Gift Retailing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 100.33 Billion |

| Market Size (2031) | USD 122.44 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

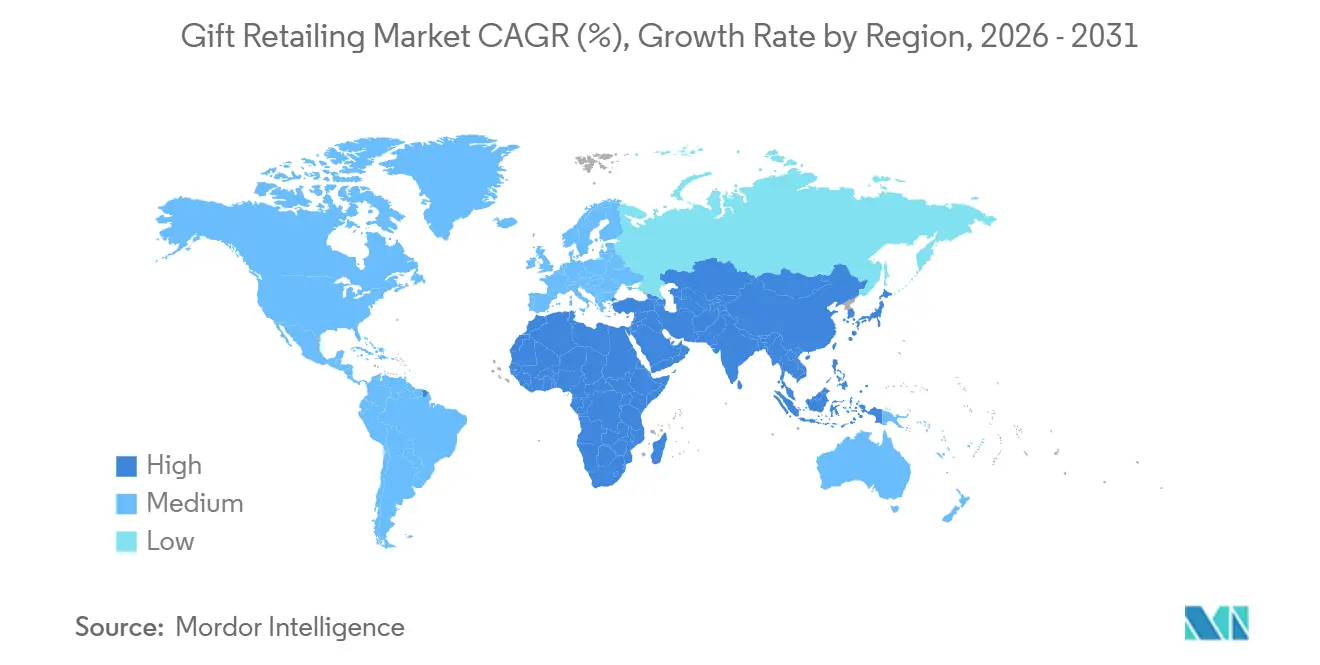

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gift Retailing Market Analysis by Mordor Intelligence

The gift retailing market size is expected to grow from USD 96.42 billion in 2025 to USD 100.33 billion in 2026 and is forecast to reach USD 122.44 billion by 2031 at a 4.06% CAGR over 2026-2031. Holiday promotions, fandom-driven licensing, and AI-aided personalization are expanding product discovery and boosting conversion across both stores and e-commerce. Same-day fulfillment, click-and-collect, and curated assortments are helping retailers capture last-minute demand in the gift retailing market, especially during peak weeks. Corporate buyers are shifting toward sustainable and traceable gifting options, favoring suppliers that can evidence recycled inputs and lower-carbon logistics. Personalization is scaling through on-demand 3D printing and digitized handwriting for cards, which supports premium pricing and higher attach rates in the gift retailing market. Retailers are also using seasonal calendars and exclusive drops to drive traffic and unlock higher sell-through for licensed collectibles in the gift retail market.

Key Report Takeaways

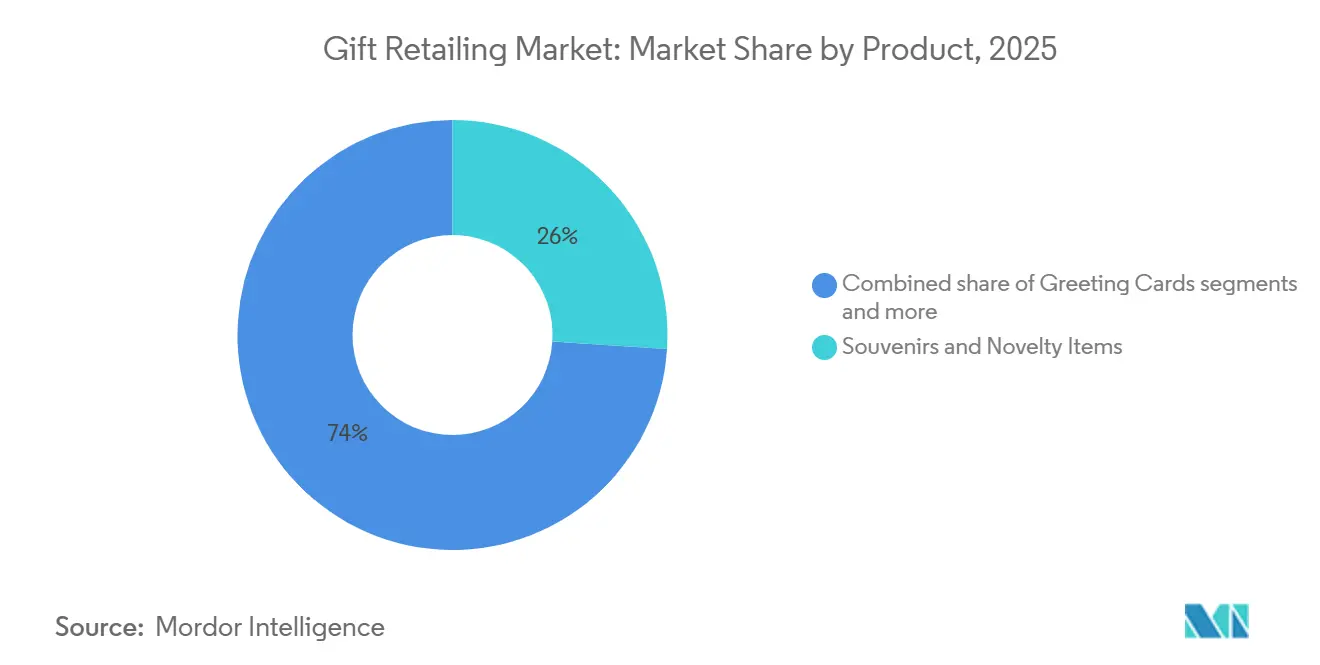

- By product, souvenirs and novelty items led the gift retail market with 26.04% share in 2025, while seasonal decorations are projected to expand at an 8.61% CAGR through 2031.

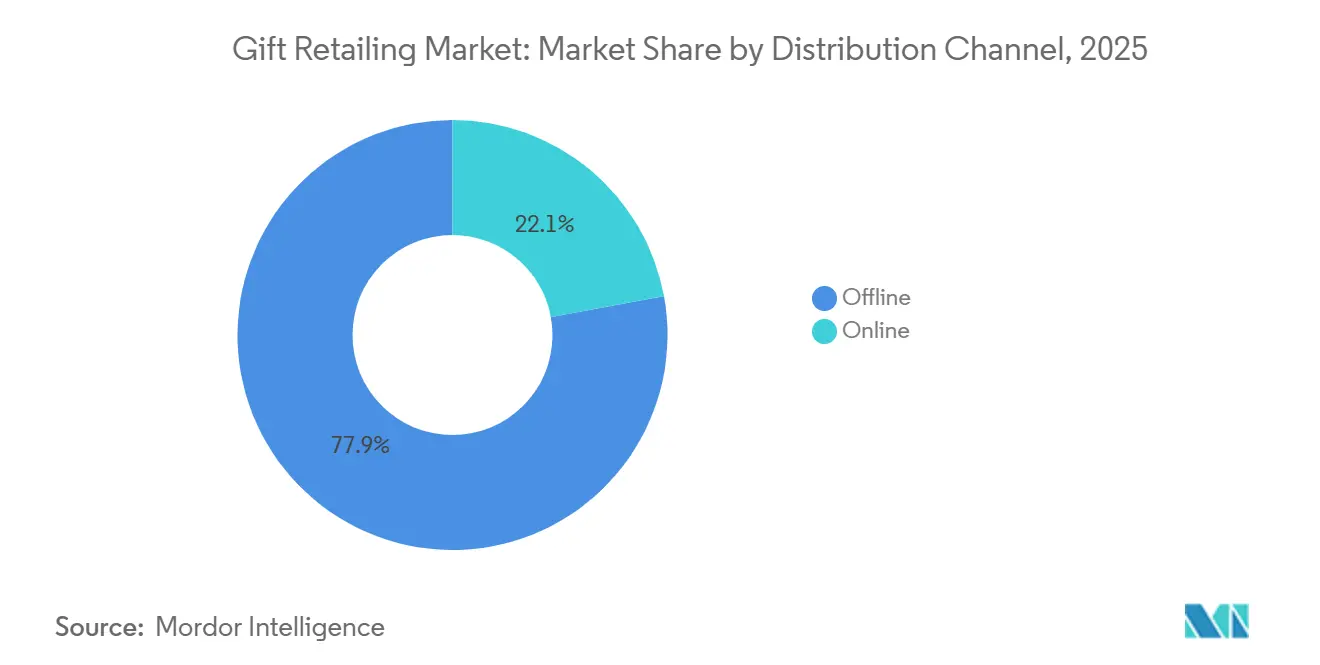

- By distribution channel, offline accounted for 77.88% of the gift retail market share in 2025, while online recorded the highest projected CAGR of 6.28% through 2031.

- By occasion, festive and holiday gifts accounted for 24.05% of the gift retailing market share in 2025, and baby and kids gifts are advancing at a 9.67% CAGR through 2031.

- By geography, Europe captured 28.10% % of the gift retailing market share in 2025, while the Middle East and Africa are forecast to grow at an 8.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gift Retailing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Experiential tourism boosts souvenir market growth | +0.9% | Global, with Asia-Pacific and Europe strongest | Medium term (2-4 years) |

| Higher disposable income drives emerging market demand | +1.2% | Asia-Pacific core, spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Seasonal promotions enhance retailer sales opportunities | +0.7% | Global | Short term (≤ 2 years) |

| 3D printing enables customization in gift products | +0.4% | North America and Europe are early adopters | Medium term (2-4 years) |

| ESG gifting trends favor sustainable product choices | +0.5% | EU, North America | Medium term (2-4 years) |

| Fandom culture fuels the licensed collectibles market | +0.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Experiential Tourism Boosts Souvenir Market Growth

Travelers continue to seek culturally anchored souvenirs, including locally made ceramics, textiles, and artisan foods with provenance, which encourages premium pricing in the gift retail market. QR codes embedded in packaging link to artisan profiles and short-form storytelling, elevating perceived value and supporting gifting moments tied to milestone trips. Vendors are prioritizing recycled and natural materials, such as bamboo, cork, and organic cotton, to meet rising sustainability expectations from tourists and corporate buyers in the gift retailing market. Hospitality and tourism merchandise ranges are also rotating toward functional travel accessories, including compact toiletry kits and lightweight backpacks, that fit minimal packing norms while remaining giftable. The travel sector’s ongoing rebound is supporting steady souvenir throughput for retailers that curate authentic designs and verifiable sourcing in the gift retailing market.

Higher Disposable Income Drives Emerging Market Demand

Digital commerce penetration has enabled gifting platforms to reach new urban and semi-urban catchments, with India’s individual e-commerce adoption at 80% in 2024 among persons aged 16-74, creating a broad base for gift discovery and fulfillment in the gift retailing market. In the Gulf region, online shopping intensity during promotional weeks has been strong, signaling rising discretionary spending power that supports gift purchases across categories and price tiers. Cross-border buying accounts for a meaningful share of digital orders, expanding consumer access to licensed collectibles and niche crafts that are not readily available locally in the gift retailing market. Retailers are aligning pricing ladders to match middle-income growth, using good-better-best merchandising and curated bundles to lift perceived value during seasonal peaks in the gifts retail market. These shifts are making emerging economies central to multi-year volume growth, especially where digital adoption, logistics reliability, and promotional calendars are converging.

Seasonal Promotions Enhance Retailer Sales Opportunities

Holiday calendars have become a foundation for traffic, with targeted free-shipping windows, tiered bundles, and time-boxed drops increasing conversion during Valentine’s Day, Mother’s Day, and Christmas in the gift retailing market. In 2025, Black Friday week spending surged 31% year over year in the UAE and 36% in Saudi Arabia, confirming the potency of synchronized promotions in high-growth markets [1]Economy Middle East, “E-commerce on the rise: UAE and Saudi Arabia record surge in digital spending,” Economy Middle East, economymiddleeast.com. In the United States, miscellaneous store retailers, including gift shops, recorded 9.2% annual growth in 2025, with November sales up 17% year over year as holiday promotions intensified and seasonal inventory reached shelves earlier [2]U.S. Census Bureau, “Advance Monthly Sales for Retail and Food Services, December 2025,” U.S. Census Bureau, census.gov. Scarcity-led licensed drops around major fandoms and sports properties drove store visits and basket expansion, as seen in curated Black Friday releases spanning trading cards, exclusive plush, and limited-edition apparel. Retailers also timed offers to payday cycles, capturing incremental 2H-of-month spending and smoothing revenue cadence during extended promotional windows in the gift retailing market.

Fandom Culture Fuels Licensed Collectibles Market

Licensed IP remains a force multiplier for gifting, with Pokémon trading cards generating USD 2.5 billion in U.S. toy sales in 2025, an 87% year-over-year increase that underscores the depth of fandom demand in the gift retail market [3]The Toy Association, “U.S. Toy Industry Returns to Growth in 2025, Circana Reports,” The Toy Association, toyassociation.org. Sports licensing remains a major draw for apparel and accessories that double as gifts, as demonstrated by the NFLPA’s recognition of high-performing licensees in 2025 across multiple categories. Specialty retailers have leaned into blind-box mechanics and original IP launches to cultivate repeat purchases and collection-completion behavior within short promotional windows in the gift retail market. MINISO’s expansion plan commits to 100 original IPs over the next decade, signaling a robust pipeline of collectibles to anchor themed assortments and experiential store zones [4]MINISO, “MINISO Announces Expanded Proprietary IP Incubation and Strengthened IP Operations,” MINISO, miniso.com. This IP-led curation is increasingly cross-category, blending plush, stationery, fragrance, and small décor that gift buyers can bundle across family and friend segments in the gift retailing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impact of raw material price volatility on decorative items | -0.3% | Global | Short term (≤ 2 years) |

| Increased competition from digital greetings and cash applications | -0.4% | North America and Europe | Medium term (2-4 years) |

| Consumer preference shifts due to minimalist movements | -0.2% | North America, Western Europe | Long term (≥ 4 years) |

| Tariffs on imported novelty items amid geopolitical tensions | -0.6% | North America, with secondary effects in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Impact of Raw Material Price Volatility on Decorative Items

Packaging paper prices trended higher in 2025 after a prolonged decline, posting a 2.6% average increase over the first 11 months compared to 2024, with cumulative growth of 8.6% from March 2024 through November 2025. Pricing levels remain almost 20% above pre-COVID benchmarks, driven by pulp, recovered paper, and energy expenses that transmit volatility into finished goods with a lag. Divergences in recovered paper and pulp price trends, up 4.5% and down 10.8% respectively, create uneven cost pressures that manufacturers pass through selectively in the gift retailing market. Gift retailers that emphasize decorative boxes, elaborate wrapping, and protective inserts face a margin squeeze, especially in premium lines where unboxing matters. Larger chains can mitigate with volume discounts and forward contracts, widening the gap with independents on cost-to-serve and price flexibility.

Tariffs on Imported Novelty Items Amid Geopolitical Tensions

Tariff changes in 2025, including the suspension of the de minimis duty-free rule for low-value shipments under USD 800, have raised landed costs for many small gift items entering the United States, affecting price ladders and promotional depth in the gift retailing market. Under the suspension, every import incurs duty, which is material for cross-border e-commerce parcels in novelty and décor categories. Retailers are diversifying sourcing, shifting purchase orders toward alternative origins to stabilize cost and supply for tariff-sensitive SKUs in the gift retailing market. These shifts are most pronounced during holiday planning cycles when late policy changes collide with long lead times and container booking windows. Merchants with agile vendor bases and flexible consolidation strategies can better preserve margins during peak gifting weeks in the gift retailing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Souvenirs Anchor Share, Seasonal Decorations Lead Velocity

Souvenirs and novelty items accounted for 26.04% of market share in 2025, setting the tone for core demand patterns in the gift retailing market. Retailers emphasize locally inspired designs, licensed character tie-ins, and augmented storytelling that validate price premiums and strengthen gifting intent. Seasonal decorations are the fastest-growing subcategory, advancing at an 8.61% CAGR through 2031 as earlier promotions and limited editions pull sales into longer holiday windows in the gift retailing market. Greeting cards continue to evolve with AI-generated stickers, short-form video messages, and digitized handwriting, refreshing the physical format and helping platforms cross-sell curated gifts. Giftware and other gift items provide a steady base across the year, including photo frames, candles, and small electronics that benefit from fandom and pop-culture cycles in the gift retailing market.

Innovation and licensing continue to drive the product mix as brands coordinate holiday drops for ornaments, collectibles, and home décor that attract both collectors and gifters in the gift retailing market. Retailers are also investing in subscription curation boxes that bundle giftware themes across wellness, gourmet, and home fragrance, reinforcing recurring purchase behavior. Blind-box mechanics for plushes and figurines nurture repeat purchases, with IP-focused specialty chains reporting strong demand for scarcity-led releases in the gift retailing market. Corporate buyers are prioritizing compliant materials and traceability in items like notebooks, tote bags, and desk accessories, which blends ESG mandates with everyday utility. This balance of collectible appeal and practical utility supports more resilient sell-through even as consumer preferences shift in the gift retailing market.

By Distribution Channel: Offline Dominates, Online Accelerates

Offline formats accounted for 77.88% of sales in 2025 as tactile evaluation, in-store curation, and immediate gratification continue to matter in the gift retailing market. Specialty gift shops, department stores, and mass merchandisers lean on experiential zones and exclusive launches to increase basket size during peak months. Online is scaling faster, projected to grow at a 6.28% CAGR through 2031 as same-day delivery, intelligent gift-finders, and seamless mobile checkout extend reach and lift conversion in the gift retailing market. Cross-border e-commerce has expanded consumer catalogues in markets like the UAE and Saudi Arabia, where digital penetration and cross-border spend are among the region’s highest. Omnichannel services, including click-and-collect and scan-and-ship, are improving inventory turnover and broadening access to local and remote assortments in the gift retailing market.

Impulse and discoverability keep stores central, with mall traffic and event-led displays continuing to influence purchase timing in the gift retailing market. Online platforms excel at personalization and automated reminders, with large user bases storing tens of millions of occasions that trigger timely prompts and reduce last-minute friction. In parallel, exclusive fandom collectibles timed to holiday weeks are pulling store visits and anchoring themed end-caps that drive cross-category attachment in the gift retailing market. The channel mix is converging as retailers adopt consistent recommendations and delivery promises across digital and physical touchpoints in the gift retailing market.

By Occasion: Festive Peaks Drive Volume, Baby and Kids Gifts Outpace

Festive and holiday gifts accounted for 24.05% of occasion-based spending in 2025, underscoring how concentrated seasonal moments shape annual outcomes in the gift retailing market. Retail calendars are expanding earlier with themed promotions, exclusive drops, and free shipping windows that smooth weekly traffic and secure inventory ahead of peaks. Baby and kids gifts are the fastest-growing occasion subcategory, projected at a 9.67% CAGR through 2031, as customization tools like embroidered blankets, personalized storybooks, and 3D-printed figurines support premium gifting in the gift retailing market. Birthday gifting runs year-round, with automated reminders and AI-aided design features boosting early conversions and card personalization. Wedding and anniversary gifts benefit from aspirational registries and experiential add-ons that align with celebrants’ push for memorable milestones in the gift retail market.

Corporate gifting is aligning with ESG requirements, pushing demand for recycled notebooks, bamboo cutlery sets, upcycled desk accessories, and plantable stationery with transparent impact metrics in the gift retailing market. Retailers are using limited editions and licensed IP around holidays to increase urgency and unit economics, supported by themed pages and curated bundles. Occasion databases continue to grow, feeding marketing triggers that improve attach rates for chocolates, flowers, small giftware, and cards in the gift retailing market. Seasonal promotions are becoming more granular by region, reflecting local festivals and pay cycles that expand peak windows and distribute demand across the quarter. This adaptive approach helps stabilize fulfillment loads and enhances the shopper experience in the gift retailing market.

Geography Analysis

Europe accounted for 28.10% of global revenue in 2025, reflecting high per-capita gifting, mature specialty retail, and strong sustainability preferences that shape gift retail assortments. E-commerce in France grew its turnover to USD 206.21 billion (EUR 175.3 billion) in 2024 and remains on a growth trajectory in 2026 as merchants invest in faster delivery and generative AI for operations. EU directives on sustainability and data protection reinforce the need for traceable supply chains, transparent materials, and robust privacy for customer data captured during personalization in the gift retailing market. Retailers in Germany, the United Kingdom, Spain, and Italy are balancing price with craftsmanship and sustainable credentials, which affects how seasonal collections are curated and priced. Licensing partnerships within lifestyle and entertainment remain central in driving seasonal excitement and in-store displays across key European markets in the gift retailing market.

North America continues to show strong gifting behavior, with United States miscellaneous store retailers, including gift shops, recording notable gains during the peak months of 2025, supported by holiday campaigns and exclusive merchandise strategies in the gift retailing market. Geopolitical tariff shifts are influencing sourcing, prompting merchants to diversify beyond single-country dependencies to manage landed costs and maintain price points in tariff-sensitive categories. Large retailers and marketplaces are expanding omnichannel fulfillment to capture time-sensitive gifting needs around holidays and paydays in the gift retailing market. Personalization advances and AI-powered recommendations in greeting cards and curated gifts are helping platforms lift attach rates, frequency, and average order values across the region. Specialty players continue to emphasize quality and narrative, supporting stable demand for premium keepsakes in the gift retailing market.

The Middle East and Africa are the fastest-growing regions, projected at an 8.23% CAGR through 2031, with GCC economies investing in digital infrastructure and experiential retail hubs that encourage gifting behaviors in the gift retailing market. In the UAE and Saudi Arabia, digital penetration and cross-border purchases open access to international brands and unique products that complement local holidays and festivals, which boosts the appeal of themed and licensed assortments in the gift retailing market. Retailers tune promotions to local calendars and salary cycles, capturing spend spikes around Ramadan, Eid periods, Black Friday week, and national days. Merchants expanding in Africa are leveraging mobile-first engagement and curated assortments that align with price and logistics constraints while building gifting occasions across urban centers in the gift retail market. These dynamics are shaping inventory, pricing, and partnership decisions for brands scaling in high-growth subregions in the gift retailing market.

Competitive Landscape

The gift retailing market combines large general merchandisers, specialized e-tailers, and legacy card brands, each leveraging distinct strengths to attract shoppers and corporate buyers. Big-box chains are using franchise tie-ins and timed exclusives to drive store traffic and anchor themed displays that lift adjacent categories in the gift retailing market. Card leaders are pairing physical SKUs with digital gifting features so recipients can redeem experiences, music, and cash-like gifts, thereby extending their relevance beyond traditional gift retailing use cases. Specialty chains built on IP and blind-box mechanics are deepening their original IP portfolios and experiential formats to amplify repeat purchases in the gift retailing market.

Licensing and retail partnerships are central to competitive differentiation, as fan communities drive outsized revenue per transaction for collectibles and themed assortments in the gift retail market. The NFLPA’s recognition of high-performing licensees in 2025 illustrates how sports IP continues to shape apparel and accessory purchases that crossover into gifting occasions. Card and gift platforms continue to highlight creative features such as AI-generated stickers, handwriting digitization, and visual previews, which increase personalization and differentiate the experience in the gift retailing market. Meanwhile, corporate gifting providers are emphasizing eco-certified materials, traceability, and measurable impact data to meet escalating ESG procurement criteria. This interplay between scale, IP access, and personalization defines category leaders’ strategies in the gift retailing market.

Restructuring and M&A are reshaping mid-market dynamics as firms recalibrate portfolios and channels. Party City’s asset sale out of bankruptcy transfers core IP and wholesale assets to a new owner, highlighting pressure points for pure-play party and décor operators in the gift retailing market. Etsy’s 2026 agreement to sell Depop to eBay positions Depop within a larger consumer-to-consumer fashion ecosystem while Etsy refocuses on core handmade marketplaces that connect gifters to artisans in the gift retailing market. Regional retailers like Norman’s Hallmark are expanding footprints through acquisitions and new stores, signaling continued neighborhood demand for curated card and gift assortments in the gift retailing market. These moves underscore a hybrid landscape that balances omnichannel personalization with physical discovery in the gift retailing market.

Gift Retailing Industry Leaders

Hallmark Cards Inc.

American Greetings Corp.

Amazon.com Inc. (Handmade & Gifts

Card Factory PLC

Walt Disney Co. (Disney Store)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: eBay agreed to acquire Depop from Etsy for USD 1.2 billion in cash, aligning Depop’s Gen Z-focused resale footprint with eBay’s consumer-to-consumer strategy. The transaction signals portfolio refocus at Etsy while expanding eBay’s youth fashion reach and community-led gifting discovery.

- January 2026: MINISO unveiled an accelerated roadmap centered on proprietary IP, evolving store formats such as MINISO LAND, and end-to-end IP operations. The company plans to introduce 100 original IPs over the next decade and has partnered with over 150 global IPs since 2020, reflecting deeper investment in licensed and original collectibles.

- November 2025: American Greetings launched its first Peanuts Digital Advent Calendar 2025 to celebrate the brand’s 75th anniversary at a USD 9.99 price point. The calendar unlocks daily animated comic strips, themed games, and shareable greetings throughout December, reinforcing digital engagement ahead of the holiday peak.

- February 2025: American Greetings expanded digital gifting with partnerships that embed retail gift cards from 100+ brands, Virgin Experience Gifts vouchers, and custom songs from Songfinch into e-cards, plus Birdie-enabled cash gifts up to USD 2,000.

Global Gift Retailing Market Report Scope

Gift retailing refers to the commercial sale of products intended as gifts for occasions, celebrations, or goodwill gestures. These products range from traditional items like greeting cards and flowers to diverse options such as electronics, fashion accessories, gourmet food baskets, and novelty items, catering to varied consumer preferences and demands.

The Gift retailing market report is segmented by product type (souvenirs and novelty items, seasonal decorations, greeting cards, giftware, other gift items), distribution channel (offline, online), occasion (birthday gifts, wedding & anniversary gifts, corporate gifts, baby & kids gifts, festive & holiday gifts), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Souvenirs and Novelty Items |

| Seasonal Decorations |

| Greeting Cards |

| Giftware |

| Other Gift Items |

| Offline |

| Online |

| Birthday Gifts |

| Wedding & Anniversary Gifts |

| Corporate Gifts |

| Baby & Kids Gifts |

| Festive & Holiday Gifts |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Souvenirs and Novelty Items | |

| Seasonal Decorations | ||

| Greeting Cards | ||

| Giftware | ||

| Other Gift Items | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Occasion | Birthday Gifts | |

| Wedding & Anniversary Gifts | ||

| Corporate Gifts | ||

| Baby & Kids Gifts | ||

| Festive & Holiday Gifts | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the gift retailing market?

The gift retailing market size is USD 100.33 billion in 2026 and is projected to reach USD 122.44 billion by 2031 at a 4.06% CAGR.

Which channels and occasions are shaping demand most in the gift retailing market?

Offline stores still dominate, while online is the fastest-growing channel, and festive and holiday gifting is the largest occasion share, with baby and kid's gifts showing the fastest growth.

How are retailers differentiating assortments in the gift retailing market?

Retailers are leveraging exclusive licensed collectibles, seasonal calendars, and AI-driven personalization across cards and curated gifts to drive traffic and attach rates.

What sustainability trends are influencing the gift retailing market?

Corporate buyers and consumers favor recycled and reusable materials with supply-chain transparency, boosting ESG-aligned gifting and upcycled lines.

How are tariffs and cross-border rules affecting the gift retailing market?

Changes such as suspending the de minimis duty-free threshold and reciprocal tariff increases are raising landed costs and encouraging sourcing diversification beyond reliance on a single country.

What role does personalization play in the gift retailing market?

Personalization through AI features and on-demand 3D printing increases perceived value, reduces returns, and raises gift attach rates on leading platforms.

Page last updated on: