Africa Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

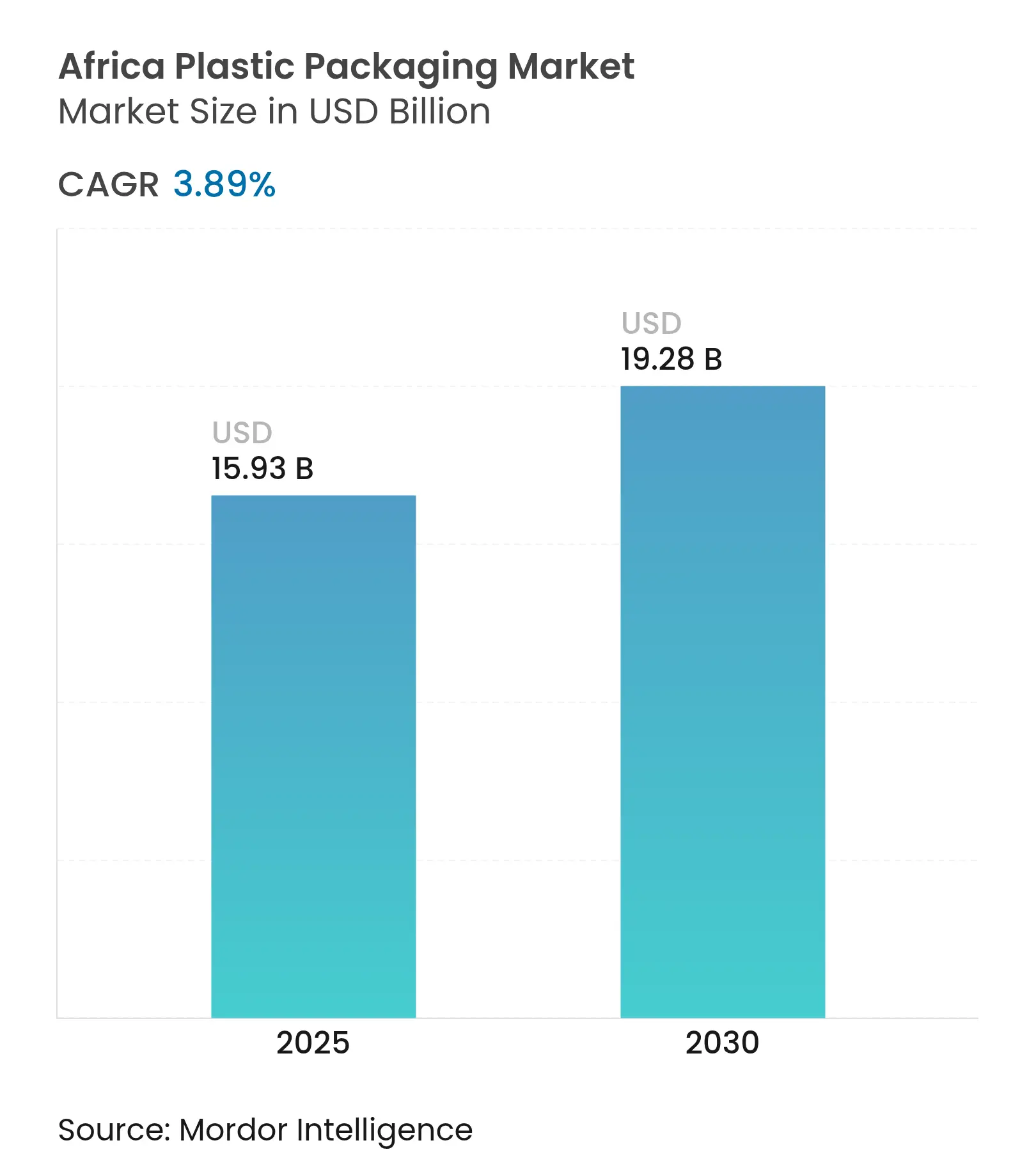

| Market Size (2025) | USD 15.93 Billion |

| Market Size (2030) | USD 19.28 Billion |

| Growth Rate (2025 - 2030) | 3.89 % CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Africa Plastic Packaging Market Analysis by Mordor Intelligence

The Africa plastic packaging market size stands at USD 15.93 billion in 2025 and is projected to reach USD 19.28 billion by 2030, growing at a CAGR of 3.89% during the forecast period. Momentum comes from resilient FMCG demand, expanding beverage bottling capacity, and retail formalization, even as anti-plastic rules accelerate material substitution. Multinationals deepen recycling investments to secure resin supply, while local converters pursue lightweight mono-material formats to lower costs and meet Extended Producer Responsibility (EPR) mandates. However, volatile crude-linked resin prices and chronic power shortages raise conversion costs, pressuring margins for non-integrated players. Businesses that combine circular-economy know-how with reliable energy solutions are positioned to capture outsized gains within the Africa plastic packaging market.

Key Report Takeaways

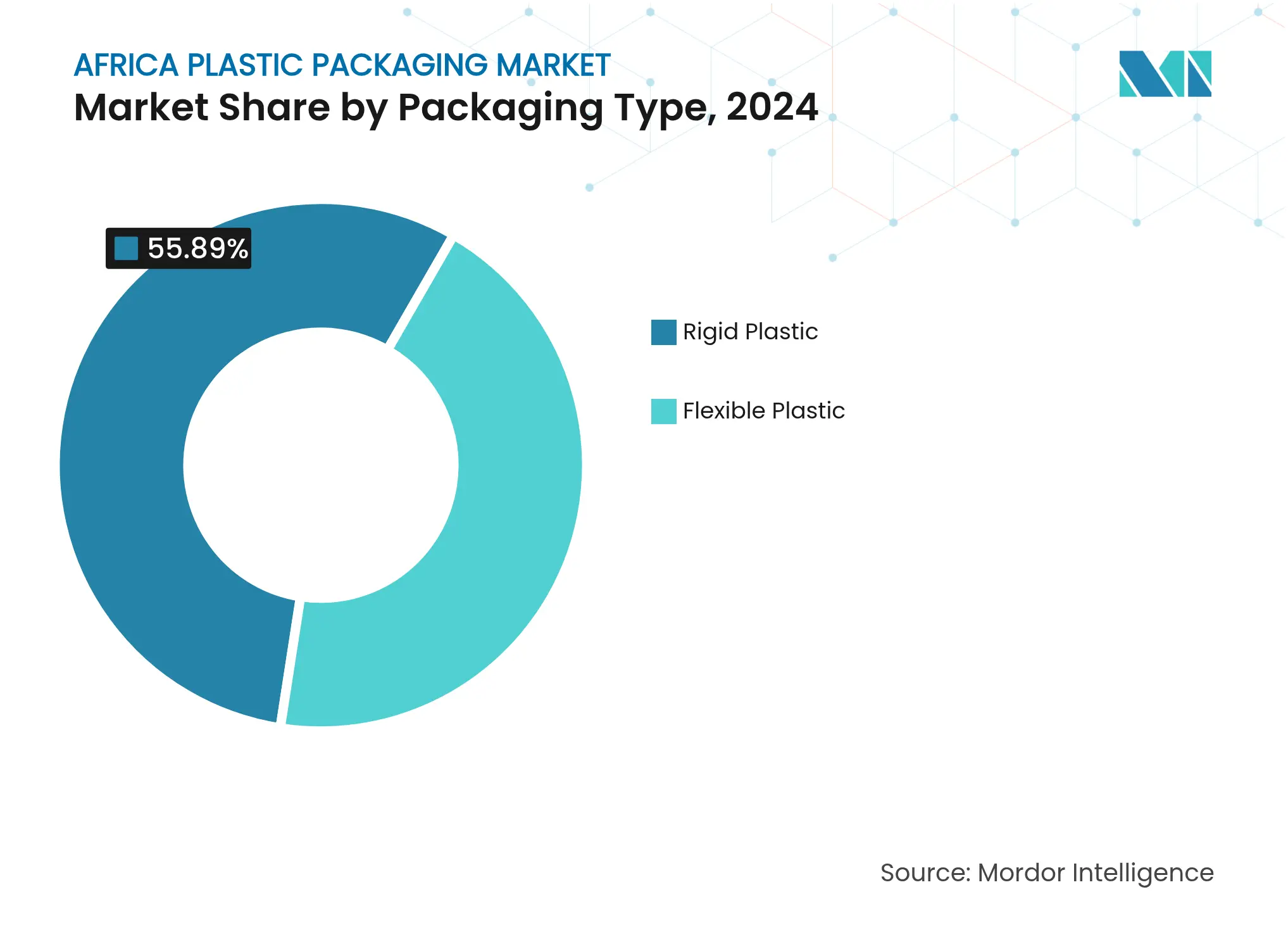

- By packaging type, rigid plastics led with 55.89% of the Africa plastic packaging market share in 2024, whereas flexible solutions are advancing at a 4.21% CAGR through 2030.

- By material, polyethylene variants commanded 33.76% share of the Africa plastic packaging market size in 2024, while EVOH and other barrier plastics are projected to expand at 4.36% CAGR between 2025-2030.

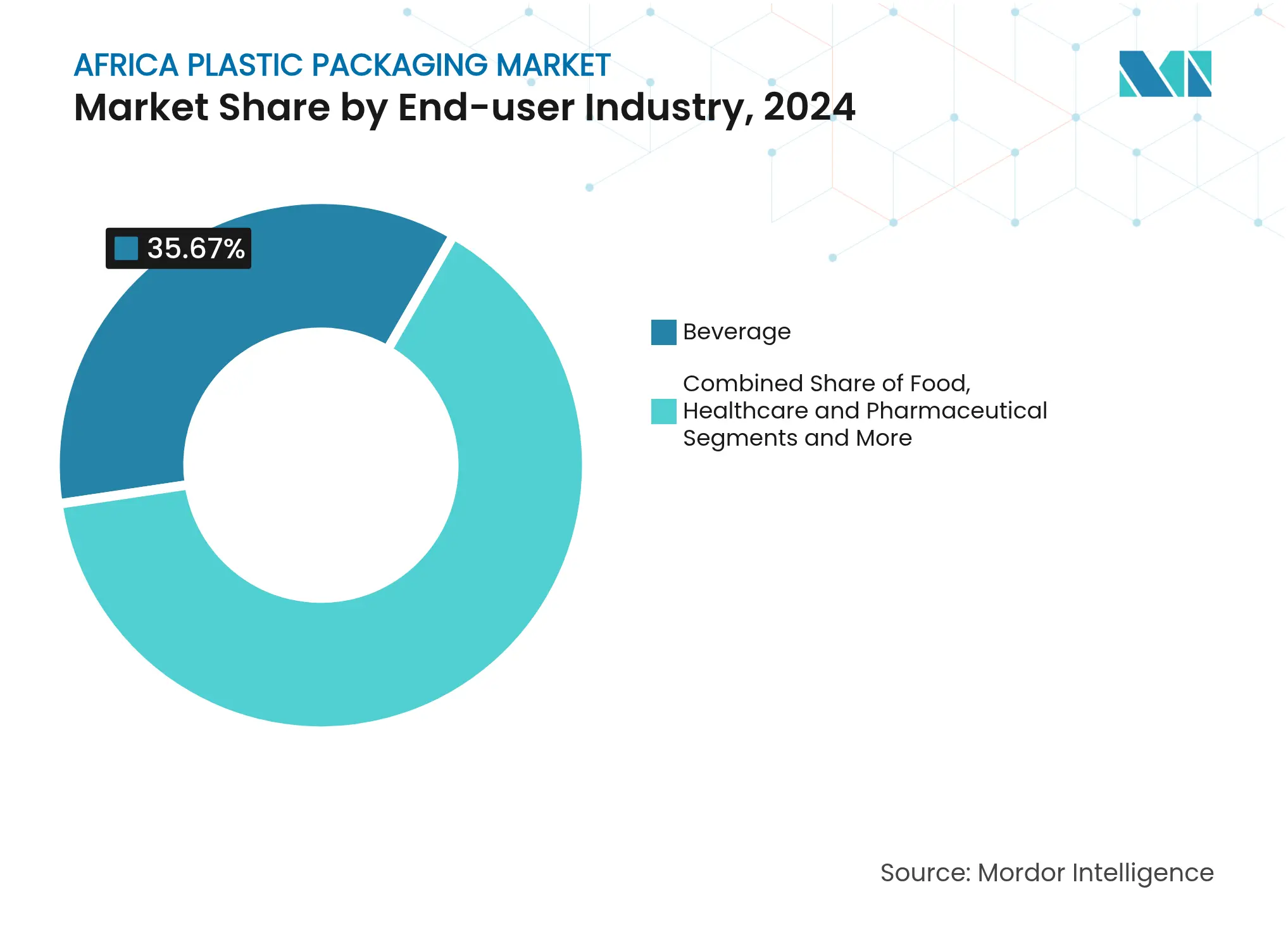

- By end-user industry, beverages accounted for 35.67% revenue in 2024; personal care products are forecast to post the fastest 4.52% CAGR to 2030.

- By pack format, bottles and jars held 29.87% share of the Africa plastic packaging market size in 2024 and pouches are growing at a 4.45% CAGR through 2030.

- By country, Nigeria dominated with 31.53% market share in 2024, while Ghana is on track for the quickest 4.63% CAGR to 2030.

Africa Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for PET beverage bottles Rising demand for PET beverage bottles | +0.8% | Nigeria, South Africa, Kenya, Ghana | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Nigeria, South Africa, Kenya, Ghana | Impact Timeline:Medium term (2-4 years) |

Growth of modern retail and e-commerce packaging Growth of modern retail and e-commerce packaging | +0.6% | Urban centers in Nigeria, South Africa, Egypt, Morocco | Short term (≤ 2 years) | |||

Booming FMCG expansion in West and East Africa Booming FMCG expansion in West and East Africa | +0.7% | Nigeria, Ghana, Kenya, Tanzania, Ethiopia | Long term (≥ 4 years) | |||

Shift to lightweight mono-material solutions Shift to lightweight mono-material solutions | +0.4% | Early adoption in South Africa, Morocco | Medium term (2-4 years) | |||

Government-backed recycling infrastructure roll-outs Government-backed recycling infrastructure roll-outs | +0.3% | Kenya, South Africa, Nigeria, Egypt | Long term (≥ 4 years) | |||

Solar-powered off-grid extrusion projects Solar-powered off-grid extrusion projects | +0.2% | Rural Nigeria, Ghana, Tanzania, Ethiopia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for PET Beverage Bottles

Soft-drink and bottled-water consumption across Africa’s metros is propelling PET usage as brands migrate from glass and metal containers to lighter, resealable options. Coca-Cola’s 2025 Lagos collection hub, able to process 13,000 t of PET annually, underlines the scaling of closed-loop systems that secure recycled feedstock and cut virgin-resin demand. Such hubs concentrate supply near consumption centers, improving logistics efficiency for integrated converters. PET’s favorable cost-to-performance ratio, combined with evolving rPET content mandates, cements its role as a growth engine within the Africa plastic packaging market. Still, localized bottle-grade resin shortages create regional price spreads that reward vertically integrated operators able to balance virgin and recycled inputs.

Growth of Modern Retail and E-commerce Packaging

Organized retail chains and digital marketplaces are replacing informal kiosks, raising requirements for shelf-ready packs that withstand longer supply chains. Investment by LabelVie, Carrefour, and Naivas demonstrates the rapid store-network build-out that demands standardized pack dimensions and superior graphics for brand visibility. E-commerce adds another layer, as protective secondary packaging must safeguard goods through multiple handling points while remaining cost-competitive for price-sensitive shoppers. These converging channels compel converters to adopt quick-change production lines and offer a wide substrate toolbox, solidifying demand for value-added solutions in the Africa plastic packaging market.

Booming FMCG Expansion in West and East Africa

Plastic consumption in West and Central Africa rose from 7.9 million t in 2021 to a projected 12 million t by 2026, spurred by population growth and rising household spend on packaged goods. FMCG outlays touching USD 240 billion underscore consumers’ shift toward branded products, anchoring long-term demand for primary and secondary packaging. Regional multinationals expand local filling capacity to shorten supply chains, creating procurement preference for converters with on-ground technical service and regulatory fluency. The demographic dividend thus reinforces steady volume growth for the Africa plastic packaging market over the next decade.

Shift to Lightweight Mono-material Solutions

Lightweighting trims resin usage and lowers freight emissions, aligning with company net-zero pledges and EPR fee structures [1]Berry Global, “Global Commitment Report on Plastic Packaging,” Ellen MacArthur Foundation, ellenmacarthurfoundation.org. Berry Global cut more than 30,000 t of plastic through design optimization, illustrating cost savings that resonate in Africa’s price-sensitive context. Mono-material laminates simplify recycling streams, helping brand owners in Kenya and South Africa comply with EPR rules that assign collection costs to producers. Successful implementation hinges on advanced polymer blends that preserve barrier and mechanical properties at reduced gauge, offering a competitive edge to converters wielding sophisticated material-science capabilities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile crude-linked resin prices Volatile crude-linked resin prices | -0.9% | Import-dependent markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Import-dependent markets | Impact Timeline:Short term (≤ 2 years) |

Import tariffs on virgin polymers Import tariffs on virgin polymers | -0.5% | Nigeria, Kenya, Egypt, Morocco | Medium term (2-4 years) | |||

Escalating anti-plastic regulations and bans Escalating anti-plastic regulations and bans | -1.2% | Nigeria, Kenya, Uganda, Ethiopia, Egypt | Short term (≤ 2 years) | |||

Power-supply instability inflating conversion costs Power-supply instability inflating conversion costs | -0.7% | Nigeria, Ghana, Tanzania, Ethiopia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Anti-plastic Regulations and Bans

Thirty-six African states have enacted or proposed single-use restrictions, fragmenting compliance requirements for converters. [2]Waruru, Maina, “Africa’s fight against plastic pollution gathers pace,” Down To Earth, downtoearth.org.in Lagos banned styrofoam packs and thin straws in July 2025, while Kenya’s EPR law obliges producers to bankroll take-back schemes. These rapid policy shifts accelerate material innovation but inject planning uncertainty, forcing packaging suppliers to redesign portfolios and absorb higher certification costs. Firms with dedicated regulatory teams and R&D resources are better equipped to adapt, whereas commodity producers face margin compression and potential plant shutdowns.

Power-Supply Instability Inflating Conversion Costs

Intermittent grid electricity compels processors to rely on diesel gensets, lifting production costs by up to 30% in Nigeria and Ghana. Energy-intensive extrusion operations become less competitive against imports from regions with stable utilities. Solar-powered recycling pilots, such as Nigeria’s GIVO Project, illustrate alternatives but demand capital beyond the reach of many SMEs. Integrated players with captive power or renewable installations gain a structural cost advantage, accelerating consolidation within the Africa plastic packaging market.

Segment Analysis

By Packaging Type: Flexible Gains on Sustainability Push

Rigid formats accounted for 55.89% of 2024 revenue, anchored by beverage bottles and personal-care containers, while flexible packaging is set to outpace at 4.21% CAGR through 2030. The Africa plastic packaging market sees flexible substrates attract brands aiming to lessen material tonnage and shipping loads. Modern retail’s centralized distribution favors overwraps and multipacks that extend shelf life without adding bulk. Rigid formats retain strength where stackability and product dispensing are critical, yet innovation in stand-up pouches with high-clarity coatings challenges this dominance. Kenyan and South African EPR levies reward designs that use fewer polymers, nudging converters toward laminates that meet recyclability guidelines. Brands valuing visual impact leverage digital printing on flexible films to run short promotional campaigns cost-effectively, further swelling volume. As government recycling targets tighten, the shift toward flexible packaging is expected to continue reshaping the Africa plastic packaging market.

By Material: Barrier Plastics Accelerate Premiumization

Polyethylene grades held 33.76% share in 2024 thanks to well-established supply chains, yet EVOH and other barrier resins are projected to climb at 4.36% CAGR to 2030. Growth mirrors rising demand for higher shelf-life foods and pharmaceuticals that urban consumers favor. Multilayer structures integrating thin EVOH layers provide oxygen protection without compromising recyclability when paired with compatibilizers. PET maintains momentum in beverages, especially where bottle-to-bottle recycling loops are forming around Lagos and Johannesburg. Polypropylene develops niche strength in retort pouches and flip-top closures, while polystyrene usage wanes under regulatory pressure. Research in Egypt converting recycled PET and PE into high-performance bricks showcases the circular potential of mainstream polymers. The evolving mix underscores a gradual premiumization trend within the Africa plastic packaging market as end-users balance cost, functionality, and compliance.

By End-user Industry: Personal Care Captures Momentum

Beverages led with 35.67% revenue in 2024, yet personal care packaging is anticipated to record the fastest 4.52% CAGR through 2030. Factors include Africa’s expanding middle class and aspirational grooming habits. Cosmetics marketers adopt airless dispensers and opaque barrier tubes to protect formulations, lifting demand for value-added pack features. Food remains a mainstay but faces heightened scrutiny under single-use bans, prompting innovation in reusable and returnable formats. Pharmaceutical uptake is buoyed by regional drug-manufacturing incentives, stimulating demand for sterile barrier films and child-resistant closures. Household chemicals post steady sales as urban infrastructure expands, though slower than consumer verticals. Diversification across these segments mitigates revenue volatility for suppliers in the Africa plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Pack Format: Pouches Lead Value Growth

Bottles and jars retained 29.87% share in 2024, yet pouches and sachets are projected to expand at 4.45% CAGR on the back of cost-effective, portion-size packaging. Rural consumers favor single-serve sachets for affordability, while urban e-commerce channels appreciate the lightweight and tamper-evident nature of doy-packs. Brands integrate easy-open laser scoring and spouts to elevate user convenience. Closure manufacturers respond with recyclable mono-material caps, exemplified by Guala Closures’ South African acquisition that broadens aluminum and crown-cork options. Cups, trays, and tubs sustain demand in QSR and ready-meal markets but must pivot toward compostable or high-recycled-content substrates to retain shelf space. The pack-format race keeps the Africa plastic packaging market dynamic as converters match evolving functional and regulatory demands.

Geography Analysis

Plastic Packaging Market in South Africa

Nigeria dominated the Africa plastic packaging market with 31.53% share in 2024, supported by the continent’s largest consumer base and more than USD 1.5 billion in capital outlay from global beverage leaders. Lagos alone generates up to 14,000 t of daily waste, spurring partnerships between LAWMA and recyclers that edge the city toward a 90% recovery target [3]Akoni, Olasunkanmi, “LAWMA targets 90% of waste generated for recycling,” Nigeria World, nigeriaworld.com. Nonetheless, frequent blackouts inflate diesel costs and complicate capacity planning, inducing larger converters to invest in gas turbines or solar hybrids.

Ghana posted the fastest 4.63% CAGR forecast, propelled by pro-business reforms and the launch of Twellium’s high-speed PET lines capable of 80,000 bph. Government incentives for agro-processing clusters further widen downstream packaging opportunities. South Africa maintains a technology lead with mature EPR legislation that rewards closed-loop initiatives, although economic headwinds slow new capital projects. Egypt leverages Suez trade corridors to attract export-oriented converters, with policymakers framing plastic waste management as both crisis and economic prospect.

Kenya, Tanzania, and Ethiopia round out high-growth corridors. Kenya’s May 2025 EPR rollout shifts compliance costs upstream, steering brands toward converters offering turnkey take-back solutions. Tanzania’s industrial parks woo foreign investors with tax holidays, whereas Ethiopia focuses on import substitution through packaging parks in Dire Dawa. Across regions, success in the Africa plastic packaging market hinges on aligning production footprints with stable power, favorable tariff regimes, and coherent waste policies.

Competitive Landscape

Market Concentration

Top Companies in Africa Plastic Packaging Market

Competition is moderately fragmented, with the top five suppliers controlling roughly half of the Africa plastic packaging market. Berry Global, Nampak, Mondi, Amcor, and ALPLA anchor the tier-one field, leveraging scale, R&D, and recycling infrastructure. Berry Global deepened local roots by partnering with Agile Capital to meet B-BBEE equity thresholds. Amcor’s USD 8.4 billion all-stock merger with Berry Global forms a USD 24 billion packaging giant targeting USD 650 million in annual synergies and broader recyclable film portfolios. Mondi earmarked EUR 1.2 billion (USD 1.39 billion) through 2026 for corrugated and flexible capacity, emphasizing lightweight paper-based alternatives.

Mid-tier players, including Mauser’s newly acquired drum assets in South Africa, chase sector niches in industrial chemicals and bulk containers. ALPLA consolidated its share in North Africa by purchasing partner Taba, underscoring a strategy to control both virgin and recycled resin flows. Regulatory proficiency and circular credentials increasingly determine tender wins with multinational brand owners, favoring companies able to certify ISO 14001 and operate food-grade rPET lines. Smaller converters, challenged by power costs and compliance complexity, face acquisition or exit, accelerating market consolidation within the Africa plastic packaging market.

Africa Plastic Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed an all-stock combination with Berry Global, forging a USD 24 billion consumer and healthcare packaging leader and targeting USD 650 million in annual synergies.

- February 2025: Coca-Cola Nigeria and Nigerian Bottling Company opened a Lagos PET collection hub processing 13,000 t per year to support circular-economy goals.

- January 2025: ALPLA acquired the remaining shares of Taba, consolidating ownership of its North African operations.

- October 2024: Twellium Industrial Company and Sidel inaugurated a packaging hub in Kumasi, Ghana, featuring Africa’s fastest 80,000 bph PET water line.

Table of Contents for Africa Plastic Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand for PET beverage bottles

- 4.2.2Growth of modern retail and e-commerce packaging

- 4.2.3Booming FMCG expansion in West and East Africa

- 4.2.4Shift to lightweight mono-material solutions

- 4.2.5Government-backed recycling infrastructure roll-outs

- 4.2.6Solar-powered off-grid extrusion projects unlocking rural demand

- 4.3Market Restraints

- 4.3.1Volatile crude-linked resin prices

- 4.3.2Import tariffs on virgin polymers in key countries

- 4.3.3Escalating anti-plastic regulations and bans

- 4.3.4Power-supply instability inflating conversion costs

- 4.4Industry Value-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Analysis of Key Emerging Markets in Africa

- 4.8Analysis of Key Raw Material Imports (HS Codes)

- 4.9Porter's Five Forces Analysis

- 4.9.1Bargaining Power of Suppliers

- 4.9.2Bargaining Power of Buyers

- 4.9.3Threat of New Entrants

- 4.9.4Threat of Substitutes

- 4.9.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Packaging Type

- 5.1.1Rigid Plastic

- 5.1.2Flexible Plastic

- 5.2By Material

- 5.2.1Polyethylene (HDPE, LDPE, LLDPE)

- 5.2.2Polyethylene Terephthalate (PET)

- 5.2.3Polypropylene (PP and BOPP/CPP)

- 5.2.4Polystyrene and EPS

- 5.2.5Polyvinyl Chloride (PVC)

- 5.2.6Ethylene-Vinyl Alcohol (EVOH) and Other Barrier Plastics

- 5.3By End-user Industry

- 5.3.1Food

- 5.3.2Beverage

- 5.3.3Healthcare and Pharmaceutical

- 5.3.4Personal Care and Cosmetics

- 5.3.5Household and Industrial Chemicals

- 5.4By Pack Format

- 5.4.1Bottles and Jars

- 5.4.2Caps, Closures and Dispensing Systems

- 5.4.3Pouches and Sachets

- 5.4.4Trays, Cups and Tubs

- 5.4.5Stretch and Shrink Films

- 5.5By Country

- 5.5.1South Africa

- 5.5.2Nigeria

- 5.5.3Egypt

- 5.5.4Kenya

- 5.5.5Morocco

- 5.5.6Ghana

- 5.5.7Ethiopia

- 5.5.8Tanzania

- 5.5.9Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Berry Global Group Inc. (Berry Astrapak)

- 6.4.2Nampak Limited

- 6.4.3Mondi plc

- 6.4.4Mpact Limited

- 6.4.5Foster International Packaging (Pty) Ltd

- 6.4.6Constantia Flexibles Group GmbH

- 6.4.7Tetra Pak International S.A.

- 6.4.8Amcor plc

- 6.4.9Liquibox Corp. (Sealed Air)

- 6.4.10Sonoco Products Company

- 6.4.11Polyoak Packaging (Pty) Ltd

- 6.4.12Huhtamaki Oyj

- 6.4.13ALPLA Werke Alwin Lehner GmbH and Co KG

- 6.4.14Plastipak Holdings, Inc.

- 6.4.15Polyoak Packaging (Pty) Ltd

- 6.4.16Greif, Inc.

- 6.4.17Twellium Industrial Company

- 6.4.18GZ Industries Ltd

- 6.4.19Packaging Industries Ltd (Kenya)

- 6.4.20Future Packaging (Pty) Ltd

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Africa Plastic Packaging Market Report Scope

Plastic packaging is a part of the multi-faceted system for providing products, from the point of manufacture to the point of consumption. Its principal purpose is to guard and ensure the product's safe and secure delivery in its flawless and perfect condition to the end user (manufacturer of product or consumer). Its role in a circular economy is to sustain the value of a product for as long as required and to help remove product waste.

The African plastic packaging market is segmented by rigid plastic packaging (material (polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), other materials), end user (food, beverage, healthcare and pharmaceutical, personal care and cosmetics, other materials)), flexible plastic packaging (material (polyethylene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH), other materials), end user (food, beverages, personal care and cosmetics, other end users)), and country (South Africa, Nigeria, Egypt, Kenya, Morocco, Ghana, Ethiopia, Tanzania, Zambia, Rest of Africa). The report offers market forecasts and size in value (USD) for all the above segments.