, knotting and pressing fibres together. A complete background analysis of the Australian home textile market, including an assessment of the economy, the contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and spending by the end-user industries, are covered in the report. Australia Home Textile Market is Segmented By Product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery and Floor Covering), and By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online and Other Distribution Channels). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Local Mom and Pop Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Direct from the Manufacturers |

By Region

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Australian Capital Territory |

| Northern Territory |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Channels | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Local Mom and Pop Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Direct from the Manufacturers | ||

| By Region | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| South Australia | ||

| Tasmania | ||

| Australian Capital Territory | ||

| Northern Territory | ||

Key Questions Answered in the Report

What is the expected value of the Australia home textile market by 2031?

It is forecast to reach USD 3.11 billion, reflecting a 5.62% CAGR over 2026-2031.

Which product category currently generates the most revenue?

Bed linen leads with a 38.02% share of 2025 sales.

Which Australian state is projected to grow fastest through 2031?

Queensland, supported by population inflows and tourism recovery, is set for a 6.45% CAGR.

How are circular-economy policies affecting suppliers?

Extended-producer-responsibility rules push brands to fund take-back programs and invest in recycling technologies, raising compliance costs but encouraging higher-quality materials.

Which distribution channel shows the highest growth outlook?

B2B direct contracts, helped by local-content procurement mandates, are projected to grow at 5.66% annually.

What technological innovation is differentiating premium bedding lines?

Nanodiamond-coated fabrics developed by RMIT lower surface temperatures by up to 3 °C, appealing to consumers in hot climates.

Page last updated on: