Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

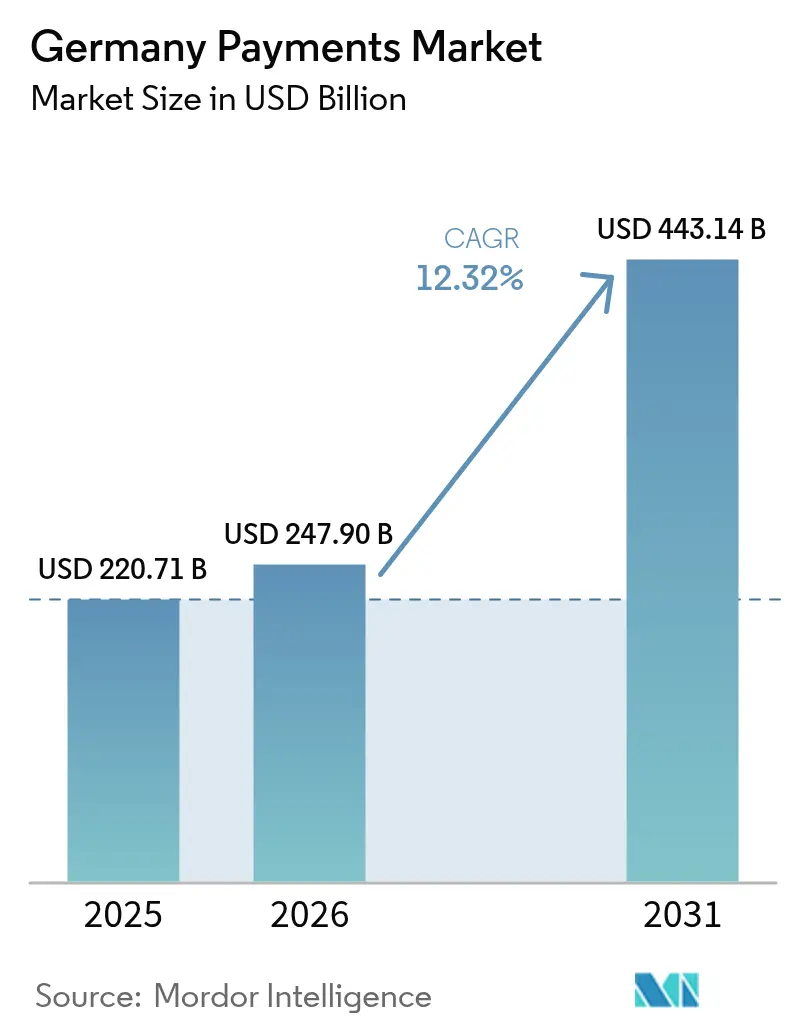

| Base Year Market Size (2025) | USD 220.71 Billion |

| Market Size (2026) | USD 247.9 Billion |

| Market Size (2031) | USD 443.14 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Payments Market Analysis by Mordor Intelligence

Germany payments market size in 2026 is estimated at USD 247.9 billion, growing from 2025 value of USD 220.71 billion with 2031 projections showing USD 443.14 billion, growing at 12.32% CAGR over 2026-2031. The up-swing signals a decisive transition from cash to digital instruments, propelled by the Instant Payments Regulation, mobile-wallet penetration, and the European Central Bank’s preparations for a digital euro. Point-of-sale (POS) transactions still anchor day-to-day commerce, but e-commerce, buy-now-pay-later (BNPL) plans, and real-time transfers are accelerating adoption curves as merchants seek faster settlement and richer data.[1]European Central Bank, “Digital Euro – Preparation Phase Report,” ecb.europa.eu Card schemes protect incumbent volumes through tokenization and strong-customer-authentication, while domestic banks leverage SEPA Instant rails to build account-to-account propositions. Competitive pressure intensifies as Wero, PayPal, and Klarna scale embedded solutions that bypass legacy card interchange economics. Headline risks include fee caps, core-banking obsolescence, and inflation-linked cost pressure on processors, yet each headwind also nudges providers toward higher-margin advisory and data services within the Germany payments market.

Key Report Takeaways

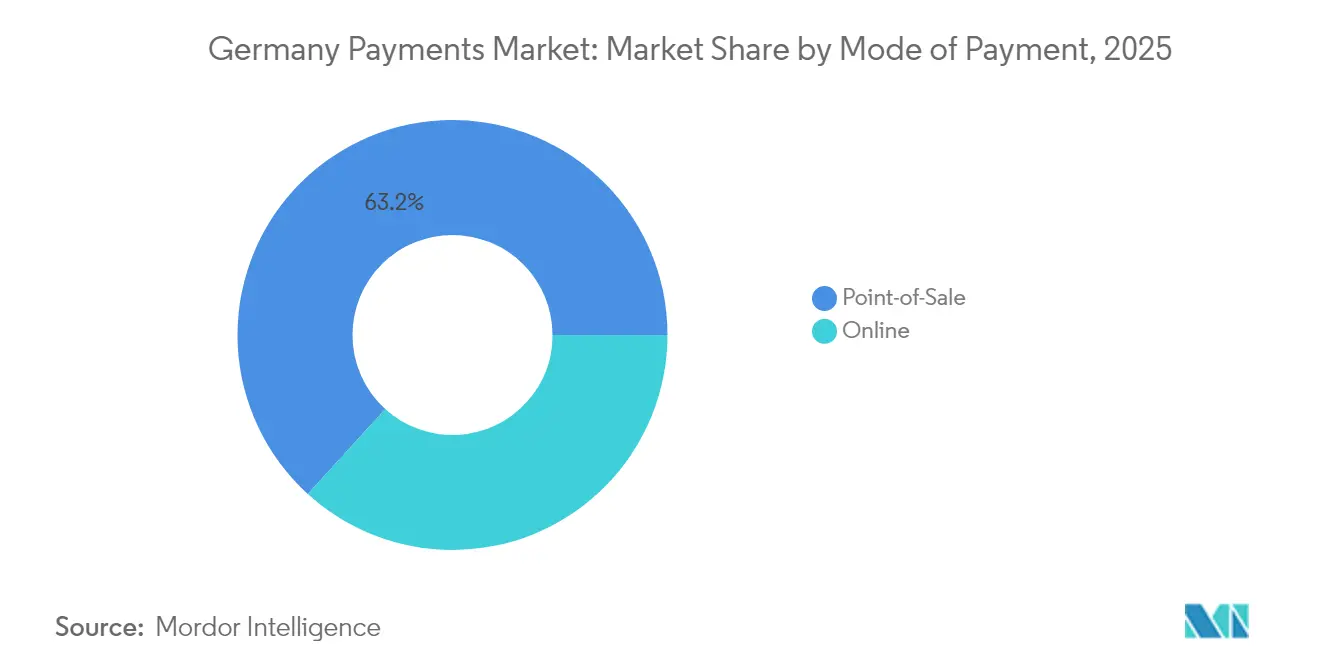

- By mode of payment, POS card payments led with 37.62% of Germany payments market share in 2025; overall Point-Of-Sale Payment held at around 63.25% share; digital wallets are forecast to grow at 15.74% CAGR to 2031.

- By interaction channel, point-of-sale retained 69.85% revenue share in 2025, while e-commerce is projected to expand at 14.25% CAGR through 2031.

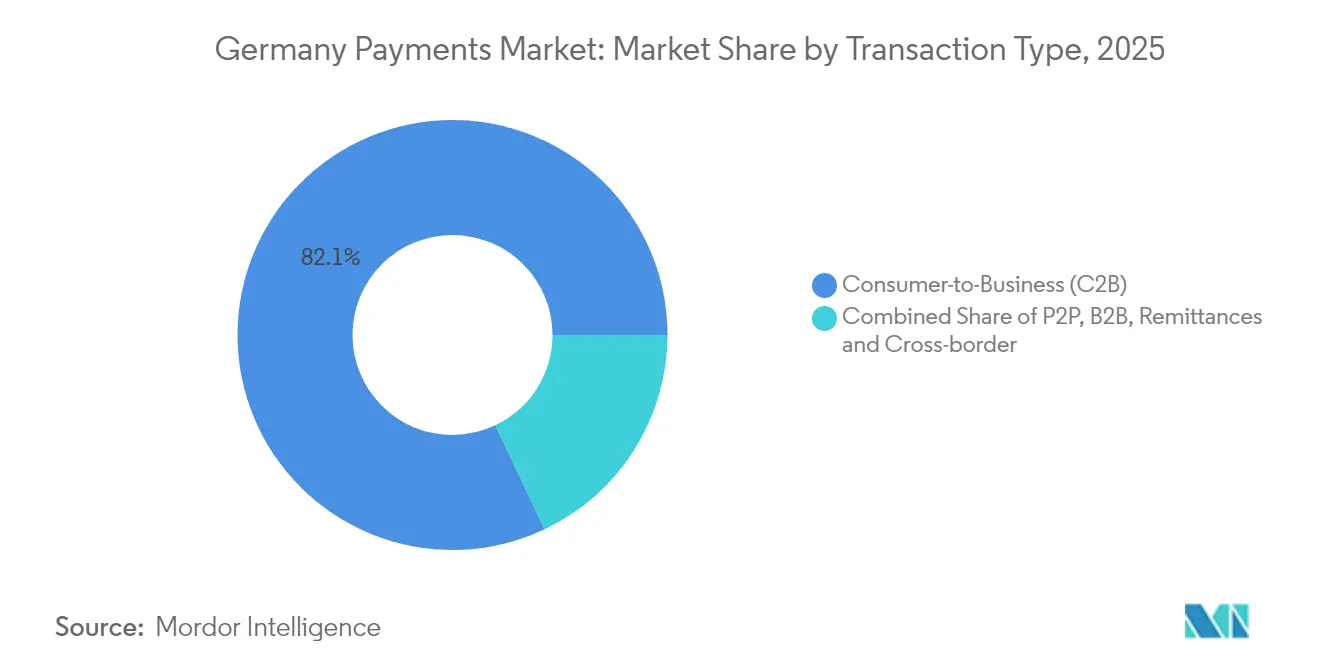

- By transaction type, consumer-to-business flows captured 82.05% of 2025 volumes; person-to-person payments should accelerate at 17.2% CAGR to 2031.

- By end-user industry, retail held 29.25% share of the Germany payments market size in 2025, whereas hospitality and travel is advancing at 14.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Mobile-Wallet Acceptance at German POS Terminals | +2.8% | National, with early gains in Berlin, Munich, Hamburg | Medium term (2-4 years) |

| E-commerce Boom Fueling Card-Not-Present Volumes | +3.2% | National, stronger in urban centers | Short term (≤ 2 years) |

| Government-backed Instant-Payment Infrastructure Drives the Market | +2.1% | EU-wide, concentrated in Germany | Short term (≤ 2 years) |

| Surging Buy-Now-Pay-Later (BNPL) Adoption Among Millennials | +1.9% | National, with spillover to Austria, Switzerland | Medium term (2-4 years) |

| Merchant Demand for Omnichannel Checkout Experiences | +1.7% | National, retail-focused regions | Medium term (2-4 years) |

| Fin-Tech Partnerships Enabling Embedded-Payment Use-Cases | +1.4% | National, B2B concentrated in Frankfurt, Stuttgart | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of Mobile-Wallet Acceptance at German POS Terminals

PayPal’s contactless debut in 2025—enabled by Digital Markets Act access to Apple’s NFC chipset—removed a long-standing technical barrier and let non-bank wallets compete directly with Apple Pay and Google Pay at 286,000 VR Payment terminals.[2]VR Payment, “Terminal Network Statistics 2025,” vr-payment.de Merchant queues shortened, checkout data improved, and mobile usage jumped as cash lost relevance. Banks responded by integrating girocard tokens into Android and iOS wallets to retain top-of-mind status at the point of tap. The network effect is self-reinforcing: each accepting merchant encourages more consumers, who in turn press other merchants to upgrade. Over the medium term the uplift adds 2.8 percentage points to the Germany payments market CAGR, particularly in high-traffic urban micro-segments.

E-commerce Boom Fueling Card-Not-Present Volumes

Online shopping reached 82% household penetration by 2023 and remains on a steep trajectory. Lidl and Kaufland’s Click to Pay roll-out trimmed authentication friction, lifting conversion while allowing Mastercard to march toward its 100% tokenization target. Higher basket values and purchase frequency in digital channels give payment providers revenue leverage even when physical retail stabilizes. Digital identity projects and one-click checkout standards converge to suppress fraud rates, further nudging late adopters into the channel. The result is a 3.2 percentage-point boost to overall growth in the Germany payments market, with CNP volumes eclipsing face-to-face growth by more than 2:1.

Government-Backed Instant-Payment Infrastructure Drives the Market

Mandatory acceptance of real-time transfers from January 2025 forced every bank to modernize clearing pipes. Deutsche Bank processed 27% more instant transfers in the first month, and corporates began shifting supplier payouts to 24/7 rails to improve working-capital rotation. Fintechs exploit these rails through API overlays, offering cash-flow dashboards and variable-recurring-payment links for subscription merchants. The rails also underpin Wero’s pan-European wallet, creating a competitive alternative to card networks. Because instant settlement removes chargeback exposure and cuts scheme fees, merchants steer customers toward it with small discounts, broadening adoption. The structural benefit adds 2.1 percentage points to the Germany payments market CAGR during 2025-2030.

Surging Buy-Now-Pay-Later Adoption Among Millennials

Klarna’s 30% revenue leap in 2024 confirmed BNPL’s journey into the mainstream. German millennials entering higher disposable-income brackets prefer flexible installment plans over revolving credit. PayPal’s in-app BNPL for in-store purchases extends the model beyond online carts. Merchants appreciate average-order-value lifts and lower checkout abandonment, while consumers enjoy cost transparency. As regulators tighten credit-worthiness rules, leading providers differentiate through open-banking data analytics to keep default rates contained. The mechanism contributes 1.9 percentage points to the compound expansion of the Germany payments market and re-shapes merchant subsidy economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Caps Compressing Issuer Economics | -1.8% | EU-wide, concentrated in Germany | Medium term (2-4 years) |

| Legacy Core-Banking Systems Slowing API Roll-outs | -1.2% | National, affecting traditional banks | Long term (≥ 4 years) |

| Consumer Privacy Concerns over PSD2 Data-Sharing | -0.9% | EU-wide, particularly Germany | Short term (≤ 2 years) |

| Fragmented KYC/AML Requirements for Cross-border Payments | -0.7% | EU cross-border, affecting German banks | Medium term |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps Compressing Issuer Economics

Proposed fee ceilings could shift USD 502 million of annual economics from issuers to merchants. German banks therefore accelerate account-to-account propositions and seek subscription-style revenues from digital identity or loyalty add-ons. Card schemes respond by unbundling value-added services—fraud scoring, token vaults, instalment APIs—to preserve relevance. Smaller issuers, lacking scale, may retreat from consumer cards altogether, trimming innovation budgets and shaving 1.8 percentage points off the otherwise robust CAGR in the Germany payments market.[3]Payment Systems Regulator, “Card Scheme Fee Changes 2019-2024,” psr.org.uk

Legacy Core-Banking Systems Slowing API Roll-outs

Many German banks still run on 1980s mainframes that complicate real-time data exposure. Middleware layers add latency, raise project costs, and create brittle integration points for fintech partners. As PSD2 successor rules mandate premium APIs, the technology debt becomes a strategic liability. Processor Worldline has already reported merchant-relationship terminations triggered by compliance delays rather than price factors. Over the long term, delayed product introductions and duplication of effort dilute growth, subtracting 1.2 percentage points from the Germany payments market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Cards Continue to Anchor but Wallets Scale Faster

POS card payments held 37.62% Germany payments market share in 2025, underscoring consumers’ familiarity with girocard and dual-network debit credentials. Overall, Point-of-Sale Payment is largest share with 63.25%. Credit and prepaid cards together stayed below 15% because many Germans prefer immediate settlement over revolving credit. Yet digital wallets, helped by open-NFC policy and SEPA Instant reach, are expanding at 15.74% CAGR. Their share of Germany payments market size for online checkouts is forecast to eclipse cards by 2028. Unlike cards, wallets can weave loyalty, buy-now-pay-later, and identity verification into one interface, making them magnets for merchant upselling. Cash use is slipping into single-digit range for transactions above EUR 50 (USD 54) as public transport and event venues pivot to tap-only acceptance. Meanwhile, QR code and wearable payments ride contactless rails but remain niche, capturing less than 2% of 2025 volume. Over the forecast period, regulators will watch wallet concentration to ensure competitive balance, yet the consumer tide is clearly in favor of tap-to-phone and in-app credentials.

By Interaction Channel: Physical POS Dominates but Digital Commerce Lifts Overall Growth

The brick-and-mortar environment delivered 69.85% of 2025 transaction value, reflecting Germany’s dense grocery and discount-retail footprint. Yet e-commerce posted a 14.25% CAGR, adding incremental spend faster than physical outlets. Mobile commerce—fueled by same-day delivery and 5G coverage—accounts for more than half of online checkouts in urban corridors. PayPal’s contactless launch blurs channel boundaries by letting shoppers re-use the same credential online and in stores. That convergence encourages merchants to invest in unified token vaults and customer-data platforms. Within the Germany payments market, omnichannel experiences will reduce stand-alone online fraud rates and harmonize loyalty programs, supporting profitable growth across both channels.

By Transaction Type: Consumer Purchases Prevail while Peer Transfers Accelerate

Consumer-to-business flows represented 82.05% of 2025 volumes and keep rising with retail turnover growth. Business-to-business payments are slower to digitize due to batch invoicing habits and enterprise resource planning (ERP) dependencies, yet API-based request-to-pay pilots hint at future change. Person-to-person transfers, growing at 17.2% CAGR, are the bright spot. Wero’s phone-number rails and Deutsche Bank’s One-Pay FX corridor ease friction and start to cannibalize cash gifting and paper giro transfers. Remittance corridors remain modest in value but gain from application programming interfaces (APIs) that drop fees below 1% and deliver funds in seconds. The embedded finance movement also opens new transaction types—gig-worker payouts, insurance claim disbursements, marketplace seller settlements—broadening the Germany payments market size without cannibalizing headline categories.

By End-user Industry: Retail is the Base, Travel Leads the Upswing

Retail owned 29.25% of 2025 value, with supermarkets, DIY stores, and discount chains keeping debit volumes high. Hospitality and travel rebound sharply, advancing at 14.65% CAGR as global tourism normalizes and events like UEFA Euro 2024 trigger surge capacity. Hotels add self-service kiosks linked to instant payment options, trimming check-in times and staffing overhead. Airlines introduce in-app wallet boarding passes with integrated duty-free ordering, monetizing ancillary services. Healthcare digitizes slower but benefits from mandatory e-prescription flows that link pharmacy payments to insured reimbursement. Utility bill payments migrate to e-invoices tied to real-time direct debits, improving collection rates and data granularity. Collectively these vertical trends expand the Germany payments market while de-risking reliance on any single sector.

Geography Analysis

Germany payments market growth is uneven across the federal landscape. Metropolitan areas—Berlin, Munich, Hamburg, and Frankfurt—show mobile-payment penetration above 60% among residents aged 18-35, while rural districts still favor cash for small-value purchases. ATM consolidations reduce cash availability, nudging older demographics toward contactless girocard and wallet options. Northern states—Schleswig-Holstein and Hamburg—exhibit the highest card penetration, mirroring Scandinavian influence, whereas Bavaria preserves stronger cash usage, citing tradition and privacy. Real-time rails reduce cross-state payment delays, enabling SMEs in Saxony and Thuringia to settle invoices 24/7.

Cross-border commerce thrives on EU harmonization. Wero’s reach into France and Belgium creates a regional network effect, and merchants in Cologne and Aachen already offer wallet acceptance to serve Belgian day-trippers. The forthcoming digital euro pilot, coordinated by the Bundesbank, could test retail scenarios in Frankfurt’s fintech cluster, where 59% of surveyed consumers express willingness to adopt a central-bank-issued instrument. Overall, geographic disparities will narrow over time as infrastructure gaps close, yet localized marketing remains vital to capture regional attitudes inside the Germany payments market.

Competitive Landscape

The Germany payments market exhibits moderate fragmentation and intensifying consolidation. International schemes (Visa, Mastercard), domestic girocard, global wallets (PayPal, Apple Pay, Google Pay), and European challengers (Wero) form overlapping layers of acceptance. Market leaders invest in tokenization, risk engines, and value-added APIs to protect interchange revenue as regulators impose caps. Banks pursue joint ventures—such as Commerz Globalpay—to modernize acquiring and keep merchant relationships.

Worldline, Nexi, and Stripe compete for enterprise omnichannel mandates, differentiating via uptime, developer tooling, and data analytics. Fintech disrupters like Ivy target B2B pay-ins and pay-outs with cloud-native stack, under-cutting legacy processor pricing. Acquirers look downstream, acquiring ISV platforms to embed payments into vertical SaaS, while processors move upstream into treasury services to offset margin squeeze. Patent filings at the European Patent Office show heightened activity around secure NFC and biometric authentication, evidencing ongoing innovation that could reshape share positions. Overall competitive tension fosters rapid product iteration, benefiting merchants and end users within the Germany payments market.

Germany Payments Industry Leaders

Mastercard Inc.

Visa Inc.

Girocard (Deutsche Kreditwirtschaft)

PayPal Holdings Inc.

Google Pay (Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Worldline launched Wero for German e-commerce, aligning with the European Payments Initiative to offer buyer protection and uniform checkout.

- May 2025: PayPal unveiled its first German contactless wallet, usable at all Mastercard-accepting merchants with BNPL built-in.

- February 2025: Unzer introduced Direct Bank Transfer, leveraging open banking to cut card fees for merchants.

- February 2025: bunq, Ginmon, and Upvest collaborated on in-app investment products targeting German retail savers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the German payments market as the total gross transaction value flowing through card, digital-wallet, account-to-account, and cash-at-checkout transactions executed either in-store or online by consumers and businesses.

Scope exclusions include transactions linked to motor-vehicle or real-estate purchases, utility bill settlement, mortgage or loan servicing, and securities trading, which are outside this assessment.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- By Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- By Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- By End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with bank payment heads, PSP product managers, large retailers, and SME merchants across all Bundesländer help us verify interchange, average ticket sizes, channel migration rates, and wallet penetration.

Follow-up email surveys allow our team to refine model inputs and sense-check growth drivers uncovered in secondary work.

Desk Research

We begin with structured desk work that benchmarks official statistics from the Deutsche Bundesbank, the European Central Bank's Statistical Data Warehouse, and Eurostat, while industry turnover data is verified against disclosures from the German Banking Industry Committee and the German Retail Association. Company filings, investor decks, and reputable press articles enrich usage trends and fee structures. To size private channels, we mine D&B Hoovers for issuer/acquirer financials and tap Dow Jones Factiva for deal pipelines that validate adoption signals. These examples illustrate the caliber of sources consulted; many more public records, academic papers, and trade bulletins are screened to anchor assumptions.

Analysts then access select paid datasets, Questel for relevant fintech patents and Volza for card-reader import flows, to cross-check technology diffusion. The list above is illustrative, not exhaustive, and other credible sources are continually referenced.

Market-Sizing & Forecasting

A top-down construct starts with Bundesbank transaction counts and values, which are then split by channel and tender type using penetration surveys before being further filtered through end-industry spending weights. Bottom-up samples, issuer volume roll-ups and average selling price checks at POS hardware distributors, are employed to reconcile totals and reveal blind spots. Key variables include active card base, contactless share, e-commerce basket size, SEPA Instant Credit Transfer uptake, and BNPL usage ratio. Multivariate regression coupled with scenario analysis projects these drivers forward, enabling CAGR estimates that reflect regulatory timelines and macro indicators. Any data gaps in bottom-up samples are bridged with conservative midpoint estimates vetted by subject experts.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer review by a senior analyst, and a live re-check with at least one original respondent. Reports refresh annually, with interim tweaks whenever material events, such as fee-cap changes or PSD3 drafts, surface.

Why Mordor's Germany Payments Figures Command Confidence

Published numbers often diverge because firms choose distinct scopes, base years, or refresh cadences. Our disciplined segmentation and annual model rebuild ensure comparability, whereas others may bundle adjacent services or carry forward older baselines.

Key gap drivers include inclusion of bill-pay and prepaid volumes by some publishers, differing currency conversion dates, and use of single-source extrapolations that ignore channel-specific growth brakes, such as interchange caps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 220.71 B (2025) | Mordor Intelligence | - |

| USD 366.05 B (2024) | Regional Consultancy A | Bundles bill-payment and managed-service fees into core payments universe |

| USD 263.70 B (2024) | Global Consultancy B | Uses broad "digital payment systems" scope and five-year-old average ticket assumptions |

| USD 113.34 B (2024) | Industry Association C | Focuses solely on B2B flows, omitting consumer POS and e-commerce spends |

These contrasts show that our carefully bounded scope, dual-path validation, and annual refresh yield a balanced, transparent baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the projected value of the Germany payments market in 2031?

It is projected to reach USD 443.14 billion, reflecting a 12.32% CAGR during 2026-2031.

Which payment mode is growing fastest in Germany?

Digital wallets are expanding at 15.74% CAGR, driven by NFC access and instant-payment rails that reduce checkout friction.

How will interchange-fee caps affect German issuers?

Fee ceilings could strip as much as 1.8 percentage points from market CAGR by compressing card-issuer margins and shifting focus to value-added services.

Why are instant payments important for merchants?

Regulated real-time transfers lower settlement risk, improve cash-flow timing, and cut scheme fees, encouraging merchants to promote account-to-account options.

Which end-user industry shows the fastest growth?

Hospitality and travel lead with a 14.65% CAGR as tourism normalizes and contactless solutions gain popularity during large events such as UEFA Euro 2024.

Are peer-to-peer transfers significant in Germany?

Yes, person-to-person payments are growing at 17.2% CAGR, propelled by Wero’s phone-number rails and broader instant-payment infrastructure.

Page last updated on: