Europe Ventilation Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

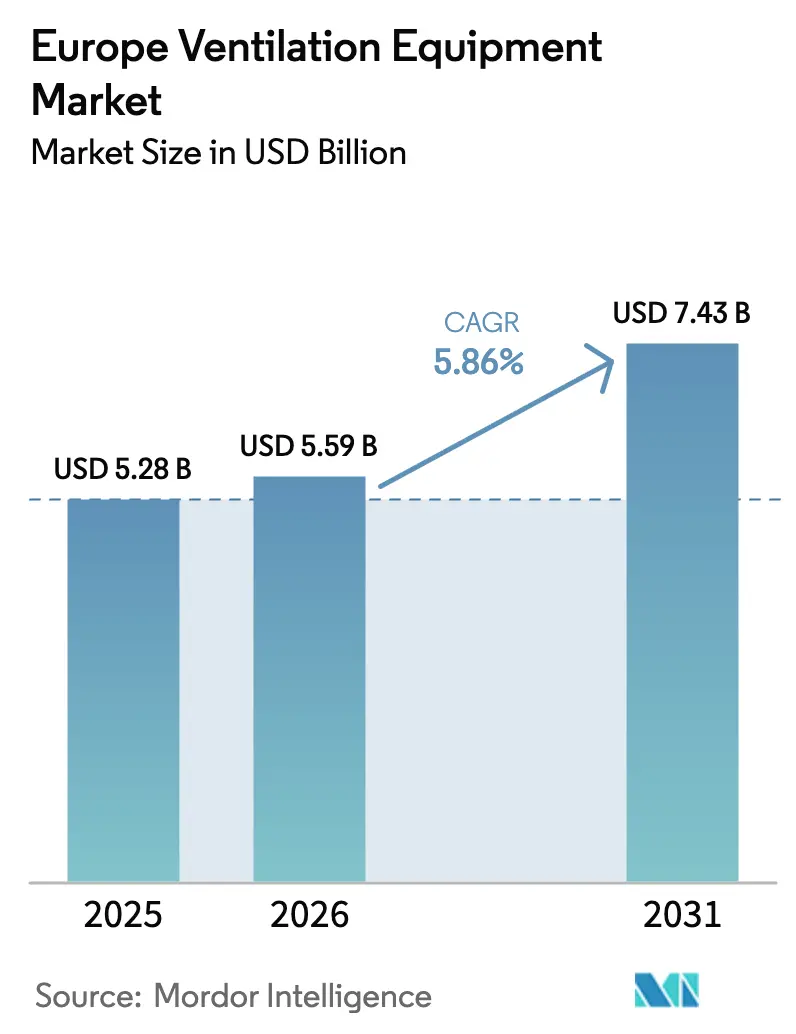

| Base Year Market Size (2025) | USD 5.28 Billion |

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.43 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

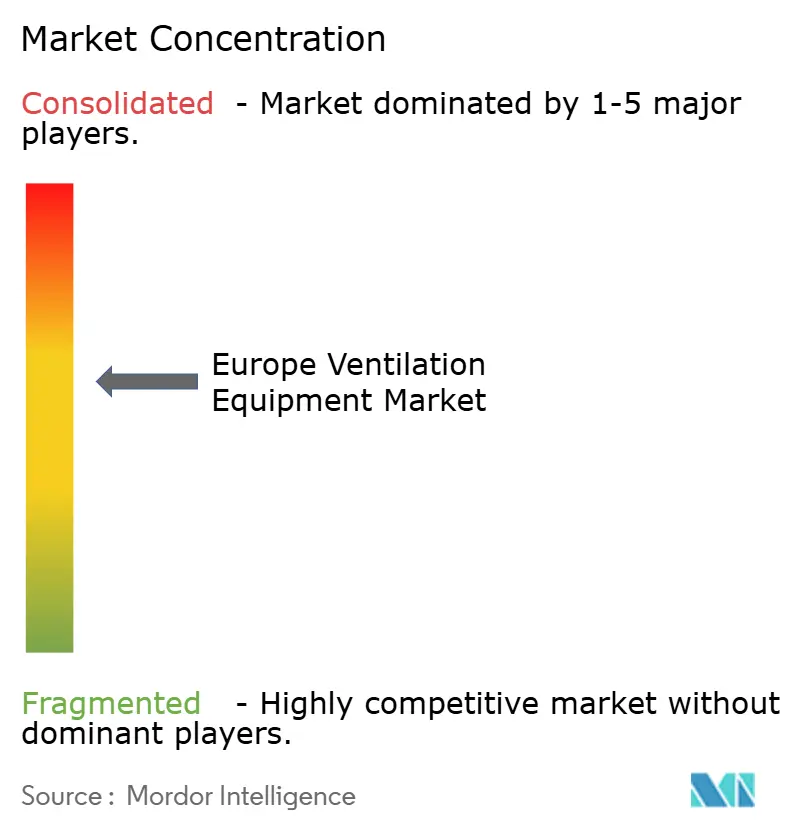

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ventilation Equipment Market Analysis by Mordor Intelligence

The Europe ventilation equipment market size is expected to grow from USD 5.28 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 7.43 billion by 2031 at 5.86% CAGR over 2026-2031. Demand is accelerating as the Energy Performance of Buildings Directive (EPBD) mandates require heat-recovery efficiencies of at least 75%, compelling a shift from extract-only systems to balanced heat-recovery ventilation. Post-pandemic indoor-air-quality targets, rapid social-housing retrofits, and data-center expansion are reinforcing procurement decisions, while installer shortages and raw-material volatility temper near-term growth. Market leaders are adding digital controls and predictive maintenance to differentiate, and hybrid mixed-mode designs are gaining traction as building owners balance energy use with occupant comfort. The European ventilation equipment market is therefore positioned for resilient mid-single-digit expansion despite supply-side headwinds.

Key Report Takeaways

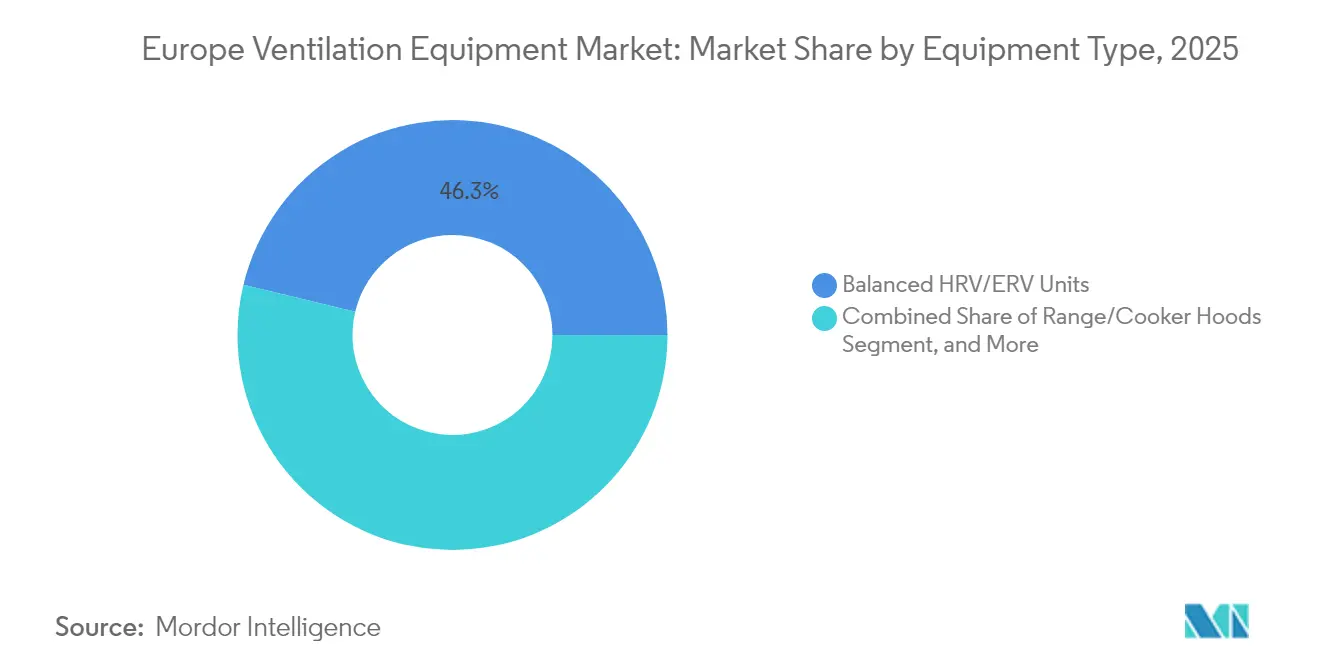

- By equipment type, balanced HRV/ERV units held 46.25% of the European ventilation equipment market share in 2025, while range/cooker hoods are forecast to grow at a 7.22% CAGR to 2031.

- By ventilation mechanism, centralized ducted systems commanded a 55.15% share of the European ventilation equipment market size in 2025; hybrid solutions are projected to expand at a 6.88% CAGR through 2031.

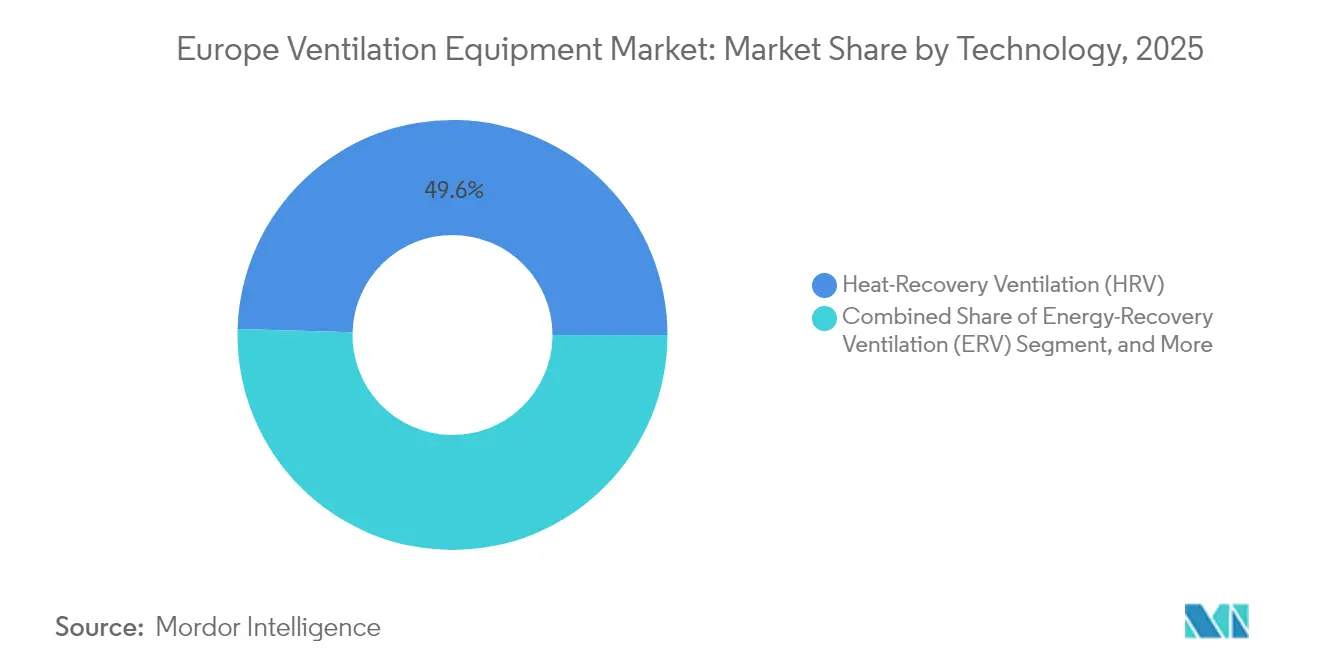

- By technology, HRV captured a 49.55% share of the European ventilation equipment market in 2025, and ERV is advancing at a 7.36% CAGR.

- By end-user, residential buildings accounted for 52.95% of the European ventilation equipment market size in 2025, yet industrial facilities led growth at a 7.31% CAGR.

- By application, living spaces dominated with a 46.12% share of the European ventilation equipment market in 2025; process/clean-room and data-center ventilation is expected to post the fastest 7.65% CAGR.

- By country, Germany led with a 30.85% share of the European ventilation equipment market in 2025, whereas Spain is projected to register the highest 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on ventilation equipment market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Ventilation Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EPBD-mandated energy-efficiency standards | +1.8% | EU-wide; strongest in Germany, Netherlands, France | Medium term (2-4 years) |

| Rapid retrofit wave for mould mitigation in social housing | +1.2% | UK, Ireland, Netherlands; spillover to Northern Europe | Short term (≤ 2 years) |

| Post-COVID focus on indoor air quality in workplaces | +1.0% | Germany, UK, Nordics | Medium term (2-4 years) |

| Electrification driving heat-recovery ventilation demand | +0.9% | Northern and Central Europe | Long term (≥ 4 years) |

| Shift to decentralized MVHR in renovation projects | +0.7% | Germany, Austria, Switzerland, France | Medium term (2-4 years) |

| Growing data-center cooling loads | +0.6% | Ireland, Netherlands, Germany, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening EPBD-Mandated Energy-Efficiency Standards

The revised EPBD requires nearly zero-energy buildings from 2030, obliging designers to specify mechanical ventilation with heat-recovery efficiencies ≥75%.[1]European Commission, “Directive (EU) 2024/1275 on the energy performance of buildings (recast),” Official Journal of the European Union, eur-lex.europa.eu Germany enforces the rule aggressively, with federal states mandating heat-recovery systems in multifamily projects exceeding four units. Renovation-wave provisions that target a 3% annual performance gain favor decentralized MVHR units, which avoid intrusive ductwork modifications. Compliance with EN 15251 and ISO 16814 supports uptake of balanced HRV/ERV equipment capable of documenting energy savings for regulatory reporting. As a result, the European ventilation equipment market is pivoting toward high-efficiency units across both residential and commercial segments.

Post-COVID Focus on Indoor Air Quality in Workplaces

Updated ECDC guidance raises minimum ventilation rates to 10 L/s-person, prompting capacity upgrades in existing offices.[2]European Centre for Disease Prevention and Control, “Heating, ventilation and air-conditioning systems in the context of COVID-19,” ecdc.europa.eu Large German employers such as SAP and Siemens have added variable-air-volume systems connected to occupancy sensors, valuing real-time air-quality data over pure energy metrics. IoT-integrated ventilation that reports particulate, CO₂, and humidity levels is becoming standard rather than premium. Suppliers that bundle analytics dashboards with equipment gain preference, reinforcing digitization across the European ventilation equipment market.

Electrification Driving Heat-Recovery Ventilation Demand

Northern European bans on fossil-fuel heating increase reliance on heat pumps, making heat-recovery ventilation essential to maintain coefficient-of-performance targets. Integrated HRV-heat-pump packages improve seasonal efficiency and flatten peak-load profiles, addressing grid constraints in Denmark, Ireland, and Sweden. Commercial buildings adopt the same logic, coupling ERV with large-capacity heat pumps to moderate winter electrical peaks. The European ventilation equipment market, therefore, benefits from electrification policies that favor energy-recovery solutions.

Rapid Retrofit Wave for Mould Mitigation in Social Housing

Awaab's Law obliges UK landlords to fix damp and mould within specific timelines, catalyzing a EUR 3.1 billion retrofit budget focused on positive-input and mechanical-extract solutions. Similar proposals in Ireland and the Netherlands widen demand for humidity-controlled units with auto-boost functions. Manufacturers offering easy-fit PIV products reduce tenant disruption and installation time, supporting fast deployment. This retrofit surge is accelerating cash cycles across the European ventilation equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified installers and commissioning engineers | -1.4% | Germany, Netherlands, UK | Medium term (2-4 years) |

| Volatile raw-material prices inflating fan/motor costs | -1.1% | All European markets | Short term (≤ 2 years) |

| Building-fabric fire-safety rules limiting duct layouts | -0.8% | UK, Ireland; spreading to EU | Long term (≥ 4 years) |

| Cross-draft risks in hybrid natural-mechanical designs | -0.5% | Southern Europe, Mediterranean | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Installers and Commissioning Engineers

The sector lacks roughly 40,000 qualified technicians, extending project schedules by eight weeks on average and raising installed costs by 25-30%.[3]Central Association of German Building Services (ZVSHK), “Skills Shortage Report 2024,” zvshk.de Germany experiences the deepest gap, but shortages are visible across Northern Europe. Complex HRV balancing and digital commissioning require specialist skills that current training pipelines cannot supply. Manufacturers respond with plug-and-play units and remote-commissioning apps, yet the constraint continues to moderate growth in the European ventilation equipment market.

Volatile Raw-Material Prices Inflating Fan/Motor Costs

Aluminum futures swung between USD 2,100-2,800 per metric ton in 2024, pushing the raw-material share of production cost to 50%. Repeated price adjustments compress margins and depress volume in price-sensitive residential retrofits. Makers such as FläktGroup hedge contracts and redesign housings to reduce metal content. While strategic inventory buffering absorbs shocks, volatility remains a short-term drag on the European ventilation equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: HRV/ERV Units Lead Market Transformation

Balanced HRV/ERV units accounted for 46.25% of the European ventilation equipment market size in 2025 as EPBD compliance drove adoption across construction and retrofit. Range/cooker hoods are projected to grow at a 7.22% CAGR, spurred by kitchen upgrades and expanding hospitality footprints.

Strong policy alignment means HRV/ERV will continue to anchor product mixes, with Daikin’s 2024 purchase of Robert Heath adding technical depth to its portfolio. Unidirectional fans remain indispensable for directional airflow in data centers, while supply/exhaust systems sustain industrial demand. These trends reinforce value migration toward energy-recovery technologies within the European ventilation equipment market.

By Ventilation Mechanism: Hybrid Solutions Gain Traction

Centralized ducted systems captured a 55.15% share of the European ventilation equipment market size in 2025, mainly in new commercial builds. Hybrid mixed-mode ventilation is set to expand at a 6.88% CAGR as building-management software optimizes between natural and mechanical modes under EN 16798 guidelines.

Operators prioritize flexibility; hybrid solutions cut energy use in mild seasons yet uphold IAQ during high occupancy. Decentralized units thrive in historic or social-housing retrofits where ducts are impractical. Together, these patterns diversify channel demand and support the sustained expansion of the European ventilation equipment market.

By Technology: ERV Systems Accelerate Market Growth

HRV held half of 2025 sales, but ERV is forecast to outpace at a 7.36% CAGR because latent-heat recovery suits humid process and data-center environments. ERV’s ability to manage moisture contrasts with HRV’s sensible-heat focus, widening its addressable base.

Data-center operators seek ±5% RH control under ISO 14644, pushing ERV uptake in hyperscale facilities. PIV excels in UK retrofits by relieving condensation, whereas MEV stays relevant for low-budget ventilation. Technology choices thereby segment the European ventilation equipment market by climate zone and application.

By End-User Industry: Industrial Facilities Drive Growth

Residential buildings represented 52.95% of the European ventilation equipment market size in 2025, owing to subsidy-backed retrofits. Industrial facilities, led by data centers, are projected to post a 7.31% CAGR to 2031 as hyperscale investments spread from Ireland to Germany.

Manufacturing plants integrate ventilation with occupational-safety sensors, while greenhouses require precise temperature and humidity for crop yield. This mix diversifies revenue streams and elevates the European ventilation equipment market beyond its traditional residential core.

By Application Area: Data Centers Drive Precision Ventilation Demand

Living and sleeping areas held a 46.12% share in 2025, reflecting the residential base. Process/clean-room and data-center ventilation will rise at 7.65% CAGR as operators demand ±1 °C temperature stability.

Edge-computing facilities in Spain and Italy adopt modular air-handling units with predictive-maintenance software, mirroring trends in pharmaceutical clean-rooms. These high-spec niches accelerate premiumization within the European ventilation equipment market.

Geography Analysis

Germany’s prominence stems from mature supply chains, strict energy legislation, and early heat-recovery adoption. Domestic firms refine products for 0.45 W/(m³/h) fan-power limits, then export high-efficiency units across the continent, reinforcing Germany’s 30.85% share. Persistent installer shortages, however, cap potential output and extend lead times.

Spain’s 7.88% projected CAGR reflects EU-funded renovation grants, updated CTE building code ventilation clauses, and attractive renewable-energy tariffs that pull hyperscale cloud operators to Madrid’s post-pandemic data hub corridor. Retrofits in dense urban housing and green-field industrial parks converge, establishing Spain as the fastest-growing node within the European ventilation equipment market.

France, Italy, and the United Kingdom post steady mid-single-digit growth. France’s RE2020 simulation requirement embeds mechanical ventilation into every new design. Italy’s modified Superbonus still funds envelope upgrades that trigger HRV installation, particularly in the North. The UK prioritizes mould-mitigation retrofits after Awaab’s Law, favoring PIV and MEV units that can be installed without decanting residents. Collectively, these markets sustain demand across a diversified European ventilation equipment market.

Competitive Landscape

The market displays moderate concentration; the top five suppliers hold roughly 45-50% of revenue. Systemair, Volution Group, and Daikin anchor the field with multi-brand portfolios, regional factories, and acquisition pipelines. Volution’s 2024 purchase of Fantech enlarged its Asia-Pacific channels and complemented its European range.[4]Volution Group plc, “Acquisition of Fantech Pty Ltd,” volutiongroupplc.com Daikin added UK-based Robert Heath to secure HRV expertise and social-housing contacts, strengthening its European ventilation position.

Digital capability differentiates offerings. Swegon’s AI-enabled GOLD air-handling series predicts component failures six months ahead, guarding uptime for data-center clients. TROX expands training centers to relieve the installer bottleneck and secures long-term service contracts. Manufacturers that embed IoT sensors, KNX interfaces, and machine-learning algorithms win bids in commercial and industrial tenders that value lifecycle visibility.

White-space opportunities persist for hybrid ventilation, edge-computing cooling, and plug-and-play retrofit units. Firms integrating natural-ventilation algorithms with motorized dampers target Mediterranean climates sensitive to cross-draft and energy costs. Materials engineers explore polymer heat-exchangers to reduce aluminum exposure. These innovation pathways sustain competition and encourage technical diversity across the European ventilation equipment market.

Europe Ventilation Equipment Industry Leaders

Systemair AB

Volution Group plc

Aldes Aéraulique S.A.

Daikin Industries Ltd.

Swegon AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The European Commission implements the final EPBD 2024 phase, requiring every new residential building to hit nearly zero-energy status with ≥75% heat-recovery mechanical ventilation, prompting immediate specification upgrades EU-wide.

- August 2025: Daikin completes the Robert Heath integration and launches the Daikin-Heath HRV range, targeting the EUR 2.8 billion UK social-housing retrofit segment.

- July 2025: Systemair reports full production at its expanded Boxberg facility, lifting European HRV output capacity by 35%.

- June 2025: The UK CMA issues new acquisition guidelines for ventilation deals above GBP 50 million, tightening consolidation pathways.

- May 2025: Spain’s Ministry of Housing allocates an additional EUR 1.2 billion in EU Next Generation funds for residential ventilation upgrades.

Europe Ventilation Equipment Market Report Scope

Ventilation refers to the process of replacing stale air with fresh air. Ventilation equipment helps to control the airflow in a building and expels a build-up of pollutants, bacteria, moisture, and unpleasant odors.

The Europe ventilation equipment market is segmented by type of equipment (supply/exhaust ventilation systems, balanced systems (heat recovery, and energy recovery units)), end user (residential, commercial/industrial), and country (Italy, United Kingdom, Germany, France, Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Supply/Exhaust Ventilation Systems |

| Balanced HRV/ERV Units |

| Unidirectional Fans (Axial, Centrifugal, Roof) |

| Range/Cooker Hoods |

| Centralised Ducted Systems |

| Decentralised Room Units |

| Hybrid (Mixed-Mode) Solutions |

| Heat-Recovery Ventilation (HRV) |

| Energy-Recovery Ventilation (ERV) |

| Positive-Input Ventilation (PIV) |

| Mechanical Extract Ventilation (MEV) |

| Residential Buildings |

| Commercial and Institutional Buildings |

| Industrial Facilities |

| Agriculture and Controlled-Environment |

| Living and Sleeping Spaces |

| Wet Rooms (Kitchens, Bathrooms) |

| Process/Clean-Room and Data Centres |

| Greenhouses and Livestock Housing |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Rest of Europe |

| By Equipment Type | Supply/Exhaust Ventilation Systems |

| Balanced HRV/ERV Units | |

| Unidirectional Fans (Axial, Centrifugal, Roof) | |

| Range/Cooker Hoods | |

| By Ventilation Mechanism | Centralised Ducted Systems |

| Decentralised Room Units | |

| Hybrid (Mixed-Mode) Solutions | |

| By Technology | Heat-Recovery Ventilation (HRV) |

| Energy-Recovery Ventilation (ERV) | |

| Positive-Input Ventilation (PIV) | |

| Mechanical Extract Ventilation (MEV) | |

| By End-User Industry | Residential Buildings |

| Commercial and Institutional Buildings | |

| Industrial Facilities | |

| Agriculture and Controlled-Environment | |

| By Application Area | Living and Sleeping Spaces |

| Wet Rooms (Kitchens, Bathrooms) | |

| Process/Clean-Room and Data Centres | |

| Greenhouses and Livestock Housing | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe ventilation equipment market in 2026?

The Europe ventilation equipment market size is USD 5.59 billion in 2026 with a projected rise to USD 7.43 billion by 2031.

Which segment leads by equipment type?

Balanced HRV/ERV units hold 46.25% of sales, the largest share across equipment categories.

Which country presents the fastest growth opportunity?

Spain is forecast to grow at a 7.88% CAGR owing to EU-funded renovation grants and expanding data-center construction.

What is the main growth driver through 2031?

Tightening EPBD efficiency mandates that require ?75% heat-recovery effectiveness are the primary growth catalyst.

Why are hybrid ventilation systems gaining popularity?

Building operators favor hybrid designs that switch between natural and mechanical modes to balance indoor-air-quality targets with lower energy use.

What competitive trend stands out in the market?

Vendors are integrating IoT-based predictive maintenance and building-automation compatibility to differentiate their ventilation equipment portfolios.

Page last updated on: