GCC Digital Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

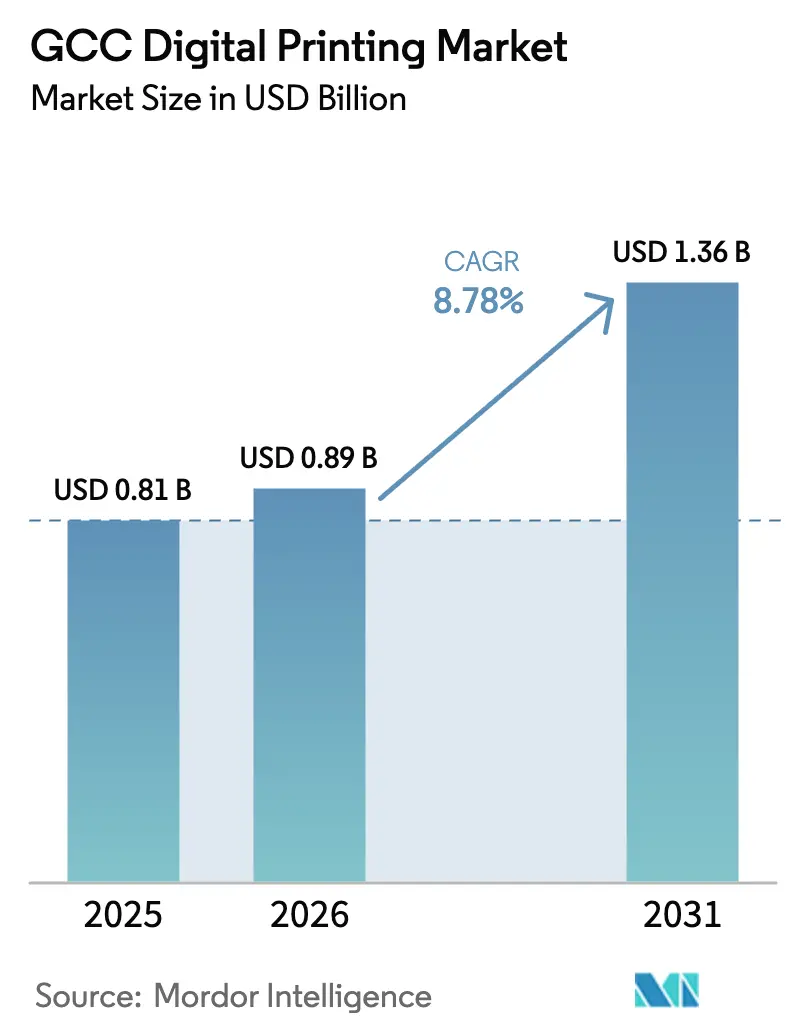

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.36 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

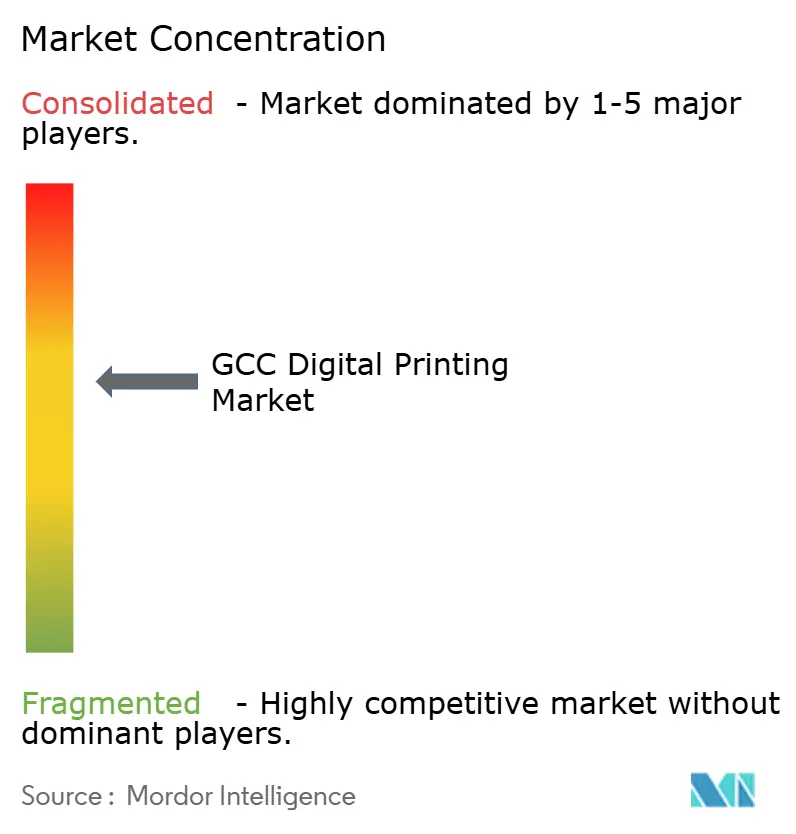

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Digital Printing Market Analysis by Mordor Intelligence

The GCC digital printing market size is expected to increase from USD 0.81 billion in 2025 to USD 0.89 billion in 2026 and reach USD 1.36 billion by 2031, growing at a CAGR of 8.78% over 2026-2031. Rapid migration from oil-linked revenue toward diversified manufacturing, surging e-commerce activity, and mandatory Arabic-language labeling rules are widening the demand base. Brand owners value the flexibility of digital press formats and their low setup costs, so converters are adding inkjet lines that can turn around jobs in 48 hours. Saudi Arabia delivers scale through Vision 2030 packaging investments, while the United Arab Emirates (UAE) supplies speed through fulfillment hubs that demand serialized labels. Capital still concentrates on LED-UV and latex platforms that eliminate water use, align with ESG-linked financing, and mitigate Gulf humidity, yet high equipment prices and skills shortages temper smaller-operator expansion.

Key Report Takeaways

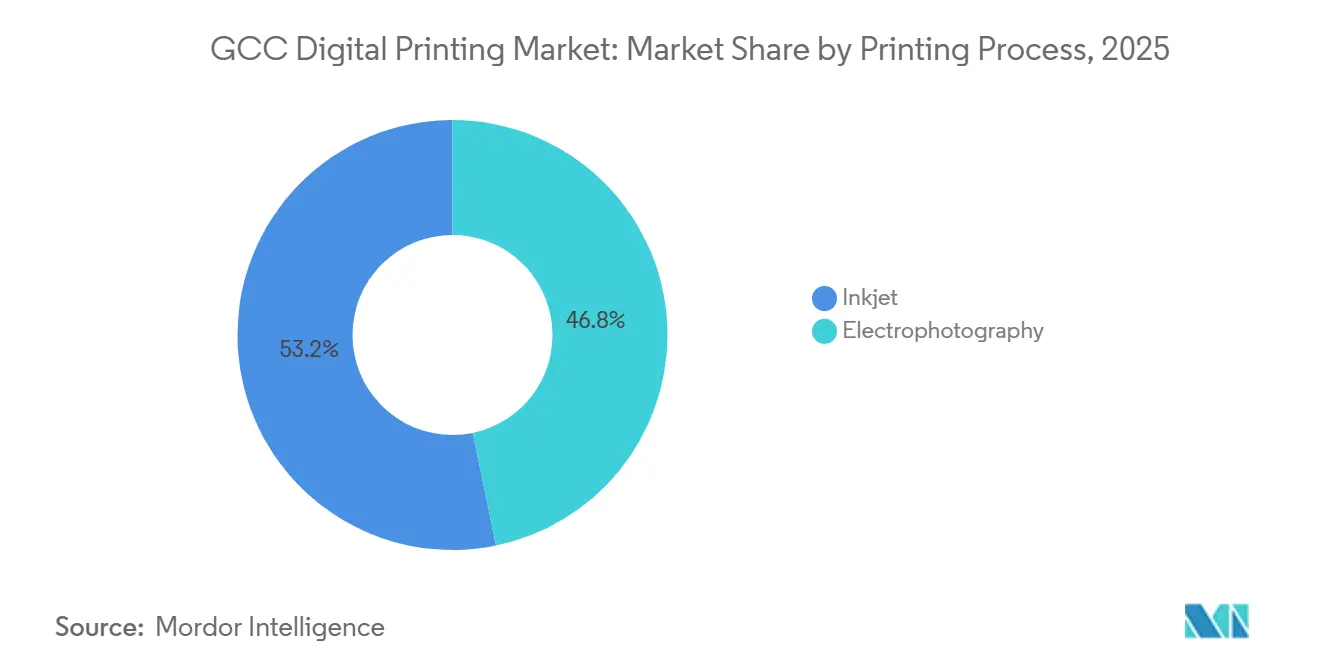

- By printing process, inkjet led with 53.24% GCC digital printing market share in 2025, and it is projected to rise at a 9.17% CAGR through 2031.

- By packaging format, labels captured 37.23% of the GCC digital printing market size in 2025, while flexible packaging is forecast to expand at a 9.92% CAGR to 2031.

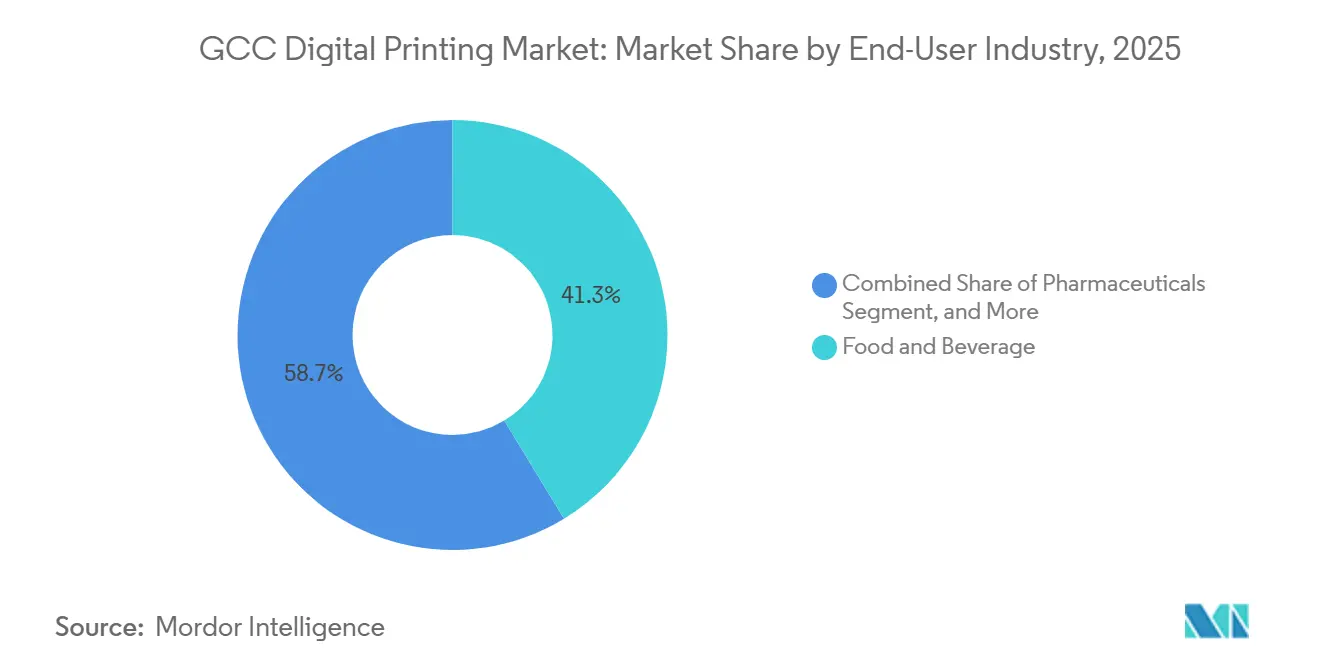

- By end-user industry, food and beverage accounted for 41.32% of 2025 revenue; personal care and cosmetics are advancing at a 9.54% CAGR through 2031.

- By ink type, UV-curable chemistries held 46.21% share of the 2025 value and will maintain a 9.61% CAGR during 2026-2031.

- By geography, Saudi Arabia dominated with 52.12% revenue share in 2025, whereas the UAE records the highest projected 9.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Middle east representing one of the more structurally developed among them. The global report on digital printing market by Mordor Intelligence reflects how these regional layers combine into a single system.

GCC Digital Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of packaging and textile industries and rising demand for digital advertisements | +2.8% | Saudi Arabia, UAE (core); spillover to Qatar, Kuwait | Medium term (2-4 years) |

| Rapid inkjet adoption for short-run and variable-data jobs | +2.3% | GCC-wide, with early gains in Dubai, Riyadh, Doha | Short term (≤ 2 years) |

| Government diversification programs fueling industrial and packaging capacity | +1.9% | Saudi Arabia (NEOM, Red Sea Project), UAE (Operation 300bn), Qatar (National Vision 2030) | Long term (≥ 4 years) |

| E-commerce Arabic-labeling rules driving short-run packaging | +1.2% | UAE, Saudi Arabia (primary); Kuwait, Bahrain (secondary) | Short term (≤ 2 years) |

| Localization of halal-compliant ink supply chains | +0.7% | Saudi Arabia, UAE, Kuwait (halal certification hubs) | Medium term (2-4 years) |

| Adoption of energy-efficient LED-UV presses to meet ESG-linked financing criteria | +0.6% | UAE, Saudi Arabia (green bond issuers); Oman (emerging) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Packaging and Textile Industries and Rising Demand for Digital Advertisements

Food and beverage converters in Riyadh and Dubai are installing HP Indigo 25K and Konica Minolta AccurioLabel 400 units to handle 50,000-label jobs that carry Arabic nutritional panels and halal logos.[1]World Bank, “Gulf Economic Update: Navigating Uncertainty,” WORLDBANK.ORG Saudi non-oil manufacturing output rose 6.2% year-on-year in Q1 2025, and each percentage-point uptick translates into additional short-run demand that analog lines cannot serve profitably. Textile microbrands in Dubai’s Al Quoz district use Epson and Mimaki direct-to-garment printers for 100-piece capsule collections, confirming that smaller-batch economics favor digital workflows. Large-format growth also remains visible, as the NEOM linear city alone is projected to need 2 million m² of branded graphics before 2030, a pipeline that underpins wide-format inkjet sales. Advertising agencies leverage these capabilities to deliver hyper-localized content across outdoor media, retail displays, and event graphics without overstocking inventories.

Rapid Inkjet Adoption for Short-Run and Variable-Data Jobs

Inkjet’s 53.24% share in 2025 reflects converters’ pivot toward LED-UV and latex systems that support variable data, multiple substrates, and quick job changes. Canon’s VarioPRINT iX-3200 at UAE-based Tenaui runs at 320 images per minute, enabling pharmaceutical cartons to be serialized in compliance with Saudi FDA track-and-trace rules. Xerox’s Iridesse adds inline spot varnish, so cosmetics brands cut makeready time by 40% on 500-unit runs. Water scarcity inflates the cost of aqueous inks to the point where UV and latex maintain an 18% operating-cost edge in the UAE.[2]Abu Dhabi Department of Energy, “Water Sustainability and Graphene Research Report,” DOE.GOV.AE Therefore, single-pass inkjet claims corrugated and flexible-film jobs once reserved for flexo, especially when converters retrofit GEW LED-UV lamps that slash power consumption by up to 70%.

Government Diversification Programs Fueling Industrial and Packaging Capacity

Saudi Vision 2030, the UAE’s Operation 300bn, and Qatar National Vision 2030 collectively earmarked USD 120 billion for manufacturing zones between 2021 and 2025, triggering the installation of digital presses within food, beverage, and pharma clusters. Qatar’s Ministry of Public Health issued three new drug-plant licenses in 2024, each demanding GMP-grade serialized packaging runs of only 5,000 units. Oman’s Ladayn Polymer Park opened in 2024 and already hosts eight digital presses serving dairy and snack clients that value 24-hour artwork changes. State-backed off-take agreements shorten payback periods on digital lines to less than four years and shield converters from order-cycle volatility. Those structural incentives ensure machinery vendors book multi-system deals rather than single-press sales.

E-Commerce Arabic-Labeling Rules Driving Short-Run Packaging

The UAE Ministry of Climate Change and Environment decreed in January 2024 that all online food shipments must carry Arabic ingredient lists and halal certification marks, forcing retailers to drop generic multilingual labels.[3]UAE Ministry of Climate Change and Environment, “E-commerce Food Labeling Mandate,” MOCCAE.GOV.AE Saudi Arabia extended similar labeling requirements to personal care products in June 2024. Online platforms such as Noon and Talabat now place label orders averaging 2,500 units, well below analog breakeven, which pushes volume toward HP Indigo and Xeikon presses with sub-USD 0.02 per-label click charges. UAE e-commerce reached USD 8.3 billion in 2024 and grew double digits in 2025, creating a recurring pipeline for variable-data shipping labels. Converters capitalize by offering 48-hour print-to-ship services that integrate directly into retailer ERP platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for presses and R&D | -1.4% | GCC-wide, acute in Bahrain, Oman (smaller converter base) | Short term (≤ 2 years) |

| Limited skilled digital-press workforce | -0.9% | Saudi Arabia, UAE (rapid capacity additions outpace training); Kuwait, Qatar (secondary) | Medium term (2-4 years) |

| Water scarcity pressures on aqueous ink utilization | -0.5% | UAE, Saudi Arabia (desalination-dependent regions) | Long term (≥ 4 years) |

| Post-oil fiscal austerity slowing government-funded signage projects | -0.4% | Saudi Arabia, Kuwait (budget consolidation); Oman (fiscal reform) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Presses and R&D

Entry-level LED-UV units start at USD 500,000, and HP Indigo 25K systems exceed USD 1.2 million, stretching the reach of converters with revenue under USD 5 million. Saudi commercial-loan approval for printing assets slid to 62% in 2024 as banks tightened standards during oil-price swings. Smaller Bahraini and Omani plants often resort to leases priced 8-10% annually, a burden that clips gross margin by 200-300 basis points. Color-server upgrades, such as Ricoh’s USD 40,000 kit for Arabic-script data, stack further on project budgets. Collectively, heavy capex slows fleet renewal cycles and leaves some labels and pouch work on aging analog lines.

Limited Skilled Digital-Press Workforce

Only 15% of GCC press operators hold advanced G7 or ISO 12647 certifications, depressing throughput on high-spec machines. PwC’s 2025 Middle East workforce survey ranks skills gaps third after CNC machining and automation. Enrollment in Saudi and UAE vocational programs rose a modest 4% per year between 2020-2024, while installed press capacity jumped 12%. Wage premiums of 25-35% emerge as converters chase certified operators, pushing payback timelines further out. Vendors answer with automation, yet complex multi-substrate work still requires human color experts, so productivity gains remain capped until the supply of trained color experts improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Process: Inkjet Expands Variable-Data Dominance

Inkjet accounted for 53.24% of the GCC digital printing market share in 2025 and is forecast to advance at a 9.17% CAGR to 2031, widening its revenue gap over electrophotography within the GCC digital printing market size. Brand owners adopt single-pass inkjet lines for serialized labels, QR-coded cartons, and short-run pouches that analog presses cannot serve profitably. Canon’s VarioPRINT iX-3200, now operating at UAE-based Tenaui, outputs 320 images per minute while keeping delamination below 0.1%, proving compliance with Saudi FDA track-and-trace rules. HP Indigo’s 25K platform extends this versatility to flexible films, printing 100 linear meters a minute with instant LED-UV curing and click costs under USD 0.02 per label. Electrophotography retains a niche in monochrome transactional statements, but humidity-driven fuser wear forces 20% more preventive maintenance in Gulf climates, pushing converters toward inkjet for high-coverage graphics.

Inkjet growth accelerates because latex and LED-UV chemistries eliminate the need for primers and reduce energy draw by up to 70% when paired with GEW retrofits. Latex also lowers substrate costs by USD 0.015 per m² on 500,000-label campaigns that dominate food and beverage orders. Electrophotography vendors counter with toner systems such as Xerox Iridesse, adding inline spot varnish that cosmetics brands value for metallic accents, yet run-length economics still tilt to inkjet at quantities below 10,000 sheets. Over the forecast horizon, nearly two-thirds of new press installations announced by Saudi and UAE converters specify inkjet engines, locking in infrastructure that will shape the next cycle of capacity expansions across the GCC digital printing market.

By Packaging Format: Flexible Pouches Lead Trajectory

Labels accounted for 37.23% of the GCC digital printing market in 2025, but flexible packaging is projected to grow at a 9.92% CAGR through 2031, the fastest among all formats in the GCC digital printing market. Dairy, confectionery, and pet-food brands switch to stand-up pouches that require variable Arabic content and halal logos, fueling demand for Domino X630i and HP Indigo 25K presses that skip USD 8,000 plate charges. Corrugated cartons ranked second with a 22% share, lifted by 180 million UAE parcels in 2024 that needed branded outers. The BHS Jetliner single-pass system fulfills these e-commerce orders by die-cutting 5 000 boxes in four hours, slicing lead times from 2 days to the same shift.

Rigid containers and metal cans together captured 15% of the 2025 value and remain constrained by capital-intensive direct-to-shape devices priced above USD 1.8 million. Konica Minolta’s PKG-675i serves niche beverage promotions, yet its thermal profile limits use on thin-wall plastics. Cartons, at 18% share, hold steady in pharma and cosmetics because tamper-evident features and serialized codes align with digital workflows. As converters perfect digital embellishment, cold foiling, tactile varnish, and micro-text security, average order sizes continue to shrink, confirming that format flexibility is now a profit driver rather than a premium-priced option within the GCC digital printing market share landscape.

By End-User Industry: Personal Care Drives Premium Upside

Food and beverage preserved the largest 41.32% slice of GCC digital printing market share in 2025, yet personal care and cosmetics are slated for a 9.54% CAGR to 2031, outpacing every other end-user inside the GCC digital printing market size. Gulf beauty spend hit USD 12 billion in 2024, and Chalhoub Group revealed 38% of shoppers prefer limited-edition Arabic scripts with metallic finishes, a design mix perfectly served by HP ElectroInk and Xerox Clear Dry Ink effects. Saudi dairy giant Almarai validated this trend by launching 12 seasonal flavors in 2025, each with a 2,500-label run produced on HP Indigo 25K machines that embed QR codes for recipe videos. Such SKU fragmentation pushes converters to real-time scheduling systems so presses toggle between flavors without idle changeovers.

Pharmaceutical demand, which accounted for 12% of 2025 revenue, is growing steadily as the Saudi FDA mandates 2D barcodes on every prescription carton by December 2025. Industrial and chemical applications, though accounting for only 6% of value, require durable UV-printed labels to withstand abrasion and solvents, and thus switch more slowly from analog. Indie cosmetics brands in Dubai’s free zones often launch with 500-piece toner runs, proving that digital printing removes entry barriers for micro-entrepreneurs. Across sectors, average run lengths drop below 3,000 units, a structural shift that secures digital presses as the default production route for new product introductions in the GCC digital printing market.

By Ink Type: UV-Cure Chemistries Secure ESG Financing

UV-curable inks held a commanding 46.21% GCC digital printing market share in 2025 and are expected to post a 9.61% CAGR through 2031, reflecting lenders' preference for presses that cut carbon intensity by at least 20% in the GCC digital printing market. LED arrays slash electricity use 55-70%, and UAE banks now bundle 50-basis-point interest rebates with each verified retrofit. Water-based inks sat at 28%, but desalination pushes their operating costs 18% above those of UV alternatives in the UAE, discouraging new adoption. Solvent chemistries at 16% retain relevance in outdoor signage, where weatherability trumps VOC concerns, while latex commands the final 10% owing to primer-free adhesion on uncoated board.

Saudi Arabia’s Public Investment Fund earmarked USD 1 billion for sustainable packaging subsidies, reimbursing 10% of LED-UV capex and accelerating upgrades in Jeddah and Dammam industrial clusters. Siegwerk’s halal-certified UV portfolio, produced locally since 2024, slashes Gulf converter lead times from 8 to 3 weeks and reduces working capital in fast-moving dairy campaigns. Latex technology wins corrugated shelf-ready trays, particularly when converters pair HP’s thermal heads with a water-resistant overprint varnish to meet Qatar humidity testing requirements. As financiers tighten ESG screens and brand owners pursue end-of-line recyclability, UV-cure and latex chemistries are well-positioned to capture incremental volume, entrenching their leadership in the evolving GCC digital printing market.

Geography Analysis

Saudi Arabia accounted for 52.12% of the GCC digital printing market share in 2025, and the country is projected to post an 8.6% CAGR by 2031 as Vision 2030 megaprojects drive continuous packaging and wide-format demand. The Red Sea Project, Qiddiya, and NEOM together require an estimated 2 million m² of branded graphics before 2030, sustaining steady equipment orders for wide-format inkjet suppliers. Private converters offset lower state signage budgets. Saudi Arabia trimmed non-essential graphics outlays by 8% in 2025 by securing multi-year label contracts from rising food and beverage exporters. Al Eqtessad Printing’s six-press HP Indigo deal illustrates how local capacity scales around these packaging corridors. Combined, these factors anchor Saudi Arabia as the core revenue and volume hub in the expanding GCC digital printing market.

The United Arab Emirates generated 28% of 2025 revenue yet will grow quickest at a 9.94% CAGR through 2031, propelled by e-commerce fulfillment hubs and drug-manufacturing free zones. Dubai Internet City hosts 24-hour label facilities that process 2,500-unit minimum orders, and the Flyeralarm–Al Nabooda joint venture adds three Xeikon CX500 lines to feed Noon and Talabat under 48-hour service-level agreements. Abu Dhabi’s Khalifa Industrial Zone received USD 420 million in pharma FDI during 2024 and stipulates GMP-grade serialized cartons, a requirement matched only by high-resolution inkjet or toner presses. Water scarcity raises aqueous-ink costs by 18% over UV alternatives, so LED-UV systems dominate new capital deployments in both Dubai and Abu Dhabi. This mix of regulatory pull and cost push positions the UAE as the fastest-growing node in the GCC digital printing market.

Qatar, Kuwait, Oman, and Bahrain collectively supplied the remaining 20% of 2025 revenue, each leveraging policy niches to accelerate adoption. Qatar National Vision 2030 promotes local drug output, and three new plant licenses issued in 2024 already triggered serialized-packaging tenders best served by short-run digital workflows. Kuwait’s January 2025 halal-ink mandate requires quarterly supplier audits and channels label contracts to converters that hold Siegwerk-certified UV formulations. Oman’s Ladayn Polymer Park offers a 5% corporate tax rate, helping eight newly installed presses chase dairy and snack orders amid rapid artwork change cycles. Bahrain’s Oriental Printing, backed by a USD 10 million 2024 expansion, ships cosmetics and pharma cartons into Saudi Arabia’s Eastern Province in less than 24 hours, beating Dubai lead times.

Competitive Landscape

The vendor field remains moderately fragmented, with the top five equipment suppliers accounting for roughly 45% of installed GCC capacity. Global brands HP, Canon, Xerox, and Konica Minolta compete head-to-head with Durst, Xeikon, Domino, and niche makers such as AstroNova. Regional converters like ePac, Oriental Printing, and Al Nabooda Printing underpin demand by chasing 48-hour turnarounds and Arabic-language prepress services that legacy offset plants cannot match.

Strategic investment activity intensified after February 2026, when HP committed USD 50 million to ePac to seed flexible-packaging plants in Dubai and Riyadh aimed at e-commerce SKUs that average 1,000-pouch runs. Earlier, FIMI purchased Landa Corporation for USD 80 million in September 2025, positioning nanography as a bridge between offset sheet quality and digital economics. Flyeralarm joined Al Nabooda Printing in April 2025 to operate a 24-hour label hub equipped with three Xeikon CX500 engines targeting UAE marketplace sellers. Saudi Printing Company followed in August 2025 with a USD 35 million loan to finance four HP Indigo 25K presses for halal-certified dairy labels.

Competition also pivots on cost-of-ownership levers. AstroNova’s AJ-1300 corrugated line sells at a 30% discount to Canon corrPRESS and booked a dozen Saudi and UAE installations across 2024-2025. ESG-linked loans favor converters that retrofit GEW or Phoseon LED-UV lamps, cutting electricity use by up to 70% and shortening payback periods to eight months. Xerox capitalizes on high-value embellishment; its Iridesse platform adds tactile varnish in one pass and reduces makeready hours by 40% for two leading Dubai cosmetics converters in 2025. Collectively, these maneuvers keep switching costs low for converters, ensure steady consumables revenue for OEMs, and maintain a competitive equilibrium in which no single player can exceed 20% unit share.

GCC Digital Printing Industry Leaders

HP Inc.

Canon Inc.

Xerox Holdings Corporation

Konica Minolta Inc.

Seiko Epson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: HP Inc. invested USD 50 million in ePac Holdings to build flexible-packaging plants in Dubai and Riyadh aimed at 48-hour e-commerce turnaround.

- September 2025: FIMI acquired Landa Corporation for USD 80 million, accelerating nanographic press rollouts in the Gulf.

- August 2025: Saudi Printing Company secured a USD 35 million facility loan from Saudi Research and Media Group to add four HP Indigo 25K presses.

- April 2025: FLYERALARM and Al Nabooda Printing opened a 24-hour label center in Dubai Internet City equipped with three Xeikon CX500 units.

GCC Digital Printing Market Report Scope

The GCC Digital Printing Market Report is Segmented by Printing Process (Electrophotography, and Inkjet), Packaging Format (Labels, Corrugated Packaging, Cartons, Flexible Packaging, Rigid Packaging, Metal Packaging), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Pharmaceuticals, Industrial and Chemical), Ink Type (UV-Curable, Water-Based, Solvent, Latex), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Electrophotography |

| Inkjet |

| Labels |

| Corrugated Packaging |

| Cartons |

| Flexible Packaging |

| Rigid Packaging |

| Metal Packaging |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Industrial and Chemical |

| UV-Curable |

| Water-Based |

| Solvent |

| Latex |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Printing Process | Electrophotography |

| Inkjet | |

| By Packaging Format | Labels |

| Corrugated Packaging | |

| Cartons | |

| Flexible Packaging | |

| Rigid Packaging | |

| Metal Packaging | |

| By End-User Industry | Food and Beverage |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Industrial and Chemical | |

| By Ink Type | UV-Curable |

| Water-Based | |

| Solvent | |

| Latex | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current value of the GCC digital printing market?

It stood at USD 0.89 billion in 2026.

How fast is the market expected to grow through 2031?

The market is projected to register an 8.78% CAGR from 2026 to 2031.

Which printing process leads regional revenue?

Inkjet leads with 53.24% share in 2025, driven by variable-data and packaging jobs.

Why are UV-curable inks gaining share?

LED-UV systems cut energy use up to 70% and help converters qualify for green financing incentives.

Which end-user segment is growing quickest?

Personal care and cosmetics packaging posts the fastest 9.54% CAGR thanks to luxury brand localization.

Which country offers the highest growth opportunity?

The UAE records the leading 9.94% CAGR, propelled by e-commerce fulfillment hubs and pharma free zones.

Page last updated on: