Thailand Folding Cartons And Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

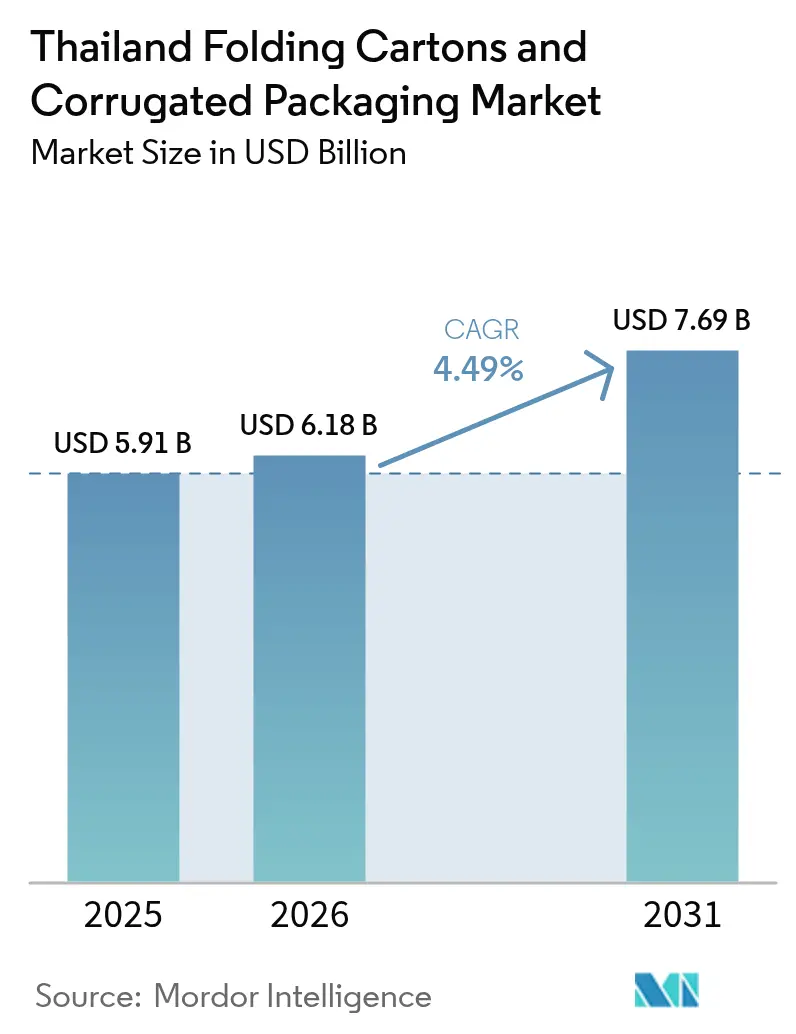

| Base Year Market Size (2025) | USD 5.91 Billion |

| Market Size (2026) | USD 6.18 Billion |

| Market Size (2031) | USD 7.69 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Folding Cartons And Corrugated Packaging Market Analysis by Mordor Intelligence

The Thailand folding cartons and corrugated packaging market size was valued at USD 5.91 billion in 2025 and estimated to grow from USD 6.18 billion in 2026 to reach USD 7.69 billion by 2031, at a CAGR of 4.49% during the forecast period (2026-2031). Rising e-commerce volumes, relocations of electronics and automotive production from China, and government incentives that reward circular packaging underpin growth while volatile recycled paper prices temper near-term margins. Corrugated boxes retain volume leadership, yet folding cartons gain momentum as premium food, personal care, and pharmaceutical brands demand shelf impact, regulatory compliance, and greener substrates. Converters differentiate through digital printing, moisture-resistant coatings, and bamboo-fiber blends that align with Thailand’s Bio-Circular-Green (BCG) agenda. Medium-sized producers increasingly automate short runs, shrinking time-to-market and enabling right-sized packaging that lowers logistics costs. Vertical integration into recovered fiber and chemical additives shields integrated players from raw-material volatility and import-tariff swings.

Key Report Takeaways

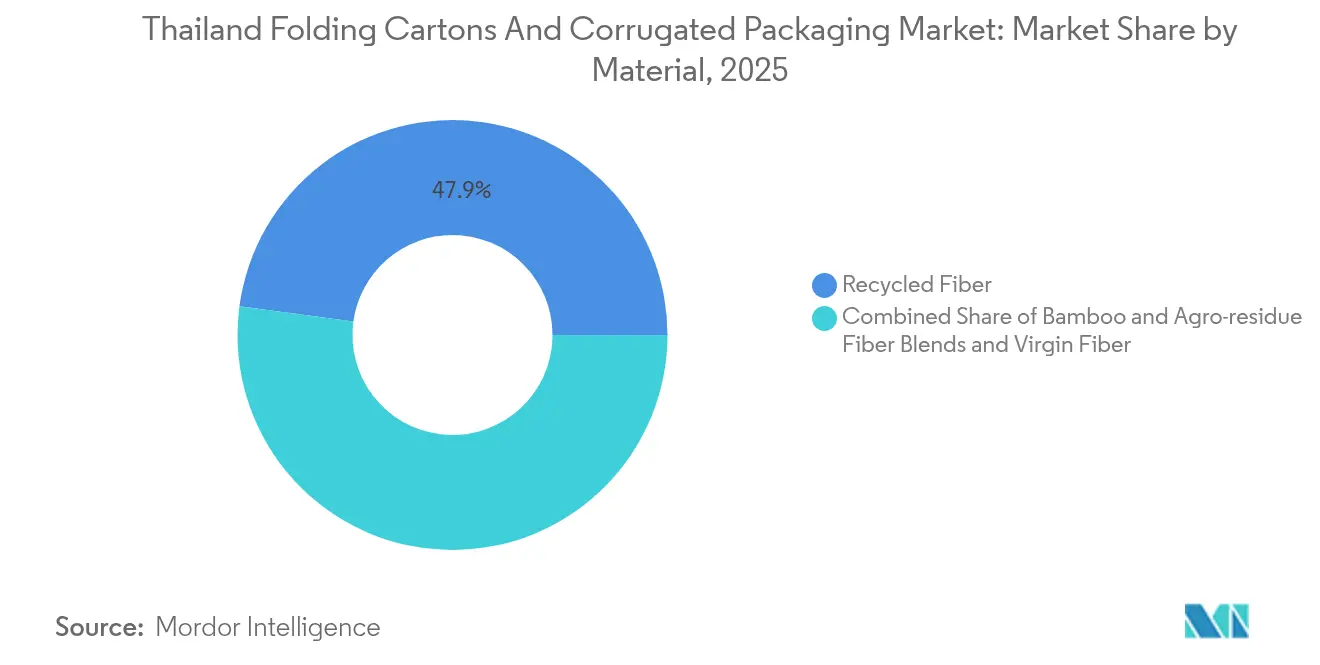

- By material, recycled fiber led with 47.86% of the Thailand folding cartons and corrugated packaging market share in 2025; Bamboo and agro-residue fiber blends are projected to expand at a 6.01% CAGR through 2031.

- By packaging type, corrugated boxes contributed 54.47% of the Thailand folding cartons and corrugated packaging market size in 2025, whereas folding cartons are set to grow at 5.07% CAGR to 2031.

- By board type, triple wall configurations are forecast to post the fastest rise at 5.63% CAGR between 2026-2031.

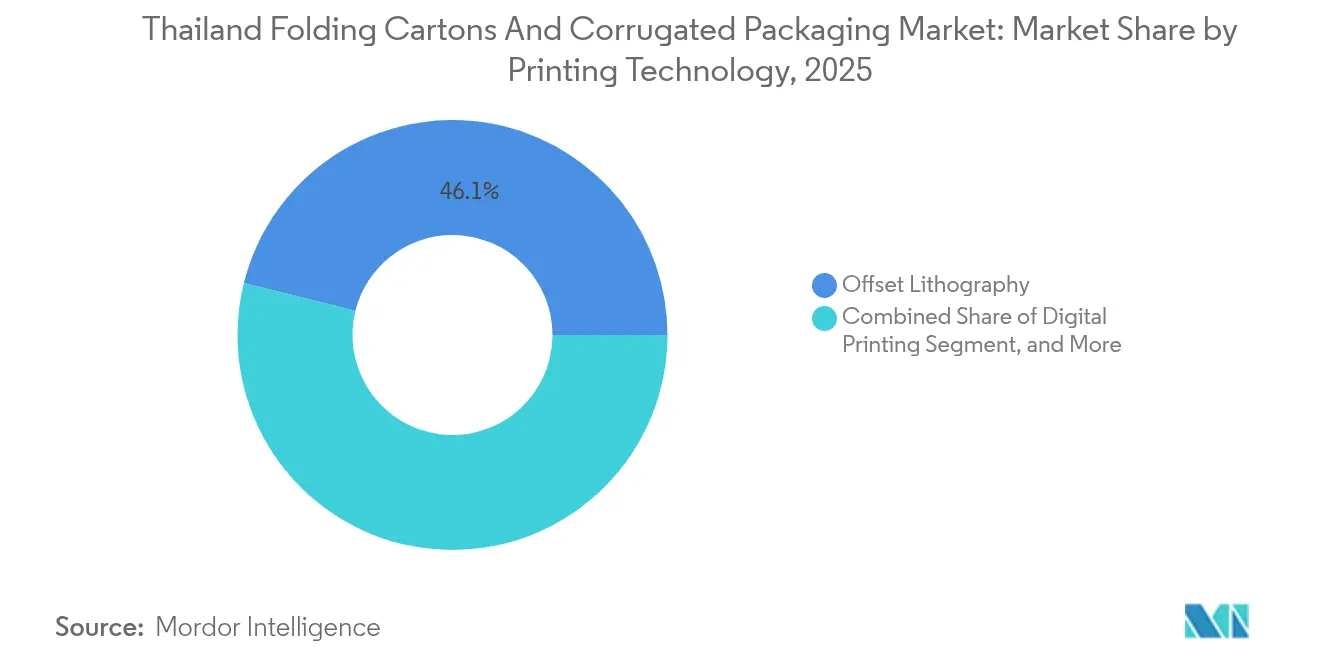

- By printing technology, digital presses will accelerate at 6.54% CAGR through 2031.

- By end-user, personal care and cosmetics packaging is estimated to climb at 6.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Folding Cartons And Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment surge | +1.2% | Bangkok and Eastern Economic Corridor | Short term (≤ 2 years) |

| OEM relocation to Thailand | +0.8% | Chonburi and Rayong | Medium term (2-4 years) |

| Government incentives for sustainable packaging | +0.6% | Nationwide (BOI zones) | Long term (≥ 4 years) |

| SME shift to short-run digital printing | +0.4% | Bangkok clusters | Medium term (2-4 years) |

| Refrigerated grocery delivery growth | +0.3% | Urban cold-chain routes | Short term (≤ 2 years) |

| Bamboo-fiber adoption to meet ESG criteria | +0.3% | Agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce fulfillment surge

Online retail accelerates demand for right-sized corrugated mailers that withstand high parcel-handling cycles, prompting logistics operators to invest in automated box-forming lines capable of customizing dimensions on the fly.[3]Nim Express, “Cold-chain Services,” nimexpress.com Cold-chain parcels for fresh groceries add a moisture-resistant layer requirement, which lifts uptake of poly-coated liners and triple-wall board. Brand owners favor paper over plastic for its curbside recyclability, pushing converters to certify supplies under Forest Stewardship Council (FSC) schemes. Rapid urbanization concentrates fulfillment centers around Bangkok and EEC provinces, tightening delivery windows and reinforcing value propositions around just-in-time packaging services. These dynamics sustain volume growth and catalyze innovation in recyclable barrier coatings.

OEM relocation to Thailand

Electronics, automotive, and appliance producers adopting “China-plus-one” strategies shift production to Rayong and Chonburi industrial estates, boosting demand for anti-static corrugated inserts, returnable interior cushions, and export-grade pallets. Foreign direct investment flows create captive volumes for local converters while incentivizing world-class quality systems such as ISO 9001 and ISTA testing. Government fast-tracks customs procedures in EEC zones, shortening lead times and compelling packaging suppliers to align inventory management with just-in-sequence assembly. Although many OEMs still import kraft liner from China, volatile freight rates motivate supply-chain localization and favor vertically integrated Thai paper producers with stable domestic collection networks.

Government incentives for sustainable packaging

The Second National Action Plan on Plastic Waste mandates 100% recyclable plastic waste management by 2027, steering food and beverage brands toward paper-based substitutes and awarding up to eight-year tax holidays for qualifying BCG investments. BOI promotion measures lower machinery import duties, spurring acquisition of energy-efficient corrugators and digital presses. Banks link loan pricing to environmental performance indicators, so converters that certify bamboo or agro-residue fiber capacity enjoy preferential financing. Public-private pilot projects on community waste-paper collection broaden feedstock pools and stabilize OCC supplies, enhancing sector resilience.

Thai SMEs’ shift to short-run digital printing

Membership in the Thai Innovative Printing Trade Association expands as converters adopt inkjet and electrophotographic presses that remove plate-making costs, enabling minimum order quantities of one and facilitating SKU proliferation for online brands. Variable-data capability supports QR-code-enabled traceability, tamper evidence, and targeted promotions. AI-driven workflow software reduces pre-press labor, elevating competitiveness of mid-tier firms and eroding entry barriers typically defined by offset press scale. Equipment suppliers host training hubs in Bangkok to upskill operators, accelerating diffusion of color management standards that meet multinational brand specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled paper supply volatility | -0.7% | Port-dependent mills | Short term (≤ 2 years) |

| Kraft-liner import tariff swings | -0.5% | Import-heavy converters | Medium term (2-4 years) |

| Land-use protests slowing corrugator installations | -0.3% | Conservation zones | Long term (≥ 4 years) |

| Reusable plastic crates in produce logistics | -0.2% | Agricultural supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled paper supply volatility

Old corrugated containers (OCC) prices fluctuate with shipping constraints and demand spikes from other Asian mills, pressuring margins for independent converters that rely on spot purchases. Integrated players hedge risk through overseas recycling acquisitions and domestic buy-back programs that lock in bale quality. Government anti-dumping duties on polymer substrates further elevate substrate switching costs, sustaining demand for local recycled fiber despite price swings. Inventory buffering and long-term contracts become essential risk-mitigation levers over the next two years.

Kraft-liner import tariff swings

Periodic adjustments to ASEAN and bilateral tariff schedules complicate landed-cost budgeting for converters importing virgin linerboard. Tariff hikes incentivize qualification of domestically produced high-tensile liners, spurring capital upgrades in Thai mills. However, transition timelines and performance testing prolong switchover, exposing converters to near-term cost spikes. Larger firms diversify sourcing across multiple ports and suppliers, whereas SMEs may pass costs to customers or narrow margin bands, slowing capex plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Dominance with Bamboo Upswing

Recycled fiber held 47.86% of Thailand folding cartons and corrugated packaging market share in 2025, underpinned by well-established OCC collection networks and cost competitiveness. Thailand folding cartons and corrugated packaging market participants leverage dual-loop recovery models that combine post-consumer pick-ups and industrial scrap, boosting bale yields and reducing landfill pressure. Bamboo and agro-residue blends, though nascent, scale at 6.01% CAGR as BOI incentives and ESG-linked financing reduce payback periods for biomass digesters and pulping lines.

Quality-sensitive applications such as pharma inserts and ready-to-eat meal trays retain virgin fiber specifications, but converters substitute recycled furnish in secondary layers to trim costs. Thai universities partner with mills to optimize enzyme treatments that raise recycled fiber tensile strength, narrowing performance gaps. As brand owners publish Scope 3 emissions targets, low-carbon bamboo boards secure pilot orders from electronics exporters. Thailand folding cartons and corrugated packaging market size gains incremental volume from agro-waste valorization, reinforcing rural economic linkages and mitigating raw-material import exposure.

By Packaging Type: Folding Cartons Ascend Premium Ladder

Corrugated shippers constituted 54.47% of Thailand folding cartons and corrugated packaging market size in 2025, reflecting robust export and e-commerce flows. Yet folding cartons register a 5.07% CAGR through 2031 by delivering print fidelity, tactile finishes, and tamper-evident structures valued by cosmetics and nutraceuticals. Digital spot-varnish effects and metallic foils elevate shelf visibility without compromising recyclability, allowing upscale brands to localize limited-edition runs.

Brand-owner consolidation in food supplements and herbal remedies drives joint development agreements with converters, integrating supply-chain forecasting and just-in-time delivery. Temperature-stable cartonboard grades with integrated oxygen barriers support ambient shelf-stable desserts, expanding total available market. Thailand folding cartons and corrugated packaging market continues to bifurcate into high-volume commodity corrugate and high-margin specialty cartons, rewarding players able to straddle both ends through multi-plant networks and hybrid print workflows.

By Board Type: Triple Wall Meets Cold-Chain Rigor

Single-wall boards command 38.05% of shipments thanks to low cost and adequate strength for domestic e-commerce. Triple-wall demand, though smaller in tonnage, is forecast to compound at 5.63% CAGR as grocery home-delivery platforms and vaccine logistics require compression resilience under humid chilled conditions. Double-wall remains mainstream for flat-panel TVs and motorcycle parts, balancing stacking strength and weight limits imposed by parcel carriers.

Investments in fluting profile optimization, starch-based waterproof sizing, and in-line slotter-scorer automation boost throughput while meeting quality audits by multinational 3PLs. Thailand folding cartons and corrugated packaging market size benefits from infrastructure stimulus that expands refrigerated warehouse footprints, pulling through higher-grade board consumption. Converters that certify ISTA-7E protocols gain preferred-supplier status with regional cold-chain operators.

By Printing Technology: Digital Gains Ground

Offset lithography still represents 46.12% of annual impressions, but digital presses accelerate at 6.54% CAGR as converters migrate toward variable-data campaigns and lower inventory holding costs. AI-assisted color management slashes makeready waste, aligning with circularity KPIs. Hybrid lines that marry flexo priming with inkjet heads enter commercial operation, bridging cost and speed gaps between legacy and fully digital workflows.

Thailand folding cartons and corrugated packaging industry leaders pilot plant-wide MES systems that integrate web-inspection data with ERP forecasting, reducing stockouts and enabling next-day turnaround for micro-brands. Equipment OEMs establish regional demo centers, shortening sales cycles and fostering skills transfer. This technology diffusion democratizes access, intensifying competition and accelerating design-to-market cycles across the value chain.

By End-User Industry: Cosmetics Propel Value Growth

Food and beverage retained 32.10% revenue share in 2025 on the back of processed seafood, rice, and canned fruit exports. Personal care and cosmetics packaging rises at a 6.42% CAGR through 2031, propelled by premium skin-care, herbal beauty, and K-beauty cross-border e-commerce that demand high-definition flexo and lens-film embellishments. Pharmaceutical cold-chain innovations, including tamper-evident, moisture-barrier cartons, add incremental tonnage and spur adoption of serialization codes.

Electronics brands expanding production in the EEC specify anti-static, moisture-indicator corrugate to protect circuit boards. Meanwhile, nutraceutical co-packers deploy oxygen-scavenging folding cartons that prolong gummy shelf life and reduce preservatives. Thailand folding cartons and corrugated packaging market attracts cross-sector collaboration, with converters offering turnkey design, prototyping, and drop-shipping services that integrate seamlessly into brand owners’ omnichannel fulfillment models.

Geography Analysis

Eastern Economic Corridor provinces Chonburi, Rayong, and Chachoengsao .anchor investment in new corrugators and high-grade folding carton lines as industrial land sales hit 6,174 rai in fiscal 2024, a record under the Industrial Estate Authority of Thailand Land prices averaging THB 6.7 million per rai underscore sustained foreign investor interest, especially from EV and electronics clusters that require export-compliant packaging. Bangkok metropolitan area remains the logistics and commercial nexus, housing flagship plants of SCG Packaging and a dense ecosystem of SME converters positioned near Suvarnabhumi Airport and Laem Chabang Port for rapid regional distribution.

Northern and northeastern provinces such as Prachin Buri attract agro-industrial projects that feed bamboo and rice-straw fiber mills, diversifying geographic fiber supply. Government incentives extend BOI tax privileges to eco-industrial estates like the newly approved 1,891-rai ARAYA Eastern Gateway, catalyzing packaging demand across semiconductors, EV batteries, and pharmaceutical tenants. Cross-border trade via Mekong corridors pulls corrugated containers into Lao, Cambodian, and Vietnamese markets, leveraging Thailand’s superior road infrastructure.

Southern seaboard cold-chain corridors experience rising triple-wall board uptake due to seafood exports and refrigerated grocery deliveries. Provincial cold-storage hubs integrate smart sensors that transmit handling data, tightening converter specifications around water-absorption rates and crush resistance. Thailand folding cartons and corrugated packaging market benefits from this diversified geographic pull, balancing cyclical export exposure with resilient domestic consumption.

Competitive Landscape

The market exhibits moderate concentration: SCG Packaging’s vertically integrated model spans recovered fiber procurement, containerboard milling, and multi-substrate converting facilities.[1]SCG Packaging Public Company Limited, “SCG Packaging (SCGP),” scgpackaging.com Kemira’s upcoming 100,000-tonne chemical plant expansion at Wellgrow boosts local wet-end additive availability, reinforcing SCG’s supply security while offering smaller mills regional sourcing options.[2]Kemira, “Kemira invests in the expansion of paper and board chemical capacity,” kemira.com Valmet continues to install quality-control systems at Thai Containers Group, signaling sustained automation investment among incumbents.

Mid-tier converters carve niches via digital print agility, FSC certification, and specialty coatings suited to cold-chain, cosmetics, and pharmaceutical markets. Imported niche bamboo fiber boards from regional mills face competition from Thai Cane Paper’s scale-up of agro-residue furnish. Logistics integrator SCGJWD leverages upstream packaging ties to offer bundled warehousing and fulfillment solutions, blurring traditional value-chain boundaries. Competitive intensity is shifting from price-per-ton toward service bundles, sustainability metrics, and technology adoption curves.

Thailand Folding Cartons And Corrugated Packaging Industry Leaders

Siam Toppan Packaging Co. Ltd

Thai Containers Group (SCG Packaging)

Thung Hua Sinn Group

Continental Packaging (Thailand) Co. Ltd

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: A leading Thai converter unveiled a USD 334 million investment plan for a new Vietnam plant, reflecting ASEAN regionalization strategies

- April 2025: IEAT approved a 1,891-rai eco-industrial estate within the ARAYA Eastern Gateway project to attract semiconductor, EV, and pharmaceutical tenants

- March 2025: Kemira confirmed a multi-million-euro expansion at its Wellgrow site to add 100,000 tpa of paper and board chemicals by Aug 2026

- March 2025: Covestro finalized expansion of specialty polycarbonate film capacity at Map Ta Phut, adding high-performance substrates for premium folding cartons

Thailand Folding Cartons And Corrugated Packaging Market Report Scope

Folding cartons and corrugated packaging is one of the most used eco-friendly packaging solutions due to their ability to be produced in various sizes with a small footprint, thus, making them feasible for use in different end-user industries. The growth of Thailand's packaging industry is driven by the country's expanding population and high demand for low-cost, flexible packaging. Folding cartons and corrugated packaging are primarily used in various end-user industries, including food and beverage, healthcare and pharmaceutical, and household and personal care.

A complete background analysis of the market, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The report also features a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain.

The Thailand Folding Cartons and Corrugated Packaging Market is segmented by end-user (food and beverage, healthcare and pharmaceutical, household and personal care, and other end-user industries (manufacturing, automotive, and others)).

The market sizes and forecasts are in terms of value in USD million for all the above segments.

| Virgin Fiber |

| Recycled Fiber |

| Bamboo and Agro-residue Fiber Blends |

| Folding Cartons |

| Corrugated Boxes |

| Single Wall |

| Double Wall |

| Triple Wall |

| Folding Boxboard (FBB) |

| Other Board Types |

| Offset Lithography |

| Flexography |

| Digital Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare and Pharmaceutical |

| Personal Care and Cosmetics |

| Electronics and Appliances |

| Other End-user Industries |

| By Material | Virgin Fiber |

| Recycled Fiber | |

| Bamboo and Agro-residue Fiber Blends | |

| By Packaging Type | Folding Cartons |

| Corrugated Boxes | |

| By Board Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| Folding Boxboard (FBB) | |

| Other Board Types | |

| By Printing Technology | Offset Lithography |

| Flexography | |

| Digital Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Electronics and Appliances | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is Thailand’s folding cartons and corrugated packaging market in 2026?

The Thailand folding cartons and corrugated packaging market size is USD 6.18 billion in 2026.

What is the expected CAGR to 2031?

Market value is projected to grow at a 4.49% CAGR during the forecast period (2026-2031).

Which material segment is growing fastest?

Bamboo and agro-residue fiber blends are forecast to expand at 6.01% CAGR as brands pursue ESG goals.

Why are triple-wall boards gaining demand?

Cold-chain grocery delivery and heavy industrial exports require the compression strength and moisture resistance that triple-wall configurations offer.

How is digital printing reshaping packaging?

Digital presses enable Thai converters to eliminate minimum order quantities, offer variable-data customization, and shorten lead times, driving a 6.54% CAGR in this technology segment.

Which end-use sector will outpace others?

Personal care and cosmetics packaging is estimated to advance at 6.42% CAGR, propelled by premiumization and sustainability mandates.

Page last updated on: