China Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

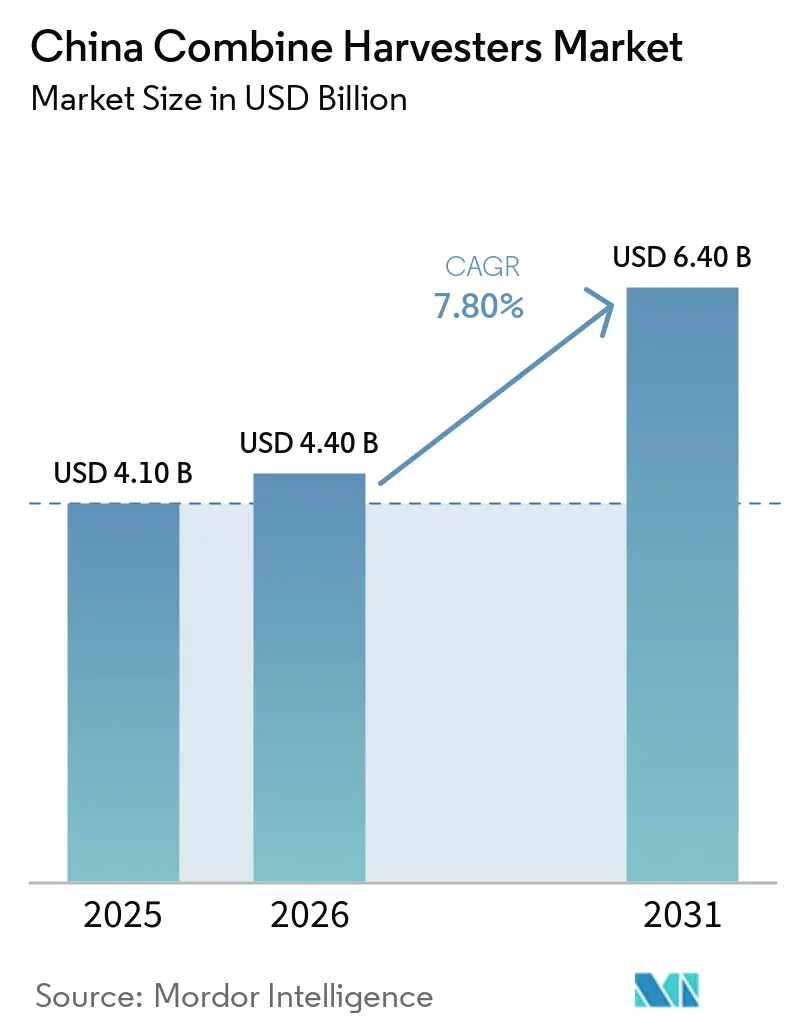

| Base Year Market Size (2025) | USD 4.10 Billion |

| Market Size (2026) | USD 4.40 Billion |

| Market Size (2031) | USD 6.40 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Combine Harvesters Market Analysis by Mordor Intelligence

The China combine harvester market size expanded to USD 4.1 billion in 2025 and is projected to reach USD 4.4 billion in 2026, and USD 6.4 billion by 2031, growing at a CAGR of 7.8% from 2026 to 2031. Government subsidies that cover up to 40% of the invoice price for BeiDou-equipped machines, tight grain-loss rules that cap harvest waste at 1.2%, and a rising share of rural workers aged 60 or older are jointly driving an accelerated replacement cycle across every grain belt. Stage IV emission compliance, which adds USD 1,100-4,100 per unit, is pushing manufacturers to bundle fuel-savings telematics and predictive maintenance to help operators offset higher ownership costs. Although wheat, rice, and corn mature within three compressed windows that leave fleets idle nine months a year, the installed base still climbed to a significant number of units in 2025, showing that the China combine harvester market continued to expand even under utilization pressure.

Key Report Takeaways

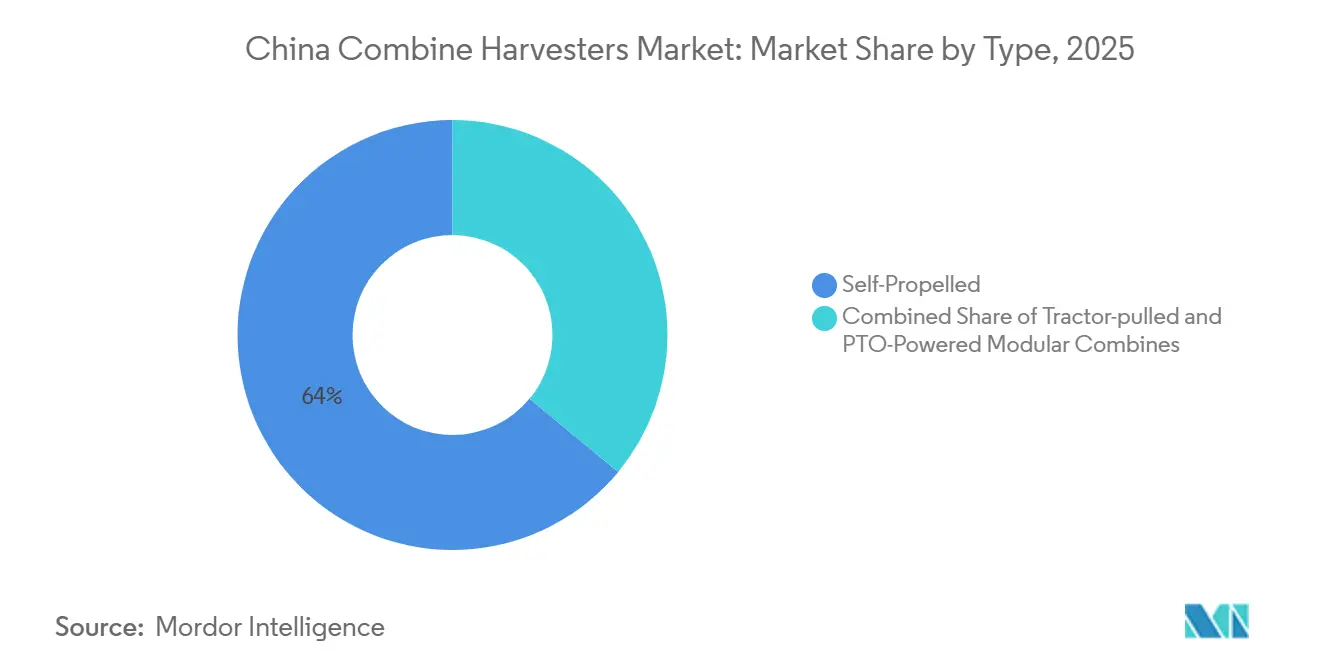

- By type, self-propelled combines captured 64% of 2025 revenue, while tractor-pulled combines are projected to post an 8.9% CAGR through 2031.

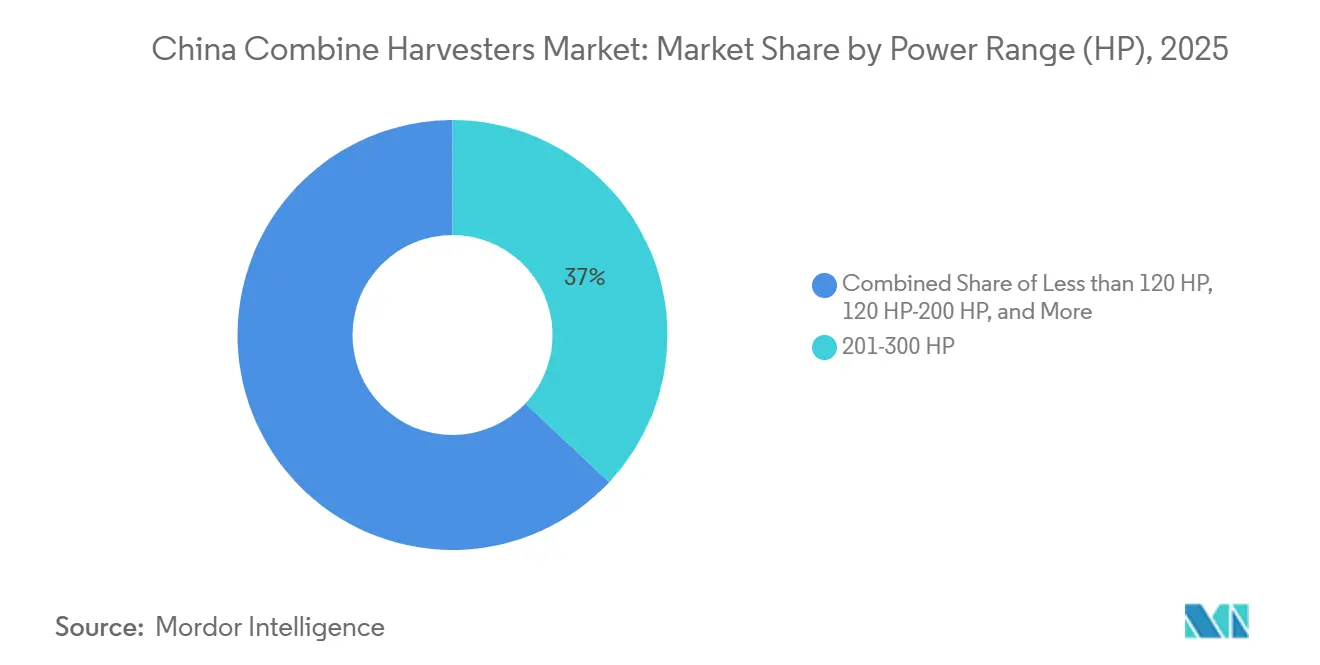

- By power range, the 201-300 horsepower category accounted for 37% of the China combine harvester market share in 2025, and units above 300 horsepower are forecast to grow at an 8.9% CAGR to 2031.

- By movement type, wheel-type models held a 59% share of the China combine harvester market size in 2025, and crawler platforms are projected to grow at an 8.9% CAGR through 2031 due to rising rice demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-backed mechanization push | +1.8% | National, strongest in Heilongjiang, Henan, Shandong, Jiangsu | Short term (≤ 2 years) |

| Rural labor shortage and rising wage costs | +1.5% | Nationwide, acute in Northeast and Central Plains | Medium term (2-4 years) |

| National food-security agenda elevating grain-loss standards | +1.2% | Nationwide, strictest in top grain provinces | Medium term (2-4 years) |

| BeiDou-enabled smart-harvester subsidy incentives | +0.8% | Nationwide, early uptake in Heilongjiang, Jilin, Inner Mongolia | Short term (≤ 2 years) |

| Stricter grain-loss quotas for state grain procurement | +0.7% | Nationwide, priority in state reserve catchment areas | Short term (≤ 2 years) |

| Land-consolidation pilot zones demanding high-HP machines | +0.6% | Heilongjiang, Inner Mongolia, Xinjiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidy-Backed Mechanization Push

China’s 2026 machinery purchase fund grew to USD 3.33 billion, a 10.7% increase over 2024, and high-feed-rate combines now receive 35-40% reimbursement, up from 30% for legacy machines[1]Source: Ministry of Agriculture and Rural Affairs, “2024 National Agricultural Mechanization Development Statistical Bulletin,” moa.gov.cn. Shaanxi lifted the subsidy ceiling for six-kilogram-per-second tracked models from USD 5,250 to USD 6,300, accelerating the retirement of tangential-drum units. Cotton pickers now qualify for USD 11,200, confirming that support extends beyond staple grains. The 2024-2026 catalog also links eligibility to BeiDou receivers and loss sensors, forcing manufacturers to bundle telematics. Heilongjiang deployed BeiDou-guided harvesters across 650,000 hectares, trimming overlap waste by up to 12%. Jiangsu cooperatives installed 3,000 units with live yield mapping, which informs variable-rate fertilization. This policy suite cuts payback from 6 to 4 years for 250-horsepower machines, directly boosting annual shipments and speeding up replacement cycles.

Rural Labor Shortage and Rising Wage Costs

The share of rural residents aged 60 and above climbed from 9.55% in 2005 to 18.57% in 2021 and is forecast to hit 30% by 2030. Daily wages for manual harvesters in Lufeng rose to USD 17 in 2024, up 35% from 2020. Mechanized services charge USD 8-11 per 0.067 hectares, resulting in a net saving of USD 42 per 0.067 hectares for smallholders. Certified harvester operators stand at 11.7 million, while the machinery workforce is 50.1 million, widening the skills gap. Wen’an Cooperative in Hebei retrofitted 15 combines with serrated sieves, reducing grain loss to 0.85%. Inner Mongolia’s Naiman Banner consolidated 75,133.3 hectares into 452 cooperatives, allowing fleets of 40 combines to serve 600-hectare blocks. As the median farmer age surpasses 55 and urban migration drains young workers, mechanization becomes the only feasible hedge against escalating labor costs.

National Food-Security Agenda Elevating Grain-Loss Standards

Rules effective January 2026 cap wheat and rice harvest loss at 1.2% to qualify for state procurement. Yancheng enforces a 2.8% limit for full-feed rice combines, audited with on-board sensors. Shanxi achieved a 0.937% wheat-loss rate in 2024 by subsidizing dual-axial-flow machines and scaling up operator training. National grain output increased 1.2% year-on-year to 714.88 million metric tons in 2025, sharpening focus on post-harvest waste. Manufacturers now ship loss cameras and acoustic sensors as standard; Weichai Lovol’s GS8188 alerts drivers when cylinder clearance drifts, while CNH and Zoomlion offer similar systems. By turning loss reduction into a revenue prerequisite, the regulation accelerates the exit of obsolete, tangential-drum inventory.

BeiDou-Enabled Smart-Harvester Subsidy Incentives

Provinces are offering 5-10% point rebates on BeiDou-ready harvesters, lifting total support to 40% in many grain belts. More than 3,000 machines in Heilongjiang now operate with ±2 centimeter real-time accuracy, reducing overlap to under 2% and saving 60 liters of diesel per 666.6 hectares. Weichai Lovol’s AI assistant predicts failures 72 hours in advance and automatically dispatches service vans. John Deere’s MY2026 series adds predictive ground-speed control; Zoomlion’s PL80 automatically modulates engine load. The incremental hardware cost of CNY 8,000-12,000 (USD 1,100-1,700) is largely offset by higher subsidies and fuel savings. Cross-region contractors use BeiDou routing to jump from Henan wheat in May to Heilongjiang rice in September, lifting annual utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront machine cost and credit gaps | −0.9% | Nationwide, sharper in western provinces and smallholder regions | Medium term (2-4 years) |

| Fragmented land holdings limit large-machine utility | −0.7% | Nationwide, particularly Sichuan, Guizhou, Yunnan hill areas | Long term (≥ 4 years) |

| Harvest-window compression causing seasonal overcapacity | −0.5% | Nationwide, especially wheat-rice rotation belts | Medium term (2-4 years) |

| China VI non-road diesel compliance costs | −0.4% | Nationwide, uniform enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Machine Cost and Credit Gaps

Self-propelled 200-300 horsepower combines cost USD 28,000-49,000 before subsidy, which is equivalent to three to five years of net farm income for households tilling 1.33 hectares[2]Source: Agricultural Machinery Distribution Association, “Industry Statistics,” camda.org.cn. Subsidy reimbursement lags purchase by up to six months, forcing reliance on bridge loans. Rural credit unions charge 4.5-6.0% interest, yet collateral rules exclude up to half of applicants. Zhengzhou Zhonglian’s 4LZ-9B lists at USD 25,200-30,800; after a USD 6,800 subsidy, the net outlay still exceeds the average household disposable income by 40%. Leasing penetration is below 15%, compared with 40% in North America. Weichai Lovol’s Feidi Leasing and Zoomlion Financial offer 24-month plans with a USD 4,200 down payment and USD 1,100 monthly payments, yet uptake is under 10%. The burden is steeper for models with more than 300 horsepower, costing USD 84,000. Financial constraints, therefore, slow fleet renewal, especially outside pilot zones.

Fragmented Land Holdings Limit Large-Machine Utility

65% of Chinese farms operate plots of less than 2 hectares, averaging 0.7 hectares in the south. Geometry favors 120-200 horsepower combines that can turn inside 20-meter headlands. Sloped terrain in Sichuan, Guizhou, and Yunnan restricts access and demands narrow-track crawlers. The 201-300 horsepower band holds 37% share because it balances capacity and agility. Although pilot zones show that pooling 1,000 hectares unlocks demand for ultra-capacity platforms, cultural and administrative barriers slow replication in the south. Outsourced machinery services help aggregate workload; a 2025 Jiangsu study confirms that outsourcing raises land transfers in and reduces transfers out. Hebei cooperatives already serve across 1,500 households. Yet, 35-40% of the arable area remains inaccessible to units with more than 150 horsepower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Anchored by Axial-Flow Gains

Self-propelled combines captured 64% of the China combine harvester market size in 2025, representing the largest share. Wider cabs and lower vibration make them the preferred choice for aging operators. Dual-axial-flow architectures meet the 1.2% loss ceiling and deliver 15-20% higher throughput than tangential drums. Half-feed rice persists in straw-retention paddies, though at a 40% throughput penalty. The tractor-pulled segment is projected to expand at a CAGR of 8.9% through 2031, outpacing other segments, as tractor-pulled units, priced at USD 11,200-16,800, remain relevant for Sichuan’s narrow terraces. PTO modular kits are gaining traction in rapeseed and peanut plots where dedicated harvesters are uneconomical. The pivot to self-propelled machines underscores where the China combine harvester market will direct most R&D funding.

Self-propelled adoption also aligns with smart-harvester subsidies; 70% of BeiDou-equipped units shipped in 2025 were factory-installed rather than retrofitted. Replacement intent is strongest among cooperatives managing 300-800 hectares that can justify the higher outlay. Tractor-pulled models still anchor entry-level mechanization, yet a lack of comfort stalls operator interest. Modular kits benefit from flexible deployment on existing tractors but face limits in heavy wheat stands. Given subsidy bias and stricter loss norms, the China combine harvester market is tilting irrevocably toward high-spec self-propelled chassis.

By Movement: Crawler Traction Gains in Paddy Regions

Wheel-type combines account for 59% of 2025 shipments, primarily due to their suitability for wheat and dryland corn applications. These combines offer road speeds of 25-35 kilometers per hour, facilitating cross-region operations. Meanwhile, crawler-type platforms are anticipated to grow at an annual rate of 8.9% through 2031, driven by increasing demand for paddy-rice harvesting in regions such as Hunan, Jiangxi, and Heilongjiang. In these areas, soil-bearing pressures below 0.3 kilograms per square centimeter make wheeled units less effective, as they are prone to sinking. Rubber-track crawlers offer lower ground compaction and 20–30% longer track life than steel alternatives. However, steel-track designs cater to extreme-wet conditions and cost-sensitive segments.

Key players in the crawler segment include Jiangsu World Agricultural Machinery's R-80 crawler rice series and KUBOTA Corporation's PRO688Q, which dominate the 6-kilogram-per-second crawler category. These models have contributed to achieving 98% mechanization in southern paddy fields, where wheel slip often exceeds 15-20%. In the wheel-type segment, four-wheel-drive combines, such as Weichai Lovol's GS8188 and Zoomlion's TF220, achieve 30-35% higher road speeds than two-wheel-drive models. This results in a 40-50% reduction in transport time between fields, enabling operators to cover service radii of 50-80 kilometers from base depots.

By Power Range: 201-300 HP Balances Scale and Versatility

The 201-300 horsepower category accounted for 37% of the China combine harvester market share in 2025, highlighting the preference for machines that balance 8-12 kilogram-per-second feed rates with maneuverability. Engines under 200 horsepower captured a larger market share, catering to smallholder cooperatives and cross-region contractors who prioritize fuel efficiency. Combines with less than 120 horsepower are predominantly used in terrace farming, where a smaller turning radius is more critical than capacity. Meanwhile, combines exceeding 300 horsepower are projected to achieve the highest CAGR of 8.9%, as pilot mega farms demonstrate the economic benefits of ultra-capacity machines.

Zoomlion’s TF220 and John Deere’s S-Series occupy the 201-300-horsepower range, offering 10-15% higher throughput compared to 200-horsepower models, albeit at a 25% price premium[3]. Weichai Lovol’s GS8188 flagship model, priced at CNY 600,000 (USD 82,800), is designed for workloads exceeding 1,000 hectares, limiting its adoption to the top 5% of operators. The segment for combine harvesters with more than 300 horsepower is anticipated to grow during the forecast period, supported by policies promoting land consolidation. However, two-thirds of farms are estimated to remain under two hectares, limiting the potential market for large-scale platforms.

Geography Analysis

The North China Plain, encompassing Henan, Shandong, and Hebei, accounted for a significant share of the 2025 China combine harvester market, highlighting its prominence in wheat production (yielding 120 million metric tons annually) and its extensive cooperative networks serving 15 million hectares. Henan alone deployed 180,000 combines in May 2025 during the peak wheat harvest, leading to congested highways, 20% delays in field access, and revealing logistical bottlenecks, such as insufficient grain elevators. The region's fleets predominantly consist of 200-horsepower wheeled units designed for efficient cross-plot transfers, with 85% equipped with BeiDou navigation to cut overlap by 10-15%.

The Northeast region, including Heilongjiang, Jilin, and Liaoning, represented a substantial share of rice and maize machinery and is projected to experience the highest growth through 2031. Heilongjiang has become a testing ground for BeiDou-enabled fleets and 300-plus-horsepower crawlers capable of operating in wet paddy fields. In Xinjiang, the 2.93 million-hectare grain area and an eight-ton-per-hectare yield drive the adoption of ultra-capacity combines. However, the 2,000-kilometer distance from coastal factories increases logistics costs by 20%.

Southern provinces such as Hunan, Jiangxi, and Guangdong prefer crawler rice combines and half-feed designs that help preserve straw. In contrast, the hilly terrains of Sichuan and Guizhou sustain demand for narrow-track machines with less than 120 horsepower. Cross-region contracting connects these areas, with fleets migrating north-south to optimize utilization. However, freight costs of USD 0.21-0.28 per kilometer reduce profit margins. Regional specialization continues to strengthen as contractors adjust their machinery mix to suit local soil conditions.

Competitive Landscape

The China combine harvester market is moderately concentrated, with Weichai Lovol Smart Agriculture Technology Co., Ltd and Jiangsu World accounting for a significant share of the 2026 revenue. The five largest manufacturers collectively hold a substantial market share. Domestic manufacturers are increasingly focusing on vertical integration and hybrid power solutions. For instance, Zoomlion’s H7-600E hybrid, launched at Agritechnica 2025, combines a 480-horsepower diesel engine with an 11.55-kilowatt-hour battery, delivering 600 horsepower at peak and achieving 30% fuel savings.

International manufacturers are leveraging local assembly operations to strengthen their presence. CNH’s Harbin plant, following a cumulative USD 250 million investment, produces a combine harvester every 90 minutes[3]Source: CNH Industrial, “Harbin Manufacturing Facility,” cnh.com. John Deere’s MY2026 series features predictive ground-speed automation, while CLAAS introduced the EVION 580, equipped with an 8,000-liter grain tank. Smaller specialized players are addressing niche markets. Additionally, Weichai Lovol Smart Agriculture Technology Co., Ltd introduced the first large-language-model AI assistant capable of predicting equipment failures 72 hours in advance.

Zhengzhou Zhonglian leads the peanut harvester segment with over 200 patents, and Zhejiang Liulin exports 26 combine harvester models to Southeast Asia and Africa. However, compliance with China VI emission standards has exerted margin pressure, leading to a 13.5% revenue decline for AGCO in 2025 and a 59.6% drop in net profit for CNH. Both companies are now focusing on platforms with capacities exceeding 10 kilograms per second which is anticipated to help them grow their market share.

China Combine Harvesters Industry Leaders

Weichai Lovol Intelligent Agricultural Technology CO., LTD

Jiangsu World Agriculture Machinery Co., Ltd.

China First Tractor Group (YTO Group)

KUBOTA Corporation

Zoomlion Heavy Industry Science & Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: CLAAS introduced the combine harvester EVION 580 with a 260-horsepower Cummins engine and an 8,000-liter grain tank.

- September 2025: KUBOTA Corporation unveiled the PRO588i-G light crawler rice combine in India, showing tech spillover applicable to China’s southern paddies.

- June 2025: Zoomlion Heavy Industry Science & Technology Co., Ltd. displayed the H7-600E hybrid harvester, the world’s first hybrid combine at AGRITECHNICA 2025.

China Combine Harvesters Market Report Scope

A combine harvester is a versatile agricultural machine that enhances efficiency by performing three key harvesting operations, such as cutting (reaping), threshing, and cleaning (winnowing), in a single pass. It is used to harvest, thresh, and separate grains such as wheat, rice, corn, and soybeans from standing crops, thereby reducing labor and time requirements.

The China Combine Harvesters Market Report is segmented by type, including self-propelled, tractor-pulled, and PTO-powered modular combines, by power range, including less than 120 HP, 120–200 HP, 201–300 HP, and more than 300 HP, and by movement, including wheel type and crawler type. The market forecasts are provided in terms of value (USD).

| Self-propelled | Full-feed axial-flow |

| Full-feed tangential-drum | |

| Half-feed rice combines | |

| Tractor-pulled (trailing) | |

| PTO-powered modular combines |

| Less than 120 HP |

| 120 – 200 HP |

| 201 – 300 HP |

| More than 300 HP |

| Wheel Type | Two-wheel-drive |

| Four-wheel-drive | |

| Crawler Type | Rubber-track crawlers |

| Steel-track crawlers |

| By Type | Self-propelled | Full-feed axial-flow |

| Full-feed tangential-drum | ||

| Half-feed rice combines | ||

| Tractor-pulled (trailing) | ||

| PTO-powered modular combines | ||

| By Power Range (HP) | Less than 120 HP | |

| 120 – 200 HP | ||

| 201 – 300 HP | ||

| More than 300 HP | ||

| By Movement | Wheel Type | Two-wheel-drive |

| Four-wheel-drive | ||

| Crawler Type | Rubber-track crawlers | |

| Steel-track crawlers | ||

Key Questions Answered in the Report

What is the projected value of the China combine harvester market in 2031?

The China combine harvester market size is forecast to reach USD 6.4 billion by 2031.

Which power range is anticipated to grow fastest through 2031?

Combines above 300 horsepower are projected to expand at an 8.9% CAGR because land-consolidation pilots demand higher throughput.

How large is the 201-300 horsepower segment today?

The 201-300 horsepower class held 37% of China combine harvester market share in 2025.

Why are crawler combines gaining traction?

Crawler machines are growing at an 8.9% CAGR through 2026-2031 because paddy soils in Hunan, Jiangxi, and Heilongjiang require low ground pressure to prevent sinkage.

What factors influence equipment replacement cycles?

Higher subsidies for BeiDou-ready models, stricter 1.2% grain-loss standards, and China VI emission compliance requirements are anticipated to shorten equipment payback periods and accelerate replacement demand during the forecast period

Page last updated on: