Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.37 Billion |

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

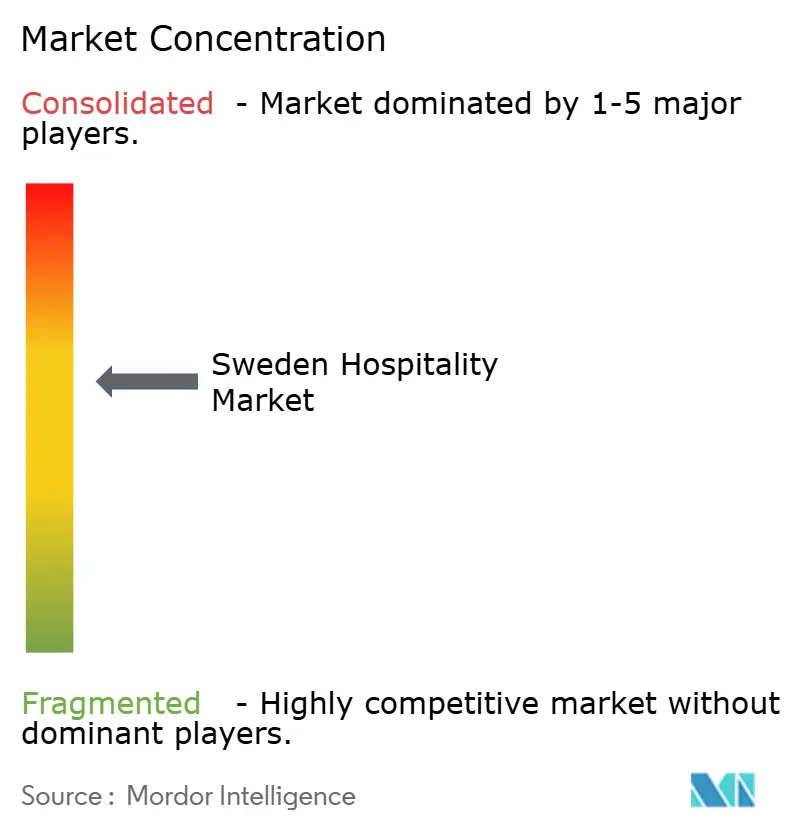

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Hospitality Market Analysis by Mordor Intelligence

The Sweden Hospitality market size is expected to grow from USD 6.37 billion in 2025 to USD 6.63 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 4.07% CAGR over 2026-2031.

The market is growing as operators unlock pent-up international demand, accelerate digital transformation, and capitalize on nationwide transport upgrades. Strong chain-hotel pipelines into Tier-2 cities, a mobile-first push that converts more OTA traffic into direct bookings, and rapid eco-label adoption all enhance revenue quality while aligning with Boverket’s carbon limits, reinforcing the Sweden hospitality market as a Nordic benchmark for sustainable growth. Counterweights, volatile construction costs, heavy OTA fees, and the 2027 retrofit mandate compress margins, yet operators deploy hedging contracts, loyalty programs, and green-finance instruments to defend profitability. These interacting forces underpin a balanced expansion trajectory that supports investment appetite and continued job creation across the Sweden hospitality market.

Key Report Takeaways

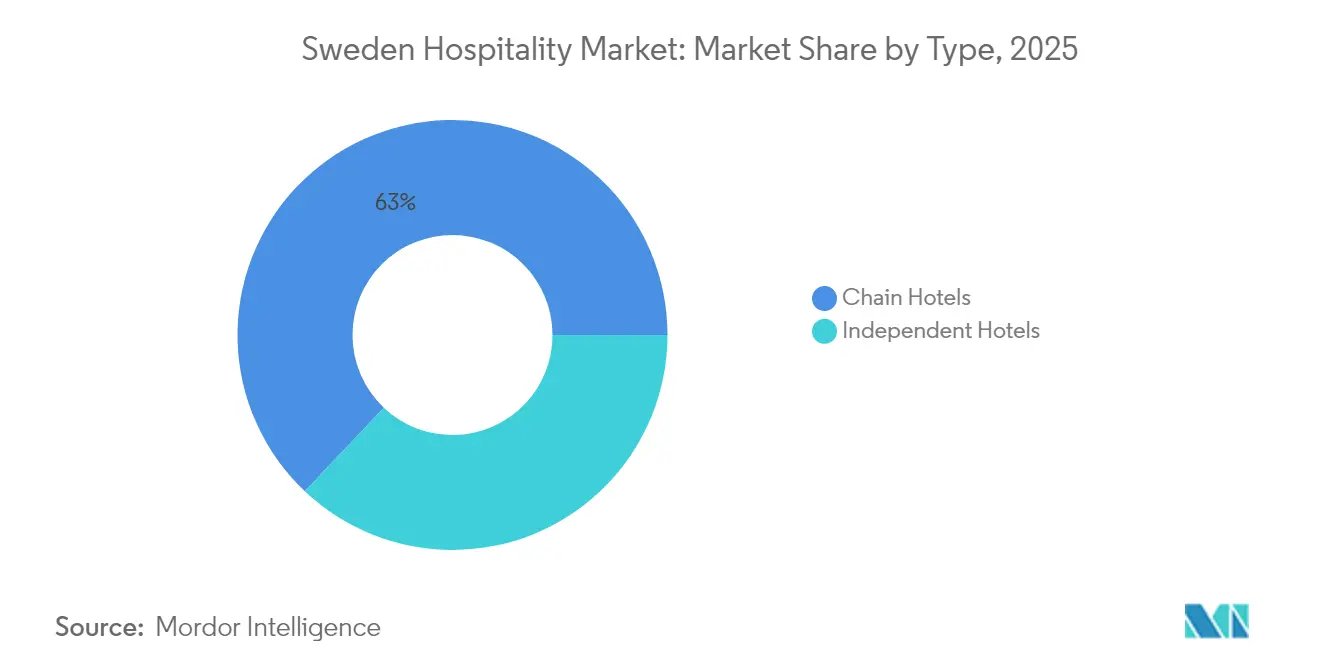

- By type, chain hotels held 62.95% of the Sweden hospitality market share in 2025, whereas independent hotels are forecast to register a 6.49% CAGR through 2031.

- By accommodation class, mid- and upper-mid-scale properties accounted for 46.90% of the Sweden hospitality market size in 2025, while luxury hotels are projected to grow at an 7.88% CAGR to 2031.

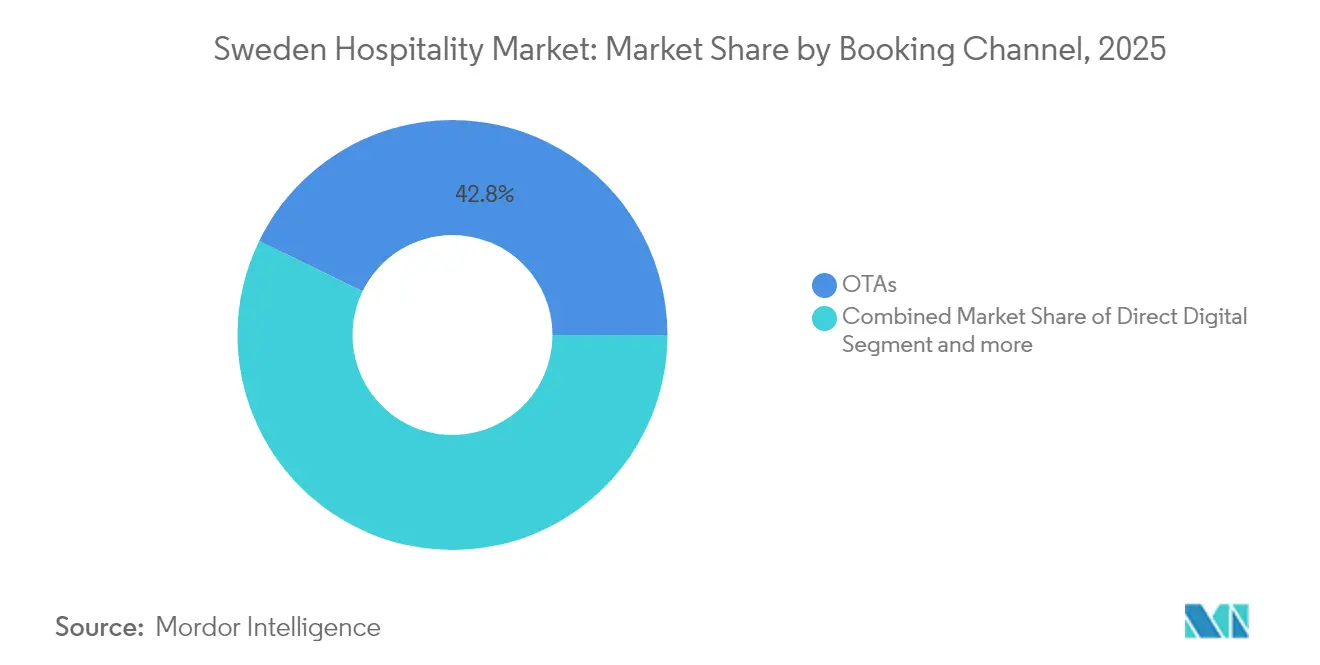

- By booking channel, OTAs captured 42.80% of the Sweden hospitality market share in 2025, but direct digital bookings are expanding at an 7.95% CAGR through 2031.

- By geography, Stockholm County generated 38.95% of sales of the Sweden hospitality market in 2025, whereas South Sweden is on course to post a 7.05% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in inbound leisure traffic | +1.2% | National – Stockholm, coastal hubs strongest | Medium term (2–4 years) |

| Chain-hotel expansion into Tier-2 Swedish cities | +0.8% | Central & Northern secondary markets | Long term (≥ 4 years) |

| Mobile-first direct booking adoption | +0.6% | National – urban centres lead | Short term (≤ 2 years) |

| Eco-label demand influencing room choice | +0.4% | National – metro areas strongest | Medium term (2–4 years) |

| Government night-train subsidies spurring domestic trips | +0.3% | Northern rail corridors | Short term (≤ 2 years) |

| Work-cation policies boosting rural weekday occupancy | +0.2% | Rural Central & Northern Sweden | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic rebound in inbound leisure traffic

Tourism export receipts rose in 2024, and guest nights from the United States hit all-time highs, signalling that the Sweden hospitality market has transcended its 2019 baseline and is now benefiting from extended trip lengths and higher average daily rates. Cultural milestones such as the 80th anniversary of Pippi Longstocking, new attractions like the Hilma af Klint Centre, and year-round festivals enhance destination appeal and stretch demand into shoulder seasons[1]Visit Sweden, “Sweden 2025 – A Year Of Exciting Travel News Ahead,” cision.com . Premium-oriented travellers gravitate toward boutique and luxury inventory, lifting RevPAR in Stockholm, Gothenburg, and coastal resort corridors. According to the Office of National Statistics, operators leverage revenue-management tools to capture upside, while government data shows sector employment at 124,000 FTEs, ensuring service capacity and reinforcing the Sweden hospitality market’s readiness for further influx.

Chain-hotel expansion into Tier-2 Swedish cities

Large groups are reallocating capital to Jönköping, Helsingborg, Uppsala, and Sundsvall, where land prices, incentives, and demographic shifts improve project yields. In February 2024, Strawberry, led by Petter Stordalen, and property investment firm Slättö have announced the launch of a new hotel chain targeting the Nordic market. The partnership focuses on establishing properties in strategic locations, delivering high-quality services, and adhering to robust sustainability standards. The venture aims to develop a minimum of 20 hotels within the next ten years[2]Nordic Property News, “Strawberry and Slättö launch new hotel chain,” nordicpropertynews.com . Secondary-city pipelines lessen exposure to high-cost metro zones and capture remote-worker migration trends. These projects typically secure municipal tax relief and expedited permitting, further accelerating return profiles and supporting balanced geographic growth inside the Sweden hospitality market.

Government night-train subsidies spurring domestic trips

The relaunch of overnight train services between Stockholm and Luleå/Narvik in December 2024, enabled by rail infrastructure upgrades and financing through EIB loans, represents a pivotal development in enhancing travel accessibility and affordability to Lapland and Arctic Circle destinations. Early ridership data demonstrates a significant uptick in hotel occupancy rates across key locations such as Narvik, Kiruna, and Abisko. This outcome highlights the critical role of transportation policies in driving regional tourism demand, fostering the growth of ancillary industries, and extending the operational season within Sweden's hospitality market. The initiative serves as a case study of how strategic investments in transportation infrastructure can improve regional connectivity, stimulate economic growth, and reinforce the tourism sector's value chain, ultimately contributing to the broader economic development of the region.

Work-cation policies boosting rural weekday occupancy

The implementation of hybrid work models has enabled urban residents to spend two to three weekdays in scenic rural destinations without requiring leave. This development has driven an increase in the average duration of stays at rural hotels, particularly during off-peak seasons. With 649 co-working hubs across 21 regions, service-apartment operators integrate ergonomic desks, high-speed Wi-Fi, and “meeting-room on demand” bundles, turning idle rooms into productive spaces[3]Tillväxtverket, “Turismstatistik,” tillvaxtverket.se . The reduction in weekday vacancy risks, coupled with an increase in rural ADRs during traditionally low-demand months, contributes to a structural improvement in the performance of Sweden's hospitality market. This development highlights a strategic shift aimed at optimizing revenue generation and addressing seasonal demand fluctuations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction & labour cost inflation | −0.9% | National – metro hotspots | Short term (≤ 2 years) |

| High OTA commission pressure | −0.6% | Nationwide | Medium term (2–4 years) |

| 2027 Boverket energy-efficiency retrofit mandate | −0.4% | National – legacy assets | Medium term (2–4 years) |

| Short-term-rental substitution in coastal resorts | −0.3% | Stockholm & Gothenburg archipelagos | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High OTA commission pressure

Booking.com maintains a dominant position in the online travel agency (OTA) market, accounting for 71% of the total market volume. Its commission structure, which charges hotels a rate of 15%, significantly impacts the gross operating profits of hotels. This high commission rate reduces profit margins, creating financial challenges for hotels and influencing their overall operational efficiency within the competitive hospitality industry[4]HOTREC, “2024 Hotel Distribution Study,” hotel.report . Independents most exposed to OTA usage face marketing outlays they can ill-afford, perpetuating dependency cycles in the Sweden hospitality market. Regulatory relief via the Digital Markets Act is years away, forcing hotels to invest in meta-search partnerships and CRM-driven remarketing now.

2027 Boverket energy-efficiency retrofit mandate

The Sweden hospitality market is witnessing significant challenges as 1980s-era properties, which often lack modern insulation and HVAC recovery systems, require retrofit capital expenditures that can equate to their entire asset value. Non-compliance with updated regulatory standards exposes these assets to operational restrictions and potential valuation reductions, creating financial strain for property owners. This situation is driving an accelerated pace of asset divestitures as stakeholders aim to mitigate risks associated with non-compliance and declining valuations. Additionally, the market is experiencing increased consolidation as larger players acquire non-compliant or underperforming assets to leverage economies of scale and modernize operations. These dynamics underscore the critical need for strategic investment in retrofitting and compliance to sustain competitiveness in the evolving market landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Dominance Drives Standardization

Chain operators hold a dominant position in the Sweden hospitality market, controlling 62.95% of the total inventory. This dominance is underpinned by their ability to leverage procurement power, establish integrated loyalty ecosystems, and utilize their financial resources to manage retrofit costs effectively. These factors collectively reinforce their leadership and competitive advantage within the market. In contrast, independent properties are demonstrating resilience and growth, achieving a robust CAGR of 6.49%. By focusing on authentic design elements and integrating local supply chains, these independent operators are successfully attracting experience-driven travellers who prioritize unique and personalized stays.

Chain brands are strategically refining their market segmentation to enhance competitiveness and expand their customer base. Initiatives include launching economy-focused sub-brands like Scandic Go, introducing lifestyle-oriented offerings such as Strawberry’s Home Hotel, and converting office spaces into upscale accommodations to maximize asset utilization. These efforts are designed to appeal to a broader audience while countering the growing presence of international competitors, including IHG’s voco brand. Meanwhile, independent operators are adopting innovative approaches to remain competitive, such as implementing cloud-based property management systems (PMS), forming regional marketing partnerships, and obtaining Nordic Swan certification to align with sustainability trends. Although the consolidation of chain operators is expected to increase their collective market share by 2030, the creativity and adaptability of boutique establishments ensure that independent properties will continue to play a significant and dynamic role in shaping the Sweden hospitality market.

By Accommodation Class: Luxury Acceleration Amid Mid-Scale Stability

The luxury segment of Sweden's hospitality market is anticipated to grow at a robust CAGR of 7.88% through 2031, driven by increasing demand from affluent travellers in the U.S., Germany, and the Middle East. These travellers are showing a strong preference for Nordic-inspired designs, wellness-focused amenities, and outdoor adventure experiences, which are becoming key differentiators in the market. Despite this growth, the mid- and upper-mid-scale segment remains a significant player, accounting for 46.90% of the market share, as it continues to attract business travellers and families with its reliable services and competitive pricing. This segment's ability to balance affordability with comfort has positioned it as a resilient choice for a diverse customer base. The coexistence of these segments highlights the evolving dynamics of Sweden's hospitality market, where premium offerings and value-driven options cater to distinct consumer needs.

Luxury hotels are increasingly integrating provenance storytelling and unique brand narratives to enhance their value proposition, as seen in examples like Hernö Gin Hotel, which leverages its craft-distillery connection. These properties are also investing heavily in wellness suites and premium facilities to justify higher ADR and attract high-spending clientele. In contrast, mid-scale hotels are focusing on upgrading in-room technology and communal spaces to maintain competitiveness and counteract downward ADR pressures from economy chains. The rise of service-apartment hybrids reflects the growing influence of corporate relocation and work-cation trends, which are extending average stay durations and reshaping accommodation preferences. Meanwhile, budget formats are capitalizing on modular wood construction and lean staffing models to expand into smaller urban centers, ensuring comprehensive nationwide coverage and contributing to the overall growth of Sweden's hospitality market.

By Booking Channel: Digital Transformation Reshapes Distribution

In 2025, OTAs captured 42.80% of total bookings, reflecting a sustained dependence on meta-search platforms for discovery, despite hoteliers' efforts to drive direct sales. The growth of direct digital channels, which are expanding at a CAGR of 7.95%, is attributed to the adoption of advanced features such as personalized push notifications, seamless one-click payment systems, and loyalty programs with points-rich membership tiers. These innovations are designed to enhance customer retention and foster long-term loyalty, providing a competitive edge to hoteliers. The increasing reliance on direct digital pipelines highlights the shift in consumer preferences toward convenience and tailored experiences. This trend underscores the importance of integrating technology-driven solutions to remain competitive in the evolving hospitality market.

Corporate and MICE (Meetings, Incentives, Conferences, and Exhibitions) channels have stabilized at lower absolute volumes, primarily due to the rise of hybrid events that reduce traditional room block bookings. However, this shift has simultaneously driven demand for flexible studio spaces and advanced green-screen technology packages, catering to the changing needs of corporate clients. The contraction of wholesale and retail travel agents continues, as consumer self-booking habits dominate the market, further reshaping the distribution landscape. Operators who effectively analyze channel performance data are better positioned to implement rate fencing strategies that minimize revenue cannibalization and safeguard brand equity. The increasing fluidity across distribution channels not only empowers customers with greater choice but also enhances operational efficiency and adaptability within Sweden's hospitality sector.

Geography Analysis

In Sweden’s hospitality market, Stockholm County represents the largest geographic sub-segment in 2025, holding a significant share of 38.95%. Looking ahead to the period from 2026 to 2031, South Sweden is expected to be the fastest-growing sub-segment, with a compound annual growth rate (CAGR) of 7.05%. Stockholm remains the sovereign demand hub, combining corporate headquarters, creative industries, and world-class conference venues that secure dependable weekday business flow. American leisure arrivals surged in 2024, and cultural programming such as Nobel Week Lights sustains winter tourism, enhancing occupancy seasonality. High land costs and stringent energy codes push developers toward office-to-hotel conversions, exemplified by IHG’s voco Stockholm Kista and Scandic Go’s 11-story retrofit in Solna, demonstrating flexible capital deployment that maintains Stockholm’s edge within the Sweden hospitality market.

Malmö’s knowledge hub, Lund’s academic cluster, and Helsingborg’s port logistics create stable weekday traffic, while the Österlen and Halland coasts generate strong summer leisure demand. Ferry routes from Travemünde and Rostock, plus the Copenhagen airport feeder market, keep arrivals flowing. Gothenburg and its West Sweden hinterland maintain balanced demand through auto manufacturing expos, port throughput, and cultural festivals such as Way Out West. Archipelago communities, confronting overtourism, consider guest levies and zoning to cap short-term rentals, potentially channelling demand toward regulated inventory and tightening ADR discipline. Northward, new night-train rolling stock reduces Stockholm–Narvik journey times to 16.5 to 18.5 hours, spurring winter-sports and aurora-tourism flows that underpin multi-season occupancy gains. Rural municipalities invest in fibre broadband, making week-long work-cations viable and embedding year-round demand into the Sweden hospitality market fabric.

Regulatory Landscape

Sweden hospitality operators manage lodging registration, alcohol licensing, and tightening building energy requirements. From January 1, 2025, Lag (2024:1082) om hotell- och pensionatsrörelser moved hotels and guest houses above defined thresholds (at least nine guests or five guest rooms) from a permit model to a notification-based requirement administered via Polismyndigheten, which reduces administrative friction for new and small-scale supply while maintaining oversight.

In food and beverage, alcohol service continues to depend on serveringstillstånd, with municipalities and national rules shaping compliance burdens for hotels with bars and restaurants. In April 2026, the Government (Regeringen) proposed changes (Prop. 2025/26:221) to remove legal requirements for food service and specialized kitchens as conditions for alcohol serving licenses, with the proposal framed for entry into force on June 1, 2026, subject to final enactment. Separately, the report context points to a 2027 Boverket energy-efficiency retrofit mandate as a key compliance milestone affecting capex planning and asset transactions for legacy properties.

Value Chain Analysis

The Sweden hospitality value chain begins with real estate owners and developers, covering new builds, conversions, and retrofits, and then passes to hotel operators (chains and independents) that manage staffing, brand standards, and day-to-day operations. Upstream inputs include construction and retrofit contractors, energy and utilities, furniture and equipment, and food and beverage procurement. With Nordic supply chains relying meaningfully on imported intermediate goods and raw materials, FX and logistics volatility remain relevant to operating costs.

Downstream, demand and distribution flow through direct digital channels and OTAs (42.80% of bookings in 2025), along with corporate/MICE and destination marketing bodies that influence visitation. Trade associations such as Visita, together with restaurant and purchasing networks (for example, Svenska Krögare), support industry coordination, training, and procurement leverage, while wholesalers such as Martin & Servera anchor F&B supply to thousands of customers across Sweden. Labor availability is a recurring constraint across the chain: broader tourism employment reached about 155,000 people in 2025 (2.8% of national employment), with lodging employing about 38,000, and operators use self-check-in, PMS upgrades, and process automation to protect service levels under wage and staffing pressure.

Competitive Landscape

The Sweden hospitality market is dominated by a handful of leading operators who control a substantial share, benefiting from economies of scale in procurement, strong loyalty programs, and access to capital that helps mitigate supply-chain disruptions and pricing shocks. One major player exemplifies this dominance with a large pipeline of over 7,000 rooms across various brand tiers, from economy to upper-mid-scale segments. Despite this concentration, the market remains open to new entrants, with international groups re-entering through asset-light management models to minimize risk while rapidly expanding their presence. This dynamic creates a competitive environment where both incumbents and newcomers coexist. Market consolidation continues as rising retrofit costs encourage strategic acquisitions and partnerships.

Technology plays a pivotal role in shaping competition, with major chains investing heavily in AI-powered chatbots, attribute-based pricing systems, and centralized customer relationship management platforms that boost repeat bookings by significant margins. Smaller, independent operators respond by forging strong local partnerships and offering unique experiences such as farm-to-table dining, craft beer collaborations, and outdoor equipment rentals. These niche offerings are increasingly featured in OTA filter searches, helping independents compete effectively despite smaller inventories. To scale efficiently without overextending financial resources, many smaller chains are turning to franchising and asset-light management agreements. This balance of innovation and strategic growth sustains competitive intensity in the market.

Consolidation efforts extend beyond Sweden’s borders, with Swedish investors actively acquiring assets abroad to diversify and enhance returns. A notable example is the acquisition of a major hospitality group operating in Ireland and the U.K., valued at approximately USD 1.46 billion, signaling a search for yield in international markets while maintaining operational synergies through flexible lease arrangements. Domestically, strong demand, favorable financing options for environmentally friendly projects, and a broad mix of traveler segments contribute to sustained attractive risk-adjusted returns. As the market evolves, operators focus on balancing growth, sustainability, and guest experience differentiation. Overall, the Sweden hospitality sector remains robust, dynamic, and poised for continued transformation.

Sweden Hospitality Industry Leaders

Scandic Hotels Group AB

Nordic Choice/Strawberry Hotels

Elite Hotels of Sweden

First Hotels

Best Western Hotels & Resorts (Sweden)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two whitespace areas stand out: (1) product upgrading in secondary leisure nodes and (2) decarbonization-led demand shaping for meetings and events. As Tier-2 city pipelines expand beyond the largest metros, operators can reposition older assets into experience-led boutique and heritage concepts in ski and coastal towns, using sustainability credentials (for example, Nordic Swan-aligned positioning referenced in the report context) to win eco-sensitive travelers and to differentiate beyond peak seasons.

On the demand enablement side, Sweden is putting more tourism infrastructure into structured data and planning tools that hospitality providers can commercialize. Visit Sweden launched a National API in September 2025 that consolidates structured tourism data for about 14,000 hotels and experiences, enabling hotels, OTAs, and third-party developers to build discovery, itinerary, and conversion tools aimed at improving direct booking performance and packaging. In parallel, Tillväxtverket and Visit Sweden have been running AI-driven strategic foresight pilots in 2026 (including Region Halland and Vadstena), giving destinations and hotel clusters a shared basis to manage seasonality, capacity, and climate-related adaptation measures. Industry advocacy also highlights regulatory and tax levers that could change unit economics for restaurants and hotel F&B, with Visita bringing forward a 2026 election agenda and Almedalen Week policy asks focused on modernized alcohol legislation and labor-cost relief.

Recent Industry Developments

- July 2026: Scandic Hotels Group AB secured a new long-term financing framework totaling SEK 7.5 billion. The funding structure strengthens liquidity and improves refinancing flexibility, supporting continued renovations and pipeline execution in a market facing higher retrofit and construction costs.

- February 2026: Strawberry announced an investment of over SEK 400 million to renovate nearly 1,500 rooms across key Stockholm properties including Clarion Hotel Sign, Clarion Hotel Stockholm, and Hotel C. The renovation program points to a quality and sustainability-focused capex cycle in the largest demand hub, with upgraded inventory positioned to capture higher-yield leisure and corporate segments.

- July 2024: Scandic Go signed conversion projects in Gothenburg and Umea totaling 276 rooms for a 2026 launch. The conversions expand budget supply using adaptive reuse, a route that shortens time-to-market versus greenfield builds and aligns with tighter urban permitting and energy-code constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue generated from hospitality stays in Sweden, where spending is captured from paid accommodation sold to domestic and inbound travelers through direct and intermediary booking routes.

Scope exclusions: passenger transport, packaged tours, and food-only venues that do not provide paid lodging are excluded from the revenue pool.

Segmentation Overview

- By Type

- Chain Hotels

- Independent Hotels

- By Accommodation Class

- Luxury

- Mid & Upper-Mid-scale

- Budget & Economy

- Service Apartments

- By Booking Channel

- Direct Digital

- OTAs

- Corporate / MICE

- Wholesale & Traditional Agents

- By Geographic Region

- Stockholm County

- West Sweden (incl. Gothenburg)

- South Sweden (incl. Skåne/Malmö)

- Central & Northern Sweden

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by anchoring the size of Sweden lodging demand using public series that reconcile year to year. We rely on sources such as Statistics Sweden accommodation statistics, Swedish Agency for Economic and Regional Growth tourism releases, and Eurostat tourism indicators to understand nights, occupancy movement, and long-run travel patterns.

To sharpen assumptions, we also review documents such as listed company annual reports, investor presentations, and reputable business press coverage on pricing and capacity additions. Where available, we use paid subscriptions for company financials and intelligence, news and financials, and a patent database to check renovation and service innovation activity that can influence rate progression. These desk sources are illustrative only, and many other references were used for data collection, cross-checks, and clarification during the work.

Primary Interviews and Surveys

Primary validation was completed through expert interviews and short surveys with accommodation operators, booking and distribution specialists, and advisors who track Sweden travel demand. We used these discussions to confirm how occupancy, ADR style pricing, and channel mix changed across key regions, and then to align our assumptions with what is being seen in the market today.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 38% | |

| Smaller Players: 22% | Managers: 50% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where national accommodation demand is reconstructed from room nights and bed nights, then translated into revenue using price indicators that reflect the Swedish market. When the model is being formed, we track occupancy rate movement, available room supply additions and removals, average daily rate direction, seasonality of leisure peaks versus business weekdays, and the booking channel split between direct and intermediary routes.

After the first pass is created, selective bottom-up approximations are used to sanity check totals, including sampled property performance checks and operator-level revenue discussions by region, before adjustments are locked. When public data is thin for smaller areas, we fill gaps using proxy indicators such as regional tourism nights and capacity utilization patterns, and then validate reasonableness through follow-up expert checks. For forecasting, we use scenario analysis supported by a simple multivariate regression on demand drivers, with the variable outlooks aligned to what interviewees expect for pricing, capacity, and travel demand normalization.

Data Validation & Update Cycle

Validation is done in layers so obvious errors are caught early and small drifts do not compound. Outputs are compared against independent signals such as lodging nights trends, supply growth, and reported pricing direction, and any large variances are investigated before sign-off.

A second analyst review is applied to assumptions, currency handling, and year-on-year continuity, followed by a final consistency pass across tables and narrative. Reports are refreshed annually, and interim updates are triggered when material events occur, such as abrupt demand shifts, major capacity changes, or regulatory changes affecting accommodation operations. Before delivery, we run a fresh check so clients receive the latest updated view based on newly available public data and recent interview feedback.

Mordor Intelligence's Sweden Hospitality Market Size Compared Against Other Published Estimates

Published market sizes for Sweden hospitality can differ even when they look similar at first glance, because the counted revenue pool and the timing of the demand and price assumptions are not always the same. Differences usually show up around what is treated as hospitality, which years are used to anchor recovery effects, and how price growth is handled.

The main gap comes from whether the estimate stays focused on paid accommodation revenue in Sweden, or whether it blends in adjacent travel and tourism spending, and Mordor Intelligence keeps the scope tied to lodging classes and booking channels while keeping rate and occupancy assumptions aligned to observable Sweden accommodation indicators.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.37 B (2025) | |

| Industry Data Portal A | USD 5.76 B (2024) | Uses a different base year and can reflect a broader hospitality framing with mixed segmentation layers, which may lead to a lower starting point versus a 2025 accommodation-focused recovery year. |

| Trade Aggregator B | USD 7.63 B (2028) | Reported figure is for accommodation services revenue in 2028 in EUR terms and then converted, so year mismatch and currency timing can inflate or deflate comparisons versus a current-year USD market value. |

The table shows that the spread is mostly explained by scope choices, base-year selection, and currency and timing treatments rather than by a single arithmetic issue. By tying the size to clear demand units like nights and capacity, and then checking pricing logic with market participants, we keep the estimate traceable to inputs a buyer can understand and replicate.

Key Questions Answered in the Report

How large is the Sweden hospitality market in 2026 and what growth is projected?

The Sweden hospitality market size is USD 6.63 billion in 2026 and is expected to reach USD 8.09 billion by 2031, reflecting a 4.07% CAGR.

Which hotel category is expanding most quickly nationwide?

Luxury properties show the fastest rise, advancing at an 7.88% CAGR as affluent visitors seek premium Nordic experiences.

What proportion of rooms do chain hotels control?

Chain brands account for 62.95% of keys, underscoring their dominant presence across the Sweden hospitality market.

Which region offers the highest forecast growth?

South Sweden leads with a 7.05% CAGR through 2031 thanks to coastal tourism rebound and cross-border connectivity.

How are operators reducing OTA dependency?

The hospitality industry is leveraging mobile-first direct booking applications, enhanced loyalty programs, and data-driven remarketing strategies. These initiatives are effectively redirecting a notable share of bookings from Online Travel Agencies (OTAs) to proprietary platforms.

What environmental regulation will affect hotels most over the next five years?

The 2027 Boverket retrofit mandate requires all large buildings to meet stringent energy-efficiency standards and undergo life-cycle carbon assessments.

Page last updated on: