Germany Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

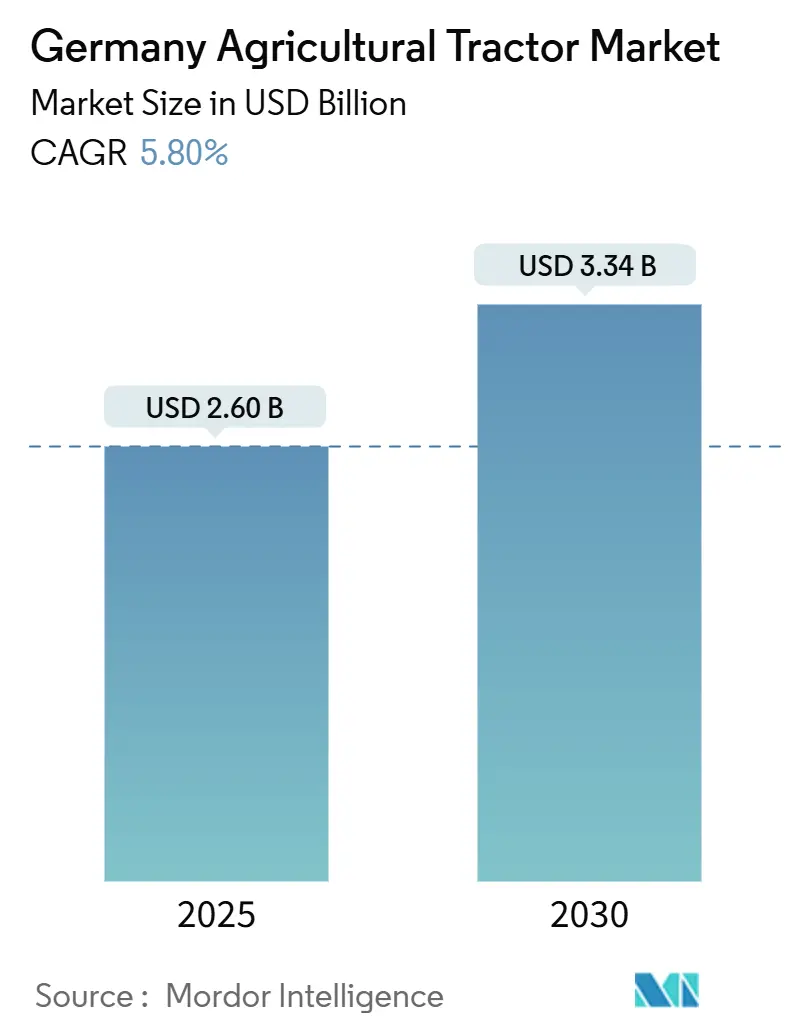

| Market Size (2025) | USD 2.60 Billion |

| Market Size (2030) | USD 3.34 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

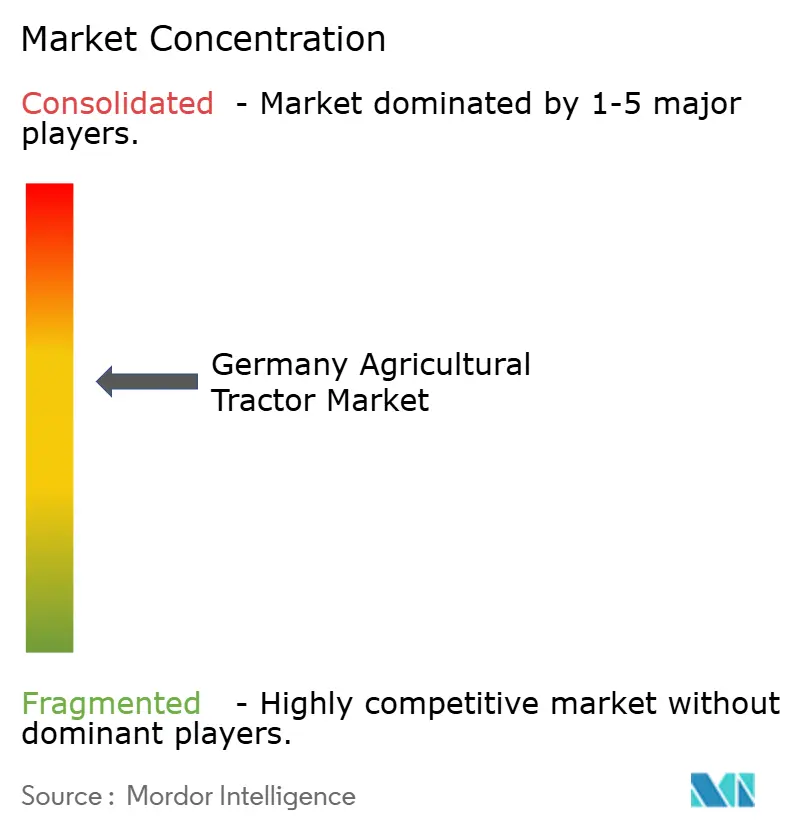

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Agricultural Tractor Market Analysis by Mordor Intelligence

Germany agricultural tractor market size reached USD 2.60 billion in 2025 and is projected to advance to USD 3.34 billion by 2030, reflecting a 5.80% CAGR. Rising demand for high-horsepower units, precision-farming subsidies, and electrification incentives underpin the positive outlook. Farm consolidation has shifted registrations toward platforms exceeding 150 horsepower, while subsidies tied to the Common Agricultural Policy (CAP) reduce the effective cost of GPS-guided, Stage V-compliant machinery. Simultaneously, labor shortages and a rapidly aging workforce encourage the adoption of autonomous and driver-assist technologies. Export strength cushions domestic cyclicality, enabling German original-equipment manufacturers to maintain elevated R&D budgets. However, capital-cost inflation, uneven rural charging infrastructure, and credit tightening temper near-term growth momentum.

Key Report Takeaways

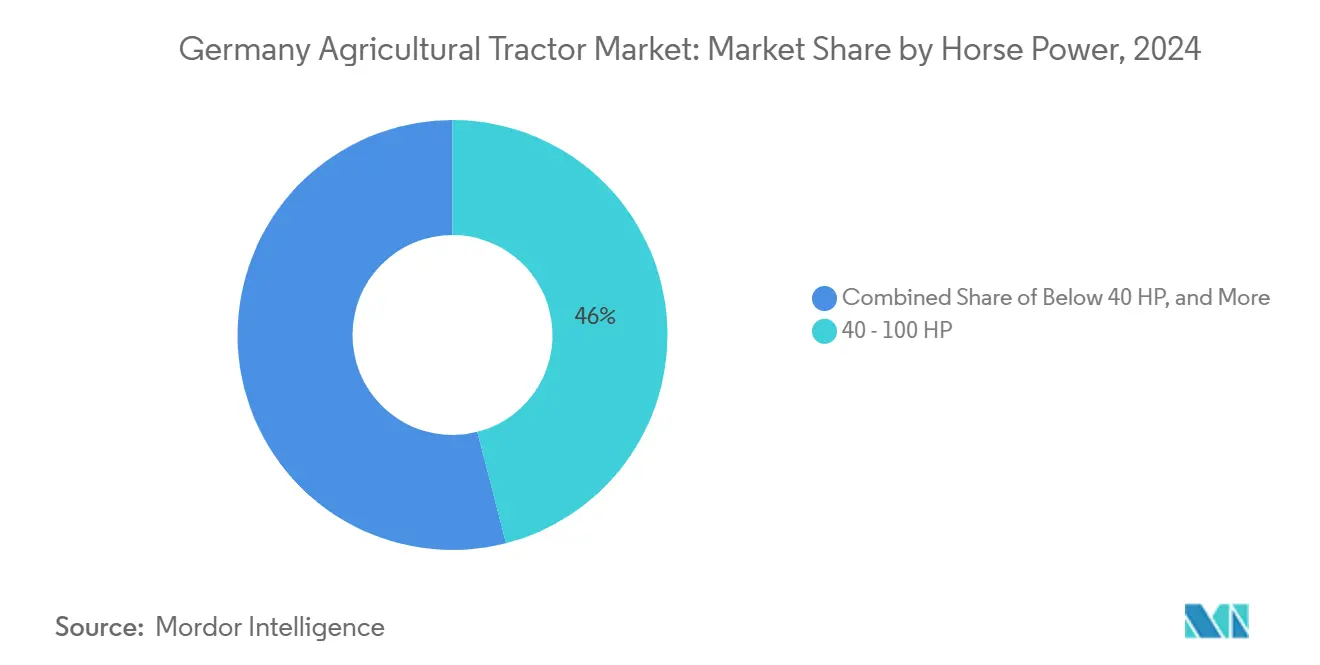

- By horsepower, the 40-100 HP band held 46% of Germany agricultural tractor market share in 2024, while the above 100 HP segment is projected to expand at a 6.8% CAGR through 2030.

- By tractor type, utility tractors accounted for 42% of the Germany agricultural tractor market size in 2024. Row-crop platforms are forecast to grow at an 8.3% CAGR through 2030.

- By drive type, two-wheel-drive units accounted for 67% of the market share in 2024, whereas autonomous or driverless platforms are projected to rise at a 12% CAGR through 2030.

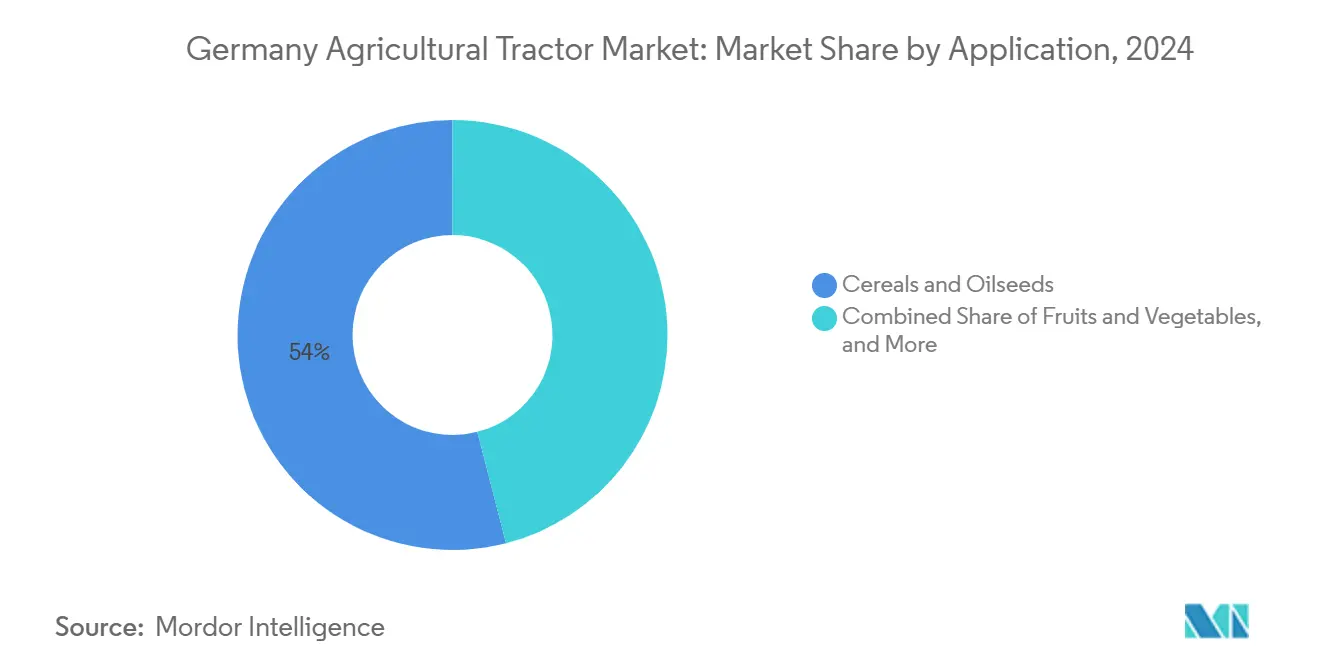

- By application, cereals and oilseeds accounted for 54% of Germany agricultural tractor market size in 2024, while fruits and vegetables are forecast to expand at a 7.2% CAGR through 2030.

Germany Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages accelerating mechanization | +1.2% | Germany and broader EU-27 | Medium term (2–4 years) |

| CAP and national subsidies for precision farming | +1.5% | Germany, France, and Netherlands | Short term (≤ 2 years) |

| Electrification incentives for e-tractors | +0.8% | Germany, Austria, and Nordics | Long term (≥ 4 years) |

| Rising demand for higher-horsepower models | +1.0% | Germany, Poland, and France | Medium term (2–4 years) |

| Export strength of German OEMs | +0.6% | Germany with global order books | Short term (≤ 2 years) |

| Tech convergence enabling autonomy | +0.7% | Germany, Netherlands, and Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages Accelerating Mechanization

Germany requires about 43,000 additional farmworkers annually, yet fewer than 15,000 trainees enter the field, resulting in an average farmer age of 56 [1]Source: Bundesagentur für Arbeit, “Fachkräfteengpass in der Landwirtschaft 2024,” arbeitsagentur.de. Operators are increasingly substituting capital for labor, favoring tractors with horsepower above 150 that cover more hectares per hour. Autonomous concepts, such as Fendt’s Xaver GT, allow one supervisor to manage multiple units, reducing labor input per hectare by about 30%. Federal funding of USD 128 million through 2027 accelerates digital-farming pilots, emphasizing automation [2]Source: Bundesministerium für Wirtschaft und Energie, “Elektromobilität in der Landwirtschaft,” bmwi.de. Manufacturers are increasingly bundling telematics and predictive maintenance, which reduces on-site technician visits and further eases labor pressure.

CAP and National Subsidies for Precision Farming

The Common Agricultural Policy (CAP) Strategic Plan channels USD 6.6 billion annually to Germany, including USD 990 million for modern equipment [3]Source: European Commission, “Common Agricultural Policy Strategic Plan: Germany,” ec.europa.eu. Eco-schemes reimburse up to 40% of precision farming spend, effectively reducing the net price of a GPS-equipped tractor by USD 16,000 - 27,000. Uptake reached 62% of eligible farms in 2024, well above the EU-European Union average, helping Germany agricultural tractor market uptake of factory-integrated guidance stacks. AGCO’s April 2024 PTx Trimble joint venture integrates Trimble software into Fendt units, enabling buyers to claim full subsidies without requiring retrofits. Subsidy funds are front-loaded into 2025 - 2026, prompting Original Equipment Manufacturers (OEMs) to offer zero-interest financing aligned with payment schedules.

Electrification Incentives for E-Tractors

An exclusive USD 1.07 billion pool for zero-emission farm equipment covers as much as 50% of the premiums for battery-electric tractors through 2028. Fendt’s e107 V Vario, priced at USD 160,000, qualifies for subsidies covering half the cost. Deere & Company's E-Power platform brings an 800-volt, 195 kWh architecture to cereal operations. Yet, fewer than 200 rural fast chargers with capacities above 150 kW hinder adoption. OEMs hedge their bets with diesel-hybrid variants to capture subsidies without relying fully on charging infrastructure.

Tech Convergence Enabling Autonomy

Germany’s rural 5G coverage climbed to 78% in 2024, creating the backbone for cloud-connected, driverless operations. Fendt’s Xaver GT logged 2,000 test hours and targets commercial release by 2026, while Deere & Company's See and Spray vision system reduces herbicide use up to 70%. Regulatory proposals would legalize fully autonomous machines operating at speeds of up to 40 km/h on rural roads by 2026. Interoperability challenges are being addressed as PTx Trimble licenses a FieldDataSync protocol to third-party implementers. Autonomous traction is likely to scale up once legal, insurance, and communication barriers are eased.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital costs for small farms | -0.90% | Germany and Southern Europe | Short term (≤ 2 years) |

| Skilled-operator and technician shortage | -0.60% | Germany and European Union | Medium term (2–4 years) |

| Credit tightening and volatile commodity prices | -0.70% | Germany, France, and Poland | Short term (≤ 2 years) |

| Rural charging and connectivity gaps | -0.40% | Germany, Austria, and Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Costs for Small Farms

The average new tractor costs nearly USD 100,000, with Stage V engines adding USD 8,500–12,800 per unit. Sixty percent of German farms operate below 50 hectares, generating annual revenues under USD 53,000 and struggling to secure co-financing despite 40% CAP reimbursements. Leasing penetration rose to 35% in 2024, but higher rates lifted monthly payments by 26% versus 2021. Dealers report that trade-in values for pre-Stage V units have fallen 20–30%. The barrier widens the performance gap between capital-rich enterprises and smallholders, eroding mid-range demand in Germany agricultural tractor market.

Credit Tightening and Volatile Commodity Prices

The European Central Bank cut its deposit rate to 3.0% in 2024, yet banks still demand lower loan-to-value ratios and higher coverage metrics. Wheat futures oscillated between (EUR 250) USD 266 and (EUR 210) USD 224 per metric ton in 2024. Replacement cycles stretched from eight to ten years as farmers prioritized repairs over new purchases, resulting in a reduction of about 2,000-3,000 units in annual demand. OEM zero-interest promotions tied to CAP payouts may front-load sales but risk a demand cliff once subsidies subside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Horsepower: Consolidation Rewards High-Capacity Platforms

The 40-100 HP accounted for about 46% of Germany agricultural tractor market size in 2024, but units above 100 HP are growing faster at 6.8% annually, steering Germany agricultural tractor market size toward high-power platforms. Tractors above 150 HP rose in 2024, driven by farms larger than 1,000 hectares seeking 12-meter seeders and 18-meter sprayers that lower field passes and labor needs.

Large-scale operators amortize Stage V premiums across wider hectares, prompting OEMs to invest in higher-output ranges like Fendt’s 900 Vario, which increased registrations in 2024. Mid-size operators explore electric alternatives such as the e107 V Vario whose post-subsidy price undercuts comparable diesel versions. The horsepower mix will keep polarizing as R&D flows to premium power and sub-50 HP niche electrics, while mid-range offerings stagnate.

By Tractor Type: Row-Crop Gains Under Controlled-Traffic Farming

Utility tractors held a 42% of Germany agricultural tractor market share in 2024, yet row-crop tractors are forecast to grow at CAGR 8.3% through 2030, the quickest within Germany agricultural tractor market. Wider implements and controlled-traffic farming require high clearance and narrow track widths that row-crop designs deliver. Deere & Company’s 8R and 9R series captured incremental demand in large cereal belts owing to integrated guidance and adjustable tracks.

CLAAS’s Axion 900 combines row-crop ergonomics with utility versatility, boosting share through mid-mount linkages and dual-implement setups. Orchard and vineyard tractors remain vital in wine regions demanding low-profile architectures. Municipal adoption of electric compacts expands the other segment. Utility tractors may cede ground to row-crop units as farms scale up and OEMs offer configurable packages within a single chassis.

By Drive Type: Autonomy Reshapes Traction

Two-wheel-drive accounted for 67% of the Germany agricultural tractor market share in 2024, favored for low cost and simple maintenance, yet autonomous or driverless platforms lead growth with a 12% CAGR to 2030. Fendt’s Xaver GT and Deere & Company’s E-Power exemplify the pivot to software-defined traction, employing swarm models and vision-guided spraying.

Four-wheel-drive growth lags at 5.2% as autonomy delivers traction management via independent wheel motors rather than mechanical drivelines. Legal, insurance, and protocol barriers remain, but draft Road Traffic Act changes promise commercial viability by 2026. Two-wheel-drive dominance will gradually erode once regulatory hurdles fall and cost of sensors declines.

By Application: Cereals Dominate, Horticulture Accelerates

Cereals and oilseeds represented 54% of the market share in 2024, maintaining Germany agricultural tractor market demand focus on staple crops. While wheat acreage decreased, maize cultivation expanded, leading to a shift in horsepower requirements toward tractors exceeding 150 HP to accommodate heavier implements. Additionally, the increase in sugar beet cultivation supported the demand for advanced equipment, including variable-rate seeders.

Fruits and vegetables are projected to grow 7.2% annually as orchard-specific autonomous units mitigate labor shortages in steep-slope vineyards. Livestock operations drive demand via feeding and manure tasks requiring versatile utility tractors. Municipal, forestry, and specialty niches grow modestly as cities procure low-noise, zero-emission equipment. Cereals will remain dominant but gradually lose share to horticulture and livestock, adopting automation sooner.

Geography Analysis

Germany’s eastern Länder, particularly Brandenburg and Mecklenburg-Vorpommern, remain the core markets for higher-horsepower tractors due to larger farm structures, while Bavaria and Baden-Württemberg continue to drive demand for utility tractors suited to smaller, fragmented holdings. Vineyard regions along the Rhine and Mosel sustain steady demand for narrow-row orchard tractors tailored to specialty crops.

At the European level, tractor registrations contracted, yet Germany showed comparatively stronger resilience supported by steady subsidy uptake and ongoing modernization efforts. Tractor exports continue to play a central role in maintaining domestic manufacturing activity, with significant volumes shipped to key European partners. Federal investment in digital-farming programs and nationwide 5G expansion further strengthens Germany’s position as a leading testing ground for autonomous and next-generation machinery.

Reliance on external markets remains a structural risk, as shifts in global credit conditions or currency movements can influence domestic production cycles. Even so, recent moves such as AGCO Corporation’s expansion in electric machinery development and CLAAS KGaA mbH’s increased R&D commitments indicate sustained confidence in Germany’s long-term status as a European center for advanced agricultural machinery innovation.

Competitive Landscape

Germany agricultural tractor market is moderately concentrated, with key players collectively accounting for about 60% of the market share in 2024. Leading companies such as AGCO Corporation, Deere & Company, CLAAS KGaA mbH, CNH Industrial N.V., and SDF Group S.p.A. maintain strong positions, supported by extensive product portfolios, financing programs, and advanced technology integration. Prominent brands such as Fendt, John Deere, CLAAS, New Holland, and Deutz-Fahr represent a significant share of national sales, highlighting the market's consolidated structure.

Recent developments indicate strategic shifts among major companies. AGCO Corporation is enhancing its digital capabilities through precision-agriculture initiatives, while Deere & Company focuses on integrated software and automation platforms to strengthen long-term customer retention. Kubota Corporation is expanding its presence in the compact and electric tractor segments through dealership growth, and Yanmar Holdings Co. is increasing its focus on mid-range horsepower categories following recent global acquisitions. These strategies align with Germany's rising demand for electrification, autonomy, and high-efficiency machinery.

Emerging market opportunities include compact electric tractors for municipal applications, autonomous platforms tailored for organic farming systems, and specialized vineyard tractors designed for sloped or narrow-row terrains. As competition shifts from horsepower to software ecosystems, manufacturers offering telematics-enabled equipment combined with flexible financing solutions are well-positioned to gain market traction. Conversely, companies that delay adopting integrated precision technologies risk losing market relevance, as German farmers increasingly prioritize digital tools to improve productivity and meet regulatory requirements.

Germany Agricultural Tractor Industry Leaders

AGCO Corporation

Deere & Company

CLAAS KGaA mbH

CNH Industrial N.V.

SDF Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SDF Group S.p.A. has inaugurated a new energy-efficient office building at the DEUTZ-FAHR Land site in Lauingen, Germany. This development consolidates key functions while enhancing the company's manufacturing and research and development (R&D) capabilities in the region. The expansion highlights SDF's ongoing commitment to the German agricultural tractor market and aims to support future product development and service improvements.

- February 2025: SDF Group S.p.A. and AGCO Corporation have entered into a supply agreement under which SDF will manufacture low- to mid-range Massey Ferguson tractors (up to 85 HP) in Lauingen. This partnership enhances SDF’s production activities in Germany and strengthens the country's role as a significant manufacturing hub in the agricultural tractor market.

- April 2024: CLAAS KGaA mbH has modernized its Harsewinkel facility, which includes the construction of a new goods receiving area and an automated, energy-efficient Hall 2. These USD 65 million (EUR 60 million) upgrades enhance production efficiency and capacity, strengthening the company's position in Germany agricultural tractor market.

Germany Agricultural Tractor Market Report Scope

| Below 40 HP |

| 40-100 HP |

| Above 100 HP |

| Utility Tractors |

| Row-Crop Tractors |

| Orchard and Vineyard Tractors |

| Other Tractor Types |

| Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) |

| Autonomous / Driverless |

| Cereals and Oilseeds |

| Fruits and Vegetables |

| Livestock Operations |

| Others |

| By Horsepower | Below 40 HP |

| 40-100 HP | |

| Above 100 HP | |

| By Tractor Type | Utility Tractors |

| Row-Crop Tractors | |

| Orchard and Vineyard Tractors | |

| Other Tractor Types | |

| By Drive Type | Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) | |

| Autonomous / Driverless | |

| By Application | Cereals and Oilseeds |

| Fruits and Vegetables | |

| Livestock Operations | |

| Others |

Key Questions Answered in the Report

How large is Germany agricultural tractor market in 2025?

Germany agricultural tractor market size stands at USD 2.60 billion in 2025 and is on course to reach USD 3.34 billion by 2030.

What CAGR is projected for high-horsepower tractors above 100 HP?

The above-100 HP segment is projected to post a 6.8% CAGR through 2030, outpacing the overall market.

How do CAP subsidies influence tractor purchases?

CAP precision-farming grants reimburse up to 40% of eligible equipment costs, compressing payback periods and front-loading purchases into 2025–2026.

What limits adoption of electric tractors in rural Germany?

Fewer than 200 fast chargers over 150 kW, high charger installation costs, and inconsistent 5G upload speeds constrain large-scale electric tractor deployment.

Page last updated on: