Anhydrous Milk Fat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

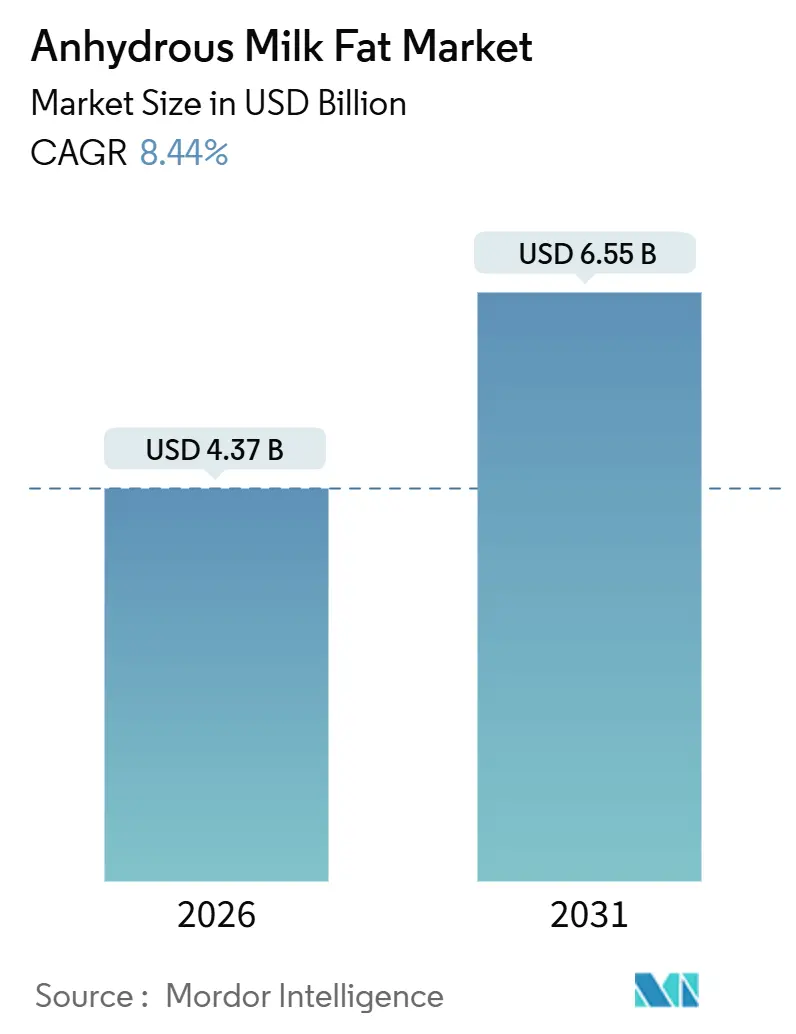

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 6.55 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

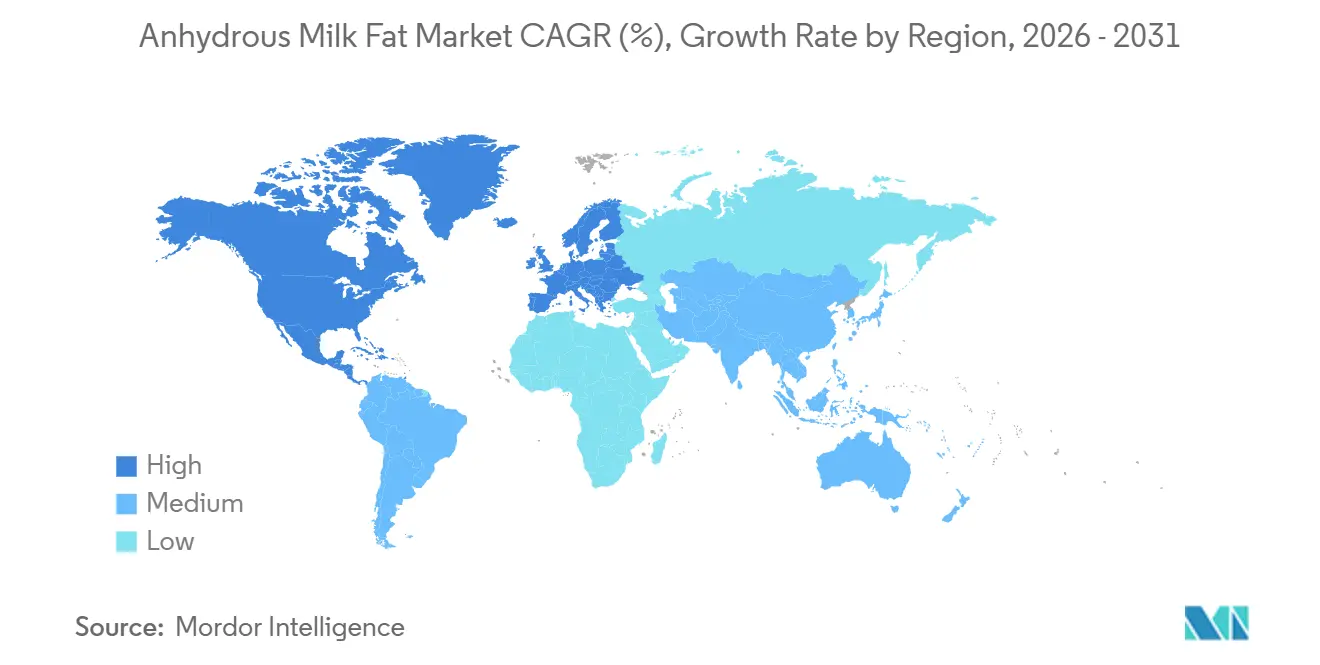

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Anhydrous Milk Fat Market Analysis by Mordor Intelligence

The anhydrous milk fat market size is USD 4.37 billion in 2026 and is forecast to reach USD 6.55 billion by 2031, translating into an 8.44% CAGR over the period. Rapid uptake in premium food manufacturing, a pivot toward infant nutrition ingredients, and steady investments in continuous‐flow processing technologies that deliver 99.8% purity underpin this expansion. Shelf stability, concentrated fat content, and clean-label positioning allow processors to secure long-term contracts with bakery, confectionery, and dairy majors that require uniform texture and flavor profiles. For instance, according to the International Food Information Council, in 2024, approximately 25% of respondents in the United States defined a "healthy food" as one with "limited or no artificial ingredients or preservatives," a key component of the "clean" label trend.[1]Source: International Food Information Council, "2024 Food and Health Survey", www.ific.org. Improved throughput from AI-enabled separators has reduced unit costs, encouraging multinational cooperatives to scale production capacity while maintaining stringent quality standards. At the same time, raw milk price volatility has intensified margin pressures, prompting vertical integration strategies that mitigate supply shocks. Geographic growth differentials remain pronounced: North America retains leadership, but Asia-Pacific is emerging as the principal volume driver on the back of rising middle-class demand for premium dairy ingredients.

Key Report Takeaways

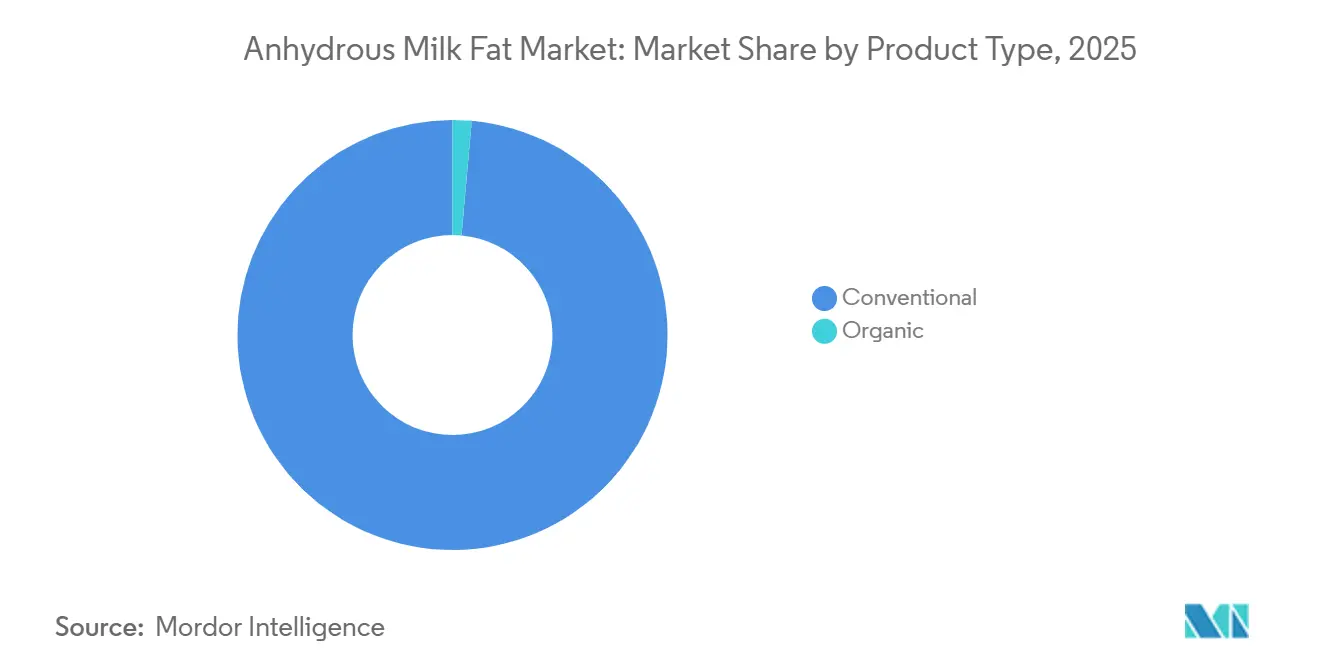

- By product type, conventional AMF led with a 98.58% anhydrous milk fat market share in 2025 and registered the highest projected CAGR at 8.48% through 2031.

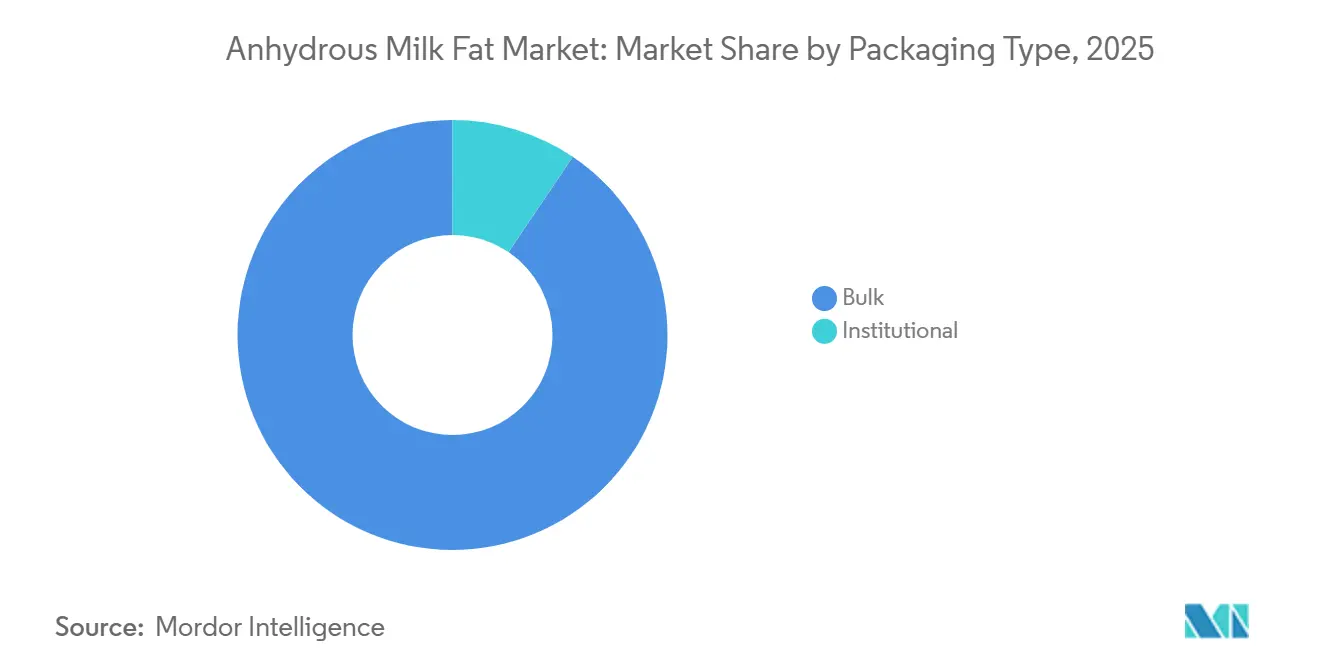

- By packaging type, bulk packaging held 90.55% share of the anhydrous milk fat market size in 2025, while the institutional packaging types are forecast to expand at an 8.97% CAGR through 2031.

- By end user, industrial food manufacturers commanded 91.94% of the anhydrous milk fat market share in 2025, while foodservice is projected to grow at a 10.7% CAGR to 2031.

- By geography, Europe accounted for 35.4% revenue share in 2024, whereas Asia-Pacific is on course for the fastest 10.58% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anhydrous Milk Fat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Trend of Consuming Dairy-Based Diets | +1.2% | Global, with the strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Rise in Fast-Food Chains and Restaurants | +1.0% | Global, concentrated in urban centers across all regions | Short term (≤ 2 years) |

| Increased Application in Infant Nutrition and Premium Food Products | +1.5% | North America and Europe regulatory approval, Asia-Pacific demand growth | Long term (≥ 4 years) |

| Technological Advancements in AMF Processing | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increasing Use in Recombined Dairy Products | +0.7% | Asia-Pacific core, spill-over to the Middle East and Africa, and South America | Medium term (2-4 years) |

| Preference for Organic and Health-Conscious Products | +0.9% | North America and Europe premium segments, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Trend of Consuming Dairy-Based Diets

Consumer preferences are shifting toward whole dairy products, with butter consumption increasing 43% over 25 years in the US market, directly benefiting AMF applications in premium food. According to the USDA Foreign Agricultural Service, in 2024, the total domestic consumption volume of butter was 6.9 million metric tons in India. This was an increase as compared to the previous year, when the consumption volume was 6.72 million metric tons. This trend extends beyond traditional dairy consumption as food manufacturers recognize AMF's superior functionality in creating rich, creamy textures that meet evolving consumer expectations for indulgent experiences. The Dairy Council of California reports increasing acceptance of whole dairy foods, with dairy farmers adapting by crossbreeding cows to enhance butterfat production, creating upstream supply advantages for AMF processors Dairy Council of California. European-style butter with 83% butterfat content is gaining market share, indicating consumer willingness to pay premiums for higher fat content products. Regulatory support through initiatives like the Whole Milk for Healthy Kids Act further validates this dietary shift, potentially expanding AMF applications in institutional foodservice. This convergence of consumer preference and regulatory backing suggests sustained demand growth across multiple AMF application segments.

Rise in Fast-Food Chains and Restaurants

The foodservice sector's expansion creates concentrated demand for AMF as restaurants prioritize ingredient consistency and shelf stability in high-volume operations. Fast-food chains increasingly specify AMF over traditional butter for applications requiring extended holding times without refrigeration, driving industrial-scale procurement patterns that favor large-scale AMF producers. Restaurant operators value AMF's standardized fat content and reduced water activity, which minimizes spoilage risks in commercial kitchen environments. Global expansion of Western-style fast-food concepts in emerging markets multiplies this demand pattern, particularly in the Asia-Pacific, where local food manufacturers adapt traditional recipes to incorporate AMF for improved texture and shelf life. Moreover, an increasing number of foodservice establishments is further supporting the market's growth. For instance, according to the National Institute of Statistics and Geography, in 2024, there were more than 640 thousand restaurant establishments in Mexico[2]Source: National Institute of Statistics and Geography, "Number of restaurants and similar establishments in Mexico", www.inegi.org.mx.

Increased Application in Infant Nutrition and Premium Food Products

Regulatory approvals are expanding AMF's addressable market in infant nutrition, with the FDA's GRAS determination enabling usage up to 7.0% by weight in calorically dense formulas. This regulatory milestone addresses manufacturers' need for fat sources that closely mimic human milk composition while meeting stringent safety requirements for infant consumption. Premium food manufacturers increasingly specify AMF for applications requiring clean label ingredients, as its single-ingredient profile aligns with consumer demands for transparency. The ingredient's 99.8% milk fat purity and minimal processing requirements support premium positioning strategies across multiple food categories. Infant formula manufacturers particularly value AMF's consistent fatty acid profile, which supports product standardization across global markets while meeting diverse regulatory requirements. The convergence of regulatory approval and clean label trends creates sustainable competitive advantages for AMF suppliers who can demonstrate consistent quality and traceability throughout their supply chains.

Technological Advancements in AMF Processing

Continuous flow processing systems are revolutionizing AMF production efficiency, with artificial intelligence applications demonstrating 20-40% productivity improvements in dairy processing operations. These technological advances enable processors to achieve higher purity levels while reducing energy consumption and processing time, creating cost advantages that can be passed through to food manufacturers. Advanced separation technologies allow for precise control of fatty acid composition, enabling customized AMF products for specific applications such as chocolate manufacturing or ice cream production. Quality control improvements through automated monitoring systems reduce batch-to-batch variation, addressing food manufacturers' requirements for consistent ingredient performance. The integration of predictive maintenance systems minimizes production disruptions, critical for maintaining supply chain reliability in time-sensitive food manufacturing operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility and Supply Chain Dependency on Raw Milk | -1.8% | Global, with the highest impact in regions with concentrated dairy production | Short term (≤ 2 years) |

| Competition from Alternative Fats and Oils | -1.1% | Global, with the strongest pressure in cost-sensitive applications | Medium term (2-4 years) |

| Stringent Regulations and Labeling Requirements | -0.6% | North America and Europe primary impact, spreading to other regions | Long term (≥ 4 years) |

| Shelf Life and Storage Sensitivity Compared to Alternatives | -0.4% | Global, particularly affecting smaller processors and distributors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Fats and Oils

Plant-based fat alternatives present cost and functionality challenges to AMF adoption, particularly in price-sensitive applications where performance requirements allow substitution. Coconut oil and palm oil derivatives offer similar melting characteristics at significantly lower costs, creating pressure on AMF pricing in industrial applications. The development of structured lipids and fat blends enables food manufacturers to achieve desired functionality while reducing ingredient costs, particularly in applications where AMF's unique flavor profile is not essential. Regulatory pressures around sustainability and environmental impact favor plant-based alternatives in certain market segments, as consumers increasingly scrutinize the carbon footprint of animal-derived ingredients. Technical advances in fat modification technologies enable alternative oils to more closely replicate AMF's performance characteristics, reducing the functional advantages that traditionally protected AMF's market share.

Price Volatility and Supply Chain Dependency on Raw Milk

Raw milk price fluctuations create significant margin pressures for AMF processors, with mailbox prices averaging USD 19.98 per cwt in March 2024, representing a USD 0.35 monthly increase that directly impacts production costs, according to the United States Department of Agriculture[3]Source: United States Department of Agriculture, "USDA Mailbox Milk Price Report - March 2024, usda.gov. Supply chain disruptions from disease outbreaks, exemplified by Highly Pathogenic Avian Influenza affecting dairy cattle, compound these pricing pressures by reducing available milk volumes for processing. The concentrated nature of dairy production in specific geographic regions creates vulnerability to weather-related disruptions, as demonstrated by Australia's production challenges affecting global milk fat availability. Processors face particular challenges during periods of tight milk supply when dairy farmers prioritize higher-value applications, potentially limiting AMF production capacity. The Federal Milk Marketing Order reforms introduce additional complexity as pricing mechanisms adjust to reflect modern dairy production realities, creating uncertainty for long-term supply contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conventional Dominance and Growth

Conventional anhydrous milk fat (AMF) accounts for the largest share (98.58%) in 2025 and remains the fastest-growing segment (8.48% CAGR, 2026-2031) in the global AMF market due to its alignment with the scale, economics, and regulatory realities of industrial food manufacturing. Conventional AMF benefits from established dairy supply chains, year-round milk availability, and standardized processing systems that enable high yields and consistent quality at lower costs, critical for bakery, confectionery, infant nutrition, and ready-to-eat food producers. Government and industry bodies such as the Food and Agriculture Organization (FAO) and the International Dairy Federation (IDF) highlight conventional dairy fats as essential for global food security due to their functional stability, long shelf life, and efficient conversion of raw milk into value-added ingredients. Supportive dairy policies, such as the EU’s Common Agricultural Policy, USDA dairy margin programs, and India’s National Dairy Development Board (NDDB) initiatives, favor conventional milk fat production by improving farm productivity, cold-chain infrastructure, and export readiness.

From a growth perspective, conventional AMF is expanding rapidly as demand for cost-effective butterfat rises in emerging markets, where price sensitivity outweighs organic certification preferences, and in industrial applications where clean-label claims can be met without organic status. Recent developments reinforce this momentum: in 2024, several large cooperatives and processors expanded conventional AMF output for bakery and confectionery use, including new bulk AMF formats and improved oxidative-stability variants for industrial users; in 2025, manufacturers launched application-specific conventional AMF products, such as high-melting-point AMF for tropical climates and reformulated AMF for infant formula and chocolate coatings, leveraging scale efficiencies rather than certification premiums. Strong policy support, mature infrastructure, lower production costs, and continuous product optimization explain why conventional AMF dominates market share and grows faster than organic alternatives globally.

By Packaging Type: Bulk Packaging Holds a Major Share

Bulk packaging holds the largest share (90.55%) in 2025 of the global anhydrous milk fat (AMF) market because the product is principally an industrial ingredient and is therefore optimized for cost-efficient, high-volume supply chains: food manufacturers, confectioners, bakeries, infant-formula producers, and exporters prefer large drums, totes, and tanker deliveries that reduce per-kilogram packaging cost, simplify cold-chain and bulk handling, and match continuous-processing lines, a reality reflected in official commodity reporting that shows tightness and active trading of bulk butter/AMF loads for international buyers. Government and multilateral outlooks (OECD-FAO, FAO) and trade bodies (IDF) also emphasize that trade, storage efficiency, and standardized commodity specifications make concentrated fats like AMF attractive to large processors and traders, reinforcing the dominance of bulk formats in global volumes. Practically, regulators and industry standards bodies made packaging and specification work easier in 2024 (for example, the ADPI AMF standard and updated industry ingredient standards), which lowered friction for selling and buying AMF in industrial bulk formats and supported steady exports and mill-scale supply.

At the same time, institutional packaging (smaller bulk packs, portioned tubs and foodservice formats) is the fastest-growing segment (8.97% CAGR, 2026-2031) because demand from the foodservice, catering, hospitality and quick-service restaurant channels has rebounded and modernized: chains and commissaries increasingly specify portioned, ready-use AMF formats that reduce on-site handling, improve food-safety consistency, and fit high-throughput kitchens, trends flagged by industry trade reports that link growth in fast-food, restaurants and institutional procurement to rising ingredient volumes and packaging innovation. National dairy-sector programs that expanded processing capacity and foodservice supply in 2024–25 (for example, expanded processor output noted in company investor reports and national dairy outlooks) further accelerated demand for institutionally packaged AMF tailored to chefs and OEM food manufacturers.

By End User: Industrial Dominance, Foodservice Acceleration

Food manufacturers and industrial processors account for the largest share of the global anhydrous milk fat (AMF) market (91.94%) in 2025 due to AMF's high purity, functional performance (texture, melting profile, shelf stability), and standardized specifications. These qualities make it ideal for large-scale bakery, confectionery, chocolate, infant formula, and dairy ingredient manufacturers requiring predictable, commodity-grade fats. International standards (Codex/FAO guidance) and industry specifications reinforce AMF's role as a traded, spec-driven input. Multilateral bodies like the International Dairy Federation highlight processed dairy ingredients' importance in global trade and sustainability. For example, New Zealand FAS reports rising AMF shipments and specialty dairy exports, driven by national dairy programs and trade facilitation, which support industrial demand.

The foodservice segment is the fastest-growing (10.7% CAGR, 2026-2031) due to recovery and expansion in restaurants, quick-service chains, commissary kitchens, and institutional catering. This growth drives demand for ready-to-use, portioned, and application-specific AMF products (e.g., chef-friendly tubs, higher-melt grades for hot kitchens, and smaller commercial packs). In 2024–25, suppliers expanded application-specific AMF portfolios for industrial users (e.g., fractionated AMF for tropical confectionery) and launched foodservice-friendly formats to meet evolving needs. Entrenched standards, large-scale processing economics, and national programs explain food manufacturers' dominance, while changing foodservice procurement practices and recent product launches drive foodservice growth.

Geography Analysis

Europe accounts for the largest share of the global anhydrous milk fat (AMF) market (35.40%) in 2025 because it combines very large and stable raw-milk supplies, mature processing and fractionation capacity, tight integration with major food manufacturers and exporters, and supportive regulatory and standards frameworks that make bulk, spec-driven AMF trade efficient. The European Dairy Association and Eurostat data show sustained milk deliveries and well-established ingredient value chains that feed industrial AMF production. Concrete, recent instances underline these dynamics: in 2024, European processors and trade platforms continued to underpin large AMF volumes for industrial buyers while producers such as Fonterra reaffirmed AMF as a reference commodity in their 2024 business updates, reflecting stable supply channels and ingredient portfolio focus.

By contrast, Asia-Pacific is the fastest-growing region (10.58% CAGR, 2026-2031) driven by accelerating demand for processed foods, infant nutrition, bakery, and confectionery in populous markets (notably China, India, and Southeast Asia), rising disposable incomes and urbanization, and expanding local processing capacity. This pattern is noted in milk-fat/fractions market analyses and the OECD–FAO outlook, which highlight higher butter and fat price dynamics in 2024 that widened the value of concentrated dairy fats and encouraged regional investment. In 2025, industry platform and supplier actions, such as Global Dairy Trade expanding AMF offerings in bulk tote/box formats and ingredient suppliers launching milk-fat-derived specialty ingredients and approvals for milk-fat globule-membrane (MFGM) components used in infant nutrition, illustrate Asia-Pacific’s rapid uptake of new, application-specific AMF products.

North America sits on a steady growth curve because of strong downstream demand for specialty dairy ingredients (infant formula, premium bakery, chocolate), ongoing innovation and export momentum (US dairy exports rose in 2024–25), and processors’ investments in application-specific AMF grades and flexible packaging that serve both domestic food manufacturers and international buyers. Taken together, strong European production and trade infrastructure explain its dominant share, while demographic and demand shifts plus targeted product and platform developments in 2024–25 explain why Asia-Pacific is the fastest-growing region and why North America is steadily expanding its AMF footprint.

Competitive Landscape

The global anhydrous milk fat (AMF) market is fragmented, characterized by the presence of a mix of large multinational dairy cooperatives, regional ingredient specialists, and country-specific exporters that compete across price, functionality, certifications, and end-use focus rather than being dominated by a single or a few players. Companies such as Fonterra Co-operative Group Limited, FrieslandCampina, Dairy Farmers of America, Inc., Lactalis Ingredients, and Yili Group (through Westland Milk Products) are key participants, but none exercises overwhelming control due to the geographically dispersed milk supply base, differing regional regulations, and varied application requirements for AMF. Government and association sources such as FAO, OECD-FAO, IDF, and national dairy boards consistently describe milk fat markets as commodity-linked but regionally differentiated, with AMF traded alongside butter and butteroil and produced by a wide array of cooperatives and private processors across Europe, Oceania, North America, and parts of Asia.

In 2024, heightened butterfat prices and supply volatility encouraged both large and mid-sized processors to channel milk fat into AMF, leading to multiple parallel capacity expansions and product introductions rather than consolidation. Major players expanded application-specific AMF grades, while smaller and regional suppliers launched standard industrial AMF for bakery and confectionery customers. In 2025, competition further diversified as leading groups such as Fonterra, FrieslandCampina, and Lactalis Ingredients focused on value-added AMF variants (fractionated, high-melting, infant-nutrition compliant), while DFA strengthened North American industrial supply and Yili/Westland aligned Oceania production with fast-growing Asia-Pacific demand.

At the same time, regional players across Europe, India, and Southeast Asia continued supplying conventional AMF for domestic food manufacturers and foodservice users, reinforcing fragmentation. Overall, the AMF market remains structurally fragmented, with competition driven by milk availability, export orientation, functional customization, and compliance with Codex, ADPI, and regional standards rather than scale alone. This dynamic allows both global cooperatives and regional processors to coexist and grow.

Anhydrous Milk Fat Industry Leaders

-

Fonterra Co-operative Group Ltd

-

FrieslandCampina N.V.

-

Dairy Farmers of America Inc.

-

Lactalis Ingredients

-

Yili Industrial Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Fonterra announced a significant expansion of its production capacity for anhydrous milk fat to meet rising global demand, especially in the food processing and confectionery industries. A key part of this investment is a new cool store at the Whareroa site in Taranaki, New Zealand, covering about 19,000 m² (the size of three rugby fields), to increase storage capacity by around 5,000 tonnes.

- November 2024: Glanbia Ingredients launched a new line of anhydrous milk fat products designed specifically for the bread and confectionery industries. These products focus on enhancing flavor, texture, and shelf life, particularly in baked goods and chocolate products, boosting the sensory quality and freshness of premium food items.

- October 2024: Arla Foods introduced an organic variety of anhydrous milk fat to respond to growing consumer demand for organic, natural, and sustainably sourced dairy products. This product caters to both food manufacturing and retail sectors, emphasizing clean-label positioning and aligning with the larger trend of rising organic food consumption. This launch strengthens Arla’s portfolio in premium and specialty dairy fats.

- January 2024: Dairy Farmers of America invested in upgrading its production facilities to better meet the increasing demand for anhydrous milk fat. The focus has been on vertical integration and local sourcing to improve supply chain control and product quality. This investment enhances the cooperative's ability to supply consistent, high-grade AMF to meet premium market needs.

Global Anhydrous Milk Fat Market Report Scope

| Conventional |

| Organic |

| Bulk (Drums and Tanks) |

| Institutional (Intermediate Bulk Containers) |

| Food Manufacturers/Industrial | Dairy |

| Bakery | |

| Confectionery | |

| Beverages | |

| Other Industrial Applications | |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Conventional | |

| Organic | ||

| Packaging Type | Bulk (Drums and Tanks) | |

| Institutional (Intermediate Bulk Containers) | ||

| End User | Food Manufacturers/Industrial | Dairy |

| Bakery | ||

| Confectionery | ||

| Beverages | ||

| Other Industrial Applications | ||

| Foodservice | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the anhydrous milk fat market in 2026?

The anhydrous milk fat market size stands at USD 4.37 billion in 2026 and is projected to grow at a 8.4% CAGR to USD 6.55 billion by 2031.

Which packaging type is growing the fastest in the anhydrous milk fat market?

Institutional packaging type is expanding at an 8.79% CAGR.

What is the main restraint impacting anhydrous milk fat processors?

Volatile raw milk prices, averaging USD 19.98 per cwt in March 2024, compress processor margins and complicate long-term supply contracts.

Which region is expected to contribute most to future anhydrous milk fat volume growth?

Asia-Pacific is forecast to post the highest 10.58% CAGR as rising middle-class consumption and urbanization fuel demand for premium dairy ingredients.

How concentrated is the competitive landscape?

The anhydrous milk fat market is fragmented.

Page last updated on: