Europe Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.22 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

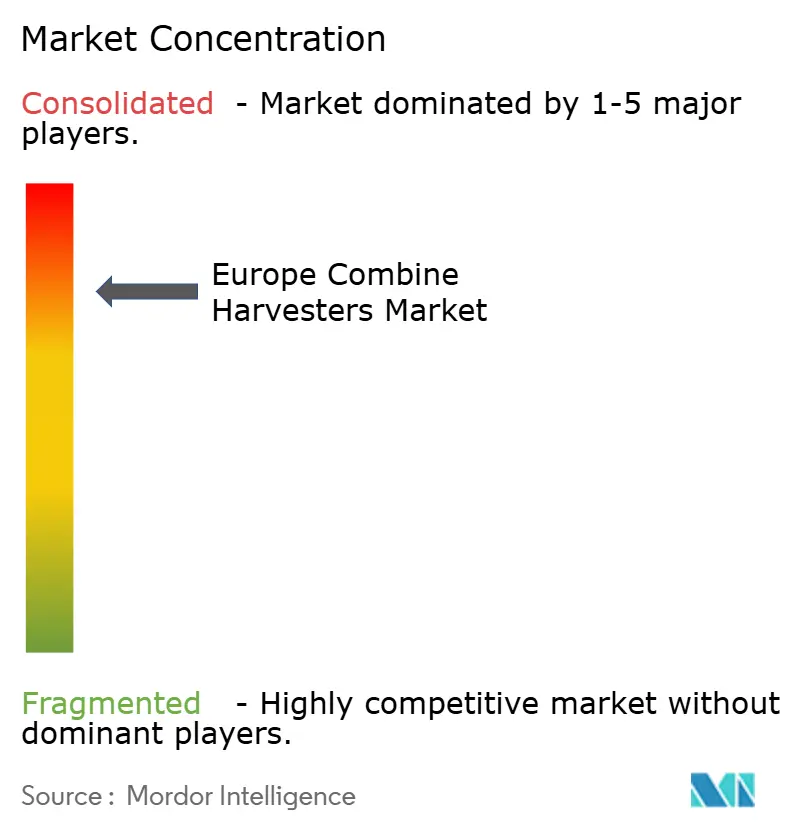

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Combine Harvesters Market Analysis by Mordor Intelligence

The Europe combine harvesters market size was valued at USD 1.22 billion in 2025 to USD 1.28 billion in 2026, and reach USD 1.59 billion by 2031, growing at a CAGR of 4.50% over the forecast period (2026-2031). The Europe combine harvesters market is experiencing a structural shift as Western European farmers replace aging diesel-powered equipment to meet stricter emission standards. Simultaneously, Eastern European farming cooperatives are pooling financial resources to modernize their harvesting operations. Self-propelled combine harvesters remain dominant due to their ability to perform harvesting, threshing, and grain cleaning in a single operation. However, smaller farmers in countries such as Poland and Romania are extending the operational life of tractor-pulled and PTO-powered machines during 2024-2025 to manage costs effectively. Manufacturers are increasingly focusing on hybrid-electric harvesting technologies as sustainability regulations and carbon reduction initiatives drive demand for lower-emission agricultural machinery. Despite strong competition among leading manufacturers, the market remained highly consolidated, with major brands navigating softer farm income conditions and cautious machinery spending across Europe.

Key Report Takeaways

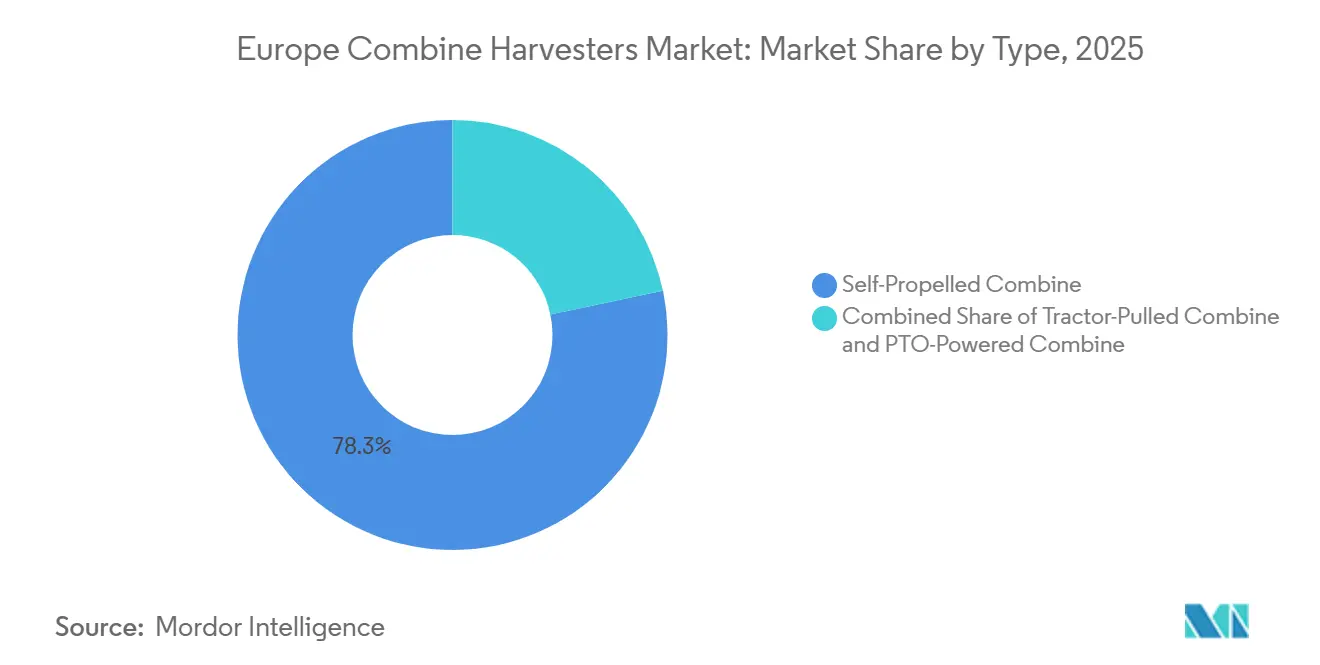

- By type, self-propelled combines held the largest share of the Europe combine harvesters market size at 78.3% in 2025, while the PTO-powered combine harvesters segment is projected to record the fastest CAGR of 7.9% during 2026-2031.

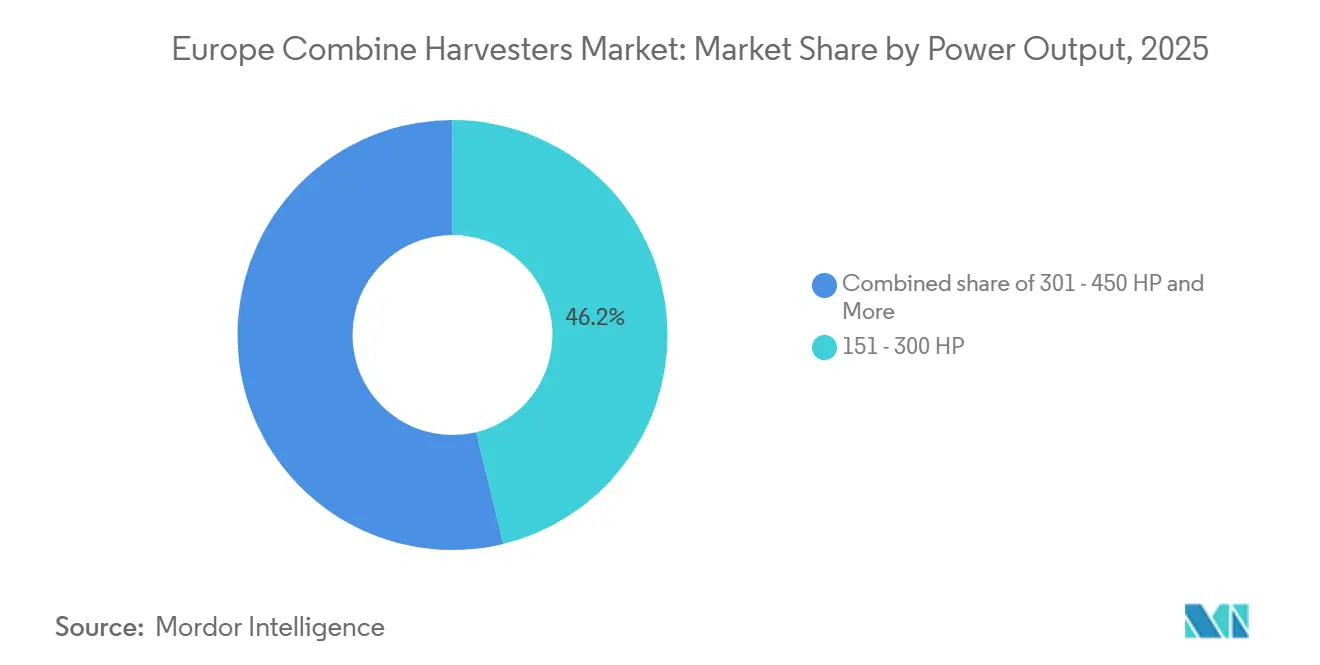

- By power output, the 151-300 horsepower segment held the largest share of the European combine harvesters market at 46.2% in 2025, whereas the above-450 horsepower segment is projected to grow at the fastest CAGR of 8.2% during 2026-2031.

- By geography, Germany accounted for the largest share of the Europe combine harvesters market size at 21.5% in 2025, while Poland is projected to witness the fastest CAGR of 6.5% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortage and rising farm-labor costs | +1.20% | Germany, France, United Kingdom, Poland, and Spain | Medium term (2-4 years) |

| EU Common Agricultural Policy subsidies for mechanization | +1.50% | Poland, Romania, Bulgaria, Italy, and Spain | Short term (≤ 2 years) |

| Stage V emission norms accelerating fleet replacement | +1.30% | EU-wide with focus on Germany, France, and Netherlands | Short term (≤ 2 years) |

| Precision-farming and telematics integration | +1.40% | Germany, United Kingdom, France, and Denmark | Medium term (2-4 years) |

| Adoption of track-based combines to cut soil compaction | +0.80% | United Kingdom, Netherlands, and Denmark | Long term (≥ 4 years) |

| Rise of machinery-sharing cooperatives in Eastern Europe | +0.60% | Poland, Romania, Hungary, and Czech Republic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortage and Rising Farm-Labor Costs

Increasing agricultural labor costs and ongoing worker shortages are driving the adoption of mechanization in the European combine harvesters market. In Northern Ireland, agricultural wage rates are due to rise from 1 April 2026, with official minimum hourly rates set at (£8.00 to £14.44), about USD 10.80 to USD 19.49 depending on age and grade, according to the Agricultural Wages Board [2]Source: Northern Ireland Agricultural Wages Board, “Minimum Wage Rates 2026,” daera-ni.gov.uk. These revised rates apply to agricultural workers covered under the Agricultural Wages (Regulation) Order in Northern Ireland. Additionally, Eurostat reported continued labor-cost inflation across Europe in 2025, with labor costs increasing by 8.8% in Poland and 10.6% in Romania, as wages in Eastern Europe gradually align with those in Western Europe. These developments are prompting farmers to invest in combine harvesters to improve harvesting efficiency, reduce reliance on seasonal labor, and ensure timely crop harvesting in large-scale farming operations.

EU Common Agricultural Policy Subsidies for Mechanization

Financial support programs under the Common Agricultural Policy are reducing purchasing barriers for combine harvesters in several European countries by subsidizing a significant portion of machinery investment costs in developing agricultural regions. Poland expanded its agricultural machinery financing programs in 2025, facilitating increased equipment purchases and fleet modernization among medium- and large-scale farms. Similarly, Romania increased grant approvals for agricultural machinery investments. However, lengthy administrative processing timelines have led many farmers to rely on bridge financing and commercial loans before receiving subsidies. Variations in subsidy timing, financing access, and loan availability continue to influence short-term machinery purchasing cycles and replacement demand patterns in the European combine harvesters market.

Stage V Emission Norms Accelerating Fleet Replacement

Stricter Stage V emission regulations across Europe are driving replacement demand for newer combine harvesters equipped with advanced low-emission engine technologies and integrated exhaust after-treatment systems [3]Source: European Commission, “Stage V Emission Standards,” ec.europa.eu. Older Tier 3 machines are being phased out as retrofit upgrades prove economically unfeasible for aging equipment fleets. In response, manufacturers are introducing new-generation Stage V combine harvesters featuring precision agriculture and fuel-efficiency technologies. These advancements enable farmers to enhance operational performance while adhering to evolving environmental compliance standards in the European combine harvesters market.

Precision-Farming and Telematics Integration

Precision farming and telematics technologies are transforming combine harvesters from standalone harvesting equipment into integrated, data-driven farm management systems across Europe. Leading manufacturers are incorporating connected platforms, predictive maintenance features, real-time yield monitoring, and high-accuracy autonomous guidance technologies into new combine models to improve harvesting efficiency and reduce operational waste. The adoption of digital agriculture tools, including GPS-guided machinery, field sensors, satellite-based monitoring, and farm management software platforms, enables combine harvesters to generate and integrate real-time field data, facilitating more precise harvesting decisions and resource management. Adoption rates are notably higher among younger farmers who are more familiar with digital agriculture technologies, while older farming populations demonstrate a comparatively slower uptake. As generational transitions in farm ownership occur and the adoption of precision agriculture expands, the demand for advanced, telematics-enabled, and precision-guided combine harvesters is projected to grow further in the European combine harvesters market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High purchase and maintenance costs | -1.80% | All Europe, acute in Italy, Spain, and Greece | Short term (≤ 2 years) |

| Commodity-price volatility dampening capital expenditure | -1.50% | Grain regions in France, Germany, and Poland | Short term (≤ 2 years) |

| Shortage of service technicians for advanced electronics | -0.90% | Germany, Belgium, Netherlands, and Poland | Medium term (2-4 years) |

| Grid limitations slowing electric and hybrid uptake | -0.60% | Rural Eastern Europe and other underserved areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity Price Volatility Dampening Capital Expenditure

Fluctuating grain and wheat prices across Europe are creating uncertainty in farm profitability and cash flows, prompting farmers to delay investments in new combine harvesters. According to the European Commission's Short-Term Outlook, EU cereal production is projected to reach approximately 280 million tonnes in 2025/26, up around 4.1% year-over-year[1]Source: European Commission, “Short-term outlook of EU agricultural markets,” ec.europa.eu. This growth is projected to improve supply conditions but will also continue to exert pressure on grain prices. Despite a recovery in production volumes, lower commodity prices and uncertainty about farm returns have weakened purchasing confidence in high-value harvesting equipment. Consequently, many farmers are focusing on managing operational costs rather than replacing machinery, leading to reduced order activity and postponed capital expenditure decisions in the European combine harvesters market.

Shortage of Service Technicians for Advanced Electronics

The growing adoption of telematics, automation, and precision farming technologies in combine harvesters is driving demand for skilled agricultural machinery technicians across Europe. Many countries are experiencing shortages of qualified service professionals capable of addressing advanced electronic, sensor, and software-related issues in modern harvesting equipment. This limited availability of technicians is leading to extended repair times and increased equipment downtime during critical harvesting periods. These challenges underscore the importance of dependable aftersales service networks in the European combine harvesters market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Masks Niche Growth

Self-propelled combines are projected to account for 78.3% of the Europe combine harvesters market share in 2025. This dominance is driven by their widespread adoption on medium- and large-scale farms, where they enhance harvesting efficiency by combining harvesting, threshing, and grain cleaning into a single operation. Leading manufacturers, including Deere & Company and Claas KGaA mbH, are continuously improving self-propelled combines with features such as GPS steering, precision farming technologies, and real-time yield monitoring systems. In contrast, the PTO-powered segment is projected to achieve the fastest CAGR of 7.9% during 2026-2031. This growth is attributed to increasing demand from small- and medium-sized farms in Eastern European countries like Poland and Romania, where farmers prioritize lower capital investment and compatibility with existing tractor infrastructure.

The market is also experiencing rising demand for compact and mid-range combine harvesters, which cater to smaller farm operations seeking mechanized harvesting solutions at reduced ownership costs. PTO-powered combines remain attractive to price-sensitive farmers due to their simpler maintenance requirements and operational flexibility with existing tractors. However, their adoption among large commercial farming operations across Europe is limited by lower harvesting productivity and the lack of advanced automation technologies.

By Power Output: High-Horsepower Surge Driven by Contractors

The 151 - 300 horsepower segment accounted for 46.2% of the Europe combine harvesters market share in 2025. This dominance is attributed to its suitability for medium-sized farms across Europe, where farmers prioritize balanced harvesting capacity, fuel efficiency, and operational versatility. Leading manufacturers such as Deere & Company and AGCO Corporation are strengthening this segment by offering combine harvesters with larger grain tanks, wider headers, and advanced harvesting technologies. In contrast, the above 450 horsepower segment is projected to register the fastest CAGR of 8.2% during 2026-2031. This growth is driven by increasing demand from agricultural contractors and large-scale farming operations seeking higher throughput capacity and improved harvesting efficiency during narrow harvesting windows.

Manufacturers are introducing high-capacity combine harvesters with advanced automation, precision farming integration, and enhanced grain-handling efficiency to support large commercial farming operations. Countries such as Germany, France, and the United Kingdom are driving demand for high-horsepower combine harvesters due to larger average farm sizes and greater adoption of contractor-based harvesting services. However, higher equipment costs and elevated maintenance requirements continue to limit adoption among smaller farms within the Europe combine harvesters market.

Geography Analysis

Germany is projected to account for the largest share of the Europe combine harvesters market, holding 21.5% in 2025. This leading position is supported by the country's extensive arable land, high levels of farm mechanization, and widespread use of advanced harvesting equipment in large-scale grain farming operations. Germany also benefits from a well-established agricultural machinery industry, strong dealer and service networks, and the increasing adoption of precision agriculture technologies that enhance harvesting efficiency and productivity. However, machinery purchasing activity remained cautious during 2024-2025 due to fluctuating crop prices and uncertain farm profitability, which delayed new equipment investments across many farming operations.

Poland is projected to be the fastest-growing market, with a CAGR of 6.5% during 2026-2031. This growth is supported by expanding agricultural machinery financing programs and increasing mechanization adoption among medium-sized farms. France holds the second-largest share of the European combine harvesters market. Demand is primarily driven by large-scale grain farms in the Paris Basin, which require high-capacity combine harvesters to improve harvesting efficiency and minimize grain losses, particularly in wheat and barley cultivation. The United Kingdom also represents a significant market, although growth remains moderate due to evolving agricultural policy frameworks and uncertainties surrounding subsidies following post-Brexit reforms.

In Southern Europe, countries such as Italy and Spain are driving market growth through demand for specialized combine harvesters for rice, corn, and sunflower harvesting. Additionally, countries like Romania, Hungary, and the Czech Republic are benefiting from machinery-sharing models and European Union funding. These factors are facilitating first-time adoption of combine harvesters and accelerating agricultural mechanization in developing farming regions across Europe.

Competitive Landscape

The Europe combine harvesters market is projected to remain highly concentrated by 2025. Key players in the market include Deere & Company, Claas KGaA mbH, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation. Deere & Company and Claas KGaA mbH hold strong positions due to their extensive dealer networks, advanced harvesting technologies, and diverse product portfolios across Western Europe. CNH Industrial N.V. emphasizes high-capacity rotary combine harvesters designed to enhance harvesting efficiency and throughput. AGCO Corporation leverages Fendt’s premium positioning in Germany and Massey Ferguson’s strong presence in Southern Europe, while Kubota Corporation focuses on compact combine harvesters tailored for Nordic and Eastern European markets.

Technological innovation remains a critical competitive factor in the Europe combine harvesters market. Deere & Company is incorporating machine learning, automation, and precision farming technologies into its combine harvesters to enhance efficiency and minimize grain losses. Claas KGaA mbH is prioritizing hybrid harvesting technologies and fuel-efficiency improvements to align with sustainability goals and reduce operating costs. Manufacturers are also increasing investments in autonomous navigation, telematics, and connected harvesting platforms to meet the growing demand for digital agricultural machinery across Europe.

Strategic acquisitions and product development initiatives are reshaping the competitive landscape of the Europe combine harvesters market. Tera Yatırım Teknoloji Holding A.Ş. (Sampo Rosenlew) is enhancing its regional presence following the acquisition of Sampo Rosenlew Oy. Additionally, manufacturers are expanding investments in hybrid propulsion systems and precision harvesting technologies. Smaller manufacturers are focusing on compact combine harvester offerings and cost-effective solutions aimed at medium- and small-scale farming operations in Eastern and Southern Europe.

Europe Combine Harvesters Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Claas KGaA mbH

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: CLAAS strengthened its harvesting equipment portfolio by expanding its combine harvester lineup with the latest LEXION 8000 series and TRION 760 models, while continuing investments in digital farming solutions through the CLAAS connect platform. The company also invested approximately (EUR 319.9 million) USD 346 million in research and development during 2025, reflecting the growing focus on precision agriculture, connectivity, and advanced harvesting technologies. These developments are projected to support technological innovation and replacement demand in the European combine harvesters market.

- September 2025: Tera Yatırım Teknoloji Holding A.Ş. acquired Finland-based combine harvester manufacturer Sampo Rosenlew Oy from Mahindra & Mahindra Ltd. This strategic acquisition is projected to strengthen Tera Yatırım Teknoloji Holding A.Ş.’s presence across the Europe combine harvesters market by expanding its manufacturing capabilities, product portfolio, and regional market reach within the agricultural machinery industry.

- April 2025: CNH Industrial N.V. completed a USD 170 million modernization of its Zedelgem, Belgium facility for production of the New Holland CR11 combine harvester. The completed investment strengthened Europe’s combine harvester manufacturing capabilities through advanced automation, higher production efficiency, and expanded export capacity, reinforcing the region’s position in technologically advanced agricultural machinery manufacturing.

Europe Combine Harvesters Market Report Scope

A combine harvester, commonly known as a combine, is a large agricultural machine used to harvest grain and seed crops. It combines multiple harvesting operations in a single process, including reaping, threshing, and cleaning, thereby improving harvesting efficiency and reducing labor requirements.

The Europe Combine Harvesters Market Report is Segmented by Type (Self-Propelled Combine, Tractor-Pulled Combine, and PTO-Powered Combine), by Power Output (Less Than 150 HP, 151 - 300 HP, 301 - 450 HP, and Above 450 HP), and by geography (Germany, France, United Kingdom, Italy, Poland, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Self-Propelled Combine |

| Tractor-Pulled Combine |

| PTO-Powered Combine |

| Less Than 150 HP |

| 151 - 300 HP |

| 301 - 450 HP |

| Above 450 HP |

| Germany |

| France |

| United Kingdom |

| Italy |

| Poland |

| Spain |

| Rest of Europe |

| By Type | Self-Propelled Combine |

| Tractor-Pulled Combine | |

| PTO-Powered Combine | |

| By Power Output | Less Than 150 HP |

| 151 - 300 HP | |

| 301 - 450 HP | |

| Above 450 HP | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Poland | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe combine harvesters market?

The Europe combine harvesters market size stands at USD 1.28 billion in 2026 and is on course to reach USD 1.59 billion by 2031.

How fast is the market projected to grow by 2031?

The market is projected to register a 4.50% CAGR between 2026 and 2031, driven by replacement demand and precision-farming adoption.

Which combine type dominates sales in Europe?

Self-propelled combines account for 78.3% of 2025 revenue due to their one-pass harvesting efficiency.

Which power class is expanding the quickest?

Models above 450 horsepower are forecast to grow at an 8.2% CAGR as contractors seek higher throughput.

Page last updated on: