Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.08 Billion |

| Market Size (2026) | USD 15.70 Billion |

| Market Size (2031) | USD 19.18 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Hospitality Market Analysis by Mordor Intelligence

The Switzerland Hospitality Market size is expected to grow from USD 15.08 billion in 2025 to USD 15.70 billion in 2026 and is forecast to reach USD 19.18 billion by 2031 at a 4.09% CAGR over 2026-2031. The market is benefitting from record visitation levels in 2024, with overnight stays reaching 42.8 million, a 50-year high that has established a stronger demand baseline for operators entering 2026 [1]Federal Statistical Office, “Tourism in 2024: Record Year with 42.8 Million Overnight Stays,” Federal Statistical Office, bfs.admin.ch. International stays rose to 22.0 million in 2024, while visits from the United States reached a record 4.6 million, reinforcing the role of long-haul demand in offsetting softness from some European feeder markets. Domestic stays were stable at 20.9 million, signaling that future expansion of the Swiss hospitality market will be tied more closely to international inflows than to incremental local travel. Growth dynamics in the Swiss hospitality market continue to reflect a pivot toward premium positioning and yield optimization rather than pure volume, as operators in urban hubs and Alpine resorts protect rate integrity and invest in upgraded experiences to sustain pricing power through 2031.

Key Report Takeaways

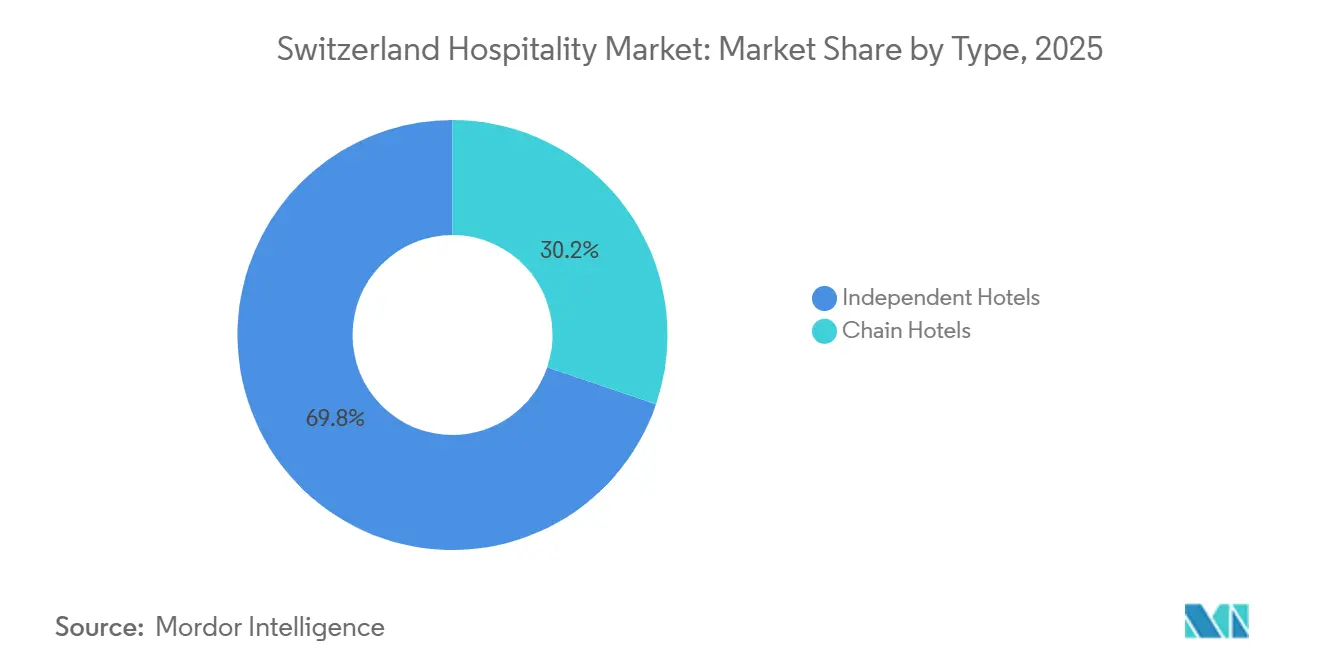

- By type, independent hotels held the largest share of the Swiss hospitality market in 2025 at 69.78%, while chain hotels are projected to post the fastest growth over 2026–2031 at a 4.72% CAGR.

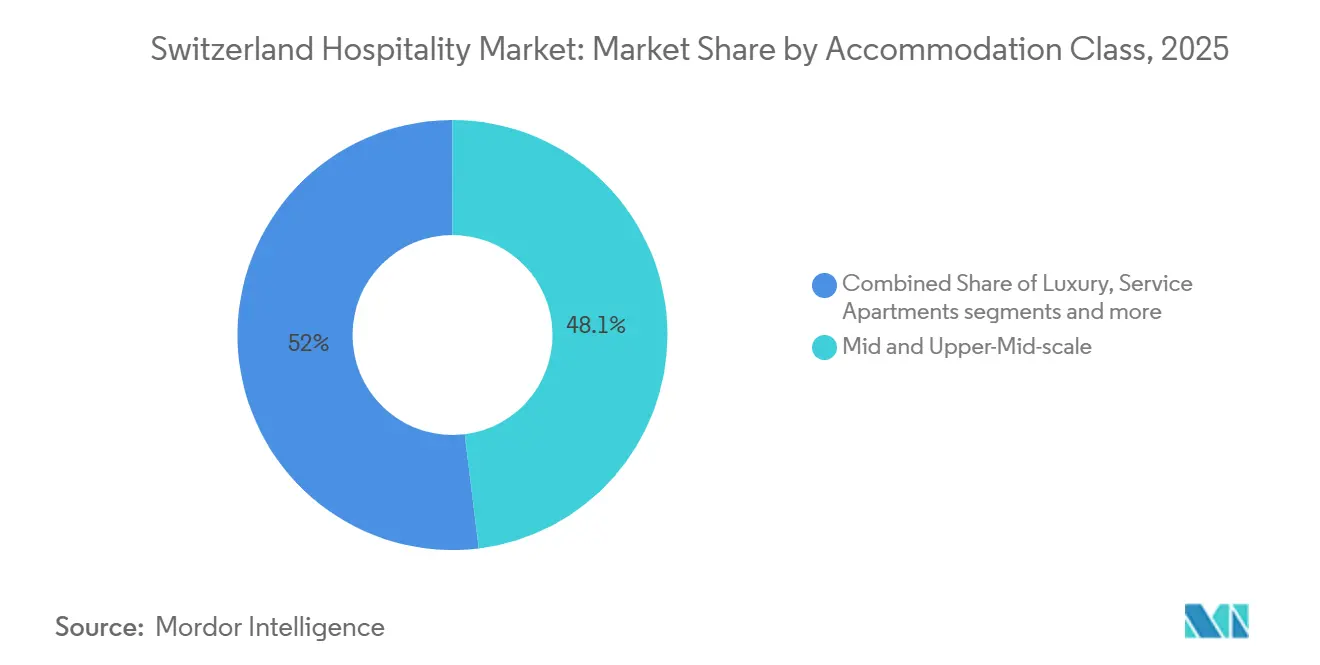

- By accommodation class, mid- and upper-mid-scale led with a 48.05% of the Switzerland hospitality market share in 2025, and service apartments are set to expand at a 6.56% CAGR through 2031.

- By booking channel, OTAs accounted for 50.40% of the Switzerland hospitality market share in 2025, while direct digital bookings recorded the highest forecast CAGR at 7.65% through 2031.

- By geographic region, the Zürich Region captured 25.10% of the Switzerland hospitality market share, and Graubünden is projected to grow the fastest with a 4.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery of international tourism post-pandemic | +0.8% | Global, with early gains in North America, Asia Pacific, and select European corridors | Short term (≤ 2 years) |

| Incentives supporting sustainable tourism development | +0.3% | National, with concentrated adoption in Graubünden, Valais, Bern Region | Medium term (2-4 years) |

| Expansion of digital booking and management platforms | +0.6% | Urban gateways Zürich, Geneva, Basel, roll-out to secondary destinations via cloud PMS | Medium term (2-4 years) |

| Growth in wellness and gastro-tourism revenue streams | +0.4% | Thermal spa clusters Bad Ragaz, Leukerbad, luxury resort zones Gstaad, Zermatt | Long term (≥ 4 years) |

| Integration of medical tourism with Swiss clinics | +0.4% | Zürich, Geneva, Basel, Bern, Lausanne | Long term (≥ 4 years) |

| Biotech clusters drive corporate tourism demand | +0.5% | Basel and Zürich life-sciences corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Incentives Supporting Sustainable Tourism Development

Switzerland Tourism’s Swisstainable program expanded to thousands of partners and created a trusted national signal that helps travelers compare environmental performance across a consistent three-level framework, which aligns operators with consumer expectations and procurement requirements in corporate travel [2]Switzerland Tourism, “Strategy & Planning 2026-2028,” Switzerland Tourism, stnet.ch. The federal tourism strategy emphasizes sustainability as a competitiveness lever and channels support through instruments such as Innotour and regional initiatives that help destinations diversify their offers and extend their seasons, strengthening the Swiss hospitality market in non-winter months. Program guidance encourages energy efficiency, circularity practices, and accessibility upgrades that, when paired with product innovation, improve both operating margins and the visitor experience. Consumer research shared through national channels shows a meaningful share of travelers willing to pay more for certified offers, validating the revenue-side case for certification in the Swiss hospitality market. This policy and market alignment reduce downside risk from climate-conscious guests and expand pricing power for properties that can verify sustainability performance outcomes within recognized frameworks.

Expansion of Digital Booking and Management Platforms

Direct digital bookings are the fastest among all channels, as hotels deploy AI chat, personalized offers, and dynamic rate engines to recover distribution margin in the Swiss hospitality market. Cloud-native property-management and commerce stacks automate inventory, rate, and message synchronization, reducing manual workload for independent and chain-affiliated properties and reallocating staff to high-value service moments. Hotels that activate first-party data and intent-matching improve conversion rates and lower customer acquisition costs as keywordless search and interest-based discovery expand across Meta and social channels [3]Bookassist, “Digital Marketing for Hotels: Strategies to Succeed in 2026,” Bookassist, go.bookassist.org. Destination marketing complements these property-level advances through content at scale that reaches international audiences and drives referral traffic to direct-booking flows managed by hotels and regional consortia. Collectively, these changes increase the addressable base for direct channels, widen upsell opportunities before arrival, and reinforce brand-controlled rate integrity in the Swiss hospitality market.

Growth in Wellness and Gastro-Tourism Revenue Streams

Wellness experiences and culinary programs have moved from add-ons to core revenue drivers as Swiss properties monetize spa, thermal, and nutrition-led offerings that lift spend per available guest and smooth demand across seasons in the Switzerland hospitality market. Properties anchored by thermal resources and medical-wellness partnerships demonstrate resilient demand from international visitors who prioritize verified outcomes and personalized care routines. Switzerland’s position within the global wellness economy supports this trajectory, with per-capita wellness spending among the highest worldwide in 2024 and a consumer base willing to pay for quality, safety, and discretion. National sustainability frameworks reward local sourcing and responsible operations, which encourage gastro-tourism programs that emphasize regional producers and seasonality and that channel premium willingness-to-pay into F&B and experience bundles. These themes expand the addressable spend per guest, differentiate offers in competitive urban corridors, and further stabilize performance in the Switzerland hospitality market outside classic ski and conference peaks.

Integration of Medical Tourism with Swiss Clinics

The Switzerland hospitality market benefits from the country’s clinical reputation and the integration of recovery and wellness packages that link accredited clinics with high-service hotels in urban and resort locations. Partnerships between luxury properties and leading clinics enable cohesive pre- and post-treatment stays that combine nutrition, physiotherapy, and spa therapies in controlled environments. This integration leverages Switzerland’s strengths in precision care and multilingual service, which attract international patients and families who prioritize safety and comfort during extended stays. Alpine and lakeside hotels capitalize on this demand by aligning program design and staffing with clinical schedules, thereby boosting shoulder-season occupancy and ancillary revenue. A visible example is the alignment between select five-star resorts and clinics in the Valais and Vaud regions, which combine diagnostics, recovery protocols, and hospitality-led service to create bundled itineraries that extend length-of-stay in the Switzerland hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor costs and persistent talent shortages | -1.1% | National, acute in Alpine resorts with seasonal swings and limited housing | Short term (≤ 2 years) |

| A strong Swiss franc is reducing global price competitiveness | -0.7% | National, particularly affecting the Eurozone leisure segments, has less impact on affluent long-haul travelers | Short term (≤ 2 years) |

| Environmental caps restricting new alpine construction projects | -0.2% | Alpine municipalities under Second Homes Act constraints | Long term (≥ 4 years) |

| Gen-Z travelers favor shorter micro-vacation stays | -0.3% | Urban hubs and accessible mountain resorts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Swiss Franc Is Reducing Global Price Competitiveness

A stronger franc compresses purchasing power for visitors from nearby Eurozone markets and shifts price-sensitive leisure travelers to alternative destinations, which pressures the Switzerland hospitality market to emphasize value, convenience, and bundled experiences rather than headline rates. Operators mitigate this by expanding direct-booking benefits and deepening loyalty offers that improve repeat conversion without third-party commissions, thereby protecting net revenue. Long-haul demand from North America and parts of Asia has shown resilience despite currency headwinds, which stabilizes upscale and luxury segments that rely on lower price elasticity. National marketing reinforces differentiation in safety, nature access, and quality, helping sustain intent even during periods of relative currency strength. The Swiss hospitality market, therefore, carefully calibrates rate strategy and value-added inclusions to manage conversion across segments without diluting positioning.

Environmental Caps Restricting New Alpine Construction Projects

Spatial planning rules limit new residential capacity in communes with high second-home ratios, constraining certain hotel-residence concepts and slowing the rate of new key additions in mature resort zones. Compliance with energy-efficiency standards and environmental criteria adds design and engineering requirements to renovations and new builds, elevating upfront costs but reducing operating intensity over the asset life. The national tourism strategy prioritizes sustainable development and encourages destinations to diversify their offerings beyond snow-dependent activities, supporting summer and shoulder-season demand patterns that strengthen asset utilization. These constraints can reinforce pricing power in existing properties with premium locations, as scarcity and quality signals sustain rate integrity in peak periods. In the Swiss hospitality market, the net effect is slower supply growth, paired with a stronger emphasis on environmental performance and year-round product curation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Branded Platforms Scale While Independents Defend Heritage

Independent hotels held 69.78% of total inventory in 2025, confirming the structural role of family-owned and boutique properties in the Switzerland hospitality market. Chain hotels are projected to grow faster, at a 4.72% CAGR through 2031, as franchise and management contracts expand in urban and high-visibility resort corridors, where brand recognition, loyalty, and revenue tools improve conversion efficiency. Independents differentiate through design authenticity, service personalization, and local partnerships that sustain premium rates even as distribution costs rise in a competitive landscape. Chains leverage centralized systems, global sales networks, and co-marketing with destinations to attract corporate and international guests who prioritize predictability and membership benefits. This balance keeps the Switzerland hospitality market diversified and resilient, as both formats address distinct customer priorities and rate elasticities within city, resort, and secondary destinations.

The operating gap narrows as independents adopt standardized quality systems and cloud-native tech stacks that synchronize inventory, rates, and messaging across channels to compete for digitally driven guests in the Swiss hospitality industry. Chain growth will likely cluster around gateway nodes where international air and rail access increases short-lead opportunities, while independents capture travelers seeking immersive, place-led narratives. The Swiss hospitality market, therefore, maintains a dual-track structure: brand ecosystems attract volume and points-driven customers, while curated independents monetize taste and heritage through strong, review-led reputations. Over the forecast period, both groups are expected to emphasize sustainability verification and experience design to convert high-intent international demand tied to year-round leisure and MICE patterns. These dynamics collectively reinforce a healthy competitive mix that supports destination goals while expanding the customer base across price tiers in the Switzerland hospitality market.

By Accommodation Class: Service Apartments Capture Extended-Stay Demand

Mid- and upper-mid-scale accommodations accounted for 48.05% in 2025, underscoring their central role in capturing corporate and quality-seeking leisure demand in the Swiss hospitality market. Service apartments are projected to grow the fastest at a 6.56% CAGR through 2031, propelled by biotech-related stays in Basel and Zürich and by families and remote workers seeking space and flexibility during longer visits to Alpine and lakeside regions. Luxury properties continue to defend rate leadership through brand equity, integrated wellness, and exclusive-access programming that target rate-insensitive guests. Budget and economy assets pursue efficiency-led models and targeted channel mixes to handle cost pressure while leveraging spillover during major events and peak seasons. These patterns reflect a Switzerland hospitality market that aligns product features and service levels to distinct use cases across city and resort micro-markets.

Looking ahead, service apartments will benefit from workplace flexibility and project-driven mobility, which anchor extended-stay demand and provide steady occupancy buffers across cycles in the Switzerland hospitality industry. Mid and upper-mid-scale hotels extend their lead by pairing reliable business amenities with visible sustainability credentials that support corporate procurement and consumer trust during trip planning. Luxury stays leverage medical-wellness tie-ins and curated experiences to increase spend per stay, while budget products in suburban nodes capitalize on overflow during city sell-outs and event spikes. As a result, the Switzerland hospitality market size associated with extended-stay formats is set to expand alongside mid-scale’s broad base, with both segments sustaining a healthy rate realization through 2031 when matched with verified environmental performance and consistent digital guest journeys.

By Booking Channel: Direct Digital Platforms Reclaim Margin from OTAs

OTAs accounted for a 50.40% share in 2025, reflecting their discovery role in a market with many independent properties, while direct digital bookings are projected to grow at a 7.65% CAGR through 2031 as hotels invest in loyalty benefits, AI chat, and personalized pricing. Cloud-native platforms reduce repetitive work and support faster offer deployment, which improves speed-to-market for packages and targeted promotions. Keywordless and intent-based advertising enhances reach for independent hotels that previously relied on broad-match search and static content libraries, which improves efficiency in a rising media-cost environment. National destination campaigns supply top-of-funnel awareness at a global scale, then hand off interest to operator-controlled booking funnels where upsell flows and direct-only benefits support conversion at stronger net rates. This channel shift is structurally positive for the Swiss hospitality market, as distribution cost discipline becomes a lever for funding staff retention, sustainability upgrades, and improvements in guest experience.

Group and corporate channels maintain relevance through negotiated volume and ancillary spend, often aligned with the life sciences and financial services calendars in Zürich, Basel, and Geneva. Secondary cities and resort corridors also benefit from direct groups that pair lodging with rail passes, and activity bundles curated by local DMO partners. Hotels that integrate CRM, PMS, and payments orchestration streamline pre-arrival communication and cross-sell in-stay experiences with minimal friction, improving satisfaction and repeat probability. The resulting mix still includes OTA-led discovery, but rate and margin realization move more favorably toward owned channels as personalization and verified sustainability credentials matter more to guests planning trips in the Swiss hospitality industry. In turn, the Swiss hospitality market size tied to direct digital revenue grows faster than average as properties consolidate loyalty and data advantages over the forecast period.

Geography Analysis

The Zürich Region captured 25.10% of overnight stays in 2025 and remains the lead node for international arrivals and corporate mobility, which sustains mid-week demand and high utilization of upper-mid- and upscale properties in the Swiss hospitality market. Urban occupancy levels in Zürich and Geneva surpassed national averages in 2024, reflecting the recovery in business travel and events that secure premium rates during compressed booking windows. Policy alignment around sustainability and public transport access supports the destination’s value proposition for corporate planners and leisure visitors seeking reliable, low-friction mobility. This combination of access, demand diversity, and operational scale continues to anchor the Switzerland hospitality market in the country’s economic hubs. It also sets a benchmark for tech deployment and sustainability verification, influencing practices in secondary cities.

Graubünden is projected to record the fastest 2026–2031 growth at a 4.75% CAGR, supported by premium repositioning, season diversification, and verified sustainability that appeals to rate-insensitive travelers in the Switzerland hospitality market. Constraints on new supply encourage asset upgrades and service innovation that lift ADRs and auxiliary revenue without overshooting capacity. Resorts that expand wellness, hiking, and culinary programs capture more shoulder-season demand and stabilize occupancy across the calendar. These moves increase revenue per guest by bundling experiences tied to local culture and access to nature. The result is a more balanced year-round profile that broadens the customer base without diluting the brand value of Alpine destinations in the Switzerland hospitality market.

Geneva and Lake Geneva benefit from international organizations and science-driven visitation that bolster corporate demand and high-visibility events, which sustain occupancy and rates above national averages during key periods. Northwestern Switzerland, around Basel, leverages life-sciences clusters and cross-border rail to attract business meetings and short-lead trips that fill weekdays. Bern and Central Switzerland absorb overflow from gateway cities while promoting lake- and mountain-access that resonates with international tour groups and independent travelers. Secondary regions in the Rest of Switzerland category emphasize summer and shoulder-season experiences designed around sustainability, local culture, and convenient public transport to grow their share of the Switzerland hospitality market. Collectively, these regional profiles diversify demand for drivers and reduce exposure to single-season volatility.

Competitive Landscape

The Swiss hospitality market remains moderately fragmented, with independents holding a clear majority of rooms, while international brands expand through asset-light models in gateways and prime resort corridors. Chains emphasize loyalty ecosystems, distribution science, and sustainability verification to earn corporate preference and repeat stays from international guests. Independents respond by elevating design and service and by adopting cloud commerce stacks that improve speed and personalization without sacrificing brand character. Both groups are converging on direct-channel growth to protect net revenue and fund staffing, training, and energy-efficiency investments aligned with national policy priorities. This balance enhances resilience at the system level and positions the Switzerland hospitality market for steady expansion through the forecast period.

Technology is a clear differentiator as leading operators integrate first-party data, PMS, and CRM to orchestrate the guest journey across search, booking, and in-stay service, thereby increasing conversion and satisfaction at a lower acquisition cost. Independent hotels accelerate parity by deploying modular cloud tools and leveraging destination content to expand organic reach and drive direct inquiries. Sustainability verification is moving from a differentiator to a prerequisite in corporate sourcing and consumer choice, so operators in the Swiss hospitality market are integrating program outcomes into product design, pricing, and brand narratives. This raises the bar for new entrants and channels capital toward properties that can document environmental performance alongside guest-experience quality. The resulting competitive arc rewards operational excellence and brand clarity across formats and price points.

Strategic moves emphasize experience-led renovations, digital direct investments, and data-enabled loyalty growth that compound over time. Corporate and group business remain anchor segments in Zürich, Basel, and Geneva, where rail and air access align with planner priorities on sustainability and travel time. Resort assets continue to differentiate on wellness and gastronomy with programming designed to lengthen stays and increase share of wallet among high-intent leisure travelers. Over the forecast period, operators that pair verified sustainability with frictionless digital service and strong local narratives should command premiums in the Switzerland hospitality market. This focus will likely accelerate direct-channel adoption and motivate portfolio upgrades that align with policy and consumer expectations on energy and sourcing.

Switzerland Hospitality Industry Leaders

Accor SA

InterContinental Hotels Group

Radisson Hotel Group

Marriott International

Sorell Hotels Switzerland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hilton partnered with Explora Journeys, the MSC Group's luxury ocean travel brand, to launch Hilton Honors Adventures, an extension of its loyalty program. This collaboration enables Hilton Honors members to access exclusive benefits and earn Points on luxury ocean travel experiences starting in summer 2026.

- August 2025: DERTOUR Group, following regulatory approval, acquired four Hotelplan Group business units, excluding Interhome (acquired by HomeToGo). This integration strengthens DERTOUR’s presence across 16 source markets, unifies iconic brands in Switzerland, expands United Kingdom specialist businesses, and enhances Germany’s B2B portfolio with vtours’ dynamic packaging.

- April 2025: Room Mate Hotels entered Switzerland by acquiring the 104-room Hotel Marmont in Geneva, near Rue du Rhône and Lake Geneva. Scheduled for renovation, it will relaunch under the Room Mate brand in early 2026, marking strategic expansion into Switzerland's resilient tourism and luxury market.

- February 2025: IHG Hotels & Resorts agreed to acquire Ruby Hotels for USD 116.0 million (EUR 110.5 million), adding 20 properties and 3,483 rooms across Europe and a pipeline of 10 hotels with 2,235 rooms. The deal includes two Swiss assets in Geneva and Zürich, expanding IHG’s lifestyle footprint in key urban locations. Management targets scaling the brand to 120 properties within 10 years and 250+ over 20 years. The acquisition strengthens IHG’s position in the European select-service and lifestyle space.

Switzerland Hospitality Market Report Scope

The hospitality industry comprises businesses such as hotels, restaurants, bars, resorts, cruise ships, and theme parks that offer accommodations, food, and beverages. It focuses on creating welcoming environments, meeting guest needs, and ensuring satisfaction. Hospitality significantly supports tourism, with both sectors closely interconnected to enhance customer experiences and economic growth.

The Switzerland hospitality market report is segmented by type (chain hotels, independent hotels), accommodation class (luxury, mid & upper-mid-scale, budget & economy, service apartments), booking channel (direct digital, OTAs, corporate/MICE, wholesale & traditional agents), and geographic region (Zürich Region, Geneva & Lake Geneva Region, Basel & Northwestern Switzerland, Bern & Central Switzerland, Graubünden, Rest of Switzerland). The market forecasts are provided in terms of value (USD).

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Zürich Region |

| Geneva & Lake Geneva Region |

| Basel & Northwestern Switzerland |

| Bern & Central Switzerland |

| Graubünden (Grisons) |

| Rest of Switzerland |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Zürich Region |

| Geneva & Lake Geneva Region | |

| Basel & Northwestern Switzerland | |

| Bern & Central Switzerland | |

| Graubünden (Grisons) | |

| Rest of Switzerland |

Key Questions Answered in the Report

What is the current size and growth outlook of the Switzerland hospitality market?

The Switzerland hospitality market size is expected to grow from USD 15.08 billion in 2025 to USD 15.70 billion in 2026 and is forecast to reach USD 19.18 billion by 2031 at a 4.09% CAGR over 2026-2031.

Which accommodation segments are leading the growth in Switzerland?

Mid and upper-mid-scale leads by share at 48.05% in 2025, while service apartments are the fastest-growing at a 6.56% CAGR through 2031 due to extended-stay demand from corporate and family travel.

How are booking channels shifting in the Switzerland hospitality market?

OTAs held 50.40% in 2025, but direct digital is growing at a 7.65% CAGR through 2031 as hotels invest in AI chat, loyalty, and personalized pricing to improve net rates.

Which regions are most important for hotel demand in Switzerland?

The Zürich Region leads with 25.10% of overnight stays in 2025, and Geneva shows above-average occupancy, while Graubünden is forecast to grow the fastest through 2031 due to premium repositioning and season diversification.

What are the main drivers of demand for Swiss hotels through 2031?

Recovery of international tourism, sustainability-aligned development, digital booking expansion, wellness and gastro-tourism, medical tourism integration, and biotech-driven corporate travel collectively support steady growth.

What key challenges could slow hotel performance in Switzerland?

Labor shortages, a strong franc that puts pressure on euro-area leisure budgets, spatial planning constraints in Alpine zones, and Gen-Z preferences for short trips are the primary headwinds operators are addressing through strategy and technology.

Page last updated on: