Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

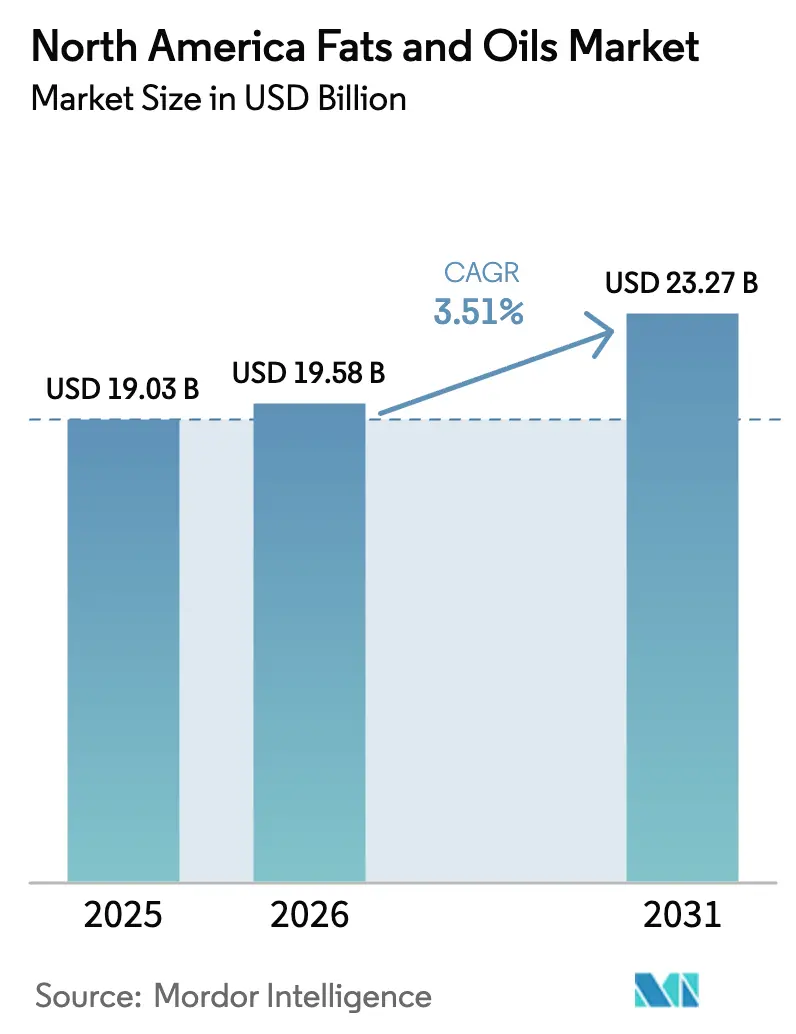

| Base Year Market Size (2025) | USD 19.03 Billion |

| Market Size (2026) | USD 19.58 Billion |

| Market Size (2031) | USD 23.27 Billion |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

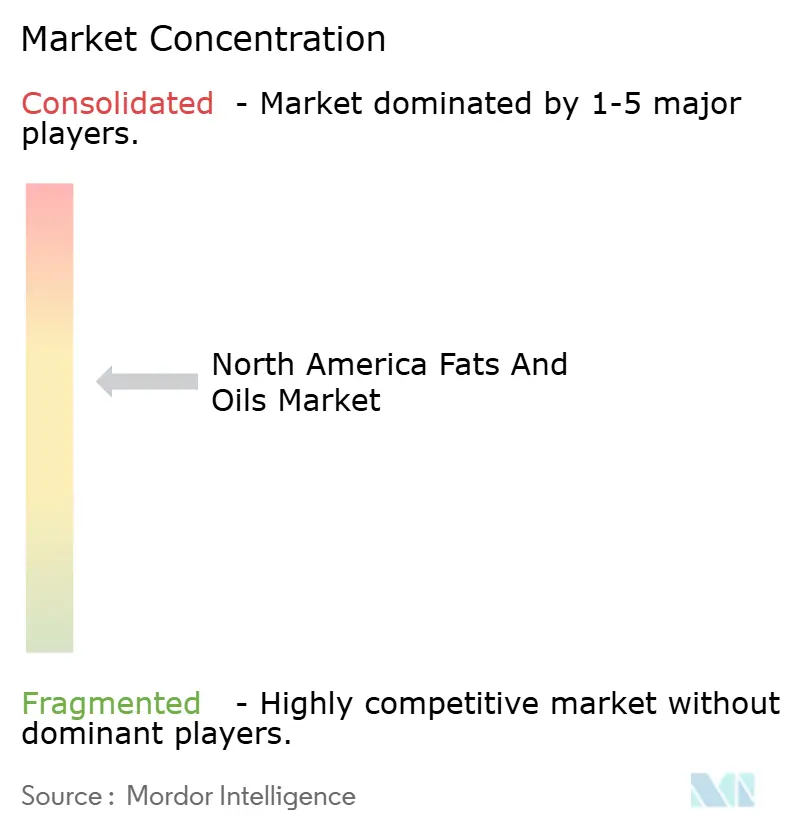

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fats And Oils Market Analysis by Mordor Intelligence

The North America fats and oils market size was valued at USD 19.03 billion in 2025 and is estimated to grow from USD 19.58 billion in 2026 to reach USD 23.27 billion by 2031, at a CAGR of 3.51% during the forecast period (2026-2031). This steady growth reflects significant structural changes within the market. Renewable diesel mandates are driving the use of animal fats and high-stability plant oils in fuel blending, with volumes now comparable to food-grade demand. At the same time, clean-label reformulation requirements are prompting processors to replace traditional palm-kernel fractions with more expensive interesterified blends. Furthermore, in December 2024, the United States Food and Drug Administration (FDA) revised its definition of the nutrient content claim "healthy," allowing oils with 20% or less saturated fat to qualify. This regulatory change has increased the preference for canola, sunflower, and high-oleic soybean oils over coconut and palm oils among formulators.

Key Report Takeaways

- By product type, oils led the market with a 56.53% share and are expected to grow at a CAGR of 5.82% during the forecast period.

- By application, the foods segment holds the largest market share of 58.92%, while animal feed is expected to grow at a CAGR of 5.37% through 2031.

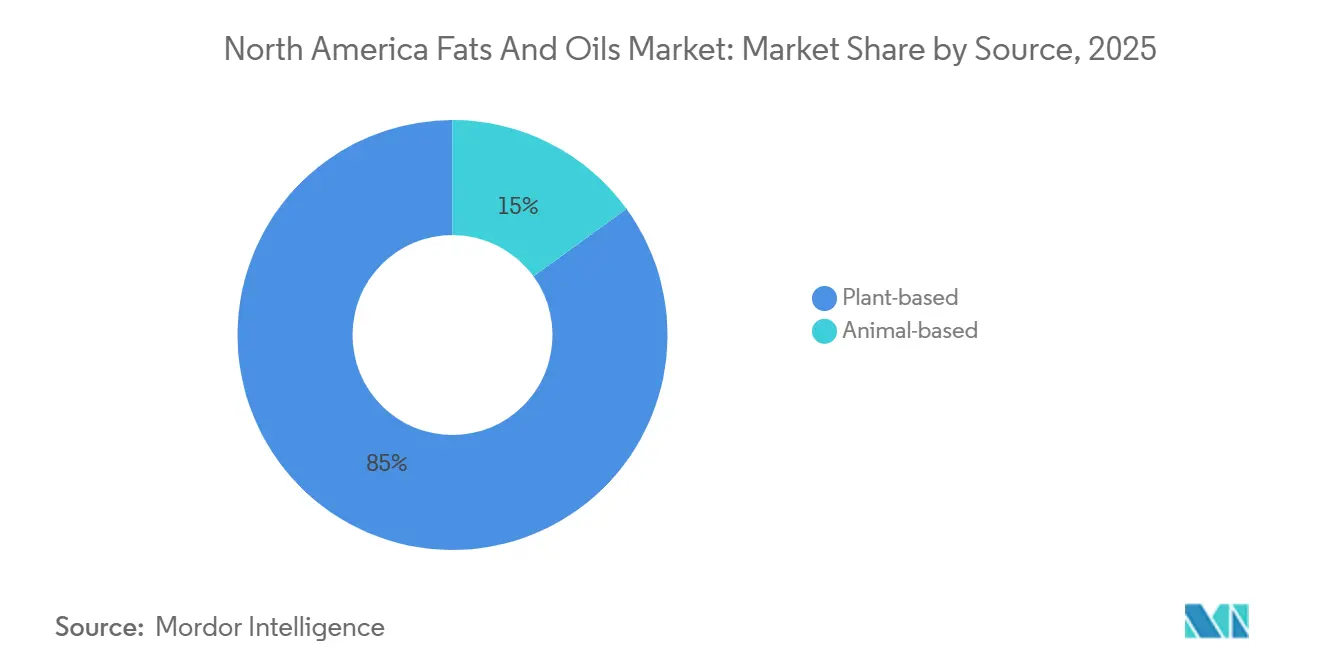

- By source, plant-based captured the fats and oils market, occupying 84.98% of the market share, while the animal-based segment is expected to reach a CAGR of 6.32%.

- By country, the United States led the market with a 71.64% share, and Canada is expected to grow at a CAGR of 4.62%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Fats And Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for organic, non-GMO, and sustainably certified fats and oils | +0.5% | United States, Canada (urban clusters) | Medium term (2-4 years) |

| Plant-based diets driving demand for diverse plant oils | +0.4% | United States, Canada | Long term (≥ 4 years) |

| Bakery and snack industries require specialty fats and oils | +0.6% | United States, Mexico | Short term (≤ 2 years) |

| Reformulation trends sustain demand for trans-fat replacements | +0.4% | United States, Canada, Mexico | Medium term (2-4 years) |

| Packaged-food processors standardize high-stability frying and baking oils | +0.5% | United States, Canada | Short term (≤ 2 years) |

| Health awareness boosts demand for omega-rich edible oils | +0.3% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preference for organic, non-GMO, and sustainably certified fats and oils

Sales of organic edible oils are increasing at a faster pace compared to conventional oils, driven by retailers dedicating more shelf space to products bearing United States Department of Agriculture (USDA) Organic and Non-GMO Project Verified labels [1]Source: Organic Trade Association, “Organic Industry Survey 2025,” ota.com . The USDA launched an Organic Transition Initiative to assist farmers in converting their acreage to organic oilseed production. This initiative aims to address supply constraints that have kept organic soybean oil prices significantly higher than conventional benchmarks. Sunflower oil, traditionally a minor crop in North America, is gaining renewed attention as organic-certified hectares in the Northern Plains have increased substantially. This growth is attributed to the rotational benefits and premium pricing, which help compensate for the lower per-acre yields compared to soybeans. Additionally, sustainability certifications are expanding beyond organic standards, with the Roundtable on Sustainable Palm Oil (RSPO) including a growing number of North American member companies. This reflects food manufacturers' responses to investor demands and non-governmental organization scorecards emphasizing supply chain transparency. These developments are particularly notable in premium retail channels and foodservice operations catering to health-conscious consumers. However, adoption remains limited in cost-sensitive institutional segments, where the cost per serving continues to be the primary factor influencing procurement decisions.

Plant-based diets driving demand for diverse plant oils

Plant-based food sales in the United States have significantly increased the demand for specialty oils, particularly in categories that rely on coconut, oat, and almond oils for texture and mouthfeel. The growing popularity of plant-based meat alternatives has created a need for oils that replicate the sizzle and browning characteristics of animal fat. To address this, formulators often blend high-oleic sunflower oil with small amounts of coconut oil, achieving the desired sensory profile while ensuring compliance with saturated-fat labeling thresholds. Olive oil imports into the United States rose by 23 percent year-over-year in early 2024, driven by the increasing adoption of the Mediterranean diet. Consumers are increasingly replacing butter with olive oil in home cooking, a behavioral shift that continues even as retail prices stabilize following the 2023 European drought [2]Source: U.S. Department of Agriculture, “Mexico: Oilseeds and Products Annual,” fas.usda.gov. Similarly, avocado oil, which was nearly absent from North American retail shelves a decade ago, now occupies dedicated sections in mainstream grocery stores. Its premium pricing is justified by its high smoke point and monounsaturated fat content, which align with cardiologist recommendations. This shift in consumer preferences is further supported by social media influencers and celebrity endorsements, which have elevated niche oils into household staples. Traditional commodity processors face challenges in replicating this marketing approach.

Bakery and snack industries require specialty fats and oils

Bakery and confectionery manufacturers are facing a unique challenge as they strive to meet consumer demands for clean labels free from hydrogenated oils while maintaining the flaky texture and extended shelf life that partially hydrogenated fats used to provide. Interesterification, a chemical process that rearranges fatty acids on the glycerol backbone, has emerged as a practical solution. This technology allows the production of solid fats from liquid oils without creating trans isomers, although it increases ingredient costs by eight to twelve cents per pound. Companies such as Cargill and AAK have made significant investments in interesterification capacity across North America, focusing on applications like laminated dough and cream fillings, where preserving functionality is essential. High-oleic soybean oil, marketed under trade names such as Vistive Gold and Plenish, extends frying life by 30 to 50 percent compared to conventional soybean oil. This advantage helps quick-service restaurants reduce oil change frequency and disposal costs. Snack manufacturers are also exploring enzyme-modified oils that enhance crispness retention in humid climates, which is particularly important for products distributed in regions like Mexico and the southern United States. Regulatory compliance frameworks, including the United States Food and Drug Administration (FDA) Generally Recognized as Safe (GRAS) determinations and Kosher certifications, add further complexity. These requirements often favor established suppliers with in-house regulatory affairs teams over smaller regional fat processors.

Reformulation trends sustain demand for trans-fat replacements

The United States Food and Drug Administration (FDA) mandated the removal of partially hydrogenated oils from the food supply in 2018, initiating a significant reformulation effort across bakery, snack, and foodservice categories. This change has driven a multi-billion-dollar wave of innovation in ingredient specifications. Interesterification has emerged as the primary replacement technology, enabling processors to create solid fats with customized melting profiles using liquid oils as feedstock. However, this process requires specialized equipment and technical expertise, which has concentrated production among a few large-scale suppliers. High-oleic soybean and sunflower oils have gained substantial market share in frying applications due to their extended oxidative stability. This stability reduces oil turnover frequency and lowers overall costs, even though these oils come with higher upfront pricing. Palm oil, which is naturally trans-fat-free and solid at room temperature, initially saw increased usage during the reformulation phase. However, sustainability concerns have prompted many brands to explore alternatives such as shea butter and enzymatically structured lipids. Reformulation efforts now extend beyond eliminating trans fats to include reducing saturated fats. The FDA's updated definition of the "healthy" claim and anticipated front-of-pack labeling requirements have created incentives to minimize the use of tropical oils. Smaller manufacturers face significant challenges in reformulation, as costs for sensory testing, shelf-life validation, and production line adjustments can exceed USD 100,000 per stock-keeping unit. These high costs favor established suppliers with robust technical support capabilities and discourage new entrants into the market. Geographic consistency is maintained across North America under the United States-Mexico-Canada Agreement (USMCA) harmonization efforts, though enforcement varies. The United States enforces the most stringent inspection and recall measures in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Negative perception of palm oil and tropical fats | -0.3% | United States, Canada | Short term (≤ 2 years) |

| Regulatory challenges on trans fats and nutrition labeling | -0.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Competition from fat replacers and alternative systems | -0.2% | United States, Canada | Long term (≥ 4 years) |

| Technical challenges in replacing animal fats and palm oils | -0.3% | United States, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Negative perception of palm oil and tropical fats

Palm oil's connection to deforestation and habitat destruction has created a significant reputational challenge, influencing consumer behavior and pressuring food manufacturers to reformulate their products to avoid social media backlash and potential removal from retail shelves. Companies such as Ferrero, Nestlé, and Unilever have committed to using 100% Roundtable on Sustainable Palm Oil (RSPO)-certified sustainable palm oil by 2025. However, certification alone has not been enough to address criticism, as satellite monitoring by organizations like Global Forest Watch continues to report forest loss in concession areas. North American confectionery brands are exploring palm-free alternatives, including shea butter and enzymatically structured blends of high-oleic sunflower oil and fully hydrogenated soybean oil. These substitutes often increase ingredient costs by 15% to 25% and require reformulation trials to replicate palm oil's unique melting properties. The technical challenges are particularly significant in applications such as chocolate coatings and sandwich cookie creams, where palm kernel oil's sharp melting point and neutral flavor are difficult to replace. Consumer surveys indicate that 43% of shoppers in the United States actively avoid palm oil when reading product labels. This shift in consumer behavior has prompted major retailers to introduce palm-free private label product lines. The impact of this trend is most evident in the confectionery and bakery segments, where palm oil has historically accounted for 20% to 30% of fat inputs. In contrast, the effect on frying oil and industrial applications has been minimal, as functionality and cost remain the primary factors influencing purchasing decisions.

Regulatory challenges on trans fats and nutrition labeling

The United States Food and Drug Administration (FDA) finalized the removal of partially hydrogenated oils from the Generally Recognized as Safe (GRAS) list, effectively banning artificial trans fats. However, compliance verification and enforcement are still ongoing, as inspectors continue to identify non-compliant products, particularly in ethnic grocery channels and small bakeries. Similarly, Canada has implemented comparable restrictions, while Mexico is gradually introducing trans-fat limits in alignment with Pan American Health Organization (PAHO) guidelines. These measures establish a North America-wide regulatory framework, eliminating opportunities for competitive arbitrage. Nutrition labeling requirements are also becoming stricter. The Food and Drug Administration has updated the Nutrition Facts panel format to emphasize saturated fat and added sugars, which disadvantages tropical oils and encourages reformulation toward alternatives such as canola, sunflower, and high-oleic soybean oils [3]Source: U.S. Food & Drug Administration, “How to Understand and Use the Nutrition Facts Label,” fda.gov. Although front-of-pack labeling schemes are not yet mandatory in the United States, they are under discussion and could penalize products high in saturated fat, further reducing the use of palm and coconut oils. Compliance costs associated with these regulatory changes are significant. Reformulation efforts require sensory testing, shelf-life validation, and production line adjustments, which can cost mid-sized manufacturers over USD 100,000 per stock-keeping unit (SKU). These high costs create barriers for smaller players and favor established suppliers with robust technical support capabilities. Additionally, the regulatory environment now includes allergen labeling updates. For instance, the inclusion of sesame oil on the major allergen list in 2023 has compelled manufacturers to audit supply chains and implement segregation protocols, adding complexity to multi-oil blending operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Oils Outpace Solid Fats on Clean-Label Momentum

In 2025, oils accounted for 56.53% of the market share and are projected to grow at an annual rate of 5.82% through 2031, representing the fastest growth among product types. This growth is driven by food manufacturers' preference for liquid formats that eliminate hydrogenation steps and simplify ingredient declarations. Soybean oil continues to play a central role in North American food processing due to its neutral flavor and competitive pricing. However, high-oleic soybean oil is increasingly replacing conventional grades in frying applications, where extended use cycles justify a 10 to 15 percent price premium. Canola oil, the second-largest segment by volume, benefits from its favorable fatty acid profile, which supports heart-health claims and high-temperature stability. Canadian production expansions ensure a steady supply for United States food manufacturers and foodservice distributors.

Palm oil, despite ongoing sustainability concerns, maintains its presence in industrial bakery and confectionery applications due to its unmatched solid-fat content and oxidative stability. However, import volumes are stabilizing as brands increasingly promote palm-free reformulations. Coconut oil serves a dual-purpose market: refined grades are used as palm oil substitutes in vegan confections, while virgin coconut oil commands premium pricing in natural food channels, despite its high saturated fat content conflicting with dietary guidelines. Olive oil, traditionally a niche import, is expanding its use beyond salad dressings into cooking applications as consumers adopt Mediterranean diet principles. California production is contributing an increasing share to the domestic supply. Sunflower and cottonseed oils cater to regional markets. Sunflower oil is gaining popularity in organic and high-oleic formats, while cottonseed oil remains concentrated in the southern United States, where it is a by-product of the textile industry. Specialty fats, including butter, tallow, lard, and engineered blends, are undergoing significant changes. Butter is being premiumized with grass-fed and European-style variants gaining retail traction. Tallow, once a low-value rendering by-product, is now in high demand as a renewable diesel feedstock, commanding prices comparable to edible grades. Lard is experiencing a resurgence in culinary applications, particularly in baking and frying, though its volumes remain modest compared to plant-based oils.

By Application: Animal Feed Fortification Drives Fastest Expansion

In 2025, food applications represented 58.92% of the market share, including categories such as confectionery, bakery, dairy, and other processed foods. Meanwhile, animal feed was the fastest-growing application, with an annual growth rate of 5.37%. This growth is primarily driven by omega-3 fatty acid fortification mandates in aquaculture and poultry production, which help improve feed conversion ratios and enhance the nutritional quality of meat and eggs.

Confectionery manufacturers are working to address the challenge of replacing palm oil by experimenting with alternatives like shea butter and interesterified blends. These substitutes replicate the snap and gloss of chocolate coatings without relying on tropical sourcing. However, the associated cost increases of 20% to 30% per formulation are putting brand loyalty and profit margins to the test. In the bakery segment, which is the largest food sub-category, there is a growing preference for liquid oils and enzyme-modified fats that extend shelf life and support clean-label declarations. High-oleic soybean oil is becoming increasingly popular, particularly in laminated doughs and frying applications. Dairy product manufacturers are incorporating specialty fats into cheese analogs and whipped toppings, as these applications require precise melting curves and emulsification properties that standard commodity oils cannot provide without modification. Additionally, other food applications, such as salad dressings, sauces, and ready meals, use oils as carriers for flavors and fat-soluble vitamins. In premium product categories, organic and non-GMO (non-genetically modified organism) certifications are becoming standard requirements.

By Source: Animal Fats Surge on Renewable Diesel Demand

Plant-based sources are expected to dominate with an 84.98% market share in 2025, highlighting the structural advantages of oilseed agriculture in North America. The cultivation of soybean, canola, and sunflower is deeply integrated into crop rotation systems and supported by extensive crushing infrastructure. Soybean oil accounts for the largest share of plant-based volume, driven by the significant production capacity of the United States soybean belt and the oil's versatility across food, feed, and industrial applications. Canola oil, the second-largest contributor to plant-based supply, benefits from Canadian production exceeding 18 million metric tons annually, with crushing facilities often located near biodiesel refineries to maximize value extraction. Sunflower, cottonseed, and specialty oils, such as olive and avocado, contribute smaller volumes but are growing faster than commodity-grade oils as consumers increasingly seek flavor diversity and health-focused ingredients. Palm oil, while plant-based, is categorized separately due to its import dependency and sustainability concerns, which differentiate it from domestically produced oils.

Animal-based fats are experiencing the fastest growth rate among source categories, expanding at 6.32% annually. This growth is driven by renewable diesel feedstock demand, which has elevated tallow from a low-value by-product to a premium commodity. Darling Ingredients, the largest North American renderer, reported tallow prices exceeding 60 cents per pound in 2024, more than double the historical average, as renewable diesel refineries compete for feedstock to meet state and federal blending mandates.

Geography Analysis

The United States dominated the North American market with a 71.64% share in 2025, driven by its robust food processing industry, extensive oilseed crushing capacity, and large population that fuels demand in both retail and foodservice sectors. Soybean oil production in the United States reached 28.6 billion pounds during the 2024-2025 marketing year, with 13.9 billion pounds allocated to biomass-based diesel production. This allocation reduces the availability of food-grade soybean oil, supporting higher prices. The U.S. market is geographically diverse, with Gulf Coast crushing facilities focusing on export-oriented production and renewable diesel feedstock, Midwest plants serving domestic food processors and livestock feed producers, and California refineries specializing in premium-priced specialty oils and organic-certified products for coastal markets. Regulatory factors such as state-level renewable fuel standards, Food and Drug Administration (FDA) nutrition labeling requirements, and United States Department of Agriculture (USDA) organic certification programs influence product offerings and investment strategies. Additionally, the United States is the primary destination for Canadian canola oil exports, with cross-border trade exceeding 2 billion pounds annually, supported by the United States-Mexico-Canada Agreement (USMCA) duty-free access and integrated logistics networks.

Canada is the fastest-growing market in North America, with an annual growth rate of 4.62% projected through 2031. This growth is fueled by expansions in canola crushing capacity, which convert domestic harvests into food-grade oil and renewable diesel feedstock within vertically integrated facilities. In 2024, Richardson International, a Canadian agribusiness, announced a USD 250 million investment in canola processing infrastructure to enhance export capacity for United States food manufacturers and Asian biodiesel refiners. Canadian canola oil enjoys a strong reputation for health benefits, with its monounsaturated fat content and omega-3 presence supporting cardiovascular health claims that resonate with North American consumers. The Canadian market also produces specialty oils, such as flaxseed and hemp seed oils, leveraging the country's cold-climate agriculture and organic certification capabilities.

Other markets in North America, including Mexico, Central America, and the Caribbean, are also contributing to the region's growth. Mexico, the third-largest market, is expanding as urbanization and rising incomes drive increased consumption of packaged foods. However, the country remains a net importer of soybean and palm oils, creating opportunities for United States exporters to leverage proximity and USMCA preferential trade access. Mexican consumers primarily use soybean oil for cooking and palm oil for industrial bakery applications, while olive oil and specialty oils are limited to affluent urban segments. Meanwhile, Central American and Caribbean markets contribute smaller volumes but are growing as regional food processors adopt North American formulation standards and sourcing practices.

Competitive Landscape

The North America Fats and Oils Market is moderately consolidated, with the top five processors, including Cargill, Archer Daniels Midland (ADM), Bunge, Wilmar, and Louis Dreyfus, accounting for nearly half of the regional crushing capacity. These companies face competition from farmer-owned cooperatives such as CHS and Ag Processing, which focus on maximizing returns for their members rather than prioritizing profit margins. The Bunge-Viterra merger, finalized in July 2024 at a valuation of USD 8.2 billion, created a USD 34 billion revenue entity with a geographic presence spanning from the Gulf Coast to the Canadian Prairies. This strategic positioning allows the company to take advantage of basis differentials and optimize logistics costs. A clear division is emerging in the market, with traditional food-grade processors concentrating on interesterification and specialty fat production for premium bakery and confectionery applications. At the same time, they are expanding crushing capacity to meet the growing demand from renewable diesel refineries. The Bunge-Chevron joint venture illustrates this dual strategy, with a soybean processing facility in Destrehan, Louisiana, dedicated to supplying feedstock exclusively to nearby renewable diesel units, effectively separating these volumes from food markets.

Opportunities are arising in niche segments such as organic and non-GMO certified oils, where supply constraints and certification complexities create barriers to entry, protecting early movers from rapid competition. Additionally, animal feed fortification oils present growth potential, as technical expertise in omega-3 stabilization and palatability enables pricing power beyond commodity segments. Technology adoption is accelerating, with processors leveraging precision agriculture and traceability systems. Blockchain pilots, for instance, are helping processors document sustainable sourcing claims with immutable audit trails, a capability increasingly demanded by major food brands to meet investor ESG reporting requirements and consumer transparency expectations.

Emerging disruptors in the market include algae fermentation companies like DSM-Firmenich, which bypass traditional oilseed agriculture to produce omega-3 oils with controlled fatty acid profiles, and enzyme technology firms developing structured lipids that mimic butter functionality using liquid plant oils. These innovations have the potential to commoditize specialty fats that currently command premium pricing. Patent activity in the sector is concentrated on processing methods, such as interesterification catalysts, cold-press extraction, and oxidative stability additives, rather than novel oil sources. This trend indicates that competitive advantage in the market is driven by manufacturing efficiency and formulation expertise rather than access to raw materials.

North America Fats And Oils Industry Leaders

Wilmar International Ltd

Cargill Incorporated

Louis Dreyfus Company

Archer Daniels Midland Company

Bunge Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Savor, a United States-based food technology company, has developed a butter product manufactured without animal or plant ingredients. The company employs a fermentation process to transform carbon dioxide (CO₂), green hydrogen (GH₂), and methane (CH₄) into structured fats.

- July 2024: Louis Dreyfus Company constructed a soybean processing facility in Ohio, United States. The plant operates with a daily crushing capacity of 175,000 bushels and manufactures soybean meal, hulls, and oil, with integrated packaging operations.

- July 2024: Construction of Cargill's new canola processing facility at the Global Transportation Hub in West Regina, Saskatchewan, Canada, has exceeded 50 percent completion. The facility will process 1 million metric tons of canola annually, manufacturing crude canola oil for food and biofuel markets, along with canola meal for animal feed.

- July 2024: Bunge expanded its product portfolio by launching Beleaf PlantBetter in North America, following its European market entry in 2023. The ingredient enables food manufacturers and bakers to incorporate plant-based alternatives that match the functional properties and performance characteristics of dairy butter. The company identified key technical challenges in butter substitutes, including maintaining optimal aeration, volume control, and flavor consistency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the North America fats and oils market as the combined annual value of edible and industrial-grade triglyceride products derived from plant and animal sources that are processed within the United States, Canada, Mexico, and the Rest of North America. This value tracks first-time commercial deliveries into food, feed, oleochemical, and biofuel channels, measured in USD at manufacturer gate prices.

Scope exclusion: petroleum-based lubricants and synthetic esters fall outside our study.

Segmentation Overview

- By Type

- Fats

- Butter

- Tallow

- Lard

- Specialty Fats

- Oils

- Soybean Oil

- Rapeseed Oil

- Palm Oil

- Coconut Oil

- Olive Oil

- Cotton Seed Oil

- Sunflower Seed Oil

- Others

- Fats

- By Application

- Food

- Confectionary

- Bakery

- Dairy Products

- Others

- Industrial

- Animal Feed

- Food

- By Source

- Plant-based

- Animal-based

- By Country

- United States

- Canada

- Mexico

- Rest of North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oilseed processors, specialty fat blenders, biodiesel producers, food formulators, and procurement managers across the United States, Canada, and Mexico. Discussions confirmed utilization rates, contract pricing windows, and adoption timelines for high-oleic variants, letting us fill data gaps and test preliminary assumptions.

Desk Research

Our desk review began with public statistics from USDA Economic Research Service, Statistics Canada, and Mexico's SIAP that detail crush volumes, trade flows, and monthly consumption. We added import-export shipment data from Volza, trade association bulletins from the American Fats & Oils Association, and peer-reviewed journals that quantify trans-fat substitution trends. Company 10-Ks, investor decks, and customs tariff filings supplied price spreads and capacity additions. Select inputs were validated through D&B Hoovers and Dow Jones Factiva feeds for revenue cross-checks and plant announcements. The sources cited illustrate the breadth, not the entirety, of references our desk study covers.

Market-Sizing & Forecasting

A top-down reconstruction starts with oilseed crush, rendered fat output, and import volumes, which are then priced using quarterly average producer prices to reach a gross demand pool. Select bottom-up checks, sampled supplier revenues, channel audits, and average selling price × volume tests calibrate segment totals. Key variables feeding the model include soybean crush yield, renewable diesel capacity, bakery fat penetration, feed inclusion ratios, regulatory trans-fat limits, and currency movements. Multivariate regression with ARIMA error correction projects each driver to 2030, while scenario analysis handles policy or weather shocks. Where bottom-up evidence is thin, weighted moving averages smooth anomalies before integration.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, peer review, and anomaly reconciliation. Reports refresh every twelve months, and we trigger interim updates after material events such as tariff shifts or crop failures. A final pre-publication audit ensures the latest data set reaches clients.

Why Mordor's North America Fats and Oils Baseline Earns Dependability

Published estimates rarely align because each publisher picks different scopes, reference years, and conversion factors. Our study, anchored to on-shore production plus net trade and filtered through price-verified interviews, narrows those variables so decision-makers start from a clear, documented baseline.

Key gap drivers often stem from including non-triglyceride lubricants, using retail prices, rolling forward historic growth without supply-demand tests, or spacing updates wider than a year. Mordor Intelligence avoids these pitfalls through its annual refresh cadence, aligned scope, and dual validation loops.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.94 B (2025) | Mordor Intelligence | - |

| USD 35.60 B (2024) | Global Consultancy A | Includes specialty chemicals and uses revenue-based roll-ups without trade reconciliation |

| USD 13.40 B (2023) | Trade Journal B | Excludes industrial biofuel demand and converts volumes with fixed 2019 price factors |

| USD 110.82 B (2022) | Industry Association C | Treats all edible oil categories, applies retail pricing, and lacks annual update discipline |

The comparison shows that figures swing widely when scope, pricing point, and refresh cadence diverge. By selecting only triglyceride products, confirming prices at the producer level, and revisiting the model each year, Mordor Intelligence delivers a balanced, transparent baseline managers can readily track and replicate.

Key Questions Answered in the Report

What is the projected value of the North America fats and oils market in 2031?

The market is forecast to reach USD 23.27 billion by 2031.

Which application category is expanding fastest?

Animal feed is growing at a 5.37% CAGR, driven by omega-3 fortification.

Why are animal fats gaining momentum despite smaller share?

Renewable diesel refineries are locking in long-term contracts for tallow and other rendered fats, pushing 6.32% CAGR growth.

Which country shows the fastest market growth?

Canada leads with a 4.62% CAGR due to canola-crushing and biodiesel integration.

Page last updated on: