PTO Powered Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

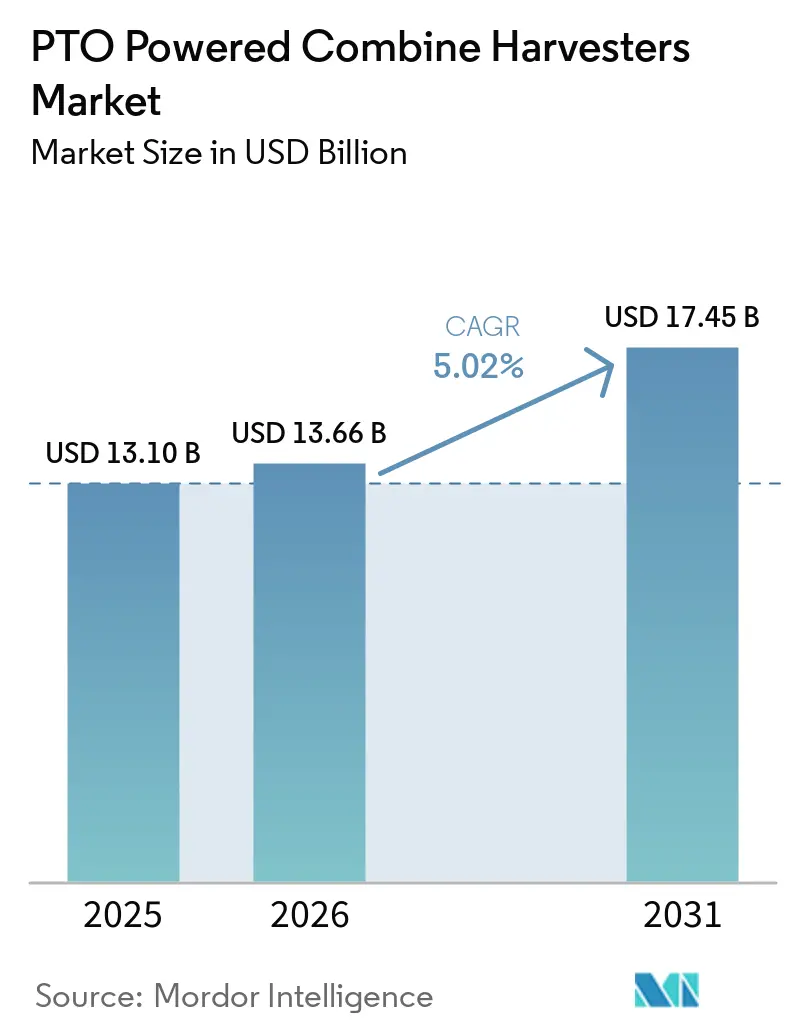

| Market Size (2026) | USD 13.66 Billion |

| Market Size (2031) | USD 17.45 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PTO Powered Combine Harvesters Market Analysis by Mordor Intelligence

The PTO powered combine harvester market size is projected to grow from USD 13.10 billion in 2025 and USD 13.66 billion in 2026, to USD 17.45 billion by 2031, registering a CAGR of 5.02% from 2026 to 2031. Growth is driven by the increasing adoption of tractor-mounted power-take-off (PTO) units in smallholder and fragmented-farm regions, as these units offer lower upfront costs and greater seasonal flexibility compared to self-propelled combines. In the Asia-Pacific region, subsidy programs are encouraging the use of modular PTO platforms that can be shared among multiple owners. Similarly, in South America, rental fleets are expanding PTO deployments to meet tight harvest schedules without the need for dedicated chassis investments. Other growth drivers include predictive maintenance kits, crawler undercarriages designed for hilly terrain, and revenue opportunities from carbon-credit programs, all of which are projected to shape market dynamics over the next five years.

Key Report Takeaways

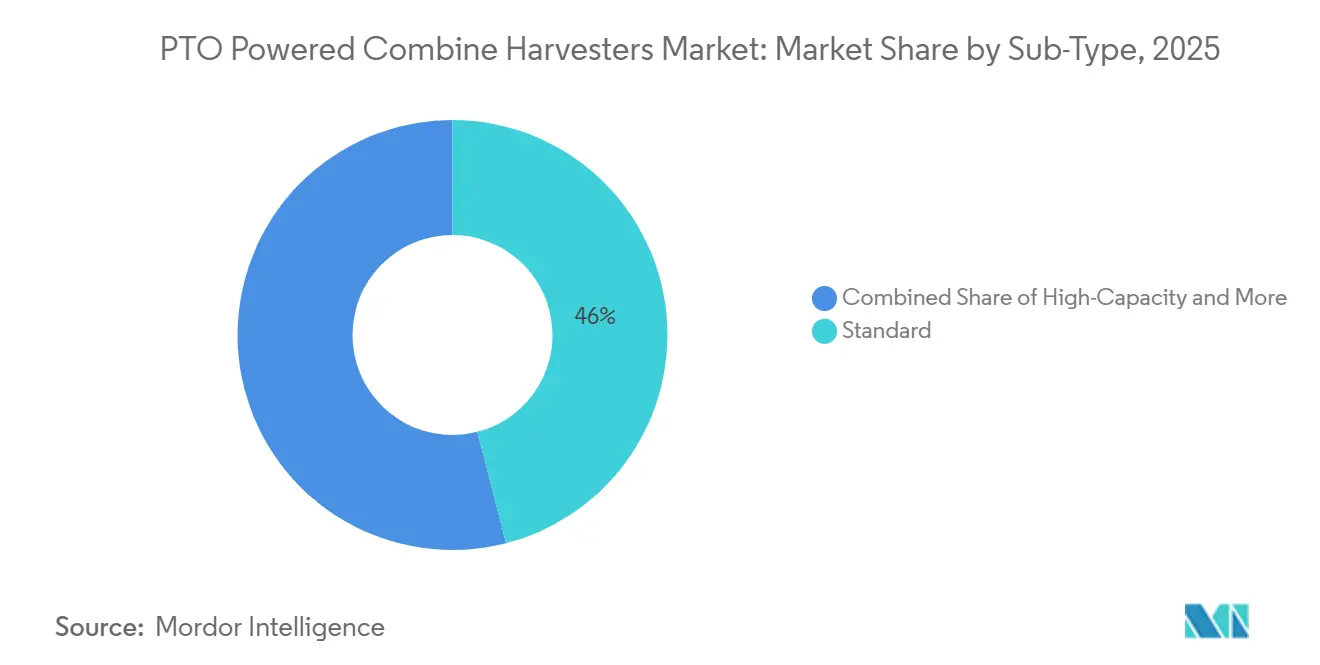

- By sub-type, standard captured the largest 46% of the PTO-powered combine harvester market share in 2025, while high-capacity is anticipated to grow at the fastest 7.6% CAGR from 2026 to 2031.

- By movement type, wheel held the largest 62% of the PTO-powered combine harvester market size in 2025, whereas the crawler segment is projected to grow at the fastest 8.2% CAGR from 2026 to 2031.

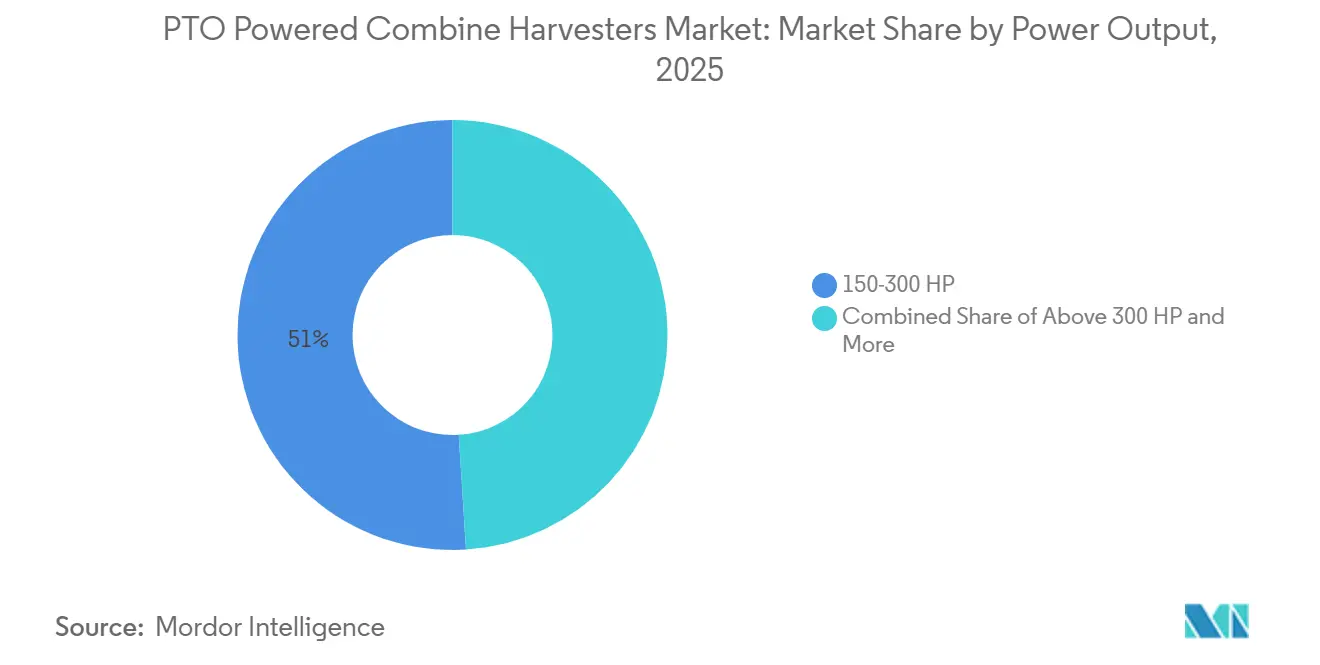

- By power output, 150-300 HP accounted for the largest 51% revenue share in 2025, while power outputs above 300 HP are forecast to expand at the fastest 9.1% CAGR from 2026 to 2031.

- By application, wheat accounted for the largest 39% revenue share in 2025, whereas rice is projected to post the fastest 8.5% CAGR from 2026 to 2031.

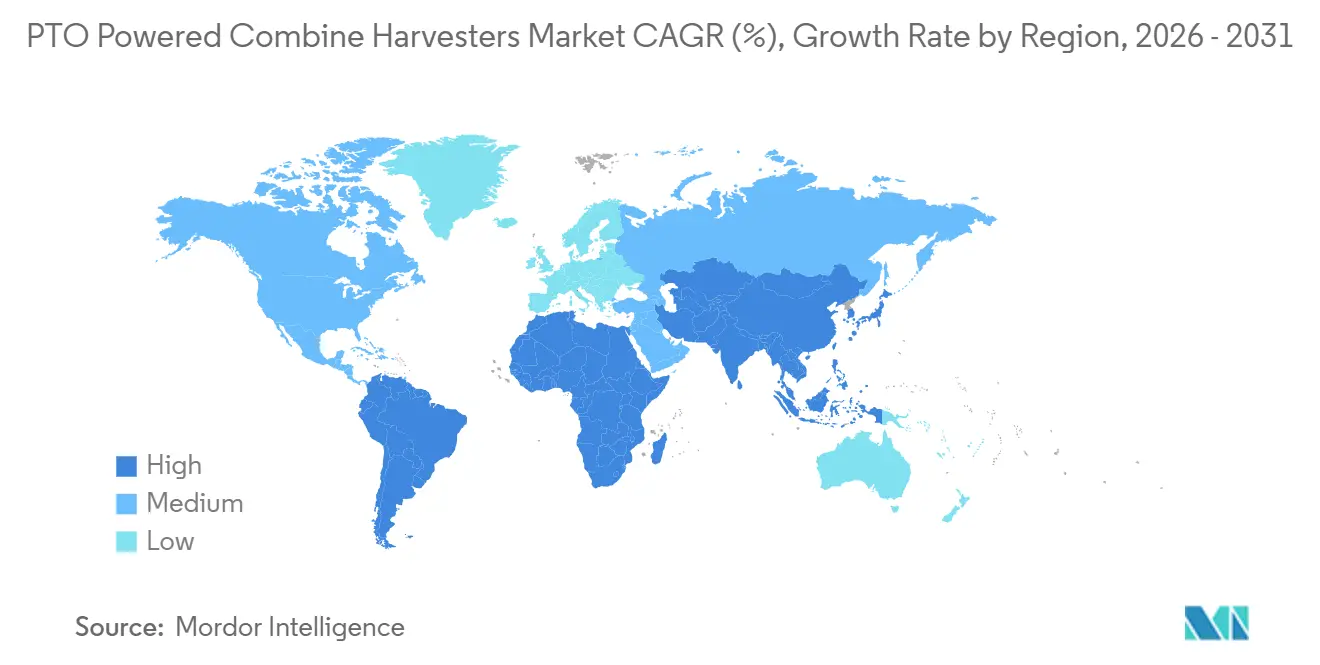

- By geography, North America commanded the largest 31.9% revenue share in 2025, while Asia-Pacific is projected to grow at the fastest 7.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PTO Powered Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-led mechanization programs | +1.2% | India, China, and Southeast Asia | Medium term (2-4 years) |

| Rapid rental-fleet penetration in South America | +0.9% | Brazil, Argentina, and Chile | Short term (≤2 years) |

| Hybrid PTO driveline retrofits that cut fuel | +0.7% | Europe and North America first movers | Medium term (2-4 years) |

| Predictive-maintenance IoT kits sold as aftermarket | +0.5% | North America and Europe pilots | Long term (≥4 years) |

| Emergence of compact crawler PTO harvesters for hilly farms | +0.6% | China, India, and Southeast Asia | Medium term (2-4 years) |

| Carbon-credit income for low-emission PTO operations | +0.4% | North America and European Union | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Subsidy-Led Mechanization Programs

Farm mechanization support programs and low-interest agricultural investment schemes across Europe are promoting the adoption of equipment compatible with existing tractor fleets, aiming to minimize capital expenditure. In France, the European Investment Fund and the French Ministry of Agriculture expanded the National Initiative for French Agriculture in May 2025. This initiative, with an investment volume exceeding EUR 2 billion (USD 2.27 billion), is projected to support over 15,000 farmers by 2028 [1]Source: European Investment Fund, “Support for Agricultural Investment in France,” eif.org. The financing program focuses on enhancing agricultural equipment investment and modernization, enabling farms and cooperatives to improve access to machinery while reducing financial barriers to adopting harvesting equipment.

Rapid Rental-Fleet Penetration in South America

The demand for agricultural machinery rental and contractor-based harvesting services is growing across South America as farmers increasingly prioritize flexible equipment access over ownership. Factors such as seasonal harvesting needs, fluctuating commodity prices, and the high acquisition costs of self-propelled machinery are driving the adoption of shared-utilization and lease-based operating models. Rental platforms and outsourced mechanized service providers allow farms to maximize equipment usage during peak harvest periods while minimizing idle machinery costs during off-seasons. This trend is particularly prominent among small and medium-sized grain producers seeking cost-effective, tractor-compatible harvesting solutions, thereby boosting the demand for PTO powered combine harvesters in the regional agricultural market.

Hybrid PTO Driveline Retrofits that Cut Fuel

Rising fuel costs and stricter emission compliance requirements are accelerating the development of hybrid-assisted and fuel-efficient driveline technologies in agricultural harvesting machinery. According to researchers from Université Laval, Québec, Canada, a 2026 study published in Cleaner Engineering and Technology found that hybrid harvesting systems demonstrated an 18% productivity increase compared to conventional diesel harvesters while improving operational efficiency under varying field conditions. The growing industry focus on reducing fuel consumption and improving lifecycle operating efficiency is encouraging the adoption of hybrid retrofit and electrified driveline technologies in harvesting equipment, supporting demand for efficient PTO-compatible harvesting systems.

Predictive-Maintenance IoT Kits Sold as Aftermarket

The adoption of AI-enabled predictive maintenance technologies is enhancing operational reliability and minimizing unplanned downtime in agricultural machinery operations. According to the researchers from the College of Mechanical and Electrical Engineering, Hunan Agricultural University, China, highlighted in a 2025 study that sensor-based monitoring and intelligent data analytics significantly improve real-time operational monitoring and fault prediction capabilities in combine harvester systems. The growing use of IoT sensors, connected diagnostics, and aftermarket monitoring solutions is driving farm operators to retrofit existing harvesting equipment with predictive maintenance technologies. These advancements enhance servicing efficiency, reduce operational interruptions, and optimize machinery utilization during peak harvesting periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High attachment-to-tractor power-ratio limits on small plots | -0.8% | South and Southeast Asia, Sub-Saharan Africa | Short term (≤2 years) |

| Scarcity of trained PTO-combine operators | -0.6% | Asia-Pacific and Africa | Medium term (2-4 years) |

| Seasonal idle time driving low return-on-investment | -0.5% | Global, acute in single-crop belts | Medium term (2-4 years) |

| Import tariffs on gearbox components | -0.4% | North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Attachment-to-Tractor Power-Ratio Limits on Small Plots

The prevalent use of low-horsepower tractors in smallholder farming regions restricts the operational compatibility of larger PTO powered combine harvesters, which require higher engine output for stable and efficient performance. Fragmented landholdings and limited farm mechanization reduce the economic viability of investing in high-capacity harvesting attachments, particularly for small and medium-sized farmers. During harvesting periods, farmers often depend on rented higher-horsepower tractors, which increases operational costs and diminishes the cost benefits of PTO based harvesting systems. Furthermore, compact PTO harvester models designed for low-horsepower tractors generally offer lower throughput, limiting harvesting efficiency and acreage coverage during peak agricultural seasons.

Import Tariffs on Gearbox Components

Rising tariffs and trade restrictions on imported industrial transmission components are driving up manufacturing costs for agricultural equipment producers reliant on foreign drivetrain and gearbox assemblies. In 2025, the United States implemented a 25% tariff on imported automobile parts, including transmissions and powertrain components, as part of expanded trade protection measures impacting global mechanical component supply chains [2]Source: The White House, “United States Imposes Import Duty of Automobiles and Automobile Parts Into the United States,” whitehouse.gov. These increased import duties on transmission-related components are raising procurement and landed costs for manufacturers sourcing drivetrain systems internationally. As a result, production costs are rising, reducing the price competitiveness of PTO-compatible combine harvesters and related agricultural machinery in cost-sensitive farming markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Type: Standard Units Dominate, High-Capacity Models Accelerate

The standard segment accounted for the largest 46% share of the PTO powered combine harvester market in 2025. This segment benefits from broad compatibility with medium-horsepower tractors, which are widely used in mixed-grain farming regions across Asia-Pacific, North America, and Europe. Farmers prefer standard models due to their lower ownership costs, ease of maintenance, and compatibility with existing tractor fleets. Additionally, the growing availability of retrofit precision farming systems and aftermarket monitoring technologies is enhancing machinery lifecycles and operational efficiency.

The high-capacity segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. Demand growth is supported by rising adoption of crop-specific harvesting systems for pulses, oilseeds, and fragile grains that minimize grain damage during harvesting operations. Manufacturers are increasingly introducing adjustable threshing systems, variable cleaning technologies, and compact harvesting attachments suitable for diverse crop conditions and fragmented agricultural fields. Growing labor shortages and increasing focus on reducing post-harvest losses continue to strengthen adoption across specialty agricultural applications.

By Movement Type: Wheels Lead, Crawlers Conquer Slopes

Wheel systems accounted for 62% of the PTO powered combine harvester market share in 2025. Their widespread adoption is attributed to lower acquisition costs, easier servicing requirements, and suitability for dryland farming conditions in major grain-producing regions. Farmers prefer wheel systems due to their superior road mobility and compatibility with existing agricultural infrastructure. Additionally, the segment benefits from the strong availability of replacement parts and lower maintenance complexity than tracked systems. Advances in suspension systems and terrain adaptability are further enhancing operational efficiency while preserving affordability for commercial farming operations.

Crawler systems are projected to grow at a CAGR of 8.2% from 2026 to 2031. This growth is driven by increasing adoption in wet-field agricultural conditions, where improved traction and reduced soil compaction are critical. Variability in rainfall and shorter field-drying periods in rice-producing regions are boosting demand for tracked harvesting systems capable of operating in challenging terrain. Farmers in paddy cultivation areas are increasingly adopting crawler systems to ensure harvesting continuity and minimize field losses during monsoon seasons.

By Power Output: Above-300 HP Units Gain on Precision Load

150-300 HP accounted for the largest 51% PTO powered combine harvester market share in 2025. The segment remains dominant due to its compatibility with the installed tractor base across North America, Europe, and the Asia-Pacific agricultural markets. Medium-horsepower systems provide balanced operational efficiency, fuel consumption, and harvesting capacity, making them suitable for diversified farming operations. Farmers continue to prefer this power category because it supports multiple agricultural applications while keeping ownership and operating costs manageable. Strong availability of compatible implements and widespread dealer support networks also contribute to stable adoption across commercial grain and mixed-crop farming regions globally.

The above-300-HP market size is forecast to expand at the fastest 9.1% CAGR from 2026 to 2031. Growth is supported by rising adoption of precision farming technologies, high-capacity harvesting operations, and advanced telemetry systems requiring greater auxiliary power output. Large-scale commercial farms are increasingly deploying high-horsepower harvesting systems to improve operational productivity and reduce harvesting turnaround time during compressed crop cycles. Manufacturers are also integrating hybrid driveline technologies and intelligent load-management systems to improve fuel efficiency in higher-capacity equipment.

By Application: Rice Leads Growth, Wheat Anchors Demand

Wheat accounted for the largest 39% share of the PTO powered combine harvester market in 2025. This dominance is attributed to extensive wheat cultivation across North America, Europe, and the Asia-Pacific region, where mechanized harvesting is critical for managing short harvesting windows and large-scale cultivation. Farmers rely on PTO-compatible harvesting systems to supplement harvesting capacity during adverse weather conditions and labor shortages. The widespread availability of compatible tractor fleets and established grain farming infrastructure further supports stable adoption in commercial wheat-producing regions. Additionally, the increasing emphasis on minimizing harvesting delays and reducing post-harvest losses sustains the global demand for mechanized wheat harvesting operations.

Rice is projected to achieve the fastest growth, with an 8.5% CAGR from 2026 to 2031. This growth is driven by increasing mechanization in major rice-producing countries such as India, China, Thailand, and Vietnam, where labor shortages and rising farm wages are boosting demand for mechanized harvesting solutions. Farmers are increasingly adopting compact and crawler-compatible PTO harvesting systems designed for wet-field paddy cultivation and fragmented agricultural landholdings. Expanding government support for agricultural mechanization and the rising adoption of semiautonomous harvesting technologies are also contributing to the segment's growth. The focus on reducing harvesting losses and improving operational productivity continues to strengthen the long-term demand for mechanized rice harvesting equipment.

Geography Analysis

North America is projected to account for 31.9% of the PTO-powered combine harvester market share in 2025. This growth is attributed to extensive farm mechanization, high tractor penetration, and strong seasonal demand for harvesting in large grain-producing regions. Farmers in the United States and Canada are increasingly adopting PTO harvesting systems to address contingency harvesting needs during compressed weather windows and peak seasonal operations. According to Statistics Canada, Canada's wheat production reached 34.96 million metric tons in 2025, driving demand for mechanized harvesting solutions in commercial grain operations. Additionally, strong rental fleet activity and the growing adoption of precision agriculture technologies are supporting the utilization of harvesting equipment across the regional agricultural sector.

The Asia-Pacific market is projected to grow at the fastest 7.9% CAGR from 2026 to 2031 due to expanding farm mechanization, rising agricultural labor shortages, and increasing adoption of tractor-compatible harvesting systems across fragmented farming structures. Countries such as India and China continue to promote mechanized farming practices to improve agricultural productivity and reduce post-harvest losses. Smaller landholdings in major agricultural economies favor modular and lower-cost harvesting solutions compatible with existing tractor fleets. The growing adoption of semiautonomous controls, precision farming technologies, and compact harvesting platforms is also strengthening regional demand. Expanding rice and wheat cultivation areas continue to support long-term harvesting equipment adoption across Asia-Pacific agricultural markets.

South America continues to witness increasing adoption of contractor-based harvesting and machinery-sharing operations as growers seek lower upfront ownership costs and flexible equipment access during seasonal crop cycles. Brazil’s cereal production reached a record 350.2 million metric tons in the 2024-25 harvest season, according to Companhia Nacional de Abastecimento (CONAB), strengthening demand for mechanized harvesting capacity across major grain-producing regions [3]Source: EFA News, “Cereals, Brazil Record Production in 2024-25 Harvested 350.2 Million Tons,” efanews.eu. Rising seasonal harvesting demand is encouraging rental fleet operators and agricultural service providers to expand the deployment of tractor-compatible harvesting systems across South America.

Competitive Landscape

The PTO-powered combine harvester market remains moderately fragmented, with five major companies, including Kubota Corporation, ISEKI & CO., LTD., Mahindra & Mahindra Ltd., Kartar Agro Industries Private Limited, and Preet Agro Industries Private Limited. Global players are investing in precision agriculture technologies, fuel-efficient harvesting systems, and digital monitoring platforms to enhance long-term customer retention. Competitive positioning is increasingly shaped by factors such as equipment reliability, aftermarket servicing capabilities, and compatibility with existing tractor fleets across diverse agricultural operations.

Technology integration remains a major competitive differentiator as manufacturers increasingly focus on predictive maintenance systems, semiautonomous steering technologies, and connected machinery platforms. Companies are forming partnerships with agricultural software providers and automation technology firms to enhance operational efficiency and ensure compatibility with precision farming practices. The growing adoption of IoT-enabled monitoring systems and remote diagnostics is driving higher aftermarket service revenue and improving equipment lifecycle management. However, compliance with stricter emission standards and agricultural safety regulations is increasing development costs, which poses challenges for smaller manufacturers.

Competitive activity continues to intensify across Europe and Asia-Pacific as agricultural machinery manufacturers expand production capabilities, dealer networks, and precision farming technologies to support rising mechanization demand. According to the European Agricultural Machinery Association (CEMA), the general business climate index for the European agricultural machinery industry improved from -11 points in February 2025 to -5 points in March 2025, indicating stronger market sentiment and better turnover expectations in regional machinery markets. Improving dealer inventory conditions and recovering order intake are prompting manufacturers to accelerate technology integration, upgrade harvesting equipment, and pursue regional expansion strategies in global agricultural machinery markets.

PTO Powered Combine Harvesters Industry Leaders

Kubota Corporation

ISEKI & CO., LTD.

Kartar Agro Industries Private Limited

Preet Agro Industries Private Limited

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CLAAS KGaA mbH launched upgraded LEXION combine harvesters featuring increased grain tank capacity, enhanced engine configurations, and improved harvesting efficiency. These upgrades support advancements in PTO-powered combine harvester operations and tractor-compatible harvesting applications.

- June 2025: Deere & Company introduced the F8 and F9 harvesters, equipped with higher horsepower engines, HarvestMotion technology, and improved harvesting efficiency. This launch aims to enhance its portfolio of tractor-compatible, PTO-powered harvesting equipment, thereby increasing productivity and fuel efficiency in large-scale forage harvesting operations.

- January 2025: Yanmar Holdings Co., Ltd. has completed the acquisition of CLAAS India to enhance its PTO-powered combine harvester manufacturing capabilities and increase the production of tractor-compatible wheel-type harvesting equipment in India.

Global PTO Powered Combine Harvesters Market Report Scope

PTO powered combine harvesters are machines that utilize a tractor's power take-off (PTO) system to transfer engine power from the tractor to the harvester. This enables operations such as cutting, threshing, and grain separation. These harvesters are commonly used on small and medium-sized farms due to their lower acquisition costs and compatibility with existing tractor fleets. The PTO powered combine harvester market report is segmented by sub-type (standard, high-capacity, and specialty-crop), by movement type (wheel and crawler), by power output (below 150 HP, 150-300 HP, and above 300 HP), by application (wheat, rice, soybean, and other crops applications), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Standard |

| High-Capacity |

| Specialty-Crop |

| Wheel |

| Crawler |

| Below 150 HP |

| 150-300 HP |

| Above 300 HP |

| Wheat |

| Rice |

| Soybean |

| Other Crops |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Sub-Type | Standard | |

| High-Capacity | ||

| Specialty-Crop | ||

| By Movement Type | Wheel | |

| Crawler | ||

| By Power Output | Below 150 HP | |

| 150-300 HP | ||

| Above 300 HP | ||

| By Application | Wheat | |

| Rice | ||

| Soybean | ||

| Other Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the PTO powered combine harvester market be by 2031?

The PTO powered combine harvester market size is forecast to reach USD 17.45 billion by 2031.

Which application segment is growing fastest?

Rice harvesting is projected to post the fastest growth at the fastest 8.5% CAGR from 2026 to 2031 as mechanization rates rise in India and China.

What drives adoption of crawler PTO harvesters?

Tracked undercarriages lower ground pressure and navigate slopes above 15 degrees, making them essential for terraced rice and hilly soybean farms.

Which region will lead future growth?

Asia-Pacific is set to record the fastest 7.9% CAGR from 2026 to 2031.

Page last updated on: