Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

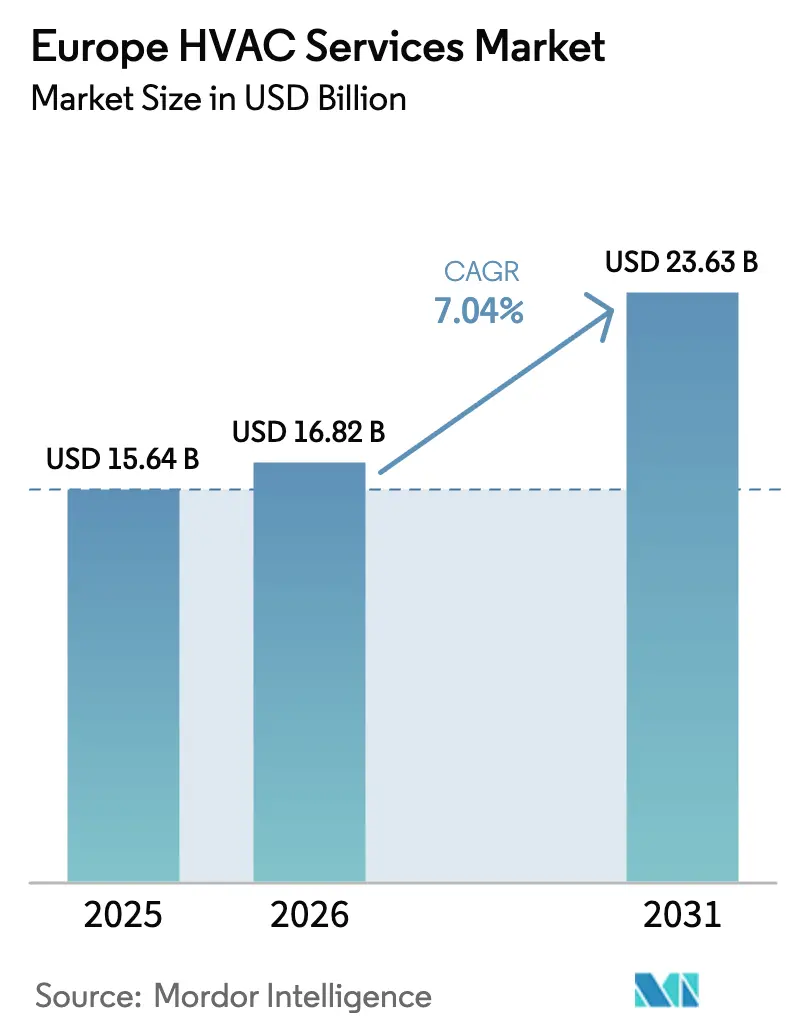

| Base Year Market Size (2025) | USD 15.64 Billion |

| Market Size (2026) | USD 16.82 Billion |

| Market Size (2031) | USD 23.63 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe HVAC Services Market Analysis by Mordor Intelligence

The Europe HVAC services market size is projected to be USD 15.64 billion in 2025, USD 16.82 billion in 2026, and reach USD 23.63 billion by 2031, growing at a CAGR of 7.04% from 2026 to 2031. Ambitious retrofit mandates, a heat-pump replacement boom, outcome-based contracting, and the expanding data-center footprint are redefining cash-flow visibility for the Europe HVAC services market. Service providers able to bundle installation, predictive maintenance, and energy-performance guarantees are defending margins as raw-material costs and wages rise. Electric-to-gas price spreads continue to favour electrification, while subsidy frameworks in Germany, France, and Poland shield homeowners from steep upfront outlays. At the same time, installer scarcity is inflating labour rates, prompting a pivot toward smart-connected operations that curb truck rolls by as much as 30%.

Key Report Takeaways

- By implementation type, retrofit buildings held 58.59% of the Europe HVAC services market share in 2025 and are advancing at a 7.84% CAGR through 2031.

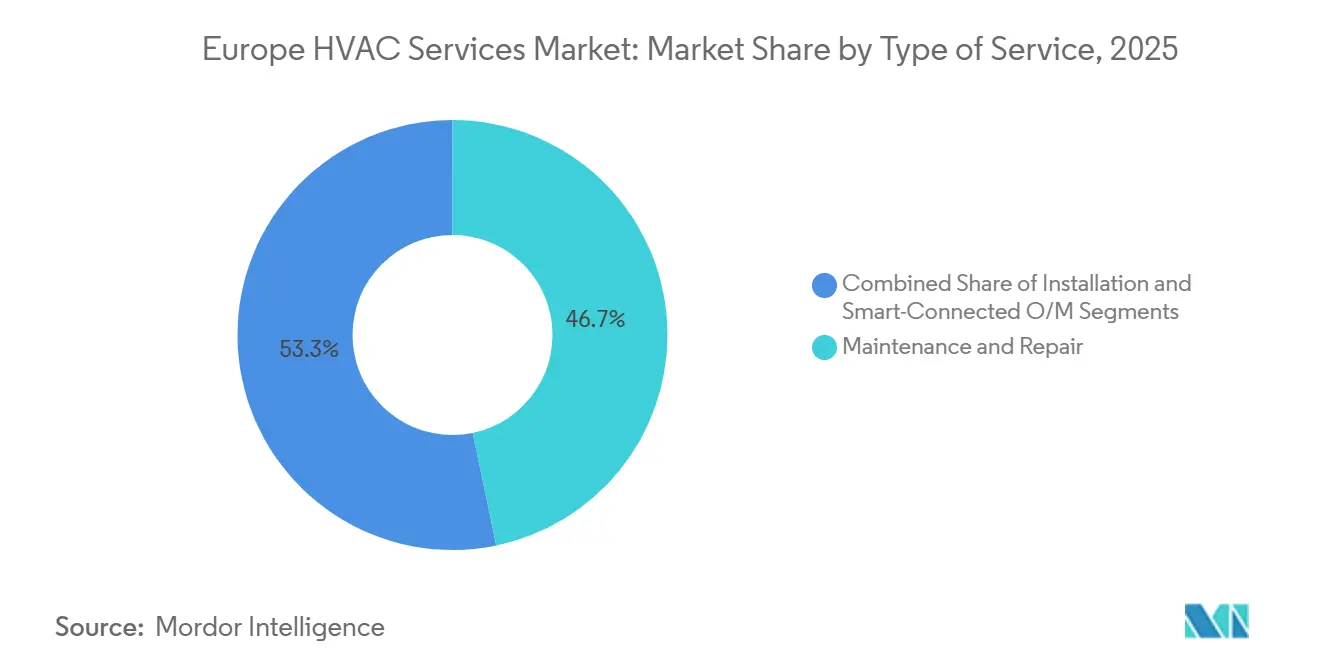

- By type of service, maintenance and repair led with 46.74% revenue share in 2025, whereas smart-connected operations and maintenance is expanding at a 7.39% CAGR to 2031.

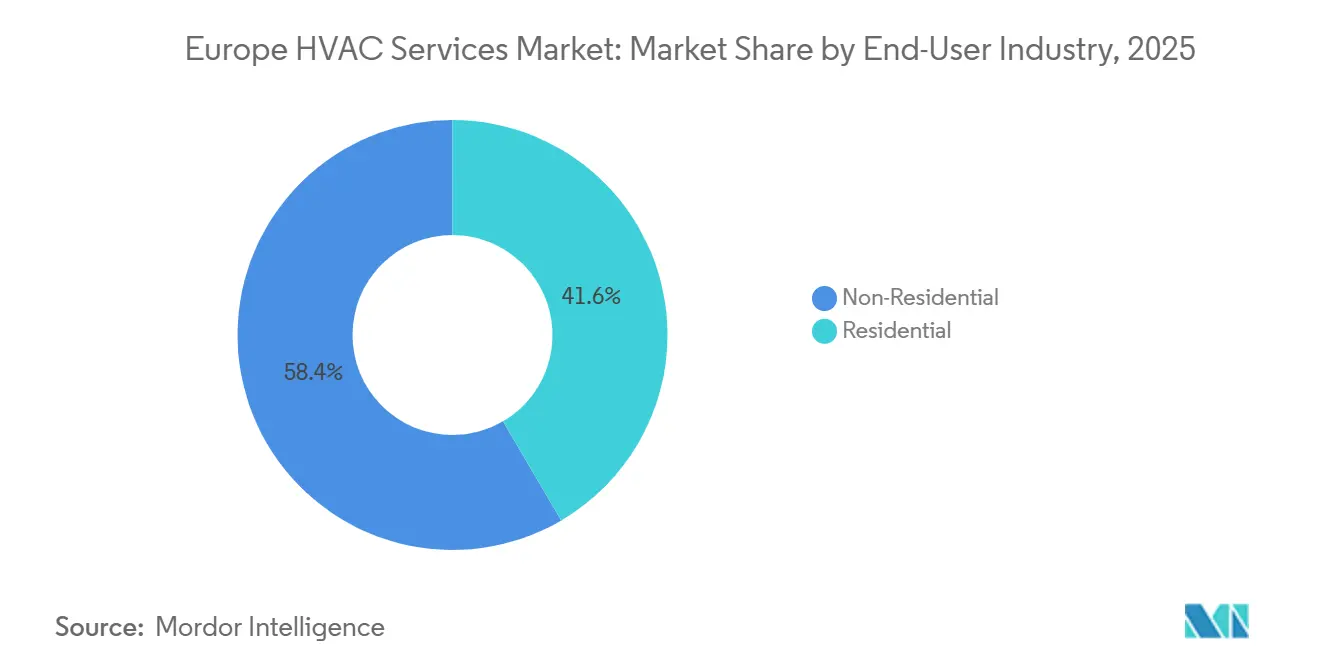

- By end-user industry, commercial facilities within the non-residential segment captured 7.63% CAGR growth, outpacing the residential segment’s 6.9% rate over 2026-2031.

- By service delivery model, heat-as-a-service contracting, although below 10% penetration in 2025, is projected to compound at 7.59% annually to 2031.

- By geography, Germany commanded 24.25% revenue in 2025, while Poland is forecast to post the fastest 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe HVAC Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave Mandates | +1.80% | Pan-European, with concentration in Germany, France, Netherlands | Medium term (2-4 years) |

| Heat-Pump Replacement Boom | +2.10% | Germany, France, Poland, Nordic region | Short term (≤ 2 years) |

| Growing Demand for Energy-Efficient Retrofits | +1.50% | Pan-European, led by Western Europe | Medium term (2-4 years) |

| Data-Center Cooling Demand Surge | +0.90% | Frankfurt, Amsterdam, Dublin, Paris, Stockholm | Short term (≤ 2 years) |

| Expansion of Heat-as-a-Service Contracting | +0.60% | Germany, UK, Netherlands, France | Long term (≥ 4 years) |

| Seasonal Thermal-Storage-Enabled Operations and Maintenance Revenue Streams | +0.40% | Nordic countries, Germany, Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Renovation Wave Mandates

The European Commission intends to renovate 35 million buildings by 2030, forcing upgrades that normally bundle envelope insulation, heat pumps, and smart controls.[1]European Commission, “Renovation Wave,” energy.ec.europa.eu Germany allocated USD 14.45 billion in 2024 to subsidize up to 70% of qualifying retrofit costs, and both France and the Netherlands run parallel grant schemes that link incentive payouts to five-year service contracts. Because roughly three-quarters of Europe’s stock predates 1990 efficiency codes, compliance guarantees a decade-long pipeline for the Europe heating, ventilation, and air conditioning services market. Eligibility rules favour certified installers, locking in recurring maintenance revenue. As subsidy budgets roll forward, service providers capable of delivering turnkey retrofits are positioned to capture premium margins.

Heat-Pump Replacement Boom

More than 356,000 units were installed in Germany during 2024, and millions of aging boilers across the bloc are entering end-of-life cycles.[2]McKinsey, “Heat Pumps: A Key Technology for Europe’s Energy Transition,” mckinsey.com Service intensity runs 40%–60% higher than gas-boiler swaps, lifting average ticket sizes for the Europe heating, ventilation, and air conditioning services market. Poland’s “My Heat” scheme alone directs USD 3.21 billion toward residential heat-pump adoption by 2026. Total cost-of-ownership models consistently favour electric systems whenever electricity-to-gas price ratios hold below four-to-one. Yet technician scarcity has pushed wait times to 16 weeks in Germany, nudging providers to invest in training and acquisition of smaller installers.

Growing Demand for Energy-Efficient Retrofits

Carbon-price exposure under the expanded EU Emissions Trading System will add USD 321–535 in annual heating costs for poorly insulated homes starting 2027.[3]European Commission, “EU Legislation to Control F-gases,” climate.ec.europa.eu Corporate landlords confront disclosure duties under the Corporate Sustainability Reporting Directive, accelerating HVAC-retrofit budgets across western capitals. Turnkey offerings that blend smart thermostats, insulation, and heat pumps command 25%–30% price premiums over equipment-only quotes, a pattern buoying profitability for the Europe heating, ventilation, and air conditioning services market. Buildings upgraded to high-efficiency classes capture 5%–8% rent premiums and double-digit sale premiums, ensuring durable retrofit demand.

Data-Center Cooling Demand Surge

European data-center capacity is on track to double by 2030, with each megawatt of IT load demanding up to 0.6 megawatts of cooling capacity. Liquid-cooling retrofits cost USD 500–1,200 per kilowatt but cut energy use by up to 40%, a value proposition that attracts hyperscalers willing to sign seven-year service contracts north of USD 200,000 per megawatt. Providers offering uptime guarantees of 99.99% plus waste-heat recovery integration are differentiating themselves within the Europe heating, ventilation, and air conditioning services market. Stockholm’s corridor showcases sub-1.15 power-usage-effectiveness ratios that hinge on sophisticated operations and maintenance programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of F-Gas-Certified Technicians | -1.20% | Pan-European, acute in Germany, France, UK | Short term (≤ 2 years) |

| High IoT Retrofit Costs for Legacy Systems | -0.70% | Southern and Eastern Europe | Medium term (2-4 years) |

| Compressor Supply-Chain Vulnerability Amid Heat-Pump Spike | -0.50% | Pan-European | Short term (≤ 2 years) |

| Data-Privacy Compliance Burdens on Remote Maintenance | -0.30% | Pan-European, especially Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of F-Gas-Certified Technicians

Europe maintains roughly 367,000 certified technicians, yet needs an additional 70,000–500,000 by 2030 to meet policy targets. Certification courses require up to 80 hours and cost USD 1,605–3,210 per trainee. Resulting labour scarcity inflates service-call fees to USD 192.60 in Germany, eroding margins for price-sensitive residential projects. The bottleneck particularly hampers retrofit timelines where complex integrations demand seasoned installers.

High IoT Retrofit Costs for Legacy Systems

Smart thermostat and sensor retrofits run USD 53.50–160.50 per square meter when legacy HVAC units lack modern communication protocols. Building owners in Southern and Eastern Europe, where energy prices remain lower, hesitate to commit capital unless payback periods fall under five years. GDPR compliance further elevates platform costs by up to 40% and exposes providers to heavy fines. Consequently, IoT uptake lags in nations such as Italy and Spain, tempering addressable volume for the Europe HVAC services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Service: Smart Platforms Redefine Maintenance Economics

Maintenance and repair represented 46.74% of revenue in 2025, anchored by an installed base exceeding 180 million HVAC units across the continent. Smart-connected operations and maintenance, however, is expanding at 7.39% to 2031 as machine-learning platforms forecast faults days in advance, cutting downtime by up to 35%. The segment’s shift toward predictive analytics elevates contract values from USD 85.60 to beyond USD 428 per unit annually. Installation services are still vital, growing at 7.2% thanks to heat-pump swaps and liquid-cooling overhauls. In Germany, the average truck-roll cost of USD 128.40 incentivizes remote diagnostics, bolstering margins. Online marketplaces are compressing installer prices by as much as 15% in residential channels, compelling providers to bundle ten-year warranties to protect revenue streams. Consequently, the Europe HVAC services market is tilting toward digitally enabled service models that monetize data rather than headcount.

Smart platforms also enable granular energy reporting, a requirement under multiple EU directives. Carrier’s Abound suite monitors 2 million connected units, scheduling maintenance during off-peak hours and reducing labour hours by 18%. Providers investing 4%–6% of revenue in digital twin’s report service-margin lifts of 200–300 basis points. Meanwhile, traditional maintenance businesses risk erosion unless they integrate IoT competencies. As subscription remote monitoring reaches critical mass, the Europe HVAC services market size for smart-connected contracts is poised to surpass conventional maintenance by the late 2020s.

By Implementation Type: Retrofit Dominance Driven by Mandate Intensity

Retrofit projects accounted for 58.59% of implementation revenue in 2025, and their 7.84% CAGR through 2031 outpaces new construction by 110 basis points. Deep-energy packages yield internal rates of return up to 9% when energy savings and avoided carbon taxes are considered. Each retrofit square meter generates 40%–60% more service revenue than new builds owing to surveys, asbestos mitigation, and legacy system integration. New construction, growing at 6.74%, benefits from heat pumps becoming the default heat source across Nordic markets, yet aggressive developer negotiations compress margins. Rising interest rates trimmed German housing starts by 18% in 2024, whereas retrofit permits climbed 27%. As a result, the retrofit share within the Europe HVAC services market will continue expanding throughout the forecast horizon.

Policy asymmetry reinforces this trend. The revised Energy Performance of Buildings Directive targets the worst 15% of stock, compelling landlords to act or risk asset devaluation. Subsidies tilt further toward retrofit depth, with German grants covering up to 70% of qualifying costs. Labor scarcity remains a wild card but also encourages digital oversight tools that reduce onsite time. Ultimately, the Europe HVAC services market size tied to retrofit activity is likely to dominate long term, particularly as carbon prices tighten.

By End-User Industry: Commercial Segment Leads on Precision Cooling

Residential customers delivered 41.57% of revenue in 2025, but commercial facilities are on a faster 7.63% growth trajectory as datacenter and office-to-lab conversions require sub-1 °C stability. Commercial contract values of USD 53,500–214,000 dwarf residential tickets and include service attachment rates above 90%. Industrial clients are adopting megawatt-scale heat pumps to offset carbon-border tariffs, while public institutions rely on performance contracts guaranteed to cut energy use by at least 20%. Nordic residential markets are nearing heat-pump saturation, capping household growth but opening replacement cycles rich in smart-services revenue. Given these dynamics, the commercial slice of the Europe HVAC services market will increasingly influence pricing discipline and technology roadmaps.

Incremental opportunity also lies in industrial process heating, where carbon compliance drives high-temperature heat-pump retrofits. Retail chains upgrading cold-chain logistics add another demand vector. Conversely, residential affordability constraints in Southern Europe temper volume, even after subsidies. Still, remote monitoring subscriptions are gaining traction, with British Gas bundling annual servicing for USD 15.36 per month and reaching 380,000 subscribers by mid-2025. As household budgets tighten, subscription models grant the Europe HVAC services industry a sticky revenue avenue.

By Service Delivery Model: Heat-as-a-Service Gains Traction

Conventional time-and-material agreements held 52.85% of service-delivery revenue in 2025, yet heat-as-a-service is staging the fastest rise at 7.59% through 2031. Utilities such as Vattenfall and Engie now charge USD 85.60–160.50 per month in contracts spanning up to 15 years, absorbing equipment risk while locking in customers. Performance-based energy contracts, prevalent in the commercial sector, post 7.3% CAGR growth by ensuring 15%–25% energy-savings guarantees. Subscription remote monitoring, at 7.1% growth, monetizes data from connected thermostats. Combined, these emerging models are shifting capital intensity away from building owners and embedding service providers deeper into client operations. That evolution multiplies the recurring-revenue share of the Europe HVAC services market.

Providers with balance-sheet strength are best placed to underwrite performance risks, further concentrating market power among top manufacturers and utilities. Smaller contractors mitigate exposure through partnerships or platform participation. As predictive analytics prove their worth in reducing emergency repairs, subscription adoption is likely to accelerate across the residential base. Over time, equipment commoditization will make service innovation, not hardware differentiation, the decisive factor in Europe HVAC services market share gains.

Geography Analysis

Germany generated 24.25% of regional revenue in 2025 on the strength of the Gebäudeenergiegesetz’s 65% renewable-heat mandate and USD 14.45 billion in subsidies. Installer shortages inflated lead times to 16 weeks, an issue expected to persist into 2027. Poland, supported by USD 3.21 billion in “My Heat” funding, is forecast to post the region’s quickest 7.88% CAGR, moving household heating away from coal. France led unit sales with more than 500,000 heat pumps installed in 2024 under MaPrimeRénov’, while the United Kingdom’s grants of USD 9,600 spurred 25,000 projects the same year. Italy’s scaled-back Superbonus slowed approvals by 35%, whereas Spain channels USD 7.28 billion from EU recovery funds into social-housing retrofits, favouring commercial and institutional contracts.

Rest-of-Europe markets, including the Nordics, Benelux, and Eastern Europe, delivered 27.75% of revenue. Norway and Sweden display heat-pump penetration above 60%, thereby pivoting demand toward replacement services and commercial retrofits. Irish and Dutch data-center clusters fuel precision-cooling contracts, complementing Frankfurt’s hyperscale corridor. Across geographies, retrofit depth and policy clarity remain the main differentiators shaping the trajectory of the Europe HVAC services market.

Differential subsidy generosity prompts cross-border installer migration, especially from Eastern to Western Europe, marginally alleviating labour tightness in Germany and France. However, language and certification barriers limit mobility. Meanwhile, energy-price volatility keeps payback economics favourable for electrification through 2031. Country-specific carbon taxes further compress fossil-fuel competitiveness. Collectively, these factors underpin a robust outlook for the Europe HVAC services market across the bloc.

Competitive Landscape

The top five players Johnson Controls, Carrier, Daikin, Trane Technologies, and Siemens collectively hold an estimated 35%–40% market share. Equipment manufacturers are vertically integrating, as shown by Carrier’s USD 12.84 billion Viessmann acquisition that added 13,000 technicians and 120 service centers. Utilities such as Vattenfall and Engie wield balance sheets to finance heat-as-a-service rollouts, capturing customers reluctant to fund USD 16,050–26,750 heat-pump installations. Technology investments are the leading differentiator: firms devote up to 6% of revenue to IoT platforms and digital twins, trimming service costs by up to 30% and lifting uptime.

Johnson Controls’ Silent-Aire acquisition bolstered data-center expertise, while Siemens linked building-management data with Microsoft Azure, delivering 22% energy savings in a Frankfurt pilot. Smaller specialists focus on compliance-intensive niches; Airedale International’s clean-room and data-center orientation earns 25%–35% price premiums. Online marketplaces such as Thermondo and Heatio compress residential pricing by unifying fragmented installer networks. Consequently, incumbents must match transparency and speed or cede share, especially in northern markets where digital readiness is high.

Strategic moves increasingly revolve around manufacturing footprints. Johnson Controls’ USD 128.4 million expansion in Poland targets 200,000 annual heat-pump units by 2027, positioning the firm near growth hot spots. Vaillant’s USD 74.9 million Remscheid plant doubled its European capacity, incorporating automated refrigerant charging that cuts defects 40%. Trane’s EUR 85 million ten-year Frankfurt data-center contract demonstrates the value of uptime guarantees that only deep-pocketed vendors can underwrite. Collectively, these moves reflect a race to secure recurring revenue in the Europe HVAC services market ahead of anticipated consolidation.

Europe HVAC Services Industry Leaders

Johnson Controls International plc

Carrier Corporation

Daikin Industries, Ltd.

Trane Technologies plc

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bosch completes its USD 8.1 billion takeover of the Johnson Controls-Hitachi JV, forming Europe’s largest residential and light-commercial service platform.

- July 2025: Thermondo secures EUR 50 million in debt financing to expand its digital heating installation services, covering more than 50,000 systems nationwide.

- June 2025: The European Commission enforces updated F-gas regulations, tightening technician-certification rules and labelling standards.

- May 2025: Vaillant launches a heat-pump range using natural refrigerant R290 alongside the ProjectPORTAL installer platform at ISH 2025.

Europe HVAC Services Market Report Scope

The Europe HVAC Services Market Report is Segmented by Type of Service (Maintenance and Repair, Installation, Smart-Connected Operations and Maintenance), Implementation Type (New Construction, Retrofit Buildings), End-User Industry (Residential, Non-Residential including Commercial, Industrial, Public and Institutional), Service Delivery Model (Conventional Time-and-Material Contracts, Performance-Based Energy Contracts, Heat-as-a-Service Contracting, Subscription Remote Monitoring), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Type of Service

| Maintenance and Repair |

| Installation |

| Smart-Connected O&M |

By Implementation Type

| New Construction |

| Retrofit Buildings |

By End-User Industry

| Residential | |

| Non-Residential | Commercial |

| Industrial | |

| Public and Institutional |

By Service Delivery Model

| Conventional Time-and-Material Contracts |

| Performance-Based Energy Contracts |

| Heat-as-a-Service Contracting |

| Subscription Remote Monitoring |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type of Service | Maintenance and Repair | |

| Installation | ||

| Smart-Connected O&M | ||

| By Implementation Type | New Construction | |

| Retrofit Buildings | ||

| By End-User Industry | Residential | |

| Non-Residential | Commercial | |

| Industrial | ||

| Public and Institutional | ||

| By Service Delivery Model | Conventional Time-and-Material Contracts | |

| Performance-Based Energy Contracts | ||

| Heat-as-a-Service Contracting | ||

| Subscription Remote Monitoring | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the forecast value of the Europe HVAC services market by 2031?

The Europe HVAC services market is projected to reach USD 23.63 billion by 2031.

Which implementation type is expanding fastest across Europe?

Retrofit buildings are growing the quickest, advancing at a 7.84% CAGR through 2031.

Why are data centers significant for service providers in Europe?

Hyperscale and colocation facilities demand liquid-cooling retrofits and multi-year uptime guarantees, driving high-value operations and maintenance contracts.

How is heat-as-a-service changing contracting models?

Heat-as-a-service shifts upfront equipment costs and performance risk to providers, generating predictable monthly fees over 1015 years.

What limits heat-pump deployment despite strong policy support?

A shortage of F-gas-certified technicians extends installation lead times and raises labor costs, constraining near-term growth.

Which country is expected to record the highest growth rate through 2031?

Poland is set to expand at a 7.88% CAGR, aided by substantial national subsidies for residential heat-pump adoption.

Page last updated on: