Edible Animal Fat Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

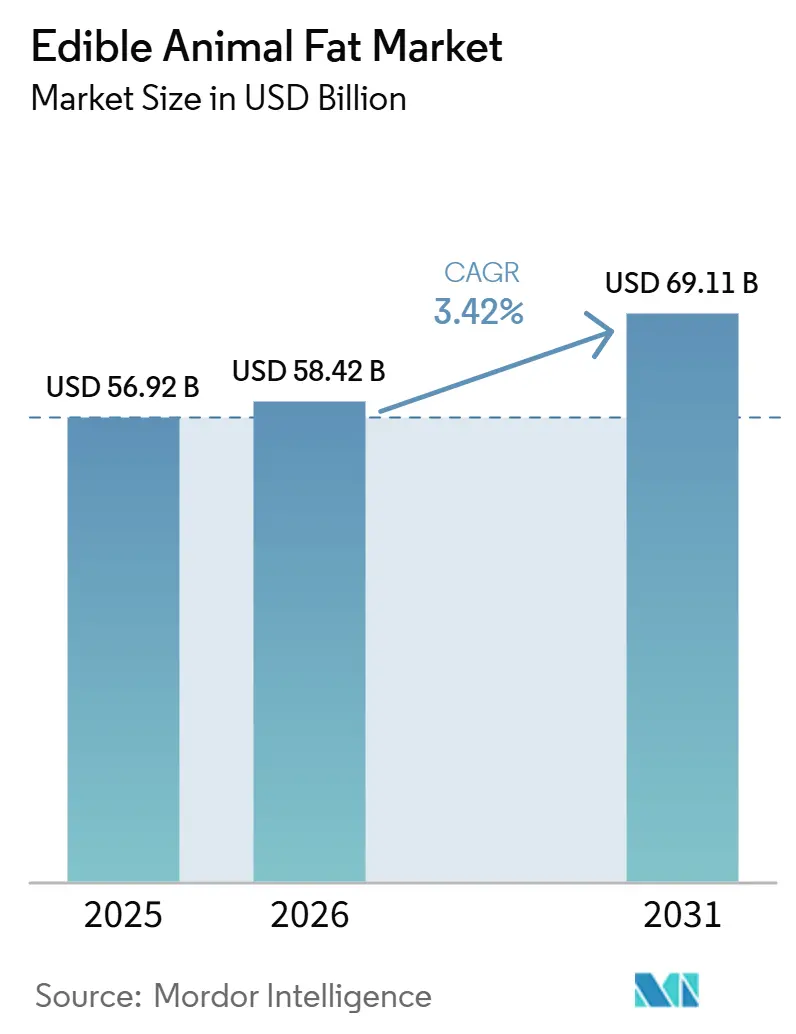

| Market Size (2026) | USD 58.42 Billion |

| Market Size (2030) | USD 69.11 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edible Animal Fat Market Analysis by Mordor Intelligence

The edible animal fat market size is expected to grow from USD 56.92 billion in 2025 to USD 58.42 billion in 2026 and is forecast to reach USD 69.11 billion by 2031 at 3.42% CAGR over 2026-2031. The market is being supported by the return of rendered fats to commercial kitchens, stronger food processing demand across Asia, and a wider shift toward simpler ingredient labels in packaged foods. Regulatory acceptance has also improved the tone of demand in the current year, especially as beef tallow and butter have regained attention in retail and foodservice channels. At the same time, the edible animal fat market still faces substitution pressure from vegetable oils and continued concern around saturated fat intake in health-aware consumer groups. Supply economics are also becoming more complex because large renderers are balancing food demand with renewable fuel demand, which can tighten availability for food-grade buyers.

Key Report Takeaways

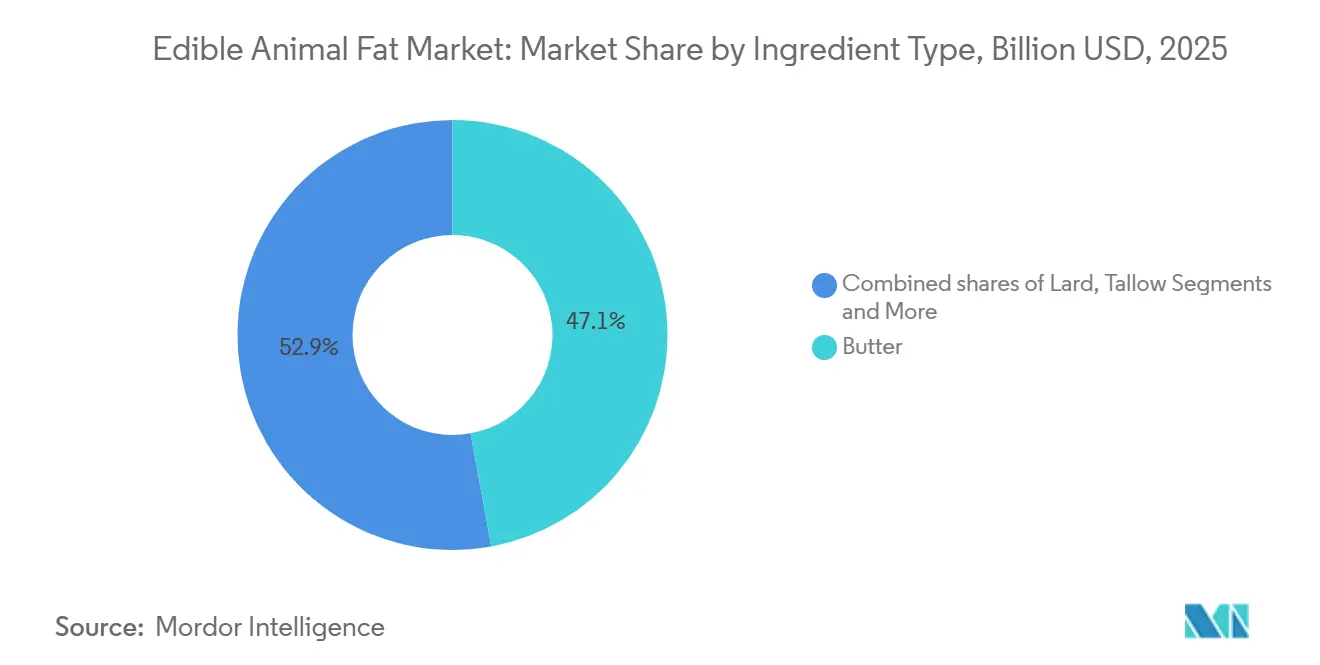

- By ingredient type, butter led with 47.11% revenue share in 2025, while lard is projected to grow at a 4.93% CAGR through 2031.

- By form, solid and paste held 63.21% share in 2025, while liquid is forecast to advance at a 4.71% CAGR through 2031.

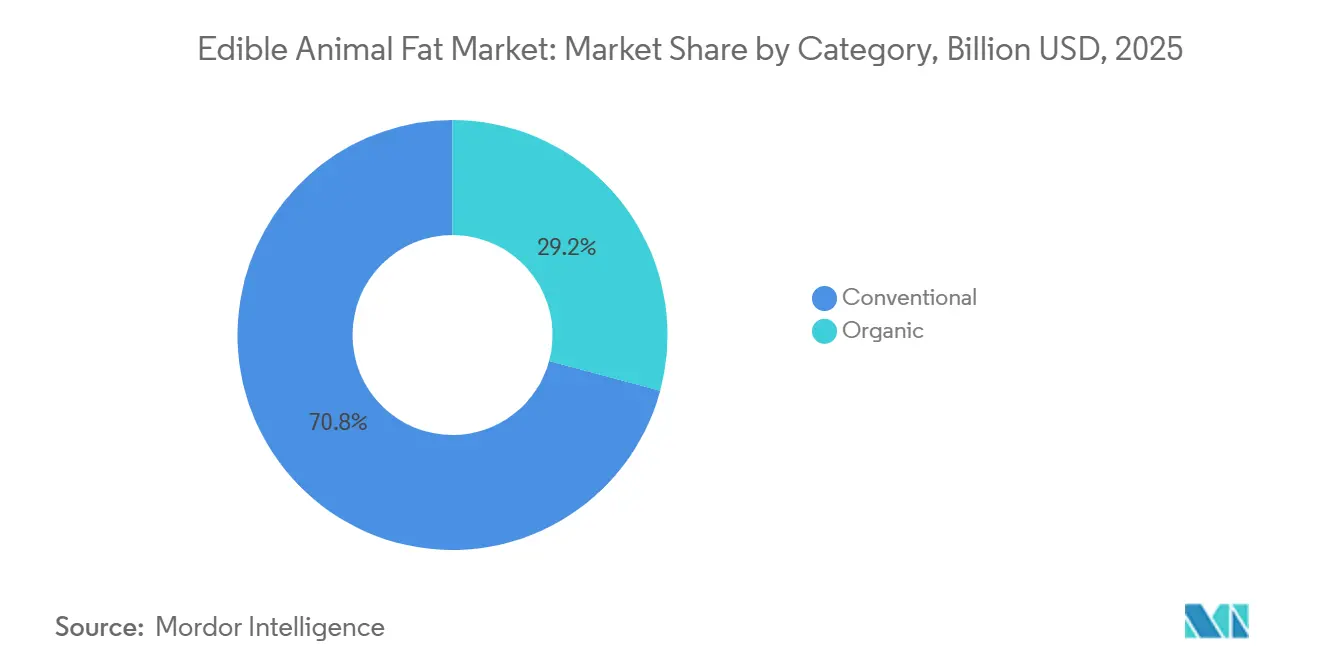

- By category, conventional accounted for 70.82% share in 2025, while organic is projected to expand at a 6.33% CAGR through 2031.

- By end-user, the food processing industry held 83.12% share in 2025, while retail is expected to grow at a 5.88% CAGR through 2031.

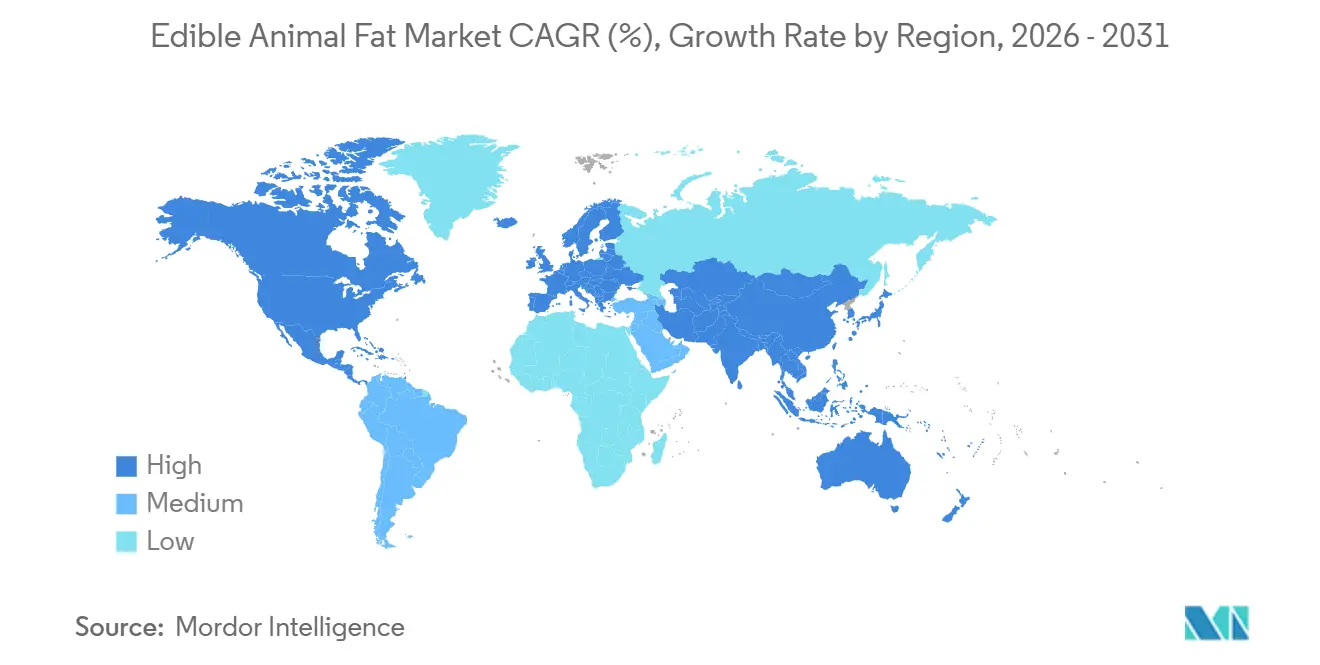

- By geography, Asia-Pacific captured 40.22% share in 2025 and is also projected to record the highest regional CAGR at 5.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Edible Animal Fat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional superiority in bakery and pastry applications | +0.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Rising demand for clean-label fats in reformulation projects | +0.7% | North America, Europe, parts of Asia-Pacific | Medium term (2-4 years) |

| Zero-waste rendering and byproduct valorization | +0.5% | Global | Long term (≥ 4 years) |

| Expanding foodservice use of high-heat stable fats | +0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Premiumization of heritage and traditional food positioning | +0.3% | North America, Europe, Asia-Pacific premium segments | Medium term (2-4 years) |

| Tightening traceability requirements favors rendered animal fats over blends | +0.3% | Europe, China, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Functional superiority in bakery and pastry applications

The widespread use of edible animal fats in bakery and pastry products is supporting market growth due to their superior performance in enhancing texture, flavor, and product quality. Ingredients such as butter, lard, and tallow provide excellent plasticity, creating flaky layers in pastries, tender crumbs in cakes, and improved mouthfeel in baked goods. Lard, in particular, is valued for producing crisp pie crusts and laminated doughs, while butter remains a preferred ingredient in premium breads, cookies, croissants, and confectionery products because of its rich flavor and aroma. Food manufacturers and artisan bakeries continue to rely on animal fats to achieve consistent product quality and processing efficiency. The growing consumer preference for premium baked goods and authentic recipes has further increased demand for traditional fat ingredients.

Rising demand for clean-label fats in reformulation projects

The increasing focus on clean-label food products is encouraging manufacturers to reformulate recipes using recognizable and minimally processed ingredients, creating greater demand for edible animal fats. Traditional fats such as butter, lard, and tallow are increasingly being incorporated into reformulation projects as alternatives to artificial additives and highly processed fat ingredients. This shift is supported by changing consumer preferences for products with shorter and more transparent ingredient lists. For instance, the American Baking Association's November 2025 pledge to remove certified FD&C colors from baked goods reflects the broader industry movement toward cleaner formulations[1]Source: Food Business News, “New regulations may accelerate shift to clean label”, foodbusinessnews.net. Furthermore, according to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to account for more than 70% of product portfolios during 2025 and 2026, up from 52% in 2021[2]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities”, cbi.eu. As food manufacturers expand clean-label initiatives across bakery, processed foods, and dairy applications, the use of naturally derived edible animal fats is expected to increase.

Zero-waste rendering and byproduct valorization

Growing emphasis on zero-waste manufacturing and resource efficiency is increasing the utilization of edible animal fats through advanced rendering and byproduct valorization practices. Meat processors and rendering companies are maximizing the value of animal byproducts by converting fat trimmings and other edible tissues into high-quality food ingredients instead of discarding them as waste. This approach improves raw material utilization, reduces environmental impact, and supports circular economy initiatives within the food industry. Advancements in rendering technologies have further enhanced the quality, safety, and consistency of edible animal fats, making them suitable for a wide range of food applications. Manufacturers are also investing in efficient recovery and purification processes to increase production yields while meeting stringent food safety standards.

Expanding foodservice use of high-heat stable fats

The increasing demand for high-heat stable cooking fats across the foodservice industry is contributing to the growing adoption of edible animal fats. Products such as tallow, lard, and duck fat are widely used by restaurants, quick-service restaurants (QSRs), hotels, and catering establishments because they offer excellent thermal stability and maintain their performance during repeated frying and high-temperature cooking. These fats also enhance the flavor, texture, and crispness of fried foods, roasted meats, and specialty dishes, making them a preferred choice for many foodservice operators. The expansion of the global foodservice sector and rising consumer demand for premium dining experiences are further increasing their commercial use. In addition, the growing popularity of traditional cooking methods and authentic regional cuisines has renewed interest in animal-based cooking fats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated fat and cholesterol perception remains a demand ceiling | -0.7% | North America and Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Substitution pressure from vegetable oils and interesterified fats | -0.8% | Global | Medium term (2-4 years) |

| Volatile livestock and rendering input supply | -0.5% | Global, concentrated in Asia-Pacific and South America | Short term (≤ 2 years) |

| Formulation constraints from odor and flavor drift | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturated fat and cholesterol perception remains a demand ceiling

Consumer concerns regarding the health effects of saturated fat and cholesterol continue to limit the widespread adoption of edible animal fats. Growing awareness of cardiovascular health and lifestyle-related diseases has encouraged many consumers to reduce the consumption of foods perceived to be high in saturated fats. As a result, food manufacturers are increasingly reformulating products with vegetable oils and other alternatives that are often viewed as healthier options. Public health recommendations and nutritional guidelines in many countries also advocate moderation in the intake of saturated fats, influencing purchasing decisions. This perception has particularly affected demand among health-conscious consumers seeking low-fat or heart-friendly food products. In addition, negative consumer attitudes toward animal-based fats create challenges for manufacturers attempting to expand their presence in wellness-focused food categories.

Substitution pressure from vegetable oils and interesterified fats

The increasing availability of vegetable oils and interesterified fats is creating significant competitive pressure on the edible animal fat market. Food manufacturers are increasingly adopting alternatives such as sunflower, canola, soybean, and palm oils because they are widely available, cost-effective, and are often perceived as healthier by consumers. Interesterified fats are also gaining traction as they provide desired texture, stability, and functionality in bakery, confectionery, and processed food applications without relying on animal-derived ingredients. In addition, these alternatives can be tailored to meet specific processing requirements while supporting clean-label, vegan, and cholesterol-conscious product positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Butter’s Premium Hold Masks Lard’s Industrial Surge

Butter accounted for 47.11% of the edible animal fat market revenue in 2025, making it the largest ingredient type due to its widespread use across food processing and foodservice applications. Its dominant position is supported by strong demand from the bakery, confectionery, dairy, and ready-to-eat food industries, where it enhances flavor, texture, and product quality. Butter is also widely preferred by consumers for its natural taste and clean-label appeal compared to synthetic or highly processed fat alternatives. Growing consumption of premium baked goods, pastries, desserts, and gourmet dairy products continues to reinforce its market leadership.

Lard is projected to register the fastest CAGR of 4.93% through 2031, driven by its expanding use in food manufacturing and specialty culinary applications. Increasing consumer interest in traditional cooking methods and authentic regional cuisines is contributing to renewed demand for lard in bakery, meat processing, and frying applications. Food manufacturers are also utilizing lard to improve texture, flakiness, and flavor in products such as pastries, pies, biscuits, and processed meat items. The growing popularity of ketogenic, paleo, and high-fat dietary patterns in several markets has further encouraged the use of animal-based fats, including lard.

By Form: Solid/Paste Formats Lead Processing Applications

The solid/paste segment's dual achievement of 63.21% market share in 2025 and 4.93% CAGR leadership through 2031 underscores the food industry's continued reliance on structured fats for texture and functionality. This format’s dominance reflected core food science principles, as solid fats provided essential structural properties in baked goods, confectionery, and processed meats that liquid alternatives could not replicate. Manufacturers increasingly required fats that remained stable across temperature variations and storage conditions, supporting demand for solid/paste formats with predictable performance characteristics.

Liquid animal fats served specialized applications in frying operations, biodiesel production, and industrial processes where flowability and heat transfer properties took priority over structural functionality. Technological advances in fat recovery and purification across the rendering industry improved liquid fat quality and expanded application opportunities in renewable fuel production. In February 2025, Coast Packing’s new USD 60 million facility in Amarillo, Texas, was expected to target increased production of animal fat shortenings for both home and commercial channels, indicating sustained demand for solid formats. Form segmentation increasingly reflected end-use optimization, with manufacturers selecting formats based on specific functional requirements rather than traditional preferences.

By Category: Conventional Dominates, Organic Commands the Margin Premium

The conventional category accounted for 70.82% of the edible animal fat market revenue in 2025, making it the dominant segment by category. Its leadership is primarily driven by widespread availability, cost-effectiveness, and established supply chains across global markets. Conventional edible animal fats are extensively used by food manufacturers, restaurants, and foodservice operators due to their consistent quality and competitive pricing. They also remain a preferred choice for large-scale production of processed foods, baked goods, meat products, and frying applications where affordability and functionality are critical.

The organic category is projected to expand at the fastest CAGR of 6.33% through 2031, supported by rising consumer preference for natural and sustainably produced food ingredients. The Organic Trade Association reported that United States organic food and product sales reached a record USD 76.6 billion in 2025 and grew 6.8% year over year, with younger consumers forming the fastest-growing buyer group[3]Source: Organic Trade Association, “Organic Market Overview”, ota.com. Increasing awareness of food quality, animal welfare, and environmentally responsible farming practices is encouraging consumers to choose organically sourced animal fats. Food manufacturers are responding by incorporating organic ingredients into premium bakery products, dairy products, processed foods, and specialty culinary applications to meet evolving consumer expectations.

By End-User: Food Industry Anchors Volumes, Retail Accelerates

The food processing industry accounted for 83.12% of the edible animal fat market revenue in 2025, making it the largest end-user segment. Its dominant position is driven by the extensive use of edible animal fats as key ingredients in processed meat products, bakery items, confectionery, dairy products, snacks, and ready-to-eat meals. Food manufacturers rely on animal fats for their ability to enhance flavor, texture, mouthfeel, and cooking performance while also improving product consistency and shelf life. The continued expansion of the global processed food industry, supported by rising urbanization and demand for convenience foods, has further strengthened consumption within this segment.

The retail segment is projected to expand at the fastest CAGR of 5.88% through 2031, driven by increasing consumer demand for cooking fats for household use. Growing interest in traditional cooking practices, home baking, and authentic recipes is encouraging consumers to purchase products such as lard, tallow, and clarified animal fats through retail channels. Rising awareness of minimally processed and natural food ingredients has also contributed to greater acceptance of edible animal fats among health-conscious consumers following high-fat and low-carbohydrate diets.

Geography Analysis

Asia-Pacific accounted for 40.22% of the animal edible fat market share in 2025 and is projected to register a CAGR of 5.67% through 2031, giving it the largest base and the fastest regional expansion. Heavy use of pork and other animal fats in Chinese, Southeast Asian, and Japanese cooking and food manufacturing supports the animal edible fat market in the region. Japan is expected to show the tightest supply conditions, with wholesale lard prices reaching JPY 5,765 per 15 kg can, or USD 38 per 15 kg, in early 2025 as raw material shortages continue at rendering facilities. India adds another growth avenue as its bakery and premium packaged food sectors expand amid improving income levels. In Hong Kong, chefs have actively supported a culinary return to rendered pork fat, strengthening premium demand and helping normalize lard use in higher-value dining channels.

Europe remains a mature part of the animal edible fat market, with France, Germany, Italy, Spain, and the Netherlands serving as major producing and consuming countries for butter, tallow, and lard. Traditional use in sausage making, pastry, and prepared meats continues to support regional demand. Regulatory tightening is also changing the supply landscape, as the 2026 amendment to EU Regulation (EC) 1069/2009 will require continuous digital CCP data logging and stronger traceability documentation at rendering facilities. This requirement raises compliance costs for smaller processors, but it also improves the verification record that premium food buyers and export customers increasingly require. South America centers on Brazil and Argentina, where large beef and pork systems create substantial rendered fat supply. Minerva Foods materially expanded this base after integrating 13 Marfrig plants acquired for BRL 5.7 billion, or USD 1.0 billion, increasing combined daily processing capacity to 41,789 cattle and 25,716 sheep across 46 industrial units in 7 countries.

The Middle East and Africa remain the smallest regional segment in the animal edible fat market, but they continue to offer opportunities in halal-certified tallow and butter supply chains. Saudi Arabia, the United Arab Emirates, and South Africa are the key demand centers, supported by foodservice growth, rising processed food use, and broader interest in halal premium foods. JBS supported this opportunity with a USD 150 million investment in a multiprotein hub in the Middle East that includes beef and lamb processing. Exporters also need to meet halal requirements from bodies such as the Gulf Standards Organization and SANHA, making certification an increasingly important procurement filter. These requirements favor suppliers that can combine scale, compliance discipline, and steady regional distribution.

Competitive Landscape

The edible animal fat market remains moderately fragmented, creating significant opportunities for consolidation through strategic acquisitions and vertical integration strategies. Key industry players include Darling Ingredients, Tyson Foods Inc., Cargill Incorporated, JBS S.A., and Mission Barns, among others. Market leaders such as Darling Ingredients leverage scale advantages by processing a significant share of global animal agricultural byproducts while maintaining technological leadership in rendering processes and renewable fuel applications.

Vertical integration strategies increasingly define the competitive landscape. For instance, Tyson Foods acquired American Proteins and AMPRO Products for USD 850 million to strengthen its rendering capabilities and expand its presence in animal feed ingredients. Companies focus their strategic positioning on sustainability credentials, regulatory compliance, and technological innovation rather than pure cost competition, as environmental regulations and consumer preferences drive demand for responsibly sourced products. Emerging disruptors from the synthetic biology sector pose long-term competitive threats through precision fermentation and lab-grown fat technologies, which offer stronger sustainability profiles and regulatory advantages.

Traditional players are responding through technology investments and strategic partnerships. Rendering companies emphasize their sustainability benefits, which they state are equivalent to removing 18.5 million cars from roads through waste reduction. Companies such as Mission Barns and Savor have secured regulatory approvals for animal-free fat products, which could disrupt traditional supply chains as production scales and costs decline. Competitive dynamics increasingly favor companies with integrated supply chains, advanced processing capabilities, and strong regulatory compliance records, as food safety standards tighten globally and customers prioritize supplier reliability over pure cost considerations.

Edible Animal Fat Industry Leaders

Darling Ingredients

Tyson Foods, Inc.

Cargill, Incorporated

JBS S.A.

Vion Food Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: JBS S.A. announced a 2026 capital expenditure plan of USD 2.4 billion, including USD 1.4 billion in expansion investments across facilities in Texas, Iowa, the Middle East, and Paraguay. JBS also separately announced a USD 150 million investment in a multiprotein hub in the Middle East covering beef and lamb processing, entering a high-growth demand region.

- December 2025: Tyson Foods acquired the former Cargill turkey processing plant in Springdale, Arkansas, for a deed-estimated value of USD 23 million. The facility, which had previously employed 1,000 workers, is planned for multi-year retooling to support chicken further processing and portioning operations.

- July 2024: Smithfield Foods completed the acquisition of Cargill’s dry sausage production facility in Nashville, Tennessee, adding 50 million pounds per year of dry sausage processing capacity and expanding pork-derived by-product throughput at adjacent processing sites to support its Margherita, Carando, and Armour brand portfolios.

Global Edible Animal Fat Market Report Scope

Edible animal fats are fats derived from animal tissues that are processed and refined for safe human consumption. The edible animal fat market is segmented by ingredient type, form, category, end-user and geography. Based on ingredient type the market is segmented into butter, tallow, lard, liquid gold and other ingredient types. Based on form, the market is segmented into solid and paste and liquid. Based on category, the market is segmented into conventional and organic. Based on end-user, the market is segmented into food processing industry, foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms.

| Butter |

| Tallow |

| Lard |

| Liquid Gold |

| Other Ingredient Types |

| Solid and Paste |

| Liquid |

| Conventional |

| Organic |

| Food Processing Industry | Bakery |

| Confectionery | |

| Savory Snacks | |

| Others | |

| Foodserivce | |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Ingredient Type | Butter | |

| Tallow | ||

| Lard | ||

| Liquid Gold | ||

| Other Ingredient Types | ||

| By Form | Solid and Paste | |

| Liquid | ||

| By Category | Conventional | |

| Organic | ||

| 5.4 By End-User | Food Processing Industry | Bakery |

| Confectionery | ||

| Savory Snacks | ||

| Others | ||

| Foodserivce | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for animal edible fat demand?

The edible animal fat market is forecast to reach USD 69.11 billion by 2031 from USD 58.42 billion in 2026, growing at a 3.42% CAGR over 2026-2031.

Which ingredient type leads revenue and which grows the fastest?

Lard is projected to grow the fastest at a 4.93% CAGR through 2031.

Which end-user channel matters most for volume?

The food processing industry remains the core demand base, holding 83.12% share in 2025 because bakery, confectionery, savory snacks, and prepared foods still depend on animal fat functionality.

Which region offers the strongest growth profile?

Asia-Pacific led with 40.22% share in 2025 and is also expected to post the fastest regional growth at a 5.7% CAGR through 2031.

Page last updated on: