Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

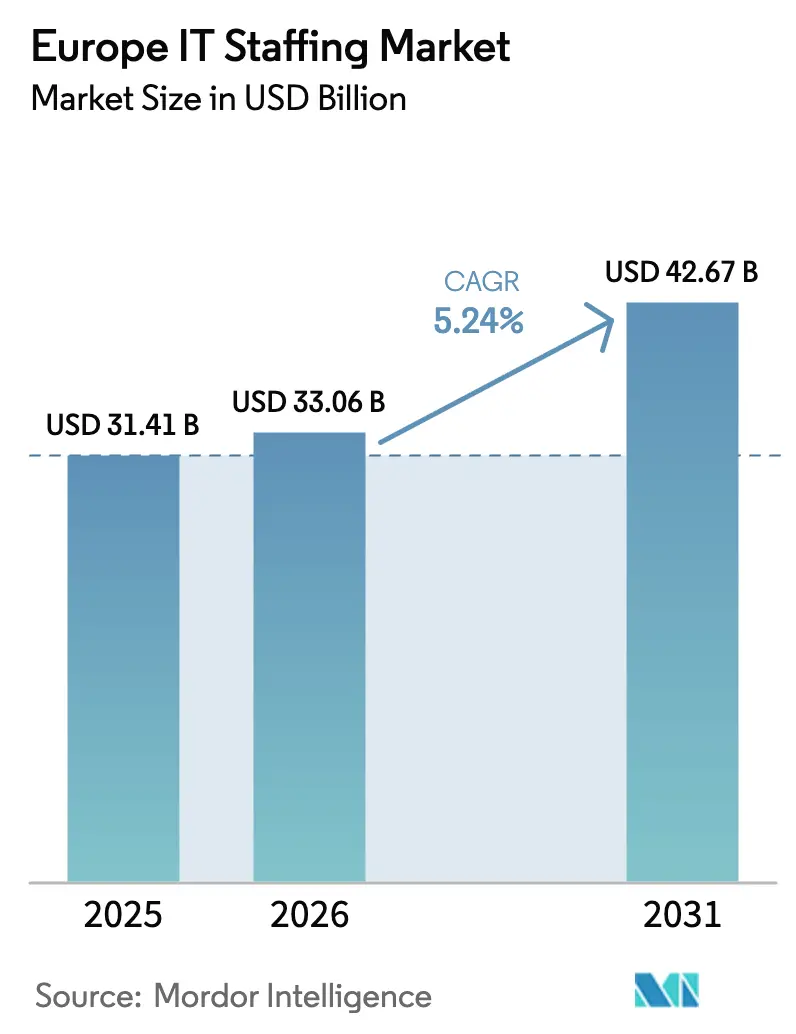

| Base Year Market Size (2025) | USD 31.41 Billion |

| Market Size (2026) | USD 33.06 Billion |

| Market Size (2031) | USD 42.67 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

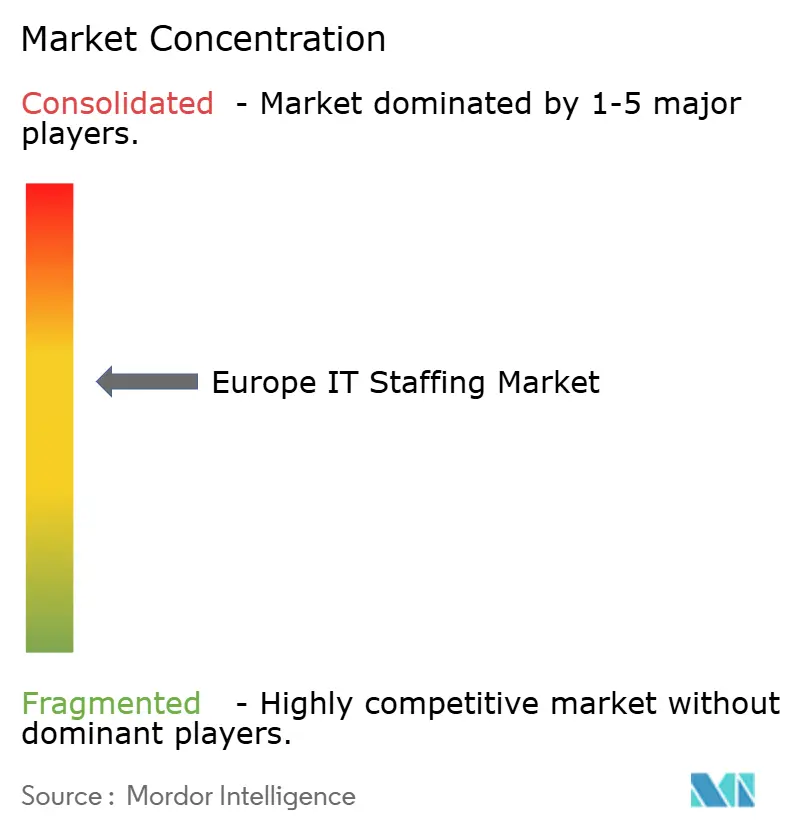

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IT Staffing Market Analysis by Mordor Intelligence

The Europe IT staffing market size is expected to grow from USD 31.41 billion in 2025 to USD 33.06 billion in 2026 and is forecast to reach USD 42.67 billion by 2031 at 5.24% CAGR over 2026-2031. This outlook reflects solid corporate spending on cloud, data, and cybersecurity programs, even as economic headwinds persist. Accelerating digital-first mandates, tighter rules under the EU AI Act, and the Corporate Sustainability Reporting Directive are expanding enterprise budgets for compliant talent solutions. Germany preserves its position as the single-largest buyer of IT staffing, while the United Kingdom is recording the swiftest expansion as post-Brexit hiring strategies prioritize specialist contractors. Contract/temporary roles continue to dominate, yet outcome-based Statement-of-Work (SOW) models are scaling quickly as clients seek cost-predictable delivery. Skills scarcity, especially for data, AI, and security roles, remains the chief pricing lever, with 75% of employers struggling to fill advanced positions.[1]ISC2, “Closing the EU’s Cybersecurity Workforce and Skills Gaps,” isc2.org

Key Report Takeaways

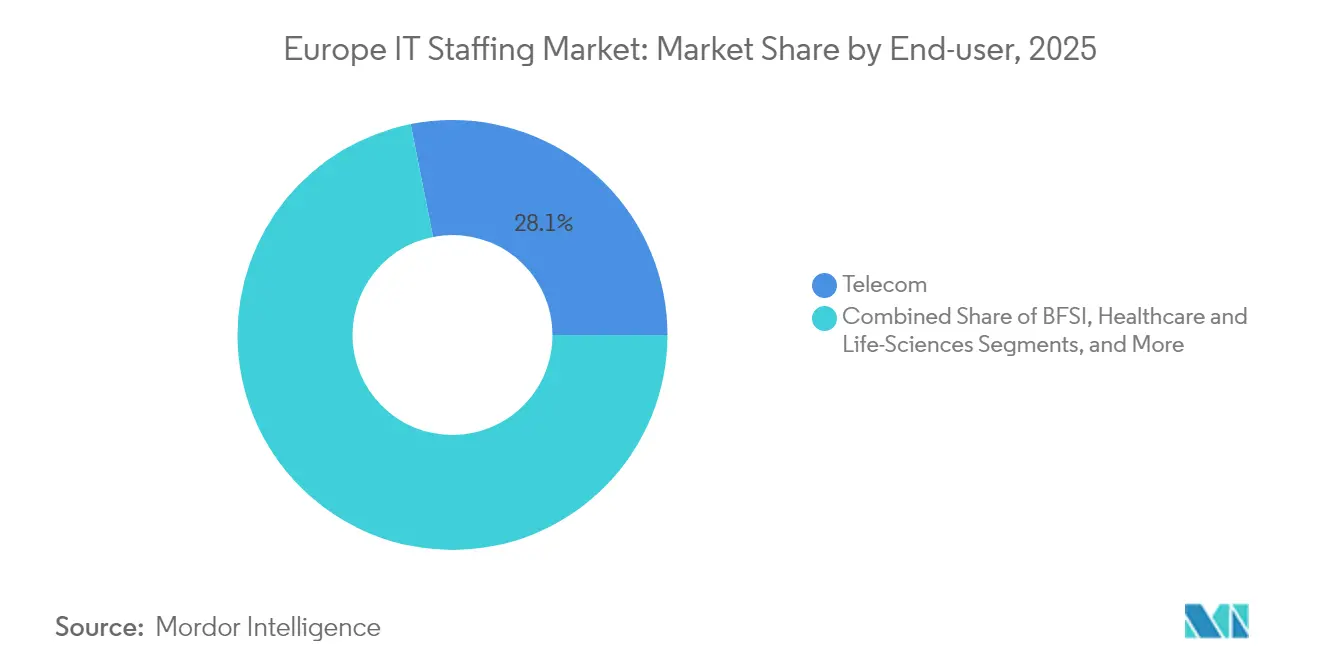

- By end-user industry, Telecom held 28.12% of Europe IT staffing market share in 2025, while Healthcare and Life Sciences is forecast to grow at a 5.88% CAGR to 2031.

- By employment model, Contract/Temporary accounted for 46.21% share of the Europe IT staffing market size in 2025; Statement-of-Work is projected to expand at a 7.05% CAGR through 2031.

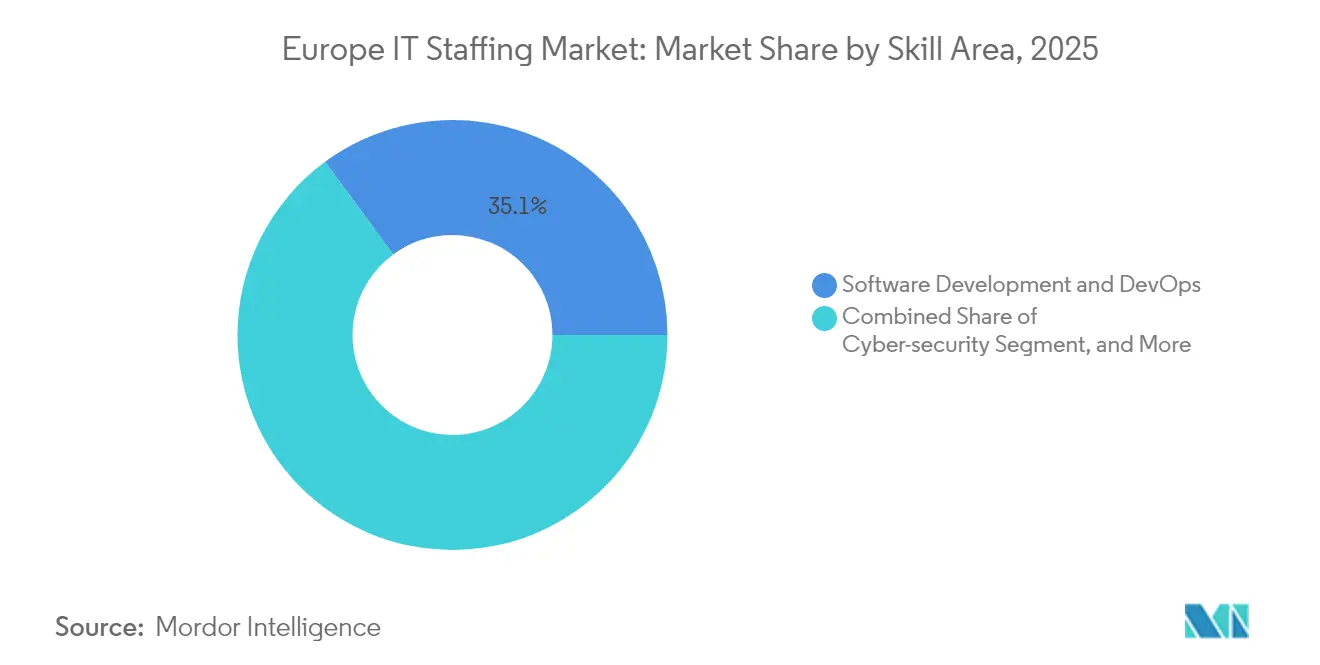

- By skill area, Software Development and DevOps commanded 35.10% share of the Europe IT staffing market size in 2025; Data, AI and Analytics is advancing at a 6.17% CAGR over the same period.

- By country, Germany led with 35.05% share of the Europe IT staffing market size in 2025, whereas the United Kingdom is expected to log the highest CAGR at 6.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe IT Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation surge across EU enterprises | +1.8% | Global, strongest in Germany and France | Medium term (2-4 years) |

| Widening ICT skills gap and ageing workforce | +1.5% | Global, acute in Northern Europe | Long term (≥ 4 years) |

| Proliferation of remote and hybrid-work staffing models | +0.9% | Global, led by UK and Netherlands | Short term (≤ 2 years) |

| Growing adoption of MSP / RPO outsourcing frameworks | +0.7% | EMEA core, expansion to Southern Europe | Medium term (2-4 years) |

| EU AI-Act compliance spurring demand for AI-ethics talent | +0.6% | EU-27, highest impact in Germany and France | Short term (≤ 2 years) |

| CSRD-driven need for "green-software" engineers | +0.4% | EU-27, early adoption in Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Surge Across EU Enterprises

EU companies are scaling cloud, AI, and advanced analytics programs at record pace, which is driving steady inflows of short-cycle project mandates for staffing suppliers. Large German manufacturers and French banks place premium demand on DevOps and cloud architects able to modernize legacy estates swiftly. Clients now issue multi-country requisitions that bundle development, migration, and security roles, encouraging vendors to cultivate pan-European talent benches. The outcome is rising average bill rates and faster assignment turnover, underpinning long-term volume growth in the Europe IT staffing market.

Widening ICT Skills Gap and Ageing Workforce

More than half of European businesses cannot secure the expertise they require, and retirement-driven attrition is widening the shortage for mid-to-senior technologists.[2]Euronews, “Looking for a job in ICT? These European countries are desperate for new hires,” euronews.com Salary inflation is most acute for data engineers and cybersecurity architects, sending total labor costs upward and steering enterprises toward contract sourcing to stay within budgets. This persistent mismatch increases client reliance on specialist firms that can recruit across borders or tap near-shore talent pools, sustaining momentum in the Europe IT staffing market through 2030.

Proliferation of Remote and Hybrid-Work Staffing Models

Widespread acceptance of location-agnostic work enables providers to source candidates from lower-cost regions, widening supply while trimming facility overheads. United Kingdom buyers are at the forefront, requesting hybrid rosters that mix on-site compliance roles with remote developers, further propelling flexible engagement forms. Technology platforms that monitor productivity and data security remotely are becoming standard value-adds, differentiating digitally mature providers in the Europe IT staffing market.

Growing Adoption of MSP / RPO Outsourcing Frameworks

Enterprise need for cost predictability and analytics-driven hiring decisions is accelerating the migration to managed service provider (MSP) and recruitment process outsourcing (RPO) agreements. Multinationals in manufacturing and retail now outsource full talent cycles, generating multi-year recurring revenues for large vendors. Providers that can overlay compliance assurance for AI Act, GDPR, and CSRD rules gain incremental wallet share, deepening client entrenchment across the Europe IT staffing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent talent shortages in niche skills (e.g., SAP/DevOps) | -1.2% | Global, most severe in Germany and UK | Long term (≥ 4 years) |

| Volatile macro conditions curbing discretionary IT hiring | -0.8% | Global, highest impact in France and Italy | Short term (≤ 2 years) |

| Stricter labour-leasing rules (e.g., Germany AÜG reforms) | -0.6% | Germany primary, spillover to Austria and Netherlands | Medium term (2-4 years) |

| Rise of direct-sourcing and freelancer platforms | -0.4% | Global, led by UK and Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Talent Shortages in Niche Skills

The cybersecurity workforce gap of 274,000 professionals across the EU and prolonged search cycles, often six months or more in Germany, are constraining delivery capacity. Clients unable to secure mission-critical skillsets delay or down-scale projects, tempering near-term revenue upside for vendors. In response, staffing firms are investing in re-skilling academies and cross-border recruitment desks to alleviate bottlenecks, but supply growth remains slower than demand.

Volatile Macro Conditions Curbing Discretionary IT Hiring

Inflationary pressure and geopolitical uncertainty make boards cautious about new project launches, producing intermittent booking cycles that weigh on contractor utilization. Leading agencies reported double-digit profit declines in 2024 as clients postponed non-essential upgrades. Though strategic digital programs continue, variance in quarterly order volumes complicates resource planning and can erode margins across the Europe IT staffing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Healthcare Pushes Digital Health Adoption

Telecom retained the largest slice of spending, accounting for 28.12% of Europe IT staffing market share in 2025, anchored by 5G roll-outs and network virtualization programs. Healthcare and Life Sciences is projected to log a 5.88% CAGR, the fastest among tracked verticals, on the back of electronic health record upgrades and telemedicine scale-ups that demand specialized security and interoperability expertise. The Europe IT staffing market size for healthcare engagements is set to widen every year through 2031 as hospitals address chronic IT vacancies that jeopardize patient data integrity.

Manufacturing continues to procure IoT and automation engineers for Industry 4.0 lines, while BFSI institutions keep security and fintech developers in steady rotation to meet open-banking deadlines. Retail and e-commerce operators, pursuing AI-driven personalization, contract data scientists for algorithm re-training. Public-sector digital-government programs in Spain and the Nordics add to baseline demand, producing a broad client mix that strengthens revenue visibility for diversified providers across the Europe IT staffing market.

By Employment Type: Outcome-Based Engagements Accelerate

Contract/temporary formats controlled 46.21% of overall spend in 2025, reflecting client preference for variable labor during budget cycles. Yet SOW engagements, designed around predefined deliverables—are forecast to expand 7.05% annually, signaling a pivot toward accountability-centric procurement. The Europe IT staffing market size linked to SOW agreements is expected to surpass permanent-placement revenues by 2028 as enterprises seek turnkey execution for cloud, AI, and cybersecurity initiatives.

Permanent placement retains relevance for leadership and regulatory-critical hires, but its share is tapering as wage inflation pushes clients toward blended workforce compositions. Temp-to-perm models offer risk-mitigation by extending evaluation periods, particularly for high-cost data and analytics roles. Vendors proficient in compliance, milestone tracking, and outcome pricing stand to capture disproportionate share of new SOW pipelines within the Europe IT staffing market.

By Skill Area: Data and AI Propel Premium Rates

Software Development and DevOps delivered 35.10% of bookings in 2025, underscoring its role as the foundation of digital ecosystems. Data, AI and Analytics, while smaller in absolute spend, will grow 6.17% per year through 2031 as the EU AI Act obliges firms to embed explainability and ethical-risk controls in deployed models. High-growth security sub-disciplines are intertwined, as AI deployments increase the attack surface and elevate demand for cybersecurity architects.

Cloud and infrastructure specialists remain essential as hybrid architectures standardize, but a shortage of multi-cloud engineers inflates pricing and extends lead times. Emerging fields, edge computing, AR/VR, and blockchain, are carving early niches, yet their share is still modest. Providers that cross-train talent into adjacent skills gain portfolio resilience, positioning them favorably to address evolving requisitions across the Europe IT staffing market.

Geography Analysis

Germany contributed 35.05% of 2025 revenue, drawn by its expansive manufacturing base and federal digitalization funds. Yet, 149,000 vacant IT posts reveal structural deficits that staffing firms are working to address through EU Blue Card and global sourcing programs. Wage premiums remain highest in automotive and industrial clusters, making Germany a stable but cost-intensive arena within the Europe IT staffing market.

The United Kingdom, advancing at a 6.55% CAGR, benefits from GBP 320 billion in projected AI-driven economic gains that continue to bolster technology headcount. Net tech employment reached 2.13 million workers in 2024, 6.4% of the national workforce, underlining deep digital adoption. London, Manchester, and the wider South East form dense hiring corridors, and flexible visa pathways help offset talent outflows.

Southern Europe is narrowing the gap through EU recovery funds that sponsor cloud and cybersecurity upgrades. Spain posted 8% IT staffing growth in 2024, while Italy recorded 3%. France remains steady, with telecom and aerospace budgets sustaining demand despite broader economic softness. The European Commission’s EUR 65 billion skills plan seeks to reduce cross-border frictions and create more even growth, a trend that should expand accessible addressable spend for regional vendors servicing the Europe IT staffing market.

Competitive Landscape

The supplier ecosystem is moderately fragmented. Randstad, Adecco, and ManpowerGroup leverage scale and diversified service menus but now face competition from data-driven specialists targeting AI, green-software, and cybersecurity niches. Randstad’s digital talent platform generated EUR 2 billion in 2024 marketplace revenue and is slated for further expansion, showcasing how incumbents are pivoting to tech-enabled fulfillment.

Deal activity is rising; private-equity backed consolidation lifted transaction counts 18% year-over-year in Q2 2024. CGI’s acquisition of BJSS added 2,400 consultants with advanced cloud and AI skills, fortifying vertical domain depth in retail and public services. Disruptors such as AI-centric matching engines increase speed and accuracy in candidate discovery, while embedded compliance checks align with tightening EU rules.

Margins remain pressured by salary inflation and regulatory overhead, but vendors that automate screening, onboarding, and timesheet processes recover cost headroom. Boutique firms exploiting narrow skills clusters-like AI ethics auditors-achieve premium pricing yet risk scalability limits. Strategic alliances between staffing houses and SaaS workforce platforms are emerging as go-to-market accelerators, sharpening competitive intensity across the Europe IT staffing market.

Europe IT Staffing Industry Leaders

Randstad N.V

AQUENT LLC

Vero HR Ltd.

VHR Consulting Ltd.

Haselhoff Groep B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CGI completed its acquisition of UK-based BJSS, adding 2,400 professionals and lifting its UK headcount above 8,500.

- February 2025: BlackRock acquired 1,749,120 additional shares of ManpowerGroup, increasing its holding to 14.40% of outstanding shares.

- January 2025: Randstad announced the merger of Monster and CareerBuilder, pending Q3 2024 regulatory clearance.

- November 2024: Mona AI secured EUR 2 million seed funding to enhance its multilingual AI recruitment avatar for European staffing agencies.

Europe IT Staffing Market Report Scope

The major goal of the IT staffing process is to locate qualified applicants to fill various job roles inside the IT firm. It involves finding applicants, evaluation, selection, recruitment, and appraisal, which are parts of the systematic implementation process of the human resources plan.

The European IT Staffing market can be classified by end-user industry (telecom, BFSI, healthcare, manufacturing, retail), by country (United Kingdom, Germany, France, Spain, Italy, and the Rest of Europe). The report offers market forecasts and size in value (USD) for all the above segments.

By End-user Industry

| Telecom |

| BFSI |

| Healthcare and Life-Sciences |

| Manufacturing and Industry 4.0 |

| Retail and e-Commerce |

| Other End-user Industries |

By Employment Type

| Contract/Temporary |

| Permanent Placement |

| Temp-to-Perm |

| Statement-of-Work (SOW) / Project-Based |

By Skill Area

| Software Development and DevOps |

| Cloud and Infrastructure |

| Data, AI and Analytics |

| Cyber-security |

| Emerging Tech (IoT/AR-VR/Blockchain) |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By End-user Industry | Telecom |

| BFSI | |

| Healthcare and Life-Sciences | |

| Manufacturing and Industry 4.0 | |

| Retail and e-Commerce | |

| Other End-user Industries | |

| By Employment Type | Contract/Temporary |

| Permanent Placement | |

| Temp-to-Perm | |

| Statement-of-Work (SOW) / Project-Based | |

| By Skill Area | Software Development and DevOps |

| Cloud and Infrastructure | |

| Data, AI and Analytics | |

| Cyber-security | |

| Emerging Tech (IoT/AR-VR/Blockchain) | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe IT staffing market in 2026?

It is valued at USD 33.06 billion and is forecast to rise to USD 42.67 billion by 2031.

Which skill set shows the fastest growth in European IT hiring?

Data, AI & Analytics roles are expanding at a 6.17% CAGR through 2031.

Why is Statement-of-Work gaining traction with European buyers?

Enterprises prefer outcome-based engagements that lock in deliverables and limit budget risk, pushing SOW demand up 7.05% annually.

Which country is the fastest-growing destination for IT staffing services?

The United Kingdom leads with a projected 6.55% CAGR through 2031 due to strong AI investment plans.

What is the biggest restraint on IT staffing growth across Europe?

Chronic shortages in niche skills, especially cybersecurity and DevOps, limit fulfillment capacity and dampen potential growth.

Page last updated on: