Germany Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 35.97 Billion |

| Market Size (2026) | USD 37.71 Billion |

| Market Size (2031) | USD 47.22 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

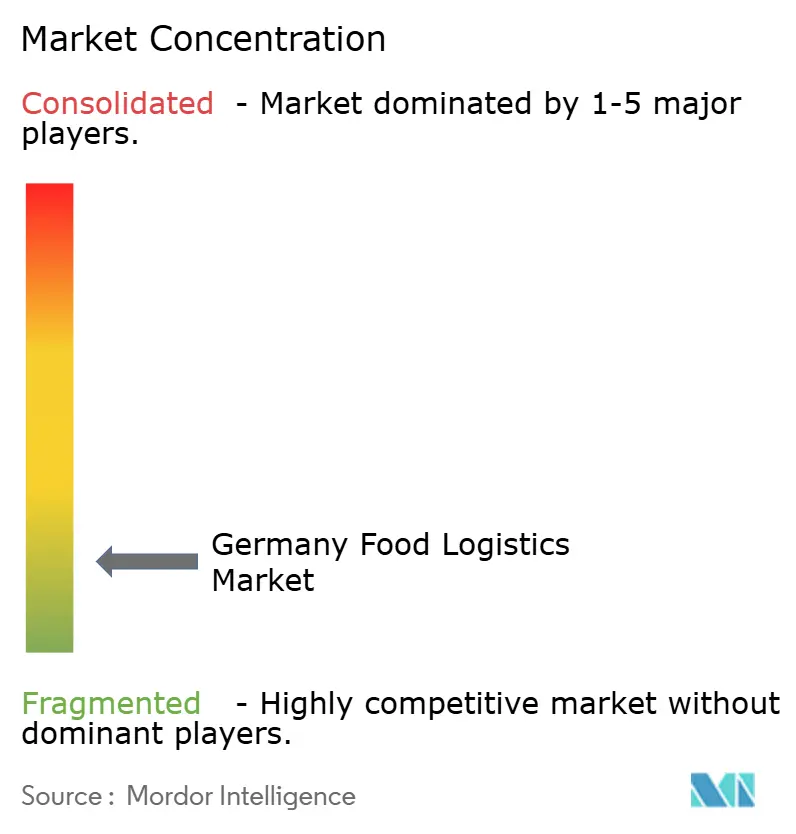

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Food Logistics Market Analysis by Mordor Intelligence

The Germany Food Logistics Market size was valued at USD 35.97 billion in 2025 and is estimated to grow from USD 37.71 billion in 2026 to reach USD 47.22 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

Expansion in online grocery and sustained discount-channel power continue to lift cold-chain volumes, while value-added services inside temperature-controlled facilities gain traction as retailers streamline in-store labor and seek flexibility for private-label runs. Capacity headwinds from driver scarcity and higher energy inputs temper growth, although toll relief for zero-emission trucks and digitized quality systems encourage long-horizon investments in fleet and infrastructure. Compliance costs around HACCP and IFS Logistics Version 3 concentrate share with larger, well-capitalized operators that can support 24/7 temperature monitoring and audit readiness as procurement standards tighten. The Supply Chain Act and Corporate Sustainability Reporting Directive further standardize expectations around human-rights diligence and Scope 3 emissions, which strengthens data-led collaboration between shippers and carriers in the Germany food logistics market.

Key Report Takeaways

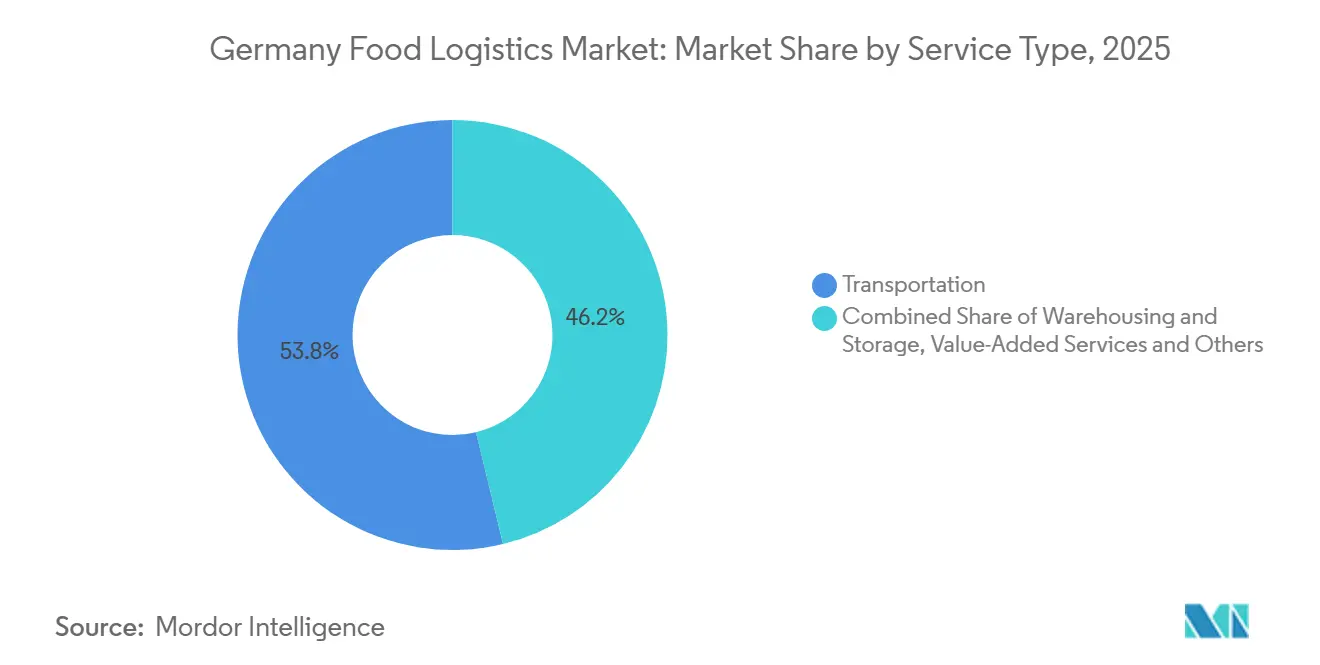

- By services, transportation led with 53.78% of the Germany food logistics market share in 2025, while value-added services are projected to grow at a 5.64% CAGR to 2031.

- By temperature-control type, cold chain accounted for 78.67% of the Germany food logistics market size in 2025 and is forecast to expand at a 6.21% CAGR through 2031.

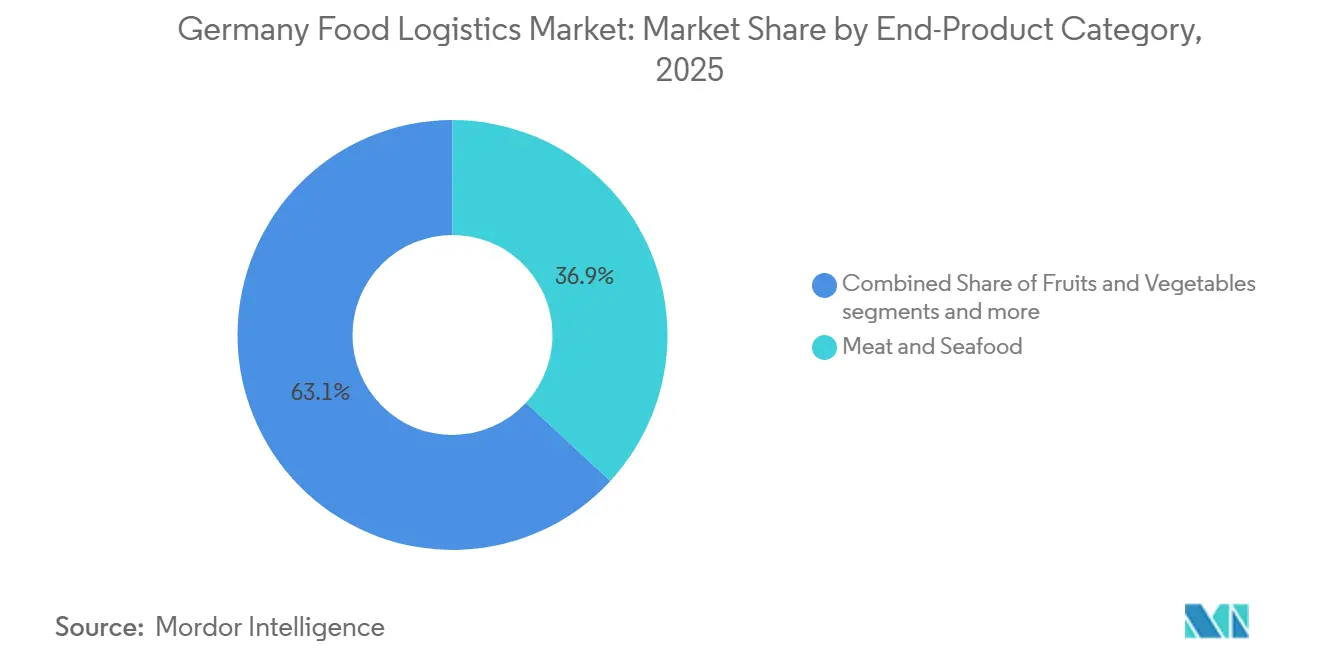

- By end-product, meat and seafood held 36.87% revenue share in 2025, while dairy and frozen desserts recorded the fastest projected CAGR at 6.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Online Grocery and Food Delivery Expansion | +1.2% | National, with early gains in Berlin, Munich, Hamburg, Rhine-Ruhr metropolitan regions | Medium term (2-4 years) |

| Discount Retailer Dominance | +0.9% | National, strongest in ex-industrial regions where price sensitivity is high | Long term (≥ 4 years) |

| Cold Chain Infrastructure Modernization | +0.8% | National core, spill-over to cross-border EU corridors via the Rhine-Danube axis. | Medium term (2-4 years) |

| Sustainability and Green Logistics Mandates | +0.7% | EU-wide, with German federal enforcement, urban low-emission zones in multiple cities | Long term (≥ 4 years) |

| Central European Distribution Hub Position | +0.6% | Trans-European, leverages A2, A3, A5 motorways and core intermodal nodes | Long term (≥ 4 years) |

| Convenience Food and Ready-Meals Growth | +0.4% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Online Grocery and Food Delivery Expansion

Food e-commerce reached an estimated 4.3% share of German grocery revenues in 2025, which sustained higher cold-chain utilization and more frequent, smaller drops to urban nodes. Retailers favor hybrid fulfillment that combines store-based picking and centralized micro-hubs, which improves asset turns and reduces spoilage in time-sensitive categories. Route-based home delivery models rely on predictable order densities and minimum-basket policies to protect unit economics, which encourages the use of scheduled slots and dynamic pricing. The shift to planned weekly baskets supports higher vehicle utilization and steadier refrigerated-lane flows across cities with dense catchment zones. These dynamics reinforce a multi-temperature footprint inside metropolitan distribution networks, which strengthens demand for integrated chilled and frozen capacity in the Germany food logistics market.[1] Foreign Agricultural Service, “Retail Foods Annual,” U.S. Department of Agriculture, usda.gov

Discount Retailer Dominance

The discount channel set the tone on price and assortment as private-label penetration deepened and value formats expanded their distribution footprints, which shaped replenishment patterns for staples and convenience items. Aldi Nord’s new Lehrte-Aligse logistics center, opened in late 2024, illustrates the scale of single-site throughput and the emphasis on fresh categories that require reliable cold storage and dock-door planning. Larger catchment areas and high pallet turns allow discounters to negotiate tighter delivery windows and consistent temperature controls, which lifts baseline service obligations for carriers. Premiumization within private labels adds packaging and kitting tasks that often shift to logistics partners, which creates growth for value-added operations linked to discount supply chains. These effects elevate the role of multi-temperature distribution and co-packing inside the Germany food logistics market as discounters seek efficiency with reliable freshness.

Cold Chain Infrastructure Modernization

Compliance and energy objectives are reshaping facility designs, equipment choices, and digital controls across chilled and frozen networks. IFS Logistics Version 3 tightened temperature-monitoring and traceability requirements that now push providers to deploy continuous sensors, automated alerts, and documented corrective actions that stand up to audits. Operators with the capital to combine multi-zone storage, solar generation, and charging bays are building resilience into cold-chain operations while managing the total cost of ownership. FIEGE’s plan for a 55,000-square-meter multi-user site with a 6,500-kilowatt-peak rooftop solar array shows how power self-sufficiency supports temperature stability and cost control inside modern food logistics. Hamburg and other major cities are also seeing low-emission distribution pilots with e-trucks in food delivery routes, which points to a gradual modernization path that begins at the last mile. Together, these moves reinforce the premium positioning of cold chain within the Germany food logistics market.

Sustainability and Green Logistics Mandates

Toll exemptions and fee reductions for zero-emission trucks remain a central lever for fleet transition plans, which improves the payback outlook for vehicles operating predictable urban routes. Logistics providers have begun to combine on-site generation, battery storage, and controlled charging to manage grid constraints and to support refrigerated bodies on e-trucks during dwell time. The Supply Chain Act and CSRD require more granular environmental and social disclosures, which drives shipper requests for carbon accounting at the shipment level and raises the value of telematics across temperature-controlled fleets. These mandates tend to favor larger carriers with the scale to integrate data systems and to fund new assets, although subcontracted regional specialists still play targeted roles inside dense urban rings. The result is a measured, compliance-led transition that supports service quality while advancing decarbonization in the Germany food logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Driver Shortage Crisis | -1.3% | National, with Eastern Germany experiencing lower wages that affect recruitment | Short term (≤ 2 years) |

| High Energy and Operational Costs | -0.9% | National, strongest in energy-intensive food-processing clusters | Medium term (2-4 years) |

| Stringent Regulatory Compliance | -0.6% | EU-wide with federal enforcement and audits | Long term (≥ 4 years) |

| Limited Urban Logistics Space | -0.5% | Berlin, Munich, and Hamburg city cores with scarce loading capacity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Driver Shortage Crisis

Germany faces an acute driver deficit that strains fleet utilization and delivery reliability, with industry and media reports pointing to persistent gaps as retirements outpace new entrants through the decade. Wage differentials between western and eastern regions complicate recruitment and retention, while training timelines and insurance requirements limit the speed at which licensing reforms can improve availability. Carriers respond with higher pay, bonuses, and route redesign, but staffing imbalances still trigger rejected tenders and missed store windows during seasonal peaks for perishables. Autonomous driving remains a long-horizon option as human handling, custody transfer, and security roles cannot be replaced in current operating models. This constraint keeps short-term pressure on capacity and costs in the Germany food logistics market until new entrants and selective automation ease the shortage.

High Energy and Operational Costs

Volatile fuel prices and CO2-linked road charges elevate operating costs, which compress margins for carriers with older diesel fleets and limited bargaining power. At EUR 2 per liter (USD 2.16 per liter), diesel inputs widen the monthly cost gap versus e-trucks by over EUR 1,700 (USD 1,901) per vehicle in some estimates, although the upfront cost of electrified tractors still doubles the purchase outlay for many operators. Food processors also face energy burdens, with sector leaders warning of sustained electricity and process-heat costs that threaten competitiveness in energy-intensive subsectors. Producer price data pointed to declines in late 2025 for distributed gas and electricity, but these shifts did not fully offset structural disadvantages relative to lower-cost neighboring markets. Combined with labor and compliance costs, these pressures curb near-term expansion in the Germany food logistics market until energy dynamics and equipment costs stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Transportation Anchors Operations, Value-Added Gains Traction

Transportation services accounted for 53.78% of revenues in 2025 as the dominant activity set, supported by dense regional flows for perishable foods and fast-moving staples across national corridors and urban catchments. Within road transport, short- to medium-haul routes underpin just-in-time replenishment for chilled and frozen items, which keeps trailer utilization and dock turns central to network performance in the Germany food logistics market. Warehousing continues to scale around multi-temperature zones and urban micro-fulfillment nodes, with operators aligning inventory placement to peak-day order profiles in major cities. Rail is regaining relevance for upstream ingredients and packaging, as seen in a 2026 contract that added more than 1,000 trains per year to connect industrial sites and reduce emissions versus road. Value-added services, including labeling, kitting, and cleanroom repacking, are projected to expand at a 5.64% CAGR to 2031, which reflects the need to localize private labels, manage promotions, and reduce store labor through pre-assembled units inside cold-chain facilities.

Scale and compliance are pivotal advantages in the Germany food logistics industry as IFS Logistics Version 3 demands always-on temperature logging, documented cleaning cycles, and mass-balance traceability that require integrated systems across sites and fleets. Strategic moves continue to strengthen national groupage and specialty routes, evidenced by a 2026 acquisition that integrated more than 100 logistics specialists and a fleet footprint into a broader European network. These network and capability upgrades lift the service floor for food shippers that depend on reliable dock appointments and shelf-life assurance. As value-added share rises, operators are embedding HACCP-compliant workflows in temperature-controlled spaces to support customization at scale while preserving audit readiness, which further differentiates full-service providers inside the Germany food logistics market.

By Temperature-Control Type: Cold Chain Supremacy Reflects Perishability Premium

Cold chain captured 78.67% of market value in 2025 and is projected to grow at a 6.21% CAGR to 2031, supported by higher service intensity per pallet and continued consumer interest in chilled and frozen convenience foods. Frozen corridors handle meat, seafood, and desserts at sub-zero temperatures, while a fast-growing chilled band supports dairy and fresh-prepared categories that require 2-8°C stability and short lead times. The Germany food logistics market share tied to cold chain reflects the perishable premium, where tariffs run higher than ambient due to energy, equipment, and liability exposures under HACCP standards. Multi-zone facilities and tri-temperature trailers have become critical to consolidate loads and balance demand volatility across frozen, chilled, and ambient-protected flows. This design enables steady slotting and allocation for weekly peaks that accompany online baskets and promotional events in urban markets.

Ambient-protected flows remain an essential complement within the Germany food logistics market for confectionery, bakery, and climate-sensitive items that do not need active refrigeration but still require temperature and humidity controls. Advanced monitoring and tight handoffs reduce spoilage risk during summer heat waves and multi-day transfers. Compliance obligations in IFS Logistics Version 3, including automated exception handling and corrective-action records, further raise the bar for operators serving premium chocolates and other sensitive SKUs. With retailers investing in private-label chilled lines and meal kits, value accrues to providers that combine precise temperature management with late-stage customization. This blend of capability supports a sustained cold-chain premium inside the Germany food logistics market as consumption patterns stabilize around ready-to-cook and ready-to-heat formats.

By End-product Category: Meat Commands Share, Dairy Drives Velocity

Meat and seafood held 36.87% of category revenues in 2025, which confirms the continued scale of frozen and chilled proteins in national distribution. This category relies on deep-frozen lanes and consistent service levels to manage seasonal peaks, import entries through major ports, and quality gates that protect shelf life at retail. Dairy and frozen desserts are the fastest-growing segments at a 6.74% CAGR to 2031, supported by premium SKUs and continuous innovation in chilled formats that encourage basket upgrades. Fresh produce flows demand responsive routing and surge capacity during harvest windows, which complicates asset planning for carriers and raises the value of accurate forecasting. These operating realities drive greater use of analytics to align orders with distribution windows in the Germany food logistics market.

Regulatory requirements vary by category, with meat and seafood subject to strict veterinary checks, dairy governed by lot-level traceability under EU food law, and produce tied to phytosanitary certificates in cross-border flows. As retailers expand private-label chilled assortments, value migrates to providers that can execute allergen segregation, controlled repacking, and accurate labeling inside HACCP-compliant zones. Technology adoption in ordering and replenishment reduces spoilage and improves on-shelf availability, which benefits temperature-controlled carriers through steadier order patterns and fewer emergency runs. These combined shifts support higher service complexity within the Germany food logistics industry, where the largest categories maintain volume while fast-growing chilled lines add value density to outbound operations.

Geography Analysis

Regional demand in the Germany food logistics market follows population concentration and retail footprints, with the Rhine-Ruhr metropolitan region generating high throughput due to dense urban clusters and established discount networks that require frequent replenishment. Southern states, including Bavaria and Baden-Württemberg, anchor premium-food distribution with links to Italy and Switzerland, which lifts cold-chain exposure tied to fresh and specialty items. Berlin-Brandenburg has accelerated e-commerce fulfillment investment as retailers respond to rising population density and closer-to-consumer expectations in the east. Hamburg’s role as an entry point for seafood and tropical goods supports last-mile pilots with zero-emission trucks in downtown zones, which aligns infrastructure decisions with city-level climate targets.

Germany captured the largest share of European food-logistics revenues in 2025, while growth within the Germany food logistics market is guided by disciplined expansion in cold-chain capacity and the speed of labor-market normalization. Cross-border trade patterns connect Polish and Czech production to western consumption centers, which drives balanced east-west flows for staples and inputs. Water-level variability on the Rhine can disrupt inland barge traffic, which forces modal shifts to road and rail and tests service continuity for scheduled replenishment. Rail maintenance on core lines and intermittent congestion at sea gateways also shape routing decisions, which puts a premium on carriers with multimodal options and contingency plans.

Policy signals matter at the state and federal levels, especially where low-emission zones and urban logistics planning dictate vehicle types and terminal access inside city limits. Toll relief for zero-emission fleets assists pilot programs in dense corridors and creates a rationale for charging infrastructure at regional depots serving grocery networks. At the national level, the Supply Chain Act and HACCP enforcement continue to standardize compliance demands that favor operators with integrated quality systems and audit-ready documentation. These geographic and policy elements, together with retailer network strategies, define how the Germany food logistics market balances service levels, cost, and decarbonization goals through 2031.

Competitive Landscape

The Germany food logistics market remains fragmented overall, although compliance requirements, capital intensity, and sustainability investments are gradually consolidating share among larger, well-capitalized operators. The market features global integrators, mid-sized temperature specialists, and regional subcontractors that together deliver national coverage with varying service intensity. Global leaders deploy scale, digital tools, and compliance resources to meet audit and sustainability requirements tied to HACCP and CSRD. Temperature-focused groups leverage long-standing customer relationships and multi-zone facilities to protect freshness and reduce spoilage for chilled and frozen categories. Urban coverage is supported by regional fleets that operate on short radii and higher drop frequencies, which remain central to store delivery and last-mile e-grocery.

Consolidation and capability-building continue to shape strategy. In 2026, an acquisition integrated a regional road-logistics specialist and its fleet into a broader European groupage network to enhance coverage and density in Germany. Retailers are also investing upstream in forecasting and replenishment systems that stabilize orders and reduce waste in fresh categories, which changes tender expectations for responsiveness and data-sharing. Facility investments that combine temperature zones with on-site energy generation demonstrate how operators are aligning cost control with environmental targets in preparation for tighter reporting standards under CSRD.

Decarbonization pilots are expanding in delivery routes and regional transfers. A leading operator deployed its 100th fully electric truck for food distribution in Hamburg in early 2026, supported by photovoltaic systems, battery storage, and managed charging at e-mobility hubs.[2]DACHSER Corporate Communications, “Dachser’s 100th Fully Electric Truck Enters Service,” DACHSER, mynewsdesk.com Rail partnerships for upstream moves aim to reduce emissions and diversify away from road on non-urgent legs, complementing last-mile electrification and supporting compliance with customer carbon-accounting requests. These strategic shifts reinforce the service differentiation in the Germany food logistics market, where the ability to pair temperature integrity with reliable delivery and lower carbon footprints is becoming a primary selection criterion.

Germany Food Logistics Industry Leaders

Nagel-Group

DHL Group

Pfenning group

Metro Logistics

Meyer Logistik

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: METRO partnered with RELEX Solutions and Accenture to roll out AI-enabled forecasting and replenishment across 540 stores and 70 distribution centers, aiming to improve availability and cut fresh-food waste in core markets, including Germany.

- January 2026: Novelis signed a strategic rail logistics contract with LINEAS to run more than 1,000 freight trains annually across its European footprint, with the company’s Göttingen site serving as the central rail hub and an expected 78% emissions reduction versus road for the covered flows.

- January 2026: DACHSER deployed its 100th fully electric truck into Hamburg food logistics distribution, supported by on-site solar generation, battery storage, and intelligent charging at designated e-mobility facilities.

Germany Food Logistics Market Report Scope

The Germany Food Logistics Market Report is Segmented by Services (Transportation, Warehousing, Value-Added Services, and Others), by Temperature-Control Type (Cold Chain and Non-Cold Chain), by End-product Category (Meat & Seafood, Dairy & Frozen Desserts, Fruits & Vegetables, Food and Beverages, and Others), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Transportation | Road |

| Rail | |

| Water | |

| Air | |

| Warehousing | |

| Value-Added Services and Others |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | |

| Frozen (Less than 0 °C) | |

| Non-Cold Chain |

| Meat & Seafood |

| Dairy & Frozen Desserts |

| Fruits & Vegetables |

| Food and Beverages |

| Others |

| By Services | Transportation | Road |

| Rail | ||

| Water | ||

| Air | ||

| Warehousing | ||

| Value-Added Services and Others | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2–8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non-Cold Chain | ||

| By End-product Category | Meat & Seafood | |

| Dairy & Frozen Desserts | ||

| Fruits & Vegetables | ||

| Food and Beverages | ||

| Others | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the Germany food logistics market?

The Germany food logistics market size was USD 35.97 billion in 2025, rising to USD 37.71 billion in 2026 and USD 47.22 billion by 2031 at a 4.6% CAGR over 2026-2031.

Which service segments are leading and growing fastest in Germany’s food logistics?

Transportation led with 53.78% revenue share in 2025, while value-added services such as kitting and labeling are projected to grow at a 5.64% CAGR through 2031.

How dominant is cold chain within the Germany food logistics market?

Cold chain accounted for 78.67% of value in 2025 and is forecast to expand at a 6.21% CAGR to 2031, reflecting a premium for temperature assurance and the rise of chilled and frozen convenience foods.

What categories drive the most volume and growth in Germany’s food logistics?

Meat and seafood held 36.87% revenue share in 2025 by volume importance, while dairy and frozen desserts are the fastest-growing at a 6.74% CAGR due to premiumization and chilled-aisle innovation.

What are the main constraints holding back faster growth in Germany’s food logistics?

Driver shortages and higher energy and operating costs are the main brakes, while compliance expectations and limited urban space add pressure; toll relief for zero-emission trucks and quality system investments help offset some of these constraints.

Where are retailers and logistics providers investing to improve performance?

Investments focus on AI-enabled forecasting and replenishment, multi-zone temperature facilities with on-site solar, and early e-truck deployments in urban routes to lift availability, reduce waste, and decarbonize last-mile delivery.

Page last updated on: