Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

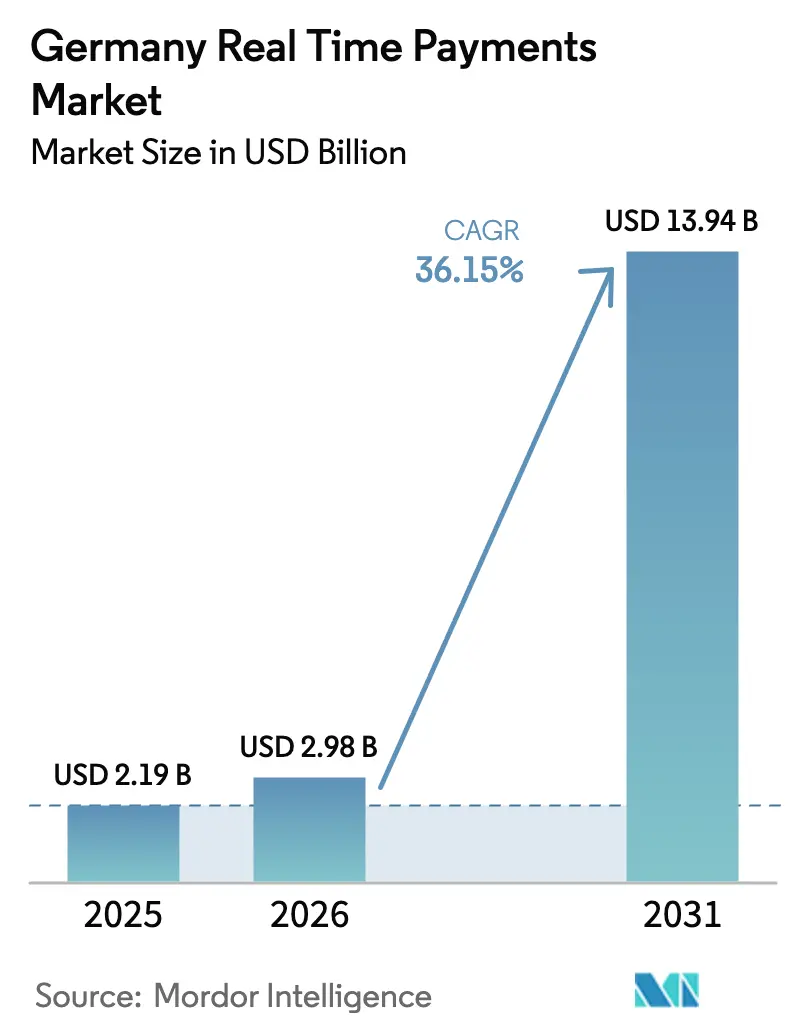

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 13.94 Billion |

| Growth Rate (2026 - 2031) | 36.15% CAGR |

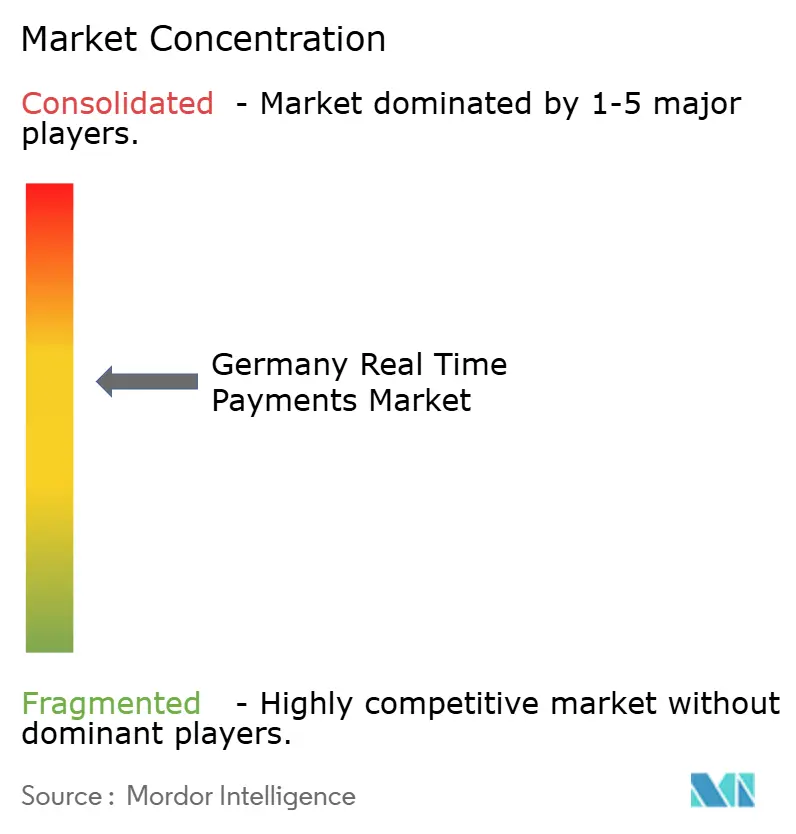

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Real Time Payments Market Analysis by Mordor Intelligence

The Germany real time payments market size is expected to grow from USD 2.19 billion in 2025 to USD 2.98 billion in 2026 and is forecast to reach USD 13.94 billion by 2031 at 36.15% CAGR over 2026-2031. The growth trajectory reflects the European Union’s Instant Payments Regulation, which compels every payment service provider to process incoming funds in 10 seconds by January 2025 and outgoing funds by October 2025.[1]European Central Bank, “Instant Payments Regulation,” European Central Bank, ecb.europa.eu. Price-parity rules remove fee barriers, while higher SEPA Instant Credit Transfer limits up to EUR 100,000 (USD 110,000) unlock high-value B2B flows.[2]European Payments Council, “2025 SEPA Rulebook Updates,” European Payments Council, europeanpaymentscouncil.eu. Large banks accelerate ISO 20022 migration, enabling richer data exchange and smoother interoperability, whereas fintechs deploy buy-now-pay-instantly models to tap retail demand. These combined forces are steering Germany real time payments market toward value-added services focused on liquidity, cash-flow visibility, and contextual checkout conversion.

Key Report Takeaways

- By transaction type: Peer-to-Peer transfers held 59.20% of Germany real time payments market share in 2025, while Peer-to-Business transactions are forecast to post a 38.71% CAGR through 2031.

- By component: Platforms/Solutions controlled 67.40% revenue in 2025; Services are set to grow at 32.37% CAGR to 2031.

- By deployment mode: On-premise captured 67.10% of Germany real time payments market size in 2025, yet cloud implementation is expected to log a 33.84% CAGR during 2026–2031.

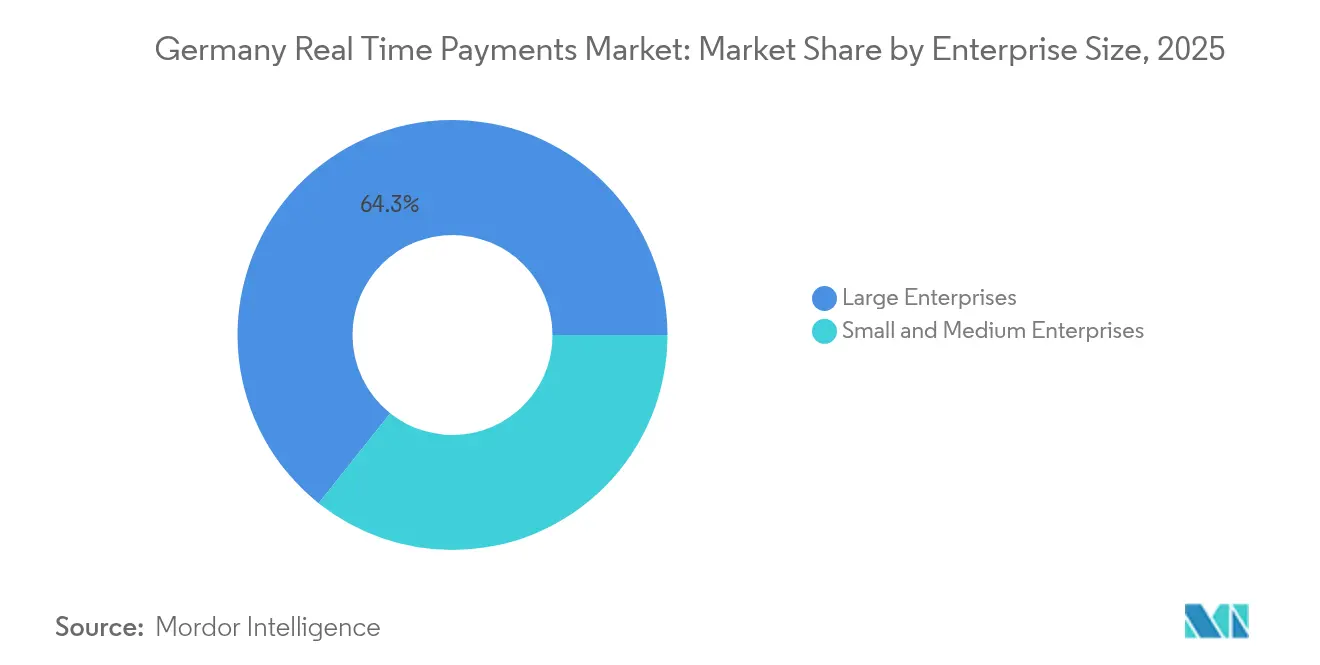

- By enterprise size: Large enterprises contributed 64.30% revenue in 2025; SMEs will advance fastest at 30.69% CAGR.

- By end-user industry: Retail & e-commerce commanded 33.40% share of Germany real time payments market size in 2025, while Government & Public Sector is projected to accelerate at 35.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SEPA Instant Credit Transfer (SCT Inst) limit increase to USD 110 k stimulating high-value B2B flows | +9.3% | EU-wide, with strong impact in Germany | Medium term (2-4 years) |

| Federal e-invoicing mandate (2025) accelerating instant settlement for corporates | +8.7% | Germany, with potential spillover to other EU markets | Short term (≤ 2 years) |

| Request-to-Pay (R2P) roll-out boosting instant checkout conversion in e-commerce | +7.4% | Germany, France, Benelux | Medium term (2-4 years) |

| Fintech "Buy Now Pay Instantly" propositions leveraging Giropay rails | +6.5% | Germany, with focus on urban centers | Short term (≤ 2 years) |

| Core-bank migration to ISO 20022 enabling ubiquity of instant rails in Sparkassen & Volksbanken | +5.9% | Germany, with emphasis on regional banks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SEPA Instant Credit Transfer Limit Expansion Transforms B2B Payments

The elevated EUR 100,000 (USD 115602.93) threshold is pushing corporates to switch from batch wires to instant rails, improving intraday liquidity management and reconciling high-value invoices in seconds. German treasurers now integrate real-time balances into cash-pooling dashboards, curbing overdraft costs and enhancing counterparty confidence. Banks that enable automated high-value SCT Inst flows win entrenched positions in corporate wallets. Technology spend concentrates on straight-through processing, fraud analytics, and ISO 20022 enrichment to accommodate richer remittance data. Over the medium term, the new ceiling is expected to blur boundaries between domestic high-value systems and retail instant rails, underpinning broader Germany real time payments market adoption. [4]European Payments Council, “SEPA Instant Credit Transfer Scheme,” European Payments Council, europeanpaymentscouncil.eu.

E-Invoicing Mandate Drives Corporate Instant Payment Adoption

Germany’s January 2025 mandate compels every enterprise to receive e-invoices in structured formats, fostering auto-triggered payment initiation. Seamless data hand-over from invoice to payment removes manual reconciliation and supplier chasing. Early adopters in manufacturing and automotive supply chains report faster days-sales-outstanding and lower dispute overheads. Fintech integrators bundle e-invoice parsing with embedded SCT Inst initiation, selling subscription APIs to accounting software providers. The regulation therefore fortifies Germany real time payments market as corporates re-engineer procure-to-pay cycles.[3]European Commission, “Payment Services Overview,” European Commission, finance.ec.europa.eu.

Request-to-Pay Revolutionizes E-Commerce Checkout Experience

R2P empowers merchants to push invoice-like requests into buyers’ mobile banking apps, allowing confirmation with biometric authentication and eliminating card fees. German fashion and electronics retailers trial R2P to reduce drop-outs at payment pages. Settlement in under 10 seconds unlocks instant shipping and same-day refunds. PSPs monetize R2P through value-adds such as partial payments, loyalty integration, and chargeback-free settlement assurances. Wider roll-out across France and Benelux spreads network effects that feed back into Germany real time payments market momentum.

Fintech Innovation Sparks ‘Buy Now Pay Instantly’ Services

Urban-focused fintechs overlay Giropay’s SCT Inst rails with proprietary scoring engines to offer immediate merchant settlement alongside installment plans for consumers. This hybrid of BNPL and instant transfer widens acceptance among younger demographics who prefer account-to-account flows. Retailers gain higher conversion and lower payment cost than traditional interchange-based models. Banks partner with fintechs to supply credit lines, creating joint products that deepen customer engagement. These services enlarge Germany real time payments market beyond low-value P2P use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IBAN-name-mismatch false positives raising abandonment rates | - 4.2% | Germany, with greater impact in cross-border scenarios | Short term (≤ 2 years) |

| Fragmented merchant surcharge rules limiting adoption in micro-ticket segments | - 3.5% | Germany, with regional variations | Medium term (2-4 years) |

| Limited evening & weekend liquidity windows for smaller PSPs | - 2.8% | Germany, with emphasis on regional banks | Short term (≤ 2 years) |

| Value-added-service monetisation uncertainty for banks | - 2.3% | Germany, EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IBAN-Name Verification Challenges Impede Transaction Completion

Mandatory name-match checks, though effective against APP fraud, currently flag numerous legitimate transfers because of abbreviations or legal entity variants. End-users abort journeys when repeated failures appear, eroding trust. Cross-border payments suffer higher drop-rates as character sets and trading names diverge. PSPs invest in fuzzy-matching engines and customer education to mitigate attrition. Until algorithms mature, false positives will cap short-term growth in Germany real time payments market.

Fragmented Surcharge Rules Limit Micro-Ticket Uptake

German merchants apply mixed approaches to passing fees on sub-EUR 5 transactions, deterring uniform rollout of instant transfers at kiosks, transit, and quick-serve restaurants. Regional interpretations of fee caps create compliance ambiguity. PSPs hesitate to promote SCT Inst for micro-ticket verticals without clear revenue logic, hampering broader Germany real time payments industry penetration. Harmonized guidance from Bundesbank and merchant associations is needed to unlock this long-tail volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: P2B Growth Outpaces P2P Dominance

Peer-to-Business volumes are projected to register a 38.71% CAGR through 2031, reflecting corporate alignment with e-invoicing and Request-to-Pay integration. P2P still accounts for 59.20% of Germany real time payments market share in 2025, yet its growth normalizes as the user base nears ubiquity. Germany real time payments market size for P2B is forecast to broaden materially as retailers, utilities, and professional services embed instant pay links into billing workflows. Fintech wallets like wero lower friction by alias-based payments, encouraging further P2P stickiness.

Businesses benefit from real-time cash positioning and reduced interchange when accepting P2B transfers. Government incentives such as public-sector acceptance for tax remittances will reinforce momentum. P2P innovation now concentrates on value-added layers including split-bill and social commerce. Collectively, these vectors diversify Germany real time payments market avenues and help achieve scale.

By Component: Services Segment Accelerates as Platforms Mature

Platform investments delivered 67.40% revenue in 2025 as banks raced to achieve basic SCT Inst capability. Now that core connectivity stabilizes, Services are forecast to contribute most incremental revenue, expanding at 32.37% CAGR. Germany real time payments market size for professional services covers integration, compliance consulting, fraud mitigation, and liquidity optimization.

Smaller PSPs outsource rulebook updates, VoP connectivity, and ISO 20022 enrichment to managed-service specialists. Treasury advisory firms package instant payments with cash-forecast modules. Competitive differentiation therefore shifts from speed of settlement to depth of data analytics and contextual value. Vendors that orchestrate multi-rail routing, combine R2P, and wrap reconciliation dashboards will capture higher margins in Germany real time payments market.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premise Dominance

On-premise solutions retained 67.10% share in 2025 as German banks prioritized sovereignty and direct oversight. However, cloud deployments are rising at a 33.84% CAGR, driven by compressed IPR deadlines and elastic scaling requirements. Smaller cooperative banks leverage payment-as-a-service offerings to comply without major capex, expanding Germany real time payments market size within regional networks.

Regulators permit cloud usage provided data residence stays within the European Economic Area. Vendors respond with in-country data centers and shared compliance certifications. Hybrid architectures, in which clearing gateways run on-premise while analytics and fraud engines sit in cloud, offer a transition path. This balanced model keeps sensitive customer data internal while exploiting external compute for surge events in Germany real time payments market.

By Enterprise Size: SMEs Embrace Digital Payment Innovation

Large enterprises generated 64.30% of 2025 revenue, but SMEs now record the highest 30.69% CAGR. Instant settlement tightens cash-conversion cycles, enabling SMEs to fund inventory without bridging loans. Open-banking payment initiation lowers onboarding complexity and cost, democratizing access to Germany real time payments industry solutions.

Fintech aggregators bundle accounting plugins, simple QR invoicing, and automated reconciliation, removing the need for internal IT. SME adoption nurtures network effects as suppliers and buyers converge on the same rails, drawing further volume into Germany real time payments market. Banks that craft tiered pricing and educational outreach stand to capture this under-served segment.

By End-User Industry: Government Sector Emerges as Growth Leader

Retail & e-commerce still drives 33.40% of Germany real time payments market size, exploiting instant settlement to reduce cart abandonment. Nevertheless, Government & Public Sector advances at 35.60% CAGR as the digital euro roadmap accelerates. Municipalities pilot instant tax disbursements and welfare payments to improve citizen experience. Public-sector involvement legitimizes instant rails and boosts trust, supporting broader Germany real time payments market expansion.

Utilities and telecom firms adopt SCT Inst for late-bill recovery, while healthcare insurers test instant claim payouts. BFSI players refine internal high-value transfers to streamline liquidity between subsidiaries. Cross-sector diversification stabilizes transaction mix and underpins sustained Germany real time payments market growth.

Geography Analysis

Germany real time payments market has uneven regional momentum. Urban conurbations such as Berlin, Munich, Hamburg, and Frankfurt dominate volume because of high fintech density and digitally savvy consumers. Bundesbank data show that cash usage fell to 51% in 2023 while mobile payments hit 6%, demonstrating readiness for account-to-account instant flows. Card or smartphone acceptance is available at 80% of point-of-sale outlets, creating fertile ground for instant transfers.

The Sparkassen and Volksbanken networks extend reach into rural areas. Their migration to ISO 20022 by end-2025 will enable universal instant capability, leveling service parity with large city banks. Cross-border commerce with France and Benelux accelerates adoption of multi-currency aliases through the EPI-backed wero wallet, positioning Germany as a pan-European hub.

Participation in European clearing schemes such as RT1 and TIPS strengthens Germany real time payments market resilience and capacity. German PSPs push for low-latency connections to neighboring economies, reducing settlement friction for exporters in automotive and machinery sectors. Overall, regional initiatives integrate previously siloed payment infrastructures, elevating Germany real time payments market competitiveness within the single market.

Competitive Landscape

The market is indicating a moderately consolidated. Incumbent banks—Deutsche Bank, Commerzbank, and the Sparkassen/Volksbanken groups—retain entrenched customer relationships and deliver trusted clearing. Yet specialist PSPs such as Worldline, Adyen, and Stripe compete with agile API platforms that integrate effortlessly into merchant checkouts. Fintech entrants, exploiting open-banking mandates, layer contextual finance on top of instant rails, forcing incumbents to modernize.

Commerzbank’s partnership with PPI to deploy the TRAVIC-Payment Hub and shift all flows to ISO 20022 by 2025 exemplifies a defensive-innovation strategy aimed at sustaining relevance while complying with IPR requirements. German banks also co-invest in the European Payments Initiative, launching the wero digital wallet to pre-empt big-tech encroachment.

Opportunities remain in niche vertical propositions, cross-border optimizations, and data-driven fraud mitigation services. Players that orchestrate comprehensive ecosystems across R2P, BNPI, and digital-euro readiness are best placed to capture incremental share in Germany real time payments market. Competitive intensity is forecast to tighten as regulatory parity in basic processing shifts rivalry toward differentiated user experience and ancillary analytics.

Germany Real Time Payments Industry Leaders

ACI Worldwide, Inc.

Mastercard Inc.

Visa Inc.

PayPal Holdings, Inc.

Finastra International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The European Central Bank emphasized the need for a digital euro to enhance integration, competitiveness, and resilience of European payment systems at the France Payments Forum.

- March 2025: Deutsche Bank issued EUR 1.5 billion (USD 1.6 billion) Additional Tier 1 Notes at 7.125%, bolstering capital for payment infrastructure enhancement.

- January 2025: The European Payments Council released the first Verification of Payee scheme rulebook, guiding PSPs on name-matching protocols.

- November 2024: Deutsche Bundesbank completed Trigger Solution trials linking DLT platforms with TARGET to achieve real-time finality.

- October 2024: The European Payments Council announced 2025 rulebook updates, including SCT Inst response times of 5, 7, and 9 seconds and higher transaction ceilings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany real-time payments market as the total value of domestic transactions cleared in ten seconds or less, routed through SEPA Instant Credit Transfer rails or equivalent immediate payment schemes that guarantee fund availability, irrevocability, and instant confirmation. All values are expressed in USD billion, exclusive of charge-backs, card-based deferred settlement, and any cross-border transfers settled outside German clearing houses.

Scope exclusion: crypto token transfers and internal netting between correspondent banks lie outside the study.

Segmentation Overview

- By Transaction Type

- Peer-to-Peer (P2P)

- Peer-to-Business (P2B)

- By Component

- Platform / Solution

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-User Industry

- Retail and E-Commerce

- BFSI

- Utilities and Telecom

- Healthcare

- Government and Public Sector

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed payment-scheme managers, treasury heads at German mid-tier banks, leading fintech product owners, and retail platform finance leads across Frankfurt, Berlin, and Munich. The discussions clarified blended average transaction fees, ramp-up timelines for mandatory instant credit regulations, and likely SME adoption curves, enabling us to validate secondary signals and fine-tune driver sensitivities.

Desk Research

We began with macro-level inputs from public sources such as Deutsche Bundesbank quarterly payment statistics, Eurostat's Digital Economy tables, BaFin regulatory circulars, and the EPC's SCT Inst adoption dashboards. We then layered insights from trade bodies like the German Banking Industry Committee and EHI Retail Institute. Company filings, PSD2 open-banking API traffic releases, and news archived in Dow Jones Factiva helped us map competitive moves. Additional granularity on transaction mix was drawn from "Prime Time for Real Time" white papers and patent trend pulls via Questel. These references illustrate only a share of the secondary corpus consulted; many others informed data checks and context.

Market-Sizing & Forecasting

A top-down construct translates Bundesbank transaction volumes into market value through average fee and float-income assumptions, which are subsequently stress-tested using bottom-up snapshots of leading bank and PSP throughput. Key variables include: SCT Inst penetration rate, average ticket size, merchant service-charge spreads, e-commerce share of retail sales, and mandated fee caps from the 2024 Instant Payments Regulation. Multivariate regression models these drivers to 2030, while ARIMA smoothing handles short-term seasonality visible around bi-annual VAT cut reversals. Where bottom-up totals diverged, gap-handling rules favored audited bank disclosures over modeled estimates.

Data Validation & Update Cycle

Outputs pass a three-layer review: peer analyst check, senior domain lead sign-off, and an automated variance scan against new Bundesbank releases. The study refreshes each year, with interim patches issued if regulatory deadlines shift or fee caps are revised. Before delivery, we run one final sweep so clients always receive the latest view.

Why Mordor's Germany Real Time Payments Baseline Earns Trust

Published estimates vary because firms choose different service scopes, fee stacks, and refresh cadences. Our disciplined scoping around domestic, rail-authenticated instant payments only, coupled with annual recalibration, yields a figure buyers can reliably calibrate strategy against.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.19 B (2025) | Mordor Intelligence | - |

| USD 5.90 B (2024) | Global Consultancy A | Bundles deferred card clearing and cross-border SWIFT gpi flows, inflating base value |

| USD 2.63 B (2024) | Industry Journal B | Uses historic flat fee per transaction, ignores 2024 regulatory fee cap and upcoming October 2025 outbound mandate |

These contrasts show that when scope creep or static fee assumptions slip in, totals swing widely. By anchoring definitions to legislation, validating fees through practitioner interviews, and revisiting models each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is driving the rapid growth of Germany real time payments market?

Regulatory mandates such as the Instant Payments Regulation, higher SCT Inst limits, and compulsory e-invoicing combine with ISO 20022 migration and fintech innovation to propel a 36.15% CAGR through 2031.

How large will Germany real time payments market size become by 2031?

It is projected to reach USD 13.94 billion by 2031, up from USD 2.98 billion in 2026.

Which segment is expected to grow fastest?

Peer-to-Business transactions are forecast to rise at a 38.71% CAGR, fueled by Request-to-Pay and e-invoicing adoption.

Why are SMEs increasingly adopting instant payments?

Instant settlement enhances cash-flow management, reduces reliance on external financing, and is accessible via open-banking APIs that lower integration costs.

What role will the digital euro play?

The digital euro aims to provide a pan-eurozone retail payment instrument that complements existing instant rails, expanding acceptance and trust among public-sector users.

How are banks responding to competition from fintechs?

Traditional banks partner with technology vendors, migrate to ISO 20022, and invest in value-added services such as liquidity dashboards and fraud analytics to differentiate their offerings.

Page last updated on: