Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

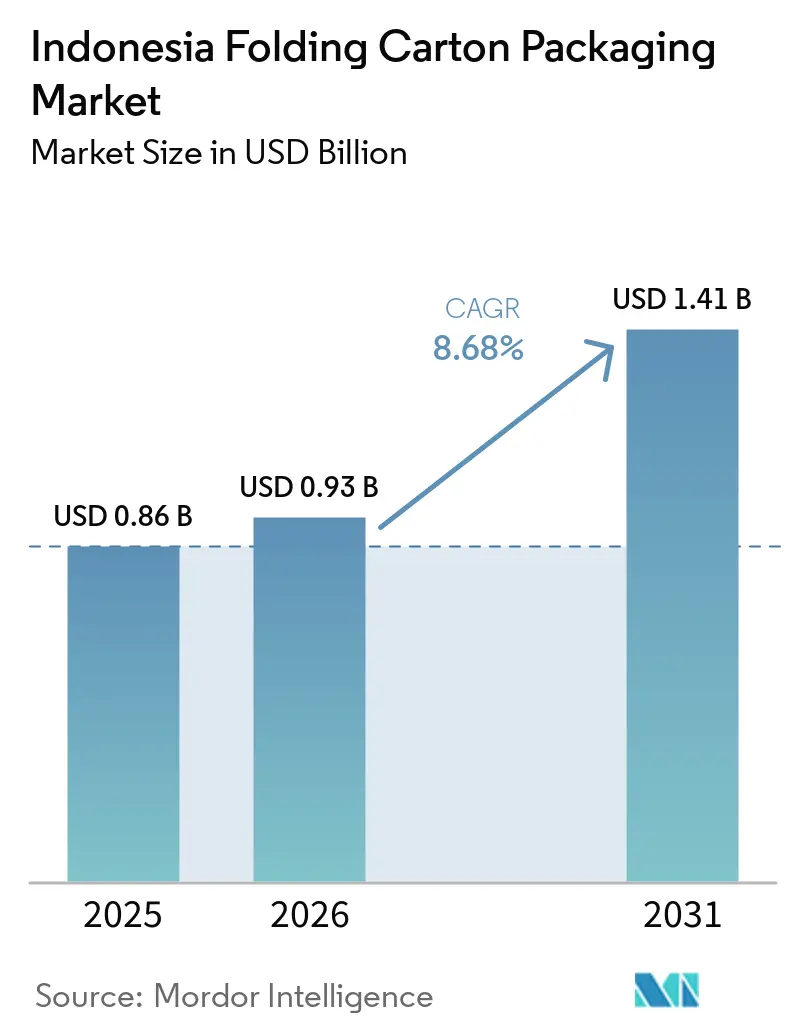

| Base Year Market Size (2025) | USD 0.86 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 8.68% CAGR |

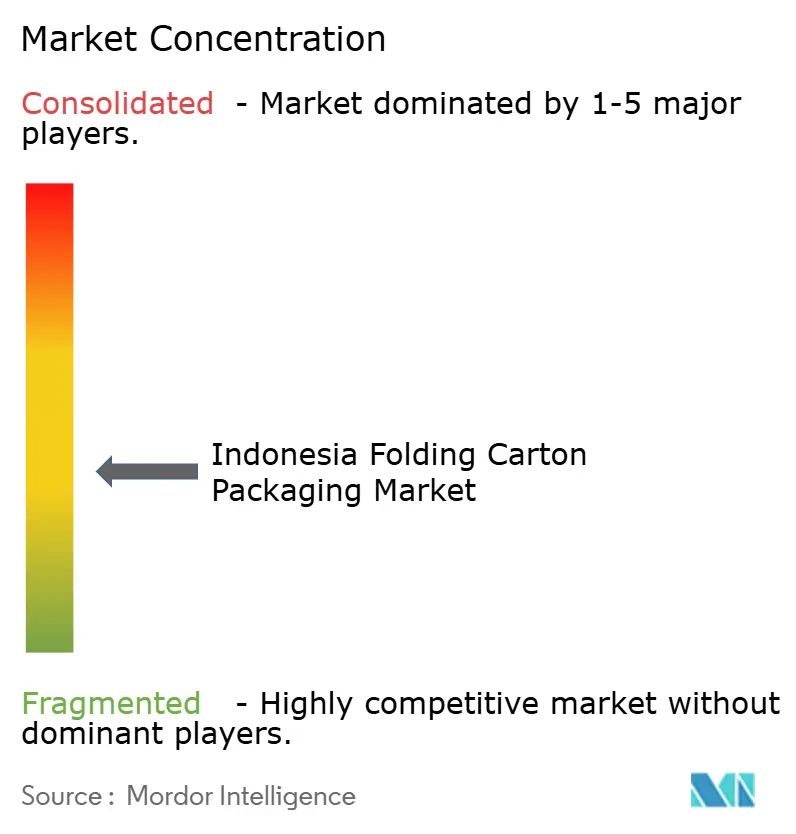

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Folding Carton Packaging Market Analysis by Mordor Intelligence

The Indonesia folding carton packaging market size was valued at USD 0.86 billion in 2025 and is projected to reach USD 1.41 billion by 2031, growing at a CAGR of 8.68% during 2026-2031. The Indonesia folding carton packaging market is expanding as procurement shifts away from flexible films toward paper-based rigid formats, driven by regulatory changes, e-commerce logistics, and brand economics. A consumer base of 285 million and broad manufacturing activity continue to support packaging demand, and the Industrial Confidence Index stood at 54.02 in February 2026, which points to continued momentum in factory output and related carton consumption. The plastic pellet price shock in 2026 has also changed material comparisons, since much higher polymer costs have made paperboard substitution more practical for several packaging uses. New domestic paperboard capacity is improving local supply, while certified substrates are becoming more important for food, healthcare, and branded consumer goods applications.

Key Report Takeaways

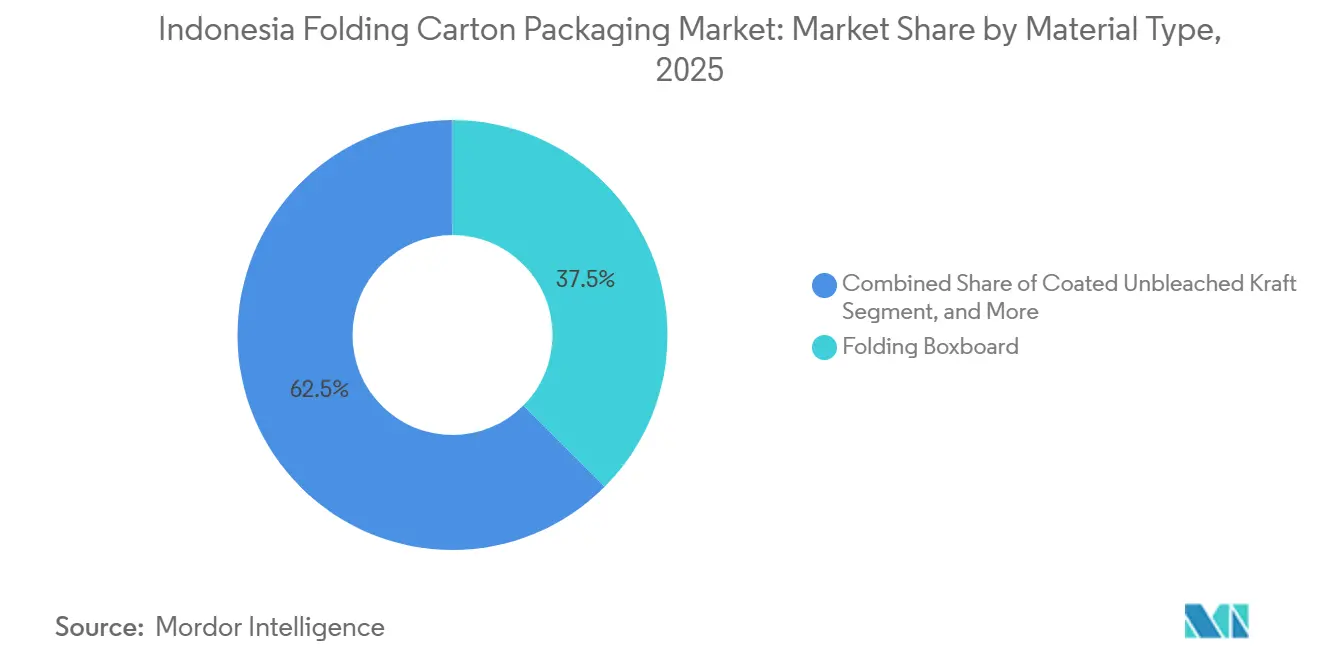

- By material type, folding boxboard captured with 37.48% of the Indonesia folding carton packaging market share in 2025.

- By printing technology, the Indonesia folding carton packaging market size for digital printing is projected to grow at a 10.93% CAGR to 2031.

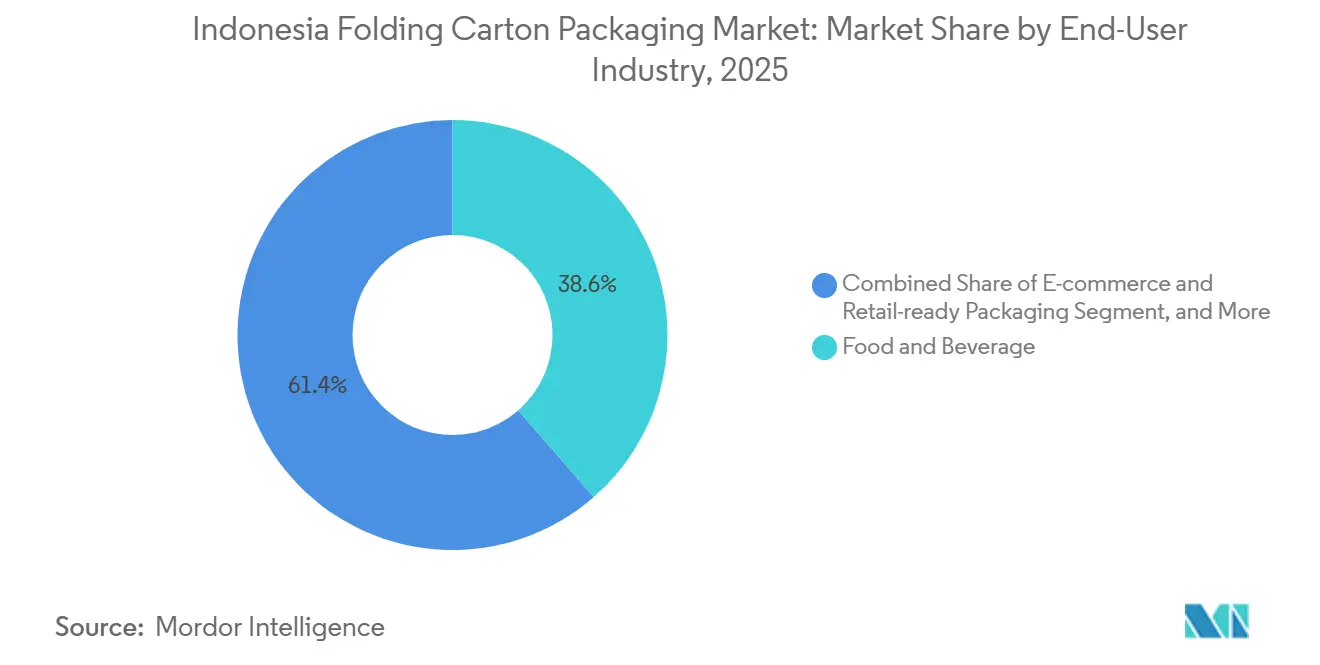

- By end-user industry, the food and beverage industry captured 38.59% of the Indonesia folding carton packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Folding Carton Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging E-Commerce Penetration Driving Demand for Ready-to-Ship Cartons | +2.3% | National, with early gains in Jakarta, Surabaya, Bandung, and Medan | Short term (≤ 2 years) |

| Rising Food-Safety Regulations Favoring Paper-Based Packaging | +1.8% | National, compliance-intensive in Java and key export-oriented production facilities | Short term (≤ 2 years) |

| Growing Middle-Class Purchasing Power Stimulating Branded Goods | +1.5% | National, concentrated in Java and Bali consumer markets | Medium term (2-4 years) |

| Expansion of Quick-Service Restaurants and Takeaway Culture | +1.2% | National, with faster penetration in secondary cities across Tier 2 and Tier 3 markets | Medium term (2-4 years) |

| Adoption of Digital Printing for Short-Run Personalization | +0.8% | APAC core, spill-over to key Indonesian metro and e-commerce hubs | Medium term (2-4 years) |

| Government Incentives for Domestic Paperboard Production | +0.7% | National, concentrated in Java and Sumatra industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging E-Commerce Penetration Driving Demand for Ready-To-Ship Cartons

The Indonesia folding carton packaging market is gaining direct support from the country’s large and still-expanding digital commerce base, with Indonesia’s digital economy nearing the USD 100 billion mark in 2025 and remaining the largest in Southeast Asia. In 2025, e-commerce GMV reached USD 71 billion, and in 2026, online transaction activity continues to broaden across both major metros and secondary cities. Cartons now serve 2 roles at once: protecting products in transit and serving as a visible brand surface during delivery and unboxing. Live-streaming commerce rose from less than 5% of Indonesia’s online GMV in 2022 to around 20% in 2025, making short-run, versioned, and camera-ready packaging far more relevant to brand owners. The daily parcel flow handled by J&T Express, JNE, and SiCepat exceeds 3 million units, so durable outer presentation has become part of the product experience rather than a secondary packaging concern. This is why converters that can deliver fast-turn, digitally printed, retail-ready packs are positioned to capture a larger share of new demand in the Indonesia folding carton packaging market.

Rising Food-Safety Regulations Favoring Paper-Based Packaging

The Indonesia folding carton packaging market is also being shaped by a tighter compliance framework for food-contact substrates. Indonesia’s Ministry of Industry issued Permenperin No. 6/2025 on January 24, 2025, which made SNI 8218:2024 mandatory for paper and cardboard used as primary food packaging materials, effective July 24, 2025, with a transition deadline of July 24, 2026, for products manufactured or imported before the effective date. The regulation covers multiple paper and board grades used in primary food packaging, meaning compliance is now tied directly to standard procurement decisions rather than treated as a specialized requirement. In parallel, the Food and Drug Authority conducted a public consultation in October 2025 on a revised food contact materials regulation that sets specific and overall migration limits for packaging materials, including paper and cardboard. This combination favors mills and converters that have already invested in certification, testing, and traceability, as it provides brand owners with a safer route to compliance. Food and beverage companies that shift toward compliant FBB and SBS grades not only meet current requirements but also reduce future enforcement risk. That dynamic gives paper-based formats a more durable place in the Indonesia folding carton packaging market.

Growing Middle-Class Purchasing Power Stimulating Branded Goods

The Indonesian folding carton packaging market continues to benefit from broad consumer demand, even as spending growth becomes more selective across household budgets. The strongest volume support is coming from everyday branded categories such as packaged food, over-the-counter health products, supplements, personal care items, and other affordable premium goods. That matters because these categories rely on secondary cartons that balance presentation, protection, and unit economics without moving into luxury packaging territory. Producers that can hold print quality while controlling substrate costs are therefore in a stronger position than suppliers focused only on the highest-end carton grades. Indonesia also remains supported by a large consumer base of 285 million and a manufacturing sector that is still expanding, which helps preserve the breadth of demand for branded packaged products. This keeps the Indonesia folding carton packaging market tied to mass consumption rather than to a narrow premium niche.

Expansion of Quick-Service Restaurants and Takeaway Culture

The Indonesian folding carton packaging market is seeing steady demand driven by the expansion of quick-service restaurants and broader takeaway habits. PT Fast Food Indonesia Tbk, the licensed KFC Indonesia operator, is targeting 60 new KFC and Taco Bell outlets in 2026 with capital expenditure of IDR 300 billion (USD 18.4 million), as part of a long-term goal of 1,000 outlets by 2030. McDonald’s Indonesia reached 300 restaurants in April 2026, indicating that national food-service chains are still expanding their physical footprint. Expansion is moving into Tier 2 and Tier 3 cities, where current outlet density remains low and maintaining supply consistency is more difficult. These markets often rely on smaller local converters, and that can create uneven performance in food-contact compliance, print quality, and turnaround speed. National franchise systems need the same burger boxes, fry cartons, meal carriers, and promotional sleeves across all regions, not only in Java. Converters that can deliver standardized, certified, and repeatable carton formats outside the main urban clusters, therefore, have a clearer growth path in the Indonesia folding carton packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper Import Policies | -1.5% | National, concentrated in Riau and West Java mill clusters | Short term (≤ 2 years) |

| Competition from Flexible Plastics in Cost-Sensitive Segments | -1.0% | National, particularly in small-format consumer goods and MSME packaging | Medium term (2-4 years) |

| Limited Collection Infrastructure for Post-Consumer Cartons | -0.8% | National, with the widest gap in Eastern Indonesia and the outer islands | Long term (≥ 4 years) |

| Energy-Price Fluctuations Escalating Converting Costs | -0.6% | National, primarily in Java-based converting facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Import Policies

The Indonesian folding carton packaging market remains exposed to input risk because domestic secondary fiber collection is still insufficient to meet mill requirements on its own. Total paper imports reached USD 3.4 billion in 2024 and an estimated USD 3.6 billion in 2025, while rising imports from China prompted the Indonesian Pulp and Paper Association to request anti-dumping investigations in duplex and packaging paper categories.[1]Dony Aprian, “Paper Imports From China Soar, Even Though Domestic Production Is Sufficient,” VOI.ID, voi.id This creates pricing pressure from 2 directions: mills face uncertainty in raw material sourcing, while local producers also have to respond to competitive import flows. Integrated players can manage that pressure more effectively because they have a larger procurement scale and stronger control over board supply. Smaller converters are more exposed, since even modest shifts in paper input costs can quickly affect quoted prices and order profitability. Until local recovery systems scale up, this issue will remain a recurring drag on the Indonesian folding carton packaging market.

Competition From Flexible Plastics in Cost-Sensitive Segments

The Indonesia folding carton packaging market also continues to compete with flexible plastics in categories where low unit cost matters more than shelf impact or stiffness. That pressure is most visible in small-format packaging for snacks, spices, and household goods, where many MSME brands still prefer film-based formats because the installed base was built around them. Plastic pellet prices doubled by April 2026 due to Middle East supply chain disruptions, narrowing the cost gap enough to trigger material reviews in several applications. Even so, switching remains uneven because converting lines cannot be retooled without capital spending, technical changes, and customer approval. This means paperboard substitution will move faster in regulated or brand-sensitive uses than in the most price-driven packs. Flexible formats, therefore, remain a meaningful restraint on the Indonesia folding carton packaging market, even while the cost advantage is less stable than it was before 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Folding Boxboard Leads as Coated Unbleached Kraft Gains Ground

Folding boxboard held 37.48% of the Indonesia folding carton packaging market share within the material type in 2025. Its lead position came from uses where stiffness, clean print reproduction, and a smooth surface are important, especially in food, healthcare, and personal care cartons. These categories tend to value both appearance and structural reliability, which keeps FBB relevant across a wide range of branded uses. Domestic supply improved after APRIL Group brought its Kerinci paperboard mill into operation, investing USD 2.3 billion and achieving an annual capacity of 1.2 million metric tons under the BoardOne and SilverPak brands.[2]APRIL Group, “Paperboard Mill, Kerinci | Renewable Plantation Fibre | PEFC Certified,” APRIL Group, aprilasia.com That capacity addition gives local converters better access to premium board and helps reduce dependence on imported supply for high-specification cartons.

Solid bleached sulfate kept a premium role in healthcare and cosmetics packaging, where whiteness, surface quality, and sharp graphics remain specification-critical. Its growth is steadier than that of more economical grades because many mid-tier brand owners still weigh visual quality against cost. The Indonesia folding carton packaging market size for coated unbleached kraft is projected to expand at 10.12% CAGR from 2026 to 2031, making it the fastest-growing material type. CUK is benefiting from its grease resistance and stronger structure, which make it useful in fast-food service packs, e-commerce transit packs, and other applications that need both durability and acceptable presentation. APP Group’s May 2025 launch of Sinar Vanda Hi-Brite C1S, which offered 10-20% higher yield at 92 brightness, shows that mills in Indonesia are still investing in product development for premium paperboard requirements without giving up cost discipline.

By Printing Technology: Lithographic Dominance Persists as Digital Accelerates

Lithographic printing accounted for 43.26% of printing technology revenue in 2025. Its lead reflects the economics of long production runs, where plate costs can be spread across large order volumes and color consistency matters over time. Food and beverage, tobacco, and personal care cartons still fit this model in many mainstream programs, especially when the same design is repeated across broad national distribution. Flexographic printing has built a meaningful role in retail-ready and corrugated-adjacent formats, where speed and substrate flexibility can matter more than the finest graphic detail. Gravure remains relevant for narrower, premium runs that require precise color matching or metallic effects, but its setup cost keeps it out of most short-run work.

The Indonesia folding carton packaging market for digital printing is projected to expand at a 10.93% CAGR through 2031, making it the fastest-growing printing format. That pace reflects a change in how brand owners are using packaging, since they now want more frequent design refreshes, smaller batches, and faster promotional response. Digital presses are becoming more attractive for e-commerce campaigns, seasonal launches, live-streaming commerce packs, and limited-edition quick-service restaurant programs that do not suit long lithographic runs. The commercial appeal of digital carton work was reinforced at a Jakarta seminar in April 2026, where folding carton was highlighted as one of the most promising areas for digital print investment and brand-led customization.

By End-User Industry: Food and Beverage Anchors Volume as E-Commerce Redefines Growth Expectations

Food and beverage accounted for 38.59% of the Indonesia folding carton packaging market size in 2025. This segment remains the main demand anchor because packaged foods, beverages, and takeaway applications generate steady repeat volumes across modern retail, convenience channels, and food service. Regulatory support also matters here, since Indonesia made SNI 8218:2024 compliance mandatory for paper and cardboard used as primary food packaging under Permenperin No. 6/2025. Healthcare and pharmaceuticals form a stable and specification-driven segment where SBS and FBB stay important because performance and compliance matter more than lowest cost. Personal care and cosmetics are also contributing more, especially in skin care and hair care sold through modern trade and online channels, where visual presentation remains part of the product value.

E-commerce and retail-ready packaging is projected to grow at a 11.57% CAGR from 2026 to 2031, making it the fastest-growing end-user group. This rise aligns with a large digital commerce base, stronger parcel movement, and the need for carton formats that serve both shipping support and branded presentation. Electrical and electronics use cartons mainly for retail-grade secondary packaging, where protection and shelf appearance are combined in a single pack. Tobacco remains a mature contributor, but growth is more constrained because excise changes and plain-packaging discussions can limit packaging upside over time. Household and industrial goods continue to rely on more cost-driven board structures, which means their carton demand is more exposed to shifts in consumer spending and procurement discipline.

Geography Analysis

Java remained the core geography for the Indonesia folding carton packaging market in 2026, with converting activity centered around Greater Jakarta, Surabaya, and Semarang. Upstream mill capacity is more concentrated in Sumatra, especially in Riau, and in Banten, which means board production and carton conversion do not always sit in the same logistics corridor. That separation adds inter-island transport cost and lead-time friction that are less visible in flatter domestic packaging systems. PT Indah Kiat Pulp and Paper Tbk’s Karawang mill ramp-up in West Java is changing part of that equation, because the site carries a combined annual capacity of 2.4 million metric tons of white and brown paper and is expected to move from 60% utilization in 2026 to 85-90% in 2027.[4]ANDRITZ Group, “Indah Kiat Starts Up New High-Capacity ANDRITZ OCC Line and Reject Treatment System in Indonesia,” ANDRITZ Group, andritz.com Closer supply near Java’s converting base should improve board availability and reduce some of the structural transport disadvantage inside the Indonesia folding carton packaging market.

Outer-island regions such as North Sumatra, Sulawesi, and East Kalimantan are still at an earlier stage of carton adoption, with many users relying more heavily on flexible packaging or shipments from Java-based suppliers. Demand is now broadening as modern retail, quick-service restaurant expansion, and branded FMCG distribution are driving standardized packaging requirements beyond the main island. The fact that around 70% of current Indonesian QSR outlets are absent from Tier 2 and Tier 3 cities shows how much room remains for food-service carton demand outside the biggest urban centers. As brands push further into these regions, they are placing more value on packs that hold up across longer transit routes and more variable handling conditions.

Indonesia’s broader pulp and paper base also gives the country a different position inside ASEAN. The country had 113 companies with annual paper production capacity of 25.37 million metric tons in 2025, ranking 6th globally. That supply depth gives local converters a more favorable position than markets that depend more heavily on imported board, and it supports the case for export-oriented converting tied to regional logistics chains. Indonesia’s role as a partner country at INNOPROM 2026 also shows that the government is actively presenting domestic pulp and paper capabilities to overseas industrial corridors. This strengthens the regional relevance of the Indonesia folding carton packaging market beyond domestic demand alone.

Competitive Landscape

The Indonesia folding carton packaging market has a two-layer competitive structure, with a more fragmented downstream converting base. APP Group, through PT Indah Kiat Pulp and Paper Tbk and PT Pabrik Kertas Tjiwi Kimia Tbk; APRIL Group, through PT Riau Andalan Paperboard International; and Pura Group hold the strongest positions in domestic paperboard supply. The converting layer is far less concentrated because many small- and mid-sized operators compete on price, lead time, and customer service rather than on control of raw-material supply. This creates a market where board access, certification readiness, and delivery consistency matter as much as headline capacity. It also means the Indonesian folding carton packaging market can appear concentrated at the substrate level while remaining highly competitive at the converter level.

PT Indah Kiat strengthened its position in February 2026 when it started up a new 2,000 TPD OCC line in Karawang, supported by AI-based quality control systems from Siemens and ABB. The project adds around 700,000 metric tons of annual recycled fiber capacity, improving cost control and providing the company with greater protection against swings in recovered paper imports. APRIL’s Kerinci paperboard mill also reinforces domestic board availability, with USD 2.3 billion of investment and 1.2 million metric tons of annual capacity aimed at premium folding boxboard demand in Indonesia and export markets. Large mill-backed moves like these raise the competitive bar for independent converters, especially when customers need secure board access and reliable compliance support.

Pura Group has also been reshaping its position, and its 2025 transformation into 5 integrated industrial solutions shows a broader push beyond traditional conversion into a wider packaging and printing platform.[3]Pura Group, “Pura Group's Transformation and 5 Future Integrated Industrial Solutions,” Pura Group, puragroup.com White-space opportunities remain strongest in pharmaceutical-grade cartons, digital short-run jobs for e-commerce, and regional service models built around Tier 2 and Tier 3 city demand. Converters that can combine compliance capability, shorter lead times, and small-batch print flexibility are starting to pressure older lithographic business models that depend on high-volume annual programs. The Indonesia folding carton packaging market is therefore likely to remain competitive, but advantage is moving toward suppliers with stronger integration, faster response, and better alignment with changing customer specifications.

Indonesia Folding Carton Packaging Industry Leaders

PT. Amcor Flexibles Indonesia

Tetra Pak International S.A.

Asia Pulp & Paper (APP) Group

PT Graphic Packaging International Indonesia

Mayr-Melnhof Karton AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pura Group advanced pharmaceutical packaging innovation across Southeast Asia through its MIFP business unit, delivering premium flexible and rigid packaging with advanced rotogravure printing and anti-counterfeit holographic solutions for pharmaceutical and FMCG brands, strengthening its position as an integrated packaging platform.

- April 2026: Indonesia's Ministry of Industry formally called for packaging diversification toward paper, glass, and metal formats in response to plastic pellet prices doubling due to Middle East supply chain disruptions.

- February 2026: PT Indah Kiat Pulp and Paper Tbk (APP Group) commissioned an advanced 2,000 TPD OCC recycling line at its Karawang, West Java mill, supplied by ANDRITZ with AI-based quality control by Siemens and ABB, adding 700,000 metric tons per year of recycled fiber capacity for containerboard and packaging production at an investment of USD 150 million.

- December 2025: Pura Group announced its transformation into 5 integrated industrial solutions, including a commercial printing solution producing premium cardboard boxes via flexographic and offset printing technology, marking a strategic reorientation from traditional packaging converter toward a vertically integrated packaging-plus-technology platform.

Indonesia Folding Carton Packaging Market Report Scope

The scope of this report covers the analysis of the folding cartons market in Indonesia. Folding cartons are paper-based packaging solutions widely used across various industries. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future prospects.

The Indonesia Folding Carton Packaging Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

By Printing Technology

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

By End-User Industry

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast value of Indonesia folding carton packaging demand?

The sector was valued at USD 0.86 billion in 2025 and is projected to reach USD 1.41 billion by 2031, with an 8.68% CAGR during 2026-2031.

What is driving carton use in Indonesia the most right now?

The strongest demand drivers are e-commerce expansion, tighter food-contact rules, higher plastic input costs, and broader quick-service restaurant growth across major and secondary cities.

Which material type leads carton use in Indonesia?

Folding boxboard led material demand with a 37.48% share in 2025 because it remains well suited to food, healthcare, and personal care packaging.

Which end-user category is expanding the fastest?

E-commerce and retail-ready packaging is the fastest growing end-user group, with an 11.57% CAGR expected through 2031.

Why is digital printing becoming more important in cartons?

Digital printing is forecast to grow at a 10.93% CAGR because brand owners want shorter runs, faster design changes, and better support for promotional and online-led campaigns.

How is geography shaping supply and demand across Indonesia?

Java remains the main converting hub, while Sumatra and Banten hold major mill capacity, and outer-island demand is rising as QSR, FMCG, and modern retail move deeper into secondary cities.

Page last updated on: