Specialty Fats and Oils Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

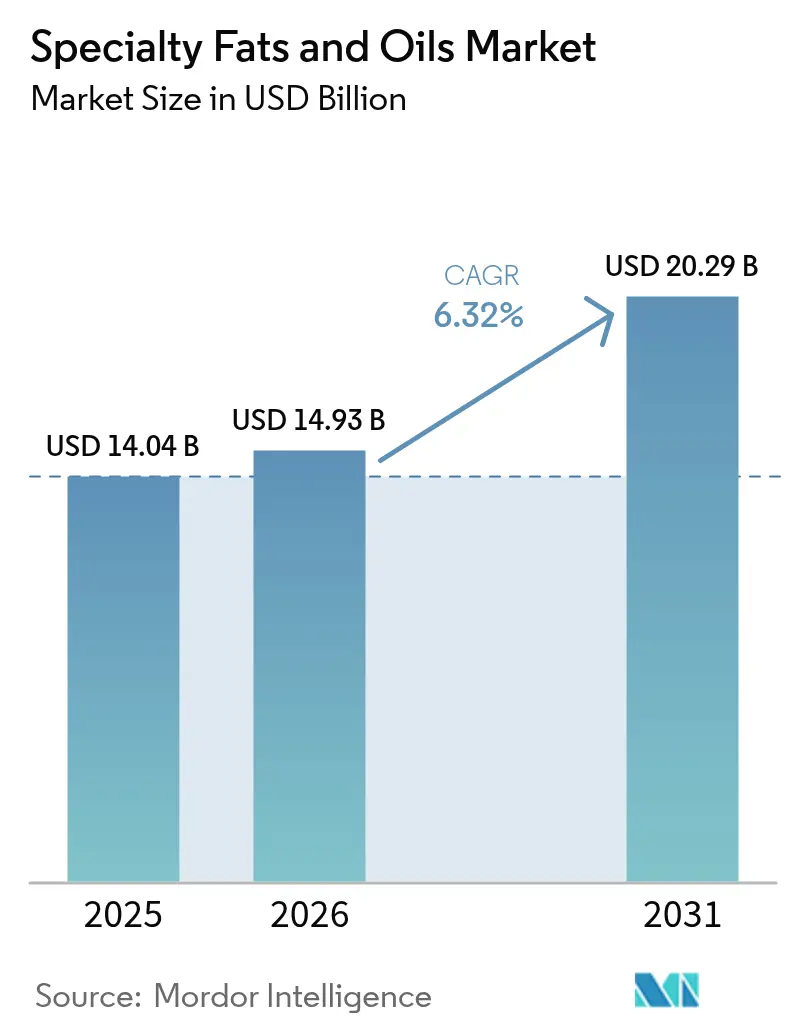

| Market Size (2026) | USD 14.93 Billion |

| Market Size (2031) | USD 20.29 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

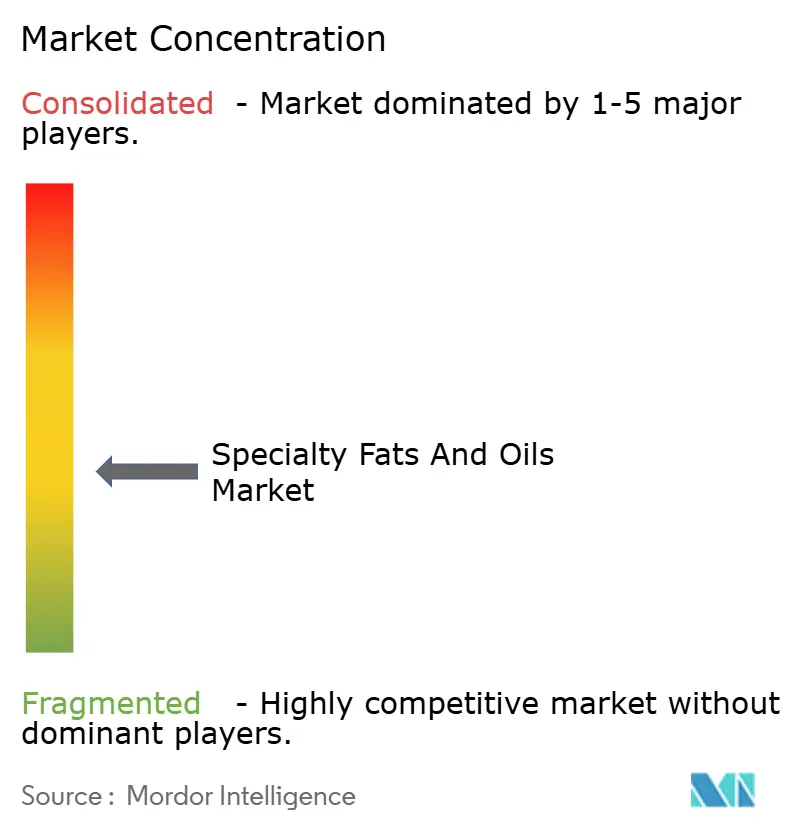

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Fats and Oils Market Analysis by Mordor Intelligence

The specialty fats and oils market size is expected to grow from USD 14.04 billion in 2025 to USD 14.93 billion in 2026 and is forecast to reach USD 20.29 billion by 2031 at 6.32% CAGR over 2026-2031. The market expansion is driven by increased demand for functional lipids as trans-fat alternatives, stricter regulations, and growing interest in plant-based food options. The consumption growth of processed foods, rising cocoa prices necessitating cocoa butter alternatives, and the FDA's revised "healthy" definition with stricter saturated fat requirements have led to increased product reformulations [1]Source: FDA, “Guidance for Industry on the Use of the Term ‘Healthy,’ 2025,” fda.gov. Asia-Pacific dominates consumption due to biodiesel mandates and palm oil trade agreements, while the Middle East & Africa shows the highest CAGR, supported by new refinery investments. The market development is further shaped by clean-label trends, supply chain diversification efforts, and advances in fat modification technology.

Key Report Takeaways

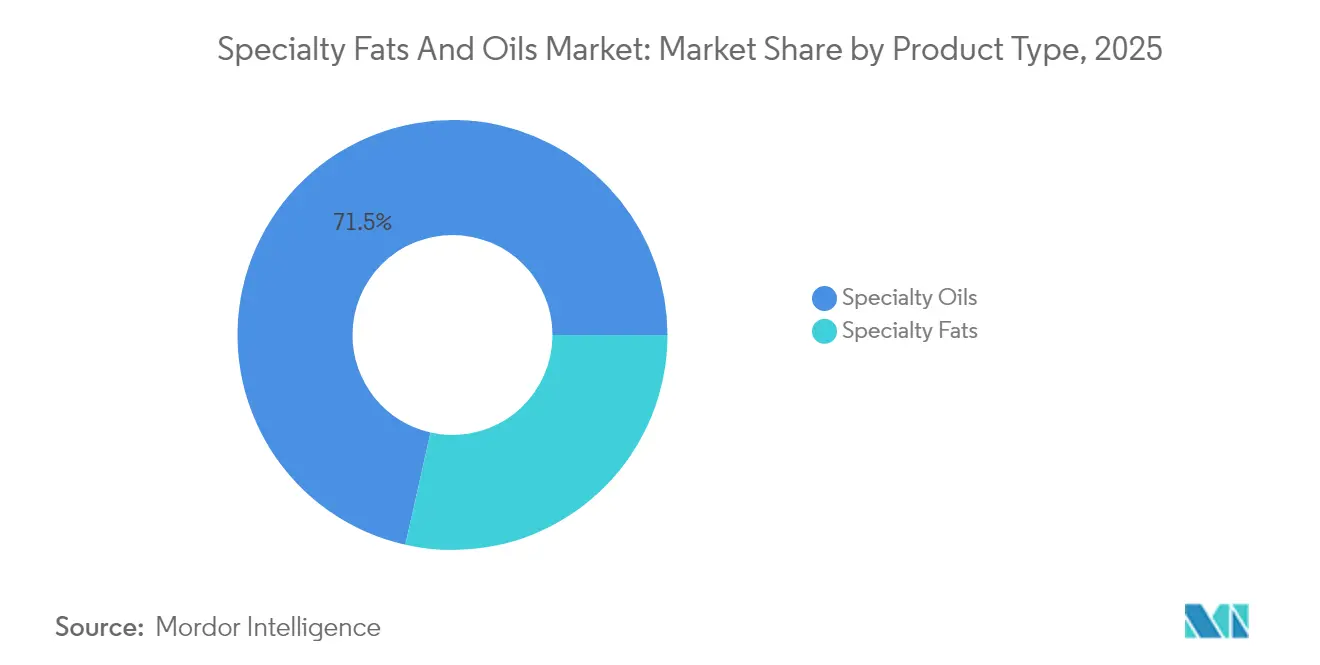

- By product type, specialty oils led with 71.48% of the 2025 specialty fats and oils market share, while specialty fats posted the fastest 7.31% CAGR.

- By form, liquid products captured 68.92% revenue share in 2025; dry formats record the highest 7.88% CAGR through 2031.

- By functionality, coating, and enrobing fats accounted for 41.98% of 2025 revenue; molding and filling fats registered an 8.23% CAGR to 2031.

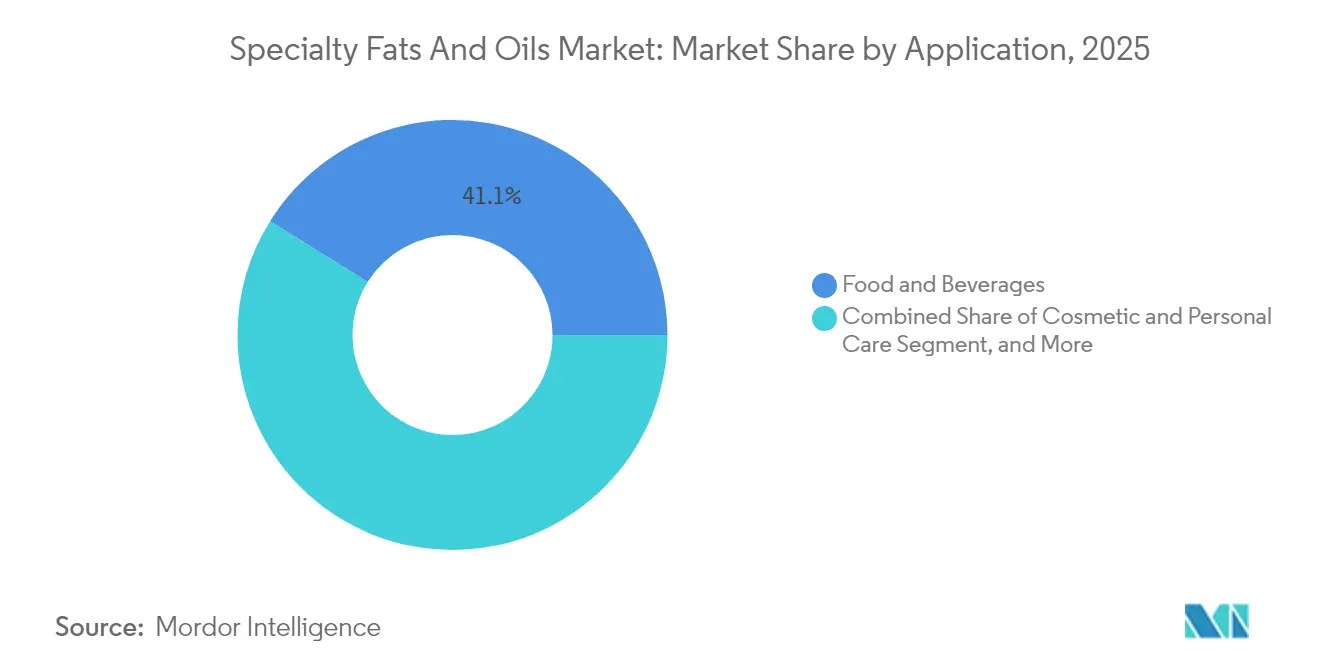

- By application, food and beverages retained 41.12% of 2025 revenue, whereas cosmetics and personal care delivered an 8.05% CAGR between 2026 and 2031.

- By geography, Asia-Pacific dominated with a 39.92% 2025 revenue share; the Middle East & Africa is the fastest-growing region at a 7.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Fats and Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in processed and packaged food consumption | +1.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rising demand for healthier and functional ingredients | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Surge in demand for cocoa-butter equivalents (CBEs) | +1.2% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Clean label and natural product trends | +1.0% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Increasing adoption of plant-based and vegan products | +0.8% | Global, with North America and Europe leading | Long term (≥ 4 years) |

| Growing use in non-food applications | +0.7% | Global, with strong growth in APAC and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Processed and Packaged Food Consumption

Food manufacturers are experiencing higher demand for specialty fats as consumers increasingly prefer processed foods. These manufacturers need functional lipids to enhance product texture, extend shelf life, and improve nutritional content. The growth of the global processed food market has prompted manufacturers to incorporate specialty fats in their confectionery, bakery, and dairy products, as these ingredients play a vital role in product formulation and quality. With the FDA's ban on partially hydrogenated oils in food products coming into effect in August 2025, manufacturers must switch to specialty fats that deliver similar functionality without trans-fat content. Cargill has set an industry benchmark by becoming the first global edible oils supplier to meet WHO standards for industrially produced trans-fatty acids, maintaining content below 2 grams per 100 grams. These regulatory requirements continue to drive the demand for specialty fats as manufacturers seek alternatives to traditional hydrogenated oils while ensuring product quality and consumer satisfaction.

Rising Demand for Healthier and Functional Ingredients

As consumers become increasingly health-conscious, they seek functional ingredients that deliver nutritional benefits beyond basic calories, making specialty fats essential in health-focused product development. The FDA's updated "healthy" food definition, taking effect in February 2025, emphasizes nutrient-dense foods and limits saturated fat content, opening new opportunities for specialty oils with beneficial fatty acid profiles [2]Source: Federal Register, “Food Labeling; Definition of ‘Healthy,’ 2025,” federalregister.gov. Plant-based beverage manufacturers have begun incorporating omega-3 fatty acids into their products, utilizing enzymatic interesterification technology to produce high-quality omega-3 triglycerides while maintaining natural oil characteristics. The FDA's approval of Barry Callebaut's qualified health claims for cocoa flavanols in April 2025 reinforces the therapeutic value of specialty lipid ingredients. The recovery of the Peruvian anchovy fishery, which produced 1.1 million tons in the latest season, has helped address the omega-3 raw material shortages that previously restricted functional ingredient applications.

Surge in Demand for Cocoa-Butter Equivalents (CBEs)

Rising cocoa prices, which reached nearly USD 10,000 per metric ton in 2024, have prompted food manufacturers to explore cocoa butter equivalents (CBEs) as cost-effective alternatives that maintain product quality. Companies like Hershey and Mondelēz have revised their production forecasts in response to these price pressures, increasingly turning to CBEs and cocoa butter substitutes in their formulations. In June 2025, Ardent Mills brought "Cocoa Replace" to market, offering a wheat-based cocoa powder alternative that replaces up to 25% of cocoa content while delivering comparable flavor and texture. Working with Voyage Foods, Cargill developed "Indulgence Redefined," a chocolate alternative that reduces carbon footprint by 61% and water usage by 95% compared to traditional chocolate, without compromising taste. The European Union's Deforestation Regulation has further encouraged manufacturers to adopt CBEs as they seek sustainable and compliant alternatives to conventional cocoa.

Clean Label and Natural Product Trends

Consumer preferences for product transparency are reshaping how manufacturers develop specialty fats, with emphasis on familiar ingredients and clear production methods. Recent FDA regulations on GRAS rule reform require manufacturer compliance for safety documentation prior to ingredient introduction, highlighting the shift toward natural fat derivatives. Manufacturing companies have adopted enzymatic interesterification methods to replace traditional chemical processes, as demonstrated by Fuji Oil's implementation of SOS fat technology for cocoa butter alternatives. Within cosmetic manufacturing, companies incorporate safflower oleosomes for natural emulsification properties, enhancing skin protection and moisture retention capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.5% | Global, with severe impact on APAC and EU | Short term (≤ 2 years) |

| Limited Availability of Quality Raw Materials | -1.2% | Global, particularly affecting North America and EU | Medium term (2-4 years) |

| Competition from Alternative Ingredients | -0.8% | North America & EU core, expanding globally | Long term (≥ 4 years) |

| Technical Challenges in Product Development | -0.5% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

The persistent instability in raw material prices significantly hampers the growth of the specialty fats market, creating operational challenges for manufacturers who must navigate unpredictable input costs. These cost fluctuations directly impact their ability to plan production schedules effectively and maintain stable profit margins. The dramatic increase in used cooking oil imports from China to the United States, which saw a threefold rise in 2023, has introduced substantial concerns about feedstock quality standards and pricing transparency within the biofuels industry. The ongoing volatility in palm oil prices, evidenced by Malaysian futures fluctuating between MYR 4,000-4,600 (USD 903-1,038) per tonne through March 2025, demonstrates the broader supply-demand disparities that ultimately affect specialty fats pricing across the value chain.

Limited Availability of Quality Raw Materials

The production of specialty fats faces constraints due to limited availability of quality raw materials, as processors compete for premium feedstocks that meet strict purity and sustainability requirements. The German Union for the Promotion of Oil and Protein Plants reports that global rapeseed production cannot meet current demand, highlighting supply deficits in key specialty oil feedstocks. Malaysia's palm oil output remains restricted due to forest protection measures, limiting the availability of sustainable palm oil despite increasing demand. The aging palm plantations in Indonesia and Malaysia require replanting programs to maintain productivity, which temporarily reduces raw material supplies during transition phases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Oils Dominate Despite Fats' Superior Growth

The global specialty oils market demonstrates strong market fundamentals, with a commanding 71.48% share in 2025. This dominance stems from the essential role these oils play across food processing operations, biodiesel manufacturing, and diverse industrial applications. Meanwhile, specialty fats are emerging as a high-potential segment, with projections indicating a robust growth rate of 7.31% through 2031. The market landscape reveals notable shifts in key oil segments. Soybean oil maintains its position as the primary vegetable oil in food applications, with U.S. suppliers strengthening their presence in Korean markets through increased export capabilities.

The rapeseed/canola oil segment faces supply challenges as production volumes lag behind market demand, creating opportunities for alternative specialty oils. El Niño-related weather impacts have severely affected coconut oil production, reducing yields by half and driving up prices. In contrast, olive oil continues to benefit from consumer preference for healthier options. The accelerated growth in specialty fats reflects their increasing importance in trans-fat elimination and clean-label initiatives, particularly as cocoa butter equivalents gain traction amid volatile cocoa prices.

By Form: Liquid Dominance Challenged by Dry Innovation

The market for specialty fats and oils continues to be dominated by liquid forms, which account for 68.92% of the market share in 2025. This preference stems from their practical advantages in food processing operations and the well-established infrastructure for oil refining and distribution. Companies like Cargill have invested in this infrastructure, operating two vegetable oil refineries in Malaysia that specialize in soft oil processing. Food manufacturers, particularly in the confectionery and bakery segments, benefit from the straightforward logistics and integration of liquid specialty oils into their production processes, where temperature-controlled handling ensures consistent product quality.

In contrast, dry specialty fats are emerging as the fastest-growing segment, with an impressive 7.88% CAGR through 2031. This growth is fueled by significant improvements in production methods, particularly in spray-drying and encapsulation technologies. These advancements have addressed key industry challenges by enhancing product stability, extending shelf life, and enabling controlled release applications. The improved protection of sensitive ingredients, such as omega-3 fatty acids, from oxidation has expanded the application potential of dry forms across food, pharmaceutical, and cosmetic industries.

By Functionality: Coating Applications Lead Amid Molding Innovation

The specialty fats market is witnessing significant shifts in its composition, with coating and enrobing fats commanding a substantial 41.98% market share in 2025. These fats play an indispensable role in confectionery and food processing industries, particularly in chocolate manufacturing, where they ensure temperature stability, gloss retention, and optimal snap characteristics for premium products. The spreading and topping fats segment maintains consistent demand in bakery and foodservice applications, where businesses rely on their spreadability and flavor release properties.

The market dynamics are evolving rapidly, with molding and filling fats emerging as the fastest-growing segment at an 8.23% CAGR through 2031. This growth is primarily driven by manufacturers adopting advanced technologies such as 3D food printing and precision molding applications. Additionally, stabilizing and texturizing fats are gaining traction in the expanding dairy alternatives and plant-based products market, where food producers seek to replicate the mouthfeel and structural stability traditionally provided by animal fats.

By Application: Food Dominance Amid Cosmetic Acceleration

The food and beverage industry continues to be the cornerstone of the specialty fats market, commanding a substantial 41.12% market share in 2025. This dominance underscores the critical role these fats play in modern food processing. Meanwhile, the cosmetic and personal care segment has emerged as a dynamic growth area, advancing at 8.05% CAGR through 2031, as manufacturers respond to consumer preferences for natural emollients and sustainable beauty solutions.

The market landscape reveals diverse applications across key sectors. In confectionery, manufacturers are increasingly turning to cocoa butter alternatives to navigate volatile cocoa prices, while bakery products benefit from specialty fats that deliver trans-fat-free solutions without compromising texture or shelf life. The dairy alternatives sector is experiencing notable expansion, with specialty fats enabling plant-based products to achieve traditional dairy characteristics. In the high-value infant nutrition segment, these specialized fats deliver essential fatty acids for cognitive development, with recent regulatory approval of Schizochytrium limacinum oil by EFSA in January 2025 opening new opportunities in infant formula applications .

Geography Analysis

The Asia-Pacific region maintains the largest share of 39.92% in the global specialty fats market through its integrated plantation-to-refinery operations and strong domestic consumption. Indonesia and Malaysia contribute more than 80% of global certified sustainable palm oil, ensuring a consistent supply of traceable specialty fats to European markets. China's domestic soybean production has reached a 20-year peak, but the country retains an 89% import dependency. Japan and Australia have enhanced their market positions by investing in domestic crushing operations, including a new canola processing facility near Perth, which reduces import dependence and improves supply chain stability.

The Middle East & Africa region exhibits the fastest growth rate at 7.41%, supported by government policies that encourage downstream processing investments. Ivory Coast expands its estates while Tanzania attracts private capital due to its agricultural potential. Saudi Arabia strengthens its regional position by developing Jeddah as a specialty oil processing hub. Regional buyers' increasing demand for RSPO-certified materials has enhanced plantation audit processes and satellite monitoring systems.

North America and Europe maintain their market positions through regulatory oversight and consumer education. The United States moves toward its trans-fat ban implementation in August 2025, while Cargill has modified its refineries to comply with RSPO and WHO standards. The European Union's Deforestation Regulation, effective January 2025, mandates geolocation data for imports, encouraging blockchain-based tracking systems. South America sustains its market presence through Brazil's record soybean production and Argentina's biodiesel policies, securing its position in the specialty fats and oils market.

Competitive Landscape

The specialty fats and oils market exhibits moderate competition, with both regional and global companies competing for market share. Companies are enhancing their market positions through vertical integration, managing operations from plantations to processing facilities. This integration enables efficient supply chain control and rapid response to market requirements. The Bunge-Viterra merger exemplifies this trend, forming an agribusiness entity projected to achieve USD 250 million in annual operational synergies through expanded capabilities and product offerings. Bunge's divestment of its European margarines and spreads business to Vandemoortele in March 2025 reflects the industry's strategic focus on specialty fats operations.

Innovation has become a key differentiator in the market, with companies investing significantly in advanced technologies to meet evolving consumer needs. These investments span enzymatic processes, fermentation-based alternatives, and precision agriculture methods to develop sustainable specialty fats. A notable example is Cargill's "Indulgence Redefined" chocolate alternative, which achieves remarkable environmental improvements with a 61% lower carbon footprint and 95% reduced water usage while maintaining the quality consumers expect.

The market continues to evolve with new opportunities emerging in specialized segments. The FDA's approval of cultured pork fat cells opens doors for innovative production methods, while companies like Savor are revolutionizing traditional approaches by producing butter alternatives through unique thermochemical processes. These developments are pushing established manufacturers to adapt and innovate, ensuring the market remains dynamic and responsive to changing consumer preferences.

Specialty Fats and Oils Industry Leaders

Bunge Limited

Cargill, Incorporated

Wilmar International Ltd.

AAK AB

Sime Darby Plantation Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Intercontinental Specialty Fats SDN. BHD. (ISF) and Petchsrivichai Enterprise (PCE) established a joint venture agreement to form Nitthai Specialty Oil and Fats Co., Ltd. The new company aims to enter Thailand's vegetable oil market, specifically targeting the high-value-added segment within the food industry.

- July 2024: Cargill invested USD 50 million to expand its edible oil processing plant in Port Klang, Malaysia. Upon completion in late 2023, the facility will supply finished specialty fats to Asia-Pacific consumers and semi-finished products to Cargill's edible oils facilities in Europe, South America, and North America. This expansion is part of a USD 150 million investment plan.

- April 2024: Nourish Ingredients developed Creamilux, a precision-fermented lipid that replicates dairy fat properties. The product delivers the creamy texture, taste, and emulsification characteristics of dairy fat at low inclusion rates without using animal sources.

Global Specialty Fats and Oils Market Report Scope

Specialty fats and oils have unique properties desired in both industrial and non-edible applications. Specialty fats are also known as hard butter, confectionery fat, and cocoa butter alternatives. Some specialty oils contain a high amount of nutritionally desired components, including essential fatty acids, phytosterol, antioxidants, phospholipids, and other bioactive phenolics.

The specialty fats and oils market is segmented based on type, application, and geography. By type, the market is segmented into specialty fats and specialty oils. The specialty fats segment is further segmented into cocoa butter equivalents (CBE), cocoa butter replacers (CBR), cocoa butter substitutes (CBS), cocoa butter improvers (CBI), milk fat replacers (MFR), and other specialty fats. The specialty oils segment is further segmented into soybean oil, rapeseed oil, palm oil, coconut oil, olive oil, and other oils. By application, the market is segmented into bakery, confectionery, dairy products, infant nutrition, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Specialty Fats | Cocoa Butter Equivalents (CBE) |

| Cocoa Butter Replacers (CBR) | |

| Cocoa Butter Substitutes (CBS) | |

| Cocoa Butter Improvers (CBI) | |

| Milk-fat Replacers (MFR) | |

| Other Specialty Fats | |

| Specialty Oils | Palm Oil |

| Soybean Oil | |

| Rapeseed/Canola Oil | |

| Coconut Oil | |

| Olive Oil | |

| Other Specialty Oils |

| Liquid |

| Dry |

| Molding and Filling Fats |

| Coating and Enrobing Fats |

| Spreading and Topping Fats |

| Stabilizing and Texturizing Fats |

| Food and Beverage | Confectionery |

| Bakery | |

| Dairy and Cheese Analogues | |

| Infant Nutrition | |

| Other Food and Beverage Applications | |

| Cosmetic and Personal Care | |

| Pharmaceutical | |

| Other Industrial Application |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Proudct Type | Specialty Fats | Cocoa Butter Equivalents (CBE) |

| Cocoa Butter Replacers (CBR) | ||

| Cocoa Butter Substitutes (CBS) | ||

| Cocoa Butter Improvers (CBI) | ||

| Milk-fat Replacers (MFR) | ||

| Other Specialty Fats | ||

| Specialty Oils | Palm Oil | |

| Soybean Oil | ||

| Rapeseed/Canola Oil | ||

| Coconut Oil | ||

| Olive Oil | ||

| Other Specialty Oils | ||

| By Form | Liquid | |

| Dry | ||

| By Functionality | Molding and Filling Fats | |

| Coating and Enrobing Fats | ||

| Spreading and Topping Fats | ||

| Stabilizing and Texturizing Fats | ||

| By Application | Food and Beverage | Confectionery |

| Bakery | ||

| Dairy and Cheese Analogues | ||

| Infant Nutrition | ||

| Other Food and Beverage Applications | ||

| Cosmetic and Personal Care | ||

| Pharmaceutical | ||

| Other Industrial Application | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Specialty Fats and Oils Market?

The Specialty Fats and Oils Market reached USD 14.93 billion in 2026 and is projected to hit USD 20.29 billion by 2031.

Which region leads global demand?

Asia-Pacific holds the top position with a 39.92% revenue share, propelled by Indonesia’s biodiesel mandate and robust palm-oil trade with China.

What segment shows the fastest growth?

Molding and filling fats post the quickest 8.23% CAGR through 2031, buoyed by 3D food-printing and precision confectionery.

How are regulatory changes influencing the market?

The FDA’s trans-fat ban and stricter “healthy” label definition intensify demand for reformulated lipids with balanced fatty-acid profiles.

What is the key threat to stable supply?

Volatile raw-material prices—particularly in coconut, palm, and rapeseed oils—pose significant procurement and margin risks for manufacturers.

Page last updated on: