Food Release Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

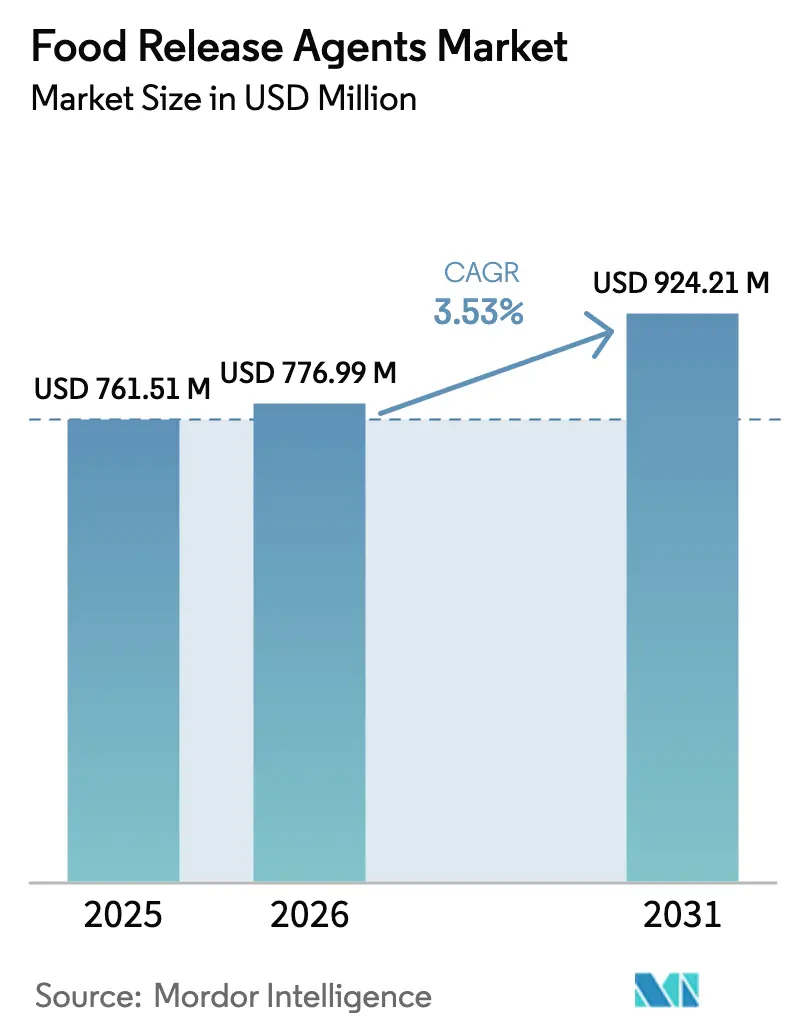

| Market Size (2026) | USD 776.99 Million |

| Market Size (2031) | USD 924.21 Million |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

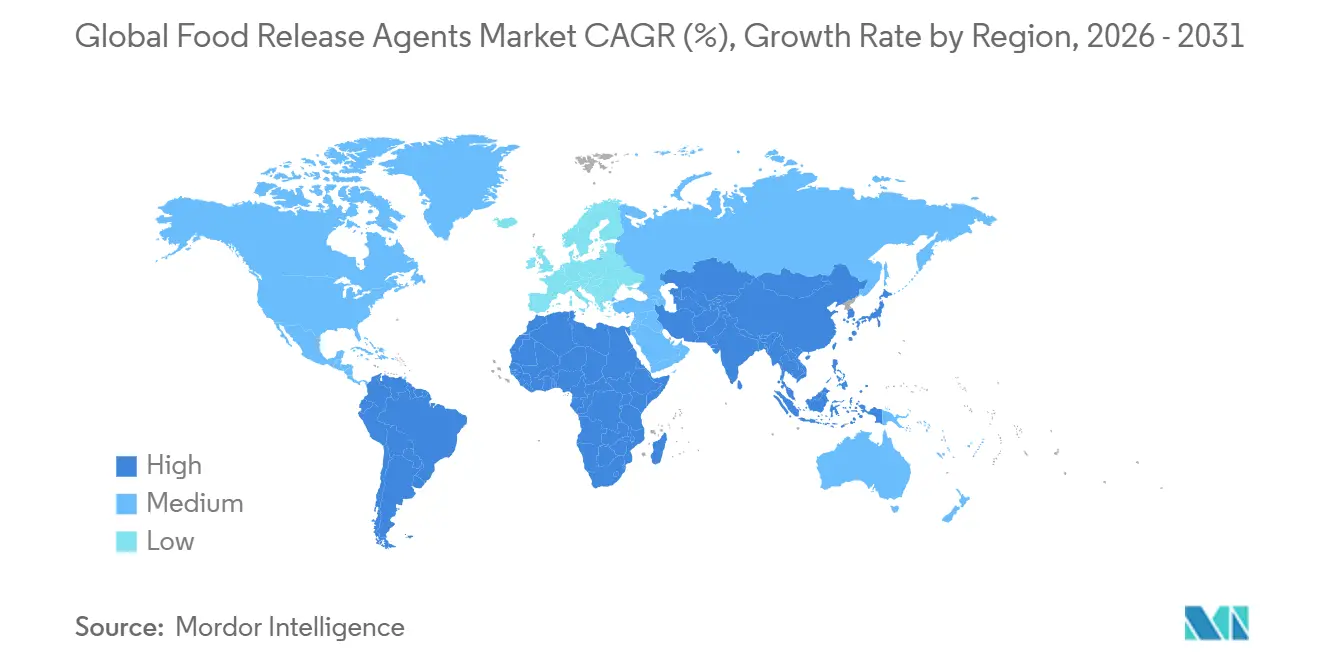

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Release Agents Market Analysis by Mordor Intelligence

The food release agents market size was valued at USD 761.51 million in 2025 and is estimated to grow from USD 776.99 million in 2026 to reach USD 924.21 million by 2031, at a CAGR of 3.53% during the forecast period (2026-2031). Bio-based agents are gaining traction due to European Union bans on bisphenol A (BPA), consumer resistance to petroleum-based additives, and the efficiency of concentrated plant-based formulations, which can reduce usage by up to 80%, thereby lowering total application costs and cleaning downtime. In the Asia-Pacific region, near-term volume growth is supported by the expansion of automated lines in the ready-to-eat sector, which require heat-stable release chemistries capable of withstanding sterilization temperatures above 100 degrees Celsius without seal failure. Meanwhile, North America and Europe are advancing reformulation initiatives to meet clean-label requirements while maintaining technical performance standards. Liquid products continue to dominate the market; however, solid powders and wax systems are the fastest-growing formats. These alternatives offer processors improved dosing control and reduced overspray, aligning well with the needs of high-throughput robotics. The competitive landscape remains moderately fragmented, with global oils and fats companies increasing vertical integration. In contrast, smaller specialized firms are gaining market share by combining precision spray hardware with high-purity formulations.

Key Report Takeaways

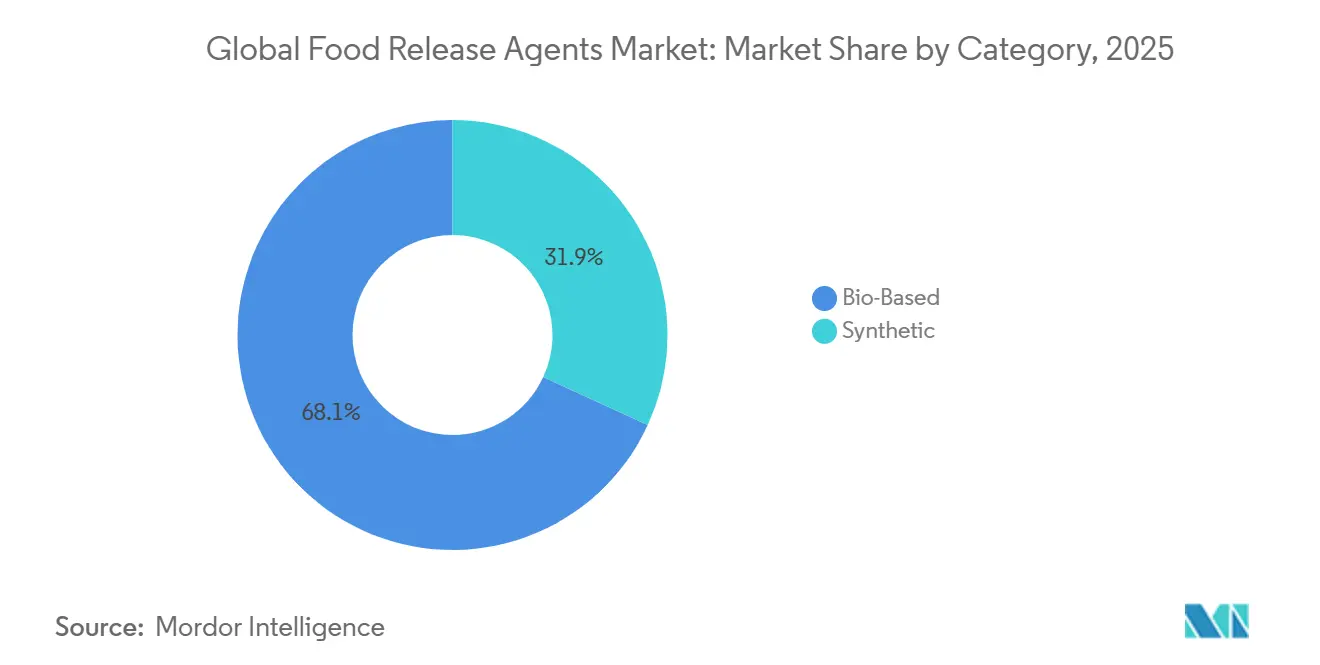

- By category, bio-based agents captured 68.12% of the food release agent market share in 2025, while synthetic alternatives are expanding at only 2.9% CAGR to 2031.

- By form, solid formulations are projected to grow at 4.01%—the highest segment CAGR—yet liquid formats retained 55.12% share of the food release agent market size in 2025.

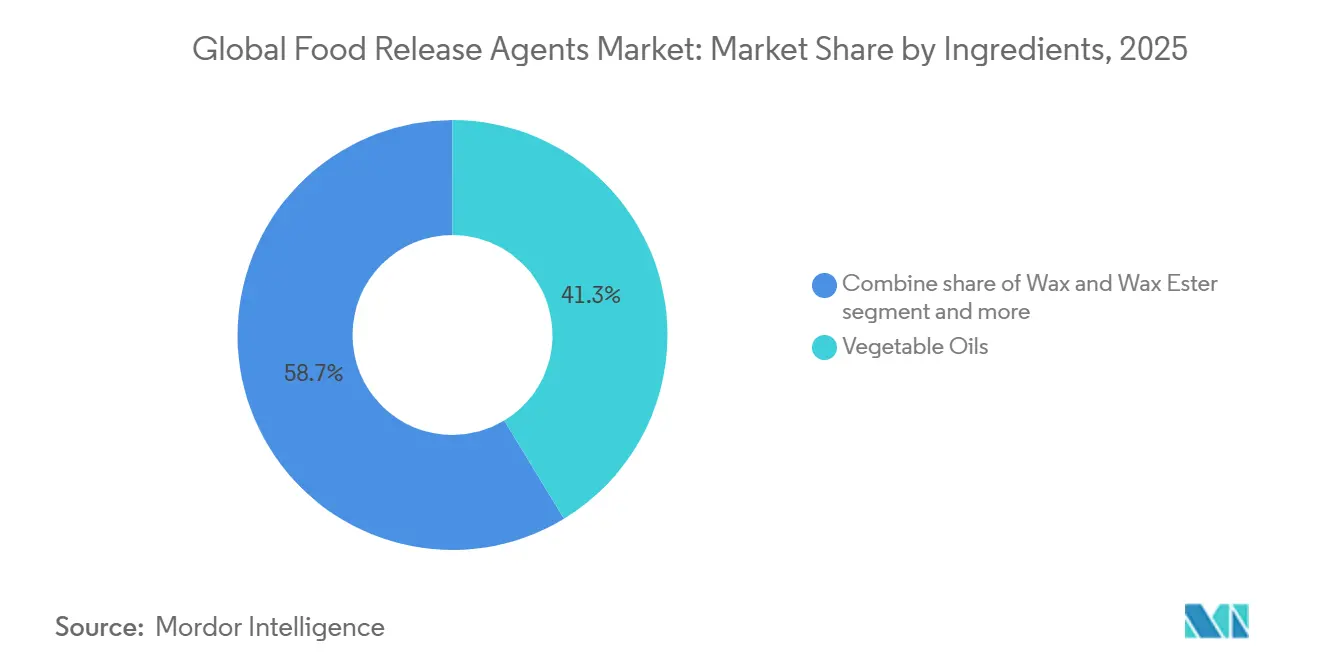

- By ingredients, vegetable oils held 41.32% of the 2025 ingredients split, but wax and wax-ester blends are on track for a 3.71% CAGR through 2031.

- By application, bakery remained the volume leader with 45.21% share in 2025, whereas confectionery is set to post the fastest growth at 3.74% CAGR through 2031.

- By geography, Asia-Pacific took 33.21% food release agent market share in 2025 and will outpace all other regions at a 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Release Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of bakery and confectionery sectors requiring anti-sticking solutions | +0.8% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing production of convenience and ready-to-eat foods | +0.7% | Asia-Pacific, North America, Middle East and Africa | Medium term (2-4 years) |

| Surge in processed meat manufacturing needing agents to prevent adhesion on equipment | +0.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements in formulations improving heat resistance and application efficiency | +0.6% | Global | Long term (≥ 4 years) |

| Innovations in spray, liquid, and powder forms for precise industrial application | +0.4% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Development of vegetable oil and emulsifier-based agents for better performance | +0.5% | Global, regulatory pull in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of bakery and confectionery sectors requiring anti-sticking solutions

The growth of industrial bakery and confectionery operations is driving changes in the demand for release agents, with a focus on automation, texture complexity, and throughput optimization rather than basic mold lubrication. The global confectionery processing equipment market has experienced notable growth, with mixing and blending equipment leading in installations, while coating, enrobing, and molding systems are seeing the fastest adoption rates. Automated production lines require release agents that enable precise dosing, resist polymerization at zoned heating and cooling interfaces, and deliver consistent performance across thousands of cycles without seasoning drift. In May 2025, Vantage Specialty Chemicals launched its OptiRelease suite, which reportedly offers up to four times higher release strength compared to canola oil alone. It also minimizes polymerized residue, thereby extending pan-glaze life and reducing the frequency of replacements. Texture-driven innovation adds another layer of complexity, as 71% of consumers indicate that texture significantly affects their enjoyment of confectionery products. Brands are increasingly incorporating contrasting textures, such as creamy and crisp elements, which require dependable demolding and barrier properties to prevent fat migration. This focus on sensory experience elevates release agents from simple processing aids to essential formulation components that influence product structure and shelf stability.

Growing production of convenience and ready-to-eat foods

Convenience food manufacturing is increasingly adopting heat-stable, non-migratory release-agent chemistries that are compatible with retort sterilization and multi-material packaging laminates. In Thailand, the ready-to-eat food industry operates 575 factories, processing 531,800 tonnes annually. Of this output, 52.9% is sold domestically, while 47.1% is exported. The industry predominantly uses crystallized polyethylene terephthalate (PET) trays and retort pouches, which can withstand sterilization temperatures exceeding 100 degrees Celsius and consumer reheating up to 220 degrees Celsius. Release agents used on forming tools, sealing surfaces, and conveyor systems must not migrate into food during these thermal processes or leave residues that could compromise the seal integrity or recyclability of packaging laminates. The European Union Regulation 2025/351 has introduced stricter purity criteria for substances used in food-contact plastics [1]Source: Official Journal of the European Union, “COMMISSION REGULATION (EU) 2025/351,” eur-lex.europa.eu. This regulation mandates high-purity documentation and migration testing with defined performance standards, effectively excluding agents containing uncharacterized non-intentionally added substances or those derived from waste streams without rigorous purity verification. In Thailand, small and medium enterprises (SMEs) account for 548 of the 575 ready-to-eat factories. These SMEs face significant cost and documentation challenges, which favor the use of standardized, well-characterized vegetable-oil and lecithin blends over custom synthetic formulations. This regulatory and operational alignment is driving the adoption of plant-based agents with established food-additive status, offering simplified compliance pathways.

Surge in processed meat manufacturing needing agents to prevent adhesion on equipment

Processed meat operations require release and anti-stick solutions that address protein adhesion, comply with hygiene protocols, and mitigate allergen cross-contact risks under United States Department of Agriculture (USDA) inspection standards. IFC Solutions offers concentrated EEZ-OUT formulations designed for use on netting, molds, screens, racks, and cutting equipment in USDA-inspected facilities, focusing on improving yield and ensuring blemish-free product appearance. In June 2025, Interflon introduced Food Lube 3H, a dual-certified National Sanitation Foundation (NSF) 3H and H1 synthetic ester lubricant and release agent. This product is per- and polyfluoroalkyl substances (PFAS)-free, mineral oil saturated hydrocarbons (MOSH)/mineral oil aromatic hydrocarbons (MOAH)-free, and allergen-free, targeting direct food-contact applications such as dough dividers, knives, cutting mechanisms, and meat-processing conveyors. The industry is also shifting toward lubrication-free bearing systems in meat-processing equipment to enhance hygiene standards. For instance, igus replaced needle roller bearings in meat-flattening rollers with polymer plain bearings, which eliminate grease contamination and withstand twice-daily high-pressure washing with aggressive chemicals. These advancements highlight a broader industry trend toward application-specific release agents that meet National Sanitation Foundation (NSF) certification, allergen-free labeling, and halal or kosher requirements, while maintaining effective anti-adhesion performance on protein-rich surfaces.

Technological advancements in formulations improving heat resistance and application efficiency

Heat-resistant formulations are improving the durability of release agents in extreme thermal environments, reducing the need for frequent reapplication and minimizing issues such as carbonization and equipment fouling. Polymethylsilsesquioxane thin films, synthesized through sol-gel spray coating, have demonstrated non-stick performance at temperatures up to 400 degrees Celsius, with water contact angles of 97.4% and burnt-on food residue reduced to 2.7% compared to uncoated surfaces. These films maintained their performance for 3 hours at 400 degrees Celsius before decomposing at 500 degrees Celsius [2]Source: Royal Society of Chemistry, “Non-stick performance of polymethylsilsesquioxane thin films synthesized by sol–gel spray coating,” pubs.rsc.org. DuPont's MOLYKOTE 316 silicone release spray forms heat-stable films resistant to oxidation at temperatures up to 199 degrees Celsius. It complies with Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) 175.300 requirements for resinous and polymeric coatings, without the intentional inclusion of polytetrafluoroethylene (PTFE) or per- and polyfluoroalkyl substances (PFAS). This spray is applied to heat-seal bars to reduce buildup, improve heat transmission, and decrease cleaning time. DÜBÖR's Trennaktiv PR 100 Z, a 100% plant-based high-viscosity agent, is oxidation-proof and heatable, leaving no residues even at very high temperatures. It is particularly effective for the initial treatment of new or washed molds, especially for products that are difficult to release, such as Florentine and bee-sting cakes. These advanced chemistries reduce the frequency of reapplication, lower energy costs by improving heat transfer, and extend equipment lifespan by preventing carbonized buildup, which can accelerate corrosion and increase fire risk.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety regulations requiring extensive compliance testing | -0.4% | Europe, North America, Asia-Pacific (export-oriented) | Short term (≤ 2 years) |

| High development costs for natural and organic alternatives | -0.3% | Global, acute in Europe and North America | Medium term (2-4 years) |

| Environmental scrutiny on non-biodegradable synthetic chemicals | -0.2% | Europe, North America | Long term (≥ 4 years) |

| Formulation complexities for heat-stable agents in diverse applications | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety regulations requiring extensive compliance testing

Regulatory tightening in food-contact materials is increasing compliance costs and extending time-to-market for new release-agent chemistries. European Union Regulation 2024/3190 prohibits the intentional use of bisphenol A (BPA) and harmonized-classified bisphenols in plastics, varnishes, coatings, printing inks, silicones, adhesives, ion-exchange resins, and rubber intended for food contact [3]Source: European Union, “Regulation 2024/3190,” eur-lex.europa.eu. The regulation includes phased transitions, ending in July 2026 for most single-use items and January 2029 for certain repeat-use articles. This compels manufacturers to validate substitute chemistries through migration testing and supplier declarations of conformity. The European Food Safety Authority (EFSA) updated its food-additives guidance in January 2026, introducing a tiered toxicological approach. This approach prioritizes New Approach Methodologies (NAMs) and the Three Rs (Replacement, Reduction, and Refinement) principles, requiring the assessment of nanoparticle fractions, vulnerable populations (including infants under 16 weeks), and the environmental fate of xenobiotics. Additionally, environmental safety has been formally integrated into dossier requirements. Regulation 2026/245 amended Annex I of Regulation 10/2011, adding six new substances with specific migration limits and maximum-content restrictions. Manufacturers must now demonstrate compliance through formulation records rather than finished-product testing alone, shifting the burden to accurate raw-material data from suppliers. Small and medium enterprises (SMEs), which dominate ready-to-eat manufacturing in markets such as Thailand, face disproportionate documentation and testing burdens. This situation favors established agents with grandfathered approvals over innovative formulations that require full dossiers for compliance. For example, SMEs often lack the resources to conduct extensive testing, which can increase compliance costs by approximately 30% compared to larger manufacturers.

High development costs for natural and organic alternatives

Developing bio-based release agents that achieve performance parity with synthetic alternatives in terms of heat resistance, migration limits, and shelf stability requires substantial research and development investments, as well as extended validation cycles. For example, Kerry Group allocated EUR 314 million to research and development in 2025. This included establishing a new biotechnology center in Leipzig, expanding enzyme production capacity in Cork, and enhancing cocoa taste capabilities in Grasse. These initiatives support fermentation-derived and enzyme-based ingredient platforms that can be adapted for release and anti-stick applications. Similarly, Archer Daniels Midland (ADM) committed USD 26 million in January 2026 to expand its Erlanger, Kentucky facility by 3,600 square feet. This expansion increased raw-material handling capacity by 40 percent and incorporated digitalization and automation to support naturally derived color and flavor solutions. This investment followed a prior USD 15 million commitment in 2025. These capital investments highlight the challenges of replacing petroleum-derived chemistries with alternatives such as plant extracts, fermentation products, or enzymatically modified starches. These alternatives must meet identical migration limits, thermal stability, and application performance standards while adhering to clean-label claims and allergen-free certifications. Smaller formulators often lack the scale to manage multi-year development timelines and regulatory submission costs, which concentrates innovation among vertically integrated ingredient conglomerates and limits competitive entry into the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Bio-Based Agents Reshape Processing Economics

Bio-based agents accounted for 68.12% of the market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 3.72% through 2031. This growth is driven by manufacturers prioritizing regulatory compliance, cost efficiency, and clean-label positioning, leading to a preference for bio-based solutions over synthetic alternatives. In 2025, ACI Group's adoption of DÜBÖR Release Oils demonstrated up to an 80% reduction in product usage compared to traditional agents. This adoption also eliminated or reduced the need for baking paper, decreased cleaning frequency and energy consumption, and offered vegan, allergen-free options. The inclusion of plant-based wax supported sustainable sourcing while reducing transport and waste footprints. In July 2024, AAK received Generally Recognized as Safe (GRAS) approval from the United States Food and Drug Administration (FDA) for shea stearin. This marked the first expansion of approved uses since 1998, positioning shea stearin as a plant-based solid fat alternative with lower saturated fat content compared to coconut oil. Its applications include bakery products, confectionery fillings, nut and seed spreads, margarine, and plant-based meat and dairy alternatives.

While synthetic agents are experiencing a decline in market share, they continue to serve niche applications. These include extreme-temperature environments and scenarios where silicone-based chemistries provide superior non-stick performance. For instance, DuPont's MOLYKOTE 316 silicone spray remains specified for heat-seal bars and high-temperature food-processing equipment, despite the absence of intentional polytetrafluoroethylene (PTFE) or per- and polyfluoroalkyl substances (PFAS) in its formulation.

By Form: Automation Drives Solid and Powder Uptake

Liquid formulations accounted for 55.12% of the market share in 2025. However, solid formulations are expected to exhibit the fastest growth, with a projected Compound Annual Growth Rate (CAGR) of 4.01% through 2031. This growth is driven by manufacturers increasingly adopting spray-dried powders and wax-based systems for automated high-throughput production lines. Vantage's OptiRelease suite, launched in May 2025, offers up to four times higher release strength compared to canola oil alone, reduces polymerized residue to extend pan-glaze life, and is immediately applicable for bread and cake production. Specialized solutions for pizza and other applications are also planned, positioning the liquid formulation as part of an integrated spray-equipment platform.

Solid and powder formats address challenges such as overspray control, dosing precision, and compatibility with dry-mixing processes. Additionally, slip and antiblock masterbatches, based on modified silicone polymers and amides, reduce the coefficient of friction in flexible-film packaging, prevent film-to-film adhesion during storage and unwinding, and provide Per- and Polyfluoroalkyl Substances (PFAS)-free alternatives. These alternatives maintain transparency and resist exudation even at high processing temperatures.

By Ingredients: Wax Esters Gain as Lecithins Consolidate

In 2025, vegetable oils accounted for 41.32% of the ingredients segment, while wax and wax ester blends are projected to grow at a compound annual growth rate (CAGR) of 3.71% through 2031. This growth is supported by regulatory approvals and their functional benefits, such as heat resistance and barrier properties. Emulsifiers, primarily lecithins, make up the remaining share and are increasingly consolidating around vertically integrated suppliers. This trend follows Bunge's acquisition of International Flavors and Fragrances' lecithin business in March 2026, which added liquid, powdered, and fractionated lecithins derived from soy, sunflower, and rapeseed. These products generated approximately USD 240 million in revenue in 2024.

LorAnn's Professional Release Agent combines medium-chain triglyceride oils and lecithin, offering solutions for confectionery mold release, starchless gummy production, and caramels. The product is marketed as kosher, genetically modified organism (GMO)-free, and vegan, with application guidance emphasizing light coating to prevent residue buildup. Wax-based systems are gaining market share due to their superior heat stability and compatibility with plant-based food matrices. For instance, carnauba oleogels used in plant-based meat analogues reduced cooking loss to 12.03%, approximately 35% lower than coconut oil controls. These oleogels also maintained viscosity and structure during cooking, attributed to their higher melting points and greater temperature sensitivity of viscosity.

By Application: Confectionery Texture Innovation Outpaces Bakery Volume

Bakery applications accounted for 45.21% of demand in 2025, driven by high-volume bread and cake production. However, the confectionery segment is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.74% through 2031, supported by texture-driven innovation and the expansion of gummy formats, which are elevating release-agent specifications. Notably, 71% of consumers identify texture as a key factor in product enjoyment, while 67% seek novelty in mouthfeel. This has prompted confectioners to incorporate contrasting textures, such as creamy and crisp, soft and snappy, or mousse-filled bars, which require reliable demolding and barrier properties to prevent fat migration between components. Mantrose Group introduced MantroShield, a fat-free encapsulated acid solution for gummy coatings. This product enhances tangy flavor intensity, reduces acid usage rates, improves stability, and extends shelf life, all while supporting cleaner labeling by eliminating added fats. Similarly, LorAnn's Professional Release Agent is marketed specifically for starchless gummy production, as well as for hard and soft caramels and other confections with sticky surfaces. The product emphasizes light application to prevent residue on both the confectionery pieces and equipment.

Meat and meat products represent a smaller but strategically significant application segment. In this category, hygiene, allergen-free certification, and National Sanitation Foundation (NSF) registration are critical factors driving premium pricing. Interflon's Food Lube 3H, launched in June 2025, holds dual NSF 3H and H1 certifications for direct and incidental food contact. It is Per- and Polyfluoroalkyl Substances (PFAS)-free, Mineral Oil Saturated Hydrocarbons (MOSH)/Mineral Oil Aromatic Hydrocarbons (MOAH)-free, and allergen-free, targeting applications such as dough dividers, knives, cutting mechanisms, baking surfaces, and meat and poultry processing. The product claims reliable performance at elevated temperatures without leaving hard residue buildup.

Geography Analysis

Asia-Pacific held 33.21% of the market share in 2025, emerging as the leading segment. This dominance is attributed to the rapid growth of ready-to-eat food manufacturing, advancements in confectionery processing infrastructure, and increasing consumer demand for convenience-oriented products. Thailand, for instance, operates 575 ready-to-eat factories, processing 531,800 tonnes annually. Among these, 548 are small and medium enterprises that require cost-effective, heat-stable release solutions compatible with crystallized polyethylene terephthalate (PET) packaging. These solutions must withstand temperatures ranging from -40°C to 220°C and endure retort sterilization cycles exceeding 100°C. Companies like Kerry Group have strengthened their regional presence by opening manufacturing facilities in Karawang, Indonesia, and innovation centers in South Jakarta and Dubai, enhancing production and application-testing capacities for bakery, confectionery, meat, and meal applications.

The fastest-growing segment is supported by investments and joint ventures aimed at improving access to sustainable raw materials and expanding production capabilities. AAK, in collaboration with Kuala Lumpur Kepong, is building a specialty palm-fraction plant in Pasir Gudang, Johor, Malaysia, with a total investment of SEK 300 million (approximately USD 31.4 million). This facility, expected to reach full capacity by 2029, will enhance access to high-purity raw materials used in cocoa butter alternatives and specialty fats, which serve as precursors for release agents. Additionally, Cargill's divestment of its starch and sweeteners business in Davangere, Karnataka, to Riddhi Siddhi Gluco Biols in January 2026 reflects portfolio rationalization in India's starch industry. This sector intersects with emulsifier and release-agent supply chains through products like maltodextrin, liquid glucose, and corn-derived co-products.

Other regions, including North America and Europe, account for the remaining global demand, driven by reformulation mandates and stricter regulations. In the United States, over 80% of consumers favor product reformulation toward healthier options, with 70% preferring recognizable ingredients and 58% seeking shorter ingredient lists. This trend is pressuring manufacturers to replace synthetic processing aids with plant-based alternatives. Archer Daniels Midland invested USD 26 million in January 2026 to expand its Erlanger, Kentucky facility by 3,600 square feet, increasing raw material handling capacity by 40% and incorporating digitalization and automation to support naturally derived color and flavor solutions. This builds on a prior USD 15 million investment made in 2025. In Europe, regulatory changes such as European Union regulations 2024/3190, 2025/351, and 2026/245 have banned bisphenol A, tightened purity criteria for food-contact plastics, and authorized new substances like rice bran wax. These compliance requirements favor established bio-based agents with grandfathered approvals and well-characterized migration profiles.

Competitive Landscape

The market demonstrates moderate fragmentation, characterized by a combination of global ingredient conglomerates pursuing vertical integration and specialized formulators focusing on niche applications or regional markets. In March 2026, Bunge acquired International Flavors and Fragrances' soy protein concentrate, lecithin, and crush businesses, which generated approximately USD 240 million in revenue in 2024. This acquisition expanded Bunge's emulsifier portfolio to include liquid, powdered, and fractionated formats derived from soy, sunflower, and rapeseed, enabling the company to provide integrated ingredient solutions that combine release functionality with protein fortification and texture optimization.

AAK enhanced its upstream integration through a joint venture with Kuala Lumpur Kepong to establish a specialty palm-fraction plant in Malaysia. This project involves an investment of Swedish Krona (SEK) 300 million (approximately USD 31.4 million) and is expected to reach full capacity by 2029. The plant aims to secure sustainable, high-purity raw materials for cocoa butter alternatives and specialty fats, which serve as precursors for release agents. These developments indicate a trend toward consolidation among suppliers capable of delivering tailored emulsifier and fat-fraction blends that meet evolving standards for purity, migration, and clean-label requirements, thereby raising entry barriers for formulators without oilseed origination and crushing networks.

Opportunities remain in enzyme and fermentation-derived release technologies that align with reformulation mandates. For instance, Kerry invested EUR 314 million in research and development in 2025, which included establishing a biotechnology center in Leipzig and expanding enzyme production capacity in Cork. These initiatives support platforms adaptable to anti-stick and controlled-release applications. Meanwhile, smaller formulators are differentiating themselves through application-specific innovations and integrated spray-equipment solutions. Vantage Specialty Chemicals introduced OptiRelease in May 2025, claiming up to 400% higher release strength compared to canola oil alone. The product is positioned as part of a comprehensive release solution, including customized spray equipment designed to minimize overspray, reduce yield loss, and decrease line downtime.

Food Release Agents Industry Leaders

Archer-Daniels-Midland Co.

Bunge Limited

Cargill Incorporated

AAK AB

Vantage Specialty Chemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ADM invested $26 million to expand and upgrade its Erlanger, Kentucky flavors facility, adding 3,600 square feet, boosting raw material handling capacity by 40%, and enhancing digitalization to meet rising food and beverage reformulation demand.

- August 2025: Vantage Food introduced the MALLET CPG 1100 spray system, incorporating POSISPRAY smart technology to accurately apply release agents in industrial bakeries. This system minimizes overspray, waste, depanning failures, and downtime by offering real-time spray verification and modular features.

- May 2025: Vantage Food launched the OptiRelease suite of next‑generation release agents for commercial cake, bread and pizza baking, delivering up to four times higher release strength, reduced residue, longer pan life and improved operational efficiency.

Global Food Release Agents Market Report Scope

Food release agents facilitate the separation of food from cooking containers after baking or roasting. The market is segmented by category, application, and geography. By category, it is divided into synthetic and bio-based products, while by form, it includes solid and liquid formats. Based on ingredients, the market encompasses vegetable oils, emulsifiers, and wax and wax ester types. In terms of application, it covers bakery, confectionery, meat and meat products, beverages, and other food categories. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in tonnes for all the abovementioned segments.

| Synthetic |

| Bio-Based |

| Solid |

| Liquid |

| Vegetable Oils |

| Emulsifiers |

| Wax and Wax Easter |

| Bakery |

| Confectionary |

| Meat and Meat Products |

| Beverage |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Synthetic | |

| Bio-Based | ||

| By Form | Solid | |

| Liquid | ||

| By Ingredients | Vegetable Oils | |

| Emulsifiers | ||

| Wax and Wax Easter | ||

| By Application | Bakery | |

| Confectionary | ||

| Meat and Meat Products | ||

| Beverage | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will bio-based formulations grow in the food release agent market to 2031?

They are projected to expand at a 3.72% CAGR, substantially outpacing synthetic counterparts.

Which form factor is gaining momentum in high-throughput automated lines?

Solid powders and wax systems, forecast to post a 4.01% CAGR thanks to tighter dosing control and reduced overspray.

Why is Asia-Pacific the fastest growing region?

A dense network of ready-to-eat manufacturers and new confectionery plants demands heat-stable, non-migratory agents, driving a 3.92% regional CAGR.

What regulatory change most affects agent formulation in Europe?

EU Regulation 2024/3190 banning bisphenol A and related substances is prompting a pivot toward documented, plant-based chemistries.

How are suppliers addressing stricter hygiene rules in meat processing?

By launching dual NSF 3H/H1 certified, PFAS-free ester lubricants that prevent protein adhesion while meeting halal and allergen-free labels.

Page last updated on: