Germany HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

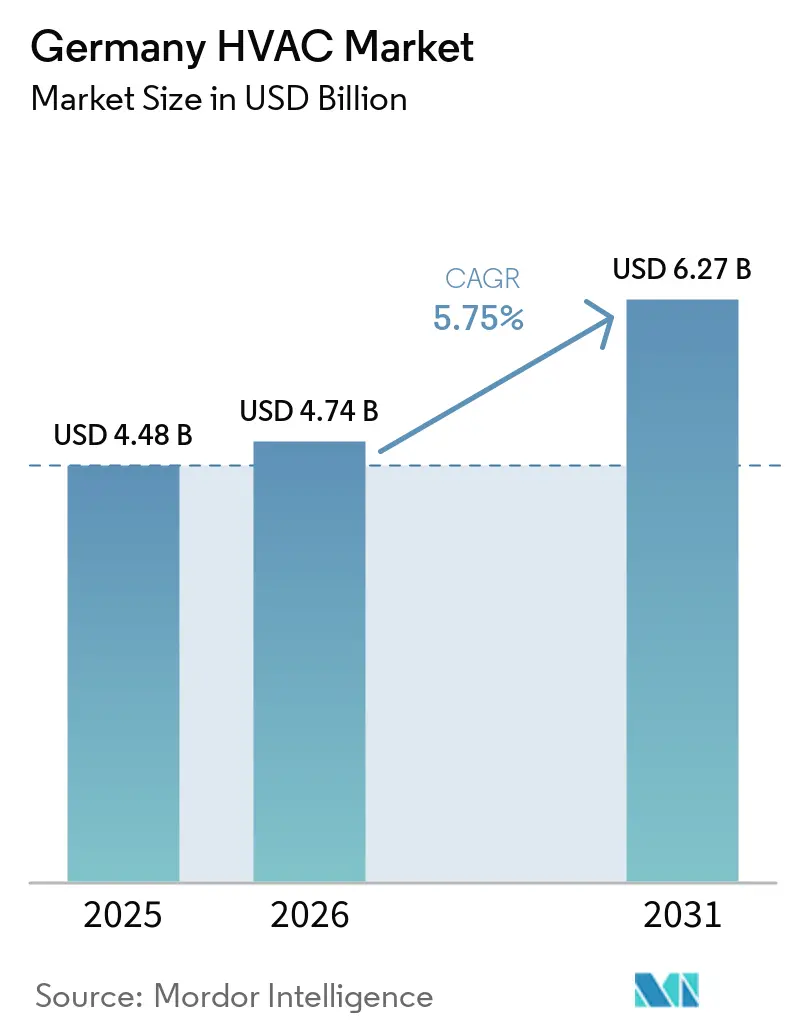

| Base Year Market Size (2025) | USD 4.48 Billion |

| Market Size (2026) | USD 4.74 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

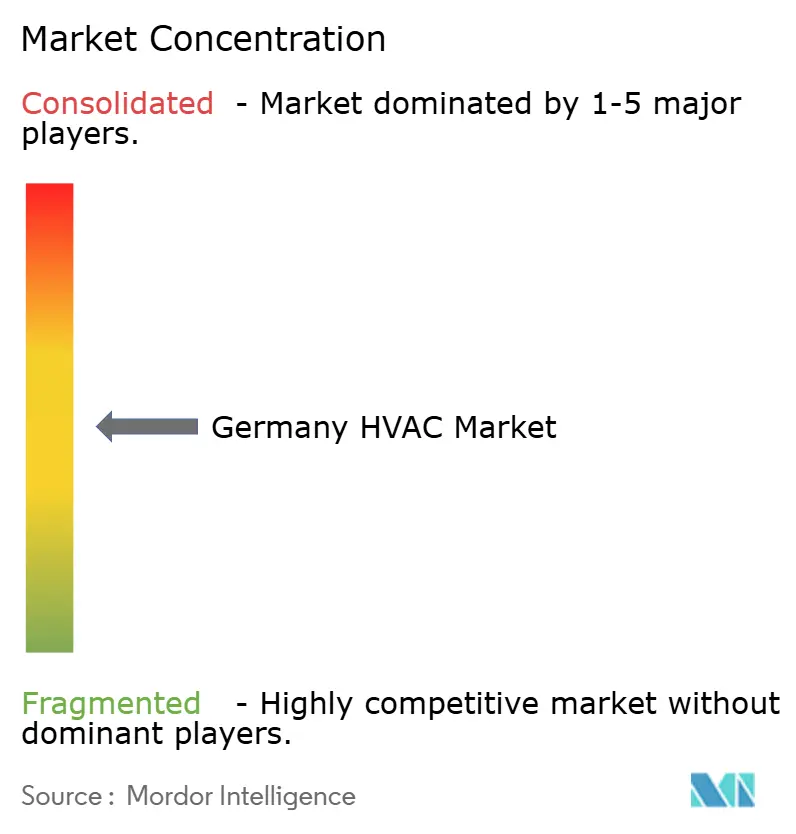

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany HVAC Market Analysis by Mordor Intelligence

The Germany HVAC market size was valued at USD 4.48 billion in 2025 and estimated to grow from USD 4.74 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031). Equipment sales continue to anchor value creation, yet demand is tilting toward integrated service offerings that optimize system performance over the full life cycle. Heat pump adoption accelerated after the Building Energy Act mandated 65% renewable energy in new heating systems, lifting the renewable share of installations to 69.4% in 2024. Service revenue gains outpace hardware expansion as installers address complex commissioning tasks and remote energy-management needs. Regional opportunities vary: Bavaria and Baden-Württemberg capture the largest slice of the Germany HVAC market, while the East registers the fastest growth because of fund-supported retrofit programs. Commercial customers amplify short-term momentum by replacing legacy chillers and boilers to satisfy corporate net-zero timelines and upcoming EU reporting rules.

Key Report Takeaways

- By component, HVAC equipment controlled 71.75% of the Germany HVAC market share in 2025, whereas HVAC services are forecast to post the highest 7.02% CAGR through 2031.

- By end-user, residential buildings held 61.15% of 2025 revenue, while the commercial segment is projected to expand at a 6.26% CAGR up to 2031.

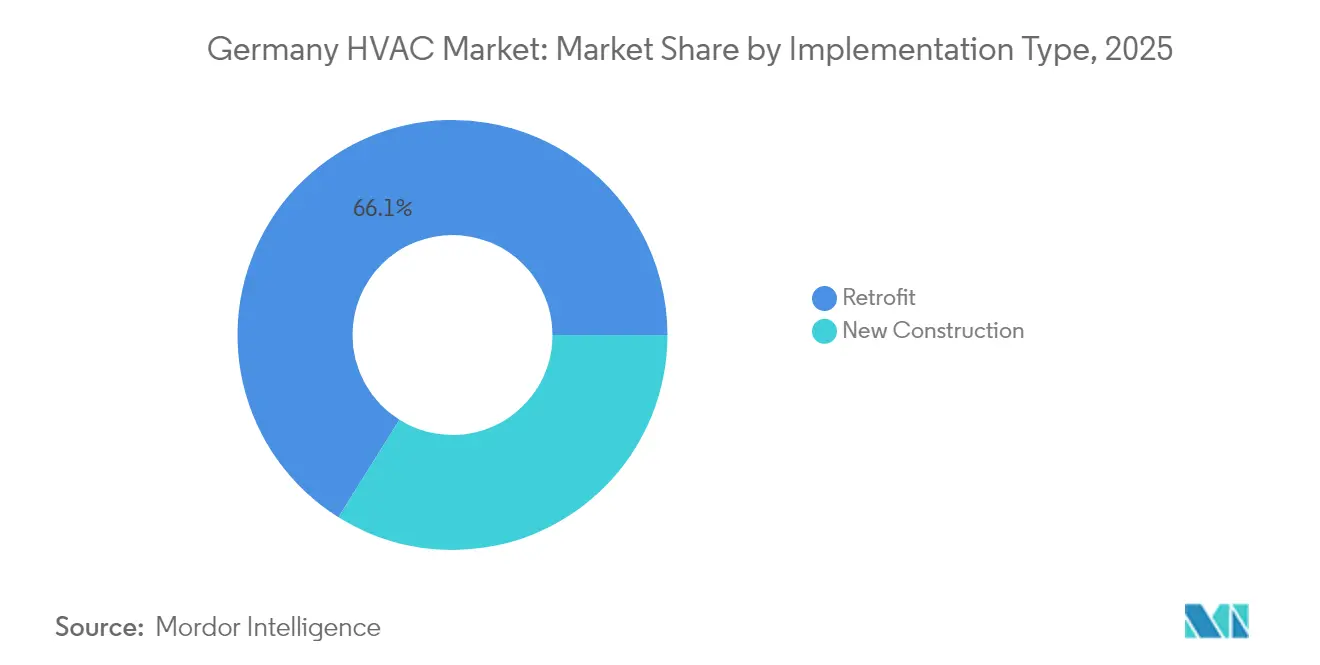

- By implementation type, retrofit projects commanded 66.10% of the Germany HVAC market size in 2025, yet new construction is set to grow at a faster 7.08% CAGR.

- By region, the South led with 24.40% revenue share in 2025; the East is poised for a 6.05% CAGR, the highest regional pace over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and retrofit surge | +1.2% | Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Building Energy Act electrification push | +2.1% | Nationwide, early in Baden-Württemberg and Bavaria | Short term (≤2 years) |

| Heat pump uptake in new residential stock | +1.8% | South and West regions | Short term (≤2 years) |

| Smart HVAC and building-automation retrofits | +0.9% | Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Climate-resilient cooling demand | +0.7% | Large urban areas | Long term (≥4 years) |

| Corporate net-zero commitments | +1.1% | Industrial corridors and metro hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Building Energy Act Electrification Push

The Building Energy Act took effect in 2024, obligating every new heating system to source at least 65% of its energy from renewables.[1]Federal Ministry for Economic Affairs and Climate Action, “Building Energy Act,” bmwk.de Enforcement triggered a rapid shift toward heat pumps in Germany, which powered nearly seven in ten new residential projects in 2024. The rule also created a predictable retrofit pipeline because fossil-fuel systems may operate until their economic end of life, but must be replaced with compliant alternatives by 2045. More than 10,000 municipalities are drafting local heat plans that favor networked heat pumps and low-temperature district grids. Together, these measures lock in sustained demand across the Germany HVAC market.

Heat Pump Uptake in New-Build Residential Segment

Heat pump penetration skyrocketed after 2024 as total system cost dropped 12% year over year while gas prices stayed elevated.[2]Federal Statistical Office, “Record Heat Pump Adoption in 2024,” destatis.de Air-source units claim 78% of new installations because of their lower capex and easier siting, whereas ground-source models serve noise-sensitive or space-constrained projects. The transition fuels parallel growth in thermal storage, smart thermostats, and envelope upgrades that maximize heat-pump efficiency. Contractors deepen specialization in refrigerant handling, commissioning, and digital controls, reinforcing the service orientation of the Germany HVAC market.

Smart HVAC and Building-Automation Retrofits

From 2025, large non-residential buildings must integrate automated HVAC controls when the system’s combined heating or cooling capacity exceeds 290 kW.[3]German Energy Agency, “Municipal Heat Planning,” dena.de This rule is nudging owners to embed sensors, analytics, and remote optimization platforms. Green-bond frameworks and EU taxonomy labels reduce financing costs for eligible smart-retrofit investments by as much as 25%, widening project pipelines in top German cities. Interoperable software layers link building controls with district-energy schemes, enabling demand response and grid-balancing services that generate incremental savings.

Corporate Net-Zero Commitments Boosting Commercial Upgrades

Sixty-seven percent of DAX-listed firms have pledged net-zero operations by 2035 at the latest. Building energy use makes up roughly one-third of their carbon footprint, so large occupiers are replacing legacy chillers, boilers, and control systems years before regulatory deadlines. Variable refrigerant flow solutions dominate these retrofits because of modular scalability and energy recovery features that cut consumption up to 30% in partial-load conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost of efficient systems | -0.8% | Rural municipalities | Short term (≤2 years) |

| Skilled installer shortage | -1.1% | East Germany and rural counties | Medium term (2-4 years) |

| Policy uncertainty on subsidies | -0.6% | Nationwide | Short term (≤2 years) |

| Supply-chain volatility for key components | -0.9% | All regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Installer Shortage

Roughly 60,000 HVAC positions were vacant in 2024, and apprenticeship enrollment fell 23% in five years. Heat pumps demand additional competencies in electrical wiring, refrigerant management, and digital commissioning, creating bottlenecks in residential and small-commercial projects. Rural districts feel the pinch most acutely because training centers cluster in urban areas. To bridge the gap, manufacturers such as Daikin opened large training campuses and rolled out mobile academies that travel to underserved regions.

Supply-Chain Volatility for Key Components

Lead times for compressors jumped beyond 16 weeks in 2024, doubling from pre-pandemic benchmarks, while semiconductor shortages raised delivery risk for electronic control boards. Heat-pump makers now keep only four to six weeks of buffer inventory, leaving projects vulnerable to shipping delays. Copper and steel price swings add double-digit cost uncertainty. Installers respond by renegotiating contracts to include escalation clauses or by adopting multivendor sourcing strategies, but margin pressure persists and tempers growth across the Germany HVAC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Equipment Remains the Bedrock While Services Accelerate

Germany HVAC market size for equipment stood at USD 3.21 billion in 2025, equal to 71.75% of total revenue. Heat pumps alone added more than 34% annual unit growth as consumers chased compliance and long-term savings. Boilers slipped 28% because gas options face an uncertain future under the Building Energy Act. Variable refrigerant flow systems won a greater share in offices and retail centers owing to zone-specific temperature control.

Service income recorded the highest trajectory at a 7.02% forecast CAGR. Complex commissioning, remote monitoring, and predictive maintenance drive spending that frequently exceeds original equipment cost over the life cycle. Energy-management projects in commercial buildings average EUR 45,000 to 65,000 (USD 48,000 to 69,000), roughly triple a standard preventive-maintenance contract. As heat-pump density grows, specialized leak testing and F-gas compliance checks become recurring revenue streams, further deepening the service dimension of the Germany HVAC market.

By End-User Industry: Residential Weight Meets Commercial Momentum

The residential segment claimed 61.15 of % Germany HVAC market share in 2025, largely because 19.3 million single-family homes still operate fossil-fuel boilers that require replacement before 2045. Heat-pump integration in new housing already outnumbers gas systems by more than two to one, turning builders into key volume drivers. Retrofit adoption remains measured because owners must first upgrade envelopes or electrical wiring to handle pump loads, although subsidy programs alleviate some of the upfront burden.

Commercial facilities will likely deliver faster expansion at a 6.26% CAGR. ESG disclosure rules push corporations to slash scope-one emissions from building operations. Office complexes, shopping centers, and hospitality venues adopt VRF and centralized controls that meet both reporting and occupant-comfort requirements. Industrial plants focus on process heat recovery and integration with district-heating networks. Public facilities capitalize on earmarked grants for schools and hospitals, creating stable order pipelines for contractors across the Germany HVAC industry.

By Implementation Type: Retrofit Dominates, New Construction Rises

Retrofit activity formed 66.10% of the Germany HVAC market size in 2025, reflecting the fact that three-quarters of German homes predate 1990 efficiency codes. Typical residential heat-pump retrofits cost EUR 18,000 to 28,000 (USD 19,000 to 30,000), partly because installers need to resize radiators or boost electrical capacity. In commercial settings, design teams employ energy audits and thermographic surveys to pinpoint savings before committing to capital upgrades.

New construction shows the strongest growth at 7.08% CAGR. Builders integrate HVAC design early through Building Information Modeling, avoiding the oversizing that plagued legacy installations. Passive-house influence is widening, leading to ventilation systems with near-total heat recovery and ultra-tight envelopes that keep mechanical loads low. These buildings often feature modular plant rooms that simplify future equipment swaps, reinforcing lifetime value for manufacturers and service partners.

Geography Analysis

The South captured the largest 24.40% slice of the Germany HVAC market in 2025 thanks to robust economic output, superior household income, and long-standing state-level subsidies that favor renewable heating. Bavaria’s craftsman network is dense, so installation backlogs remain shorter there than in other regions. Baden-Württemberg’s local building code anticipates federal targets, further accelerating orders. Public-funded commercial projects such as hospitals and universities also underpin stable demand.

The East is the fastest-growing region, poised for a 6.05% CAGR, because municipal funding channels direct EU cohesion money to upgrade dated multifamily blocks erected before reunification. Saxony and Thuringia lure manufacturers with lower land costs, generating factory expansions that create process-heating opportunities. Training partnerships between equipment firms and technical universities have started to address the installer shortage in Dresden and Leipzig, narrowing a key bottleneck.

The West continues to record solid activity grounded in dense population and the industrial heft of North Rhine-Westphalia, where energy-intensive sectors rush to recover waste heat and electrify space heating. Meanwhile, the North integrates offshore wind into heat-pump operations, leveraging cheap renewable electricity to power residential and commercial systems. Central Germany and Berlin harness smart-building pilots that explore district-level load orchestration. Across all regions, supply-chain swings and technician availability define the pace at which the Germany HVAC market can fully exploit its renewable-heating potential.

Competitive Landscape

Market concentration is moderate as domestic champions contend with global groups. Viessmann, Vaillant, and Bosch Thermotechnik benefit from strong distributor ties and service fleets, anchoring a combined share large enough to influence channel pricing. International players such as Daikin, Mitsubishi Electric, and Johnson Controls expand local production and training to offset the incumbents’ home-field edge. Product breadth, compliance support, and digital service layers now matter more than headline equipment cost.

Growth strategies pivot toward factory expansions, acquisitions, and alliances with software developers. Viessmann earmarked EUR 200 million to expand Allendorf heat-pump output and add 800 jobs in 2025. Vaillant bought Stiebel Eltron’s commercial controls arm to speed smart-HVAC growth. Bosch rolled out an IoT platform that links heat pumps with rooftop PV and storage, giving homeowners a single mobile interface. Partnering with utilities, Johnson Controls will deploy 10,000 grid-connected heat-pump units that act as a flexible load during high-renewable generation periods.

White-space opportunities persist in rural coverage, data-center cooling, and industrial process electrification. Emerging disruptors experiment with direct-to-consumer ecommerce and subscription models that bundle equipment, installation, and predictive maintenance. Larger incumbents counter by embedding long-term service agreements into product sales. Regulation favors firms that can provide F-gas compliant refrigerants and transparent life-cycle assessments, filtering out lower-tier importers and boosting brand-equity advantages across the Germany HVAC market.

Germany HVAC Industry Leaders

Carrier Corporation

Robert Bosch GmbH

Midea Group Co. Ltd

Johnson Controls International PLC

Daikin Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Viessmann Climate Solutions committed EUR 200 million (USD 213 million) to enlarge heat-pump production in Allendorf, adding 800 jobs.

- December 2024: Bosch Thermotechnik unveiled IDS Connect, a platform that unifies heat pumps, solar arrays, and storage into one smart-home ecosystem.

- November 2024: Daikin opened a EUR 150 million (USD 160 million) European training center in Düsseldorf to certify installers for next-generation heat pumps.

- October 2024: Vaillant acquired Stiebel Eltron’s commercial building-automation unit for EUR 85 million (USD 91 million), bolstering its smart-HVAC portfolio.

Germany HVAC Market Report Scope

HVAC systems, short for heating, ventilation, and air conditioning, are designed to regulate temperature and humidity, ensuring comfortable environmental conditions and delivering clean air in buildings. They comprise various components, including boilers, furnaces, refrigerators, humidifiers, and heat pumps.

The study tracks the revenue accrued through the sale of HVAC products in residential, commercial, industrial sector by various players in Germany. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The Germany HVAC Market Report is Segmented by Component (HVAC Equipment, HVAC Services), End-User Industry (Residential, Commercial, Industrial, Public and Institutional), Implementation Type (New Construction, Retrofit), and Geography (North, South, East, West, Central). The Market Forecasts are Provided in Terms of Value (USD).

| HVAC Equipment | Heating Equipment | Heat Pumps |

| Boilers | ||

| Radiators | ||

| Cooling Equipment | Air Conditioners | |

| Chillers | ||

| Variable Refrigerant Flow Systems | ||

| Ventilation Equipment | Air Handling Units | |

| Energy Recovery Ventilators | ||

| HVAC Services | Installation | |

| Maintenance and Repair | ||

| Energy Management and Building Automation | ||

| Residential |

| Commercial |

| Industrial |

| Public and Institutional |

| New Construction |

| Retrofit |

| North |

| South |

| East |

| West |

| Central |

| By Component | HVAC Equipment | Heating Equipment | Heat Pumps |

| Boilers | |||

| Radiators | |||

| Cooling Equipment | Air Conditioners | ||

| Chillers | |||

| Variable Refrigerant Flow Systems | |||

| Ventilation Equipment | Air Handling Units | ||

| Energy Recovery Ventilators | |||

| HVAC Services | Installation | ||

| Maintenance and Repair | |||

| Energy Management and Building Automation | |||

| By End-User Industry | Residential | ||

| Commercial | |||

| Industrial | |||

| Public and Institutional | |||

| By Implementation Type | New Construction | ||

| Retrofit | |||

| By Region | North | ||

| South | |||

| East | |||

| West | |||

| Central | |||

Key Questions Answered in the Report

How big is the Germany HVAC market in 2026?

The Germany HVAC market size reached USD 4.74 billion in 2026 and is forecast to hit USD 6.27 billion by 2031.

What is driving heat-pump adoption across Germany?

A 2024 law mandating 65% renewable energy in new heating systems and rising gas prices are propelling rapid heat-pump penetration.

Which region is growing fastest in Germany’s HVAC sector?

The East is projected to expand at a 6.05% CAGR because EU funds back large-scale retrofits of aging building stock.

Why are HVAC services outpacing equipment growth?

Complex commissioning, smart-control retrofits, and ongoing optimization now generate recurring revenue that often surpasses initial hardware cost.

What limits Germany HVAC market growth?

Key obstacles include a shortage of skilled installers, higher upfront cost of efficient systems, and supply-chain delays for compressors and electronics.

Page last updated on: