Germany Student Accommodation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

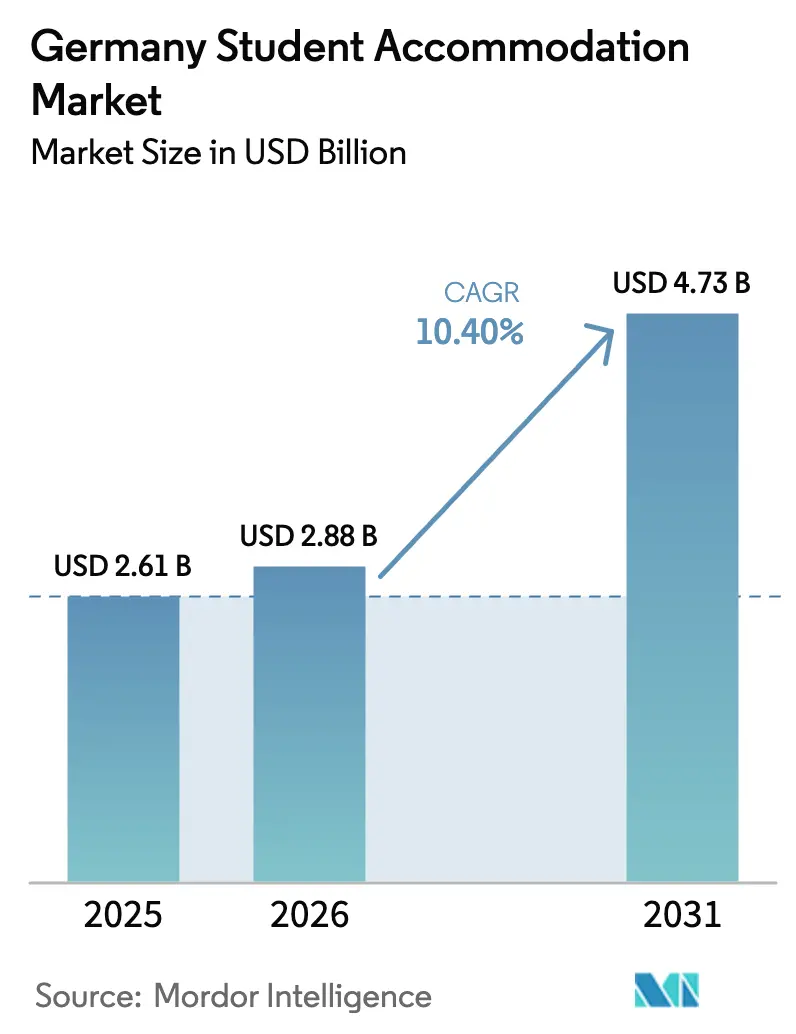

| Base Year Market Size (2025) | USD 2.61 Billion |

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 10.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Student Accommodation Market Analysis by Mordor Intelligence

The Germany student accommodation market size is expected to grow from USD 2.61 billion in 2025 to USD 2.88 billion in 2026 and is forecast to reach USD 4.73 billion by 2031 at 10.4% CAGR over 2026-2031. Investors see resilience in the asset class because international enrollments bounced back sharply, domestic demand remained steady, and federal funding programs preserved supply pipelines despite construction headwinds. Purpose-built student accommodation (PBSA) continues replacing legacy halls, as students favor amenities such as high-speed connectivity, furnished rooms, and flexible leases that align with hybrid learning routines. Record inflows of 380,000 international students in 2024 tightened vacancy rates around major universities, giving professionally managed operators significant pricing power in peak intake months. At the same time, PropTech adoption accelerated leasing cycles and lowered acquisition costs, allowing operators to scale portfolios quickly across multiple German states.

Key Report Takeaways

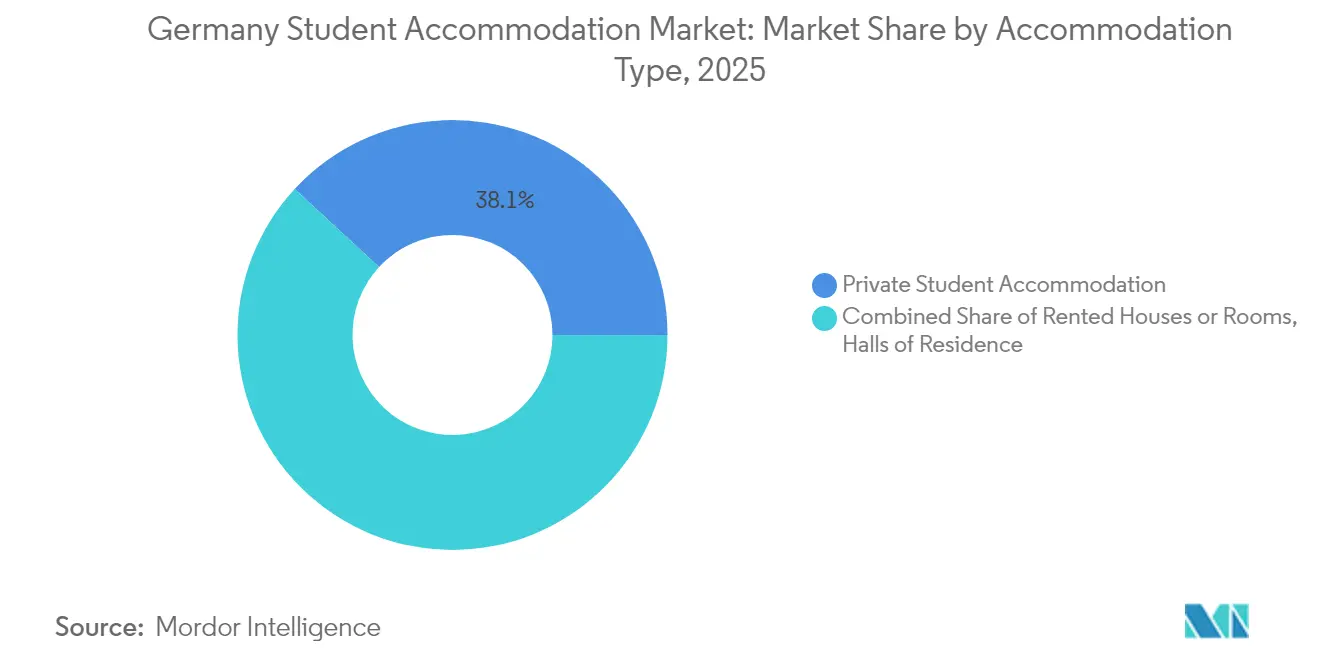

- By accommodation type, private student accommodation led with 38.12% Germany student accommodation market share in 2025 and is set to expand at a 6.58% CAGR through 2031.

- By location, city center assets captured 54.12% of the Germany student accommodation market in 2025, while peripheral developments are forecast to post a 5.74% CAGR through 2031.

- By booking mode, online channels accounted for 62.05% share of the Germany student accommodation market in 2025, and they will rise at an 8.07% CAGR to 2031.

- Regionally, Berlin held 19.10% of the Germany student accommodation market size in 2025; Bavaria is projected to record the fastest 6.58% CAGR by 2031.

- GSA, Uninest, and The FIZZ together controlled just under 15% of national beds in 2024, highlighting an opportunity for consolidation among the next tier of operators.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Germany representing one among them. The global report on student accommodation market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Germany Student Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising international student inflows post-pandemic easing | +2.8% | National, concentrated in Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Growing investor appetite for alternative real-estate asset classes | +1.9% | National, with focus on Tier-1 cities | Long term (≥ 4 years) |

| Federal government's housing initiatives and funding programs | +1.5% | National, prioritizing tight urban markets | Medium term (2-4 years) |

| Surge in dual-study programmes boosting demand outside traditional university hubs | +1.2% | Regional, strongest in Bavaria, Baden-Württemberg, NRW | Long term (≥ 4 years) |

| Blockchain-enabled rent payment platforms reducing default risk | +0.8% | National, early adoption in major cities | Short term (≤ 2 years) |

| Conversion of ageing office stock into micro-apartments | +0.6% | Urban centers with high office vacancy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising International Student Inflows Post-Pandemic Easing

Germany welcomed 380,000 international students in 2024, the highest count in its higher-education history [1]Source: Staff Reporter, “Record 380,000 international students choose Germany in 2024,” University World News, universityworldnews.com. STEM and business programs captured most of this growth, crowding supply near technical universities and private business schools in Berlin and Munich. Only 9.4% of students accessed subsidized halls, down from 15% in 1991, so newcomers turned to the Germany student accommodation market where PBSA could deliver furnished units and bilingual support. Operators leveraged this imbalance to raise rents and achieve high occupancy, especially in premium studios. The sustained influx of non-EU enrollees suggests enduring demand that underpins long-term revenue visibility for asset owners.

Growing Investor Appetite for Alternative Real-Estate Asset Classes

Institutional capital pivoted to the Germany student accommodation market after remote work weakened office yields and e-commerce eroded retail values. CBRE data show PBSA’s defensive qualities, counter-cyclical enrollment spikes and inflation-linked leases, have shielded cash flows better than hotel or serviced-apartment segments. GSA’s USD 387.52 million (EUR 330 million) joint acquisition with Singapore’s GIC added nearly 3,000 German beds, illustrating the scale of cross-border capital flowing into the sector. Large allocations accelerate portfolio roll-ups, professionalize property management, and compress operating costs through centralized procurement. As liquidity deepens, exit avenues through REIT listings or core-fund disposals will further validate PBSA’s mainstream status.

Federal Government Housing Initiatives and Funding Programs

Berlin’s 2025 budget earmarked more than USD 4.70 billion (EUR 4 billion) annually for social housing and urban development through 2029, alongside USD 13.21 billion (EUR 11.25 billion) in subsidies from the Special Infrastructure Fund [2]Source: Federal Ministry of Finance, “2025 Federal Budget Highlights,” Bundesministerium der Finanzen, bundesfinanzministerium.de. Student accommodation benefits indirectly because overall residential deliveries ease pressure on scarce urban land, and directly through targeted grants for trainee residences. The Wohngeld-Plus reform raised allowances by roughly 15% in 2025, improving affordability and lowering default risk for operators that house low-income students. Capital commitments also fund digital permitting pilots that could shave months off approval cycles in high-demand cities. Execution risk remains, yet the scale of fiscal support materially lifts supply-side confidence over the medium term.

Surge in Dual-Study Programs Boosting Demand Outside Traditional University Hubs

Dual-study enrollments expanded rapidly as firms like Volkswagen, BASF, and Mercedes-Benz integrated vocational training with academic curricula, drawing students to industrial centers beyond classical university towns. Participants alternate between campus and workplace, needing flexible leases near manufacturing plants as much as near lecture halls. This dispersion pushes the Germany student accommodation market into secondary cities where land prices are lower and planning regimes are friendlier. Operators diversify revenue streams by balancing Tier-1 assets with growth pockets in places such as Wolfsburg, Ludwigshafen, and Stuttgart. Long-term demand appears secure because dual-study tracks bridge Germany’s skilled-labor gap and enjoy bipartisan policy backing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-material inflation squeezing project IRRs | -2.1% | National, acute in high-cost urban markets | Short term (≤ 2 years) |

| Lengthy municipal permitting cycles | -1.4% | National, severe in Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Demographic plateau of domestic student population | -0.9% | National, offset by international growth | Long term (≥ 4 years) |

| NIMBY opposition to high-density dorm projects | -0.7% | Urban centers, particularly affluent neighborhoods | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-Material Inflation Squeezing Project IRRs

The construction-materials index hit 118.9 in 2024 versus 63.1 in 2000, nearly doubling real build costs in just two decades . Specialized PBSA fixtures like fire-rated furniture and smart-access systems resist substitution, magnifying cost pressure. Building permits plunged 24.2% year-over-year in 2024, revealing developer hesitancy amid eroding economics [3]Source: Economic Bulletin, “2024 building approvals slump 24%,” Destatis, destatis.de. Higher European Central Bank rates compounded pain by lifting debt-service coverage tests. Unless material-price growth cools or subsidies offset the spike, several planned projects may remain shelved through 2026.

Lengthy Municipal Permitting Cycles

Approval timelines in cities such as Stuttgart stretch past three years because of complex environmental reviews and neighborhood appeals. Carrying costs for land and preparatory work erode project net present value, discouraging new entrants to the Germany student accommodation market. Digitalization pilots aim to standardize processes, but municipal adoption varies widely, prolonging uncertainty for sponsors. Backlogs constrain supply precisely as international enrollments surge, intensifying price pressures on existing inventory. Streamlined e-permitting could unlock latent development capacity if federal-state coordination improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation Type: Private Operators Reshape Market Structure

Private student accommodation contributed 38.12% of the Germany student accommodation market in 2025, outpacing all other formats with a 6.58% CAGR forecast through 2031. Operators such as GSA, Uninest, and The FIZZ deploy institutional capital to build PBSA assets featuring cowork lounges, cinema rooms, and multilingual reception staff, luring both domestic and international tenants. The Germany student accommodation market size for private provision will climb steadily as aging Studentenwerk halls suffer under-investment and limited amenity offerings. Meanwhile, traditional rented rooms face supply compression because small landlords increasingly prefer young professionals over transient students. The resulting structural pivot should entrench private dominance well beyond the forecast horizon.

Second-tier halls controlled a shrinking share in 2024, unable to match the experience standards private brands now set. Funding constraints slow refurbishment cycles, keeping average room sizes below student expectations and limiting digital services such as mobile access cards. Rented houses remain relevant in lower-density towns but lose appeal where PBSA clusters near transit hubs enhance convenience. Because private operators can leverage economies of scale in procurement and marketing, they capture margin even at competitive rent levels. These advantages enable accelerated roll-ups that consolidate fragmented stock into coherent branded portfolios.

By Location: Urban Core Dominance Faces Peripheral Challenge

City center properties held 54.12% of the Germany student accommodation market in 2025 thanks to walkability and proximity to lecture halls, nightlife, and public transit. Premium rents sustain developer interest despite land scarcity and permitting friction. However, the Germany student accommodation market size in peripheral zones is expanding faster at a 5.74% CAGR, as transit upgrades cut commute times and rents stay manageable for budget-conscious students. Operators increasingly adopt hub-and-spoke models where central flagship assets drive brand visibility while suburban sites deliver volume. This balancing act protects yield across economic cycles and diversifies regulatory exposure.

Peripheral growth reflects Berlin’s Ringbahn expansion and Munich’s S-Bahn upgrades, which boost accessibility for districts once deemed too remote. Land-banking costs fall dramatically outside prime grids, improving build-to-core economics even amid material inflation. Students value larger room footprints and quieter neighborhoods, offsetting longer travel times. As hybrid learning reduces on-campus presence, daily proximity becomes less critical, further validating periphery locations. Investors therefore underwrite mixed portfolios that blend CBD prestige with outer-ring scalability.

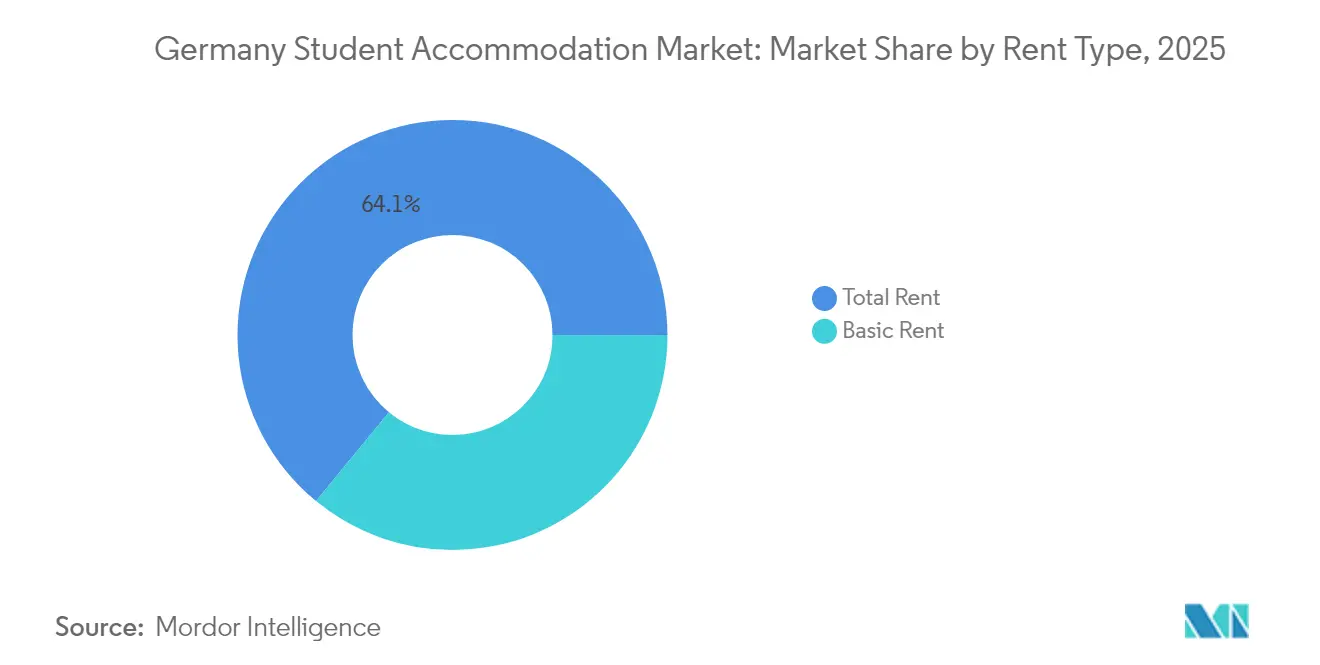

By Rent Type: Total Rent Model Gains Traction

Total rent plans covered 64.05% of contracts in 2025, locking in utilities, Wi-Fi, and sometimes furniture, which simplifies budgeting for tenants unfamiliar with Germany’s billing complexity. The Germany student accommodation market size attached to total-rent offers will keep expanding at a 6.56% CAGR as inflation concerns heighten demand for cost certainty. Operators benefit from streamlined invoicing and fewer arrears, lifting net operating income even after bulk-purchase utility discounts. Basic rent contracts endure mostly in historic flats where landlords lack the scale to aggregate ancillary services. Over time, competitive pressure from PBSA brands will likely marginalize basic rent to small private segments.

Bundled pricing also supports value-added upselling, ranging from housekeeping to bike-sharing, which boosts revenue per bed without raising headline rent uncontrollably. PropTech dashboards enable real-time monitoring of energy use, allowing operators to optimize consumption and contain costs. Students appreciate the transparency and sustainability metrics, tying ESG credentials to brand loyalty. With growing emphasis on climate-friendly living, all-inclusive models that showcase renewable-energy sourcing will differentiate premium offerings.

By Mode: Digital Platforms Transform Booking Behavior

Online channels captured 62.05% share in 2025, and their 8.07% CAGR trajectory signals further dominance as Gen Z cohorts rely on mobile-first research and remote lease execution. HousingAnywhere’s funding round and rent-index publications illustrate investor confidence in the platform model’s scalability. Digital-native operations provide 360-degree virtual tours, AI-driven matchmaking, and instant contract generation, shortening vacancy downtime for landlords. Offline bookings linger mainly for legacy halls where in-person allocation persists, yet their share declines annually. Integrated digital payments and chat-based support increase user satisfaction and generate data that feeds continuous service improvements.

Cross-listing tools let operators advertise vacancies across multiple marketplaces simultaneously, enhancing reach to international students before visa issuance. Personalized push alerts drive conversion by flagging price drops or roommate matches aligned to user profiles. Gamification tactics such as loyalty points for on-time payments further cement retention. As blockchain rent settlements gain traction, online ecosystems will integrate smart-contract modules, creating seamless end-to-end pipelines. Offline brokers must reinvent value propositions or risk obsolescence in a fully digitized Germany student accommodation industry.

Geography Analysis

Berlin’s 19.10% share in 2025 underscores its magnetism for global education seekers and early-career professionals. Only 5.6% of students secured Studentenwerk beds, well below the 9.7% national average, intensifying competition for private units and pushing average rents above USD 762.78 (EUR 650) per month. Robust transit links like the U-Bahn allow expansions into outer districts without sacrificing accessibility. Yet complex zoning and heritage protections add multi-year delays and higher consultation costs that dampen new supply. Operators must therefore combine infill refurbishments with adaptive-reuse projects to maintain growth momentum.

Bavaria’s Germany student accommodation market size is rising swiftly, lifted by Munich’s USD 704.10 (EUR 600) average monthly rent and a constant inflow of STEM students drawn to corporate internships at companies such as BMW and Siemens. Dual-study rollouts in cities like Ingolstadt and Regensburg broaden geographic demand, distributing risk beyond the Bavarian capital. State-level incentives for energy-efficient buildings reduce financing spreads, enhancing project viability despite elevated land costs. Developers partner with universities to pre-lease blocks, securing occupancy before completion and supporting debt underwriting. Consequently, Bavaria exemplifies how industry-academic-corporate synergy fuels sustainable accommodation growth.

North Rhine-Westphalia and Baden-Württemberg round out major contributors by virtue of their populous universities, diversified economies, and sustained housing programs. NRW’s USD 12.33 billion (EUR 10.5 billion) housing initiative supports refurbishments in Cologne and Düsseldorf that incorporate student allocations. Baden-Württemberg leverages Stuttgart’s automotive heritage and Karlsruhe’s IT sector to attract engineering candidates needing high-spec accommodation close to research centers. Both states experiment with digital permitting to expedite projects and reduce soft costs. These reforms, if fully implemented, could release dormant land reservoirs and temper rent inflation. Together, the four leading regions account for over 60% of total beds, reflecting Germany’s polycentric higher-education structure.

Mordor Intelligence provides coverage of the student accommodation market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom, India, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

The Germany student accommodation market remains moderately fragmented, with the top five operators holding a significant share of the market. GSA and Uninest accelerate scale through acquisitions and forward-funding agreements that lock in pipeline inventory before construction starts. Youniq and SMARTments Student rely on city-specific expertise to optimize occupancy and navigate local bureaucracy effectively. Legacy Studentenwerk networks still run sizable hall portfolios but face modernization deficits due to capped public budgets and ESG retrofitting mandates. Market entrants armed with PropTech platforms attract institutional backing by demonstrating data-driven asset management and superior tenant experience.

Strategic moves highlight the race for operational excellence. Limehome’s technology-enabled conversion of empty offices into serviced micro-apartments exemplifies cost-efficient capacity expansion that bypasses greenfield restrictions. International Campus extended The FIZZ brand to Hamburg and Ludwigshafen, pre-leasing units via immersive virtual-tour campaigns to overseas students months ahead of opening. Vonovia doubled its capital-expenditure plan through 2028 to renovate stock, integrate solar arrays, and roll out digital tenant portals, signaling a pivot toward value-add services. Operators also experiment with ESG-linked financing where interest margins fall when carbon-intensity targets are met, aligning with EU taxonomy pressures.

Technology adoption distinguishes winners from laggards. AI-powered revenue-management systems adjust pricing daily based on occupancy forecasts, competitor rates, and university enrollment data feeds. Mobile apps enable maintenance requests, social-event sign-ups, and biometric door entry, fostering community and reducing staff workload. Data analytics unearth cross-selling opportunities such as short-term summer lets to language-school groups. As institutional portfolios expand, centralized procurement contracts deliver volume discounts on furniture and utilities, widening margin over standalone landlords. Consolidation is therefore poised to continue, with mid-sized operators likely acquisition targets for cash-rich global funds seeking rapid market entry.

Germany Student Accommodation Industry Leaders

Uninest Student Residences

The FIZZ (International Campus)

Basecamp Student

Staytoo (Corestate Capital)

Milestone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Limehome surpassed 100,000 square meters of office-to-apartment conversions, including a 167-unit Bremen project slated for 2026.

- October 2024: The KNN program launched low-interest loans and grants that funded 676 affordable units with USD 79.85 million (EUR 68 million) in commitments.

- August 2024: HousingAnywhere rent index revealed German cities among Europe’s most expensive student markets, underlining persistent affordability tension.

- June 2024: SMARTments business expanded Berlin operations with digital key and 24-hour check-in, reflecting contactless trend.

Germany Student Accommodation Market Report Scope

Student Accommodation is defined as providing purpose-built student housing and private rentals to meet the needs of the growing student population, which includes dormitories, student residences, and shared apartments. The market is driven by increasing student enrollment and demand for quality living options for international students.

The German Student Accommodation Market Report is Segmented by Room Type (Entire Place/Studio, Private Room, Shared Room), by Education Type (Graduate, Post-Graduate, Others). The Report Offers Market Size and Forecasts in Volume and Value (USD) for all the Above Segments.

| Halls of Residence |

| Rented Houses or Rooms |

| Private Student Accommodation |

| City Center |

| Periphery |

| Basic Rent |

| Total Rent |

| Online |

| Offline |

| Baden-Württemberg |

| Bavaria (Bayern) |

| Berlin |

| Brandenburg |

| Bremen |

| Rest of Germany |

| By Accommodation Type | Halls of Residence |

| Rented Houses or Rooms | |

| Private Student Accommodation | |

| By Location | City Center |

| Periphery | |

| By Rent Type | Basic Rent |

| Total Rent | |

| By Mode | Online |

| Offline | |

| By Geography | Baden-Württemberg |

| Bavaria (Bayern) | |

| Berlin | |

| Brandenburg | |

| Bremen | |

| Rest of Germany |

Key Questions Answered in the Report

How large is the Germany student accommodation market in 2026?

The sector is valued at USD 2.88 billion in 2026 and is forecast to reach USD 4.73 billion by 2031.

What CAGR is expected for German PBSA investments?

Purpose-built student accommodation revenues are projected to grow at 6.58% CAGR between 2026 and 2031.

Which German city holds the biggest share of student housing demand?

Berlin accounts for 19.10% of national student accommodation demand owing to its 200,000-plus student population.

Why are peripheral locations growing in popularity among students?

Improved transit links and lower rents give peripheral areas a 5.74% CAGR growth edge over city centers through 2031.

What technology trends shape future student leasing?

Online booking platforms and blockchain-enabled rent payments streamline leasing, reduce defaults, and enhance tenant experience across German university cities.

Page last updated on: