Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 50.38 Billion |

| Market Size (2026) | USD 51.66 Billion |

| Market Size (2031) | USD 58.56 Billion |

| Growth Rate (2026 - 2031) | 2.54% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Retail Market Analysis by Mordor Intelligence

The Singapore Retail Market size is projected to be USD 50.38 billion in 2025, USD 51.66 billion in 2026, and reach USD 58.56 billion by 2031, growing at a CAGR of 2.54% from 2026 to 2031.

Growth rests on structural shifts toward omnichannel integration, with online penetration rising through 2026 and logistics micro-hubs enabling faster delivery options that convert browsing into purchase. Wage inflation under the progressive wage model is pushing wider adoption of automation, data-driven merchandising, and self-service workflows that preserve service quality while improving productivity. Prime retail rents remain firm despite pockets of vacancy, which favors footprint rationalization and smaller formats that sustain sales per square foot. Tourism recovery supports discretionary categories such as watches and jewelry, yet shoppers also shift toward experiences, which moderates the direct lift to general merchandise.

Key Report Takeaways

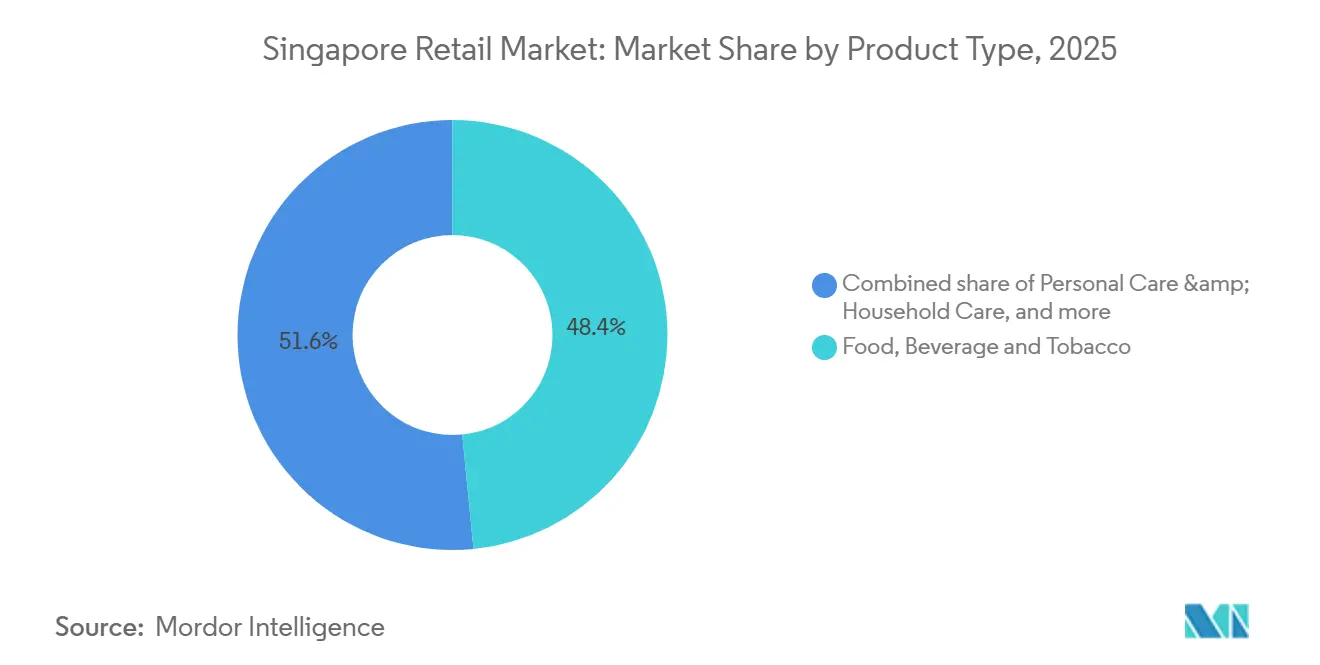

- By product type, Food, Beverage & Tobacco captured 48.44% of the Singapore retail market share in 2025, while Personal Care & Household is projected to grow at a 10.87% CAGR through 2031.

- By retail channel, Modern Trade Retail captured 59.87% of the Singapore retail market share in 2025, while E-Commerce & Others is projected to grow at a 6.37% CAGR through 2031.

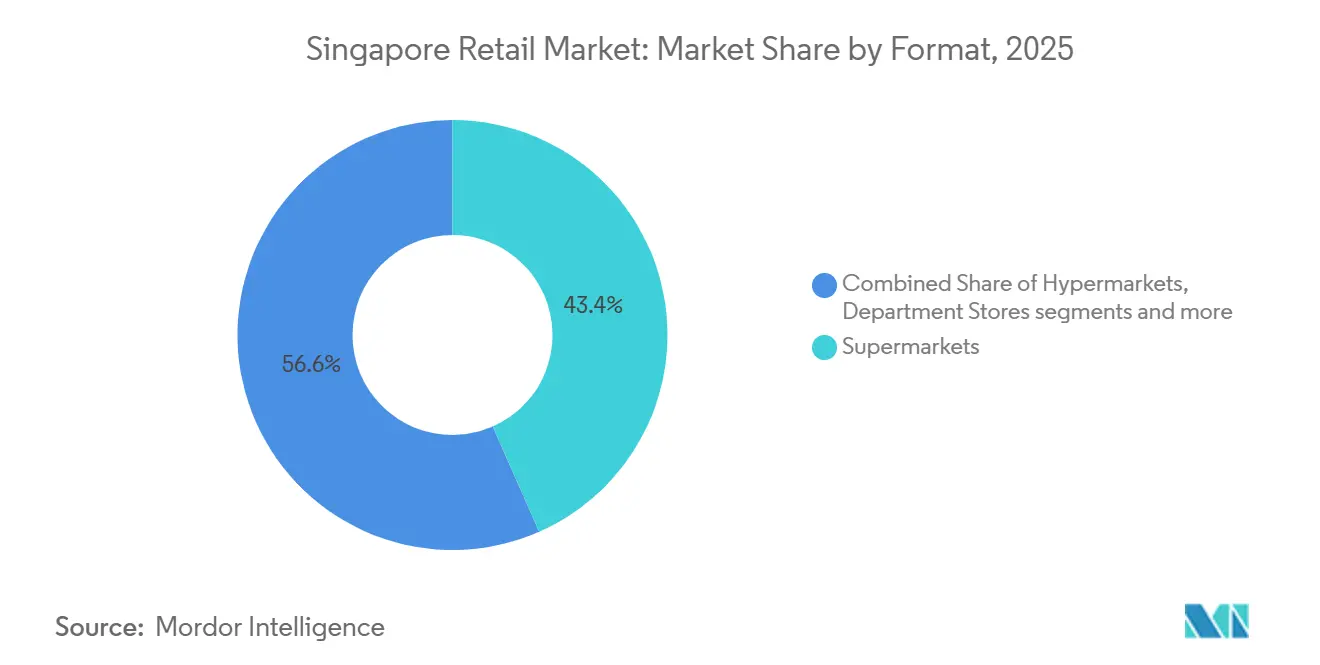

- By format, Supermarkets captured 43.39% of the Singapore retail market share in 2025, while Convenience Stores are projected to grow at 3.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Omnichannel Consumer Journey Adoption | + 1.2% | Island-wide, highest in Downtown Core, Marina Bay, Orchard, East Coast | Medium term (2-4 years) |

| Expansion of Supermarket Private-Label Penetration | + 0.6% | Island-wide supermarkets, higher in HDB heartlands like Ang Mo Kio, Bedok, Woodlands | Short term (≤ 2 years) |

| Tourism Rebound Boosting Discretionary Spend | + 0.8% | Downtown Core, Orchard, Changi Airport, and spillover to major suburban malls | Medium term (2-4 years) |

| ESG-Linked Financing Lowering Capex For Retrofit | + 0.4% | Island-wide for listed retailers and landlords, early gains in CapitaLand and Frasers malls | Long term (≥ 4 years) |

| Real-Time Retail Analytics Via 5G Edge Networks | + 0.7% | Nationwide 5G coverage, early in large formats | Medium term (2-4 years) |

| Urban Logistics Micro-Hub Policy Roll-Out | + 0.9% | High-density HDB towns and mixed-use precincts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Omnichannel Consumer Journey Adoption

Singapore shoppers expect a unified experience across browsing, payment, fulfillment, and returns, which forces retailers to integrate online and store systems. IMDA reports that 91% of retail SMEs had adopted at least one sector-specific digital solution by 2023, although overall adoption depth was still modest, which implies meaningful headroom for advanced capabilities like AI and real-time inventory routing in 2026.[1]IMDA.GOV.SG https://www.imda.gov.sg/-/media/imda/files/about/resources/corporate-publications/annual-report/imda-sgde-report-fy2024-2025.pdf. IMDA’s Advanced Digital Solutions program for Omnichannel Retail Management launched in July 2024 with 70% funding support, which lowers barriers for SMEs to add integrated POS, cross-channel inventory, and last-mile orchestration. Online retail penetration reached 14.5% in October 2025, up from 13.1% in July 2025, and categories such as electronics exceeded 50% online share, which illustrates the widening role of digital in total spending.[2]SINGSTAT.GOV.SG https://www.singstat.gov.sg/-/media/files/news/mrsnov2025.ashx. Retailers combine store pickup and rapid delivery windows to reduce friction, while privacy rules require clear consent for personalization that relies on first-party data strategies. The retail industry in Singapore benefits as omnichannel convenience complements, rather than substitutes, physical proximity.

Urban Logistics Micro-Hub Policy Roll-Out

Flexible zoning in the URA Master Plan 2025 allows urban micro-hubs that position inventory near demand, which shortens last-mile distances and supports economically viable 2-hour and same-day delivery. This shift reduces delivery cost per order, supports dark-store models, and lets stores double as local fulfillment nodes that sustain online grocery expansion from low double digits toward higher penetration through 2031. The micro-hub model is well-suited to dense HDB towns and mixed-use precincts where demand can be predicted with fine-grained data. The Singapore retail market sees service-level improvements without requiring significant new GFA, which aligns with land-use priorities. Shared micro-hubs also enable route consolidation and electric van adoption, which supports national emissions goals. The overall result is faster delivery and optimized capacity utilization that improves conversion in time-sensitive categories.

Real-Time Retail Analytics Via 5G Edge Networks

Nationwide 5G coverage enables sub-10-millisecond latency that supports in-store edge analytics for dynamic pricing, restocking, and queue optimization. Retailers use shelf sensors and computer vision to track inventory and fix out-of-stocks in real time, which cuts working capital and lifts sales through improved availability. This analytics layer pairs well with the micro-hub network, so the nearest node can fulfill orders as soon as a local stock level drops below a threshold. The Singapore retail market is also using low-latency analytics for loss prevention that detects patterns associated with shrinkage in open-shelf formats. These tools are scaling faster due to wage inflation, which increases the return on automation and workforce redeployment[3]MOM.GOV.SG https://www.mom.gov.sg/newsroom/press-releases/2025/0811-tcr-recommendations-for-retail-pwm. . Retailers still must meet PDPC consent standards when they link in-store telemetry to customer identity for location-based offers.

Expansion of Supermarket Private-Label Penetration

Private labels deliver higher gross margins than equivalent branded goods, which helps offset rising labor costs and rent. Large chains expand house brands across staples and into premium and functional segments, often supported by regional contract manufacturing and improved cold-chain logistics in Singapore. The retail industry in Singapore sees private-label momentum because shoppers trust incumbent chains, and because store brands can be positioned as smart value or even premium options. Enhanced control over pricing, shelf placement, and promotion lets retailers manage category profitability more tightly, even when online comparison puts pressure on national brands. Loyalty programs and direct data feedback loops improve targeted trial and repeat purchase for house brands under consented marketing regimes.

Restraints Impact Analysis*

| RESTRAINT | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated Mall Density And Limited New Retail Space | - 0.8% | Island-wide, acute in OCR and mature suburban malls | Short term (≤ 2 years) |

| Labour Shortages & Rising Minimum-Wage Floor | - 1.1% | Island-wide, strongest in labor-intensive formats | Short term (≤ 2 years) |

| Persistent Rental Cost Inflation In Prime Districts | - 0.6% | Downtown Core, Orchard, Central Region | Medium term (2-4 years) |

| Data-Privacy Tightening Curbing 3rd-Party Ad-Targeting | - 0.5% | Island-wide digital operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Saturated Mall Density and Limited New Retail Space

Island-wide retail vacancy registered 7.2% in Q3 2025, with regional divergence as the Downtown Core tightened while the Outer Central Region loosened, which signals selective oversupply and limited room for expansive GFA additions. The URA Master Plan 2025 focuses on housing, logistics, and advanced industry, which channels retail growth toward productivity over new footprints. This pattern narrows the greenfield pipeline for large-box formats and pushes retailers to optimize existing locations and formats that can justify rent with higher throughput. The Singapore retail market adjusts to this cap through format conversion, densification in best-in-class assets, and stronger reliance on omnichannel to expand effective catchments. In less productive malls, legacy leases can trap capital, which accelerates selective closures and subdivision strategies by landlords to raise aggregate rent.

Labor Shortages & Rising Minimum-Wage Floor

The progressive wage model set a baseline monthly wage of USD 1,794.6 for retail assistants in September 2025, with a step-up to USD 1,997.05 by September 2027, which raises operating costs for labor-intensive formats.[4]MOM.GOV.SG https://www.mom.gov.sg/newsroom/press-releases/2025/0811-tcr-recommendations-for-retail-pwm.Population aging and tight foreign worker quotas add to the shortage, which pushes retailers toward automation, self-checkout, and inventory robotics to protect margins. Co-funding under the Progressive Wage Credit Scheme helps in 2025 and 2026, but the structural increase persists afterward, which increases the urgency of end-to-end workflow redesign. The Singapore retail market is seeing uneven impact, since larger chains amortize technology investments across many stores while smaller independents lack the scale to do so. Service models are being rethought so human labor focuses on high-value help and experience while transactional tasks are automated where feasible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food, Beverage & Tobacco Anchor Grocery Dominance

Food, Beverage & Tobacco Products held 48.44% in 2025, reflecting stable everyday demand and deep supermarket networks, while other product types follow category-specific trajectories across online and offline. Personal Care & Household shows the fastest expansion at a 10.87% CAGR through 2031 as shoppers upgrade into premium skincare, wellness, and specialized formats. The Singapore retail market continues to rely on grocery fundamentals for traffic while discretionary categories adjust to changing fashion cycles and online discovery effects. Watches and jewelry benefited from tourism-led spending and duty-free pricing in central precincts, while apparel was softer due to shifting work patterns and higher online return rates that weigh on store productivity. Food, Beverage & Tobacco is positioned to maintain volume resilience even when consumer budgets are tight.

Private labels in staples and pantry categories continue to broaden as chains improve sourcing and cold-chain capabilities that support quality upgrades. The Singapore retail market size for Food, Beverage & Tobacco is anchored by weekly basket missions in HDB towns that keep store visits frequent. Electronics and appliances sustain the highest online penetration in the 52–55% band, which reflects standardized specs and strong digital research behavior that shifts purchase to e-commerce. Furniture, toys, and hobby categories sit near one-third of online share as home delivery and price comparison drive digital adoption. The Singapore retail industry in personal care benefits from omnichannel sampling and subscriptions that raise repeat purchases and support the segment’s premiumization path.

By Retail Channel: Modern Trade Sustains Lead Amid E-Commerce Surge

Modern Trade Retail captured 59.87% in 2025, underpinned by national supermarket chains, convenience networks, and large specialty formats. E-Commerce & Others is the fastest-growing channel at a projected 6.37% CAGR through 2031, supported by micro-hubs, 5G connectivity, and platform competition that improves service levels and pricing. The Singapore retail market reflects a complementary channel dynamic where online expands assortment and speed while stores anchor trust, immediacy, and experiential discovery. Traditional mom-and-pop retail faces structural headwinds in cost, assortment, and technology adoption that are difficult to overcome without scale. Shoppers continue to split baskets between convenience, supermarket top-ups, and online orders aligned to delivery windows.

Category-level online penetration remains uneven, which shapes merchandising and fulfillment strategies. Electronics surpass half online, and furniture sits near one-third online, while supermarkets and hypermarkets remain in the 11–12% range with strong room to grow as micro-fulfillment and dark-store models scale. The Singapore retail market size attributed to Modern Trade remains significant due to near-universal physical proximity, but channel share shifts toward E-Commerce & Others as delivery speeds improve. Consent requirements and algorithm transparency rules are reshaping how personalization can be executed, which favors first-party data environments and loyalty ecosystems. The Singapore retail industry will see more cross-channel orchestration as SMEs use IMDA-backed solutions to unify POS, inventory, and customer data.

By Format: Supermarkets Anchor; Convenience Stores Surge

Supermarkets accounted for 43.39% in 2025 and remain the largest format as neighborhood locations and weekly basket missions sustain traffic. Convenience stores show the fastest growth at a projected 3.46% CAGR through 2031, driven by density, 24/7 access, and ready-to-eat innovation that serves time-sensitive trips. Hypermarkets continue to consolidate or downsize as sites for large-format builds remain scarce, and category specialists and online channels supplant the multi-category mission. Department stores stay under pressure as assortments fragment across category killers, marketplaces, and direct-to-consumer options. The Singapore retail market favors smaller formats that keep sales per square foot high as rents and wages rise.

Specialty stores remain resilient by differentiating with depth, expertise, and curated assortments that are hard to replicate online. The Singapore retail market size for supermarkets is supported by multi-format strategies that place premium stores in affluent clusters and value formats in heartlands. Convenience gains also flow from strong MRT and HDB integration that increases footfall throughout the day. Automation, self-checkout, and RFID support format productivity in supermarkets and specialty stores as wage floors step up through 2027. The Singapore retail industry continues to diversify formats while anchoring fulfillment on stores that double as local nodes.

Geography Analysis

Downtown Core and Orchard account for a significant portion of discretionary retail value due to tourist traffic and affluent resident demand. Retail vacancy in the Downtown Core fell to 7.1% in Q3 2025, and Central Region rents rose 0.9% quarter-on-quarter, which shows firm pricing in trophy assets despite island-wide vacancy at 7.2%. In 2024, Singapore welcomed 16.5 million visitors and achieved USD 23.2 billion (SGD 29.8 billion) in receipts, which boosted premium categories dependent on tourist spending. Shopping’s share of tourist spend drifted below 20% in 2024 as visitors favored experiences, which encourages central retailers to sharpen luxury and beauty assortments aligned to traveler preferences. The retail industry in Singapore maintains a central gravity for high-end and travel-related purchases.

Outer Central Region towns and mature suburban malls capture day-to-day consumption through supermarkets, specialty, and F&B anchors. OCR vacancy rose from 4.5% to 5.9% in Q3 2025, which suggests rising competition from e-commerce and strengthening convenience formats that soak up top-up missions. The Singapore retail market size in suburban catchments adjusts through omnichannel features such as click-and-collect and rapid local delivery that help preserve wallet share. As micro-hubs are deployed, e-commerce adoption in groceries can lift further because delivery windows become practical at neighborhood distances. Network strategies will balance store rationalization with proximity coverage to retain weekly and top-up trips.

Regional centers such as Tampines, Jurong East, and Woodlands play a stabilizing role by combining large specialty anchors with entertainment. The Singapore retail market reflects weekend traffic concentration in these hubs, with central stores benefiting more from weekday tourist and CBD flows. Motor-related clusters and industrial fringe zones serve commercial customers and households for specific durable purchases. The URA Master Plan 2025 encourages mixed-use locations that integrate logistics into neighborhoods, which supports broader access to two-hour fulfillment for routine items. Over time, this shifts some growth from physical expansion to digital enablement tied to first-party data and loyalty ecosystems.

Competitive Landscape

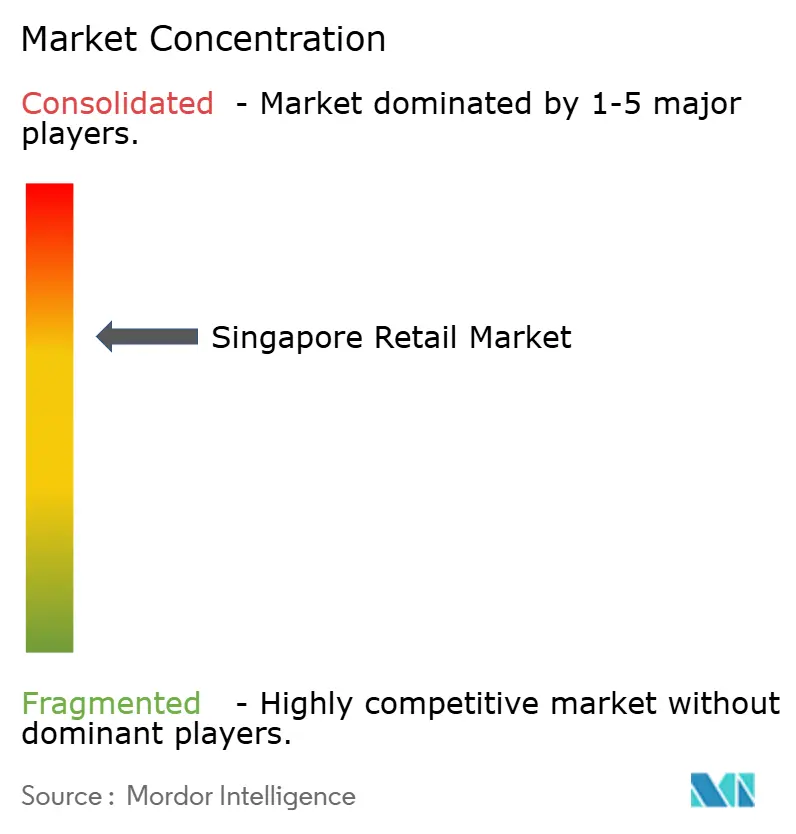

The Singapore retail market is moderately fragmented at the total market level, with no single company surpassing low double-digit share across all categories. Grocery is more concentrated among leading chains that anchor supermarket formats with multi-brand portfolios and value or premium positioning. Convenience is also concentrated, where network density and site control create durable advantages that are difficult to replicate quickly. E-commerce marketplaces account for a growing share of online GMV and use logistics, payments integration, and sponsored listings to compete. Apparel and specialty retail remain competitive between international brands, local champions, and marketplaces that serve wide preference ranges.

Strategic moves focus on omnichannel enablement, private-label expansion, and automation. FairPrice integrates stores with rapid delivery and pickup choices, while Sheng Siong tilts toward store-led economics and value positioning supported by selective online capabilities. DFI Retail Group’s intention to divest the Singapore Food business reflects portfolio adjustment under wage and rent pressures in a digitally competitive environment. The Singapore retail market also sees stronger loyalty playbooks that build first-party data reservoirs for compliant personalization under PDPC rules. In specialty, brands use experiential retail and services to defend margins that are otherwise exposed to online price transparency.

Cost-side shifts are shaping capital allocation and store design. Wage floors create a clear return case for self-checkout, RFID, and real-time replenishment that reduce low-value labor while preserving human-led service for advice and experiences. Rental inflation in prime sites encourages smaller, high-throughput stores and sharper category focus, while regional and suburban nodes lean into omnichannel logistics to protect sales density. IMDA support helps SMEs close technology gaps so larger chains do not capture all gains from omnichannel integration. The Singapore retail market continues to converge on a model where physical proximity and digital convenience reinforce each other.

Singapore Retail Industry Leaders

FairPrice Group

Sheng Siong Group

DFI Retail Group (Giant & Cold Storage)

Shopee (Sea Ltd)

Lazada (Alibaba)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Edition (EPO Fashion Group, luxury Chinese womenswear) launched its first boutique outside China at Raffles City Singapore, offering contemporary high-end collections with prices in the premium segment.

- November 2025: Mo&Co expanded with a second Singapore store at Jewel Changi Airport, strengthening its presence in key tourist and transit hubs.

- November 2025: Judydoll (Chinese makeup brand) opened a new store at Bugis+, coinciding with its 100th location in China and highlighting the rapid global push of affordable C-beauty.

- October 2025: Mo&Co (EPO Fashion Group, Chinese womenswear) opened its first Singapore store at Raffles City, featuring edgy, rock-chic fashion as part of the brand's international debut.

Singapore Retail Market Report Scope

The Singapore retail market includes businesses that sell goods directly to consumers through physical stores, malls, and online platforms. It is driven by strong consumer spending, tourism demand, and a well-developed urban and digital infrastructure.The report on the Singapore retail sector provides a comprehensive evaluation of the market, with an analysis of the segments in the market.

The Singapore Retail Market Report is Segmented by Product Type (Food, Beverage & Tobacco Products; Personal Care & Household Care; Apparel, Footwear & Accessories; Furniture, Toys & Hobby; Industrial & Automotive; Electronic & Household Appliances; Other Products), By Retail Channel (Traditional Mom & Pop Retail, Modern Trade Retail, E-Commerce & Others), By Format (Hypermarkets, Supermarkets, Convenience Stores, Department Stores, Specialty Stores, Others), and Geography (Intra-Singapore Regional Variations: Downtown Core, Orchard Planning Area, Outer Central Region, Regional Centers, Fringe Areas).

By Product Type

| Food, Beverage, & Tobacco Products |

| Personal Care & Household Care |

| Apparel, Footwear, & Accessories |

| Furniture, Toys, & Hobby |

| Industrial & Automotive |

| Electronic & Household Appliances |

| Other Products |

By Retail Channel

| Traditional Mom & Pop Retail |

| Modern Trade Retail |

| E-Commerce & Others |

By Format

| Hypermarkets |

| Supermarkets |

| Convenience Stores |

| Department Stores |

| Specialty Stores |

| Others (Drugstore, Cash & Carry, Wholesaler) |

By Region

| Central Region |

| East Region |

| North Region |

| North-East Region |

| West Region |

| By Product Type | Food, Beverage, & Tobacco Products |

| Personal Care & Household Care | |

| Apparel, Footwear, & Accessories | |

| Furniture, Toys, & Hobby | |

| Industrial & Automotive | |

| Electronic & Household Appliances | |

| Other Products | |

| By Retail Channel | Traditional Mom & Pop Retail |

| Modern Trade Retail | |

| E-Commerce & Others | |

| By Format | Hypermarkets |

| Supermarkets | |

| Convenience Stores | |

| Department Stores | |

| Specialty Stores | |

| Others (Drugstore, Cash & Carry, Wholesaler) | |

| By Region | Central Region |

| East Region | |

| North Region | |

| North-East Region | |

| West Region |

Key Questions Answered in the Report

What is the current size and growth outlook for the Singapore retail market?

The Singapore retail market size is USD 51.66 billion in 2026 and is projected to reach USD 58.56 billion by 2031 at a 2.54% CAGR.

Which channels are growing fastest in Singapore retail?

E-Commerce & Others is the fastest-growing channel and is projected to expand at a 6.37% CAGR through 2031, supported by logistics micro-hubs and 5G-enabled operations.

Which product categories lead the Singapore retail market in share and growth?

Food, Beverage & Tobacco leads with 48.44% share in 2025, while Personal Care & Household is the fastest-growing with a 10.87% CAGR through 2031.

How is tourism shaping demand in the Singapore retail market?

Singapore welcomed 16.5 million visitors and reached USD 23.2 billion in receipts in 2024, which lifted luxury and beauty spending, although shopping’s share of visitor spend edged below 20% as tourists prioritized experiences.

What are the main compliance considerations for personalization and online retail in Singapore?

Retailers must secure explicit consent for tracking and meet algorithm transparency and fake review prohibitions under PDPC and CCCS guidelines, which favor first-party data and loyalty programs.

Page last updated on: