Analytics As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

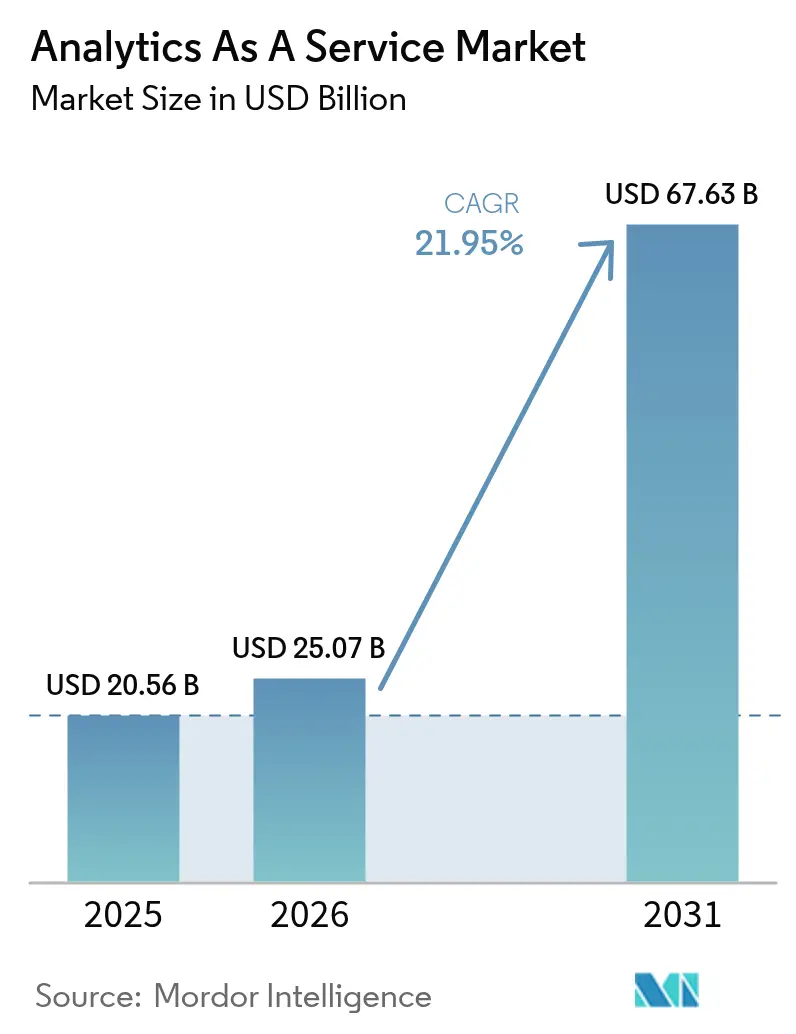

| Market Size (2026) | USD 25.07 Billion |

| Market Size (2031) | USD 67.63 Billion |

| Growth Rate (2026 - 2031) | 21.95% CAGR |

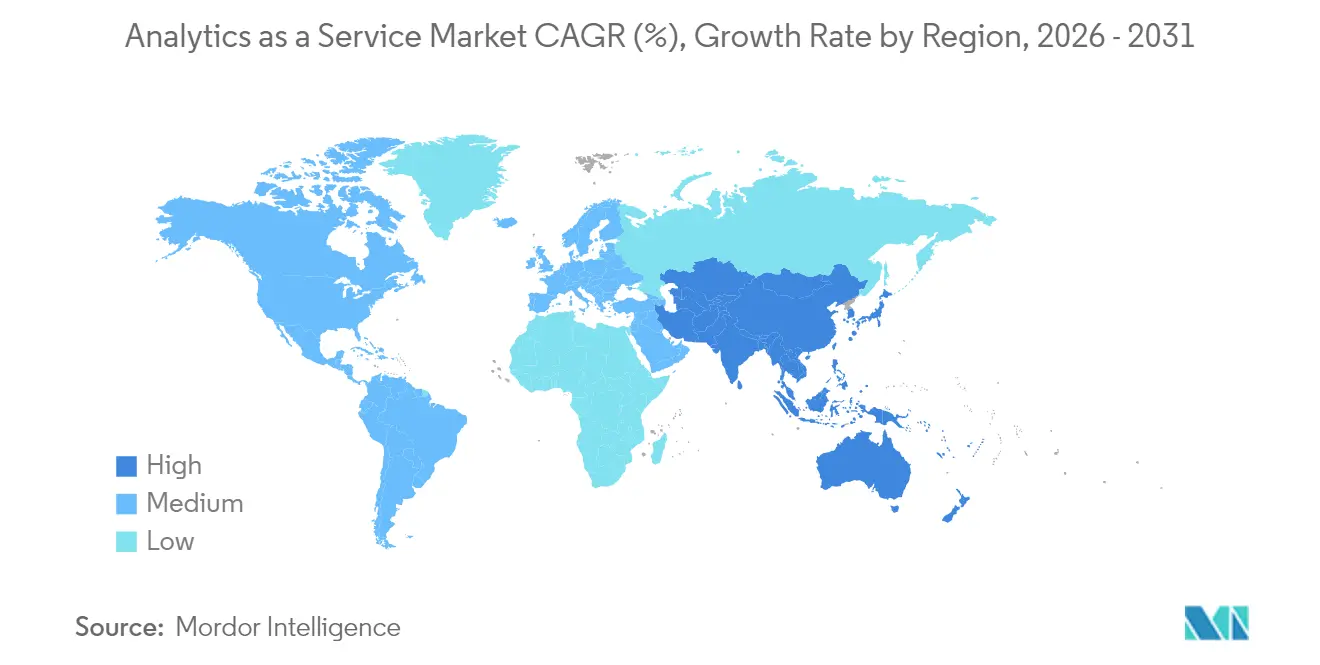

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analytics As A Service Market Analysis by Mordor Intelligence

The Analytics as a Service market size is expected to grow from USD 20.56 billion in 2025 to USD 25.07 billion in 2026 and is forecast to reach USD 67.63 billion by 2031 at 21.95% CAGR over 2026-2031. Demand is rising because cloud-first data-modernization programs allow enterprises to retire on-premises analytics stacks and shift to pay-as-you-go services. The fast spread of vector-native data stores is also enabling real-time processing of unstructured data for generative AI. Public cloud deployments lead today, yet hybrid strategies are advancing as firms balance cost control with data-sovereignty rules. Competitive intensity is mounting as hyperscale platforms deepen AI capabilities while specialist providers focus on vertical solutions and embedded analytics. Talent shortages and data-egress economics, however, continue to influence implementation timelines and ROI calculations.

Key Report Takeaways

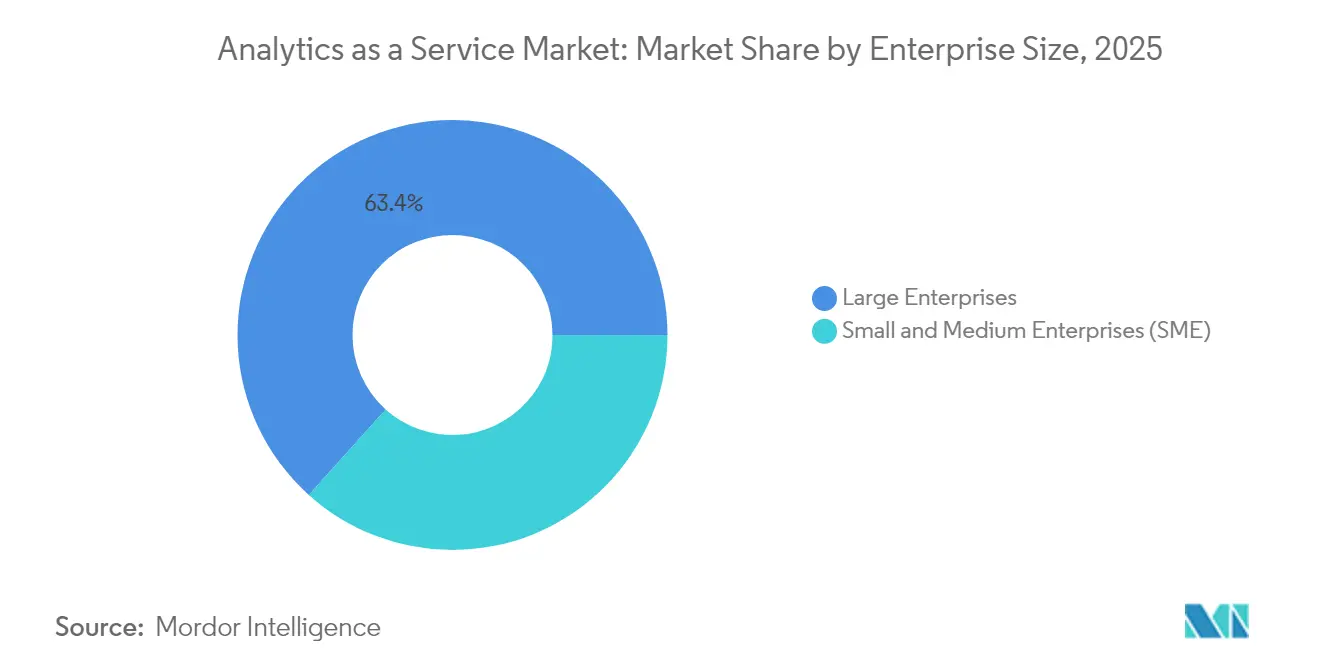

- By enterprise size, Large Enterprises led with 63.35% revenue share in 2025, while SMEs are projected to expand at a 23.40% CAGR through 2031.

- By deployment model, Public Cloud held 47.95% of the Analytics as a Service market share in 2025; Hybrid Cloud is forecast to post the fastest 25.80% CAGR to 2031.

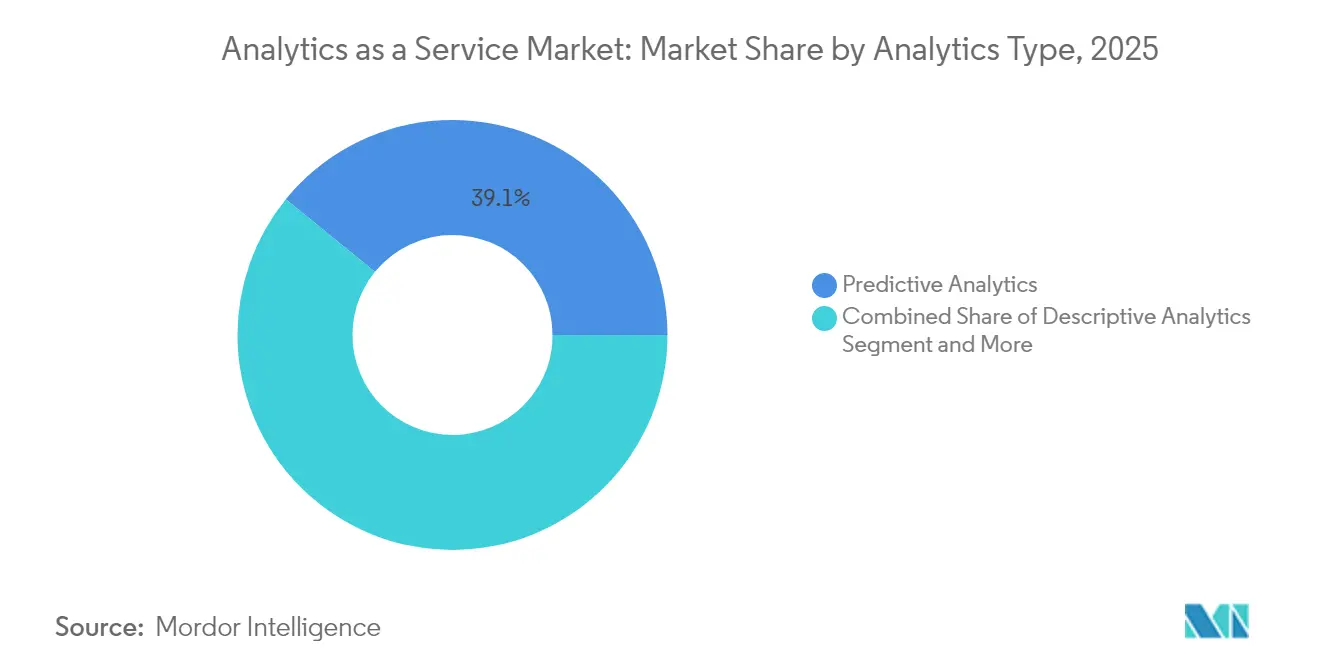

- By analytics type, Predictive Analytics commanded 39.12% of the Analytics as a Service market size in 2025; Prescriptive Analytics is advancing at a 26.10% CAGR through 2031.

- By end-user industry, BFSI accounted for 21.25% share of the Analytics as a Service market size in 2025, while Manufacturing is projected to grow at a 23.30% CAGR to 2031.

- By geography, North America generated 42.35% revenue in 2025; Asia-Pacific is anticipated to deliver the highest 24.60% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Analytics As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first enterprise data-modernization programmes | +9% | Global; strongest in North America and Western Europe | Medium term (2-4 years) |

| Gen-AI-ready vector-native data stores | +6.7% | North America, Western Europe, advanced APAC markets | Short term (≤ 2 years) |

| Pay-as-you-go demand from SMB cloud migrations | +5.6% | Global, emphasis on emerging markets | Medium term (2-4 years) |

| Compliance-driven real-time audit analytics | +4.5% | North America and EU | Medium term (2-4 years) |

| Embedded analytics in vertical SaaS mini-clouds | +3.4% | Global, concentration in North America | Short term (≤ 2 years) |

| Sovereign-cloud mandates driving regional build-outs | +2.2% | EU, APAC, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Enterprise Data-Modernization Programmes

Modernization projects are motivating organisations to consolidate siloed data into cloud-native platforms that support AI-ready pipelines. IBM reports that a majority of large enterprises plan to run most workloads in the cloud by 2025, underscoring a pivot away from legacy data warehouses. [1]IBM, “Optimizing Data Flexibility and Performance with Hybrid Cloud,” ibm.com Vendors position full-stack migration toolkits to simplify workload portability, automate schema conversion, and uphold security controls across multi-region environments. Financial services, healthcare, and retail adopters cite quicker time-to-insight and lower infrastructure overhead as primary benefits. As spending shifts from capital expenditure to operating expenditure, service providers differentiate on transparent pricing, integrated governance, and pre-built AI services to accelerate deployment.

Proliferation of Gen-AI-Ready, Vector-Native Data Stores

Vector databases are helping firms unlock unstructured content for generative AI search, recommendation, and chat experiences. Oracle embedded automated vector stores inside its HeatWave GenAI offering. [2]Oracle, “Oracle Announces In-Database LLMs and Automated Vector Store with HeatWave GenAI,” oracle.com Salesforce followed by enabling vector capabilities in Data Cloud. These integrations simplify similarity queries at scale without separate indexing layers. Enterprises gain the ability to combine text, audio, and image embeddings with transactional data inside a single platform, reducing latency and operational complexity. Early adopters in retail and media use the approach to personalise experiences, while industrial firms employ vector search to refine quality-inspection models. Market entrants emphasise open-source compatibility and orchestrated pipelines that ease model retraining.

Rising Pay-as-You-Go Demand from SMB Cloud Migrations

Flexible consumption models are attracting small and mid-size businesses that lack the capital for on-premises analytics hardware. Leading hyperscalers advertise tiered storage, instant-on compute, and auto-scaling clusters to keep entry costs low. The approach supports incremental adoption: firms can begin with descriptive dashboards, then layer predictive and prescriptive modules as data maturity improves. Industry cloud bundles that package security, compliance, and vertical data models further accelerate uptake among resource-constrained teams. As a result, the Analytics as a Service market is broadening beyond its earlier enterprise focus and adding thousands of new customer logos annually.

Compliance-Driven Real-Time Audit Analytics

Legislations such as the EU Digital Operational Resilience Act and enhanced SEC reporting rules compel organisations to monitor risk indicators continuously rather than via quarterly reviews. MetricStream notes a shift toward integrated GRC platforms that embed analytics into control workflows. Financial institutions deploy streaming analytics to flag anomalous transactions within seconds, reducing remediation time. Vendors enhance their offerings with pre-configured regulatory logic and audit trails that simplify attestation. Demand is notably strong in sectors with high penalty exposure, including banking, telecom, and energy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating hyperscaler egress-fee economics | -6.7% | Global | Medium term (2-4 years) |

| Shortage of FinOps and Data-Ops talent | -5.6% | Global; most acute in emerging markets | Short term (≤ 2 years) |

| Model-explainability regulations delaying roll-outs | -3.4% | EU, North America | Medium term (2-4 years) |

| Carbon-intensity quotas on non-green data centres | -2.2% | EU, selected APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Hyperscaler Egress-Fee Economics

Data-transfer fees can represent 10%–15% of a typical cloud invoice. These charges deter multi-cloud analytics architectures because shifting terabytes between platforms inflates total cost of ownership. The UK Competition and Markets Authority flagged egress fees as a switching barrier. Although some providers have introduced fee waivers under certain conditions, customers still face contractual hurdles. Service integrators now promote architectures that keep large datasets in neutral storage tiers or employ data-in-motion optimisation, such as Rackspace’s Data Freedom offering, claiming up to 85% cost reduction.

Shortage of FinOps and Data-Ops Talent

Ever-expanding cloud feature sets have outpaced the labour market’s ability to supply professionals skilled in cost-governance and automated data-pipeline design. Surveys show that 42% of companies lack FinOps expertise, leading to budget overruns and delayed analytics projects. The skills gap widens in regions where educational pipelines have not kept up with AI and cloud curricula. Enterprises counter by upskilling internal staff, engaging managed-service partners, and adopting low-code workflow orchestration tools. Nonetheless, hiring constraints lengthen implementation timelines and can stall proof-of-concept conversions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: SMEs Accelerate Digital Transformation

Large Enterprises accounted for 63.35% of 2025 revenue as they leverage deep budgets to deploy enterprise-wide data lakes and advanced modelling tools. Their analytics estates often integrate with long-standing ERP and CRM systems, enabling cross-functional dashboards and AI-driven forecasting. Multi-nationals also prioritise sovereignty controls, leading to region-specific deployments that interconnect via private backbone networks.

SMEs contribute a smaller share today yet will record the highest 23.40% CAGR to 2031. Pay-as-you-go pricing and turnkey templates lower barriers for firms without dedicated data-science teams. No-code interfaces, auto-ML services, and packaged vertical analytics help founders draw insights quickly, supporting inventory optimisation and targeted marketing. As SMB adoption broadens, vendors pilot simplified FinOps consoles that map workload cost to business KPIs, fostering transparent budgeting across finance and operations teams. The influx of SMEs broadens the Analytics as a Service market customer base, encouraging providers to release lightweight service tiers and community-led education.

By Deployment Model: Hybrid Strategies Gain Momentum

Public cloud maintained 47.95% of 2025 revenue because its shared infrastructure grants instant elasticity, global reach, and continuous feature upgrades. Start-ups and digital natives rely on fully managed analytics stacks, avoiding data-centre expenditures while accessing the latest AI accelerators. However, firms in regulated industries retain sensitive workloads in private environments to satisfy residency mandates and internal risk policies.

Hybrid architectures are set to expand at a 25.80% CAGR, blending public scalability with private-cloud control. IBM notes that hybrid deployments improve flexibility by letting teams locate data and compute where each performs best. Enterprises commonly stage raw data in private object stores, then burst to public clusters for large-scale model training. This topology mitigates egress fees and supports tiered disaster-recovery postures. As sovereignty requirements rise, providers introduce region-specific sovereign cloud zones and inter-cloud networking services, further reinforcing hybrid appeal within the Analytics as a Service market.

By Analytics Type: Prescriptive Insights Drive Business Value

Predictive Analytics dominated 2025 with 39.12% share as demand forecasting, churn prediction, and risk scoring became core to day-to-day operations. Streaming ingestion, automated feature engineering, and managed ML pipelines lower development overhead, letting business analysts test scenarios without coding expertise.

Prescriptive Analytics will grow fastest at 26.10% CAGR through 2031 thanks to optimisation engines that translate forecasts into concrete actions. IBM highlights use cases in production scheduling, inventory balancing, and logistics planning. Early manufacturing adopters achieved double-digit efficiency gains by adjusting line setups in real time. As more providers embed decision-optimisation solvers into BI dashboards, line-of-business users can run what-if analyses and compare cost, time, and sustainability outcomes. This capability elevates the Analytics as a Service market from insight delivery to direct business impact, accelerating adoption across verticals.

By End-User Industry: Manufacturing Embraces Data-Driven Operations

BFSI generated 21.25% of 2025 revenue by using fraud-detection models, credit-risk scoring, and regulatory surveillance. Banks integrate data lineage and automated reporting to satisfy evolving supervisory expectations. Concurrently, the sector invests in generative-AI chatbots that leverage internal knowledge graphs to improve customer service.

Manufacturing will post a 23.30% CAGR to 2031 as plants digitise machinery and adopt predictive-maintenance analytics. TechTarget notes growing use of digital twins and AI-driven quality inspection to minimise downtime and scrap. Alteryx supports factory data blending that unites sensor streams with procurement and warehouse records. As supply-chain volatility persists, manufacturers rely on real-time dashboards to align production with material availability, thereby tightening inventory cycles and enhancing on-time delivery metrics within the Analytics as a Service market.

Geography Analysis

North America held 42.35% of 2025 revenue, anchored by widespread cloud adoption, mature AI talent pools, and constant product innovation from dominant hyperscalers. United States enterprises in healthcare, retail, and media apply large-scale analytics to personalise experiences, optimise logistics, and drive precision medicine. Government agencies also expand data-sharing initiatives that fuel analytic workloads. Canadian organisations follow with fast uptake of sovereign cloud zones that fulfil public-sector data-residency laws. Mexico’s manufacturing corridors integrate cloud analytics into export-oriented supply chains, closing operational insight gaps.

Asia-Pacific is projected to produce the highest 24.60% CAGR, driven by aggressive digital-economic agendas in China, Japan, India, and Southeast Asia. Rapidly scaling e-commerce platforms ingest terabytes of behavioural data daily, while fintechs roll out credit models targeting underserved populations. Local cloud providers partner with multinational hyperscalers to build regionally compliant infrastructure, lowering latency and enabling sovereign-ready Analytics as a Service market offerings. Government stimulus programmes for smart-factory rollouts further stimulate demand, and SMEs leverage low-cost service bundles to leapfrog legacy systems.

Europe occupies a significant share shaped by privacy and AI governance frameworks. Strict GDPR enforcement and forthcoming EU AI Act rules push firms to deploy explainable models, audit layers, and sovereign cloud controls. AWS announced a Germany-based corporate entity to operate an independent European Sovereign Cloud with launch targeted for late 2025. Financial institutions implement multi-region redundancy to maintain operational resilience, while manufacturers connect IoT data into analytics pipelines that support energy-efficiency targets. The Analytics as a Service market in Europe thus balances innovation with compliance, promoting hybrid patterns that satisfy both business and regulatory imperatives.

Regulatory Landscape

Regulation for Analytics-as-a-Service increasingly combines privacy, data-access, operational resilience, and AI governance requirements that shape how cloud analytics platforms collect, process, and present outputs. In the EU, Regulation (EU) 2024/1689 (AI Act) introduces risk-based obligations, including transparency duties and compliance requirements for high-risk AI use cases, which pushes providers and enterprise deployers to strengthen model documentation, monitoring, and human oversight across analytics workflows.

Data governance obligations also tighten around portability and access. Regulation (EU) 2023/2854 (Data Act) explicitly covers related data services, shaping contractual terms for data sharing and cloud switching, while national and regional sovereign cloud initiatives add procurement and residency constraints for public-sector and regulated workloads. In the United States, NIST work on securing AI systems, including the NISTIR 8605 series and related control-overlay efforts, is being used as a reference point in security and assurance programs, reinforcing expectations for risk controls, auditability, and secure AI pipeline operations in enterprise and government procurement.

Value Chain Analysis

The Analytics-as-a-Service value chain starts with cloud infrastructure and accelerators (compute, storage, networking, and AI stacks), then moves through data management layers (ingestion, integration, catalog and lineage, governance, and lakehouse or warehouse engines) that enable analytics services delivered as subscriptions. Hyperscalers and major platform vendors package these layers into managed services, while specialist analytics providers, embedded BI vendors, and data-collaboration companies differentiate through vertical templates, low-code tooling, and performance-optimized engines. System integrators and managed-service partners sit downstream to design architectures, migrate workloads, and run DataOps and FinOps operating models.

Ecosystem partnerships are a core distribution and delivery mechanism because buyers want interoperable data access, embedded analytics, and operationalized AI in existing systems of record. Recent tie-ups show how value is created and captured across the chain, including LiveRamp partnering with Akkio (April 2026) to add AI capabilities within its data collaboration network, and MediaMelon joining the Akamai Qualified Compute Partner Program (April 2026) to run video analytics on Akamai Cloud, linking edge or cloud compute with real-time analytics delivery. Bottlenecks remain concentrated in upstream data readiness (siloed sources and lineage gaps), talent constraints in DataOps and FinOps, and latency between operational events and data availability, which can delay production deployment even when model tooling is mature.

Competitive Landscape

The Analytics as a Service market shows moderate concentration. AWS leverages its breadth of managed services and partner network to anchor workloads ranging from real-time dashboards to serverless ML. Microsoft capitalises on existing enterprise agreements and tight Office productivity integration to upsell analytics workloads within Azure Synapse and Fabric. Google Cloud differentiates through advanced AI tooling, recently adding multimodal analytics inside BigQuery and Looker.

Specialist providers intensify competition by offering decoupled data layers and performance-optimised engines. Snowflake emphasises cross-cloud collaboration, while Databricks merges data-engineering and lakehouse analytics into a unified platform. Salesforce embeds analytics in its CRM workflow, enhancing data-driven selling. Oracle’s collaboration with AWS to launch Oracle Database@AWS demonstrates a multi-cloud pivot that simplifies enterprise migration paths.

Strategic moves underscore the evolving battleground. AWS committed EUR 7.8 billion to a European Sovereign Cloud scheduled for Brandenburg to satisfy local residency mandates. IBM unveiled watsonx Orchestrate and watsonx.data to weave data-fabric governance with lakehouse economics. Nvidia’s 2025 GTC announcements introduced Blackwell Ultra GPUs on Azure and Google Cloud, aiming to accelerate generative-AI workloads that underpin advanced analytics services. These examples highlight how hardware, software, and ecosystem partnerships shape differentiation within the Analytics as a Service market.

Emerging white-space lies in industry-specific accelerators, embedded analytics for SaaS platforms, and privacy-preserving computation that complies with cross-border data regulations. Vendors that package domain data models, curated feature stores, and low-code interfaces are well-positioned to win adoption among non-technical business users.

Analytics As A Service Industry Leaders

Amazon Web Services

Microsoft Corporation

Google Cloud (Alphabet Inc.)

IBM Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity lies in real-time analytics that supports compliance and auditability across regulated industries and geographies with sovereignty constraints. The EU AI Act and the EU Data Act elevate requirements around transparency, monitoring, and data access, reinforcing demand for analytics services that embed policy controls, lineage, and explainability, rather than treating governance as add-on tooling. In parallel, sovereign-cloud initiatives in Europe keep driving localized deployment patterns and hybrid operating models, creating room for providers to deliver consistent analytics capabilities across multiple regions while meeting residency and procurement rules.

Another opportunity is zero-copy and agent-enabled analytics that reduces data replication and makes enterprise systems of record usable for AI-driven decision workflows without duplicating sensitive datasets. Vendor moves in 2026 provide concrete signals of this direction, including SAP Business Data Cloud (BDC) Connect integrations announced with AWS (Athena) and with Google Cloud (BigQuery), which focus on bi-directional, governed access to SAP business data for analytics and AI use cases. As platforms and partners expand these integration patterns, differentiation shifts toward secure interoperability, operational cost control (including egress-aware architectures), and packaged vertical solutions that shorten time-to-value for both large enterprises and SMEs.

Recent Industry Developments

- July 2026: Cloudera and VAST Data announced a strategic partnership to integrate Cloudera's containerized data services with the VAST Data AI Operating System for enterprise analytics and AI training. The combined approach targets hybrid and multi-environment deployments, aligning with enterprise demand for unified data and AI stacks that can run consistently across infrastructure choices.

- May 2026: SAP and AWS announced development of SAP Business Data Cloud (BDC) Connect for Amazon Athena to enable bi-directional, zero-copy data sharing between SAP BDC and AWS services. The integration reduces data duplication and accelerates governed analytics on SAP data, supporting modern data-product and AI use cases inside enterprise workflows.

- September 2024: Oracle added an Intelligent Data Lake with generative-AI analytics to its Data Intelligence Platform. The update strengthened Oracle's integrated data-to-insight proposition for cloud buyers looking to combine governed data management with GenAI-enabled analytics capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the analytics as a service market covers vendor revenues earned from delivering analytics capabilities through a cloud or service-based model, where customers access tools and outcomes on a subscription or consumption basis.

Scope exclusions: We exclude pure hardware resale and standalone one-off consulting or support work when it is not bundled into the recurring service subscription.

Segmentation Overview

- By Enterprise Size

- Small and Medium Enterprises (SME)

- Large Enterprises

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Analytics Type

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- By End-user Industry

- IT and Telecommunication

- BFSI

- Healthcare and Life-Sciences

- Retail and E-Commerce

- Manufacturing

- Energy and Utilities

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helps us set the fact base on cloud adoption, enterprise IT spending patterns, and digital economy growth, before we build the sizing model. We refer to public sources such as OECD digital economy indicators, World Bank macro series, ITU connectivity metrics, and national statistics offices for baseline business and ICT signals. We also use materials such as SEC filings, annual reports, earnings call transcripts, and investor presentations to understand how service-led analytics revenues are described, and where they sit inside wider cloud and software lines.

To cross-check supply-side context, we review sources such as WTO trade statistics for related ICT equipment signals, WIPO patent databases for analytics and AI filing trends, and reputable industry association publications on cloud, data, and security topics. A paid subscription for company financials and intelligence is used selectively to standardize segment mapping where disclosures differ, and a paid patent database is used to speed up keyword validation. These desk sources are not exhaustive, and we also used other public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and survey responses are used to pressure-test the desk assumptions around what buyers pay for in an AaaS contract, how pricing moves with usage and seats, and which delivery elements are typically bundled. We speak with a mix of service providers, cloud-focused analytics teams, channel partners, and enterprise buyers across APAC, EMEA, and the Americas, then we re-check differences by company size and by regulated versus non-regulated industries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 41% |

| Mid tier: 50% | Functional/Unit leaders: 25% | EMEA: 36% |

| Smaller Players: 16% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that reconstructs addressable spend from cloud and analytics adoption signals, and then it is narrowed to service-based delivery. Inputs we rely on include enterprise cloud penetration, analytics workload migration trends, average contract duration, seat and usage mix (user-based versus consumption-based), and the share of spending going to recurring subscriptions versus project-only work. Where public data is reported in mixed categories, we apply assumptions only after checking patterns through interviews and disclosure language.

After the top-down build, totals are corroborated using selective bottom-up approximations, such as sampled vendor revenue disclosures mapped to AaaS, channel checks on typical annual contract value by region, and simple ASP times volume sanity checks using enterprise counts by size band. When smaller-provider disclosures are limited, gaps are handled through conservative cohorting by geography and customer segment, then adjusted based on primary feedback. For forecasting, we use scenario analysis supported by regression-style sensitivity on drivers like cloud spending growth, AI-enabled analytics adoption, and compliance-led demand, followed by an analyst review so the trajectory stays realistic.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including cloud spending direction, vendor commentary on recurring revenue mix, and observed pricing changes in renewal cycles. If a region or year shows an unusual jump, we revisit the assumptions behind adoption, pricing, or bundling and trigger follow-up calls where needed. Before sign-off, the model and key inputs go through multi-step analyst checks so arithmetic, currency timing, and scope logic are consistent.

The report is refreshed annually, and interim updates are made when major market events materially change demand or pricing assumptions. Right before delivery, a final pass is completed so clients receive the most current version of the market view.

Mordor Intelligence's Global Analytics As A Service Market Market Size Compared With Other Published Estimates

Published numbers for analytics as a service can vary because teams do not always count the same revenue lines, and they may also choose different base years and currency timing. Differences also come from how recurring subscriptions are separated from one-off project work, and how regional coverage is handled in the final roll-up.

The benchmark table shows a higher 2026 value than some 2024-based estimates, and in Mordor Intelligence's model the total is built from subscription-led analytics delivery across public, private, and hybrid deployments, while excluding pure implementation-only or hardware-tied revenue when it is not part of the recurring service line.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.07 B (2026) | |

| Global Consultancy A | USD 11.32 B (2024) | Uses an earlier base year and does not clearly state whether recurring subscriptions are separated from project-only analytics services, which can compress the counted spend for later years. |

| Market Publisher B | USD 13.57 B (2024) | Provides limited disclosure on inclusions and may mix software, services, and adjacent analytics offerings, and the 2024 starting point leads to a different currency timing and adoption ramp versus a 2026 anchored model. |

Taken together, the spread is mainly explained by timing, plus how each publisher treats bundled services versus standalone projects. Our approach stays traceable because the counted revenue is tied back to recurring service delivery signals, pricing logic, and validation checks collected during interviews, which can be repeated when the market is updated.

Key Questions Answered in the Report

What is the current size of the Analytics as a Service market?

The market is valued at USD 25.07 billion in 2026 and is forecast to reach USD 67.63 billion by 2031.

Which region generates the highest revenue today?

North America leads with 42.35% of 2025 revenue, driven by advanced cloud infrastructure and early AI adoption.

Which deployment model is growing fastest?

Hybrid cloud deployments are projected to expand at a 25.80% CAGR between 2026-2031 as firms balance flexibility and data sovereignty.

Why are vector-native databases important for Analytics as a Service?

They enable efficient similarity search across unstructured data, supporting generative-AI workloads and reducing integration complexity.

Which end-user industry will deliver the fastest growth?

Manufacturing is expected to grow at a 23.30% CAGR through 2031 owing to predictive maintenance, quality analytics, and supply-chain optimisation.

What are the main restraints affecting market growth?

Rising data-egress fees and a shortage of FinOps and Data-Ops professionals can increase costs and delay project rollouts.

Page last updated on: