Gelling Agent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

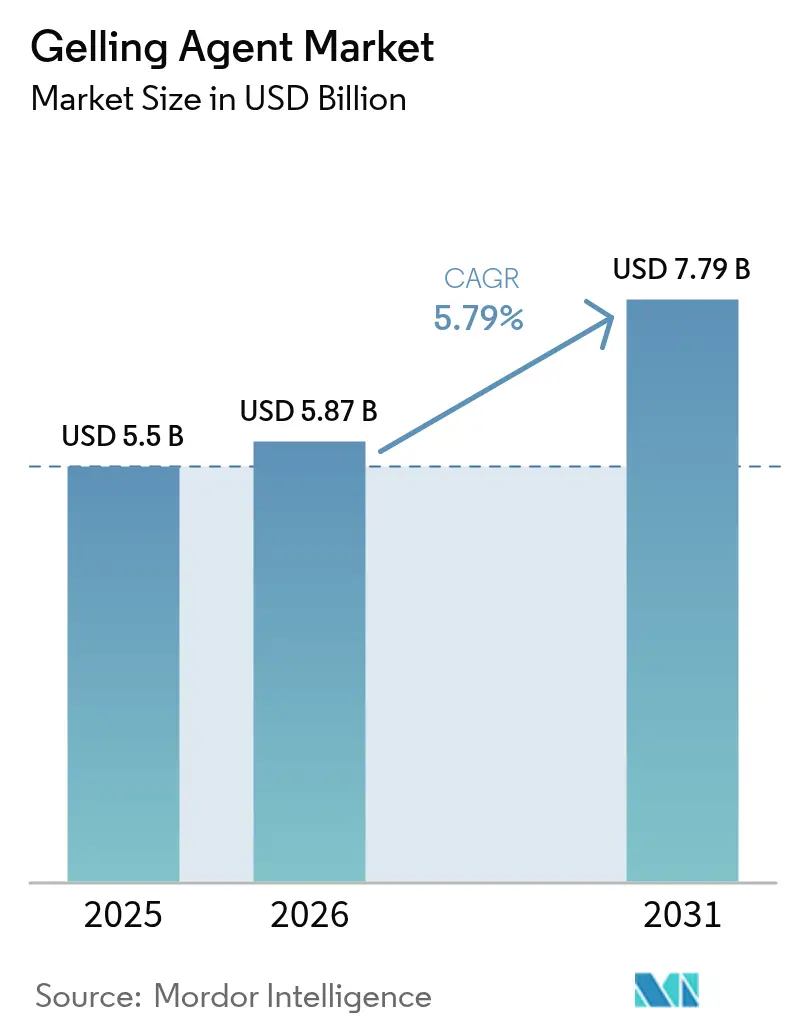

| Market Size (2026) | USD 5.87 Billion |

| Market Size (2031) | USD 7.79 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

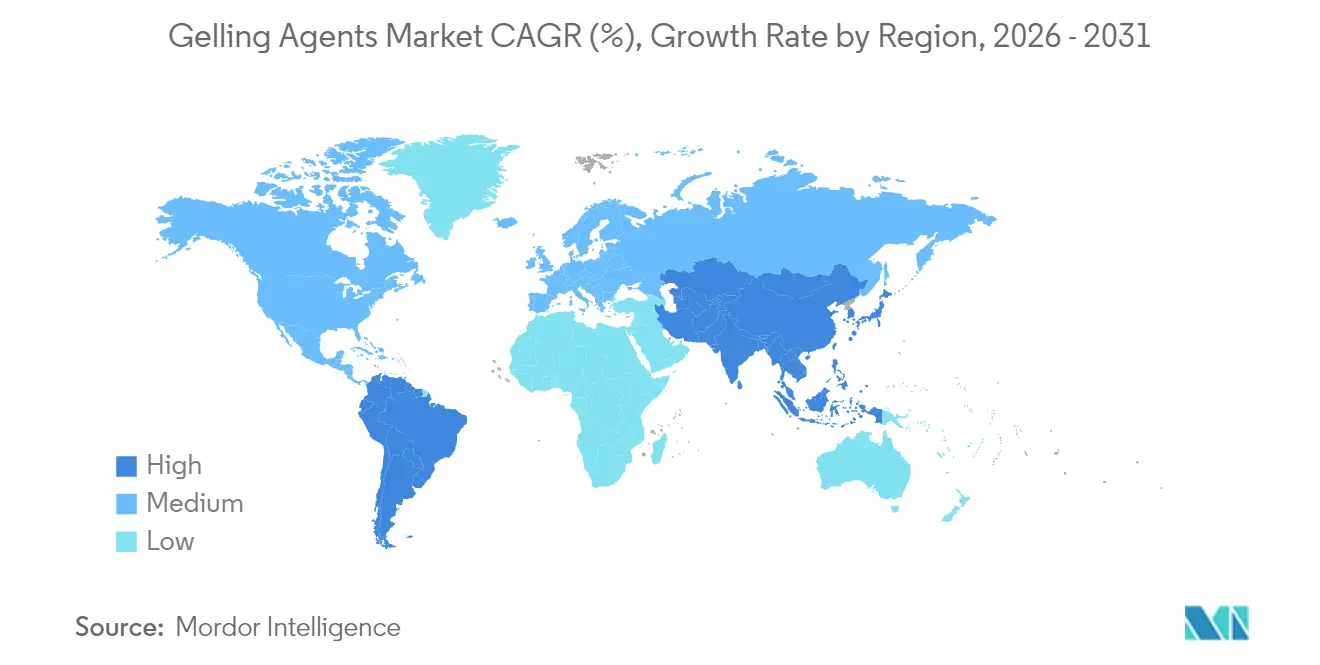

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

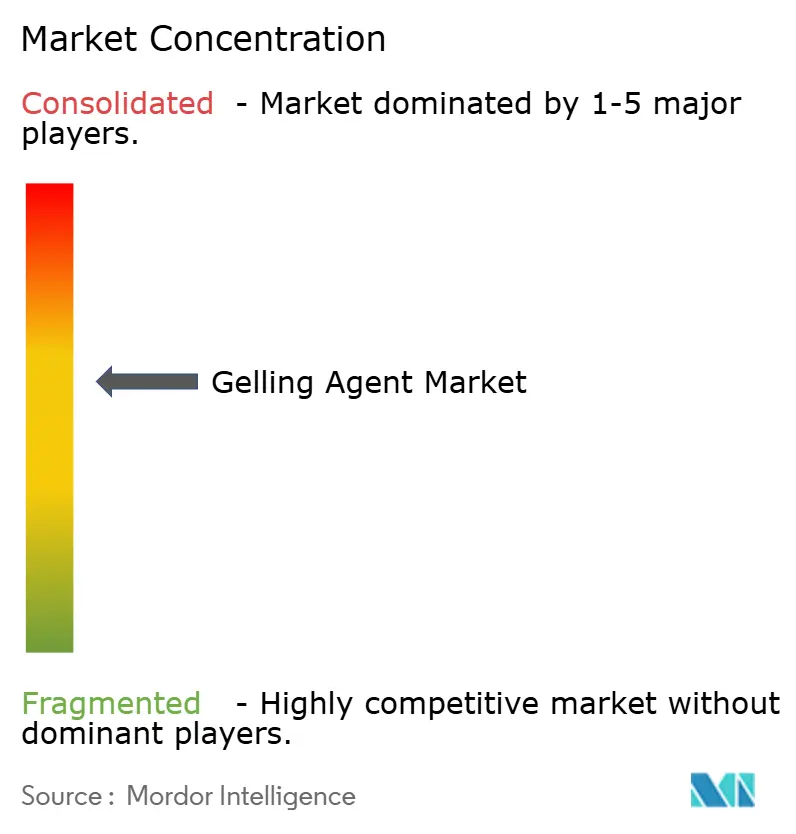

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gelling Agent Market Analysis by Mordor Intelligence

The gelling agents market size in 2026 is estimated at USD 5.87 billion, growing from 2025 value of USD 5.5 billion with 2031 projections showing USD 7.79 billion, growing at 5.79% CAGR over 2026-2031. Robust demand for clean-label ingredients, expanding applications in hydrogel-enabled drug delivery, and step-change improvements in extraction efficiency anchor this trajectory. Natural product substitution is accelerating after the United States Food and Drug Administration (FDA)[1]Food and Drug Administration, "Generally Recognized as Safe (GRAS) documentation rules", www.fda.gov strengthened Generally Recognized as Safe (GRAS) documentation rules in 2025, rewarding suppliers able to provide deep safety dossiers. Simultaneously, plant-based diets and the rise of dairy alternatives are broadening the commercial scope of high-performance hydrocolloids, while breakthroughs in microbial fermentation improve functional consistency and shorten production lead times. South America, led by Brazil’s USD 231 billion food-processing base, is becoming the fastest-growing region, whereas Asia-Pacific retains volume leadership on the back of dominant seaweed and guar cultivation [2]U.S Department of Agriculture, "food-processing base", www.fas.usda.gov.

Key Report Takeaways

• By type, pectin held 34.19% of gelling agents market share in 2024; gellan gum is forecast to expand at 8.34% CAGR through 2030.

• By source, plant-derived materials accounted for 58.45% of gelling agents market size in 2024, while microbial-derived alternatives are projected to grow at 8.56% CAGR to 2030.

• By function, thickening applications led with 27.45% revenue share in 2024; encapsulation and controlled release is advancing at 9.01% CAGR.

• By application, food and beverages commanded 35.89% share of the gelling agents market size in 2024, whereas pharmaceuticals are set to climb at 9.34% CAGR.

• By geography, Asia-Pacific contributed 36.73% of global revenue in 2024; South America is poised for 8.45% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gelling Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed and convenience food demand | +1.2% | Global; strongest in Asia-Pacific & North America | Medium term (2-4 years) |

| Clean-label and natural additive preference | +1.5% | North America & EU; spreading to Asia-Pacific | Short term (≤ 2 years) |

| Dairy and dairy-alternative consumption | +0.8% | Global; led by North America & Europe | Medium term (2-4 years) |

| Extraction and processing innovation | +1.0% | Global; R&D hubs in EU & North America | Long term (≥ 4 years) |

| Widening Addoption in Pharmaceutical Formulation | +1.0% | Global; led by North America & Europe | Long term (≥ 4 years) |

| Application in plant based meat and seafood | +0.8% | Global; led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for processed and convenience foods

Urban lifestyles and dual-income households continue to push ready-to-eat meal uptake, requiring hydrocolloids with superior freeze-thaw tolerance and thermal stability. China's imports of high-value food ingredients rose sharply in 2024, lifting regional consumption of texture enhancers, thickeners, and stabilizers. Processors are engineering hybrid systems—such as carrageenan-starch blends—to maintain viscosity across cold-chain fluctuations. These tailored formulations underpin higher specification standards in frozen entrées, soups, and premium sauces. Consequently, the gelling agents market is experiencing a product-mix shift toward multi-component solutions that guarantee texture integrity over extended shelf life. The growing adoption of plant-based alternatives in food products has increased the demand for natural gelling agents derived from seaweed and fruit sources. Additionally, manufacturers are investing in research and development to create clean-label gelling agents that meet consumer preferences for transparent ingredient lists.

Increasing demand for clean-label and natural food additives

Regulatory bodies and consumers are intensifying their examination of ingredient lists. The 2024 ban on specific synthetic dyes in California and the European Food Safety Authority's (EFSA) [3]European Food Safety Authority’s (EFSA), "tighter heavy-metal limits", www.efsa.europa.eustricter heavy-metal restrictions for guar gum demonstrate this increased oversight. Hydrocolloid suppliers with established, transparent supply chains, particularly for pectin and alginate, are securing reformulation contracts in confectionery and beverage applications. While premium natural grades cost significantly more than their chemically modified alternatives, brand owners accept these higher costs to achieve clearer labels and regulatory compliance. This transition strengthens the gelling agents market as manufacturers switch from synthetic thickeners to plant-based and seaweed-derived alternatives. The market is further bolstered by increasing consumer awareness of natural ingredients and their health benefits. Additionally, technological advancements in extraction and processing methods are enabling manufacturers to produce higher quality natural gelling agents at improved efficiency levels.

Rising consumption of dairy and dairy-alternative products

Global retail sales of plant-based beverages reached new highs in 2024, increasing the demand for hydrocolloids that replicate dairy mouthfeel. Ashland's Benecel methylcellulose, designed to enhance body and suspension in oat-milk lattes, demonstrates application-specific innovation. Carrageenan-locust bean gum combinations continue to be essential in vegan cheese slices for meltability, while gellan gum provides clarity and protein stabilization in ambient nut-milk drinks. The expansion of dairy-alternative portfolios enables multinational ingredient suppliers to enter premium nutrition segments, thus expanding the gelling agents market. The growing consumer preference for clean-label products has led manufacturers to develop natural gelling agents derived from seaweed and plant sources. Additionally, the rising adoption of gelling agents in the pharmaceutical industry for drug delivery systems and capsule manufacturing contributes to market growth.

Technological advancements in hydrocolloid extraction and processing

The extraction of pectin from citrus peels using ultrasound technology achieves higher yields while consuming less energy, enhancing cost efficiency. The implementation of AI-controlled monitoring systems for viscosity and color reduces production failures and material waste. In pharmaceutical applications, the development of pH-responsive hydrogels through green chemistry methods enables targeted drug delivery, expanding pharmaceutical applications. These technological improvements support increased profit margins for innovative suppliers and create additional product specifications that expand the gelling agents market. The food industry's growing demand for natural and clean-label ingredients has accelerated research into plant-based gelling alternatives. Additionally, the increasing adoption of gelling agents in cosmetic formulations for texture enhancement and stability has opened new market opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -0.7% | Global; highest in Asia-Pacific | Short term (≤ 2 years) |

| High extraction and purification costs | -0.5% | Global; smaller firms hardest hit | Medium term (2-4 years) |

| Stringent regulatory and clean-label compliance challenges | -0.6% | Global; highest in Northa America and Europe | Medium term (2-4 years) |

| Low awareness and adoption in emerging and underdeveloped markets | -0.3% | Asia-pacific, Africa, Latin America | Long term (4+ years) |

| Source: Mordor Intelligence | |||

Fluctuating raw material prices

Seaweed-derived carrageenan and agar remain vulnerable to climate events and trade restrictions in Indonesia and the Philippines, causing spot price swings that challenge profit forecasting. Guar gum relies heavily on monsoon patterns in India and Pakistan, where drought can cut yields up to 40%. Large buyers now use long-term offtake contracts and partial vertical integration into seaweed farming to buffer cost volatility. At the same time, fermentation-based xanthan and gellan gum provide a hedge because their carbon sources are more diversified, although they are not immune to global dextrose and energy price movements. The market's heavy dependence on specific geographic regions exposes manufacturers to significant supply chain disruptions. Natural disasters and changing weather patterns continue to threaten raw material availability and price stability. Additionally, regulatory changes in key producing countries can create unexpected barriers to trade and impact global supply dynamics.

High costs of extraction and purification processes

The gelling agents market faces significant operational challenges due to traditional extraction methods and evolving regulatory requirements. Conventional hot-acid extraction of seaweed hydrocolloids consumes significant steam and generates saline effluent that demands treatment, inflating production overheads. Continuous-flow reactors and membrane filtration reduce wastewater volumes by 30–50% but require upfront investment. Smaller regional processors struggle to finance such upgrades, limiting their ability to serve high-margin medical and cosmetics segments. The increasing environmental regulations across regions require manufacturers to implement costly wastewater treatment systems, further straining their operational budgets. Additionally, the rising energy costs and raw material prices have pushed many small and medium-sized producers to operate at reduced capacities, affecting the overall market supply. The lack of technological innovation in extraction processes has resulted in stagnant production efficiency levels across the industry. Market consolidation is expected as larger manufacturers with stronger financial capabilities acquire smaller players struggling with operational costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pectin Dominance Amid Gellan Innovation

Pectin dominated the global gelling agents market with a 33.89% revenue share in 2025, generating USD 1.88 billion. The stable supply chain from citrus peel and apple pomace, combined with increasing applications in reduced-sugar jams and nutraceutical gummies, maintains its market leadership. Cargill's recent UniPECTINE capacity expansion in Brazil demonstrates strong market confidence in sustained demand growth. The versatility of pectin in clean-label formulations and its natural origin further strengthen its market position. Consumer preference for plant-based ingredients continues to drive pectin adoption across various food applications. Gelatin maintains its strong presence in confectionery and capsule shells, although ethical and religious considerations encourage manufacturers to explore pectin-gelatin combinations.

Gellan gum, while currently occupying a smaller market share, projects a robust growth rate of 8.09% CAGR, driven by its thermoreversible properties and high efficiency at low dosages, particularly in premium dairy alternatives and ophthalmic drugs. Carrageenan and agar maintain consistent market uptake in applications requiring vegan certification, despite facing geographic supply concentration challenges. The increasing demand for plant-based alternatives in Asian markets particularly supports the growth of these marine-derived gelling agents. The continuous development of specialized gelling agents expands the overall market scope by enabling manufacturers to achieve specific functional properties in various applications. The trend toward clean-label products and natural ingredients further accelerates innovation in the gelling agents segment.

By Source: Plant-Derived Leadership Challenged by Microbial Innovation

Plant-based raw materials generated 57.92% of 2025 revenues, reinforcing consumer trust in recognizable botanical origins such as guar, locust bean, and citrus pectin. The widespread adoption of plant-based ingredients reflects the growing consumer preference for natural and sustainable food solutions. Seaweed sources, while technically plant-derived, deliver differentiated rheology that commands price premiums in dairy and meat analogues. The versatility of seaweed-based gelling agents has led to their increased incorporation in various food applications, particularly in Asian cuisine and modern plant-based products.

Microbial-derived gums—xanthan and gellan—are on track for the fastest expansion at 8.18% CAGR through 2031. Animal-derived gelatin remains critical in biomedical scaffolds and high-bloom confectionery, even as vegan claims temper volume growth. Synthetic and chemically modified alternatives keep niche relevance where exacting functional thresholds outweigh clean-label positioning. The mix shift toward fermentation platforms helps diversify supply and dampen raw-material risk for the gelling agents industry. The advancement in fermentation technology has improved production efficiency and reduced costs, making microbial-derived gums more commercially viable. The increasing investment in research and development of novel fermentation processes is expected to further enhance the quality and functionality of microbial gelling agents.

By Function: Thickening Applications Lead While Encapsulation Accelerates

Thickening retained 27.12% of 2025 turnover, reflecting the central role of hydrocolloids in viscosity control for soups, sauces, and dairy desserts. The increasing consumer preference for convenience foods has accelerated the adoption of thickening agents in ready-to-eat products. Robust conversion to instant mixes and frozen entrées safeguards baseline demand, while manufacturers continue to innovate with clean-label thickening solutions to meet evolving consumer preferences.

Encapsulation and controlled-release systems will post the highest 8.62% CAGR as pharmaceutical and nutraceutical players exploit hydrogel matrices to regulate bio-active release. Recent approvals of sodium alginate edible coatings for fresh produce preservation illustrate cross-sector uptake according to food standards agency (UK). Multi-functional products combining gelation, stabilization, and encapsulation within one hydrocolloid blend open new design latitude for formulators, supporting additional revenue streams for the gelling agents market. The integration of nanotechnology in encapsulation systems has enhanced the efficiency of active ingredient delivery. The development of sustainable and biodegradable encapsulation materials aligns with growing environmental concerns and regulatory requirements.

By Application: Food Dominance Amid Pharmaceutical Acceleration

Food and beverage manufacturers absorbed 35.41% of global sales in 2025, spotlighting hydrocolloids' ubiquity in texture, suspension, and moisture control. Gluten-free bakery, low-sugar confectionery, and premium ice-cream lines act as innovation hotbeds where differentiated mouthfeel commands shelf premiums. The increasing consumer demand for clean-label products has further accelerated hydrocolloid adoption in natural formulations. Manufacturers are investing heavily in research and development to optimize hydrocolloid combinations that deliver superior functionality at lower usage levels.

Pharmaceutical applications, however, will register the quickest 8.97% CAGR. Cosmetics, personal care, and pet nutrition round out the portfolio, each capitalizing on the moisture-binding and film-forming attributes inherent to hydrocolloids. The broadening use cases reinforce the structural growth narrative for the gelling agents market. The pharmaceutical sector's rapid growth stems from increased tablet coating applications and controlled-release drug delivery systems. Rising healthcare expenditure and pharmaceutical manufacturing expansion in emerging economies further strengthen the demand outlook.

Geography Analysis

Asia-Pacific accounted for 36.28% of global revenue in 2025, buoyed by dominant seaweed and guar cultivation plus the world’s largest population of processed-food consumers. China alone supplies more than 60% of global carrageenan and agar raw material, while India produces roughly 80% of guar gum. Rapid urbanization and rising disposable incomes in Southeast Asia further stimulate convenience-food demand, reinforcing regional buying power.

South America delivers the fastest 8.12% CAGR projection through 2031. Brazil’s USD 231 billion food-processing industry, which logged 7.2% growth in 2024, underpins a surge in demand for functional ingredients that extend shelf life in tropical distribution conditions according to U.S Department of Agriculture. Abundant citrus and sugarcane residues also present cost-effective substrates for future pectin and xanthan production, enhancing import substitution prospects. Collectively, these regional dynamics diversify revenue streams and mitigate single-market exposure for global participants in the gelling agents market.

North America and Europe contribute lower volume yet higher unit value, thanks to strict regulatory regimes and advanced R&D ecosystems. The FDA’s 2025 GRAS reforms accelerate clean-label substitution, coaxing formulators to secure supply from pectin, alginate, and celluloses with proven safety records. Europe’s sustainability ethos and EFSA’s rigorous contaminant limits incentivize traceable supply chains and green extraction technologies, elevating profit pools for compliant suppliers.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The gelling agents market shows moderate consolidation with a concentration ratio of 6 out of 10. The top five companies - Tate & Lyle, CP Kelco, Cargill, Ashland, and Jungbunzlauer - account for the majority of market revenue in 2024. These companies benefit from economies of scale, enabling vertical integration in raw material procurement and investments in extraction and fermentation capabilities.

Tate & Lyle's USD 1.8 billion acquisition of CP Kelco demonstrates the industry trend toward specialty hydrocolloids expansion, enabling enhanced cross-selling opportunities and research synergies. Companies differentiate through technological capabilities - Jungbunzlauer operates a continuous fermentation xanthan gum facility in Canada to reduce emissions, while Cargill implements artificial intelligence for quality control. The increase in patent applications for pH-responsive hydrogels and multi-polymer complexes indicates growing competition in intellectual property.

Mid-sized companies focus on specialized applications, including tissue scaffolds and biodegradable packaging, utilizing their flexibility and close customer relationships. Large companies invest in seaweed farming operations and fermentation alternatives to protect against raw material supply fluctuations and weather-related disruptions. This diverse range of business strategies maintains market competition and supports continuous innovation in the gelling agents industry.

Gelling Agent Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ashland Global Holdings

-

Tate and Lyle plc

-

International Flavors and Fragrances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GELITA introduced Endotoxin Controlled Excipients (ECE) for bioscience applications. The product line includes VACCIPRO and MEDELLAPRO, which meet the requirements of biomedical and pharmaceutical applications. The ECE portfolio consists of medical-grade gelatins and collagen peptides for biomedical applications. VACCIPRO and MEDELLAPRO offer stability, biocompatibility, and support the development of safe and effective products.

- September 2024: Jungbunzlauer, a producer of ingredients from natural sources, invested USD 200 million to establish Canada's first xanthan gum manufacturing facility in Port Colborne, Ontario, with support from Invest Ontario.

- June 2024: Tate & Lyle completed acquisition of CP Kelco for USD 1.8 billion, creating leading global specialty food and beverage solutions business with enhanced capabilities in pectin and specialty gums. The transaction strengthens market position in the USD 19 billion specialty ingredients sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence treats the gelling agents market as the annual revenues generated from natural or semi-synthetic hydrocolloids, such as pectin, gelatin, agar, carrageenan, alginate, gellan, xanthan, guar, and selected cellulose or locust-bean gums, sold in bulk or formulated form to food, beverage, personal-care, and pharmaceutical manufacturers worldwide.

Scope exclusion: industrial drilling and paper-grade thickeners fall outside this study.

Segmentation Overview

-

By Type

- Pectin

- Gelatin

- Agar

- Carrageenan

- Alginate

- Gellan Gum

- Xanthan Gum

- Guar Gum

- Cellulose Derivatives

- Locust Bean Gum

- Others

-

By Source

- Plant-derived

- Seaweed-derived

- Microbial-Derived

- Animal-derived

- Synthetic/Chemically-modified

-

By Function

- Gelling

- Thickening

- Stabilising/Emulsifying

- Film-forming and Coating

- Encapsulation/Controlled Release

-

By Application

-

Food and Beverage

- Bakery

- Confectionery

- Dairy and Frozen Desserts

- Beverages

- Meat and Poultry Products

- Plant-based and Vegan Alternatives

- Pet Food

- Other Food and Beverage Applications

-

Cosmetics and Personal Care

- Skin-care

- Hair-care

- Oral-care

- Colour Cosmetics

- Pharmaceuticals

- Others

-

Food and Beverage

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview procurement heads at food processors, regional distributors, and formulation scientists across Asia-Pacific, Europe, and North America to validate average selling prices, purity-grade splits, and substitution trends.

Follow-up surveys with nutraceutical brands test adoption rates for next-gen plant gums and feed findings back into the model.

Desk Research

We start with open data sets from agencies that track agricultural output and trade (USDA, Eurostat, FAO), customs shipment records, and tariff schedules that list each hydrocolloid under distinct HS codes.

Industry position papers from bodies such as the International Pectin Producers Association, Seaweed Industry Association, and Gelatin Manufacturers Institute of America help clarify supply shifts.

Company 10-Ks, investor decks, and patent filings reveal capacity expansions or process innovations, while news archives in Dow Jones Factiva give context on pricing moves.

This list is illustrative; many other sources underpin the model.

Market-Sizing & Forecasting

A top-down construct translates production and trade data into an apparent consumption pool, which is then reconciled with bottom-up checks built from sampled ASP times volume calculations at leading suppliers.

Key drivers, citrus peel availability, gelatin slaughter yields, vegan product launches, seaweed farming acreage, regulatory label changes, and average inclusion rates per finished good, anchor yearly growth assumptions.

Multivariate regression coupled with scenario analysis projects 2025 to 2030 demand; missing inputs are bridged through price-volume elasticity ranges discussed with experts.

Data Validation & Update Cycle

Outputs pass variance screens against historical price indices and quarterly shipment trends before senior review.

The study updates every twelve months, with interim refreshes triggered by material events such as crop failures or major capacity additions, ensuring clients receive the freshest view.

Why Our Gelling Agents Baseline Commands Reliability

Published estimates seldom match because firms differ on additive grades, currency conversions, and refresh cadence.

Key gap drivers here include whether pharmaceutical excipients are counted, the treatment of low-viscosity starch blends, and how average selling prices are smoothed during raw-material spikes, which Mordor revisits each quarter, whereas others update less often.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.55 B (2025) | Mordor Intelligence | - |

| USD 4.52 B (2022) | Global Consultancy A | Excludes cosmetic grades and converts at fixed 2021 FX rates |

| USD 5.37 B (2025) | Trade Journal B | Relies on supplier press releases without shipment reconciliation |

| USD 5.19 B (2025) | Regional Consultancy C | Aggregates plant and animal agents but omits microbial gellan volumes |

Taken together, the comparison shows that Mordor's transparent scope choices, rolling price audits, and hybrid modeling keep the baseline balanced and traceable, giving decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the gelling agents market?

The gelling agents market size reached USD 5.87 billion in 2026 and is projected to climb to USD 7.79 billion by 2031 at a 5.79% CAGR.

Which product type holds the largest market share?

Pectin leads with 33.89% gelling agents market share in 2025 due to its versatility in reduced-sugar foods and nutraceutical gummies.

What is driving pharmaceutical demand for gelling agents?

Hydrogel-based formulations enable controlled and targeted drug delivery, propelling pharmaceutical applications at a 8.97% CAGR.

Which region is expected to grow the fastest?

South America, anchored by Brazil’s expanding food-processing industry, is forecast to achieve an 8.12% CAGR between 2026 and 2031.

Page last updated on: