France Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

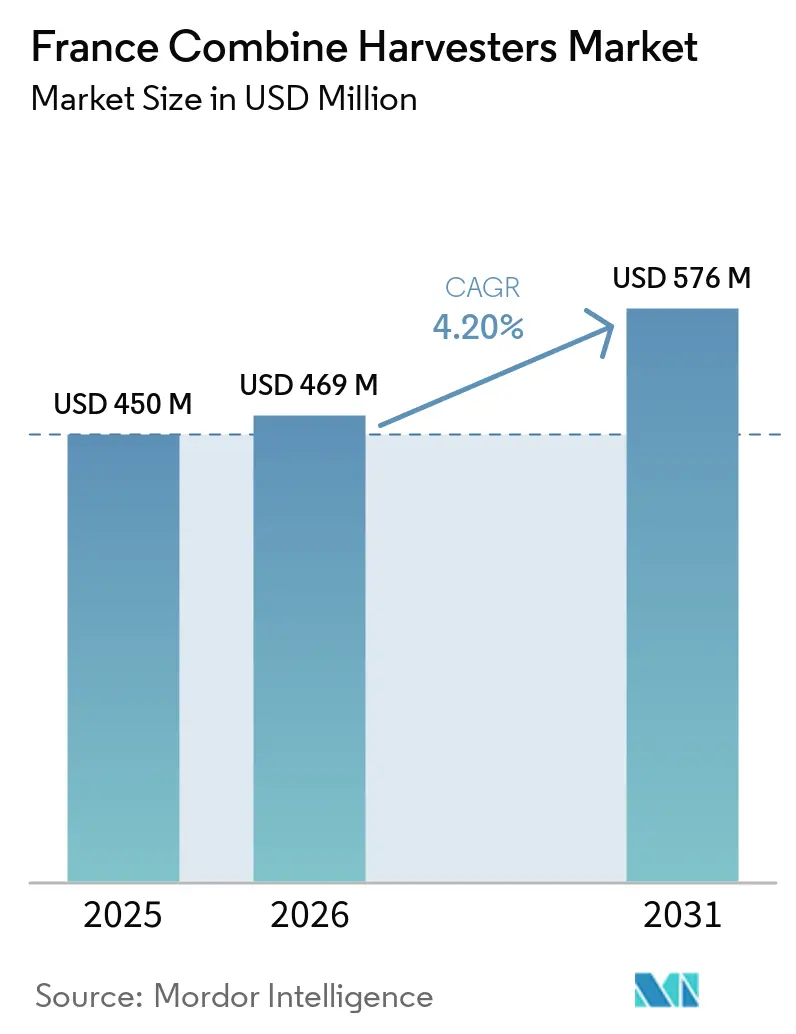

| Base Year Market Size (2025) | USD 450 Million |

| Market Size (2026) | USD 469 Million |

| Market Size (2031) | USD 576 Million |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Combine Harvesters Market Analysis by Mordor Intelligence

The France combine harvesters market was valued at USD 450.0 million in 2025 and is projected to grow from USD 469.0 million in 2026 to USD 576.0 million by 2031, with a CAGR of 4.2% during the forecasted period from 2026 to 2031. Key factors driving this growth include shorter harvest windows, increasing rural wages, and a reduction in cereal cultivation areas, which are encouraging investments in high-throughput machines equipped with telematics and automation technologies. Market expansion is further supported by growing farm consolidation, the adoption of precision agriculture technologies, and the demand for fuel-efficient harvesting equipment in major cereal-producing regions. Farmers are increasingly opting for high-capacity combine harvesters with automation and real-time monitoring systems to enhance operational efficiency and minimize crop losses. Additionally, financing programs offering lower interest rates and the growth of digital agriculture platforms are facilitating the modernization of harvesting machinery.

Key Report Takeaways

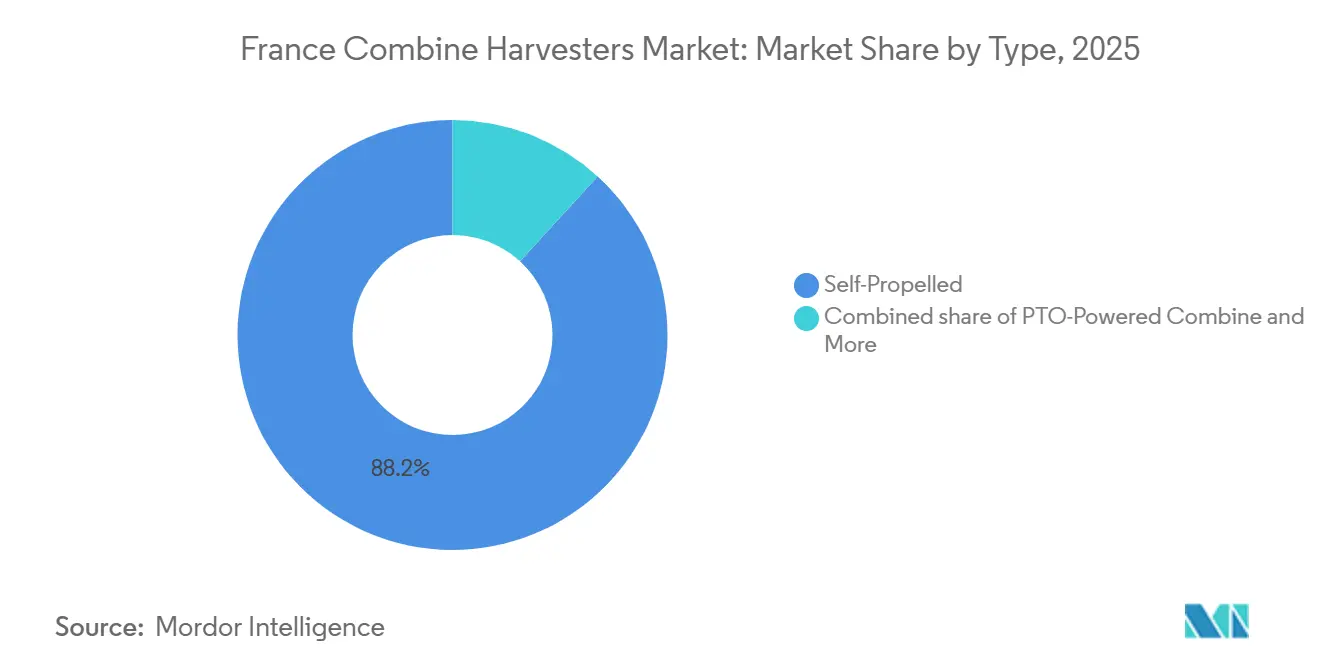

- By type, self-propelled accounted for the largest 88.2% share in 2025, whereas the PTO-powered combine segment is projected to grow at the fastest CAGR of 6.4% from 2026 to 2031.

- By power output, the 150 to 300 HP segment accounted for the largest 48.6% share of the France combine harvesters market in 2025, whereas the France combine harvesters market size for the above 450 HP segment is projected to expand at the fastest 6.8% CAGR from 2026 to 2031.

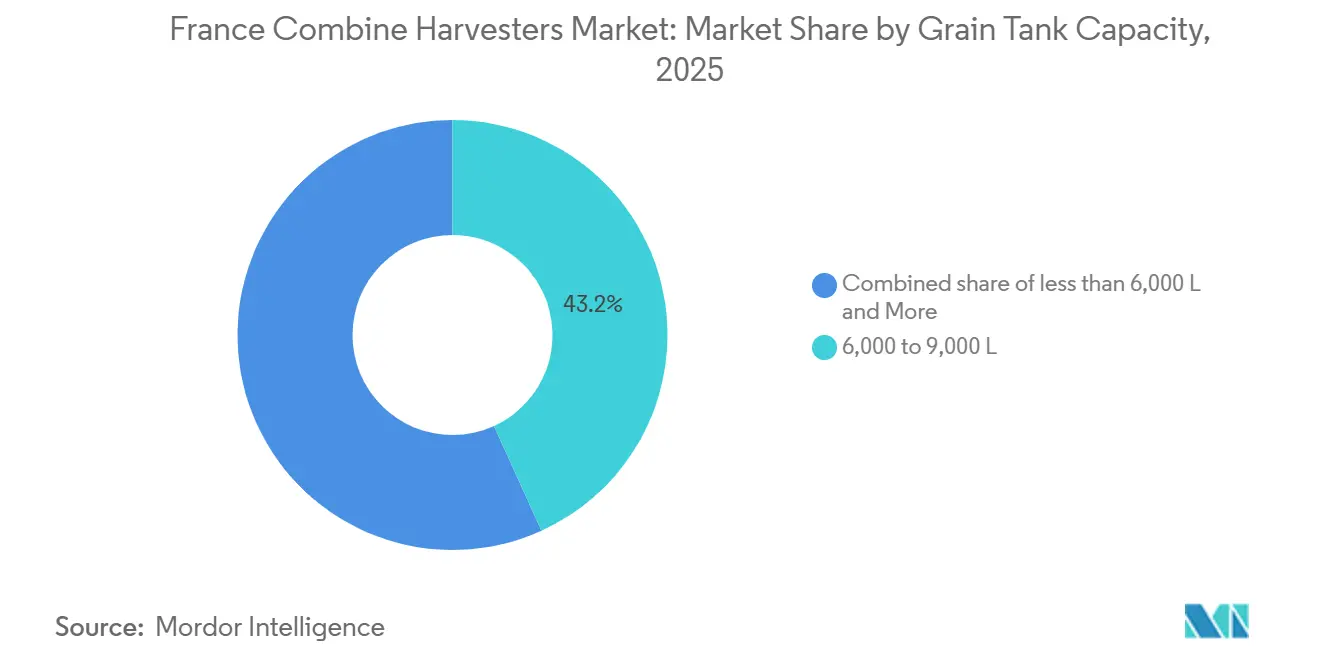

- By grain tank capacity, the 6 000–9 000 L segment held the largest 43.2% revenue share in 2025, whereas above 9 000 L is projected to grow at the fastest 6.3% CAGR from 2026 to 2031.

- By drive type, wheel drive units commanded the largest 62.3% share in 2025, while track drive is forecast to grow at the fastest 7.2% CAGR from 2026 to 2031.

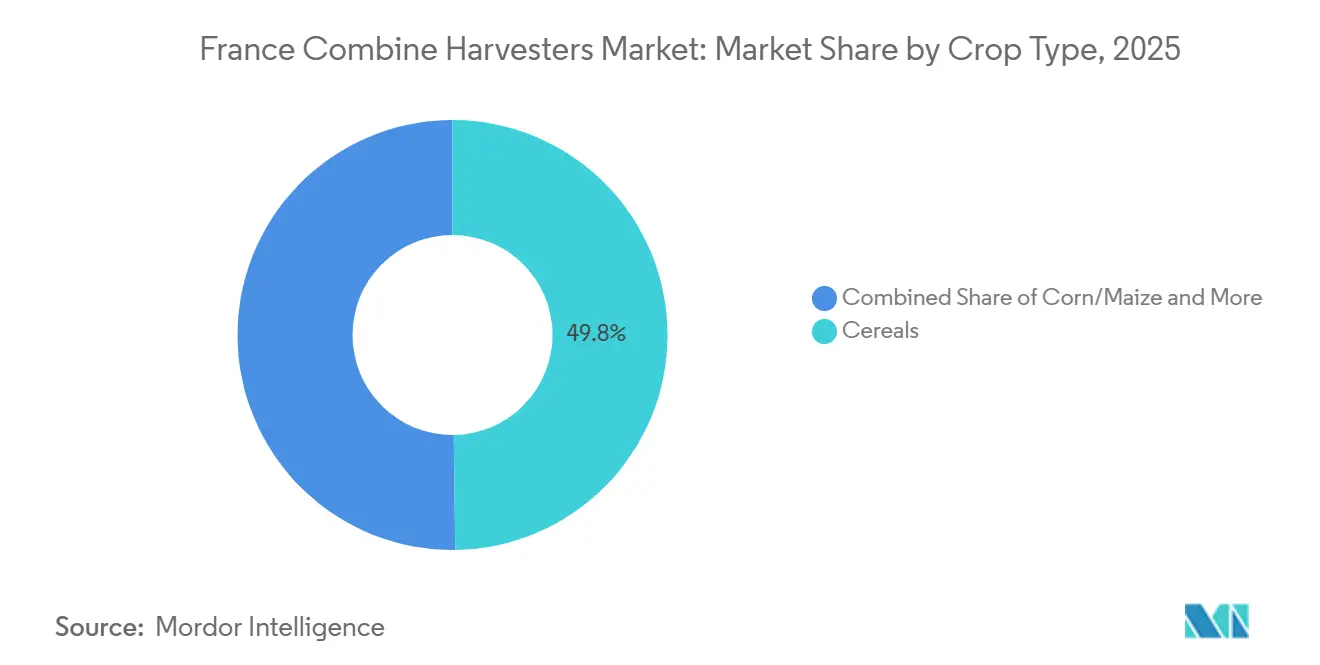

- By crop type, cereals accounted for the largest 49.8% share in 2025, whereas corn/maize is projected to expand at the fastest 5.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision agriculture adoption among French cereal growers | +0.8% | National, strongest in Hauts-de-France and Grand Est | Medium term (2-4 years) |

| Demand for high-horsepower harvesters on large farms | +0.7% | National, led by Hauts-de-France and Grand Est | Long term (≥ 4 years) |

| European Union Farm-to-Fork subsidies supporting machinery renewal | +0.6% | National, aligned with the Common Agricultural Policy | Short term (≤ 2 years) |

| Manufacturer financing programs for used equipment trade-ins | +0.5% | National, with higher uptake in Nouvelle-Aquitaine and Occitanie | Medium term (2-4 years) |

| Telematics adoption driving preventive maintenance demand | +0.4% | National, early adopters in northern cereal belt | Medium term (2-4 years) |

| Growth of custom harvesting contractors in Occitanie and Nouvelle-Aquitaine | +0.3% | Occitanie and Nouvelle-Aquitaine | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision Agriculture Adoption Among French Cereal Growers

The adoption of precision agriculture among French cereal growers is driving demand for advanced combine harvesters equipped with automation, telematics, and digital farm management systems. Farmers are increasingly utilizing connected harvesting equipment to enhance operational efficiency, lower fuel consumption, reduce crop losses, and optimize input usage during harvesting. Rising awareness of sustainable farming practices and data-driven agriculture is promoting investment in smart combine harvesters with real-time monitoring and precision harvesting capabilities.

Demand for High-Horsepower Harvesters on Large Farms

The demand for high-horsepower combine harvesters is rising among large farming operations in France, driven by the need for higher harvesting efficiency, faster field coverage, and minimized operational downtime during limited harvesting periods. Large cereal farms are increasingly utilizing combines with wider headers, larger grain tanks, automation systems, and advanced telematics to enhance productivity and reduce grain losses. Additionally, farm consolidation and the growing reliance on contractor-based harvesting services are boosting the demand for high-capacity harvesting equipment capable of efficient operation across extensive agricultural areas. Financing programs and the integration of precision farming technologies are further promoting the adoption of advanced high-horsepower combine harvesters in France.

European Union Farm-to-Fork Subsidies Supporting Machinery Renewal

The European Union's Farm-to-Fork strategy and Common Agricultural Policy (CAP) initiatives are driving machinery upgrades and the adoption of advanced combine harvesters in France. As per the European Commission, at least 25% of direct payment budgets under the CAP must be dedicated to eco-schemes that support environmentally sustainable agricultural practices and equipment modernization [1]Source: European Commission, “Eco-schemes – 25% of the direct payments are to be allocated to eco-schemes,” ec.europa.eu. This policy framework is encouraging farmers to replace outdated harvesting machinery with modern combines featuring precision farming systems, telematics, and low-emission technologies. Increased access to sustainability-linked funding and cooperative machinery investment models is boosting the demand for advanced harvesting equipment in France's key cereal-producing regions.

Manufacturer Financing Programs for Used Equipment Trade-Ins

Manufacturer financing programs are facilitating the replacement of combine harvesters and the modernization of fleets in France by enhancing machinery affordability for farmers and agricultural contractors. AGCO Finance reports supporting over 175,000 customers across more than 20 countries through customized agricultural equipment financing and flexible lease options [2]Source: AGCO Finance, “Tailored agricultural equipment financing and leasing solutions,” agcofinance.com. Financing solutions, including seasonal payment plans, operating leases, and trade-in support, are motivating growers and harvesting contractors to upgrade older combine harvesters to advanced machinery featuring automation and precision farming technologies. The availability of flexible financing is thus driving the adoption of modern harvesting equipment and enabling shorter fleet replacement cycles in France.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crop prices reducing capital expenditure plans | -0.6% | National, acute in northern cereal belt | Short term (≤ 2 years) |

| Aging farmer population limiting new machinery purchases | -0.5% | National, pronounced in Centre-Val de Loire | Long term (≥ 4 years) |

| Rural labor shortages delaying harvesting operations | -0.3% | Occitanie and Nouvelle-Aquitaine | Medium term (2-4 years) |

| Slow approval process for autonomous harvesters | -0.2% | Nationwide after Machinery Regulation 2023/1230 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crop Prices Reducing Capital Expenditure Plans

Volatile crop prices are causing uncertainty for cereal growers in France, restricting long-term capital investment in agricultural machinery and delaying the replacement of combine harvesters. Fluctuations in wheat and grain markets, coupled with high production costs and reduced export competitiveness, are diminishing farmer confidence in making significant equipment purchases. As a result, many growers are focusing on controlling operational costs and prolonging the service life of existing harvesting machinery rather than investing in new combines. The uncertain profitability environment is also driving increased dependence on contractor-based harvesting services and the used machinery market, particularly among small and medium-sized farms facing tighter financial constraints in key cereal-producing regions of France.

Aging Farmer Population Limiting New Machinery Purchases

Aging farmer demographics in France are constraining investments in new combine harvesters and increasing reliance on contractor-based harvesting services. Data from NAOS International indicates that 43% of French farmers were over 55 years old, underscoring the impact of an aging workforce on the agricultural sector [3]Source: NAOS International, “Anticipating retirements in the French agricultural sector,” naos-international.com. This demographic trend, coupled with succession challenges and the rising costs of machinery ownership, is prompting many farm operators to postpone purchasing new harvesting equipment. Additionally, land consolidation and a growing preference for outsourced harvesting services are contributing to a decline in direct combine ownership among smaller cereal growers in key agricultural regions of France.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Masks Niche Growth Share

The self-propelled segment is anticipated to account for 88.2% of the France combine harvesters market revenue in 2025, highlighting the preference of large cereal-producing farms for high-capacity harvesting equipment. These machines incorporate advanced powertrains, automation systems, and precision harvesting technologies, enabling efficient harvesting of extensive acreage within limited seasonal windows. Their ability to deliver higher throughput, reduce reliance on additional tractor units, and enhance operational efficiency has established them as the preferred choice in major agricultural regions. Ongoing investments in telematics and fleet management solutions further bolster adoption, maintaining the segment’s leading position in the market.

The PTO-powered combine segment is projected to grow at the fastest CAGR of 6.4% during 2026–2031, driven by demand from small and medium-sized farms seeking cost-effective harvesting solutions. These combines enable growers to utilize existing tractors, significantly lowering capital investment compared to self-propelled models. The segment is particularly appealing for mixed-crop operations, farms with seasonal harvesting needs, and operators aiming to maximize equipment utilization. Increasing interest in affordable mechanization, along with the availability of compact and lower-cost harvesting models, is projected to support steady growth and expand the segment’s presence in the France combine harvesters market.

By Power Output: Flagship Models Drive Premium Tier

France combine harvesters market share for the 150 to 300 HP segment accounted for the largest 48.6% in 2025, supported by widespread adoption across medium and large cereal farms operating in northern France. Farmers prefer this power range because it balances fuel efficiency, harvesting speed, and compatibility with conventional grain handling infrastructure. Equipment manufacturers continue introducing precision harvesting systems, automated threshing controls, and integrated telematics in this category to improve operational productivity. The segment also benefits from strong contractor demand, since machines within this range can efficiently handle wheat, barley, rapeseed, and maize harvesting applications across varied field conditions.

France combine harvesters market size for the above 450 HP segment is projected to expand at the fastest 6.8% CAGR from 2026 to 2031, driven by rising demand for high-capacity harvesting solutions among large agricultural contractors. Farmers increasingly prioritize rapid harvesting windows to minimize weather-related crop losses and labor dependency during peak harvesting seasons. Advanced combines within this category integrate larger grain tanks, wider headers, and intelligent automation technologies that improve throughput efficiency across extensive cereal fields. Strong adoption in regions cultivating irrigated maize and high-yield wheat varieties also supports growth. Manufacturers are strengthening financing and after-sales support programs to improve accessibility for premium harvesting equipment.

By Grain Tank Capacity: Logistics Optimization Favors Larger Tanks

The 6,000 to 9,000 L segment held the largest 43.2% of the France combine harvesters market share in 2025 because these grain tanks align effectively with conventional unloading cycles and regional transportation practices. Farmers prefer this segment due to its balance between operational efficiency, machine weight distribution, and fuel performance during harvesting. These combines are commonly used on wheat, barley, and rapeseed farms, where moderate field sizes dominate agricultural activities. Manufacturers are incorporating advanced grain monitoring systems, automated unloading controls, and improved residue handling technologies to enhance operational performance. Agricultural contractors also favor this segment for its flexibility in deployment across various crop applications.

The above 9,000 L segment market size is projected to grow at the fastest CAGR of 6.3% from 2026 to 2031, supported by increasing demand for high-capacity harvesting systems among commercial farming contractors. Larger grain tanks reduce unloading frequency, allowing operators to maintain harvesting continuity during peak seasonal operations. Farmers cultivating high-yield cereal and maize crops increasingly adopt these systems for improved logistical coordination with grain transport vehicles. Manufacturers are introducing features such as enhanced unloading speeds, radar-based fill monitoring systems, and integrated telematics platforms to boost operational productivity. Adoption is particularly strong among contractors managing extensive harvesting operations across multiple farms within compressed harvest periods.

By Drive Type: Track Configurations Address Soil Compaction

Wheel drive units commanded the largest 62.3% share of the France combine harvesters market in 2025 because they offer lower acquisition costs, easier maintenance requirements, and superior road mobility across dispersed agricultural fields. Farmers prefer wheel-driven combines due to their adaptability to diverse harvesting conditions and compatibility with existing transport infrastructure. These machines are in high demand, particularly in cereal-producing regions where frequent road travel between farms is necessary during harvesting seasons. Manufacturers are focusing on enhancing traction control systems, tire technology, and fuel efficiency in wheel-drive models to improve operational reliability.

Track drive are forecast to grow at the fastest 7.2% CAGR from 2026 to 2031, driven by increasing focus on soil protection and all-weather harvesting performance. Farmers in regions with heavy clay soils and high seasonal rainfall are increasingly opting for track systems due to their ability to minimize soil compaction and enhance field stability. Track-equipped combines also deliver higher operational efficiency in challenging harvesting conditions where wheeled systems face traction limitations. Manufacturers are developing lighter track assemblies, hybrid wheel-track systems, and advanced suspension technologies to improve field performance and operator comfort. The rising demand from agricultural contractors for premium harvesting capabilities further supports the long-term growth of this segment.

By Crop Type: Cereals Anchor Demand, Corn Gains Share

Cereals accounted for the largest 49.8% share of the France combine harvesters market in 2025 because wheat and barley remain dominant crops across major agricultural regions. Combine manufacturers continue optimizing threshing systems, residue management technologies, and grain quality monitoring solutions specifically for cereal harvesting applications. Farmers prioritize reliable harvesting performance to reduce crop losses during narrow seasonal windows influenced by changing weather conditions. Demand for combines within cereal cultivation areas also benefits from strong contractor activity and large-scale mechanized farming operations. Equipment utilization rates remain comparatively high in cereal production, supporting consistent replacement demand across established agricultural regions.

Corn/maize harvesting is projected to expand at the fastest 5.9% CAGR from 2026 to 2031, supported by increasing adoption of specialized row-crop harvesting equipment in irrigated farming regions. Farmers cultivating maize require high-capacity combines equipped with advanced corn headers, improved residue management systems, and stronger engine performance to manage intensive harvesting operations. Growth is particularly evident in southern and southwestern France where irrigated maize cultivation remains commercially significant. Manufacturers are introducing precision harvesting technologies that improve grain recovery efficiency and reduce field losses during maize harvesting. Rising contractor investments in multi-crop harvesting fleets also contribute to sustained segment development.

Geography Analysis

Hauts-de-France and Grand Est remain the leading regional markets for combine harvesters in France because these regions support extensive wheat and barley cultivation supported by large commercial farms. Farmers in these northern agricultural regions increasingly opt for high-capacity combines equipped with advanced telematics, precision harvesting systems, and wide cutter bars to enhance harvesting efficiency during limited weather windows. Additionally, strong contractor activity supports equipment replacement demand, as harvesting services are essential for medium-sized farms. The regional demand is further bolstered by high mechanization levels and consistent cereal production across expansive agricultural landscapes, necessitating efficient harvesting operations throughout seasonal crop cycles.

Nouvelle-Aquitaine and Occitanie continue witnessing rising demand for premium combine harvesters because irrigated maize and durum wheat cultivation require higher-powered harvesting systems. Agricultural contractors in these regions are increasingly investing in advanced combines with larger grain tanks, row-crop headers, and track drive systems to enhance productivity, particularly during wet harvesting conditions. Government-backed agricultural modernization initiatives and farm mechanization support programs further encourage equipment replacement among commercial farming operations. Additionally, the demand for precision harvesting technologies is rising as farmers seek improved fuel efficiency, reduced grain losses, and optimized performance across diversified crop cultivation systems.

Western regions including Bretagne, Normandie, and Pays de la Loire maintain stable demand for compact and mid-sized combine harvesters due to the prevalence of mixed farming operations and smaller field structures. Farmers in these areas prioritize harvesting equipment that offers operational flexibility, lower maintenance requirements, and efficient mobility between fragmented agricultural plots. The demand for conventional wheel-drive combines remains strong, as these machines support diverse crop harvesting applications while maintaining lower ownership costs. Agricultural contractors and mixed-crop farmers also favor adaptable combine configurations capable of operating efficiently across varying soil conditions and seasonal harvesting requirements in western France.

Competitive Landscape

The market is highly consolidated, with the top five companies, including Deere & Company, CNH Industrial N.V., AGCO Corporation, CLAAS KGaA mbH, and Kubota Corporation, maintaining strong competitive positions through integrated telematics ecosystems, financing capabilities, and extensive dealer support networks. Leading manufacturers are focusing on enhancing automation technologies and connected machinery platforms to improve harvesting efficiency for commercial farms and agricultural contractors. Additionally, companies are expanding predictive maintenance services, remote diagnostics systems, and flexible financing programs to bolster long-term customer retention. In France, demand for advanced digital harvesting solutions is rising as contractors and large cereal producers increasingly prioritize operational uptime, fuel efficiency, and data-driven farm management capabilities.

Asian manufacturers are gradually increasing their presence in the France combine harvesters market by introducing competitively priced harvesting equipment aimed at mixed farming operations and value-conscious buyers. Companies such as Zoomlion, Kubota, and Lovol are strengthening distribution partnerships and localized service capabilities to enhance market penetration in regional agricultural markets. These manufacturers are also investing in automation technologies, hybrid harvesting systems, and strategic collaborations to improve their competitiveness against established European and North American brands. While price-sensitive farmers are showing interest in lower-cost combine alternatives, challenges such as limited aftersales support infrastructure and spare parts logistics continue to hinder broader adoption among professional contractor fleets.

Agricultural contractors in southwestern France are a significant competitive focus, as these buyers emphasize operational reliability, prompt service responsiveness, and long-term maintenance support during seasonal harvesting periods. Manufacturers are investing in harvesting automation, precision agriculture technologies, and connected machinery to enhance operational efficiency in large-scale farming. Companies are also expanding predictive diagnostics, remote monitoring systems, and tailored aftersales service programs to maximize equipment uptime and improve customer retention. Additionally, flexible financing options, extended maintenance agreements, and robust dealer support networks continue to be critical competitive strategies in the France combine harvesters market.

France Combine Harvesters Industry Leaders

Deere & Company

CNH Industrial N.V.

CLAAS KGaA mbH

AGCO Corporation

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CLAAS KGaA mbH introduced the LEXION 8500 combine harvester featuring APS SYNFLOW HYBRID threshing technology, enhanced throughput performance, and upgraded connectivity features.

- January 2026: Deere & Company announced new models for the X9 and S7 combine harvesters, featuring expanded Harvest Settings Automation, larger grain tank configurations, and predictive ground speed automation. These enhancements aim to improve harvesting productivity and operational efficiency for large-scale cereal farms.

- July 2025: CLAAS KGaA mbH announced the launch of upgraded LEXION combine harvesters, featuring larger grain tanks, enhanced engine performance, and improved cab systems, in preparation for the 2026 harvesting season.

France Combine Harvesters Market Report Scope

A combine harvester is an agricultural machine that performs multiple harvesting tasks, including reaping, threshing, and grain cleaning, in a single operation. It is commonly used for harvesting cereal crops such as wheat, barley, corn, rice, and oats, enhancing efficiency, reducing labor needs, and minimizing crop losses during field operations. The France Combine Harvesters Market Report is Segmented by Type (Self-Propelled, Tractor-Pulled Combine, and and More), by Power Output (Less Than 150 HP, 150 To 300 HP, 301 To 450 HP, and More), by Grain Tank Capacity (Less Than 6, 000 L, 6, 000 To 9, 000 L, and More), by Drive Type (Wheel Drive and Track Drive), and by Crop Type (Cereals, Corn/Maize, and Other Crops). The Market Forecasts are Provided in Terms of Value (USD).

| Self-Propelled |

| Tractor-Pulled Combine |

| PTO-Powered Combine |

| Less than 150 HP |

| 150 to 300 HP |

| 301 to 450 HP |

| Above 450 HP |

| Less than 6,000 L |

| 6,000 to 9,000 L |

| Above 9,000 L |

| Wheel Drive |

| Track Drive |

| Cereals |

| Corn / Maize |

| Oilseeds |

| Other Crops |

| By Type | Self-Propelled |

| Tractor-Pulled Combine | |

| PTO-Powered Combine | |

| By Power Output | Less than 150 HP |

| 150 to 300 HP | |

| 301 to 450 HP | |

| Above 450 HP | |

| By Grain Tank Capacity | Less than 6,000 L |

| 6,000 to 9,000 L | |

| Above 9,000 L | |

| By Drive Type | Wheel Drive |

| Track Drive | |

| By Crop Type | Cereals |

| Corn / Maize | |

| Oilseeds | |

| Other Crops |

Key Questions Answered in the Report

How large is the France combine harvesters market in 2026?

The France combine harvesters market size stands at USD 469.0 million in 2026.

What is the projected growth rate for combines above 450 HP?

Combines in the above 450 HP segment are projected to grow at the fastest 6.8% CAGR between 2026 and 2031.

What share do self-propelled combines currently hold in France?

Self-propelled units accounted for the largest 88.2% of French combine sales in 2025.

What role do custom harvesting contractors play in France?

Contractors already service thousands of hectares in the southwest, and grants plus labor shortages are accelerating their share of harvested area each season.

Page last updated on: