Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.90 Billion |

| Market Size (2026) | USD 8.30 Billion |

| Market Size (2031) | USD 10.60 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Hospitality Market Analysis by Mordor Intelligence

The Argentine hospitality market size is expected to grow from USD 7.90 billion in 2025 to USD 8.30 billion in 2026 and is forecast to reach USD 10.60 billion by 2031 at a 5.02% CAGR over 2026-2031. Domestic demand has stayed resilient amid peso volatility, while inbound flows softened in 2025 as the exchange-rate stance reduced Argentina’s price appeal for foreign visitors. Even so, brand pipelines from global chains point to sustained investment, with multi-year conversions and select greenfield projects in Buenos Aires, Patagonia, and Cuyo targeting recovery segments that prize reliability, loyalty benefits, and standardized service. Booking dynamics remain shaped by platform reach and margin recapture strategies, as OTAs command the largest share while direct digital grows fastest on brand-site optimization and loyalty incentives. Geography continues to concentrate revenue in Buenos Aires, while Patagonia leads growth through expedition travel and premium outdoor experiences that attract international travelers, regardless of short-term currency moves. Public stimulus such as PreViaje has supported domestic travel spending, offset part of the inbound shortfall, and preserved capacity across under-saturated destinations.

Key Report Takeaways

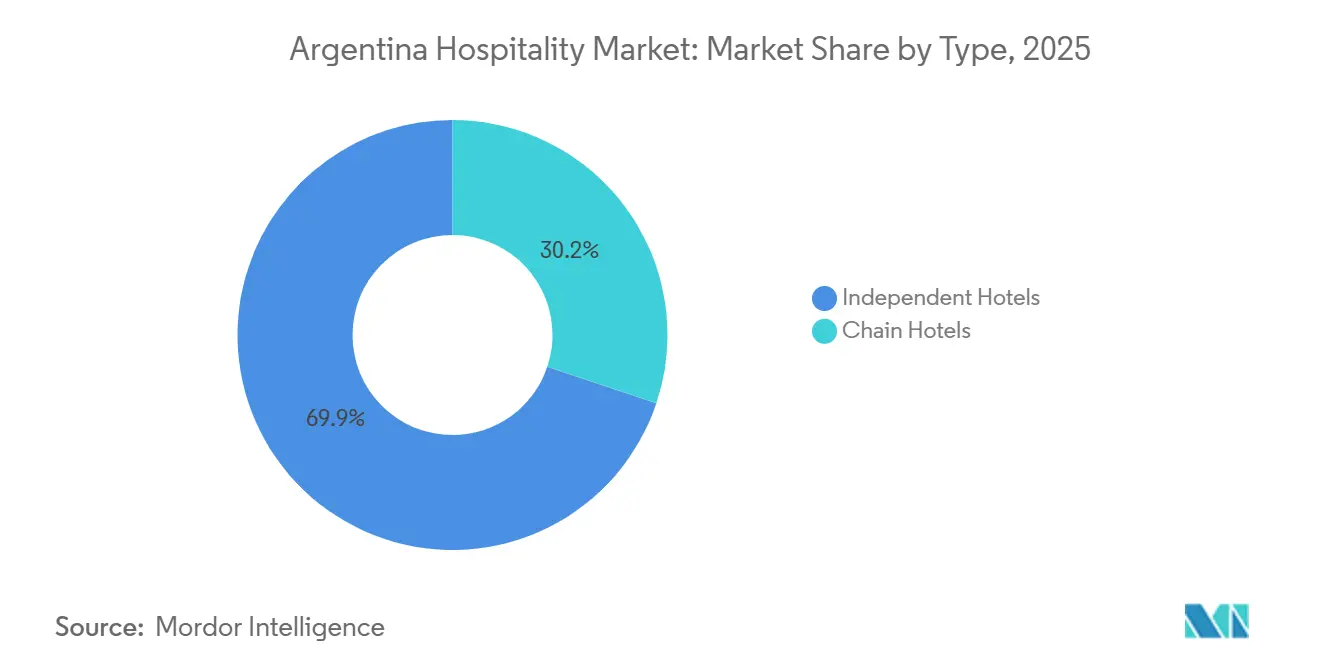

- By type, independent hotels led the Argentine hospitality market with 69.85% market share in 2025, while chain hotels are projected to expand at a 7.85% CAGR through 2031, the fastest across this segmentation.

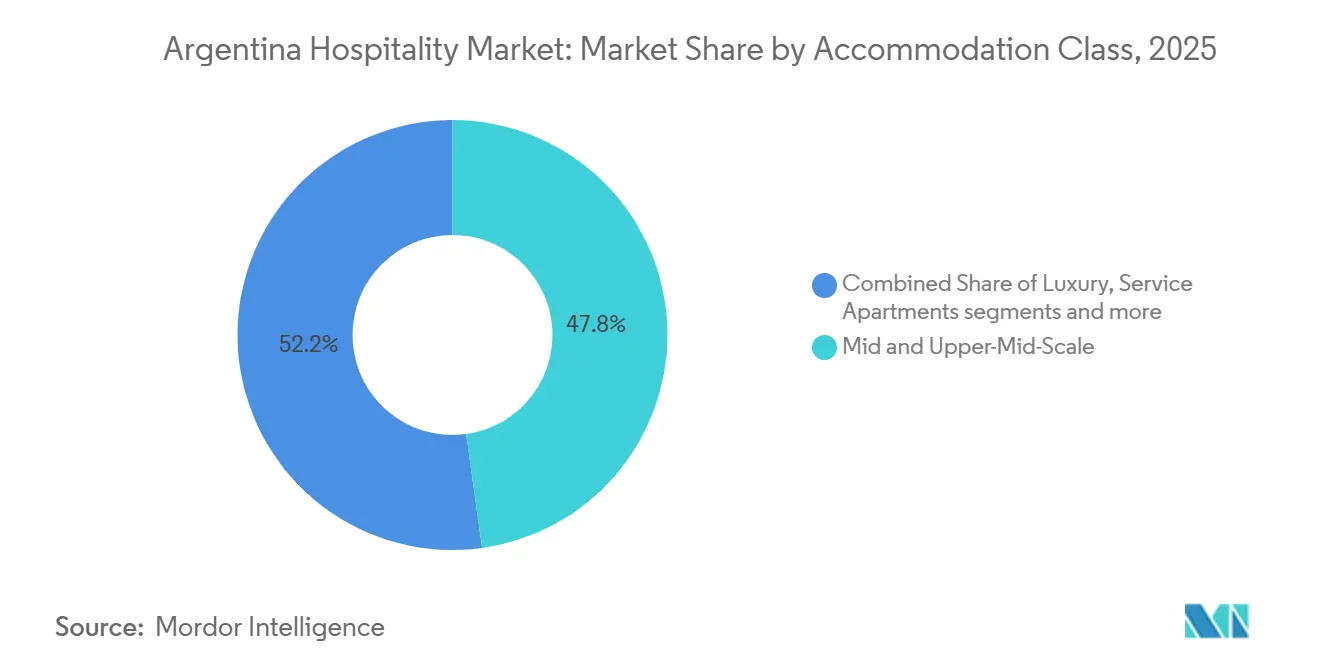

- By accommodation class, mid- and upper-mid-scale accounted for 47.80% of the Argentine hospitality market share in 2025, while luxury is forecasted to grow at an 8.05% CAGR to 2031, the fastest in this segment.

- By booking channel, OTAs held a 41.10% market share of the Argentine hospitality market in 2025, while direct digital is projected to register the highest CAGR at 9.68% through 2031.

- By geography, the Buenos Aires region accounted for 40.10% of the Argentine hospitality market share in 2025, while the Patagonia region is expected to be the fastest-growing, with a 7.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak pesos drive growth in inbound tourism | +1.2% | National, with early gains in Buenos Aires, Patagonia, and Mendoza | Medium term (2-4 years) |

| "Pre-viaje" program encourages domestic travel | +0.9% | National, higher uptake in off-peak destinations, including Bariloche and Salta | Short term (≤ 2 years) |

| Global hotel chains expand operations in Argentina | +1.1% | Buenos Aires for conversions, Patagonia for greenfield, Cuyo for resort plays | Long term (≥ 4 years) |

| Corporate and mice travel shows strong recovery | +0.7% | Buenos Aires, Córdoba, Rosario business hubs | Medium term (2-4 years) |

| Buenos Aires digital-nomad visa attraction | +0.3% | Buenos Aires, Mendoza, spill-over to Bariloche | Medium term (2-4 years) |

| Enotourism boosts lodge demand in the Cuyo region | +0.5% | Mendoza and San Juan wine regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Peso Drives Growth in Inbound Tourism

Exchange-rate dynamics shape inbound affordability, and the policy shift that raised the peso’s effective value during 2025 reduced Argentina’s historical price advantage, which corresponded with a 19.7% year-over-year slip in foreign arrivals that weighed on the Argentina hospitality market[1]James Grainger, “Outbound trips by Argentines up 38% year-on-year, doubling foreign arrivals,” Buenos Aires Times, batimes.com.ar. News flow during 2025 documented month-specific declines in tourist entries, reinforcing that the currency stance can invert traditional competitiveness until equilibrium returns. IMF guidance suggests depreciation toward a more sustainable level by late 2026, which would restore purchasing-power parity for visitors and support a rebound in urban luxury, wine circuits, and Patagonian lodges that elevate the Argentina hospitality market. Operators that recalibrate rate fences and enhance value-included packages are positioned to capture deferred demand once pricing signals normalize and confidence returns among North American and European travelers who typically book multi-night stays. Public policy that supports formal accommodations, including the VAT treatment for foreign guests, should amplify the impact of a restored exchange-rate advantage on the Argentine hospitality market once macro distortions fade.

"Pre-Viaje" Program Encourages Domestic Travel

PreViaje continues to stimulate domestic spending by reimbursing a portion of eligible travel outlays through a prepaid mechanism, thereby increasing occupancy in off-peak windows and spreading demand beyond marquee months in the Argentine hospitality market. Program research reported that millions of beneficiaries and tens of thousands of jobs were supported, while formal supplier enrollment requirements enhanced tax visibility and broadened the formal accommodation base. Operators in Patagonia, the Northwest, and other seasonally volatile destinations reported steadier bookings, validating the role of targeted credits in smoothing occupancy and enabling clearer workforce planning. As a fiscal instrument, PreViaje remains subject to annual budget review, which defines it as a short-term stabilizer rather than a structural driver, but its effect on dispersing demand has been meaningful for the Argentine hospitality market.

Global Hotel Chains Expand Operations in Argentina

Global brands are extending their presence through a mix of conversions in major cities and greenfield projects in resort corridors, strengthening segmentation depth and loyalty capture across the Argentine hospitality market. Accor acquired 17 management agreements across the region, coupled with a USD 130 million renovation plan to reflag assets under the Swissôtel, Mercure, Mercure Living, and ibis Styles brands, a move that deepens midscale and premium inventory in Argentina [2]Accor, “Accor expands its network in the Americas with the addition of 17 hotels,” Accor Press, press.accor.com. Hilton expanded its Caribbean and Latin America pipeline and validated Argentina’s long-term appeal with new signings in Ushuaia and Buenos Aires, adding lifestyle- and business-oriented flags to regional choices that are boosting the Argentina hospitality market. [3]Hilton, “Hilton Ends 2025 with Robust Luxury and Lifestyle Growth,” Hilton Stories, stories.hilton.com. Choice Hotels debuted with Radisson Blu Bariloche in 2025 and announced a Radisson Red near Rosario, elevating branded offerings in Patagonia and the country’s interior, where upscale demand is growing. Hyatt complemented its Buenos Aires luxury base by greenlighting Casa Duhau in Mendoza’s Alto Agrelo under The Unbound Collection, anchoring the wine corridor with a high-end lodge that integrates premium residential components to support multi-night leisure trips in the Argentine hospitality market.

Corporate and MICE Travel Shows Strong Recovery

Business and conference travel has been improving from pandemic troughs, with Córdoba hosting scientific congresses and preparing for high-profile regional events that diversify revenue beyond leisure in the Argentine hospitality market. The national tourism board highlighted Argentina’s positioning at regional trade shows in 2025, signaling coordinated destination marketing that supports city bureaus and venue operators. The GBTA LATAM Business Travel Forum event in Buenos Aires reinforced corporate travel’s gradual normalization, with meeting planners and procurement leaders prioritizing reliability and connectivity as booking criteria that benefit branded hotels in the Argentine hospitality market. Airport and venue upgrades in provincial capitals, including Córdoba, are expanding the addressable base for regional events, while hotels are redesigning meeting spaces and integrating hybrid capabilities to serve clients who mix in-person and remote formats. Macroeconomic uncertainty continues to temper multi-year contracts, yet the return of incentive travel and regional congresses is lifting weekday occupancy and average rates across the Argentine hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent macro-economic challenges and inflation | -1.1% | National, with acute pressure on EBITDA margins in Buenos Aires | Medium term (2-4 years) |

| High peso interest rates are impacting capex | -0.7% | Tier-2 cities, including Salta, Mendoza, and Mar del Plata, face local-credit constraints. | Medium term (2-4 years) |

| Increased property taxes on Buenos Aires hotels | -0.4% | Buenos Aires City, particularly the premium districts | Short term (≤ 2 years) |

| Oversupply of short-term rentals in core cities | -0.6% | Buenos Aires, Bariloche, Mendoza city centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Macro-Economic Challenges and Inflation

The operating backdrop has been volatile, with a hyperinflationary pulse in 2024 that forced hotels to reprice frequently and delayed upgrades that rely on imported inputs priced in hard currency, which compressed profitability in the Argentine hospitality market. INDEC-reported inflation metrics into early 2026 showed moderation from 2025’s full-year rate, yet monthly readings remained elevated and kept pressure on wage negotiations, utilities, and consumables that move faster than headline room revenue in the Argentine hospitality market. Corporate disclosures in 2025 from regional operators noted revenue softness in Argentina tied to inflation-recession dynamics and currency depreciation, which reduced reported results when translated to parent-company currencies. IMF program documents have framed a disinflation path into late 2026, but the risk of under-delivery is non-trivial, so investor sentiment remains cautious, translating into selective capital deployment and elevated return hurdles in the Argentine hospitality market. Properties with access to hard-currency contracts or internal balance-sheet support are better positioned to navigate the current cycle, while leveraged independents face higher refinancing risk and constrained renovation budgets that can erode competitiveness within the Argentine hospitality market.

High Peso Interest Rates are Impacting CAPEX

The central bank’s easing cycle reduced the benchmark rate multiple times into early 2025, but real borrowing costs stayed high once adjusted for ongoing inflation, which preserved a tough financing hurdle for developers in the Argentine hospitality market. Official series reported elevated borrowing rates across personal and current-account credit, which are restricting peso-denominated hotel CAPEX and complicating renovation timelines, especially in tier-2 cities with limited access to foreign-currency credit lines. Multinationals have relied on parent balance sheets to fund rebranding and renovations, as seen in Accor’s regional transaction and associated refurbishment plan that will reflag and upgrade properties under established banners. Independent owners without external funding sources delay room and systems upgrades, which can create brand-standard compliance gaps over time and weaken positioning versus chains that can absorb soft cycles across broader portfolios in the Argentine hospitality market. The interest-rate path into 2026 depends on consistent disinflation and reserve accumulation, and until those conditions materialize, the cost of local capital will continue to slow greenfield hotel development across the Argentine hospitality market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Scale Remains Large While Chains Gain Momentum Through Conversions

Independent hotels accounted for 69.85% of revenue in 2025, confirming their scale advantage, while chain hotels are projected to expand at a 7.85% CAGR through 2031, signaling faster brand-led share capture in the Argentine hospitality market. Family-owned assets in hubs such as Mar del Plata, Bariloche, and Palermo have long relied on local expertise and flexible pricing, yet the balance is shifting as franchises bring loyalty reach, central reservations, and playbooks that ease operational complexity across the Argentine hospitality market. Conversion platforms like City Express by Marriott and midscale flags from Accor enable faster onboarding of independent properties, reducing downtime while delivering brand recognition that supports pricing power in the Argentine hospitality market. New entrants add to competitive intensity, as seen when Choice Hotels introduced Radisson Blu in Bariloche with an upscale positioning that targets outdoor luxury travelers who value consistency and curated amenities. Regulatory enforcement in Buenos Aires that requires ENTUR registration for short-term rentals increases the compliance burden for informal operators, modestly improving the relative appeal of licensed hotels across the Argentine hospitality market.

Independent operators with a strong identity and direct-booking focus can preserve margins by partnering with niche tour firms in wine corridors and adventure routes, though digital marketing scale remains a structural edge for chains in the Argentine hospitality market. Portfolio transactions and brand-led reactivations have accelerated, as highlighted by the acquisition and rebranding of multiple former Selina properties into Socialtel, a move aimed at younger travelers via hybrid hostel-hotel formats and curated experiences within the Argentine hospitality market. Hotels that invest in revenue management systems, channel mix optimization, and guest engagement will be better positioned as conversion-led growth expands the reach of global loyalty programs, steering bookings toward branded properties in the Argentine hospitality market. As chains win more conversions, owners gain access to procurement savings and operating standards that stabilize service delivery through the cycle, while independents maintain an edge in highly localized experience design inside the Argentine hospitality industry.

By Accommodation Class: Mid-Scale Leads by Size, Luxury and Service Apartments Outpace in Growth

Mid- and upper-mid-scale properties accounted for 47.80% of revenue in 2025, anchoring demand from business travelers and tour groups seeking reliable amenities and value in the Argentine hospitality market. Luxury is projected to expand at a 6.15% CAGR through 2031. Growth underscores the price resilience among high-net-worth travelers whose trip selection prioritizes distinctive experiences, design, and culinary credentials that justify premium rates in the Argentine hospitality market. New branded extended-stay properties in Buenos Aires entering via affiliations add distribution power without major changes to operating models, helping capture multi-week bookings that stabilize cash flow in the Argentine hospitality market. Budget and economy formats face intense competition from regulated short-term rentals that appeal to price-sensitive travelers, a dynamic that raises the bar for service differentiation and direct-booking incentives across the Argentine hospitality market.

In wine tourism corridors, Michelin Key recognitions in 2025 elevated the brand equity of vineyard-integrated lodges, reinforcing the appeal of immersive stays that combine tasting rooms, gastronomy, and spa services within the Argentine hospitality market. Winery destinations reported strong guest volumes and measurable local employment, which bolsters the investment case for upscale and luxury properties that align with regional oenophile itineraries and high willingness to pay in the Argentine hospitality market. With chains planning renovations and reflags across midscale and premium brands, the quality gap between older independents and refreshed branded assets is set to widen unless owners accelerate refurbishments that meet evolving traveler expectations in the Argentine hospitality industry. Across classes, properties that integrate coworking areas, wellness, and curated local experiences improve conversion and rate integrity in a landscape where choice breadth and transparency continue to increase in the Argentine hospitality market.

By Booking Channel: OTAs Hold Scale, Direct Digital Grows Fastest on Loyalty and Margin Goals

OTAs captured 41.10% of bookings in 2025 and remain critical for reach, discovery, and last-minute transactions, especially for independents that lack global marketing budgets in the Argentine hospitality market. At the same time, direct digital channels, including brand sites and apps, are forecast to grow at a 9.68% CAGR through 2031, as hotels deploy best-rate guarantees, member-only perks, and personalized offers that reclaim margins otherwise ceded to intermediaries in the Argentine hospitality market. Global loyalty ecosystems are central to this shift, with brands cross-selling inventory to regional members and bundling points-earning with ancillary benefits that increase on-platform conversion inside the Argentine hospitality market. Corporate and MICE channels, while smaller by share, are normalizing, aided by destination marketing and event wins that direct weekday demand to hotels with upgraded meeting spaces and reliable connectivity in the Argentine hospitality market. Wholesale and traditional agents remain relevant for multi-stop itineraries that combine Buenos Aires, Iguazú, and Patagonia, though their share is likely to edge down as direct and OTA channels improve localized content and itinerary-building tools in the Argentine hospitality market.

Hotels that invest in SEO, content localization, and conversion-rate optimization are capturing a greater share of repeat bookings at lower acquisition costs, supporting more stable profitability through cycles in the Argentine hospitality market. Independent properties that lack the tools or staffing to execute continuous A/B testing and CRM personalization remain more reliant on OTAs’ algorithmic demand engines, which is a trade-off between fill and fee leakage in the Argentine hospitality market. The Argentina hospitality market share for OTAs will remain significant, but channel mix should gradually tilt toward direct as brands automate merchandising, improve mobile UX, and integrate flexible payment options that match traveler preferences. Compliance rules in Buenos Aires that require ENTUR registration numbers for all online listings also reinforce the advantage of formal hotels over non-compliant short-term rentals that risk delisting, thereby improving the quality of supply across regulated channels in the Argentine hospitality market.

Geography Analysis

The Buenos Aires region accounted for 40.10% of revenue in 2025, reflecting its role as the main international gateway, corporate hub, and cultural center for the Argentine hospitality market. Inbound softness in 2025, tied to currency policy, led to weaker international arrivals, placing greater weight on domestic and regional travelers to fill urban inventory in the Argentine hospitality market. Short-term rental density in neighborhoods such as Palermo and Recoleta increased competitive pressure on independent boutique hotels, though enforcement of registration rules has improved, creating a clearer framework for compliant listings and formal operators. New branded capacity continues to enter, including a Tribute Portfolio opening in Recoleta in mid-2025 and a Hilton Garden Inn slated for Buenos Aires in 2026, both serving price-sensitive corporate accounts and higher-yield leisure demand in the Argentine hospitality market. Hotels are responding to shifting patterns by refining packages, enhancing connectivity, and tailoring experiences for remote professionals and cultural travelers who value neighborhood authenticity in the Argentine hospitality market.

Patagonia is projected to grow at a 7.82% CAGR through 2031, the fastest rate among regions, supported by expedition travel, glacier and lake access, and high-end adventure experiences that command premium rates within the Argentine hospitality market. Global brands are expanding in Patagonia, Argentina, with Radisson Blu's 2025 opening in Bariloche and Anantara's Ushuaia resort, reflecting confidence in attracting affluent international travelers seeking immersive, activity-focused experiences. Announced luxury developments for Ushuaia and other Patagonian nodes support the outlook for higher-rated inventory that complements the region’s nature-led positioning in the Argentine hospitality market. Public incentives have also helped distribute domestic demand into shoulder seasons, improving occupancy stability for operators in Bariloche and other mountain towns that are expanding adventure and wellness offerings in the Argentine hospitality market.

Beyond these anchors, Cuyo’s wine corridors in Mendoza and San Juan continue to expand visitor volumes and local employment linked to winery experiences, with association data citing more than 1.59 million guests and clear spending patterns that sustain nearby lodges and boutique hotels in the Argentine hospitality market. In the Central region, Córdoba demonstrated MICE resilience through notable congresses and a growing events calendar, which have benefited upgraded hotel inventory and improved air links, reinforcing a balanced mix of corporate and leisure demand within the Argentine hospitality market. The Litoral region around Iguazú saw new midscale-branded capacity scheduled and sustained premium performance from existing high-end properties that leverage proximity to the falls to attract international travelers into the Argentine hospitality market. In the North, branded additions in Salta and youth-focused hybrid formats expanded choice, while high-altitude wine routes in Cafayate provided distinct narratives that attract experience-driven visitors in the Argentine hospitality market. As connectivity improves and product depth broadens, dispersed demand should support a more even contribution from secondary regions to the Argentine hospitality market over the forecast period.

Competitive Landscape

Competition remains intense and diversified, with global brands deepening their presence through conversions and selective greenfield projects while independents defend share through location appeal and distinctive experiences in the Argentine hospitality market. Portfolio reshaping continued through 2025 as some owners divested assets to recalibrate capital deployment, while new entrants introduced upscale concepts in high-demand corridors, enhancing brand visibility and rate integrity in the Argentine hospitality market. Short-term rentals add a structural layer of price competition, pushing hotels to invest in service, amenities, and digital engagement to differentiate their value propositions in the Argentine hospitality market. Operators that pair data-driven revenue management with loyalty-backed direct sales are weathering cycles better than peers, suggesting ongoing share shifts toward portfolios that can fund continuous upgrades in the Argentine hospitality market.

Brands advanced several strategic moves that strengthen positioning. Accor closed a regional acquisition of management agreements and committed to a multi-year renovation program to reflag assets under well-known banners, adding scale and consistency that benefit corporate buyers in the Argentine hospitality market. Hilton announced new signings across Argentina that blend lifestyle appeal in Ushuaia with a business-ready Garden Inn in Buenos Aires, keeping its development slate balanced across use cases in the Argentine hospitality market. Choice Hotels entered with an upper-upscale opening in Bariloche and added another pipeline deal near Rosario, targeting destinations where brand scarcity can support outsized rate performance in the Argentine hospitality market. Hyatt extended its luxury reach with a planned Unbound Collection property in Mendoza’s wine country, reinforcing the premium tier that has shown steady growth in the Argentine hospitality market.

White-space opportunities span adaptive reuse of urban offices into lifestyle hotels, sustainability-forward lodges in Patagonia and vineyards, and service-apartment growth aligned to extended-stay patterns in the Argentine hospitality market. Hybrid hostel-hotel models are expanding under new ownership investing to elevate the guest experience and community programming, a strategy targeting Gen Z and millennial travelers in key cities and gateway leisure nodes within the Argentine hospitality market. As municipalities more rigorously enforce licensing for short-term rentals, formal hotels gain a clearer competitive edge, though the enforcement pace varies by district and resource availability in the Argentine hospitality market. Over the forecast horizon, portfolios that marry conversion-led growth with consistent brand standards, digital engagement, and credible sustainability programs are best placed to capture share in the Argentine hospitality market.

Argentina Hospitality Industry Leaders

Marriott International, Inc

Hilton Worldwide Holdings Inc.

NH Hotel Group (Minor)

Wyndham Hotels & Resorts Inc.

Accor S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Hilton announced robust luxury and lifestyle growth across the Caribbean and Latin America for 2025, ending the year with over 300 operating hotels and a pipeline exceeding 150 properties (21,000+ rooms). In Argentina, Hilton signed WIA Ushuaia under its Tapestry Collection and confirmed Hilton Garden Inn Buenos Aires Parque Leloir for 2026, reflecting confidence in Argentina's recovery despite macroeconomic challenges. The Tapestry Collection appeals to travelers seeking local experiences, while Garden Inn targets corporate clients prioritizing brand consistency.

- January 2026: Choice Hotels International reported record 2025 global development performance, expanding its international portfolio to nearly 160,000 rooms outside the United States (13% growth). The company entered Argentina with the Radisson Blu Bariloche (80 rooms, September 2025) and signed a Radisson Red near Rosario, advancing into under-penetrated South American markets. The upscale Radisson Blu brand positions Bariloche as a luxury-adventure destination, featuring lakeside suites, signature dining, and a wellness spa to attract high-net-worth travelers.

- November 2025: Accor entered exclusive negotiations with Royal Holiday Group to acquire 17 management agreements, encompassing 3,200 keys. This includes six All-inclusive Resorts in Mexico (1,660 keys) managed by Ennismore and eleven resorts and city hotels across Mexico, Argentina, Puerto Rico, and the USA (1,540 keys) managed by Accor PM&E Americas. The USD 79 Million consideration, paid in phases, will partially fund a USD 130 Million renovation plan for completion within 30 months.

- September 2025: Sonesta International Hotels Corporation finalized a strategic alliance with AKEN Hotels & Resorts, effective September 2, 2025, adding two properties in Córdoba: La Urumpta Hotel & Spa and Böden Hotel & Spa. The partnership integrates AKEN's wellness positioning with Sonesta's global reach and loyalty program, enabling both brands to expand their LATAM presence while offering wellness-focused experiences.

Argentina Hospitality Market Report Scope

The hospitality market comprises businesses that offer accommodation, food and beverage services, and leisure experiences, including hotels, restaurants, cafes, and tourism-related activities. It encompasses establishments such as resorts, cruise ships, and theme parks, focusing on creating welcoming environments, delivering exceptional customer service, and meeting guest needs to ensure satisfaction and comfort.

The Argentina hospitality market report is segmented by type (chain hotels, independent hotels), accommodation class (luxury, mid & upper-mid-scale, budget & economy, service apartments), booking channel (direct digital, OTAs, corporate / mice, wholesale & traditional agents), and geography (Buenos Aires Region, Central Region, Cuyo Region, Patagonia Region, Litoral Region, North Region). The market forecasts are provided in terms of value (USD).

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Buenos Aires Region |

| Central Region |

| Cuyo Region |

| Patagonia Region |

| Litoral Region |

| North Region |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Buenos Aires Region |

| Central Region | |

| Cuyo Region | |

| Patagonia Region | |

| Litoral Region | |

| North Region |

Key Questions Answered in the Report

What is the current size and growth outlook for the Argentine hospitality market?

The Argentine hospitality market is expected to grow from USD 7.90 billion in 2025 to USD 8.30 billion in 2026 and is forecast to reach USD 10.60 billion by 2031 at a 5.02% CAGR over 2026-2031.

Which region contributes the most revenue within the Argentine hospitality market?

Buenos Aires leads with 40.10% of revenue in 2025, driven by its role as the main gateway, corporate hub, and cultural center.

Which region is growing fastest in the Argentine hospitality market?

Patagonia is forecast to grow at a 7.82% CAGR through 2031 on the strength of expedition travel and premium outdoor experiences.

Which booking channels are most important for hotels in Argentina?

OTAs hold the largest share at 41.10% in 2025, while direct digital is growing fastest at a 9.68% CAGR through 2031 as brands push loyalty and margin recapture.

Which segments are expanding the fastest in the Argentine hospitality market?

Chain hotels by type and service apartments by accommodation class are the fastest-growing segments based on their projected CAGRs.

What factors are supporting demand in the Argentine hospitality market despite macro volatility?

Government travel credits, chain expansion, MICE recovery, and wine tourism are helping balance near-term headwinds.

Page last updated on: