Castor Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 2.40 Billion |

| Market Size (2030) | USD 3.09 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Castor Oil Market Analysis by Mordor Intelligence

The castor oil market size stands at USD 2.4 billion in 2025 and is forecast to reach USD 3.09 billion by 2030, advancing at a 5.20% CAGR. Momentum comes from the rapid shift toward bio-based chemicals, stricter rules that reward renewable feedstocks, and widening use of castor derivatives in electric-vehicle thermal fluids, cosmetics, and sustainable aviation fuels. India’s export-oriented supply base, Africa’s new cultivation projects, and rising vertical integration among major processors collectively underpin long-term supply security even as weather-linked volatility persists. Clean-label preferences in North America and Europe accelerate the adoption of hydrogenated and Jamaican Black variants, while regulatory clarity under the FDA’s Modernization of Cosmetics Regulation Act lowers compliance risk for natural oils. Corporate divestitures and downstream acquisitions are reshaping competitive dynamics, with leading suppliers deploying sustainability programs that certify farmers and cut water use—moves that enhance traceability and justify premium pricing.

Key Report Takeaways

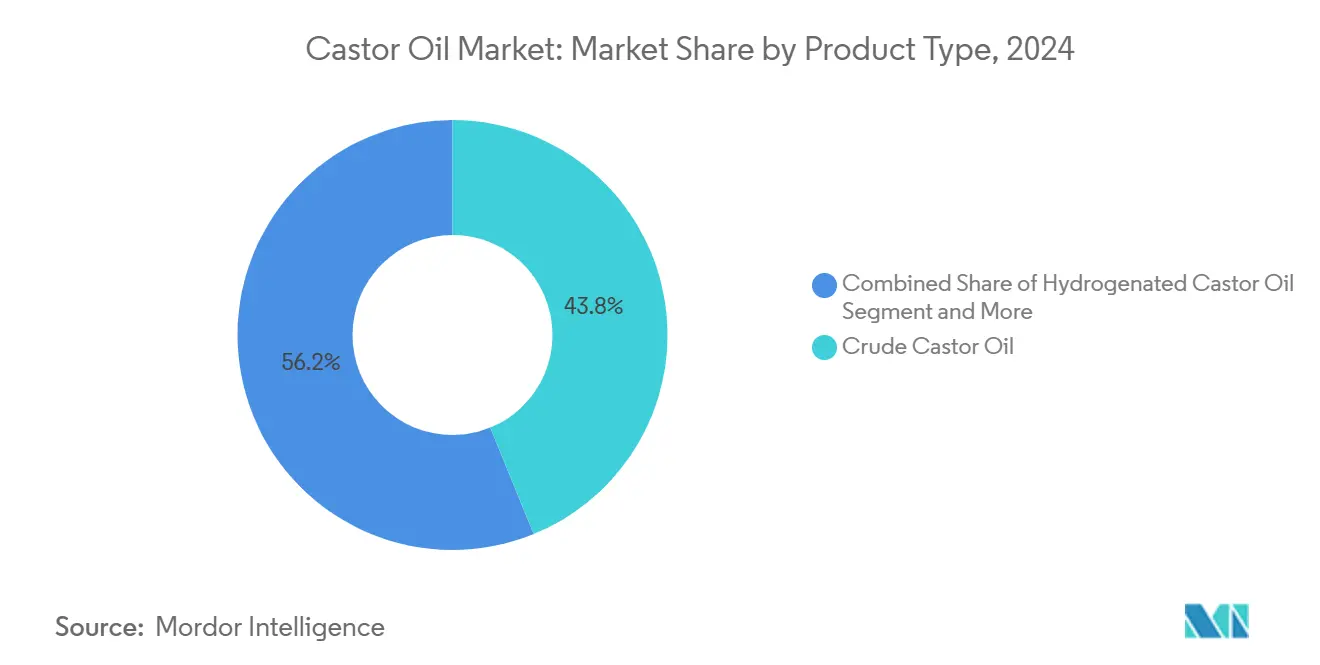

- By product type, crude castor oil led with 44.27% revenue share in 2024, while Jamaican Black castor oil is projected to expand at a 7.48% CAGR to 2030.

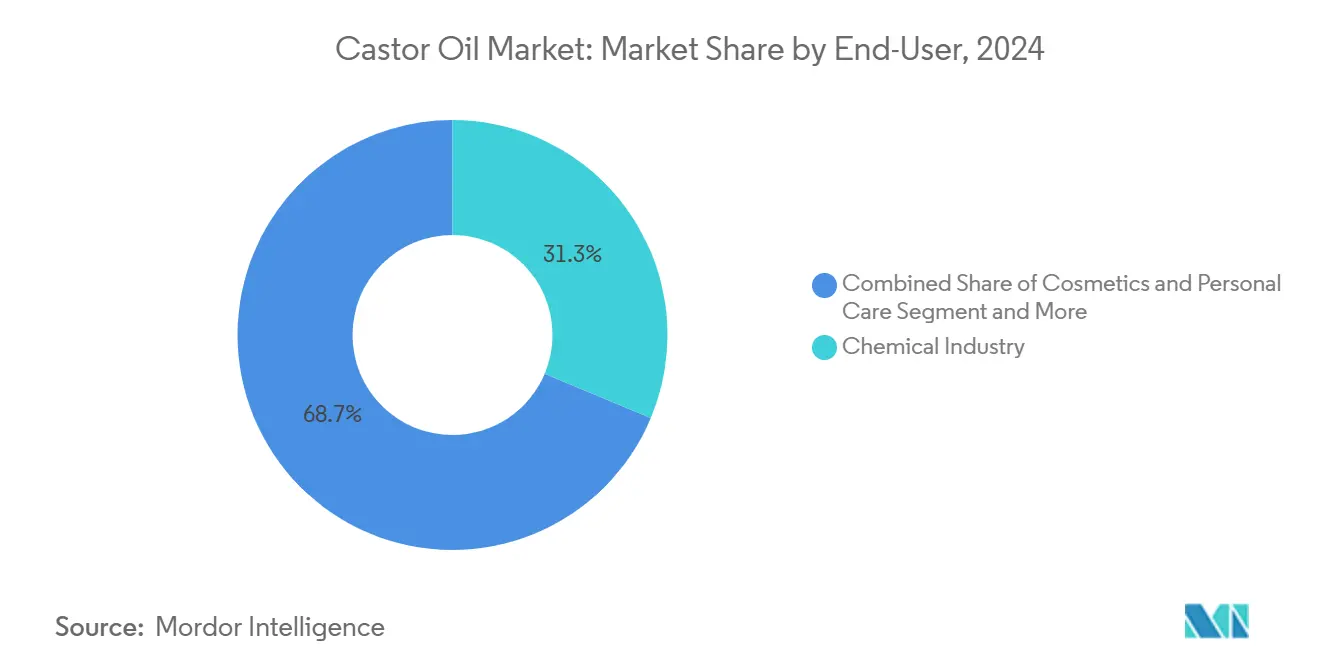

- By end-user, the chemical industry accounted for 31.63% share of the castor oil market size in 2024, and cosmetics and personal care are advancing at a 6.74% CAGR through 2030.

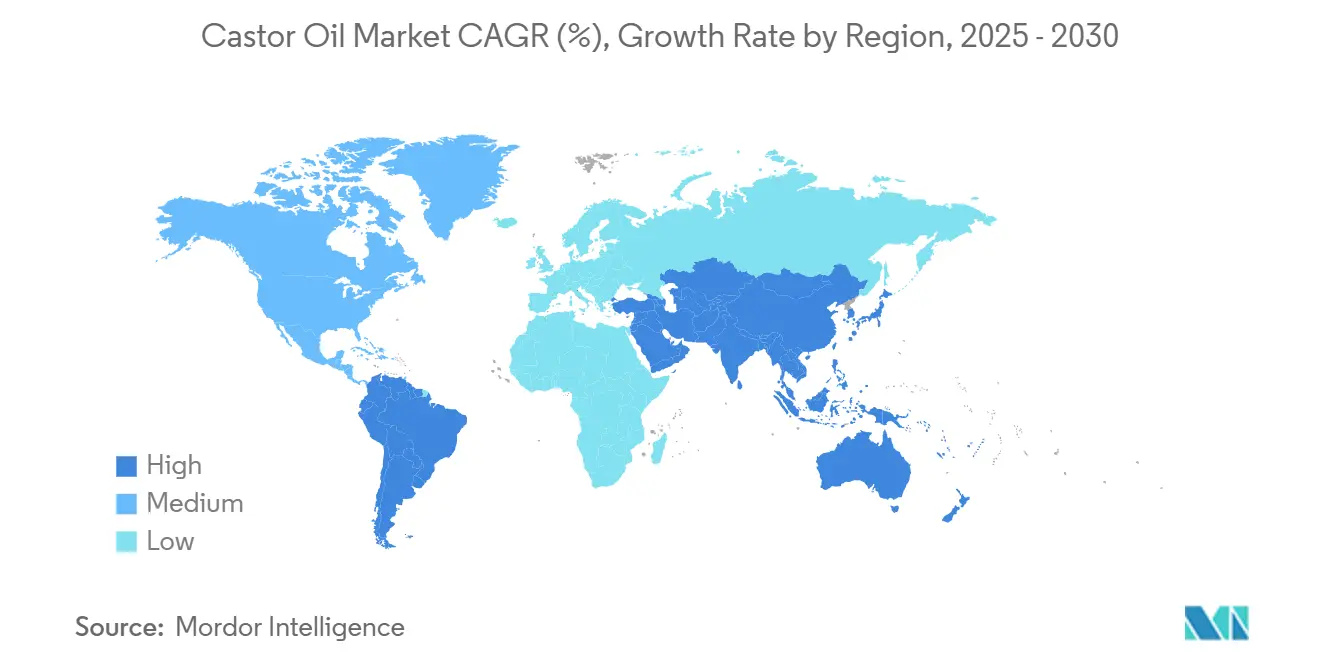

- By geography, Asia-Pacific held 59.73% of the castor oil market share in 2024; the Middle East and Africa region records the highest projected CAGR at 5.93% to 2030.

Global Castor Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-based lubricants demand surge | +1.2% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Cosmeceutical clean-label shift | +0.9% | North America & EU, expanding to APAC urban markets | Short term (≤ 2 years) |

| Rising pharma excipient substitution | +0.7% | Global, concentrated in US and European pharmaceutical hubs | Medium term (2-4 years) |

| EV thermal-management fluids adoption | +0.8% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Derivatives in bioplastics for niche medical devices | +0.4% | North America & EU regulatory markets | Long term (≥ 4 years) |

| Agro-based aviation bio-fuel pilots | +0.3% | Global, led by US SAF Grand Challenge and UK Mandate | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bio-based Lubricants Demand Surge

As the automotive industry pivots towards renewable lubricants, castor oil derivatives are witnessing a surge in demand, especially in electric vehicles. Traditional petroleum-based fluids fall short in meeting the thermal management needs of these vehicles. Highlighting this shift, the Advanced Fluids for Electrified Vehicles Consortium at Southwest Research Institute points out that electric powertrains impose unique demands on fluids. These fluids need specialized formulations to enhance heat transfer and ensure compatibility with materials. Castor oil, with its natural hydroxyl functionality, offers enhanced lubrication, especially when mixed with other vegetable oils. This was evident in grinding applications, where blends of castor and soybean oils outperformed formulations using only pure castor oil. The U.S. Department of Agriculture's Oil Crops Yearbook notes a rising industrial appetite for specialty oil applications[1]U.S. Department of Agriculture. "Oil Crops Outlook: May 2025." June 16, 2025. https://www.ers.usda.gov/publications/pub-details?pubid=112582.. This trend underscores a broader movement away from traditional petroleum-based lubricants towards bio-derived alternatives. As automotive manufacturers increasingly prioritize lubricants that align with both performance and sustainability goals, castor derivatives are carving out a niche, especially in high-temperature applications, solidifying their role in the future of automotive fluids.

Cosmeceutical Clean-Label Shift

Driven by consumer demand for transparency in ingredient lists, cosmetic manufacturers are increasingly turning to castor oil derivatives. This shift comes in light of the FDA's Modernization of Cosmetics Regulation Act, which mandates enhanced facility registration and product listing requirements by July 2024. Under this regulatory framework, manufacturers are required to disclose detailed ingredient information, leading to a preference for naturally derived components, such as castor oil, over synthetic alternatives. Notably, hydrogenated castor oil has garnered specific FDA approval for food-contact applications, as outlined in 21 CFR 178.3280[2]U.S. Food and Drug Administration. "21 CFR 178.3280 -- Castor oil, hydrogenated." May 6, 2025. https://www.ecfr.gov/current/title-21/chapter-I/subchapter-B/part-178/subpart-D/section-178.3280.. This includes its incorporation in vinyl chloride polymers, permitted at up to 4% by weight, and in various packaging materials. Furthermore, the United States Pharmacopeia's 2024 revision has updated the monographs for Polyethylene Glycol 40 Castor Oil, now mandating ethylene glycol contamination testing. This move underscores the heightened quality standards, particularly benefiting premium castor oil producers. Additionally, Jamaica Black castor oil, known for its unique processing methods and touted efficacy benefits, commands a premium price in cosmetic formulations. As these regulatory changes unfold, they present competitive advantages for suppliers who not only comply with the new quality standards but also align with the growing demand for clean-label products.

Rising Pharma Excipient Substitution

Pharmaceutical manufacturers are increasingly turning to castor oil derivatives, moving away from synthetic excipients. This shift not only meets biocompatibility standards but also simplifies regulatory hurdles, especially in drug delivery systems that utilize biodegradable polymers. The FDA's DailyMed database highlights castor oil's credibility, listing it as a 100% active ingredient stimulant laxative, underscoring its safety in pharmaceuticals. Ricinoleic acid, which makes up 90% of castor oil's fatty acid content, is being utilized as a petrochemical substitute in both industrial and pharmaceutical settings. Furthermore, there's a push in genetic engineering to cultivate ricinoleate in alternative oilseed crops, addressing the need for a diversified supply chain. Thanks to its unique hydroxyl functionality, ricinoleic acid is pivotal in creating biodegradable and biocompatible polymers, crucial for controlled drug release. Additionally, hydrolyzing castor oil yields sebacic acid, a vital component in producing polyamides, polyesters, and polyurethanes, all of which are integral to medical device manufacturing. This trend underscores the pharmaceutical industry's growing preference for naturally-derived excipients, a move that resonates with regulatory agencies prioritizing ingredient safety and biocompatibility. As a result, there's a consistent demand for castor oil derivatives in drug formulation.

EV Thermal-Management Fluids Adoption

Electric vehicle manufacturers are turning to castor oil-derived thermal management fluids to tackle battery cooling challenges. These challenges often elude conventional water-glycol systems, especially during fast-charging scenarios that demand enhanced heat dissipation. A webinar by Lubrizol spotlighted the benefits of these specialized fluids, emphasizing their role in enabling quicker charging and mitigating thermal runaway risks. Castrol's ON e-thermal fluid boasts a 41% faster charging rate than its traditional counterparts, all while ensuring batteries remain at optimal temperatures during discharge. This positions Castrol's derivatives as pivotal in the evolution of EV architecture. The flashpoint attributes of these thermal fluids are vital for safety adherence. Formulated fluids have outperformed standard base oils in automotive settings. In response to tightening global regulations, particularly in China, there's a push for stringent safety measures against thermal runaway incidents, amplifying the demand for cutting-edge cooling solutions. Furthermore, castor oil derivatives not only address material compatibility issues with EV components but also promise enduring performance without the need for replacements, bolstering the automotive sector's shift towards electrification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Castor seed yield volatility | -0.8% | APAC core, particularly India and China production regions | Short term (≤ 2 years) |

| Price sensitivity vs. soybean/sunflower oils | -0.6% | Global, with higher impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Supply-chain bottlenecks in Gujarat ports | -0.4% | APAC export-dependent regions, spillover to global supply | Short term (≤ 2 years) |

| Mycotoxin contamination risk in storage | -0.3% | Global, concentrated in humid tropical storage regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Castor Seed Yield Volatility

Major castor-growing regions grapple with agricultural production variability, leading to supply instability and hindering market growth. This challenge is exacerbated as climate patterns increasingly disrupt traditional cultivation cycles, especially in Gujarat and Rajasthan. The ICAR-Indian Institute of Oilseeds Research highlights pronounced yield variations among castor cultivars. For instance, the DCH-32 cultivar yields 1,030 kg/ha under rainfed conditions but jumps to 2,460 kg/ha with irrigation, underscoring the crop's water sensitivity. Research conducted in humid tropics pinpoints optimal sowing windows between June 18 and July 2. Early sowing can yield between 773.7-799.1 kg/ha, starkly contrasting with a mere 129.2 kg/ha for late sowing. Such narrow cultivation parameters heighten production risks. Reflecting these concerns, the U.S. Department of Agriculture's Risk Management Agency has set projected prices and volatility factors for the 2025 crop year. Addressing yield volatility, BASF's Pragati program promotes sustainable farming practices. Having certified over 8,000 farmers, the program boasts a 33% reduction in water consumption alongside improved individual yields. Yet, with its focus on semi-arid regions, the program remains vulnerable to weather-related disruptions, posing risks to the global castor oil supply chain.

Price Sensitivity vs. Soybean/Sunflower Oils

Despite its superior functional properties, castor oil's premium pricing compared to commodity oilseeds has hindered its adoption in price-sensitive applications, especially when soybean and sunflower oil prices remain significantly lower. Data from the World Bank highlights that in 2023, India's castor oil exports averaged around USD 1.60 per kg[3]World Bank. "Castor oil and its fractions exports by country |2023.", https://wits.worldbank.org/trade/comtrade/en/country/ALL/year/2023/tradeflow/Exports/partner/WLD/product/151530., a price point that stands in stark contrast to conventional vegetable oils, thus posing challenges for cost-conscious industrial applications. Research indicates that blending castor oil with other vegetable oils in a 1:1 ratio not only enhances lubrication performance over using pure castor oil but also curtails overall formulation costs. This suggests a potential strategy to mitigate price sensitivity concerns. Reports from the USDA's Oil Crops Outlook highlight ongoing volatility in oilseed markets. Yet, castor oil retains its premium status, attributed to its unique chemical properties and a production scale that's limited when juxtaposed with major commodity oils. Industrial users are shifting their focus from just raw material pricing to a broader evaluation of total cost of ownership. They recognize castor oil's superior performance and environmental benefits. Nonetheless, the initial price premiums of castor oil still limit its market penetration, especially in emerging markets where the functional advantages don't always justify the higher costs and purchasing power for specialty chemical inputs is constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Crude Dominance Meets Premium Specialization

Crude castor oil captured 44.27% of the castor oil market share in 2024, underscoring its centrality as the base stock for downstream chemicals and lubricants. Stable demand from polyurethane and plasticizer producers keeps bulk extraction plants running near capacity, ensuring economies of scale that defend margin stability. Hydrogenated grades enjoy niche demand in food-contact polymers regulated under 21 CFR 178.3280, which permits usage up to 4% by weight in vinyl chloride polymers. Dehydrated variants serve as fast-drying resins in protective coatings, while emerging aviation-fuel pathways evaluate hydrotreated crude for iso-paraffin production.

Premium Jamaican Black volumes, though smaller, expand at a 7.48% CAGR through 2030, riding consumer fascination with traditional roasting methods that impart a darker hue and higher ash content valued in hair serums. Differentiation allows brand owners to charge double the average FOB price, lifting seed-to-oil conversion margins for small Caribbean processors. Meanwhile, derivative streams such as sebacic acid and 12-HSA register the fastest unit growth, fueled by polyamide-11 demand in lightweight automotive parts and 3-D printing powders. BASF’s purchase of full ownership in its Alsachimie joint venture secures in-house KA-oil supply, signaling how major chemical groups lock in feedstock for high-value polymers. Collectively these shifts illustrate a castor oil market gravitating toward specialized, high-margin outputs without relinquishing the scale advantages of crude oil.

By End-User: Chemical Leadership Challenged by Cosmetics Growth

The chemical sector commanded 31.63% of 2024 revenue, underpinning the castor oil market size through steady consumption in polyurethanes, lubricants, and nylon intermediates. OEM decarbonization targets elevate bio-content requirements, ensuring long-run offtake that supports investment in catalytic cracking units optimized for ricinoleic derivatives. Pharmaceutical demand builds on the laxative’s long safety record, but the real upside stems from biodegradable polymer excipients that streamline regulatory reviews.

Cosmetics and personal care, expanding at a 6.74% CAGR, absorb rising volumes of PEG-40 hydrogenated castor oil as gentle surfactants, benefitting from MoCRA-driven ingredient transparency that favors naturally derived inputs. Brands leverage fair-trade sourcing to differentiate SKUs, a trend that funnels premiums back to farm cooperatives and sustains community livelihoods in Gujarat and, increasingly, Kenya. Food-grade uses remain limited: the FDA caps hard-candy release agents at 500 ppm and endorses castor oil for vitamin tablet coatings under 21 CFR 172.876, keeping volumes modest but regulatory visibility high. Emerging thermal-management and SAF sectors, though small today, promise outsized growth as technology scale-up de-risks cost curves.

Geography Analysis

Asia-Pacific’s 59.73% hold on the castor oil market share in 2024 flows from India’s USD 1.009 billion export performance on 629.8 million kg shipped, anchored by Gujarat’s integrated crushing and port infrastructure. Regional public-sector banks extend low-interest credit to processors adopting zero-liquid-discharge effluent systems, bolstering compliance with EU sustainability audits. China leans on imports for derivative manufacturing, funneling crude oil into domestic sebacic and nylon-11 lines to serve its fast-growing EV parts sector.

North America and Europe maintain mature yet high-value positions, driven by pharmaceutical and specialty polymer demand. The U.S. FAA awarded nearly USD 300 million in 2024 to accelerate SAF projects, some of which target castor esters for hydrotreated jet blends. The EU’s Green Deal cements demand for low-carbon materials, encouraging automotive Tier-1 suppliers to ink multi-year contracts with certified Indian crushers. Stringent REACH dossiers and MoCRA filings constrain smaller exporters but reward compliant incumbents with price premiums approaching 12% over commodity quotes.

The Middle East and Africa headline future supply growth at a forecast 5.93% CAGR, propelled by Casterra’s 100-ton Kenyan seed shipment in October 2024 and Ethiopia’s 2,225-hectare irrigation project promising 6 tonnes per hectare yields. Governments promote castor as a drought-resilient cash crop that revitalizes semi-arid zones, while proximity to Europe shortens freight times for derivative processors. Pilot crushing plants in Mombasa and Addis Ababa plan to export crude oil by 2026, diversifying global supply chains and tempering India-centric risk. South America stays a small player but could scale rapidly if bio-jet mandates boost demand for regional feedstock, aligning with refinery expansion plans in Brazil and Thailand.

Competitive Landscape

Market concentration sits at a moderate level as legacy giants reposition portfolios and regional entrants gain scale. Adani’s USD 2 billion divestiture from Adani Wilmar in December 2024 frees capital for infrastructure while granting Wilmar International full control to deepen downstream integration. Subsequent acquisitions, such as Adani Wilmar’s 67% stake in Omkar Chemicals, extend reach into surfactants and food additives, consolidating value capture across detergent, bakery, and agrochemical verticals.

BASF’s Pragati program remains the most extensive sustainability initiative, having certified 8,000 farmers across 9,000 hectares and cut water use by 33%, a move that secures preferred-supplier status with European automotive OEMs. Emerging players deploy advanced agronomy and AI-assisted breeding. Casterra Ag’s Kenyan operations already span 700 hectares and target multi-tonne yields, signaling Africa’s capacity to erode India’s supply dominance within the decade.

Technology is another competitive lever: Castrol’s ON e-thermal fluid, formulated with castor esters, sets a benchmark for 41% faster battery charging, raising barriers to entry for firms lacking formulation expertise. High-performance polyamide producers lock up sebacic acid supply through long-term offtake agreements, tightening raw-material availability for spot buyers. Against this backdrop, the castor oil market rewards vertically integrated strategies that control seed, oil, and derivative processing, while lean newcomers capture share via niche, value-added applications.

Castor Oil Industry Leaders

-

Adani Wilmar Ltd.

-

Jayant Agro-Organics Ltd.

-

NK Proteins Pvt Ltd.

-

Thai Castor Oil Industries Co.

-

Gokul Agri International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mangalam Global Enterprise expanded its 'NEAT CASTOR OIL' line, introducing 200 ml and 500 ml bottles, complementing the already available 100 ml variant.

- March 2023: Biofeel® Eleven, a newly launched yarn derived from natural sources, traces its origins back to India. The journey starts with "Eranda," a small bean in Hindi, from which the ideal oil is extracted. This oil, Castor oil, serves as the foundation for these innovative 100% sustainable yarns. These yarns find applications across diverse sectors, including fashion, sports, automotive, and home textiles, catering to both fabrics and premium garments.

Global Castor Oil Market Report Scope

| Crude Castor Oil |

| Hydrogenated Castor Oil |

| Dehydrated Castor Oil |

| Jamaican Black Castor Oil |

| Others |

| Chemical Industry |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Food and beverages |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Crude Castor Oil | |

| Hydrogenated Castor Oil | ||

| Dehydrated Castor Oil | ||

| Jamaican Black Castor Oil | ||

| Others | ||

| End-User | Chemical Industry | |

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Food and beverages | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the castor oil market?

The castor oil market size stands at USD 2.4 billion in 2025 and is projected to reach USD 3.09 billion by 2030.

Which region holds the largest share of global castor oil trade?

Asia-Pacific leads with 59.73% share in 2024, anchored by India’s dominant export base.

Which product type is growing the fastest?

Jamaican Black castor oil is advancing at a 7.48% CAGR thanks to premium demand in cosmetics.

Why is castor oil important for electric vehicles?

Castor-based thermal fluids enable 41% faster battery charging and meet new safety standards for high-voltage architectures.

Page last updated on: