Germany Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

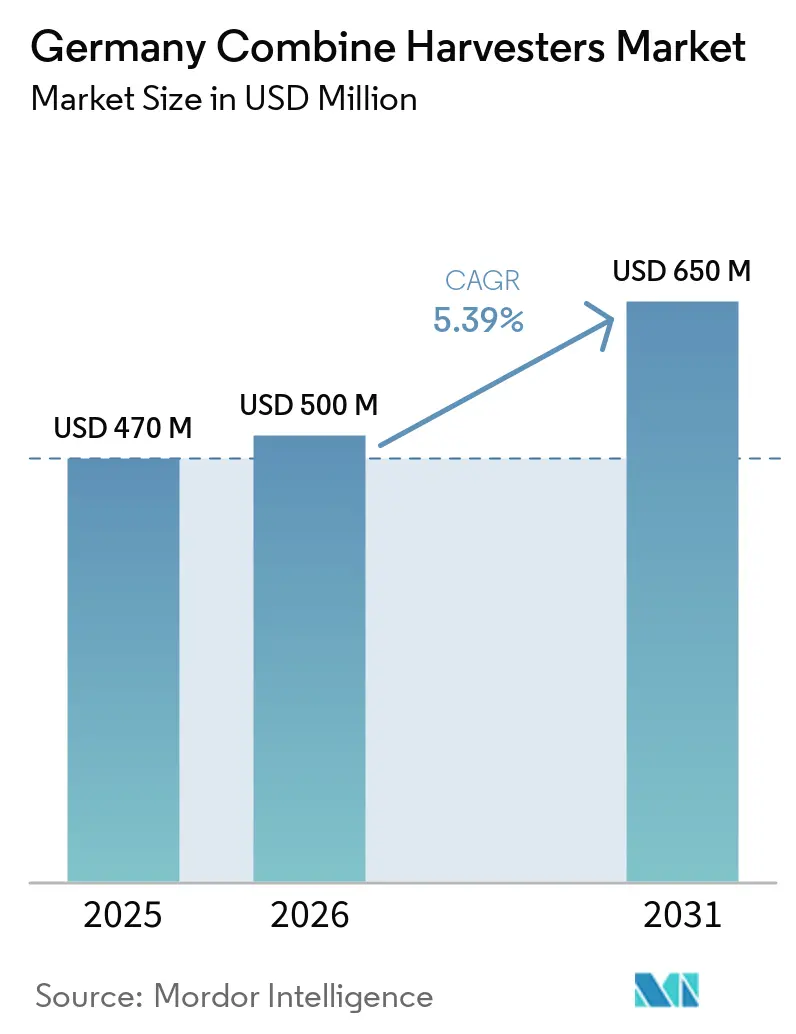

| Base Year Market Size (2025) | USD 470 Million |

| Market Size (2026) | USD 500 Million |

| Market Size (2031) | USD 650 Million |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

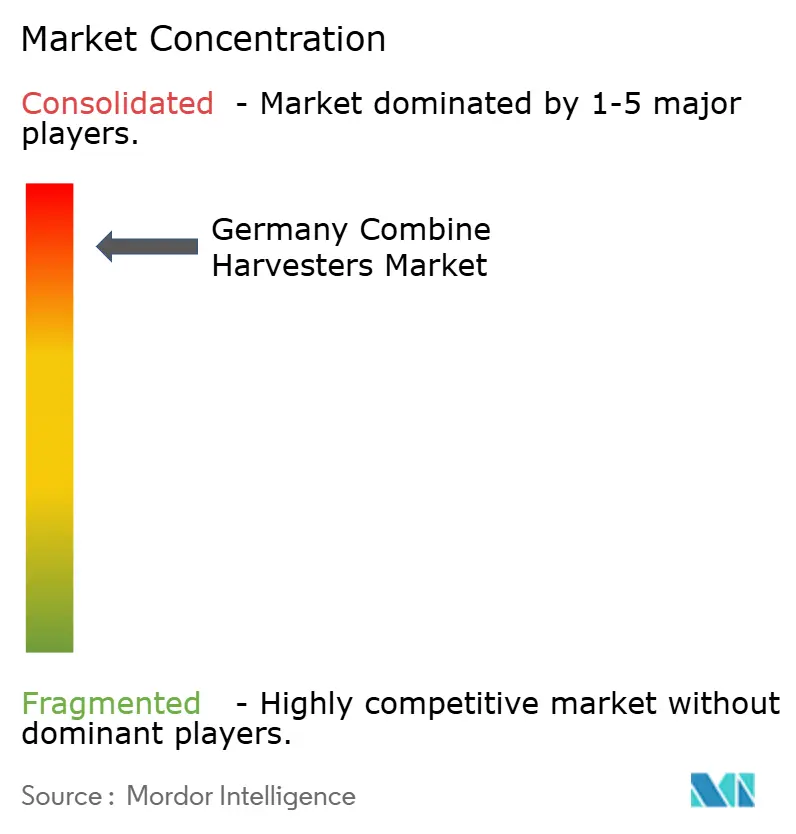

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Combine Harvesters Market Analysis by Mordor Intelligence

The Germany combine harvesters market size was valued at USD 470 million in 2025 and is projected to reach USD 500 million in 2026 and USD 650 million by 2031, registering a CAGR of 5.39% between 2026 and 2031. Fleet modernization is advancing faster than basic replacement as European Union Stage V emission regulations, labor shortages, and precision-agriculture economics influence purchasing decisions. For instance, European Union Regulation 2025/14 on type-approval for non-road mobile machinery came into full effect in January 2025, requiring particulate matter emissions below 0.4 grams per kilowatt-hour and NOx emissions under 0.4 grams per kilowatt-hour for combines exceeding 56 kilowatts. Subsidized loans from the Landwirtschaftliche Rentenbank have reduced borrowing costs for high-capacity, sensor-equipped machines. The increasing use of Hydrotreated Vegetable Oil (HVO)100 fuel is lowering life-cycle costs and aligning with sustainability goals. High demand for automation and data-capture capabilities is driving large commercial operators to invest in 300 to 400 HP units with cloud connectivity.

Key Report Takeaways

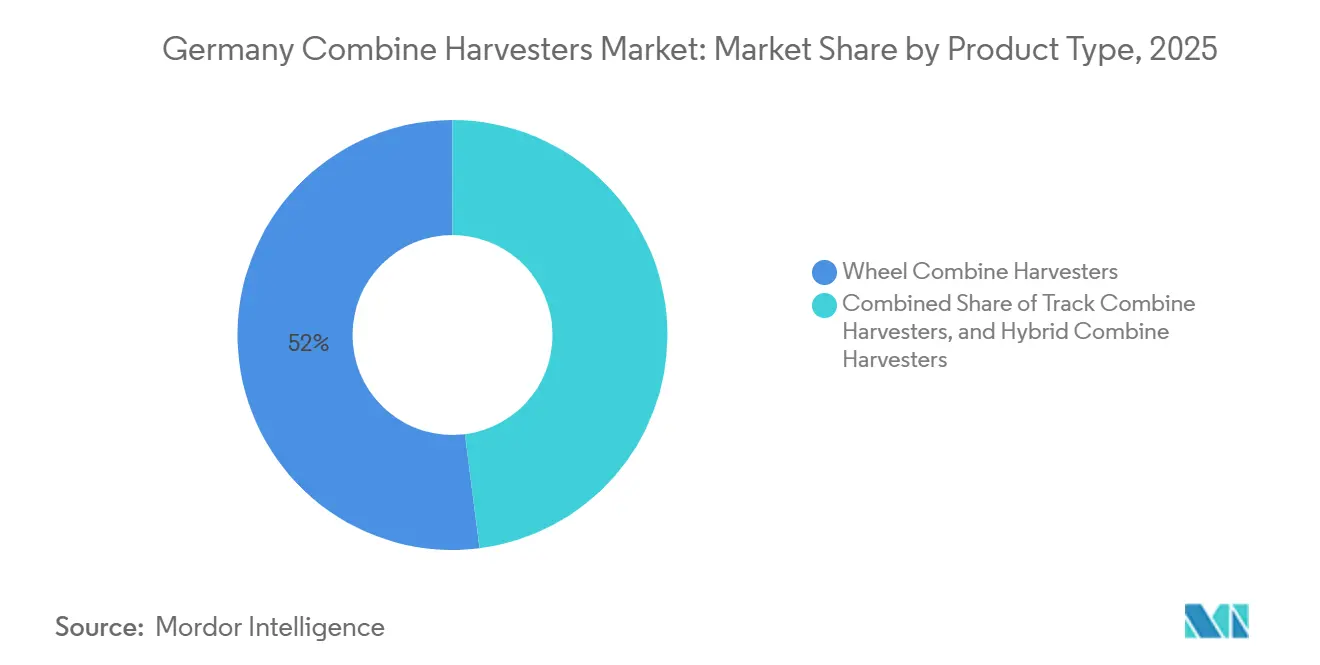

- By product type, wheel combine harvesters accounted for the largest segment, 52% of the Germany combine harvesters market size in 2025. Hybrid combine harvesters are projected to be the fastest-growing segment at a 9.2% CAGR from 2026 to 2031.

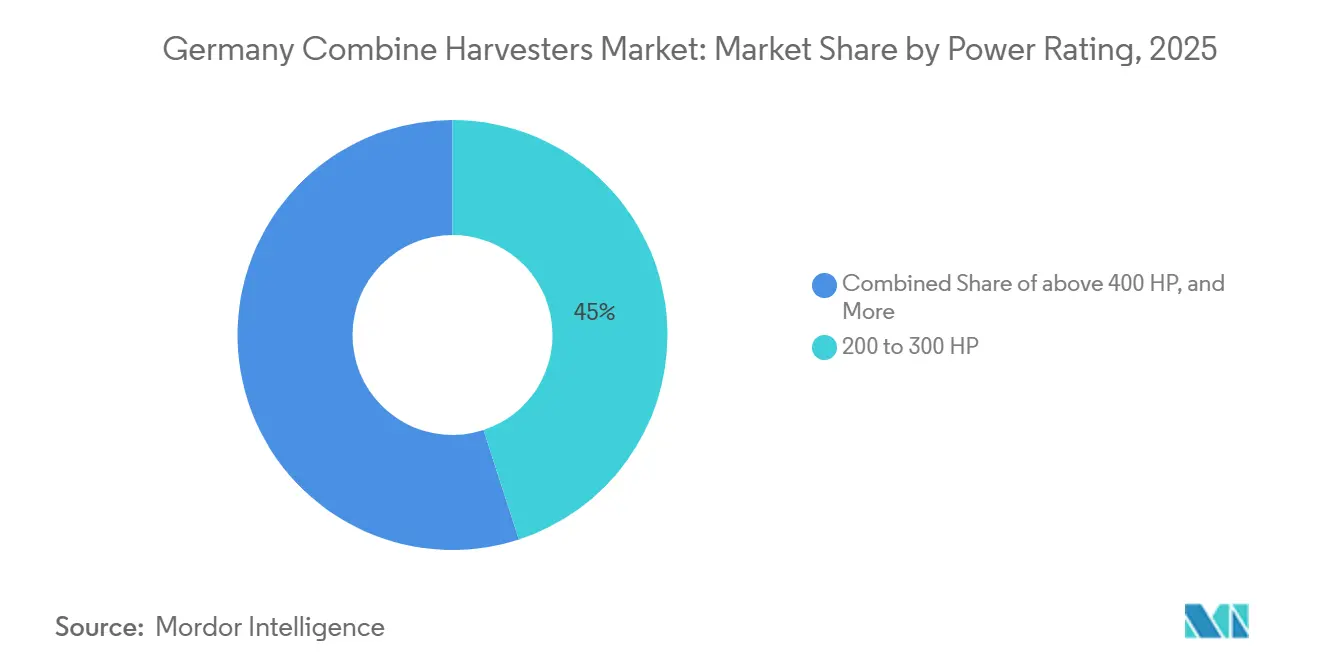

- By power rating, the 200 to 300 HP segment accounted for the largest segment, with 45% of Germany combine harvesters market share in 2025. The above 400 HP segment is projected to be the fastest-growing, with a 10.4% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union Stage V emission norms triggering fleet renewal | +1.8% | Germany-wide, concentrated in Northern and Eastern regions | Medium term (2-4 years) |

| Labor scarcity accelerating demand for automation | +1.5% | Germany-wide, acute in Eastern and Southern regions | Long term (≥ 4 years) |

| Subsidized financing from Landwirtschaftliche Rentenbank | +1.2% | Germany-wide, higher uptake in medium-farm segments | Short term (≤ 2 years) |

| Precision-agriculture adoption is improving Return of Investment (ROI) on high-capacity combine | +1.0% | Germany-wide, early gains in Northern and Western regions | Medium term (2-4 years) |

| Rising biofuel-feedstock acreage needs specialty headers | +0.6% | Eastern Germany (Brandenburg, Mecklenburg-Vorpommern, Sachsen-Anhalt) | Medium term (2-4 years) |

| Hydrotreated Vegetable Oil (HVO) ready engines lower lifecycle fuel costs | +0.6% | Germany-wide, led by large commercial farms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Stage V Emission Norms Triggering Fleet Renewal

New particulate matter and nitrogen oxide thresholds that became mandatory in 2025 rendered older combines uneconomical to retrofit. CLAAS responded by factory-filling all Stage V combine manufactured at its Harsewinkel and Le Mans plants with Hydrotreated Vegetable Oil (HVO) 100 from October 2023, enabling operators to achieve up to 90% CO2 reduction compared to fossil diesel while maintaining warranty coverage [1]Source: CLAAS Group, “CLAAS Approves HVO for All Stage V Machines,” Claas.com . Tight North American output has limited the pool of compliant imports, sustaining residual values and encouraging buyers to secure new inventory quickly. Stage V norms serve as a long-term driver of demand by accelerating replacement cycles, promoting the adoption of advanced technology, and supporting growth in Germany's combine harvester market.

Labor Scarcity Accelerating Demand for Automation

An aging farm workforce and fewer seasonal operators have pushed automation to the top of procurement criteria. Preliminary data for 2025 indicates that employment in Germany's agriculture, forestry, and fishing sector declined by 3,000 individuals, representing a 0.5% decrease to a total of 562,000. This reduction highlights a long-term structural decline in the sector's workforce. Cooperative farms in Eastern Germany, which consolidated large landholdings following reunification, face staffing challenges during multi-shift harvest periods. Deere’s Predictive Ground Speed Automation and CNH’s autonomous grain cart system enable less-experienced staff to achieve consistent throughput, offsetting labor tightness in large eastern cooperatives.

Subsidized Financing from Landwirtschaftliche Rentenbank

In 2025, new business in special promotional loans grew by 82.1% across all promotional lines, reaching EUR 6.6 billion (USD 7.7 billion). Rentenbank introduced guidelines under the federal Special Purpose Fund to support agricultural machinery, including combine harvesters. Access to low-cost capital also fuels demand for lease-back structures that keep equipment off balance sheets. This trend leads to shorter replacement cycles and motivates farmers and contractors to invest in larger, higher-specification machines as the cost difference decreases.

Precision-Agriculture Adoption Improving Return of Investment (ROI) on High-Capacity Combine

The increasing adoption of precision agriculture in Germany is a significant driver of the combine harvesters market, as it enhances the return on investment for high-capacity machines. Technologies such as GPS guidance, yield mapping, variable rate applications, and real-time data analytics enable farmers to optimize harvesting efficiency, minimize grain losses, and manage inputs more effectively across fields. When integrated into large, high-throughput combines, these technologies substantially boost productivity during limited harvest periods, making the investment in expensive equipment more economically viable. This trend is particularly relevant in Germany, where farm consolidation and the expanding role of contractors favor machines capable of covering larger areas with higher precision. Consequently, farmers are increasingly investing in premium combine equipped with advanced sensors and automation systems, driving fleet modernization and shifting demand toward larger, technology-focused models, thereby supporting overall market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital outlay | -1.0% | Germany-wide, acute for medium and smallholder farms | Short term (≤ 2 years) |

| Grain-price volatility is squeezing farm cash flow | -0.8% | Germany-wide, concentrated in wheat and barley regions | Medium term (2-4 years) |

| Emerging state-level neonics restrictions | -0.5% | Germany-wide, most severe in the Southern and Western regions | Long term (≥ 4 years) |

| Shortage of dealer technicians for advanced electronics | -0.4% | Germany-wide, critical in Eastern regions with sparse dealer networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Outlay

High upfront capital requirements remain a significant restraint on Germany's combine harvesters market, as they increase the purchase barrier, extend payback periods, and delay fleet renewal, particularly for small and medium-sized farms. While Germany continues to lead Europe's combine harvesters market, the high cost burden slows replacement demand and encourages buyers to explore financing, leasing, or shared-use models instead of outright ownership. For example, in 2025, combine harvesters prices in Germany vary significantly depending on the model and specifications, with listings ranging from USD 675,648 for a John Deere S7900 to USD 318,435 for a John Deere T5500. For a 150-hectare farm, ownership costs can equate to three to five years of net income, prompting many buyers to opt for rental contracts priced at EUR 200 (USD 210) per hour, which also compresses contractor margins.

Grain-Price Volatility Squeezing Farm Cash Flow

Grain price volatility is affecting farm cash flow in Germany, leading farmers to adopt a more cautious approach to major machinery investments, including combine harvesters. With cereal prices declining sharply from their 2023 peaks and European Union cereal production decreased in 2024, many farmers are projected to postpone fleet upgrades, extend the operational lifespan of their current equipment, or opt for used machinery and financing rather than purchasing new models. Germany remains a key grain producer, contributing 39.1 million metric tons of cereals, equivalent to 15.2% of the European Union's output[2]Source: Eurostat, “EU Cereal Prices 2024,” Ec.europa.eu. This makes the country highly sensitive to price fluctuations, which significantly influence the demand for combine harvesters. Additionally, uncertainty in grain prices is prompting farmers to focus on cost management strategies, such as optimizing existing resources and delaying capital-intensive investments, which is further impacting the market for new machinery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wheel Combine Dominance, Hybrid Momentum

Wheel combine harvesters accounted for the largest segment, 52% of the Germany combine harvesters market share in 2025. The dominance of wheel combine is attributed to their versatility across various soil conditions and ease of movement between fields and public roads. Their suitability for mixed farming operations and relatively straightforward mobility make them a practical choice for many German farmers. Track combine harvesters hold a smaller market share, primarily concentrated in Southern Germany's hilly terrain. For instance, CLAAS's Lexion 8500, introduced in July 2025, features a 549 HP engine and advanced suspension systems designed to reduce soil compaction in sensitive areas[3]Source: CLAAS Group, “CLAAS Launches Trion 760 and Lexion 8500 Combines,” Claas.com.

Hybrid combine harvesters are the fastest-growing segment, forecast to grow at a 9.2% CAGR from 2026 to 2031. Hybrid adoption also benefits rental fleets because lower fuel burn improves hourly margins. As battery prices drop, Original Equipment Manufacturers (OEMs) plan mid-decade rollouts that could lift the Germany combine harvesters market share for hybrids to double digits by 2031. Stricter emissions regulations and the demand for more efficient harvesting solutions are projected to drive adoption. Enhanced performance in high-output operations may also make hybrids more appealing to large commercial farms.

By Power Rating: Mid-Range Workhorse and Autonomous Upside

The 200 to 300 HP segment accounted for the largest segment, held 45% of the Germany combine harvesters market size in 2025. Machines in this range are versatile, capable of handling various crops and field conditions, while avoiding the higher purchase and maintenance costs associated with higher-horsepower models. These combines are particularly well-suited for farms that require reliable performance during standard harvesting seasons and align with the budgets and acreage needs of many German growers. For instance, a CLAAS 220 HP combine offers sufficient capacity for mixed cereal operations in Germany while remaining cost-effective for regular use.

Above 400 HP is the fastest-growing segment, forecast to grow at a 10.4% CAGR from 2026 to 2031. This growth is driven by larger commercial farms seeking higher throughput and reduced harvesting times. These machines are particularly appealing for operations managing extensive acreage, as they enable faster coverage and improved labor efficiency during peak seasons. In 2024, John Deere globally introduced the new S series of combine, including in Germany, featuring the S7 models. These models emphasized improved efficiency, an enhanced operator experience, and laid the foundation for future autonomy systems. The four S7 models offered rated engine horsepower ranging from 333 to 543.

Geography Analysis

Northern Germany holds a significant share of the Germany combine harvesters market due to its large, flat wheat and rapeseed fields, which are well-suited for 300 to 400 HP wheel machines equipped with 13,500-liter grain tanks. The region benefits from a dense dealer network that ensures quick parts supply, rapid servicing, and efficient fleet maintenance. Additionally, early broadband infrastructure supports real-time data transfer, enabling precision-farming tools such as yield mapping and variable-rate harvesting. These tools enhance harvest efficiency and simplify field documentation.

Eastern Germany is emerging as a growing market, driven by post-consolidation cooperatives and larger farm structures investing in high-capacity combine fleets and specialized rapeseed headers. The consolidation trend has increased the average farm size, making large-capacity machines more economically viable. Sparse dealer coverage can extend repair cycles and increase downtime risks. This has led to higher demand for remote diagnostics, telematics, and predictive maintenance systems, which help minimize unplanned failures.

Southern and Western Germany are characterized by fragmented plots, mixed crops, and rolling terrain, favoring mid-range combine and track variants designed for hilly or wet soils. An older operator demographic in these regions may slow the adoption of advanced digital features and automation, as operators often prefer familiar, simpler controls. Meanwhile, strong biogas and biodiesel industries in these areas promote the use of Hydrotreated Vegetable Oil (HVO100), which operates on fully renewable fuel, reducing life-cycle greenhouse gas emissions and operating costs.

Competitive Landscape

The Germany combine harvesters market is highly concentrated, with the top five players projected to account for a significant share of revenue by 2025. This concentration reflects economies of scale in manufacturing, dense dealer networks, and strong brand loyalty developed over decades. Claas KGaA mbH leads the market, followed by Deere and Company, CNH Industrial N.V., AGCO Corporation, and SDF S.p.A. Claas utilizes its Harsewinkel manufacturing facility, which produces more than 10,000 combines annually and has integrated factory-fill HVO100 capability for all Stage V machines since October 2023.

These leading players capitalize on scale, established brand trust, and extensive dealer networks to secure contracts with large farms, cooperatives, and machinery rental operators. They also offer integrated precision agriculture solutions and financing options, further enhancing customer retention. Meanwhile, regional and niche manufacturers focus on mid-range or specialized machines designed for fragmented plots, hilly terrain, or specific crops such as rapeseed, where maneuverability and versatility are prioritized over capacity.

Key players differentiate themselves by providing tailored configurations, localized support, and often a lower total cost of ownership. Their influence on the broader market remains limited compared to global Original Equipment Manufacturers (OEMs). The combination of premium-brand dominance and competition from specialist segments ensures a dynamic market landscape, even within a highly consolidated environment.

Germany Combine Harvesters Industry Leaders

CLAAS KGaA mbH

CNH Industrial N.V.

AGCO Corporation

SDF S.p.A.

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AGCO showcased advanced AI-powered harvesting technology at AGRITECHNICA 2025 in Hanover, Germany. This included the Fendt IDEAL combine and Katana forage harvesters, emphasizing sustainable and high-productivity solutions for European agriculture.

- November 2024: Case IH launched the AF9 and AF10 axial-flow combine at EIMA in Europe, including Germany. These models feature 635 HP and 775 HP engines, respectively. The AF10 is equipped with a 20,000-liter grain tank, the largest in the industry, allowing unloading cycles every 90 to 120 minutes compared to 60 to 75 minutes for conventional 13,000-liter tanks.

- July 2024: John Deere introduced the T6 800 combine harvesters. With increasing demand from European farmers for conventional combines, the T6 800s were manufactured at Deere’s combine plant in Zweibrücken, Germany, rather than at its Harvesters Works facility in East Moline, Illinois, where rotary combines are assembled.

Germany Combine Harvesters Market Report Scope

A combine harvester, commonly called a "combine," is a large agricultural machine designed to harvest grain and seed crops. It performs multiple operations in a single pass, including cutting the standing crop, threshing the grain from the stalks, and cleaning the grain. Germany combine harvesters market report is segmented by product type (wheel combine harvesters, track combine harvesters, and hybrid combine harvesters) and by power rating (below 200 HP, 200 to 300 HP, 300 to 400 HP, and above 400 HP). The market forecasts are provided in terms of value (USD).

| Wheel Combine Harvesters |

| Track Combine Harvesters |

| Hybrid Combine Harvesters |

| Below 200 HP |

| 200 to 300 HP |

| 300 to 400 HP |

| Above 400 HP |

| By Product Type | Wheel Combine Harvesters |

| Track Combine Harvesters | |

| Hybrid Combine Harvesters | |

| By Power Rating | Below 200 HP |

| 200 to 300 HP | |

| 300 to 400 HP | |

| Above 400 HP |

Key Questions Answered in the Report

What is the size of the Germany combine harvesters’ market in 2026?

The Germany combine harvesters market size is estimated at USD 500 million in 2026, according to Mordor Intelligence.

How does biofuel growth affect header technology?

Rising rapeseed acreage associated with renewable fuel production is increasing demand for specialty headers that help reduce pod shatter losses, particularly in Eastern Germany.

Which product type currently holds the largest share of combine sales?

Wheel combine harvesters accounted for 52% of the Germany combine harvesters market share in 2025.

What financing support is available for purchasing new combine?

Landwirtschaftliche Rentenbank provides subsidized financing programs that help farmers purchase Stage V-compliant combine harvesters and accelerate fleet modernization.

Page last updated on: