Release Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

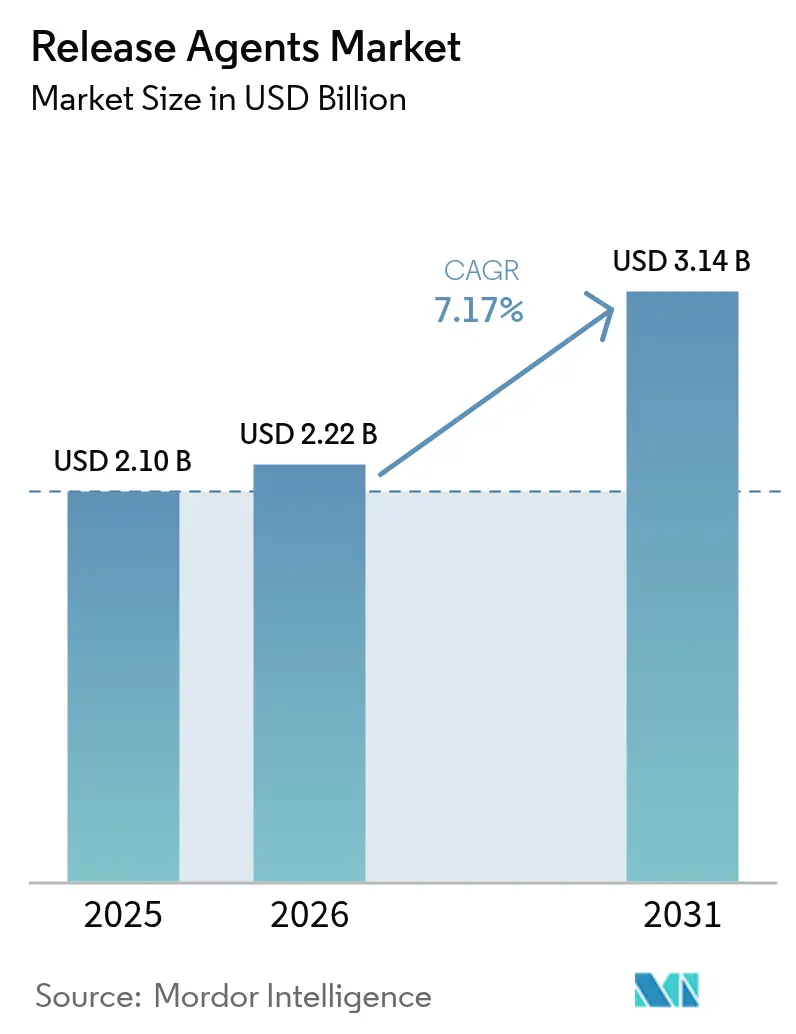

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 3.14 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Release Agents Market Analysis by Mordor Intelligence

The release agents market size was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 3.14 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031). This growth reflects manufacturers' efforts to balance strict food-contact regulations with automated production requirements. The market expansion is supported by infrastructure investments in emerging economies, particularly in the Asia-Pacific region, where the growth of dairy, meat, and convenience food operations exceeds local expertise in specialized release technologies. Companies are focusing on PFAS-free formulations, biodegradable wax esters, and plant-based oils to meet sustainability goals and consumer transparency demands while maintaining effective anti-stick properties. Additionally, fluctuating commodity prices and regional migration testing requirements are driving supplier consolidation, emphasizing the importance of regulatory compliance and reliable global supply chains.

Key Report Takeaways

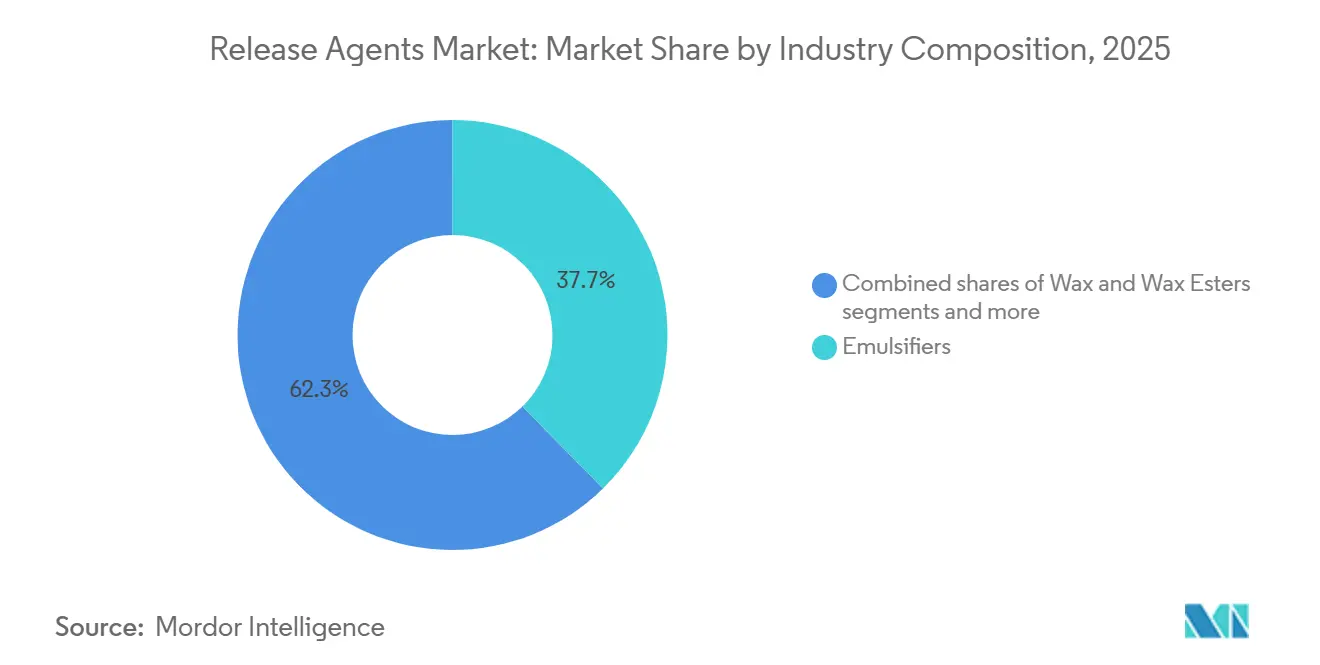

- By industry composition, emulsifiers led with 37.66% of the release agents market share in 2025, while wax and wax esters are projected to expand at a 8.16% CAGR through 2031.

- By form, liquid and spray formats held 51.29% revenue share of the release agents market in 2025; solid formats are set to register a 8.01% CAGR between 2026 and 2031.

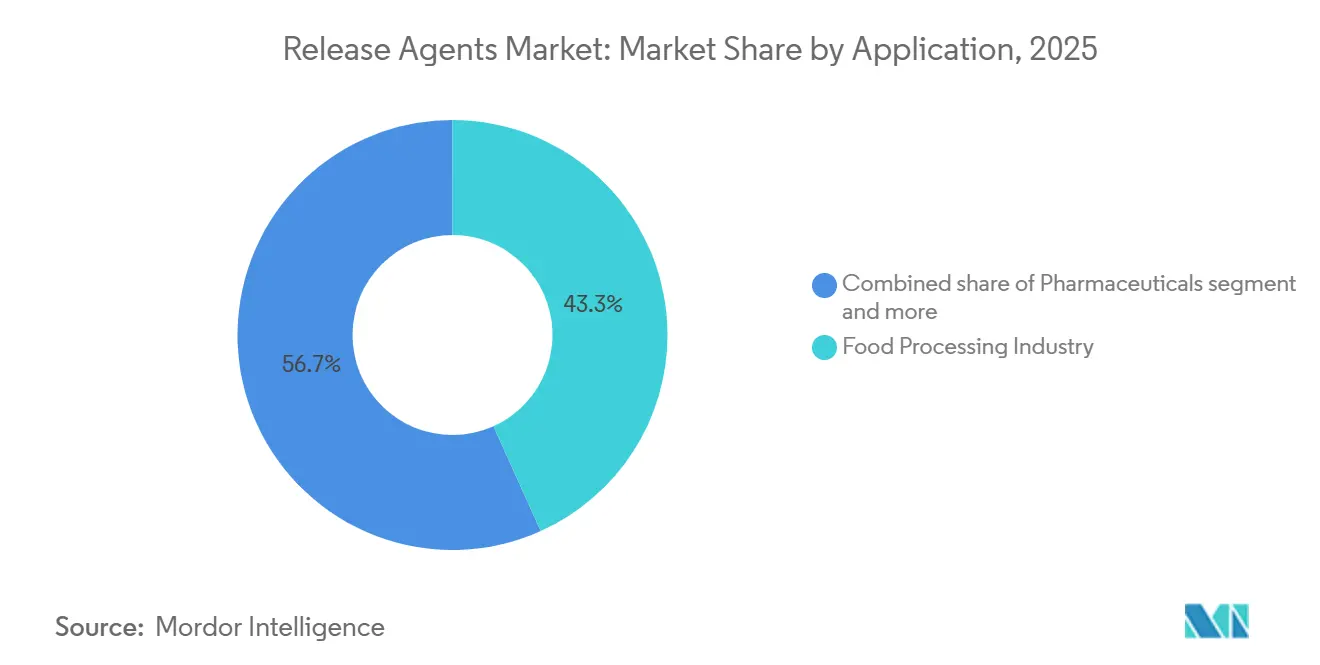

- By end-use industry, the food-processing industry accounted for 43.27% of the release agents market in 2025, whereas pharmaceuticals and healthcare are advancing at a 8.73% CAGR to 2031.

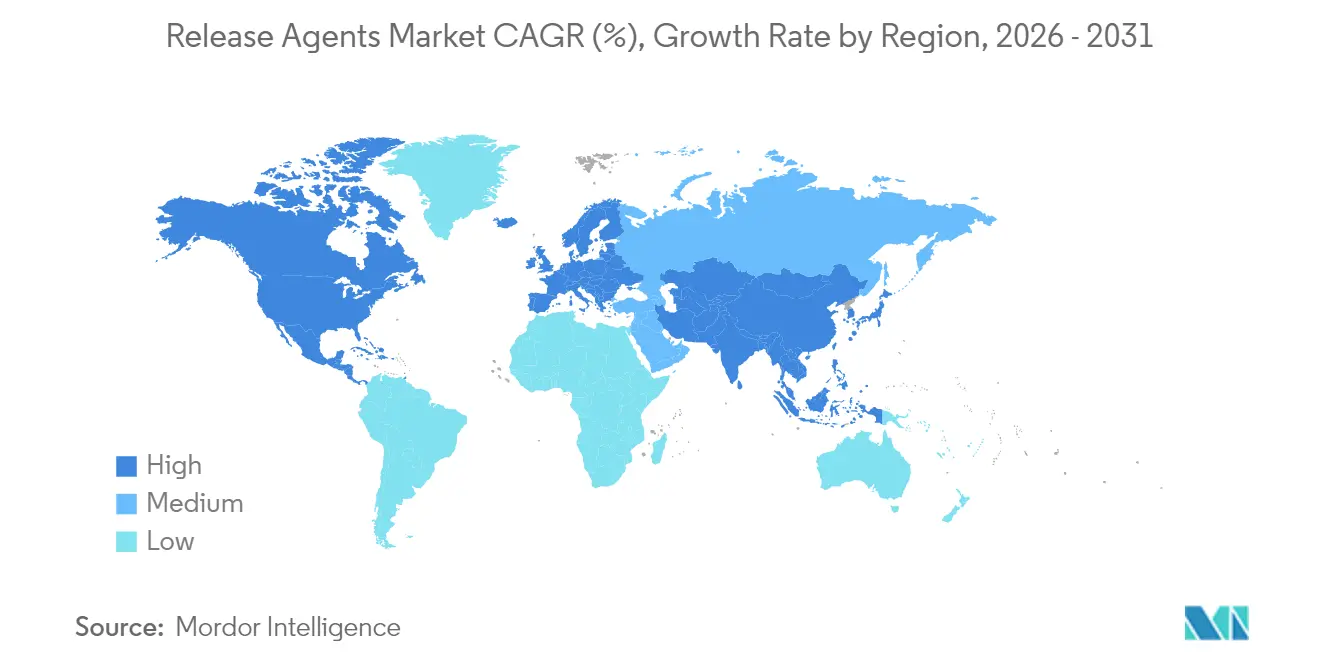

- By geography, North America commanded 33.28% revenue share in 2025; Asia-Pacific is forecast to record the fastest 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Release Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for non-hydrogenated vegetable oils | +1.2% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Expanding food processing industry | +1.8% | Asia-Pacific core, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Regulatory push for food-grade, compliant release agents | +0.9% | North America and Eurpoean Union, emerging compliance in Asia-Pacific | Short term (≤ 2 years) |

| Shift toward clean-label, plant-based formulations | +1.1% | Global, premium segments in North America and Western Europe | Medium term (2-4 years) |

| Technological advances in high-performance water-based systems | +0.8% | Global, early adoption in North America and European Union | Long term (≥ 4 years) |

| Rising demand for packaged and convenience foods | +1.5% | Asia-Pacific and Middle East, steady in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Preference for non-hydrogenated vegetable oils

Manufacturers are shifting to alternatives like liquid vegetable oils and interesterified fats in response to the phase-out of partially hydrogenated oils. These substitutes match pan-release performance while eliminating trans-fatty-acid residues, meeting regulatory standards and consumer preferences. Regulatory changes have driven bakeries to adopt safer, sustainable oil blends, ensuring compliance and catering to the demand for cleaner labels and certifications like non-GMO and organic. In Europe, restrictions on trans fats have accelerated the use of enzymatically modified lipids as replacements for hydrogenated shortenings. However, smaller formulators face challenges as larger, vertically integrated firms leverage technological and operational advantages to dominate the market.

Expanding food processing industry

The food manufacturing sector across the Asia-Pacific region is witnessing significant growth, reshaping the demand for release agents. India, one of the largest milk producers globally, has achieved notable advancements in its dairy processing ecosystem, as reported by the Ministry of Food Processing Industries. The country’s milk production rose from 230.58 million tonnes in 2022-23 to 239.30 million tonnes in 2023-24, reflecting a 3.78% growth [1]Source: Ministry of Food Processing Industries "Sector Profile Dairy", mofpi.gov. Dairy cooperatives are investing in ice-cream and paneer production facilities, emphasizing high-throughput automation to ensure efficiency and maximize yield. Processors are adopting premium emulsifier blends, despite their higher cost, to prevent downtime caused by sticking. In Japan, the convenience-store sector is driving demand for release agents that withstand retort sterilization while maintaining taste neutrality, favoring lecithin-polyglycerol ester hybrids. Latin America’s meat-processing industry is expanding, with new sausage-casing lines in Brazil and Argentina by 2025, requiring food-grade lubricants compliant with MERCOSUR Regulation GMC/RES No 26/03.

Regulatory push for food-grade, compliant release agents

Regulatory authorities worldwide are driving the demand for food-grade, compliant release agents by implementing stricter safety standards. In the European Union (EU), regulations such as Framework Regulation 1935/2004 and GMP Regulation 2023/2006 ensure that food contact materials, including release agents, are manufactured using approved substances and follow Good Manufacturing Practices (GMP). These regulations also require that materials do not transfer harmful chemicals into food. In the United States, the FDA's Code of Federal Regulations 21 (CFR 21) mandates the approval of substances used in food contact materials and emphasizes safety through compliance testing [2]Source: U.S. Food and Drug Administration, "Determining the Regulatory Status of Components of a Food Contact Material", fda.gov. In China, recent updates to food contact legislation have introduced specific standards for food-grade materials, requiring migration testing and GMP adherence. This regulatory push is encouraging food and beverage original equipment manufacturers (OEMs) to collaborate with suppliers who understand and comply with these evolving standards, ensuring the safe use of release agents in the market.

Shift toward clean label, non-hydrogenated, and plant-based formulations

As consumers grow wary of synthetic additives, manufacturers are reformulating products, often surpassing regulatory standards. This trend is reshaping release-agent portfolios. Sunflower-derived lecithin is replacing soy-based alternatives, avoiding allergen declarations and appealing to non-GMO-conscious consumers. Carnauba wax, once limited to confectionery glazes, is now used in bakery pan coatings due to its plant-based nature, despite its higher cost. In plant-based meats, release agents prevent protein isolates from sticking to equipment. Blends of rice-bran oil and candelilla wax are emerging as preferred alternatives to mineral oils. Formulators are also exploring enzymatically produced mono- and diglycerides from non-hydrogenated palm stearin, offering emulsification benefits without synthetic labels. However, ensuring thermal stability remains a challenge, as many plant-based alternatives degrade at high temperatures, limiting their use in baking and frying.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.7% | Global, acute in APAC and South America | Short term (≤ 2 years) |

| Low end-user awareness in emerging meat-processing clusters | -0.4% | Sub-Saharan Africa, Southeast Asia, parts of South America | Medium term (2-4 years) |

| Ingredient transparency concerns hinder adoption | -0.3% | North America and EU premium channels | Medium term (2-4 years) |

| Environmental and safety concerns restrict growth | -0.5% | Global, regulatory focus in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material price volatility

Volatility in raw material prices poses a significant restraint for the release agent market, as fluctuations in the costs of key inputs like vegetable oils, waxes, and silicones directly impact production expenses and disrupt pricing strategies. For instance, the FAO Vegetable Oil Price Index averaged 168.6 points in January, reflecting a 3.4-point 2.1% increase from December and a 10.2% rise year-over-year, driven by higher global prices for palm, soy, and sunflower oils [3]Source :Food and Agriculture Organization of United Nations, "FAO Food Price Index falls for fifth consecutive month in January 2026", driven by lower dairy, meat and sugar prices", fao.org. Notably, international palm oil prices experienced a second consecutive monthly rise due to seasonal production slowdowns in Southeast Asia and robust global import demand. Such unpredictability in raw material costs can disrupt supply chains, reduce profit margins, and hinder market growth during the forecast period. These fluctuations highlight the challenges manufacturers face in maintaining stable operations and profitability, further emphasizing the impact of raw material price volatility on the market's growth potential.

Low end user awareness in emerging meat processing clusters

In sub-Saharan Africa and parts of Southeast Asia, meat processors often rely on basic release solutions like vegetable shortening, mineral oil, or even diesel fuel in informal operations. This is mainly due to limited awareness of food-grade alternatives and a lack of technical support. Many small-scale sausage manufacturers in Nigeria, for example, are unfamiliar with approved release agents and struggle to source them locally. As a result, they often use palm oil, which can lead to inconsistent results and hygiene concerns. Even as multinational meat companies expand into these regions, local suppliers dominate the small-scale market and are hesitant to invest in higher-quality inputs since consumers tend to focus more on price than on food safety. Similarly, in Vietnam, the processed-meat sector faces challenges, with many provincial processors not using food-grade lubricants for their equipment. This has created a divide in the market, where export-focused facilities follow international standards, while domestic-focused operations remain underserved, limiting the overall market's growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry Composition: Emulsifiers lead, wax esters accelerate

Emulsifiers captured 37.66% of the release agents market share in 2025, reflecting their dual role as dough conditioners and pan-release components in large-scale bakery operations. The market for emulsifiers is expected to grow steadily, driven by clean-label initiatives supported by enzymatically derived mono- and diglycerides. Lecithin remains dominant, but plant-based alternatives like sunflower and canola are gaining popularity due to allergen concerns with soy. Antioxidants such as mixed tocopherols enhance shelf life in high-oleic formulations, aiding global distribution. Meanwhile, declining demand for polymeric resins and fluoropolymers under PFAS scrutiny is pushing bakeries toward ceramic-coated pans compatible with lecithin or wax sprays.

Wax and wax esters are projected to outpace other industry composition segments with an 8.16% CAGR, supported by carnauba’s high melting point and beeswax’s pharmaceutical compatibility. Confectioners use wax blends to prevent bloom, while tablet manufacturers leverage their controlled-release properties. Candelilla wax, though supply-constrained at around 1,200 tons annually, caters to vegan bakery niches. Regional regulatory differences, such as Japan’s restrictions on certain wax esters, require formulation adjustments, but the global trend favors natural waxes as synthetic polymers are phased out.

By Form: Spray dominance, solid gains in automation

Liquid and spray releases comprised 51.29% of 2025 revenue as processors favored ease of handheld or automated aerosol application. Sprays are highly valued for their ability to provide precise dosing, which minimizes residue that could otherwise hinder crust development in artisan bread. In addition, the pharmaceutical industry depends on uniform aerosol coverage to reduce the risk of tablet defects during production. The liquid segment plays a leading role in the market, integrating seamlessly with spray technologies. This integration not only reduces material waste but also ensures consistent and even application, making it a preferred choice across various industries.

Solid release agents are projected to grow at a CAGR of 8.01% through 2031, driven by their increasing use in automated pan lines that benefit from dust-free wax-lecithin blends. These solid formulations are particularly suitable for environments requiring long-term storage or those exposed to extreme temperatures, as they maintain their effectiveness under such conditions. Furthermore, their adoption is supported by cost efficiency, as they help manufacturers save on consumable volumes. This combination of durability and cost savings makes solid release agents an attractive option for automation-focused production processes.

By End-Use Industry: Food processing anchors, pharma surges

The food-processing sector retained 43.27% of global volume in 2025, driven by strong demand from bakeries, confectioners, and meat processors for consistent non-stick performance in mixed-dough and high-protein matrices. Industrial baking, characterized by high pan-turnover intensity, has amplified the need for release agents that can endure repeated exposure to temperatures of 200°C without compromising performance. This demand is further fueled by the growing focus on efficiency and quality in food production processes. Additionally, snack manufacturers are increasingly adopting water-based agents, which offer the dual benefits of effective non-stick properties and simplified clean-in-place routines. These trends underline the critical role of advanced release agents in meeting the evolving needs of the food-processing industry.

The pharmaceutical and healthcare sectors are projected to grow at a strong CAGR of 8.73% by 2031. High-speed tablet presses, which produce large volumes of units per hour, are increasingly using next-generation lubricants like sodium stearyl fumarate and glyceryl behenate to avoid the dissolution-rate issues associated with magnesium stearate. In the construction sector, formwork applications maintain modest but stable demand, particularly where LEED guidelines encourage the use of biodegradable soy-methyl-ester systems. While cosmetics and rubber molding remain niche segments, medical-device silicone applications requiring FDA 21 CFR-compliant release agents are expanding, creating high-margin specialty opportunities within the broader release agents market.

Geography Analysis

In 2025, North America contributed 33.28% of the market value, primarily due to stringent FDA regulations that allow only pre-approved food-contact substances. The growing snack-food industry in Mexico, which adheres to global technical standards, has significantly boosted the demand for NSF-certified lubricants. Although the region's growth is slowing as the market matures, there are still opportunities driven by the replacement cycles for PFAS-free coatings. These coatings are critical in the release agents market, ensuring compliance with safety regulations and maintaining product performance. Additionally, the region's established infrastructure and focus on innovation continue to support market stability and growth.

Asia-Pacific is expected to register the fastest growth globally, with a projected CAGR of 8.04%. This growth is largely attributed to China's expansion of frozen-food production facilities and India's modernization of dairy plants to meet rising domestic and export demands. In Japan, convenience stores are increasingly favoring high-stability emulsifiers that meet retort-resistance requirements, replacing traditional lecithin. Australia's meat exporters are adopting food-grade lubricants to meet stringent residue testing standards in Asian markets. However, countries like Cambodia and Myanmar face challenges due to underdeveloped distributor networks and limited market penetration. Despite these hurdles, investments in regional technology hubs, such as Palsgaard's Shanghai facility, are gradually improving market accessibility and fostering growth across the region.

Europe is projected to hold a significant share of the 2025 market revenue, with Germany, the United Kingdom, and France leading due to their large industrial bakeries that adhere to strict EFSA migration thresholds. The Netherlands is focusing on using carnauba wax in its chocolate production to prevent bloom, while Spain is utilizing locally sourced olive-pomace derivatives in spray formulations to enhance product quality. In South America and the Middle East and Africa, Brazil's investments in meat processing and the UAE's free-zone incentives are attracting multinational companies. However, these regions face challenges such as inadequate cold-chain infrastructure and limited technical support, which hinder the full adoption of advanced release systems. Despite these obstacles, ongoing investments and government initiatives in these regions are expected to create growth opportunities in the coming years.

Competitive Landscape

In 2025, the release agents market exhibits moderate consolidation and is led by five major players: Cargill, Incorporated, Archer Daniels Midland, Bunge Limited, and Kerry Group. These companies benefit from their vertically integrated oilseed operations, which allow them to manage input cost fluctuations effectively, invest in research and development, and maintain extensive global distribution networks. Their scale and operational efficiency provide them with a competitive edge in the market. At the same time, niche players like Palsgaard and Dow are focusing on specialized segments to differentiate themselves. Palsgaard’s ability to offer on-site troubleshooting has enabled it to secure bakery contracts with a 10-15% price premium, while Dow has positioned itself as an innovator by filing 14 PFAS-free patents in 2025, anticipating future regulatory changes.

The competitive landscape is also influenced by emerging opportunities in plant-protein emulsifiers derived from mung beans or faba beans, which align with the growing consumer preference for locally sourced ingredients in the plant-based meat sector. Additionally, construction formwork release agents are gaining attention, particularly soy-methyl-ester blends that meet LEED (Leadership in Energy and Environmental Design) standards and reduce dependency on traditional solvents. However, the market presents significant challenges for new entrants due to high barriers such as stringent multi-region regulatory compliance and the requirement for comprehensive toxicological data. Companies that can navigate these complexities and deliver innovative, compliant solutions are likely to strengthen their market position.

Competition in the release agents market is further shaped by the strategic importance of patent portfolios and application-center footprints. Larger players are expanding their intellectual property assets to secure long-term advantages, while smaller companies are focusing on specialized applications to establish their presence. Regional dynamics also play a critical role in defining the competitive landscape. In North America and Europe, companies are emphasizing sustainability and regulatory compliance to meet evolving standards. In Asia-Pacific, rapid industrialization and the expansion of the food processing industry are driving demand for advanced solutions. Meanwhile, in Latin America and the Middle East and Africa, steady growth is supported by increasing investments in food production and infrastructure development. Across all regions, the ability to innovate and adapt to market demands remains a key factor in maintaining competitiveness.

Release Agents Industry Leaders

-

Archer Daniels Midland Company

-

AAK AB

-

Palsgaard A/S

-

Dow Inc.

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Synova, a division of Bundy Baking Solutions and a leading manufacturer of release agents for the baking, restaurant, and foodservice sectors, announced the expansion of its product portfolio with the launch of new Integra release agents.

- March 2025: Chem-Trend, a frontrunner in mold release solutions, introduced Chem-Trend SL-10187 as an important development, designed for high-pressure aluminum casting. This release agent improved performance and operational efficiency while offering better biostability.

- October 2024: ChemPoint and PLZ Corp announced their partnership to enhance the sales and distribution of food release agents. This collaboration aimed to leverage ChemPoint's expertise in marketing and distribution with PLZ Corp's manufacturing capabilities.

Global Release Agents Market Report Scope

Release agents, or parting agents, are substances used in production facilities as a barrier between the product and the mold, belt, or pan. The Release Agents Market Report Segments by the Industry Composition (Emulsifiers, Antioxidants, Vegetable Oils, Wax and Wax Esters, and More), Form (Liquid/Spray, Solid), End-Use Industry (Bakery and Confectionery, Meat and Meat Products, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Emulsifiers |

| Antioxidants |

| Vegetable Oils |

| Wax and Wax Esters |

| Others |

| Liquid/Spray |

| Solid |

| Food Processing Industry | Bakery and Confectionery |

| Meat and Meat Products | |

| Dairy and Frozen Desserts | |

| Others | |

| Construction and Materials | |

| Pharmaceuticals and Healthcare | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Composition | Emulsifiers | |

| Antioxidants | ||

| Vegetable Oils | ||

| Wax and Wax Esters | ||

| Others | ||

| By Form | Liquid/Spray | |

| Solid | ||

| By End-Use Industry | Food Processing Industry | Bakery and Confectionery |

| Meat and Meat Products | ||

| Dairy and Frozen Desserts | ||

| Others | ||

| Construction and Materials | ||

| Pharmaceuticals and Healthcare | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the release agents market in 2031?

It is forecast to reach USD 3.14 billion by 2031, expanding at a 7.17% CAGR from 2026.

Which region will grow fastest through 2031?

Asia-Pacific is projected to post the quickest 8.04% CAGR, led by new frozen-food and dairy capacity.

Which composition segment dominates current demand?

Emulsifiers lead, holding 37.66% of 2025 revenue due to their dual release and dough-conditioning roles.

Why are wax esters gaining popularity?

They integrate seamlessly with automated spray systems, ensuring uniform coverage and minimal waste.

Page last updated on: