GCC Labeling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

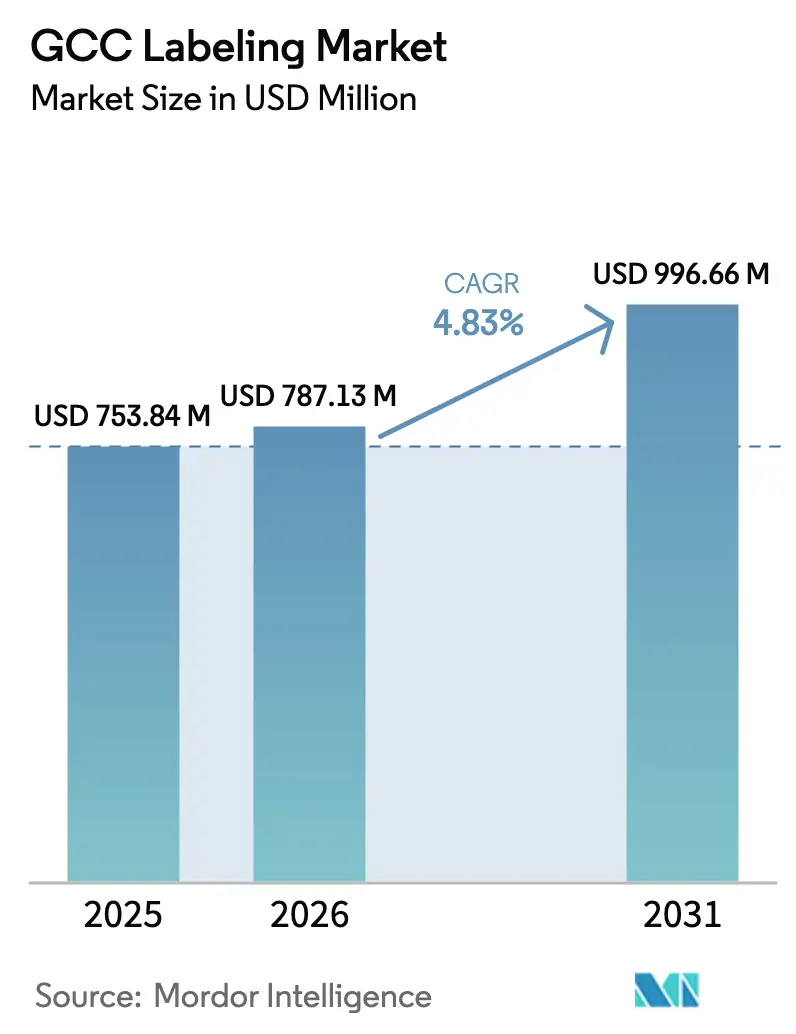

| Base Year Market Size (2025) | USD 753.84 Million |

| Market Size (2026) | USD 787.13 Million |

| Market Size (2031) | USD 996.66 Million |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Labeling Market Analysis by Mordor Intelligence

The GCC labeling market size is expected to grow from USD 753.84 million in 2025 to USD 787.13 million in 2026 and is forecast to reach USD 996.66 million by 2031 at a 4.83% CAGR over 2026-2031. Demand fundamentals remain favorable because consumer packaged goods manufacturers are localizing production, online shopping volumes keep rising, and regional governments are mandating stricter disclosure of nutrition and allergen information. Accelerating e-commerce fulfillment drives soaring demand for variable-data shipping labels, while Saudi Arabia’s Vision 2030 and the UAE’s Operation 300bn channel low-cost capital toward domestic converting capacity. Material selection is also evolving as polypropylene benefits from abundant regional feedstock and mono-material recyclability, yet polyethylene terephthalate films gain share with bottled-water brands that prioritize clarity and circular-economy compliance. Intensifying capital expenditure on digital presses and inspection systems underscores how the competitive frontier is shifting from scale alone to speed, traceability, and smart-packaging readiness. Key tailwinds are balanced by raw-material price volatility, freight surcharges, and the steep investment required for high-speed digital lines that can meet stringent traceability codes. Polypropylene and polyethylene prices spiked in early 2025 after refinery maintenance shut-downs, and logistics disruptions in March 2026 introduced emergency surcharges that reached USD 3,000 per forty-foot container, squeezing converter gross margins for at least two quarters. Smaller converters in Oman, Kuwait, and Bahrain struggle to secure equipment financing because local banks favor real estate over manufacturing, leading to a widening capability gap versus multinationals. At the same time, harmonized Gulf standards on GS1 Digital Link barcodes force brand owners to refresh artwork and serialize every unit, creating first-mover advantages for converters that have installed inline inspection, variable-data engines, and ISO 22000 food-safety systems. These structural pivots suggest that the headline GCC labeling market growth masks deeper shifts in buyer preferences, technology adoption, and supply-chain design that will determine long-run profitability across the converter base.

Key Report Takeaways

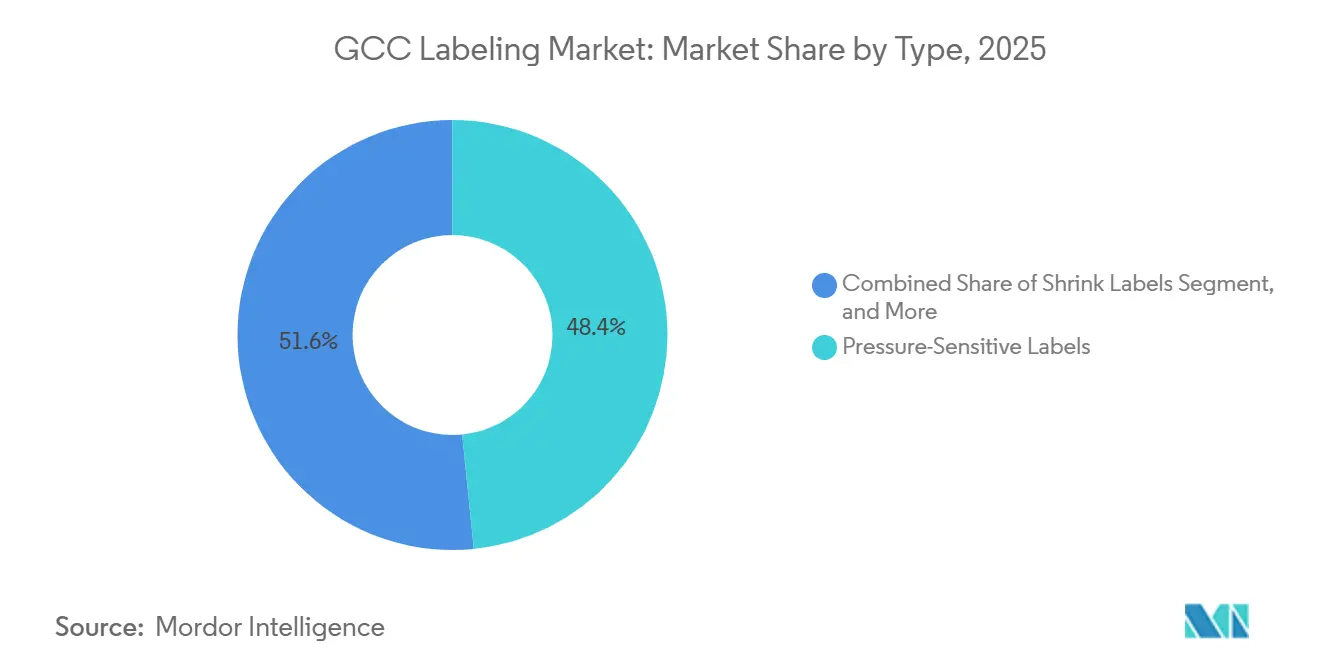

- By label type, pressure-sensitive labels led with 48.43% of GCC labeling market share in 2025, while shrink labels are projected to expand at a 5.63% CAGR through 2031.

- By material, polypropylene films accounted for 37.68% of GCC labeling market size in 2025, and polyethylene terephthalate films are forecast to grow at a 5.71% CAGR through 2031.

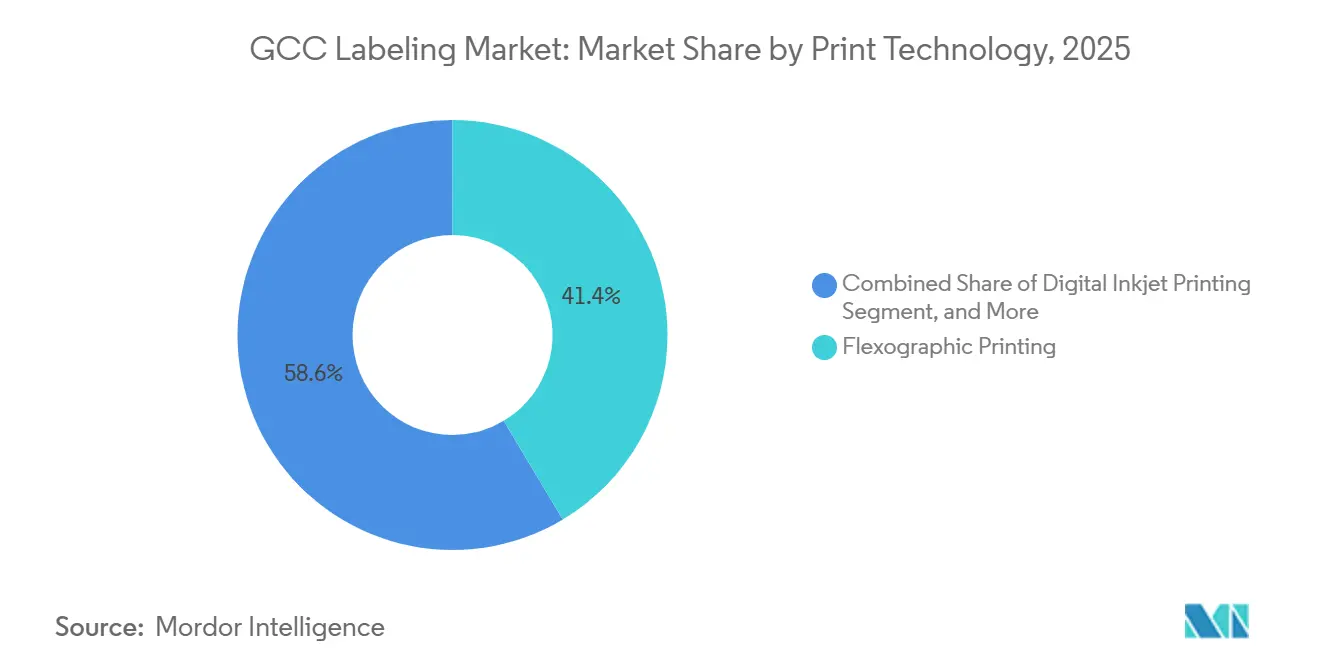

- By print technology, flexography commanded 41.42% revenue in 2025, whereas digital inkjet is expected to advance at a 5.59% CAGR to 2031.

- By end-user, food captured 32.76% share in 2025, and cosmetics and personal care is set to register a 6.18% CAGR through 2031.

- By geography, Saudi Arabia held 38.67% of GCC labeling revenue in 2025, while the United Arab Emirates is projected to log the fastest 6.01% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Labeling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitally-Printed Label Adoption Surges | +1.2% | Saudi Arabia and UAE core, spillover to Qatar and Oman | Medium term (2-4 years) |

| Food-Grade Regulatory Tightening | +0.9% | GCC-wide, led by Saudi SFDA and UAE ESMA | Short term (≤ 2 years) |

| Smart-Packaging and IoT-Enabled Labels | +0.8% | UAE early adoption, Saudi Arabia scaling, Qatar emerging | Long term (≥ 4 years) |

| Localization Push Under GCC Industrial Strategies | +0.7% | Saudi Arabia (Vision 2030), UAE (Operation 300bn), Oman (Vision 2040) | Medium term (2-4 years) |

| E-Commerce Fulfillment Labeling Boom | +0.6% | UAE (logistics hub), Saudi Arabia (consumer base), Kuwait niche | Short term (≤ 2 years) |

| Foreign Direct Investment in FMCG Manufacturing | +0.5% | Saudi Arabia and UAE primary, Qatar selective | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitally-Printed Label Adoption Surges

Converters are accelerating digital press purchases to satisfy variable-data requirements, reduce plate waste, and capitalize on e-commerce that demands on-demand shipping labels.[1]Canon Middle East, “LabelStream 2000 Adoption,” canon-me.com HP Indigo 6K+ installations let mid-sized firms compete for serialized pharmaceutical work, while waste savings protect margins when polypropylene prices swing into double digits. Compliance with GS1 barcodes embeds traceability without manual intervention.[2]GS1 UAE, “Digital Link Standards,” gs1ae.org Canon reported a 30% year-on-year revenue jump from Saudi customers in 2025 after demonstrating its LabelStream 2000 alongside inline finishing modules. HP Indigo 6K+ users in the UAE cut lead times from two weeks to forty-eight hours for limited-edition cosmetics runs, creating tangible brand agility. The combined economic, regulatory, and e-commerce packaging urgency push digital adoption forward by at least 2 years relative to prior forecasts.

Food-Grade Regulatory Tightening

The GSO issued GSO 2810:2025 mandating allergen declarations in Arabic and English, while GSO 2233:2021 standardized nutritional tables, compelling redesign of label real estate. The Saudi Food and Drug Authority further requires GS1-registered barcodes in EAN-13 format on all packaged foods, which increases the character count and forces converters to refine micro-text legibility. UAE ESMA rolled out NutriMark in June 2025, a front-of-pack traffic-light scheme that calls for color-accurate inks and extended gamut printing to ensure consistent red, amber, and green hues. Converters have responded by certifying to ISO 22000 and investing in spectral color measurement to guarantee Delta-E tolerances stay within two units for regulatory colors. Frequent GSO amendment cycles, averaging eighteen months, place a premium on agile press scheduling and short label inventories, which advantages regional suppliers over Asia-based print farms.

Smart-Packaging and IoT-Enabled Labels

GS1 UAE and the UAE Food Cluster launched the Universal Product Catalog in September 2025, pledging to host at least 80,000 product entries and cut listing lead times by 60%. The platform standardizes GS1 Digital Link QR codes, letting shoppers verify authenticity, trace allergen alerts, and access carbon footprint data with one scan. Saudi Arabia’s USD 65 billion hospital expansion simultaneously stimulates serialized pharmaceutical labels that log temperature excursions in real time, aligning with Good Distribution Practice requirements. Cosmetics and infant-formula brands increasingly embed NFC chips within shrink sleeves to deter counterfeits, and initial pilots report a 15% lift in consumer engagement rates once interactive serial codes are active. As national regulators prioritize anti-counterfeiting, converters that integrate RFID inlays and infrared-readable inks gain defensible competitive positions in premium segments.

Localization Push Under GCC Industrial Strategies

Saudi Vision 2030, the UAE’s Operation 300bn, and Oman Vision 2040 accelerate joint ventures and on-shore manufacturing to reduce dependence on imports and raise non-oil GDP. Brady Corporation opened a Dammam facility in March 2025, cutting delivery times to Gulf customers from weeks to twenty-four hours and avoiding pandemic-style ocean delays. Sidel signed a Saudi localization agreement in May 2025 to assemble blow-molders and filling lines domestically, ensuring converters gain immediate machine-service support. Public Investment Fund spending hit USD 36.2 billion in 2025, up 81% year on year, signaling ample liquidity for equipment finance across packaging value chains. Local-content quotas embedded in government procurement shift label sourcing toward homegrown plants, spurring capacity expansions in Riyadh, Jeddah, and Abu Dhabi.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital Intensity of High-Speed Lines | -0.6% | GCC-wide, acute in smaller emirates and Oman | Short term (≤ 2 years) |

| Volatile Petrochemical-Based Raw Material Prices | -0.5% | Saudi Arabia and UAE (polymer hubs), ripple to Qatar and Kuwait | Short term (≤ 2 years) |

| Skills Gap in Digital Pre-Press Operations | -0.3% | Saudi Arabia and UAE labor markets, Oman emerging | Medium term (2-4 years) |

| Fragmented Regulatory Barcode Standards | -0.2% | Cross-border GCC trade, customs alignment lag | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital Intensity of High-Speed Lines

A modern narrow-web flexographic press with six colors costs USD 73,707 for equipment alone, yet converters must also budget for chill rolls, corona treaters, and inspection units, lifting total outlay toward USD 400,000. A digital HP Indigo 6K+ demands climate-controlled rooms, reinforced floors, and trained operators, often pushing project cash needs above USD 1 million, while vendors require 30% down payments. Equipment leasing in the GCC is nascent, and banks apply collateral haircuts as high as 50%, preferring working-capital facilities for trading firms rather than long-tenor asset finance. Rapid technology cycles further erode investment confidence, because presses purchased in 2022 can lack inline embellishment or digital-link encoding demanded in 2026 tenders. These barriers lock out smaller Kuwaiti or Bahraini converters, tilt awards toward multinationals, and slow the GCC labeling market capacity ramp despite healthy end-use demand.

Volatile Petrochemical-Based Raw Material Prices

Polypropylene, polyethylene, and polyethylene terephthalate account for 60-70% of label cost stacks, and they track Brent crude, regional outages, and Asian import parity. February 2025 saw SAR 15 per tonne surges in Saudi polypropylene and SAR 38 per tonne in polyethylene after a shutdown at Yanbu, slicing converter gross margins by up to 300 basis points. UAE suppliers followed by adding USD 40-60 per tonne on polypropylene during contract reseatings, while converters struggled with thirty-day pass-through lags on fixed-price customer agreements. March 2026 geopolitical tensions triggered USD 3,000 emergency surcharges per forty-foot container out of Jebel Ali, delaying inbound PET pellets two weeks and forcing high-value label jobs to move to less efficient air freight.[3]Maersk, “Logistics Surcharge Notice,” maersk.com Absent liquid futures markets for GCC polymers, converters hedge only via inventory, tying up working capital and throttling reinvestment in growth segments such as shrink sleeves and RFID tags.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrink Sleeves Accelerate on Tamper-Evidence and 360-Degree Graphics

Pressure-sensitive labels commanded 48.43% of GCC labeling market revenue in 2025 because most narrow-web presses in the region are optimized for roll-fed adhesive stocks and legacy die sets. Beverage and personal-care brands, however, increasingly specify shrink sleeves because they deliver full-body graphics, neck tamper bands, and moisture resistance needed for chilled supply chains. Shrink sleeves are projected to grow at a 5.63% CAGR to 2031, lifted by energy drinks, premium water, and deodorant cans that pay 15-20% premiums over pressure-sensitive constructions. Taghleef Industries launched SHAPE360 TDSW floatable white polyolefin film in May 2025, allowing sleeves to separate in PET bottle recycling float-sink tanks and easing brand compliance with European import standards. Converters installing steam tunnels and hot-air ovens for shrink application incur capital costs of USD 50,000-150,000 but unlock higher margins and entry into export-oriented beverage programs.

Other labeling formats continue to occupy focused niches within the GCC labeling market. Wrap-around film labels remain prevalent on high-speed bottled-water lines operating above 600 bottles per minute, because adhesive application can withstand condensation without label lift. Glue-applied and cut-and-stack paper labels survive in industrial oils and bulk chemicals where aesthetics matter less than solvent resistance, and in-mold labels are gaining ground in yogurt and margarine tubs where mono-material polypropylene supports recycling targets. Brand owners also experiment with hybrid constructions, embedding RFID inlays within shrink sleeves or pressure-sensitives to improve supply-chain visibility, particularly for premium cosmetics and infant nutrition jars. The product-type mix therefore tilts toward innovation-laden films, even as mature adhesive labels hold share on entrenched capital bases across scores of small Saudi and UAE converters.

By Material: PET Films Climb While Polypropylene Retains Cost Leadership

Polypropylene films represented 37.68% of GCC labeling market size in 2025, sustained by SABIC and Borouge feedstock integration that assures resin security at competitive prices. The material’s stiffness, hot-melt adhesive compatibility, and mono-material recycling with polypropylene tubs help retailers meet extended producer-responsibility goals emerging in Saudi Arabia and the UAE. Polyethylene terephthalate films, however, are forecast to outpace the average market at a 5.71% CAGR through 2031 because bottled-water and juice brands want crystal-clear, scuff-resistant sleeves that survive ice-bucket service without delamination. UPM Adhesive Materials, rebranded in June 2025, unveiled PCR-based polypropylene film grades co-developed with SABIC, giving converters a premium substrate that meets EU food-contact migration limits while keeping supply chains Gulf-centric. Polyethylene films cover squeezable sauces and shampoos thanks to low-temperature flexibility, yet price competitiveness and reduced opacity constrain their share growth relative to polypropylene.

Niche substrates also contribute to the GCC labeling market portfolio by serving design-heavy segments. Metallized PET delivers mirror-like effects on energy drinks and hair-care bottles, lenticular sheets enable motion graphics for seasonal promotions, and direct-thermal paper dominates low-duration logistics labels where heat-sensitive coatings negate ribbon needs. GCC Standardization Organization migration limits, specifically GSO 2700:2022, require every film batch to include certificates of conformity, prompting converters to qualify multiple suppliers to mitigate price and lead-time risk. With resin volatility and sustainability mandates converging, forward-thinking converters are trialing mono-material laminates and solvent-free adhesives that simplify recycling without sacrificing shelf appeal, ensuring material choice becomes a competitive lever, not merely a cost variable.

By Print Technology: Digital Inkjet Expands as Serialization Deadlines Near

Flexographic printing retained 41.42% share in 2025 because its low unit costs on runs beyond 10,000 linear meters keep it indispensable for mass-volume dairy, bakery, and bottled-water labels. Nevertheless, digital inkjet is projected to grow at a 5.59% CAGR through 2031, reflecting mandates for unique item identifiers, late-stage differentiation, and rapid artwork changes in a social-media-driven product cycle. Canon’s LabelStream 2000, launched regionally in early 2025, prints six colors plus opaque white at up to 75 meters per minute and adds inline varnish, enabling converters to deliver embellishments once limited to screen printing. HP Indigo 6K+ units already running in Dubai have reduced make-ready waste from 8% to under 2%, saving substrates worth thousands of dollars each month when polypropylene contracts hover above USD 1,200 per tonne. Offset and gravure lines persist for mega-runs exceeding a million impressions, yet they now integrate hybrid inkjet bars to add serialized data, indicating that pure analog platforms are approaching obsolescence in the region.

Screen printing maintains relevance for chemical drums and automotive parts that demand thick ink layers for abrasion and solvent resistance. Converters also deploy rotary screen modules inline with flexo or digital to apply tactile varnishes and Braille dots on pharmaceutical labels. As labor shortages in pre-press widen, Gulf Print & Pack exhibitors in 2025 highlighted workflow automation that cuts file preparation times by half, helping converters handle frequent design changes without hiring scarce color-management experts. The interplay of print-quality expectations, serialization regulations, and capex funding access will determine the speed at which digital surpasses 25% share of the GCC labeling market by value within the next decade.

By End-User Industry: Cosmetics and Personal Care Race Ahead of Food Staples

Food applications generated 32.76% of GCC labeling revenue in 2025 as bakery, dairy, and snack brands reformulated packaging to comply with allergen declarations and nutritional front-of-pack icons. Converters servicing multinational food plants in Jeddah and Dubai must now manage bilingual text, extended ingredient lists, and GS1 barcodes that link to traceability databases, increasing color separations and plate counts on flexo jobs. Cosmetics and personal care labels are forecast to expand at a 6.18% CAGR through 2031, reflecting Saudi Arabia’s USD 5.95 billion beauty market and a consumer shift toward premium imported brands produced locally for tariff relief and freshness. Embossed metallic films, cold foils, and UV-raised varnishes differentiate perfumes, serums, and high-luminance lipsticks, commanding margins 25-30% above mass-market food labels and incentivizing converters to allocate press time to beauty SKUs. Beverage labels, although classified under food, have distinct technical demands such as condensation resistance, warp-free application, and passthrough of bottle-neck sleeving machinery at 60,000 units per hour on mega water plants.

Healthcare and pharmaceutical labeling gains momentum alongside Saudi Arabia’s USD 65 billion hospital build-out, driving demand for tamper-evident seals, temperature-monitoring indicators, and serialized barcodes that comply with the Drug Track and Trace system. Industrial chemicals, lubricants, and agrochemicals sustain orders for durable polyethylene and polypropylene labels that resist UV fading and solvent exposure, often printed with screen and UV-flexo inks. Smaller niches such as consumer electronics and auto aftermarket parts specify high-performance polyimide and polyester materials with heat tolerance beyond 300 °C for under-hood or motherboard placement. Collectively, these dynamics nudge the GCC labeling market mix toward higher added-value applications, prompting converters to diversify into embellishment, smart-label encoding, and cross-border logistics to pursue resilient margin pools.

Geography Analysis

Saudi Arabia generated 38.67% of GCC labeling revenue in 2025, leveraging the Kingdom’s USD 11-12 billion packaging market and public incentives that reward local content on consumer goods. Unilever, for example, installed a new OMO detergent line in January 2026 and deodorant aerosol lines in September 2025, cementing label supply contracts with converters in Jeddah industrial city. Vision 2030 continues to unlock low-interest loans, customs duty rebates, and land grants, allowing converters to expand plants in Riyadh’s Sudair and Yanbu’s industrial zones. The Saudi Food and Drug Authority enforces barcodes and ISO 22000 audits, ensuring that only converters with robust quality systems capture long-term food and pharma work. While polypropylene and polyethylene price swings weigh on margins, Saudi converters offset volatility through resin supply agreements with SABIC that smooth quarterly cost curves and underpin competitive bids across the wider GCC labeling market.

The United Arab Emirates is projected to grow labeling revenue at a 6.01% CAGR through 2031, buoyed by the Universal Product Catalog that standardizes 2D barcodes across 80,000 SKUs and accelerates smart-packaging adoption. Jebel Ali Free Zone attracts multinational FMCG fillers, and Solico Group’s USD 35.4 million expansion in January 2026 broadens demand for food-grade adhesive films. DHL’s USD 570 million fulfillment investment, announced in November 2025, multiplies the volume of variable-data shipping labels processed each day through Dubai’s logistics corridors, giving digital-press converters steady mid-volume runs. Huhtamaki’s consolidation of UAE sites illustrates confidence in the Emirati ecosystem, yet also raises competitive pressure on smaller players that lack multinational backing. Rapid labor-force multiculturalism supports a skilled pre-press talent pool, providing operational resilience that neighboring states sometimes lack.

Qatar, Oman, Kuwait, and Bahrain collectively contribute a smaller revenue share but represent strategic plays for converters willing to specialize. Qatar’s petrochemical clusters demand industrial tags, valve labels, and hydrocarbon-resistant films, while its FIFA legacy stadium refresh cycles depend on safety signage and RFID-embedded maintenance labels. Oman’s Vision 2040 diversification plan stimulates agri-food and pharma projects near Sohar and Salalah, driving label orders that reward fast turnaround and bilingual compliance documentation. Kuwait’s high disposable-income consumer base fuels niche cosmetics imports that need limited-edition embellishment, although small domestic converter footprints require cross-border supply from Saudi or UAE plants. Bahrain, hosting a growing fintech hub, harbors limited FMCG filling capacity but imports branded beverages that still need regional language compliance, sustaining a baseline for on-demand converters able to ship within forty-eight hours. Collectively, the smaller Gulf states create a mosaic of opportunity whose risk-adjusted attractiveness hinges on trade-route agility, customs harmonization, and scale economics.

Competitive Landscape

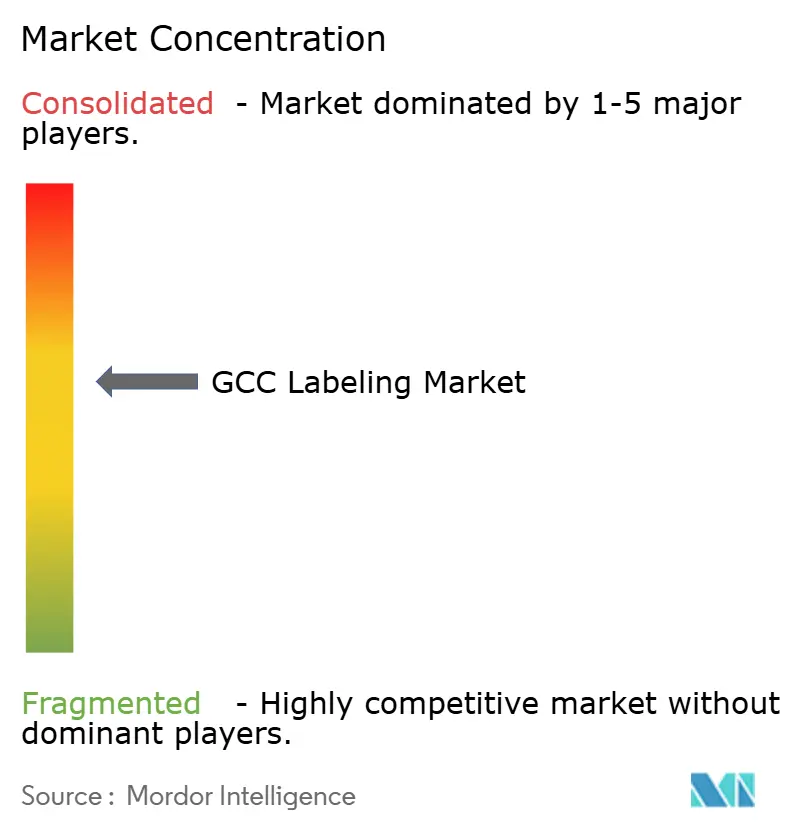

The GCC labeling industry exhibits moderate concentration, with the playerslike CCL Industries, Avery Dennison, Mondi, 3M, and others. CCL Industries closed a USD 143 million buy-out of its Middle East joint venture in June 2024, then reported double-digit organic growth during Q4 2025 as it leveraged global resin contracts and unveiled RFID-ready pressure-sensitives for pharmaceuticals. Avery Dennison extended its Intelligent Labels program into Dubai Logistics City late in 2025, embedding NFC and near-field sensors within pressure-sensitive constructions that help retailers monitor cold-chain breaches in dairy and ready meals. Mondi applied nano-embossing to vacuum-pack label films at its Abu Dhabi innovation center, giving meat processors tamper-evident seals that delaminate if punctured, a feature already commercialized at two Saudi poultry plants.

Regional specialists compete through proximity, agility, and willingness to run sub-5,000-meter jobs that multinationals often decline. Sigma Middle East Label Industries operates flexo and hybrid digital presses in Ras Al Khaimah and Doha, shipping same-day to Bahrain beauty brands that need emergency replenishment. Print Pack Labels in Jeddah gained halal cosmetics accounts by adding Arabic calligraphy embellishment modules and now pilots an inline digital cold-foil unit to capture premium fragrance SKUs. Rotopack Labeling Solutions forged a March 2025 distribution pact with Rotocon to supply Ecoline and Chrome narrow-web converting equipment, shortening lead times on spare parts for Omani converters that previously flew components in from Europe. Equipment manufacturers also engage in vertical integration; Brady Corporation’s Dammam plant assembles die-cut safety signs and serialized asset tags, effectively competing with its own converter customers in certain niches yet raising overall GCC labeling market standards on delivery speed.

Competitive dynamics increasingly pivot on digital fleet scale, resin-procurement leverage, and data-management capability rather than raw printing capacity alone. Multinationals leverage hedging programs to lock polymer prices six months forward, cushioning shocks that cripple thin-capitalized local shops. They also operate regional color labs that pre-approve PMS codes, saving press-approval trips and slashing time-to-market for brand extensions. Conversely, regional champions counterbalance with round-the-clock customer service, drop-in plate changes, and Arabic copy review teams that catch regulatory errors before print, rescuing clients from SFDA recalls. As Vision 2030 and Operation 300bn disburse more soft loans, mid-tier Gulf converters may yet scale through press upgrades, but consolidation looms because digital capex and raw-material volatility reward those with balance-sheet depth and cross-border sales teams.

GCC Labeling Industry Leaders

CCL Industries Inc.

Mondi Group

3M Company

Huhtamaki OYJ

Taghleef Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unilever launched a new OMO Liquid detergent line in Saudi Arabia, expanding local label demand and emphasizing Vision 2030 content thresholds.

- January 2026: Solico Group invested USD 35.4 million in a Jafza food production hub, adding 5,000 square meters and raising daily capacity by 40 tonnes.

- September 2025: Taghleef Industries debuted an easy-peel in-mold label film targeting yogurt, cheese, and premium personal-care tubs.

- September 2025: Unilever opened new deodorant production lines in Jeddah, capable of 30 million aerosol units per year.

GCC Labeling Market Report Scope

Labeling encompasses creating and applying labels on a product's outer packaging. They convey vital information and product features.

The GCC Labeling Market Report is Segmented by Type (Pressure-Sensitive Labels, Shrink Labels, In-Mold Labels, Wrap-Around Labels, and Other Types), Material (Paper, Polypropylene, Polyethylene, Polyethylene-Terephthalate, and Other Materials), Print Technology (Flexographic Printing, Offset Printing, Gravure Printing, Digital Inkjet Printing, and Screen Printing), End-User Industry (Food, Beverage, Healthcare and Pharmaceutical, Cosmetics and Personal Care, Chemicals and Industrial, and Other End-user Industries), and Country (United Arab Emirates, Saudi Arabia, Qatar, and Rest of GCC). The Market Forecasts are Provided in Terms of Value (USD).

| Pressure-Sensitive Labels |

| Shrink Labels |

| In-Mold Labels |

| Wrap-Around Labels |

| Other Types |

| Paper |

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene-Terephthalate (PET) |

| Other Materials |

| Flexographic Printing |

| Offset Printing |

| Gravure Printing |

| Digital Inkjet Printing |

| Screen Printing |

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Cosmetics and Personal Care |

| Chemicals and Industrial |

| Other End-user Industries |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Rest of GCC |

| By Type | Pressure-Sensitive Labels |

| Shrink Labels | |

| In-Mold Labels | |

| Wrap-Around Labels | |

| Other Types | |

| By Material | Paper |

| Polypropylene (PP) | |

| Polyethylene (PE) | |

| Polyethylene-Terephthalate (PET) | |

| Other Materials | |

| By Print Technology | Flexographic Printing |

| Offset Printing | |

| Gravure Printing | |

| Digital Inkjet Printing | |

| Screen Printing | |

| By End-User Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Cosmetics and Personal Care | |

| Chemicals and Industrial | |

| Other End-user Industries | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of GCC |

Key Questions Answered in the Report

What is the projected value of the GCC labeling market by 2031?

It is forecast to reach USD 996.66 million in 2031, up from USD 753.84 million in 2025.

Which label type is expanding fastest in the Gulf?

Shrink sleeves are on track for a 5.63% CAGR, propelled by tamper-evidence and 360-degree graphics.

Why are PET films gaining traction over polypropylene?

PET offers superior clarity and cold-chain durability, supporting bottled-water brands that target closed-loop recycling goals.

How do digital presses benefit converters?

They eliminate plate costs, shorten lead times to forty-eight hours, and embed GS1-compliant serial codes on every label.

Which Gulf country will grow labeling demand most quickly?

The United Arab Emirates, supported by smart-packaging mandates and e-commerce penetration approaching 60%.

What challenges hinder small converters from upgrading equipment?

High capital costs, limited leasing options, and rapid tech obsolescence deter investment in state-of-the-art digital lines.

Page last updated on: