Europe Student Accommodation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

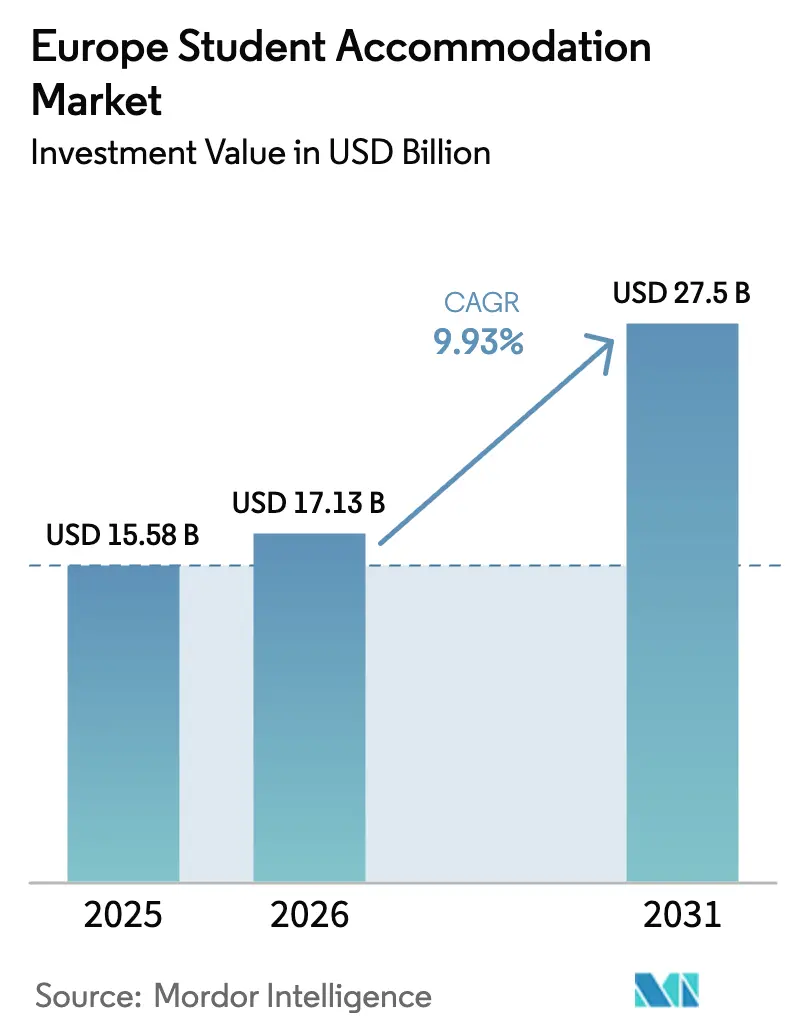

| Base Year Market Size (2025) | USD 15.58 Billion |

| Market Size (2026) | USD 17.13 Billion |

| Market Size (2031) | USD 27.5 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Student Accommodation Market Analysis by Mordor Intelligence

The Europe student accommodation market size is expected to grow from USD 15.58 billion in 2025 to USD 17.13 billion in 2026 and is forecast to reach USD 27.50 billion by 2031 at 9.93% CAGR over 2026-2031.. The market is supported by persistent demand–supply imbalances in major university cities, which sustain high occupancy levels. Rental growth remains resilient as purpose-built student accommodation continues to attract strong pre-leasing activity. Rising international student mobility across the UK, Germany, France, Spain, and the Netherlands is a key structural growth driver. Increasing participation in higher education and cross-border study programs further strengthens demand fundamentals. Institutional investors are expanding allocations to the sector, attracted by stable, long-duration cash flows and defensive characteristics. Cross-border capital deployment is particularly strong in core UK markets and emerging Southern European hubs. Supportive policy measures and housing-focused initiatives are helping accelerate planning approvals and project funding. Developers are increasingly adopting modular construction methods to manage rising land and material costs. ESG-certified and energy-efficient buildings are gaining traction as sustainability becomes a priority for investors and students alike. Digital leasing platforms and data-driven pricing strategies are enhancing occupancy optimization and tenant retention.

Key Report Takeaways

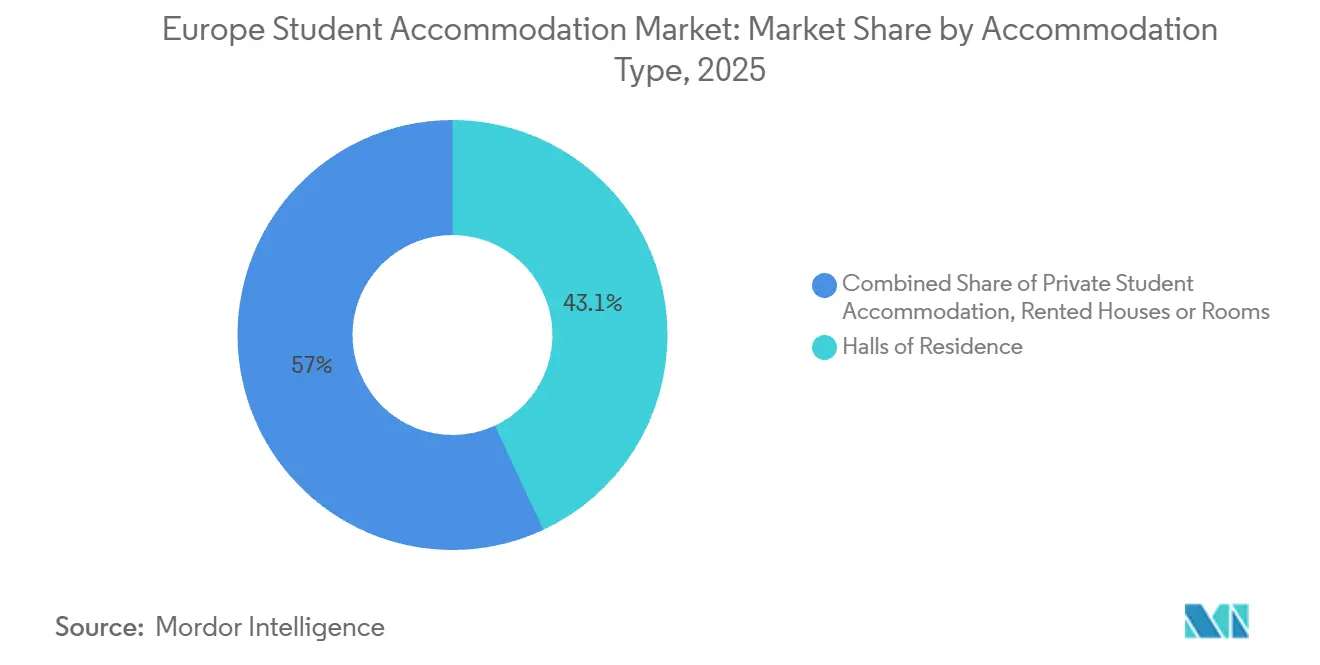

- By accommodation type, Halls of Residence captured 43.05% of the Europe student accommodation market size in 2025, while Private Student Accommodation is forecast to expand at a 6.03% CAGR through 2031.

- By location, city-center properties accounted for 56.72% of the Europe student accommodation market in 2025, and periphery developments are advancing at a 7.48% CAGR as improved transit connectivity supports outlying districts.

- By mode, offline channels accounted for 71.65% of the Europe student accommodation market in 2025, while online platforms are growing at a 9.12% CAGR on the back of virtual tours and instant reservations.

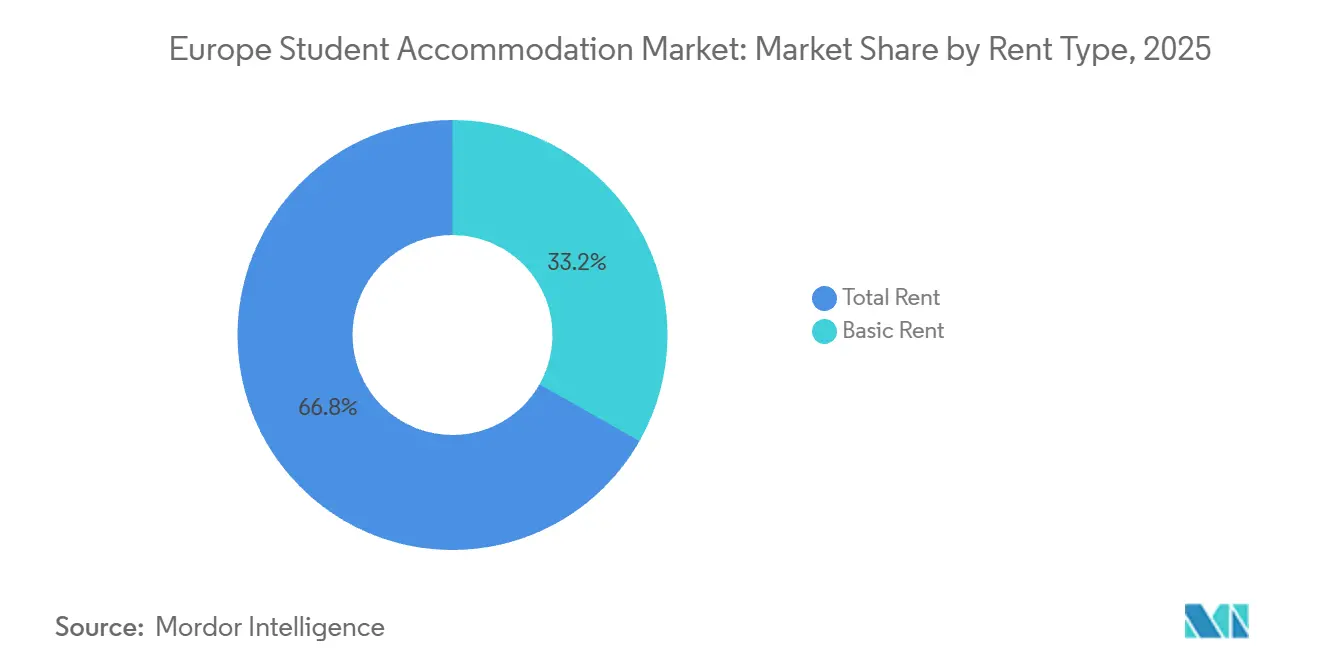

- By rent type, Total Rent packages held 66.78% of the Europe student accommodation market size in 2025, and Basic Rent contracts are growing at a 4.75% CAGR as budget-sensitive cohorts navigate rent caps in select countries.

- By geography, the United Kingdom commanded 37.95% of the Europe student accommodation market size in 2025, while Spain records the fastest regional CAGR at 7.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple regions, with Europe contributing to the overall trajectory. The outlook on worldwide united kingdom student accommodation market reflects how these are expected to evolve collectively.

Europe Student Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing International Student Enrollment Across Europe | +2.8% | Global, strongest in the UK, Germany, France, Spain, Italy | Medium term (2-4 years) |

| Supply Shortages in Tier-1 University Cities | +2.4% | UK, France, Germany, Spain, Netherlands | Long term (≥ 4 years) |

| Growing Institutional Investment in PBSA Assets | +1.9% | Pan-European, concentrated in Southern Europe, the UK, Germany, and France | Medium term (2-4 years) |

| Government Reforms Accelerating Planning Approvals | +1.2% | UK, Ireland, Netherlands, select German states | Medium term (2-4 years) |

| Modular and Micro-Living Units Reducing Construction Costs | +0.9% | UK, Ireland, Nordics, Germany | Long term (≥ 4 years) |

| ESG-Certified Buildings Driving Higher Occupancy | +0.8% | Northern Europe, expanding to Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing International Student Enrollment Across Europe

International enrollment expanded strongly into 2026, following a 16.3% increase between 2019 and 2024, with EU-27 totals surpassing 1.76 million in 2023, as Germany, France, and the Netherlands attracted the largest cohorts among member states. Germany hosted 423,200 foreign students, while France recorded 276,200 and the Netherlands 169,500, reinforcing diversified demand anchors across multiple language markets within the Europe student accommodation market.[1]Source: Eurostat, “Learning Mobility Statistics,” Eurostat, ec.europa.eu. Affordability and living costs feature in student decision-making, and policy support, such as Germany’s Skilled Immigration Act and Spain’s post-study work reforms, improve study-to-work transitions that sustain length of stay. Stricter visa regimes in other destinations have redirected flows, reflected in higher non-EU applications to UK universities into 2026 and broadened interest across Continental campuses with English-taught programs. Conversion from application to arrival remains constrained by local housing bottlenecks, with many inbound students citing accommodation availability as a key uncertainty that drives pre-booking and the adoption of all-inclusive packages in the Europe student accommodation market.

Growing Institutional Investment in PBSA Assets

Institutional investment in European purpose-built student accommodation (PBSA) is rising sharply as investors respond to strong demand and limited supply. Across Europe, there are an estimated two million PBSA beds, with a growing share owned by private institutional operators. Investors surveyed by Savills, representing roughly 16 percent of private PBSA stock with about 132,000 beds and an estimated USD 29.9 billion in assets, are planning significant portfolio expansion. These investors expect to increase the number of beds they own by around 70 percent over the next few years, adding approximately 92,500 beds and deploying an additional USD 25.9 billion of capital into the sector. PBSA has been ranked among the most sought-after living sectors for future investment, with many investors targeting the asset class and planning substantial deployments.[2]Source: Savills, “European Purpose‑Built Student Accommodation Investment Barometer Report,” Savills, savills.com. Even with this anticipated growth, overall PBSA provision levels are expected to increase only modestly relative to total student numbers, highlighting the continuing opportunity for institutional capital to address the ongoing supply shortfall across European markets.

Government Reforms Accelerating Planning Approvals

Across Europe, governments and policy makers are introducing planning and housing reforms to help unlock student accommodation supply and streamline development processes. In the UK, reforms are being proposed to shorten approval windows for large schemes that include purpose-built student accommodation, aiming to reduce delays and improve delivery timelines. Ireland has introduced new planning frameworks that designate targeted urban development zones around major cities to fast-track student housing projects and other residential developments. In the Netherlands, national strategies and regional action plans are being pursued to increase housing capacity and address persistent shortages of student beds through coordinated planning. Other countries are also recognizing the need to simplify permitting procedures and integrate student housing into broader housing affordability strategies, reflecting a growing policy focus on expanding supply and reducing barriers to entry for new projects across European markets.[3]Source: European Commission, “Commission Takes Action for More Affordable Housing Across Europe,” European Commission, ec.europa.eu.

Modular and Micro-Living Units Reducing Construction Costs

Modular techniques reduce waste and embodied carbon, and industry research shows up to a 40% cut in both when compared with traditional onsite methods, which helps sponsors manage cost inflation risk in the Europe student accommodation market. Volumetric construction is strongest in the UK and Ireland because unit repetition, tight sites, and speed-to-market align well with PBSA requirements.[4]Source: Modular Building Institute, “About MBI’s European Council & Growth Opportunities,” Modular Building Institute, modular.org. Developers also shrink average studio sizes and expand micro-living formats to improve affordability without sacrificing community spaces and building performance. Operators increasingly refurbish older blocks rather than demolish to control capex and emissions, with retrofit programs offering sizable savings relative to rebuild pathways in the Europe student accommodation market. Country programs in the Nordics favor timber and industrialized methods, while Southern Europe moves up the learning curve as international investors back pilot projects and pipeline platforms across Spain and Portugal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Land and Construction Expenses | -1.8% | UK, Netherlands, France, Germany, Nordics | Long term (≥ 4 years) |

| Challenging Zoning and Rent-Cap Regulations | -1.4% | France, Spain, Germany, Scotland, Ireland | Medium term (2-4 years) |

| Competition from Short-Stay Rental Platforms | -0.7% | Spain, Italy, France, Portugal, UK | Short term (≤ 2 years) |

| Declining Domestic Student Enrollment in Some Regions | -0.6% | Netherlands, Portugal, Denmark, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Land and Construction Expenses

Escalating development costs continue to constrain growth in the Europe student accommodation market. Per-bed build costs have increased significantly in core markets, driven by higher materials, labor, and financing expenses, which compress returns and challenge the feasibility of new projects, particularly in dense urban cores. Across the continent, construction cost inflation remains elevated relative to long-term averages, adding pressure to developers’ pro forma models and increasing their sensitivity to land pricing. Limited land availability in constrained city centers further exacerbates cost pressures, prompting some investors to look to secondary cities with lower land and permitting costs. While institutional equity supports well-capitalized sponsors, tighter lending criteria and conservative loan terms make financing more difficult for smaller development schemes. These dynamics are slowing the pace of new supply and sustaining the existing supply–demand imbalance, which continues to place upward pressure on rents and occupancy levels in the student housing sector.

Challenging Zoning and Rent-Cap Regulations

Complex and varied local regulations are creating obstacles for student housing development and influencing revenue prospects in key European university cities. In several markets, rent control measures and zoning restrictions limit how much operators can increase rents and where purpose-built student accommodation can be developed, which can reduce financial incentives and lengthen approval timelines for new projects. Policy uncertainty and regulatory complexity have been cited by developers and investors as major concerns, with some deferring planned investments due to unclear frameworks and shifting rules in priority locations. In some regions, heightened tenant protections and rent caps have dampened investor confidence and made it more difficult to deliver new beds at the scale needed to meet demand. This regulatory patchwork continues to challenge the rollout of new student housing supply, contributing to persistent undersupply and maintaining pressure on affordability and development viability across the European market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation Type: Private Assets Narrow Share Gap

Halls of Residence captured 43.05% of the European student accommodation market share in 2025, maintaining a strong base among first-year students who value on-campus proximity and inclusive pricing aligned with university calendars. Private Student Accommodation is forecast to expand at a 6.03% CAGR through 2031, reflecting investor appetite for professionally managed assets that offer gyms, study areas, and high-spec connectivity that drive resilience in occupancy. International students account for a larger share of PBSA tenants than of total student populations across Continental Europe, which supports demand for furnished, all-inclusive contracts that simplify utility management and payments. Investor focus has shifted to larger platforms and pipeline-led strategies to capture operating efficiencies, ESG performance, and brand-led demand in the Europe student accommodation market. Over time, accreditation frameworks and national quality codes reinforce a preference for regulated PBSA over fragmented private rentals, thereby supporting standardization in service and safety for the European student accommodation market.

The Europe student accommodation market for Private Student Accommodation is projected to expand at a 6.03% CAGR between 2026 and 2031, narrowing the revenue gap with Halls through asset upgrades, digital leasing, and value-add refurbishments aligned with net-zero objectives. Hybrid co-living formats complement PBSA by offering shorter stays and shared amenities, which can absorb exchange and Erasmus cohorts who require flexible terms within university semesters. Regulatory tightening in private HMO markets is redirecting some demand to PBSA, aided by transparent pricing and bundled rent models that reduce bill shock during peak energy seasons in the Europe student accommodation market. As planning reforms take effect and capital costs stabilize, professionally managed assets are positioned to capture continued share gains, especially in metros with rising international enrollments and large university clusters. Brand differentiation now spans community programming, wellness, and study support, increasing stickiness and renewal rates for PBSA operators in the core and growth cities of the Europe student accommodation market.

By Location: Periphery Gains as Transit Improves

City-center properties accounted for 56.72% in 2025, helped by proximity to campus clusters, transit hubs, and urban amenities that support premium rents and high year-round utilization in the Europe student accommodation market. As affordability challenges mount, periphery locations are advancing at a 7.48% CAGR through 2031, supported by rail and metro upgrades that compress travel times and expand development options where land is more available. Investors calibrate between prime city cores and super-prime regional locations, balancing yield differentials with leasing depth, brand awareness, and local permitting dynamics in the Europe student accommodation market. Markets with high average city-center rents like Amsterdam are pushing students to nearby cities, which broadens catchments and diversifies occupancy risk during intake peaks. Transit-oriented development near new lines and interchanges is a growing theme in Copenhagen, Madrid, and Milan, with operators clustering beds around multi-campus footprints for route redundancy and convenience.

Provision rates show wide dispersion between Northern and Southern Europe, which influences pricing strategies and the sequencing of new beds within city pipelines across the Europe student accommodation market. Pipelines in 2025 covered only a small fraction of deficits in the largest cities, reinforcing the case for phased deliveries and mixed typologies that match demand by year of study and budget bands. Campuses with higher international shares achieve stronger PBSA rental premia, which supports near-campus positioning even as periphery gains momentum with improved transit links in the Europe student accommodation market. Fire safety and building safety rules raise retrofit needs for older city-center blocks, which also redirects some capital to greenfield periphery sites with modern compliance from day one. Over the forecast, balanced exposure to center and periphery assets can help stabilize occupancy and rate growth through seasonal and macro cycles in the Europe student accommodation market.

By Rent Type: All-Inclusive Dominance Persists

Total Rent packages held 66.78% in 2025, signaling clear tenant preference for single-invoice predictability that covers utilities, insurance, and connectivity within a furnished setting typical of PBSA in the Europe student accommodation market. The model simplifies compliance in rent-capped cities and reduces disputes over variable bills, which supports operator satisfaction scores and renewals during peak leasing cycles. Basic Rent contracts are growing at a 4.75% CAGR through 2031, serving price-sensitive students who want more control over energy usage and lease length in heavily regulated markets of the Europe student accommodation market. Student accommodation operators across Europe are increasingly offering flexible lease durations and bundled pricing packages to better serve exchange students, internship participants, and those whose stays do not align with standard academic contracts, reflecting evolving tenant preferences and mobility patterns. Despite this shift, rental growth in purpose built student accommodation continues to outpace broader inflation in key markets, supporting stable cash flows for well located and professionally managed assets, even as affordability concerns rise.

Energy price volatility and demand for predictable living costs are reinforcing the appeal of all inclusive rent structures that cover utilities and services, particularly among international tenants seeking budget certainty. University managed housing markets in some regions have shown rent growth that exceeds that of private PBSA, highlighting the influence of price benchmarks and the need for tiered product offerings to attract students across income segments. In markets with stringent rent controls and regulatory caps, operators are placing greater emphasis on value added amenities and differentiated service offerings to maintain competitiveness within permitted pricing frameworks. To mitigate operating cost pressures, many providers are adopting smart building systems and energy efficiency measures that help stabilize overall rent structures and support renewals. Over time, combining both bundled total rent and basic rent offerings enables operators to optimize occupancy and capture demand from diverse student segments. These dynamics underscore ongoing affordability challenges and shape how pricing strategies evolve in the European student accommodation sector.

By Mode: Digital Channels Accelerate Bookings

Offline leasing accounted for 71.65% of bookings in 2025, reflecting continued preference for on-site viewings and in-person interactions among first-year students and parents who prioritize safety and community fit in the Europe student accommodation market. Online channels are projected to grow at a 9.12% CAGR through 2031, as virtual tours, instant reservation tools, and AI-guided recommendations streamline cross-border moves and speed up pre-arrival commitments. Online marketplaces and digital platforms now list a large and growing number of accommodation units across major European cities, improving liquidity and transparency for students comparing neighborhoods, prices, and amenities. These platforms are enabling easier search, booking, and comparison of student housing options, which enhances decision making and supports more fluid movement between markets. Student accommodation providers are increasingly adopting dynamic pricing tools and online engagement flows to optimize occupancy prior to term start, supported by strong pre leasing trends in recent academic cycles. Integration of smart building sensors and operational efficiency software helps control utility and maintenance costs while tying into enhanced digital user experiences during the lease term.

Online marketplaces and digital platforms are playing an increasingly important role in the European student accommodation market by listing a wide range of units across major university cities, giving students greater transparency when comparing locations and amenities and streamlining the search process through virtual tools and booking functionality. Operators are leveraging dynamic pricing engines and digital engagement workflows to optimise occupancy ahead of academic terms, supported by strong pre‑leasing performance through online channels. Integration of smart building technologies and efficiency software also enhances operational performance and contributes to improved digital user experiences throughout the lease lifecycle. Many providers are investing in customer relationship management systems, marketing automation, and seamless payment integration to support frictionless check‑in, renewals, and communication with residents. As omnichannel strategies evolve, combining virtual tours, digital contracts, and online support helps protect occupancy levels, reduce acquisition costs per lease, and meet the expectations of increasingly digital‑native student tenants across Europe.

Geography Analysis

The United Kingdom remains the largest national market with 37.95% of the Europe student accommodation market in 2025, supported by well developed purpose built student accommodation infrastructure and strong demand from both domestic and international students. High application volumes and increased enrollments at leading universities are driving strong pre leasing activity and near full occupancy in major cities. Robust investment activity has continued, with developers and institutional sponsors advancing substantial pipelines in anticipation of planning reforms that could accelerate approvals and supply delivery. The UK’s attractiveness to overseas students further reinforces demand, underpinning rental growth and stable income streams for well located assets. Operators are also adjusting pricing strategies and expanding amenity offerings to address affordability pressures and enhance competitiveness.

Spain is the fastest-growing market with a 7.55% forecast CAGR through 2031, driven by high university enrollment rates and significant gaps between student demand and available purpose built beds. Madrid and Barcelona, in particular, exhibit strong rental fundamentals, which have attracted institutional capital eager to capitalise on tight supply and favourable yields. Cross border investors are increasingly active in the Iberian market, validating its appeal through large portfolio acquisitions and development partnerships. National policy improvements aimed at supporting student mobility and post study work opportunities are expected to further lengthen stays and bolster housing demand. Regional rent regulations are shaping supply expansion, encouraging development in cities with more supportive pricing environments.

Germany hosts one of the largest international student populations in the EU and offers a broad base of investable university cities with persistently low vacancy rates and rising rents that support strong project underwriting. Despite existing rent control frameworks in some cities, developers and investors are targeting secondary and regional markets with lower land costs and quicker permitting to expand portfolios. Large cross border sponsors are launching dedicated PBSA platforms with ESG objectives to tap this sustained net demand and long term growth potential. Policy adjustments in certain regions have eased development constraints, allowing student housing on repurposed commercial land and improving project feasibility. These dynamics, combined with ongoing international mobility and skilled graduate retention policies, underpin continued growth prospects for the student accommodation market across Germany and wider Europe.

Analysis of the united kingdom student accommodation market by Mordor Intelligence spans multiple other regional evaluations across Asia, supported by country-level insights for Germany, United Kingdom, India, and United States, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Europe student accommodation market is moderately concentrated, with the largest operators controlling a meaningful share of purpose‑built beds while fragmentation persists, especially in regional and secondary cities. Established players such as Unite Students, iQ Student Accommodation, Student Roost, GSA, and Scape have developed significant footprints in key markets, leveraging development pipelines, acquisitions, and partnerships with universities to strengthen their positions. Mergers, joint ventures, and platform‑level transactions have supported investor confidence by reinforcing stable occupancy and long‑dated cash flows in core hubs. New entrants and re‑entries in markets such as Denmark, Spain, and Germany show continued portfolio building where demand remains strong and provision rates lag student growth. Brand differentiation through amenities, digital leasing, and community programming is helping operators improve pre‑lease velocity and renewal rates across competitive environments.

Strategic themes such as ESG delivery, smart building technology, and embedded campus partnerships are shaping operator strategies across Europe. Many providers report utility savings and improved environmental performance through smart controls and energy efficiency initiatives that help mitigate cost pressures and stabilize margins. Joint ventures with universities continue to de risk development and secure steady nominations, particularly in large on campus schemes with longer concession horizons. ESG credentials, including green building certifications and sustainability targets, are increasingly featured in marketing and financing efforts, enhancing access to institutional capital. Technology also plays a growing role in yield management, with AI driven pricing tools and digital service portals supporting occupancy resilience and elevating student experiences.

White space opportunities remain in parts of Southern Europe and selected secondary cities across Germany, Italy, and Spain, where provision rates lag enrolment growth and planning reforms are beginning to shorten approval timelines. To capture this potential, investors are forming country-level platforms to accelerate delivery, while development lenders are selectively reopening financing for experienced sponsors with strong pre-leasing records and ESG specifications. Multi-country operators are also experimenting with integrated offerings that blend student housing with co-working and short-stay components to optimize year-round utilization and community engagement. Brand scale, cost discipline, and proximity to campuses remain central to competitive advantage as platforms look to expand their presence. As demand continues to grow and supply constraints persist, operators that combine operational excellence with sustainability leadership are well-positioned to gain market share through 2031.

Europe Student Accommodation Industry Leaders

Unite Students

iQ Student Accommodation

Student Roost

GSA

Scape

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: MCR Property Group launched a USD 484 million (GBP 360 million) Flow Student Platform to scale UK PBSA, and Maslow Capital committed GBP 116.6 million to a Wembley scheme, signaling sustained lender and sponsor commitment to the sector.

- February 2026: Greece began an USD 21.8 million (Euro 18.6 million) renovation of the Athens Student Residence, a state‑run university housing facility in central Athens, signing a contract to upgrade the aging building. The project will cover more than 10,000 m² and focus on energy‑efficiency improvements, structural reinforcement, and modernizing outdated infrastructure to enhance living conditions.

- January 2026: CDP launched a USD 703.8 million (EUR 599 million) PNRR initiative for new university housing in Italy, targeting 60 projects by 2027 to accelerate supply in cities such as Rome and Milan.

- January 2026: Ardian and Rockfield expanded their pan-European student housing venture by 1,500 beds through acquisitions in Milan, Bordeaux, and Barcelona, reinforcing exposure to undersupplied Southern European cities.

Europe Student Accommodation Market Report Scope

While studying away from home, finding a place to stay is an important factor, as a student will be living comfortably during his stay and equipped with his daily needs. As Europe has become a hub for global higher education, the student housing market plays a major role. The market is divided by the type of housing (dorms, rented houses or rooms, and private student housing), location (city center, outskirts), type of rent (basic rent, total rent), mode (online, offline), and country (Germany, Iceland, Ireland, Italy, France, Belgium, Norway, Rest of Europe). The study keeps track of the key market parameters, factors that affect growth, and student accommodation service providers in the industry. This helps to back up market estimates and growth rates for the next few years. The report offers market size and values (in USD million) during the forecasted years for the above segments.

| Halls of Residence |

| Rented Houses or Rooms |

| Private Student Accommodation |

| City Center |

| Periphery |

| Basic Rent |

| Total Rent |

| Online |

| Offline |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Accommodation Type | Halls of Residence |

| Rented Houses or Rooms | |

| Private Student Accommodation | |

| By Location | City Center |

| Periphery | |

| By Rent Type | Basic Rent |

| Total Rent | |

| By Mode | Online |

| Offline | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe student accommodation market?

The Europe student accommodation market size is USD 15.58 billion in 2025 and is projected to reach USD 27.50 billion by 2031 at a 9.93% CAGR.

Which segments are leading by share and growth within Europe’s student housing?

Halls of Residence led with 43.05% revenue share in 2025, while Private Student Accommodation is the fastest-growing at a 6.03% CAGR through 2031.

How do macro and policy trends affect the Europe student accommodation market?

EU recognition of student housing as critical infrastructure and national planning reforms are accelerating approvals, while rent caps and zoning rules in select cities temper revenue upside in 2026.

Where are the biggest geographic opportunities across Europe?

Spain records the fastest growth at a 7.55% CAGR and Germany offers depth across 70+ investable cities, while the UK remains the largest market by share with mature PBSA infrastructure.

What operating models are gaining traction among students?

Total Rent packages dominate with 66.78% share due to bundled utilities and predictability, and online bookings are growing at a 9.12% CAGR with virtual tours and instant reservations.

Page last updated on: