Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

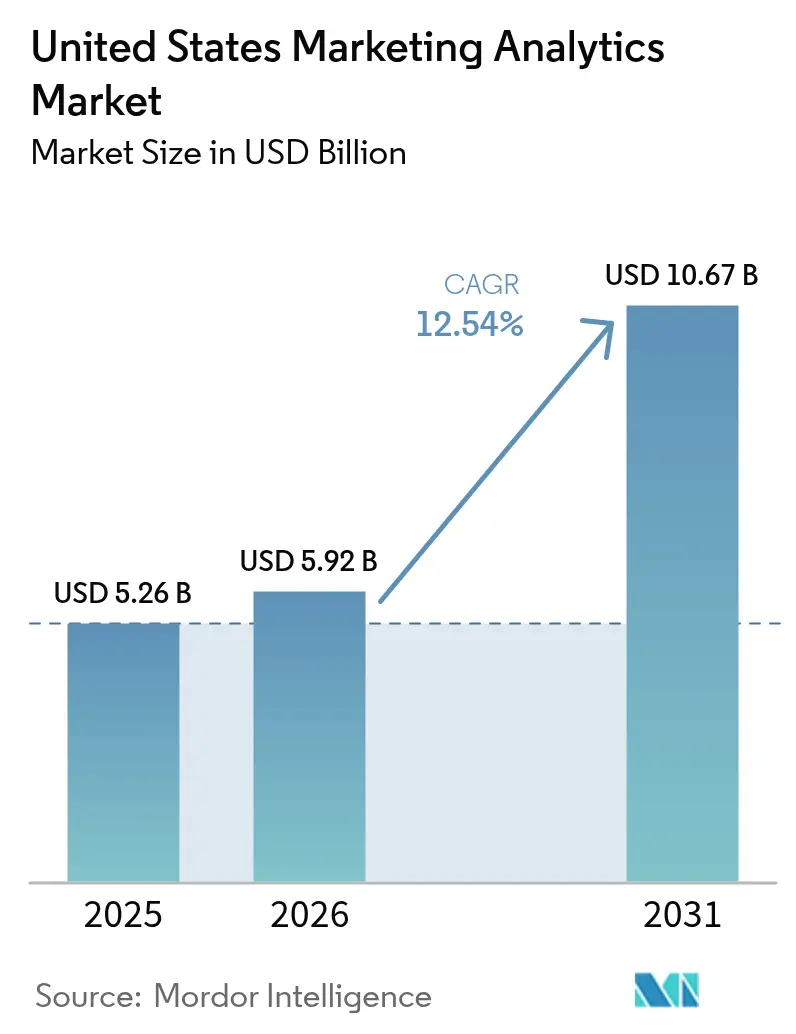

| Base Year Market Size (2025) | USD 5.26 Billion |

| Market Size (2026) | USD 5.92 Billion |

| Market Size (2031) | USD 10.67 Billion |

| Growth Rate (2026 - 2031) | 12.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Marketing Analytics Market Analysis by Mordor Intelligence

The United States marketing analytics market size was valued at USD 5.26 billion in 2025 and estimated to grow from USD 5.92 billion in 2026 to reach USD 10.67 billion by 2031, at a CAGR of 12.54% during the forecast period (2026-2031). This expansion stems from enterprises shifting away from intuition-based campaigns toward data-anchored attribution that links every dollar spent across digital and offline channels. Demand is reinforced by accelerated cloud migration, heightened first-party data strategies in response to state-level privacy statutes, and growing use of real-time personalization engines that improve conversion rates while respecting consumer consent signals.[1]Interactive Advertising Bureau, “First-Party Data Strategies for 2024,” iab.com Vendor competition is intensifying as incumbents embed generative AI into marketing suites and product-analytics specialists court mid-market buyers through consumption-based pricing. Meanwhile, talent shortages and a fragmented privacy landscape pressure platforms to automate data preparation and adopt privacy-preserving techniques that unlock aggregate insights without exposing individual-level records.

Key Report Takeaways

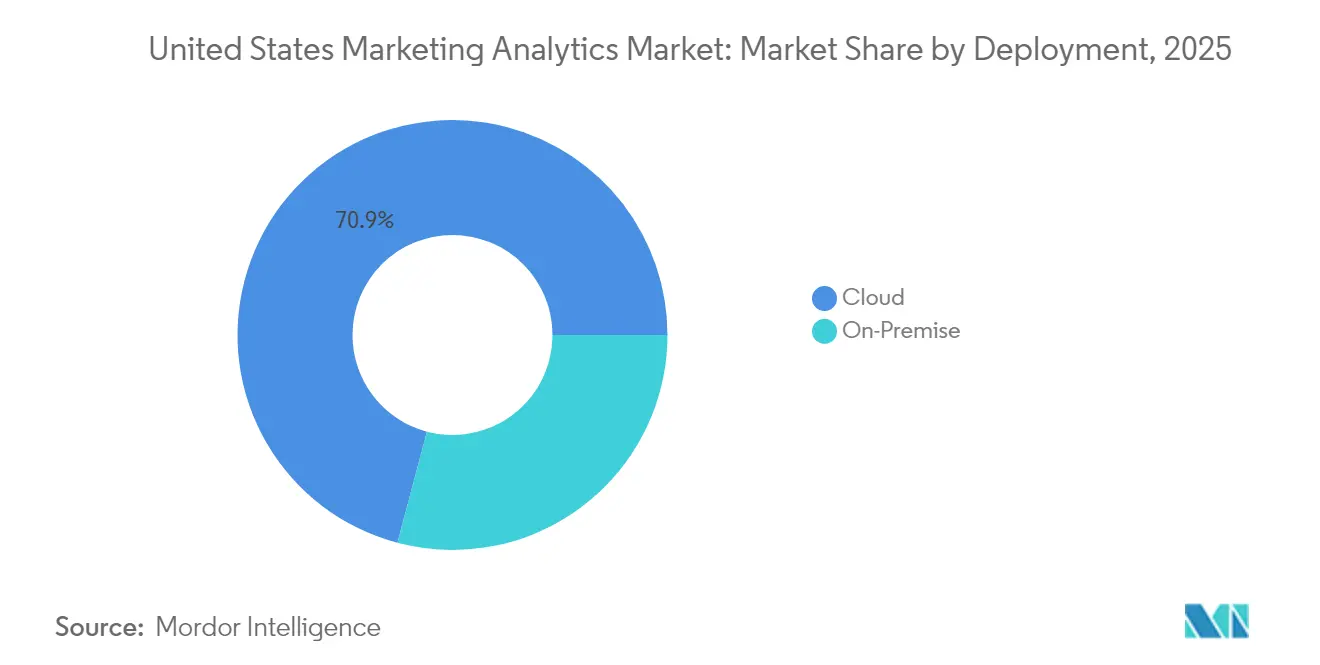

- By deployment, cloud commanded 70.88% of United States marketing analytics market share in 2025, and the segment is advancing at a 13.74% CAGR through 2031.

- By analytics type, predictive analytics held 34.35% share of the United States marketing analytics market size in 2025, while prescriptive analytics is forecast to expand at 13.28% CAGR to 2031.

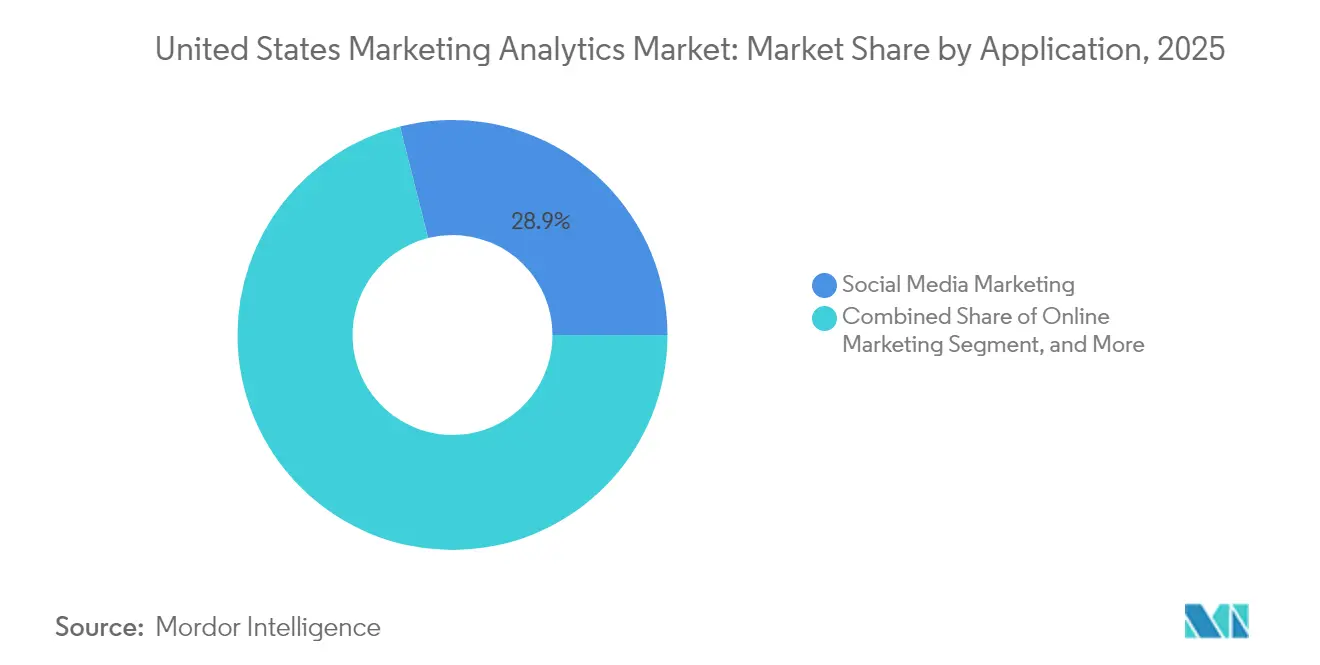

- By application, social media analytics captured 28.93% spending in 2025 and is growing at a 12.98% CAGR through 2031.

- By end user, retail led with 22.19% revenue share in 2025; healthcare is recording the highest projected CAGR at 13.12% to 2031.

- Adobe, Salesforce, Microsoft, Oracle, and IBM together held a moderate share, leaving room for specialists such as Amplitude and Mixpanel to capture price-sensitive mid-market demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Marketing Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Need to Utilize Marketing Budgets for an Effective ROI | +2.8% | National, concentrated in Northeast financial services and West Coast technology hubs | Medium term (2-4 years) |

| Adoption of Cloud Technology and Big Data | +3.2% | National, with accelerated uptake in South retail corridors and Midwest manufacturing clusters | Short term (≤ 2 years) |

| Proliferation of Social Media Channels | +2.1% | National, strongest in West Coast and Northeast urban markets | Short term (≤ 2 years) |

| Growing Regulatory Focus on First-Party Data Strategies | +1.9% | National, led by California, Virginia, Colorado early adopters | Medium term (2-4 years) |

| Accelerated Shift to Real-Time Personalization Engines | +2.3% | National, early gains in e-commerce and travel verticals | Short term (≤ 2 years) |

| Emergence of Privacy-Preserving Analytics Frameworks | +1.2% | National, with pilot deployments in healthcare and financial services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Need to Utilize Marketing Budgets for an Effective ROI

Boards are scrutinizing discretionary spending, prompting chief marketing officers to demonstrate the direct contribution of every campaign to revenue. The Duke CMO Survey showed that martech utilization remained below 40% in Fall 2024, even as budgets held steady at 9.1% of firm revenue, underscoring a gap between investment and realized value.[2]Christine Moorman, “CMO Survey Results: Fall 2024,” cmosurvey.org Unified dashboards that consolidate data from advertising, CRM, and commerce platforms are replacing siloed point solutions, enabling multi-touch attribution and lifetime-value modeling. Vendors offering no-code connectors shorten implementation windows from quarters to weeks, making advanced analytics accessible to non-technical teams. As return-on-ad-spend becomes the North Star metric, enterprises that operationalize analytics experience faster budget approval cycles and higher campaign velocity.

Adoption of Cloud Technology and Big Data

Elastic cloud infrastructure has become the default for martech workloads, with 71% of enterprises migrating at least one marketing analytics process to the cloud in 2024, up from 58% in 2023. Cloud data lakes ingest streaming web, mobile, and point-of-sale events, then execute machine-learning models that create micro-segments in real time. Partnerships such as Snowflake’s integration with Adobe Experience Platform allow activation of first-party data without duplicating storage, cutting latency and reducing cost. Open-source engines like Apache Spark now power incremental processing that updates profiles within seconds rather than overnight batches. These architectural gains translate into agile experimentation and faster feedback loops.

Proliferation of Social Media Channels

Closed-loop application programming interfaces (APIs) from TikTok, Meta, and LinkedIn bypass browser cookies and deliver deterministic attribution, restoring marketer confidence in social media spend. As short-form video and influencer collaborations mature, brands need granular metrics covering reach, engagement, and conversion. Server-side event transmission improves match rates even when users block tracking scripts, allowing advertisers to optimize creative variants in near real time. Growing creator economies further push enterprises to synthesize platform data with first-party customer identifiers, deepening demand for adaptable analytics pipelines.

Growing Regulatory Focus on First-Party Data Strategies

Nineteen states enacted consumer-data statutes by 2024, each mandating distinct consent, deletion, and opt-out rules. California’s Privacy Rights Act requires honoring browser-based opt-out signals, compelling server-to-server data pipelines that respect jurisdiction boundaries. Consequently, 68% of U.S. advertisers prioritized first-party data infrastructure in 2024, investing in consent management, identity resolution, and customer data platforms. Brands that consolidate CRM, commerce, and service interactions unlock higher match rates, boosting audience addressability while maintaining compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Implementation and System Integration Issues | -1.8% | National, acute in mid-market enterprises with legacy infrastructure | Short term (≤ 2 years) |

| Availability of Feature-Rich Open-Source Tools | -0.9% | National, concentrated in technology and startup sectors | Medium term (2-4 years) |

| Increasing State-Level Consumer Data-Protection Statutes | -1.4% | National, led by California, Virginia, Colorado, Connecticut, Utah | Medium term (2-4 years) |

| Talent Shortage in Advanced Analytics and Data Engineering | -1.6% | National, most severe in Midwest and South regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Implementation and System Integration Issues

Deploying a full-stack analytics solution requires software licenses, cloud resources, data engineering, and change management. Mid-market firms often manage more than 90 marketing applications, which creates fragmented schemas and duplicate customer identifiers that inflate the labor needed for integration. Cloud spending can also exceed projections as data volumes surge, prompting finance teams to re-examine total cost of ownership. Vendors now respond with bundled managed services, consumption-based pricing, and pre-built connectors, yet the up-front lift still delays time-to-insight for resource-constrained buyers.

Increasing State-Level Consumer Data-Protection Statutes

The absence of federal privacy legislation has produced a patchwork of rules defining “sale,” “sharing,” and “targeted advertising” differently across states. Enterprises must embed jurisdiction logic that triggers unique consent flows based on user location, raising engineering complexity and compliance risk. The need to audit vendor data usage and honor deletion requests within 30-day windows adds operational overhead. Platforms now bake consent checks into audience activation, but suppressing records for opt-out users reduces reachable audience size and can impair cross-channel measurement accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Extends Its Lead

The United States marketing analytics market size for cloud deployment stood at USD 3.73 billion in 2025 and is forecast to rise at a 13.74% CAGR, cementing its dominance over on-premise alternatives. Cloud captured 70.88% of United States marketing analytics market share in 2025, reflecting enterprises’ preference for elastic capacity, automatic feature releases, and usage-based billing. Cost avoidance from hardware refresh cycles and data-center overhead further tilts investment toward infrastructure-as-a-service.

Major providers now offer HIPAA-eligible environments, FedRAMP authorizations, and SOC 2 Type II attestations, giving compliance teams confidence to migrate regulated workloads. Even highly regulated sectors are piloting hybrid architectures that keep sensitive data on-premise while offloading compute-intensive analytics to the cloud. Machine-learning services embedded within the same environment reduce data-movement costs and speed model deployment, a benefit resonating with mid-market firms lacking data-science headcount.

By Analytics Type: Prescriptive Models Move Front and Center

Predictive analytics maintained the largest slice of the United States marketing analytics market size at USD 1.81 billion in 2025, equal to 34.35% share in 2025. Prescriptive analytics, however, is expanding at a 13.28% CAGR, reflecting marketer appetite for automated next-best-action recommendations that close the gap between insight and activation. Prescriptive engines evaluate permutations of send times, offer values, and creative variants, then trigger the highest-yield action in real time.

AutoML tooling embedded in cloud platforms automates feature engineering and model tuning, democratizing access for teams with limited data-science resources. Diagnostic and descriptive analytics remain table stakes for executive reporting, yet their reactive nature limits strategic impact. As algorithmic decision-making permeates daily operations, governance processes around explainability and bias review are becoming standard, particularly in financial-services and healthcare use cases.

By Application: Social Media Analytics Sustains Double-Digit Growth

Social media analytics represented USD 1.52 billion of United States marketing analytics market size in 2025 and is on track for a 12.98% CAGR through 2031. Closed-loop APIs from Meta, TikTok, and LinkedIn now allow hashed first-party identifiers to be sent server-side, increasing match accuracy even when cookies are blocked. Brands newly confident in post-privacy measurement are reallocating budget toward influencer collaborations and short-form video ads.

Email analytics follows closely, driven by predictive send-time optimization and content recommendation that raise open and click rates. Content-marketing analytics focusing on organic search and thought-leadership performance harness natural-language processing to gauge sentiment and topic resonance. Offline measurement tying store visits to digital exposures gains traction within omnichannel retail, though state privacy rules constrain certain location-based techniques, prompting wider adoption of consent-centric data collection.

By End User: Healthcare Accelerates, Retail Retains the Crown

Retail accounted for 22.19% of United States marketing analytics market share in 2025, relying on analytics to cut acquisition costs and synchronize promotions across web, mobile, and store touchpoints. Healthcare, although smaller in absolute terms, is growing at the fastest rate of 13.12% CAGR as providers leverage patient portals and telehealth platforms that generate behavioral data suitable for personalization. HIPAA rules require rigorous consent and de-identification, so vendors offer configuration toggles that isolate protected health information in secure enclaves.

BFSI firms adopt analytics to enhance credit-card acquisition and deposit growth, but compliance teams vet algorithms for fair lending adherence. Education, manufacturing, and travel each exploit analytics to refine enrollment funnels, partner programs, and dynamic pricing, respectively. Cross-vertical momentum underlines how the United States marketing analytics market continues to broaden its footprint beyond digital-native pioneers.

Geography Analysis

West-coast states dominate adoption owing to the density of technology headquarters in California and Washington. Early exposure to the California Consumer Privacy Act pushed companies to develop first-party data frameworks ahead of peers, sharpening the region’s competitive edge in cookieless measurement. Product analytics vendors such as Amplitude and Mixpanel thrive here, serving software-as-a-service firms that demand granular funnel insights.

The Northeast follows, led by New York’s concentration of banking, insurance, and healthcare systems. Financial institutions deploy consent-aware analytics that audit algorithmic decisions and log data lineage, meeting examiners’ expectations. Boston-area hospitals employ engagement platforms that respect HIPAA while personalizing appointment reminders and wellness content.

Southern and Midwestern enterprises are accelerating investment as retail chains headquartered in Texas and Georgia unify in-store and e-commerce data streams. Manufacturing clusters in Illinois and Ohio integrate channel-partner analytics to forecast distributor demand, though talent shortages slow adoption compared with coastal hubs. States such as Virginia, Colorado, and Utah enforce unique privacy provisions, compelling firms operating nationwide to implement the strictest protocol across all geographies to avoid non-compliance.

Competitive Landscape

The United States marketing analytics market balances established platform vendors and nimble specialists. Adobe, Salesforce, Microsoft, Oracle, and IBM cross-sell analytics modules into existing CRM, commerce, and content portfolios, simplifying procurement for global brands. Microsoft’s Copilot lets marketers craft segments via natural language, while Adobe’s GenStudio auto-produces creative assets consistent with brand standards.

Mid-market share shifts toward consumption-priced specialists such as Amplitude, Mixpanel, and Heap. Their event-centric data models excel for digital products where user journeys unfold inside web or mobile applications. No-code analytics lowers barriers, enabling product managers to run cohort analyses without SQL. Yet enterprise buyers weigh these gains against concerns around feature depth, global support, and governance.

White-space opportunity surfaces in privacy-preserving analytics. Techniques such as differential privacy and federated learning remain nascent but promise compliant cross-brand insights without raw-data exchange. Vendors also race to embed low-code orchestration that auto-pushes insights into ad networks and email services, critical for marketers who lack engineering bandwidth. As talent scarcity persists, ease of deployment and automated model maintenance will increasingly separate leaders from laggards.

United States Marketing Analytics Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Salesforce Inc.

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft enabled Copilot AI to auto-generate testing hypotheses for email campaigns within Dynamics 365 Customer Insights.

- October 2024: Microsoft expanded Copilot AI capabilities inside Dynamics 365, allowing natural-language segment creation and journey orchestration.

- September 2024: Salesforce unveiled Agentforce, an AI agent platform integrated with Data Cloud to automate multi-step marketing workflows.

- June 2024: Adobe introduced GenStudio, a generative AI application that drafts email copy, social posts, and display ads while enforcing brand compliance.

United States Marketing Analytics Market Report Scope

Marketing analytics software aid a company in tracking the data pertaining to traffic leads and sales. Implementing marketing analytics helps the person of interest compare various mediums of operation, such as social media vs. blogging vs. email marketing. These analytics also aid in diagnosing the difficulties faced in a particular channel and the tactical steps needed to improve the background.

The United States Marketing Analytics Market Report is Segmented by Deployment (Cloud and On-Premise), Analytics Type (Descriptive Analytics, Diagnostic Analytics, Predictive Analytics, and Prescriptive Analytics), Application (Online Marketing, E-Mail Marketing, Content Marketing, Social Media Marketing, and Other Applications), End User (Retail, Banking Financial Services and Insurance, Education, Healthcare, Manufacturing, Travel and Hospitality, and Other End Users), and Geography (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment

| Cloud |

| On-Premise |

By Analytics Type

| Descriptive Analytics |

| Diagnostic Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

By Application

| Online Marketing |

| E-Mail Marketing |

| Content Marketing |

| Social Media Marketing |

| Other Applications |

By End User

| Retail |

| Banking, Financial Services and Insurance |

| Education |

| Healthcare |

| Manufacturing |

| Travel and Hospitality |

| Other End Users |

| By Deployment | Cloud |

| On-Premise | |

| By Analytics Type | Descriptive Analytics |

| Diagnostic Analytics | |

| Predictive Analytics | |

| Prescriptive Analytics | |

| By Application | Online Marketing |

| E-Mail Marketing | |

| Content Marketing | |

| Social Media Marketing | |

| Other Applications | |

| By End User | Retail |

| Banking, Financial Services and Insurance | |

| Education | |

| Healthcare | |

| Manufacturing | |

| Travel and Hospitality | |

| Other End Users |

Key Questions Answered in the Report

What was the value of the United States marketing analytics market in 2026?

It reached USD 5.92 billion and is forecast to climb to USD 10.67 billion by 2031 at a 12.54% CAGR.

Which deployment model leads spending?

Cloud deployment led with 70.88% share in 2025 and is expanding at a 13.74% CAGR as enterprises migrate from on-premise stacks.

Which application area is expanding fastest?

Social media analytics is growing at a 12.98% CAGR as platforms provide server-side APIs for accurate attribution.

Why is healthcare the fastest-growing vertical?

Patient portals and telehealth generate rich behavioral data, and vendors offer HIPAA-ready solutions, pushing healthcare to a 13.12% CAGR.

How are state privacy laws affecting analytics strategies?

A patchwork of 19 statutes forces companies to adopt first-party data frameworks and consent management systems to stay compliant.

What role does AI play in vendor differentiation?

Leading platforms embed generative and prescriptive AI to automate content creation, segmentation, and next-best-action orchestration, reducing manual effort.

Page last updated on: