United Kingdom Combined Harvester Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

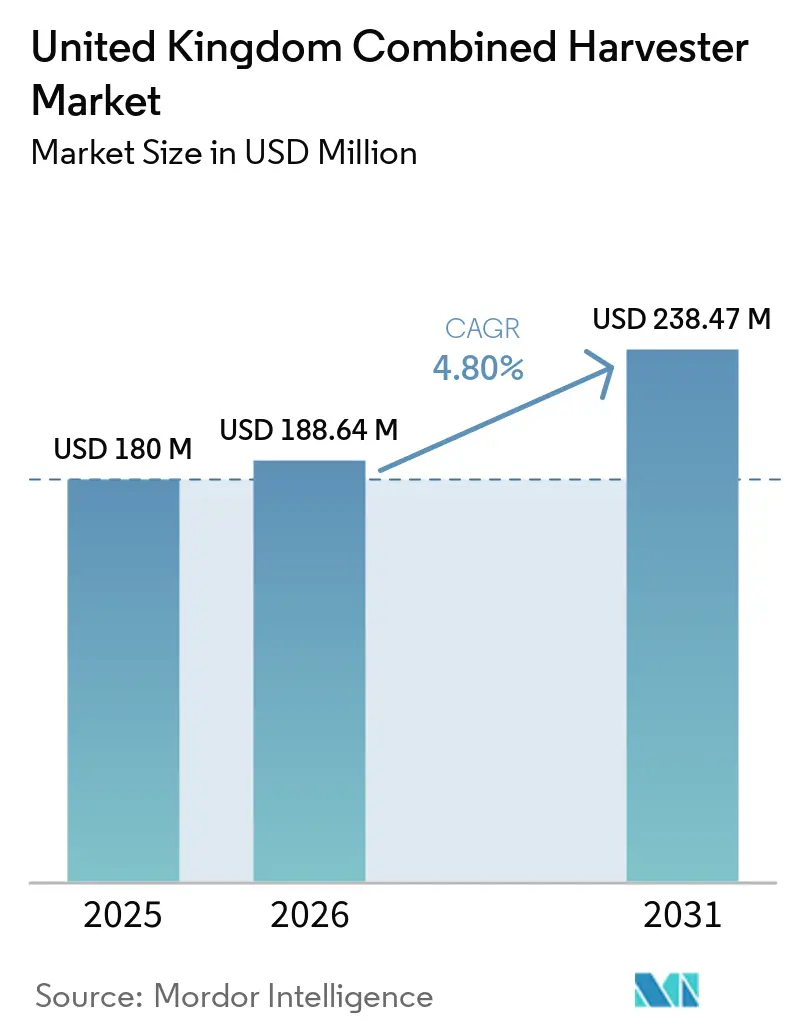

| Base Year Market Size (2025) | USD 180 Million |

| Market Size (2026) | USD 188.64 Million |

| Market Size (2031) | USD 238.47 Million |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

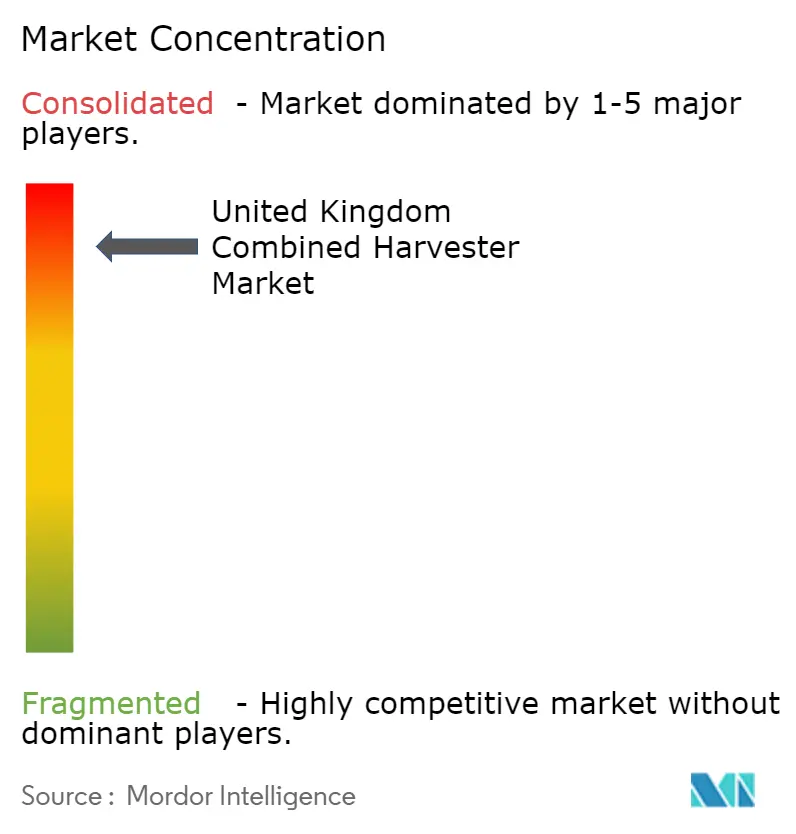

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Combined Harvester Market Analysis by Mordor Intelligence

The United Kingdom combined harvester market is projected to grow from USD 180.0 million in 2025 to USD 188.64 million in 2026 and USD 238.47 million by 2031, registering a CAGR of 4.8% between 2026 and 2031. Market growth is driven by increasing replacement demand for aging harvesting fleets, farm consolidation, and ongoing agricultural labor shortages, all of which are encouraging the adoption of mechanized harvesting solutions. Farmers are increasingly utilizing precision and smart harvesting technologies to enhance operational efficiency, minimize crop losses, and promote sustainable farming practices. The demand for high-capacity harvesters is rising among large commercial farms and contractor service providers seeking greater productivity and faster harvesting. Additionally, government-supported agricultural equipment funding and manufacturer financing programs are facilitating the adoption of machinery. However, market growth is constrained by fluctuating grain prices, high equipment acquisition costs, and post-Brexit import-related challenges, particularly affecting smaller farming operations.

Key Report Takeaways

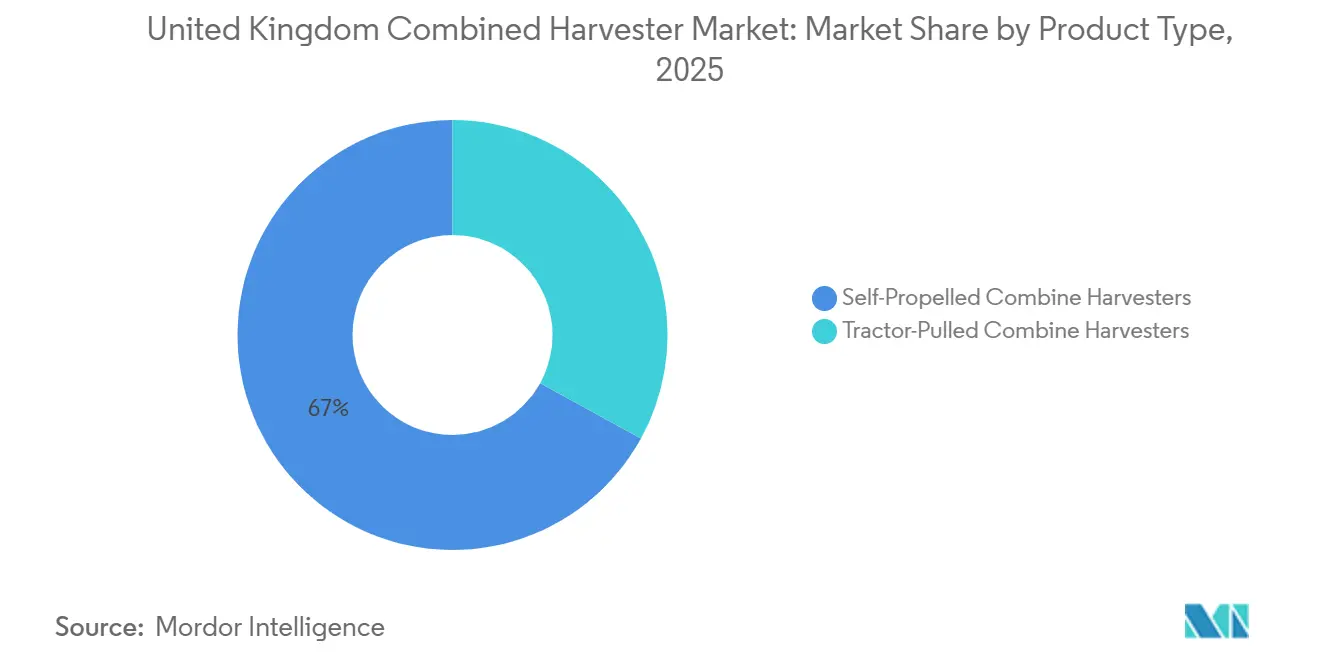

- By product type, self-propelled combined harvesters accounted for the largest 67% of the United Kingdom combined harvester market share in 2025, whereas tractor-pulled combined harvesters are projected to expand at the fastest 6.8% CAGR from 2026 to 2031.

- By power rating, above 300 HP held the largest 46% of the United Kingdom combined harvester market share in 2025, while the market size of up to 200 HP is anticipated to grow at the fastest 7.3% CAGR from 2026 to 2031.

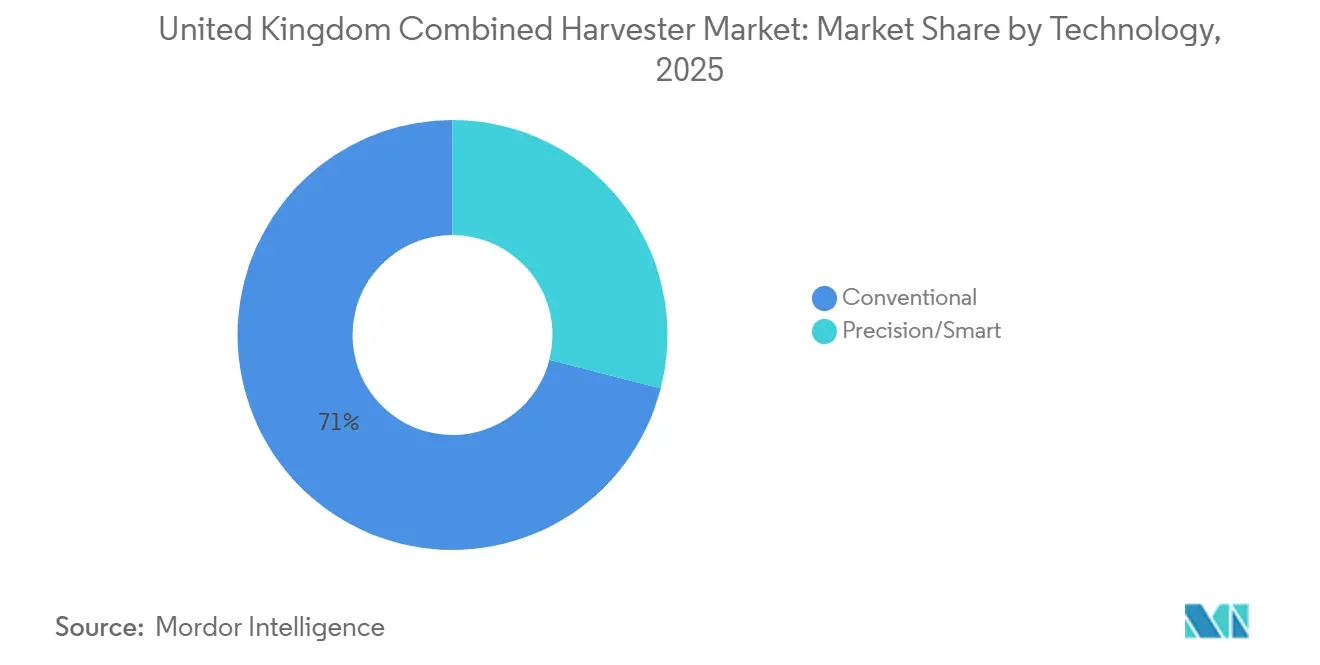

- By technology, conventional technology captured the largest 71% of the United Kingdom combined harvester market size in 2025, whereas precision/smart technology is forecast to register the fastest 9.5% CAGR from 2026 to 2031.

- By grain tank capacity, the 8,001–12,000 L segment accounted for the largest 53% revenue share in 2025, while harvesters with above 12,000 L capacity are projected to grow at the fastest 7.8% CAGR through 2031.

- By end user, large-scale commercial farms commanded the largest 58% revenue share in 2025, whereas custom hiring service providers are projected to grow at the fastest 8.1% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Combined Harvester Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement demand for aging combine harvesters | +0.9% | England and Scotland | Medium term (2-4 years) |

| Government support through farming equipment grants | +0.7% | Nationwide, highest in England and Scotland | Short term (≤ 2 years) |

| Growth in average farm size from land consolidation | +0.8% | Core England, secondary Scotland | Long term (≥ 4 years) |

| Farm labor shortages and rising wages | +0.6% | All regions, acute in eastern England | Medium term (2-4 years) |

| Demand for harvesters suited for regenerative farming | +0.5% | England and Scotland, early Wales uptake | Long term (≥ 4 years) |

| Manufacturer financing reducing equipment investment barriers | +0.7% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Replacement Demand for Aging Combine Harvesters

Replacement demand in the United Kingdom's combined harvester market is being influenced by the prolonged use of older harvesting equipment on farms. According to the Agricultural Engineers Association, combine harvesters in the United Kingdom dropped to 280 units during the 2024/25 season, marking a 30% decrease compared to the previous season[1] Source: Agricultural Engineers Association, “Industry Facts – Combine registrations in the United Kingdom declined ,” aea.uk.com. This reduction in new machinery purchases is attributed to weak farm profitability and growers' postponed capital investments due to fluctuating agricultural returns. As farmers extend the operational lifespan of their existing combines, long-term replacement demand is anticipated to grow for more fuel-efficient, high-capacity, and technologically advanced harvesting equipment nationwide.

Government Support Through Farming Equipment Grants

Government support through agricultural equipment grants is driving machinery modernization and the adoption of precision farming in the United Kingdom's combined harvester market. According to the United Kingdom Government, the Farming Equipment and Technology Fund 2025 offers grants ranging from GBP 1,000 (USD 1,340) to GBP 25,000 (USD 33,500). This initiative promotes advanced agricultural technologies, including precision farming systems, crop-monitoring tools, and combine-mounted weed-seed-reduction systems. The continued availability of government-backed funding is encouraging farmers and contractors to invest in technologically advanced harvesting equipment and precision-compatible combine harvesters, enhancing operational efficiency, reducing input costs, and supporting sustainable farming practices within the agricultural market.

Growth in Average Farm Size from Land Consolidation

Increasing farm sizes through land consolidation is driving the demand for high-capacity combine harvesters in the United Kingdom's agricultural market. According to the United Kingdom Government, the average farm size in England reached 87 hectares, and the East Midlands and East of England reported higher average farm sizes of 102 hectares and 130 hectares in 2024, respectively[2]Source: United Kingdom Government, “Agricultural Facts Summary – Average farm size in England,” gov.uk. Larger farming operations are increasingly adopting self-propelled combine harvesters with greater horsepower and wider cutting widths to enhance harvesting efficiency and minimize operational time during peak crop seasons.

Farm Labor Shortages and Rising Wages

Farm labor shortages and increasing wage costs are driving the demand for mechanization in the United Kingdom's combine harvester market. According to the United Kingdom Government, the National Living Wage is set to rise by 6.7%, from GBP 11.44 (USD 14.55) per hour in 2024 to GBP 12.21 (USD 15.53) per hour in April 2025 for workers aged 21 and above. The growing labor costs, along with challenges in finding skilled seasonal farm workers, are prompting farmers and contractors to adopt advanced combine harvesters. These machines, equipped with automation and precision features, help reduce reliance on operators, enhance harvesting efficiency, and lower overall field operation costs during peak harvesting periods nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | ||

|---|---|---|---|---|---|

| Fluctuating crop prices affecting farmer income | -0.6% | Nationwide, strongest in cereal heartlands | Short term (≤ 2 years) | ||

| High purchase cost compared to tractor attachments | -0.4% | Wales, Northern Ireland, and small farms | Medium term (2-4 years) | ||

| Limited dealer expertise in telematics-based servicing | -0.3% | Rural Scotland and Wales | Medium term (2-4 years) | ||

| Rising import tariffs on non-European machinery after Brexit | -0.2% | Nationwide | Long term (≥ 4 years) | ||

| Source: Mordor Intelligence | |||||

Fluctuating Crop Prices Affecting Farmer Income

Fluctuating crop prices are impacting farmer profitability and limiting investment capacity in the United Kingdom's combine harvester market. According to Brown & Co’s Quarterly Agricultural Update, feed wheat prices in the United Kingdom fell to GBP 178.3 (USD 212.18) per metric ton by the end of Feb 2025, against GBP 158.0 (USD 210.35) in 2024[3]Source: Brown & Co, “Quarterly Agricultural Update January-March 2025,” brown-co.com. Declining grain prices have significantly reduced margins for cereal growers, particularly amid rising input costs and uncertain farm incomes. Consequently, many arable farmers are postponing capital-intensive purchases, such as new combine harvesters, and extending the operational lifespan of existing machinery.

High Purchase Cost Compared to Tractor Attachments

The high purchase costs of advanced harvesting machinery are restricting the ownership of combines among small and medium-sized farms in the United Kingdom. Modern self-propelled combine harvesters, featuring high horsepower, automation systems, precision farming technologies, and large grain tanks, require significant capital investment, making them less accessible to smaller agricultural operators. Consequently, many farms rely on contractors, used machinery, or more affordable tractor-based harvesting alternatives instead of acquiring new combines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Self-Propelled Dominance, Tractor-Pulled Revival

Self-propelled combine harvesters accounted for the largest 67% of the United Kingdom's combined harvester market share in 2025. Large commercial farms and agricultural contractors prefer self-propelled combines due to their higher operational efficiency, wider cutting capacity, and faster harvesting speeds during short crop collection periods. Adoption is particularly strong among consolidated farming estates aiming to reduce labor dependency and enhance field productivity. These machines increasingly feature advanced automation, telematics, and precision farming technologies, improving fuel efficiency and minimizing crop losses. Additionally, strong dealer support networks and manufacturer-backed financing programs are driving sustained demand for high-capacity self-propelled harvesting equipment.

The tractor-pulled combine harvesters market size is projected to grow at the fastest CAGR of 6.8% from 2026 to 2031. Growth is driven by increasing demand from small and medium-sized farms seeking cost-effective harvesting solutions with lower initial investment requirements. These systems are particularly appealing to growers managing limited cereal acreage, as they reduce ownership costs and offer flexibility for mixed-farming operations. The reliance on used machinery markets and contractor-supported harvesting services is further boosting demand in this segment. Additionally, trends in farm consolidation are encouraging smaller agricultural operators to adopt more affordable harvesting alternatives instead of investing in large self-propelled combine harvesters.

By Power Rating: High-Horsepower Surge, Entry-Level Acceleration

Above 300 HP held 46% of the United Kingdom's combined harvester market share in 2025. Large-scale cereal farms and contractor-operated harvesting fleets increasingly prefer high-horsepower combines because they improve harvesting speed, reduce field passes, and support wider headers during short harvesting windows. These machines are gaining traction across consolidated farming operations where labor shortages and weather variability require faster crop collection. Demand also benefits from rising adoption of self-propelled combines equipped with automation technologies, larger grain tanks, and precision farming systems. Premium combine models remain concentrated among commercial farms, and contractors focused on maximizing operational productivity and reducing harvesting downtime.

Up to 200 HP machines are anticipated to grow at the fastest 7.3% CAGR from 2026 to 2031. Entry-level combine harvesters continue attracting small and medium-sized farms seeking lower ownership costs and reduced financing burdens compared to larger harvesting equipment. These combines remain suitable for mixed-farming operations and smaller cereal acreage where high-capacity machinery is not economically viable. Growth in this segment is further supported by increasing demand for affordable harvesting solutions, the availability of compact machines with modern features, and expanding adoption among growers shifting from manual or contractor-based harvesting toward mechanized operations.

By Technology: Conventional Inertia, Precision Lift-Off

Conventional technology accounted for the largest 71% of the United Kingdom combine harvester market share in 2025. This dominance is attributed to growers prioritizing reliability, lower maintenance requirements, and familiarity with existing machinery platforms. Farmers with older fleets often opt for conventional harvesting systems due to their lower upfront costs and minimal reliance on advanced telematics or software-based functions. Additionally, traditional combines remain widely used on small and medium-sized farms, where the adoption of precision farming technologies is relatively low. The segment is further supported by strong aftermarket networks and the availability of used conventional combines, sustaining demand across the agricultural market.

The precision and smart technology segment is projected to grow at the fastest CAGR of 9.5% from 2026 to 2031. This growth is driven by the increasing adoption of automated harvesting systems, yield-monitoring technologies, and variable-rate farming practices to enhance operational efficiency and reduce input costs. Farmers are investing in combines equipped with advanced sensors, automation features, and data-driven farm management tools to optimize productivity and achieve sustainability goals. Government-supported precision agriculture funding programs and growing awareness of fuel efficiency and crop-loss reduction are further boosting demand for technologically advanced combine harvesters, particularly in large-scale farming operations.

By Grain Tank Capacity: Mid-Range Mainstay, High-Capacity Growth

The 8,001–12,000 L segment accounted for the largest 53% of the United Kingdom combine harvester market share in 2025. Mid-capacity combine harvesters are widely preferred due to their balanced productivity, manageable operating costs, and compatibility with most farm sizes in the agricultural market. These combines are particularly well-suited for medium-to-large cereal farms that require efficient harvesting without the higher investment associated with ultra-large harvesting platforms. Additional demand drivers include easier transport logistics, compatibility with existing grain-handling infrastructure, and operational flexibility across various crop types. This segment continues to see strong adoption among commercial farms and contractor-operated harvesting fleets.

Above 12,000 L capacity is projected to grow at the fastest 7.8% CAGR from 2026 to 2031. This growth is driven by increasing demand from large commercial farms and agricultural contractors aiming to reduce unloading frequency and enhance harvesting efficiency during peak crop periods. High-capacity grain tanks improve operational productivity by minimizing field interruptions and supporting wider cutting headers for extensive cereal acreage. Adoption is further bolstered by labor shortages, prompting farms to complete harvesting operations with fewer workers and machines. Additionally, the trend of farm consolidation is strengthening the demand for larger and higher-capacity combine harvesting equipment.

By End User: Commercial Scale Leads, Contracting Rises

Large-scale commercial farms accounted for 58% of the United Kingdom's combine harvester market share in 2025. Large farming operations remain the primary customer base for combine harvesters due to their extensive cereal cultivation areas, greater financial resources, and higher mechanization needs. These farms are increasingly investing in technologically advanced harvesting equipment to enhance productivity, reduce harvesting time, and optimize fuel efficiency during narrow crop collection periods. Demand is particularly strong for self-propelled combines equipped with precision farming technologies, automation systems, and large grain-handling capacities. Additionally, ongoing agricultural land consolidation is driving the growth of large commercial farming operations across the country.

Custom hiring service providers are projected to grow at the fastest 8.1% CAGR from 2026 to 2031. Rising machinery ownership costs and fluctuating farm profitability are prompting smaller growers to rely more on contractor-based harvesting services rather than purchasing combines directly. Custom operators are expanding their fleets to cover larger harvesting areas and meet seasonal demand in cereal-producing regions. This segment is also benefiting from labor shortages and a growing preference for outsourced harvesting operations, which reduce capital investment burdens for farmers. The increasing adoption of high-capacity and technologically advanced combines by contractors is further driving the segment's growth.

Geography Analysis

England remains the leading regional market due to its extensive cereal cultivation areas and the prevalence of large commercial farming operations. Key arable regions, including East Anglia, Lincolnshire, and Yorkshire, continue to drive demand for high-capacity self-propelled combine harvesters equipped with automation and precision farming technologies. The presence of large farm structures and contractor-operated harvesting models supports the adoption of combines with higher horsepower and wider cutting headers. Additionally, the region benefits from robust agricultural infrastructure, established dealer networks, and higher levels of mechanization than in other parts of the country. Ongoing land consolidation further bolsters the demand for technologically advanced harvesting equipment.

Scotland is an emerging market, driven by improving cereal production and increasing demand for efficient harvesting machinery across large agricultural estates. According to the Scottish Government, Scotland’s wheat production rose by 25% to 1.03 million metric tons in 2025 against 1.00 million metric tons in 2024. This growth in crop output is encouraging the adoption of high-capacity combine harvesters capable of operating efficiently across variable terrain and within shorter harvesting periods. Contractor-led harvesting operations play a significant role in meeting mechanization demand across Scotland’s cereal-producing regions.

Wales and Northern Ireland represent smaller markets due to limited cereal cultivation areas and the dominance of mixed-farming systems centered on livestock production. The prevalence of smaller farm structures and lower harvesting intensity reduces the demand for large self-propelled combine harvesters in these regions. Many farms rely on contractor services or shared machinery ownership models rather than direct equipment purchases. However, growing interest in sustainable farming practices and regenerative agriculture is gradually driving the adoption of specialized harvesting technologies designed to improve residue management and minimize soil disturbance. Regional demand is primarily concentrated among medium-sized cereal growers and agricultural contractors serving multiple farms.

Competitive Landscape

The market is highly concentrated, with the top five companies, including Deere & Company, CNH Industrial N.V., AGCO Corporation, CLAAS KGaA mbH, and Kubota Corporation, maintaining strong positions. These companies leverage extensive dealer networks, broad product portfolios, and established customer relationships within the agricultural sector. Competition increasingly focuses on high-capacity self-propelled combine harvesters equipped with automation, telematics, and precision farming technologies. Leading manufacturers are enhancing aftermarket service capabilities and financing support to improve customer retention and drive machinery adoption. Dealer consolidation trends are reshaping the competitive landscape as companies aim for stronger regional coverage, improved servicing capacity, and greater operational efficiency in major cereal-producing regions.

Manufacturers are prioritizing automation upgrades, software integration, and precision farming compatibility to differentiate their harvesting equipment portfolios. Companies are introducing retrofit solutions and advanced automation packages that enable growers to enhance harvesting performance without replacing entire machinery fleets. Competitive strategies also include strengthening digital agriculture ecosystems, expanding telematics support, and improving data-driven farm management capabilities. Financing partnerships and dealer-network expansion remain critical for increasing machinery accessibility among commercial farms and contractor-operated businesses. Product development efforts emphasize fuel efficiency, reduced crop losses, and improved operational productivity in large-scale harvesting operations.

Niche manufacturers and technology providers are addressing specialized harvesting requirements and retrofit demand for older machinery fleets. Companies offering retrofit yield-monitoring systems, residue-management technologies, and specialized harvesting attachments are benefiting from growers seeking cost-effective modernization alternatives instead of purchasing new combines. Additionally, post-Brexit trade frictions and import-related costs are bolstering established domestic dealer networks and incumbent manufacturers by limiting aggressive price competition from external suppliers within the agricultural machinery industry.

United Kingdom Combined Harvester Industry Leaders

Deere and Company

CNH Industrial N.V.

AGCO Corporation

CLAAS KGaA mbH

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Deere & Company has upgraded its 2027 X9 and S7 combine harvester series by incorporating enhanced Harvest Settings Automation, Predictive Ground Speed Automation, and increased grain tank capacity. These improvements aim to boost harvesting productivity and minimize operator intervention.

- July 2025: CLAAS KGaA mbH has expanded its TRION combine harvester series by introducing upgraded models with engine outputs of up to 507 horsepower and grain tank capacities of 13,500 liters, aimed at enhancing harvesting productivity.

- January 2024: CNH Industrial N.V.’s New Holland brand launched the CR11 combine harvester in the United Kingdom market during LAMMA 2024. The model includes improved automation, reduced grain loss, and enhanced productivity features.

United Kingdom Combined Harvester Market Report Scope

A combine harvester is an agricultural machine that performs multiple harvesting tasks, including reaping, threshing, and grain cleaning, in a single operation. It is commonly used for harvesting cereal crops such as wheat, barley, corn, rice, and oats, enhancing efficiency, reducing labor needs, and minimizing crop losses during field operations. The United Kingdom combined harvester market report is segmented by product type (self-propelled combine harvester and tractor-pulled combine harvester), by power rating (up to 200 HP, 201-300 HP, and above 300 HP), by technology (conventional and precision/smart), by grain tank capacity (up to 8,000 L, 8,001-12,000 L, and above 12,000 L), and by end user (large-scale commercial farms, small and medium farms, and custom hiring service providers). The market forecasts are provided in terms of value (USD).

| Self-Propelled Combine Harvesters |

| Tractor-Pulled Combine Harvesters |

| Up to 200 HP |

| 201-300 HP |

| Above 300 HP |

| Conventional |

| Precision/Smart |

| Up to 8,000 L |

| 8,001-12,000 L |

| Above 12,000 L |

| Large-Scale Commercial Farms |

| Small and Medium Farms |

| Custom Hiring Service Providers |

| By Product Type | Self-Propelled Combine Harvesters |

| Tractor-Pulled Combine Harvesters | |

| By Power Rating | Up to 200 HP |

| 201-300 HP | |

| Above 300 HP | |

| By Technology | Conventional |

| Precision/Smart | |

| By Grain Tank Capacity | Up to 8,000 L |

| 8,001-12,000 L | |

| Above 12,000 L | |

| By End User | Large-Scale Commercial Farms |

| Small and Medium Farms | |

| Custom Hiring Service Providers |

Key Questions Answered in the Report

What is the market size of the United Kingdom combined harvester market in 2026?

The United Kingdom combined harvester market size stands at USD 188.64 million in 2026.

How fast is the market growing?

The market is projected to log a 4.8% CAGR during 2026-2031, supported by farm consolidation, labor shortages, and equipment grants.

Which product type dominates sales?

Self-propelled combine harvesters machines held the largest 67% of the United Kingdom combined harvester market share in 2025.

Who are the leading manufacturers?

Deere and Company, CNH Industrial, AGCO, and CLAAS KGaA mbH command the most premium self-propelled combine harvester sale.

Page last updated on: