Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

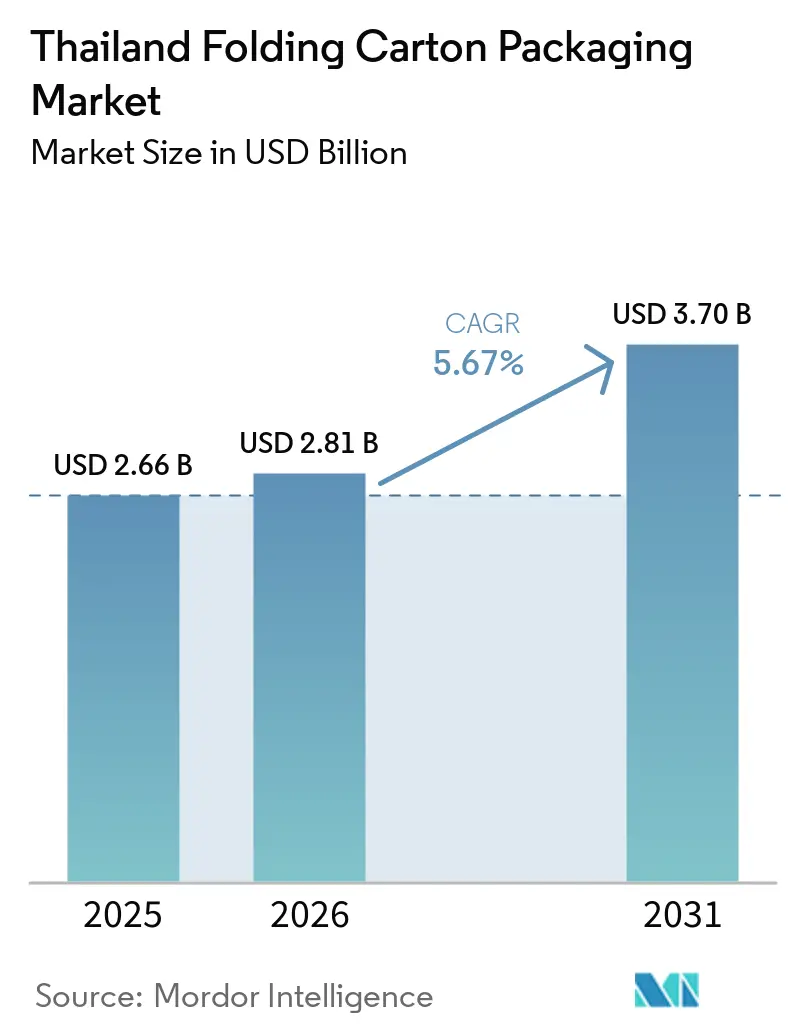

| Base Year Market Size (2025) | USD 2.66 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.70 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

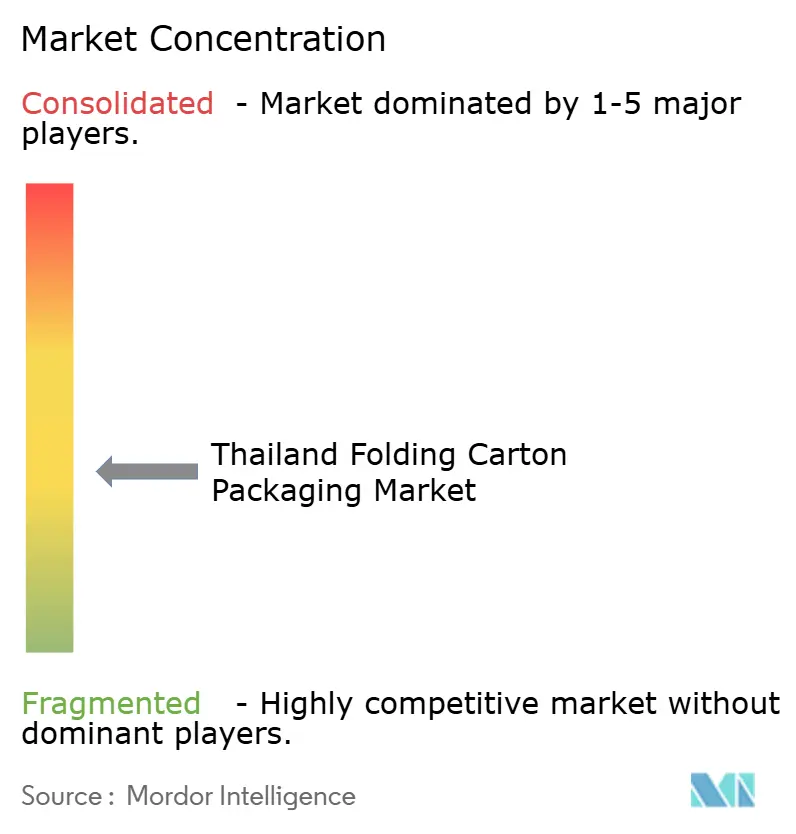

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Folding Carton Packaging Market Analysis by Mordor Intelligence

The Thailand folding carton packaging market was valued at USD 2.66 billion in 2025 and estimated to grow from USD 2.81 billion in 2026 to reach USD 3.7 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031). Robust e-commerce volume, relocations of printing and converting capacity from China, and a sustained consumer shift to packaged foods anchor demand. Digital short-run carton presses are lowering minimum order quantities for small brands, while mandatory extended producer responsibility (EPR) rules are nudging converters toward recycled-content substrates. Rising tourism recovery is also inflating demand for premium personal-care and confectionery cartons as international brands localize manufacturing. Capacity additions within the Eastern Economic Corridor keep supply responsive, but electricity price uncertainty and recycled fiber cost swings test converter margins.

Key Report Takeaways

- By printing technology, offset lithography captured 51.98% of the Thailand folding carton packaging market share in 2025.

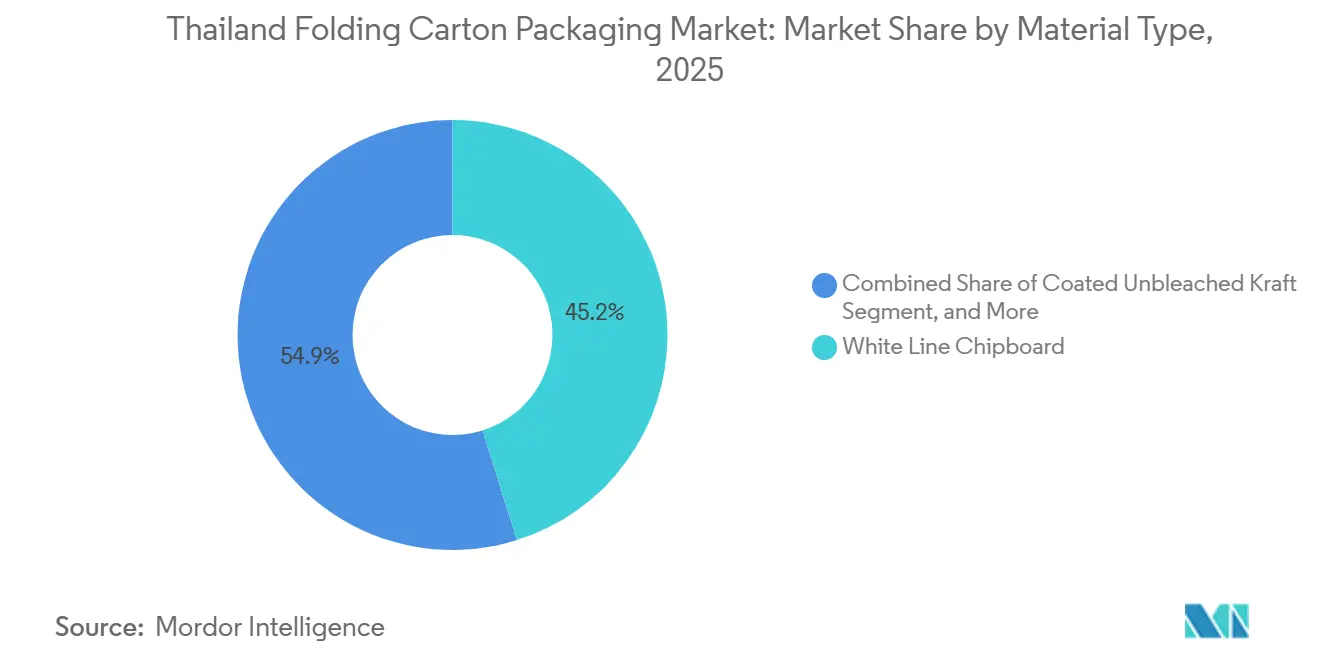

- By material type, the Thailand folding carton packaging market size for folding boxboard is projected to grow at a 6.51% CAGR between 2026 to 2031.

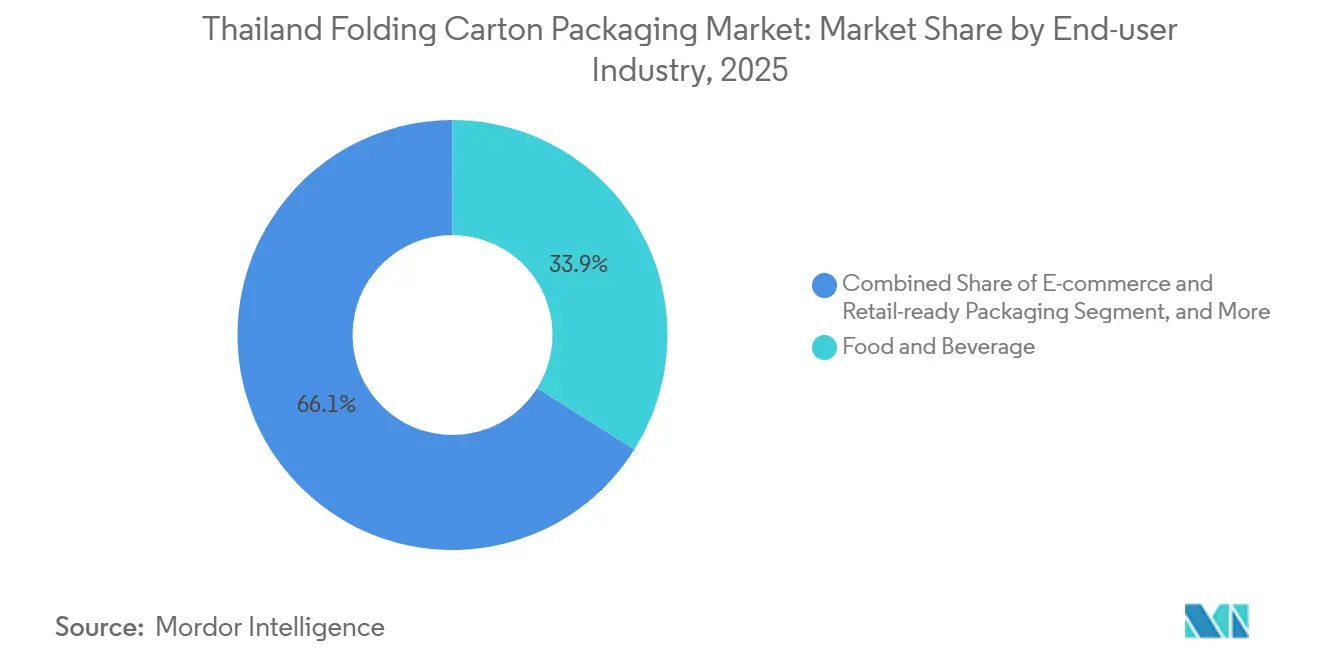

- By end-user industry, food and beverages captured a 33.92% of the Thailand folding carton packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Folding Carton Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust E-Commerce Volume Growth and Sustainability Commitments | +1.2% | National (Bangkok, major urban centers) | Medium term (2-4 years) |

| FMCG Brand Shift Toward Premium Printed Cartons | +0.9% | National (premium focus in Bangkok, tourist zones) | Medium term (2-4 years) |

| Government EPR Draft Law Catalyzing Recycled-Content Demand | +0.7% | National (industrial zones) | Long term (≥ 4 years) |

| Commercial Rollout of Digital Short-Run Carton Presses | +0.8% | National (manufacturing clusters) | Short term (≤ 2 years) |

| High-Speed Offset Capacity Relocations from China to Thailand | +1.1% | Eastern Economic Corridor | Medium term (2-4 years) |

| Meal-Kit and Ready-Meal Subscriptions Surge | +0.6% | Urban centers, secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust E-Commerce Volume Growth and Sustainability Commitments

Thai online retail sales reached USD 26.5 billion in 2023 and are projected to reach USD 32 billion by 2025, driving demand for protective yet brand-forward folding cartons. Large platforms increasingly mandate recycled content to align with corporate ESG goals, compelling converters to secure stable recycled fiber supplies despite volatile import flows. Retailers expanding their omnichannel operations require standardized die lines that can move seamlessly from warehouse to doorstep, pushing multipurpose carton designs. Sustainability pledges are driving the adoption of water-based coatings as PFAS-free alternatives, despite the persistence of cost premiums of USD 0.02-0.05 per m². Together, rising parcel counts and green-packaging targets underpin consistent mid-single-digit volume growth for the Thailand folding carton packaging market.

FMCG Brand Shift Toward Premium Printed Cartons

Thailand’s middle-income households and tourist influx encourage brand owners to upgrade shelf presence with embossed, matte-varnish, and holographic carton finishes. Shorter product lifecycles and seasonal collections require nimble changeovers, a sweet spot for digital presses capable of 15-minute makereadies. R&D spending by technology vendors such as Tetra Pak, about EUR 100 million (USD 118 million) per year, is channeling barrier coatings that enable the reduction of plant energy use by 40% while supporting premium graphics. Premiumization is most visible in personal-care, cosmetics, and specialty confectionery, where packaging is a primary purchase trigger.

Government EPR Draft Law Catalyzing Recycled-Content Demand

The draft Extended Producer Responsibility framework will make brand owners financially liable for post-consumer packaging collection, likely phasing in across industrial zones first. Early compliance strategies include contracts with cooperatives to secure baled fiber, mirroring pilot schemes in neighboring Vietnam. Exporters must also heed China’s express-package standard, GB 43352-2023, which caps heavy-metal content, thereby pushing Thai converters toward certified recovered paper streams.[1]CIRS Testing, “China’s First Mandatory Express Packaging Standard GB 43352-2023,” cirs-ck.com The three-year runway to full implementation incentivizes investments in optical sorting lines and moisture-controlled warehouses that stabilize fiber quality and costs.

Commercial Rollout of Digital Short-Run Carton Presses

Next-generation web-fed digital presses now deliver up to 25,000 impressions per hour, closing total-cost-of-ownership gaps with mid-volume offset jobs. Board of Investment incentives allow accelerated depreciation and interest-rate subsidies, lowering capital hurdles. Economic quantities have dropped to 500–1,000 units, enabling D2C start-ups to procure store-quality cartons without excess inventory. Converters leverage variable-data capability for pharmaceutical serialization and QR-enabled promotions that enhance consumer engagement. The technology also cuts waste by about 20% through single-pass workflows, supporting both cost savings and ESG metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paperboard Price Volatility Linked to China’s Import Policy | -0.8% | National (all converters) | Medium term (2-4 years) |

| Soaring Industrial Electricity Tariffs | -0.6% | National (energy-intensive operations) | Short term (≤ 2 years) |

| Fragmented SME Converting Base Limiting Quality Control | -0.4% | National (smaller converters) | Long term (≥ 4 years) |

| PFAS-Free Coating Compliance Costs | -0.3% | National (food-contact uses) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paperboard Price Volatility Linked to China’s Import Policy

China’s 2018 ban on mixed-paper imports cascaded into Southeast Asia, flooding Thai mills with inconsistent feedstock and sending mixed-paper prices from above USD 60 per ton in 2017 to near zero before rebounding.[2]U.S. International Trade Commission, “China’s Recycled Wastepaper Import Policies: Part 1,” usitc.gov Converters struggle to hedge cost swings because domestic collection rates lag developed-market norms. Recent capacity additions in regional recycling plants are narrowing quality gaps, yet policy pivots, such as potential quota reductions in Indonesia, keep price risk elevated. Larger Thai players stock three-month fiber inventories, but SMEs operating on thin working capital cannot absorb sudden spikes, compressing margins and occasionally prompting production halts.

Soaring Industrial Electricity Tariffs

Thailand’s Energy Regulatory Commission toyed with a 44% tariff hike in 2024 before freezing rates at around THB 4.18 per kWh (USD 0.12 per kWh) to preserve export competitiveness. The reprieve is temporary; planned LNG-fired generation and grid upgrades presage upward adjustments once elections pass. Converters running UV curing, hot-foil stamping, and climate-controlled die-cutting rooms are disproportionately exposed. Those installing rooftop solar arrays meet up to 10% of their load and lock in long-term savings, but project paybacks stretch to seven years for firms lacking preferential financing. Thus, rising energy costs remain a profitability headwind for the Thailand folding carton packaging market over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Chipboard dominance faces sustainable alternatives

White-lined chipboard accounted for 45.15% of the Thailand folding carton packaging market in 2025, due to its printability and cost advantage. Brands favor its smooth surface for high-resolution imagery, but folding boxboard is growing at a 6.51% CAGR as retailers pledge to reach 30% recycled content by 2030. Folding boxboard’s stiffness-to-weight ratio enables down-gauging, which reduces freight costs by 8-10% for cross-border shipments to the CLMV (Cambodia, Laos, Myanmar, Vietnam). Solid bleached board maintains a niche use in cosmetics, where brightness metrics serve shelf-impact goals; however, its higher cost limits mass adoption. Coated unbleached kraftboard appeals to electronics exporters who value puncture resistance for heavy components.

Barrier-coated grades integrating vapor-deposited aluminum oxide (AlOx) raise the functional ceiling for folding boxboard, enabling migration-safe packaging for nuts, chocolate, and powdered drinks. SRF Limited’s third BOBST metallizer installation, scheduled for September 2025 in Rayong, will increase the regional output of high-barrier films that feed laminate structures.[3]Packaging Strategies, “SRF Limited Purchases Third BOBST Machine,” packagingstrategies.com These material shifts underscore an emerging hierarchy where chipboard dominates volume but folding boxboard captures reputational mindshare in the Thailand folding carton packaging market.

By Printing Technology: Digital transformation accelerates customization

Offset lithography retained 51.98% share in 2025 as long-run snack and cigarette cartons keep presses booked, yet digital printing is climbing 6.92% CAGR thanks to beverage brands increasingly personalizing campaigns for TikTok micro-influencers. Hybrid lines route static base graphics through offset units and variable text or codes through inkjet heads, blending economies of scale with flexibility. Run lengths of 3,000-5,000 units, once uneconomical digitally, are now break-even under click-charge contracts offered by equipment makers.

Color-management software complying with ISO 12647 standards curbs delta-E variance below 2.0 and satisfies multinational buyers. Flexography maintains relevance on kraft-board vegetable crates that demand heavy ink laydown, while gravure sees limited use in duty-free confectionery multipacks where print cylinders amortize across millions of impressions. Taken together, technology diversification positions converters to offer multi-tier service models essential for the Thailand folding carton packaging market.

By End-user Industry: Food sector drives premium packaging evolution

The food and beverage segment held 33.92% of the Thailand folding carton packaging market share in 2025 as processors prioritized hygienic, brand-centric cartons that extend shelf life for ready-to-eat meals. Convenience-oriented portion packs, especially meal-kit inserts, account for a rising slice of volume. Tight traceability rules imposed by supermarket chains are guiding converters toward digital watermarks and tamper-evident closures that justify price premiums. Meanwhile, healthcare and pharmaceuticals are the fastest-growing users at a 7.63% CAGR. Foreign drug makers localizing blister-card packaging in Rayong and Chonburi demand serialization and 100% print-defect inspection, channeling investment into high-speed camera systems.

The Thailand folding carton packaging market for healthcare cartons is forecast to expand further as medical tourism traffic rebounds and local vaccine fill-and-finish plants add capacity. In cosmetics and personal care, tourist-led gift purchases support textured UV lacquers and foil accents. Converters able to simulate a luxury rigid-box appearance with single-piece folding techniques capture incremental margins. The tobacco segment, constrained by plain-pack rules, is substituting minimalist brown chipboard but remains price sensitive. Overall, cross-segment convergence on PFAS-free and recycled-content substrates is reshaping procurement contracts and prompting multiyear volume guarantees that stabilize plant utilization rates across the Thailand folding carton packaging market.

Geography Analysis

Eastern Economic Corridor plants account for about 60% of the nation's converting capacity, leveraging proximity to the Laem Chabang port and well-developed paper mills. Board of Investment tax holidays spur capital migration from Guangdong and Fujian, injecting modern high-speed offset lines.[4]Thailand Board of Investment, “Investment Promotion Measures in the Eastern Economic Corridor,” boi.go.th Bangkok accounts for over 40% of carton consumption due to its dense FMCG headquarters, 3PL hubs, and the country’s largest e-commerce fulfillment centers.

Tourism-heavy Phuket and Chiang Mai experience seasonal surges in demand for personal-care gift packs, while Khon Kaen in the northeast is advancing as an agro-processing hub that requires moisture-barrier cartons. Digital printing clusters around Samut Prakan and Pathum Thani, where skilled operators and service engineers are readily available. These areas also benefit from proximity to industrial zones, enhancing operational efficiency.

Rural regions rely on Bangkok-area mega-plants shipping knock-down blanks for final gluing near product-filling sites, optimizing freight costs. Government zoning for eco-industrial estates integrates waste-heat recovery networks that lower process-steam expenses for integrated board and converting mills, sustaining competitive landed costs across the Thailand folding carton packaging market. Such measures also align with sustainability goals, enhancing the market's long-term viability.

Competitive Landscape

The market is moderately fragmented, with the top five converters accounting for about 45% of revenue, creating opportunities for nimble specialists. Siam Toppan Packaging, through a strategic joint venture, minimizes press downtime, achieving over 90% utilization and focusing on high-color beverage cartons. The company also explores advanced printing technologies to enhance product differentiation. SCG Packaging uses its integrated pulp and paper operations as a buffer against fluctuations in raw material prices. It is also expanding its product portfolio to cater to diverse end-user industries.

Thai Containers Group secures supply contracts linked to retailer EPR commitments by adopting cradle-to-cradle certification. Additionally, the company invests in sustainable packaging innovations to align with evolving consumer preferences. Meanwhile, international players like TOPPAN Holdings introduce gravure cylinder expertise and advanced printing techniques for confectionery tins, resulting in significant technology transfers. These players are also leveraging their global networks to penetrate niche segments in the Thai market. While SMEs carve a niche by offering rapid gluing services for micro-flute cartons to local snack producers, they encounter certification challenges when pursuing pharmaceutical contracts.

Converters that invest early in serialization lines are reaping the rewards with multi-year contracts from vaccine manufacturers. These investments also position them as reliable partners in the pharmaceutical supply chain. Furthermore, such advancements are enabling these converters to meet stringent regulatory requirements. Technological prowess and compliance credentials are becoming the key determinants of competitive positioning in the Thai folding carton packaging landscape. Firms that emphasize these elements are poised for significant market advantages and sustained growth in the coming years.

Thailand Folding Carton Packaging Industry Leaders

Oji Paper (Thailand) Ltd.

Huhtamaki (Thailand) Ltd.

Tetra Pak (Thailand) Ltd.

Stora Enso (Thailand) Co., Ltd.

Charoen Pokphand Packaging Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fitch Ratings affirmed SCG Packaging Public Company Limited’s (SCGP) National Long-Term Rating at 'A(tha)' with a stable outlook, forecasting a recovery in EBITDA to THB 15-16 billion (USD 430-460 million) for the 2026-2027 period.

- January 2026: ProPak Asia announced its 2026 edition will move to IMPACT Muang Thong Thani with expanded industry zones. Future Food Corner and Eco-Design Innovation showcase, featuring Thai packaging manufacturers and automation systems with emphasis on sustainability and Net Zero goals.

- September 2025: Friesland Campina Ingredients opened its second APAC Application Center in Singapore to develop functional foods for Thailand and neighboring markets.

- June 2025: Green Bay Packaging committed USD 1 billion to expand an Arkansas kraft linerboard mill, adding supply that may moderate Asian containerboard pricing.

Thailand Folding Carton Packaging Market Report Scope

The folding carton market is the industry that produces, distributes, and uses paperboard-based packaging solutions that can be folded into various shapes and sizes. The scope of the study includes analyzing current market trends, growth drivers, challenges, and opportunities in Thailand's folding carton market.

The Thailand Folding Carton Packaging Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and More). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

By Printing Technology

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

By End-User Industry

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Thailand folding carton packaging market in 2026?

The market reached USD 2.81 billion in 2026 and is forecast to approach USD 3.7 billion by 2031.

Which user segment shows the fastest volume growth?

Healthcare and pharmaceuticals cartons are rising at a 7.63% CAGR through 2031 on the back of expanding drug manufacturing and medical tourism.

What material gains share from sustainability commitments?

Folding boxboard is growing 6.51% CAGR because its recycled-content profile aligns with brand EPR targets.

Why are converters investing in digital presses?

Digital technology allows 15-minute changeovers and viable runs as small as 500 units, supporting mass customization for e-commerce and seasonal SKUs.

How does electricity pricing affect Thai converters?

The freeze at THB 4.18 per kWh (USD 0.12 per kWh) keeps short-term costs stable, but anticipated hikes could squeeze margins for energy-intensive printing lines over the next two years.

What policy will reshape packaging recyclability?

Thailand’s draft Extended Producer Responsibility law will phase in producer fees for post-consumer packaging, spurring recycled-content adoption and converter consolidation.

Page last updated on: