Microprinting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

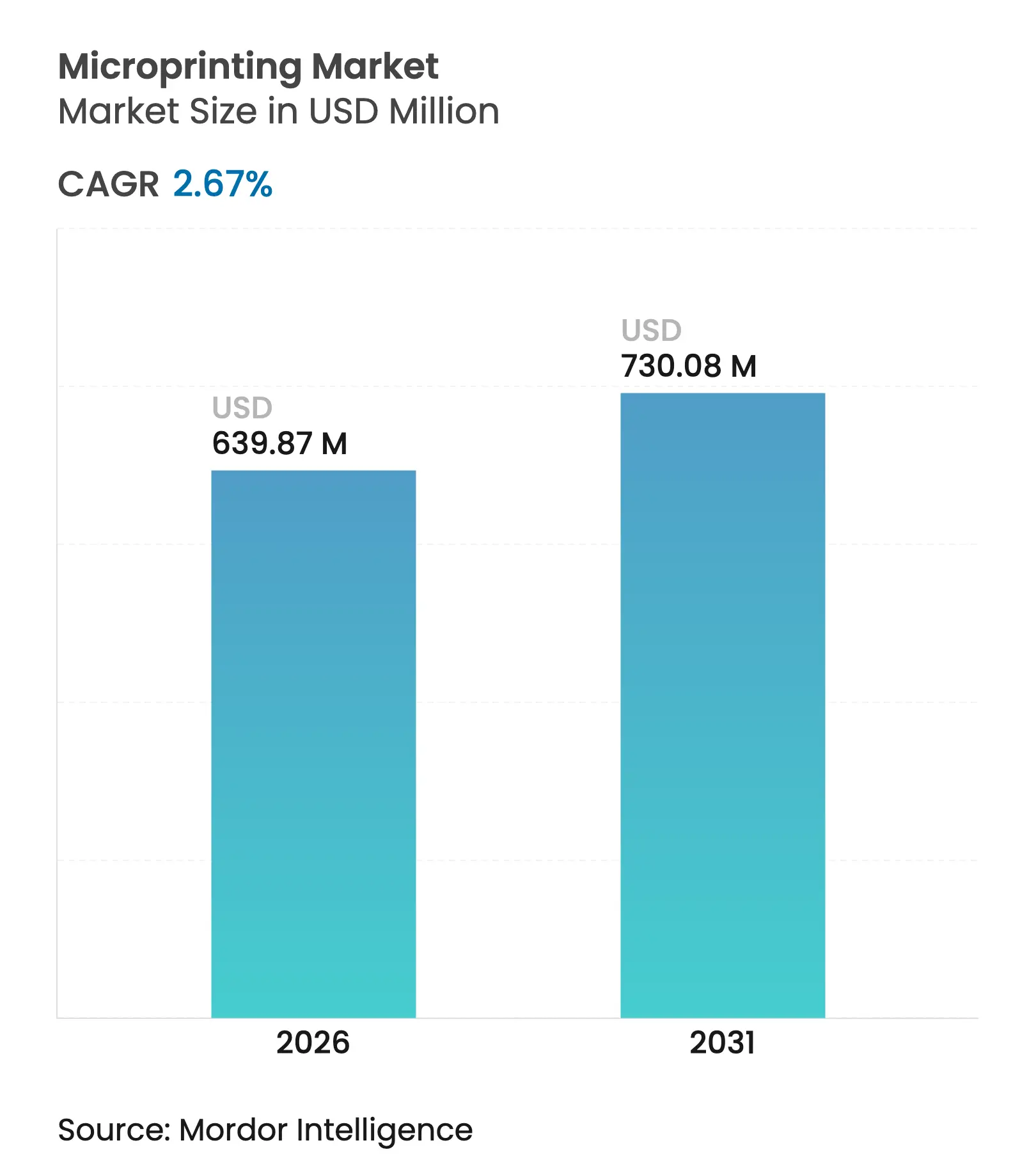

| Market Size (2026) | USD 639.87 Million |

| Market Size (2031) | USD 730.08 Million |

| Growth Rate (2026 - 2031) | 2.67 % CAGR |

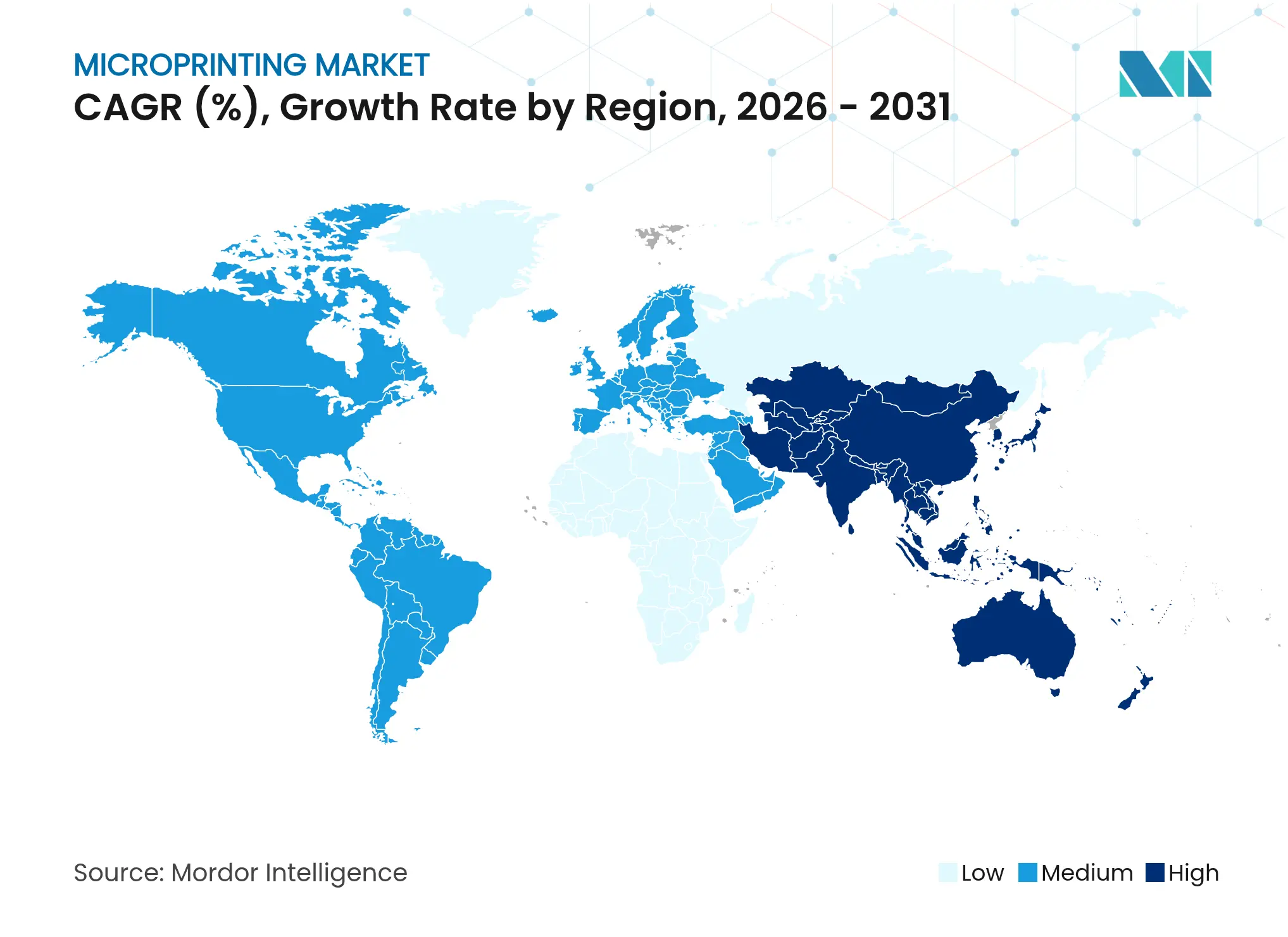

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Microprinting Market Analysis by Mordor Intelligence

Microprinting market size in 2026 is estimated at USD 639.87 million, growing from 2025 value of USD 623.24 million with 2031 projections showing USD 730.08 million, growing at 2.67% CAGR over 2026-2031. Heightened regulatory focus on document security in banking, pharmaceuticals, and government identification keeps demand resilient even as digital transactions grow. Expansion continues as nanoparticle-enhanced inks, blockchain-linked authentication, and high-resolution modular presses unlock fresh revenue opportunities. Environmental mandates are reshaping ink chemistry, yet compliance investments are balanced by stronger customer preference for tamper-proof packaging and identity credentials. Competitive intensity rises as traditional press suppliers partner with or acquire security-technology firms to deepen portfolios while specialized vendors push 1,200 dpi hybrid engines that cut change-over times and enable variable data printing at scale.

Key Report Takeaways

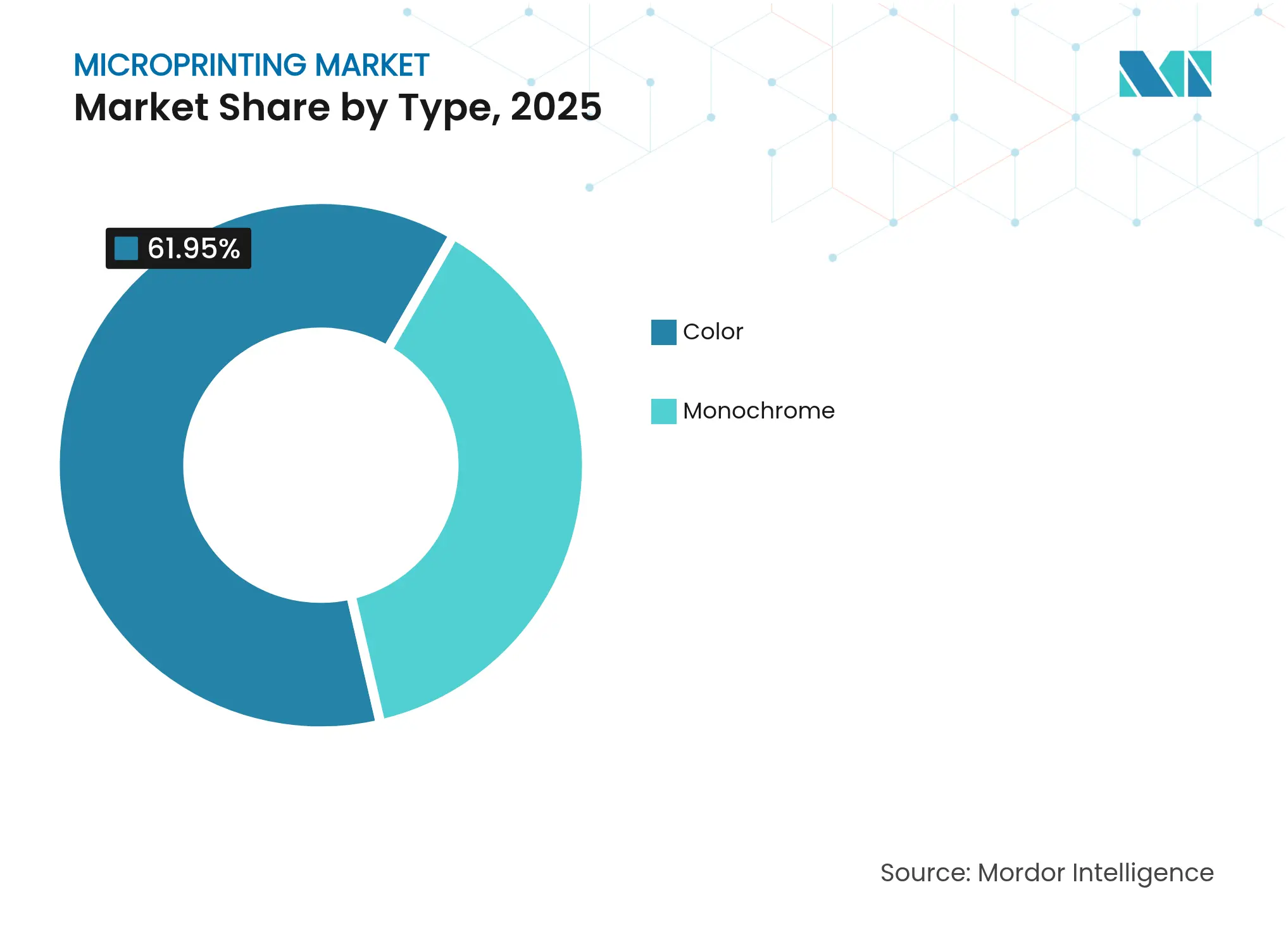

- By type, color microprinting led with 61.95% revenue share in 2025; monochrome is projected to expand at a 4.05% CAGR through 2031.

- By print type, single-sided held 54.35% of the microprinting market share in 2025, whereas double-sided systems are forecast to post a 3.28% CAGR by 2031.

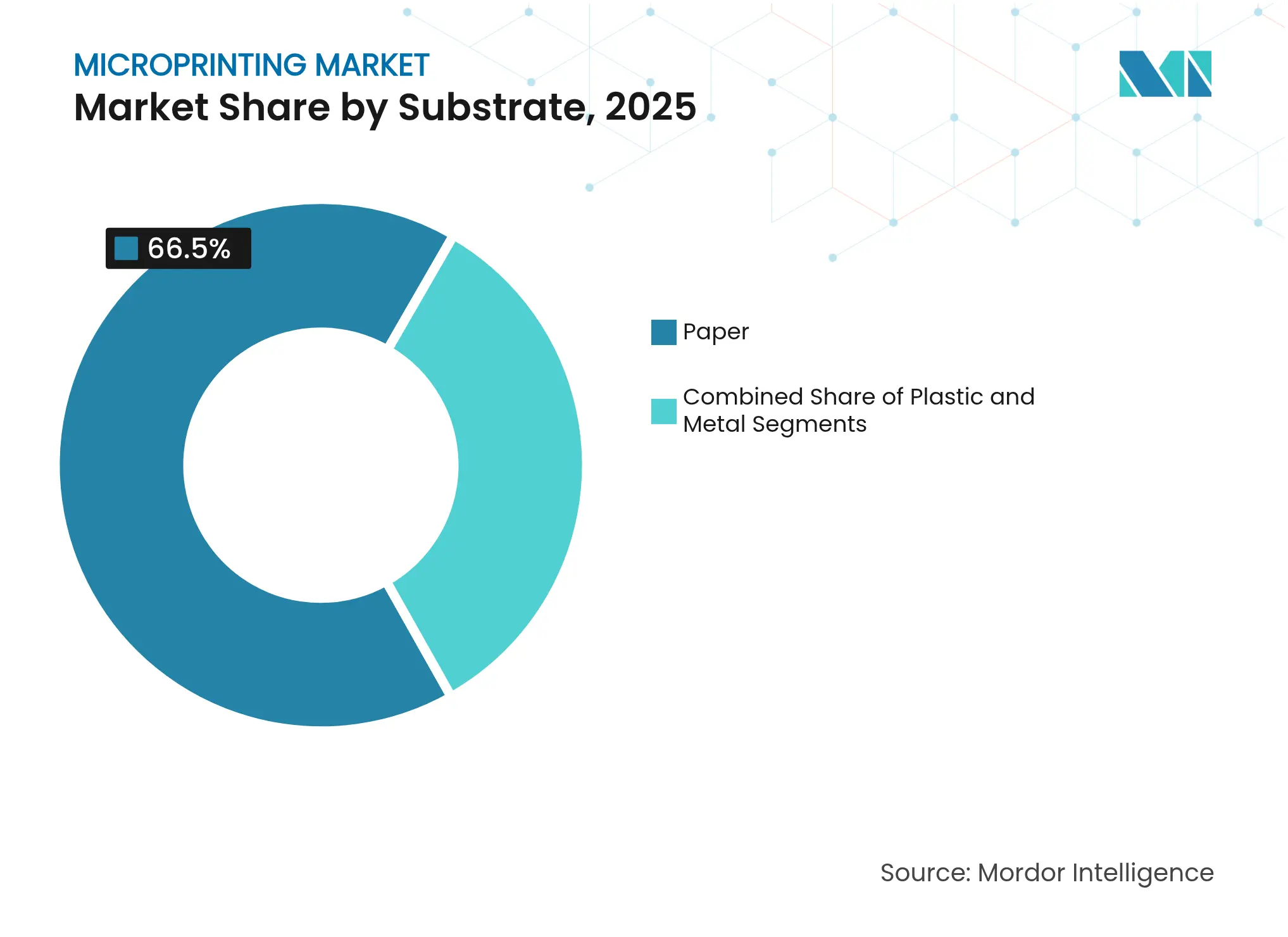

- By substrate, paper accounted for 66.50% of the microprinting market size in 2025; plastic is set to grow at 2.78% CAGR to 2031.

- By application, the BFSI segment commanded 36.62% share of the microprinting market in 2025, while pharmaceutical packaging is advancing at a 3.92% CAGR through 2031.

- By geography, North America dominated with 35.05% share in 2025; Asia-Pacific is the fastest-growing region with a 3.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microprinting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating demand for anti-counterfeit document security

Escalating demand for anti-counterfeit document security

| +0.8% | Global, with concentration in North America and EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+0.8%

|

Geographic Relevance

:

Global, with concentration in North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Stricter pharma serialization and packaging mandates

Stricter pharma serialization and packaging mandates

| +0.6% | Global, led by US DSCSA and EU FMD requirements | Short term (≤ 2 years) | |||

Rapid MICR adoption in banking cheque processing

Rapid MICR adoption in banking cheque processing

| +0.4% | North America and Asia-Pacific core markets | Long term (≥ 4 years) | |||

Surge in e-passport and national-ID roll-outs

Surge in e-passport and national-ID roll-outs

| +0.5% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) | |||

Nanoparticle functional inks enabling ultra-durable

microtext

Nanoparticle functional inks enabling ultra-durable

microtext

| +0.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) | |||

Blockchain-linked on-pack microtext for consumer

authentication

Blockchain-linked on-pack microtext for consumer

authentication

| +0.2% | Global, with pilot programs in premium brands | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Demand for Anti-Counterfeit Document Security

Governments and corporations face sophisticated forgery methods, prompting wider adoption of micro-scale security marks in currency, licences, and brand certificates. The U.S. Department of Homeland Security released guidelines that retrofit high-end presses to embed 0.5-point microtext, maintaining production speed while raising forgery deterrence.[1]U.S. Department of Homeland Security, “Counterfeit Deterrence Paper,” dhs.gov New Jersey regulations now require prescriptions to carry microtext legible only at 500% magnification, a measure aimed at cutting USD 100 billion lost annually to fake scripts. Financial institutions further integrate magnetic ink with biometric checks to form multilayer defences.

Stricter Pharma Serialization and Packaging Mandates

The U.S. Drug Supply Chain Security Act obliges every prescription unit to bear unique, machine-readable serials, creating sustained demand for high-resolution inline coders.[2] U.S. Food & Drug Administration, “Drug Supply Chain Security Act (DSCSA),” fda.gov UPM Pharmaceuticals demonstrated real-time tracking that trims recall time from days to hours. In Europe, the Falsified Medicines Directive accelerates line upgrades as firms add microprinted batch data, expiry dates and QR codes. Partnerships such as Siegfried-TraceLink provide scale-out cloud traceability that dovetails with on-pack microtext.

Rapid MICR Adoption in Banking Cheque Processing

Magnetic-ink character recognition retains relevance as a fraud-mitigation tool that electronic alternatives cannot fully match. Bank of Baroda rolled out MICR clearing across its India network, lifting processing speed while keeping error rates below 0.02%.[3]Bank of Baroda, “MICR Clearing Rollout,” bankofbaroda.in Check 21 statutes in the United States further protect the legal standing of MICR-encoded cheques, sustaining equipment investment cycles. Emerging markets combine MICR with biometric approval to strengthen identity assurance.

Surge in E-Passport and National-ID Roll-Outs

India’s Passport Seva 2.0 deploys RFID-enabled passports with multilayer microtext, opening a USD 1 billion procurement pipeline. Costa Rica’s biometric e-passport reached 68,000 issuances within three months, indicating rapid citizen adoption. Nepal’s multi-layer personalization integrates color photos and embedded chips compliant with ICAO standards. Governments balance fee cuts with upgraded security, broadening the addressable microprinting market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex for less than 10 µm resolution press lines High capex for less than 10 µm resolution press lines | -0.4% | Global, particularly impacting SMEs | Short term (≤ 2 years) |

% Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

Global, particularly impacting SMEs

|

Impact Timeline

:

Short term (≤ 2 years)

|

Digitisation reducing paper-based transactions

Digitisation reducing paper-based transactions

| -0.3% | Developed markets, led by North America and EU | Medium term (2-4 years) | |||

Vision-system readability rejects for ultra-fine text

Vision-system readability rejects for ultra-fine text

| -0.2% | Global manufacturing hubs | Short term (≤ 2 years) | |||

Environmental limits on heavy-metal and nano-pigment inks

Environmental limits on heavy-metal and nano-pigment inks

| -0.3% | EU-led, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capex for Less than 10 µm Resolution Press Lines

Installing sub-10 µm platforms demands multi-million-dollar outlays and specialist operators. Heidelberger Druckmaschinen targets 8% EBITDA by streamlining spend on such assets while still meeting security-print tolerances. HP’s supply-chain relocation outside China adds tariff-related cost layers that small converters find difficult to absorb. The capital hurdle delays entry by SMEs even as regulatory bars rise.

Environmental Limits on Heavy-Metal and Nano-Pigment Inks

France’s 2025 mineral-oil ban forces ink reformulation, requiring validated test methods published by the European Printing Ink Association. U.S. EPA SNUR filings oblige manufacturers to pre-clear new chemistries, extending development cycles. Orion S.A. responded with bio-circular PRINTEX Nature 35, proving performance parity for secure graphics without restricted oils. Early adopters of compliant inks gain first-mover advantage in regulated tenders.

Segment Analysis

By Type: Color Dominance Drives Premium Applications

Color microprinting generated the largest revenue share at 61.95% in 2025 as users valued multi-layer chromatic effects that complicate counterfeiting attempts. The segment integrates optically variable inks and quantum-dot tags that produce triple-level encryption, thereby cementing its hold on high-value documents. Monochrome retains a niche, yet nanoparticle black inks make it attractive for cheque and label lines that rely on legacy presses. Research groups now embed gold or silver nanoparticles into transparent varnishes, enabling covert watermarks within either segment. Color advances such as fluorescence-lifetime coding extend security by adding time-based verification.

Growing cost sensitivity keeps monochrome in focus, especially for institutions upgrading in phases. Nano-ink blends lower viscosity, permitting retrofits without overhauling print heads and supporting a 4.05% CAGR to 2031. Hybrid workflows let converters switch between monochrome base layouts and targeted color micro-text overlays, optimizing ink spend while preserving traceability. Vendors that offer drop-in fluids compliant with sub-10 µm nozzles win share as converters aim for minimal downtime. The dual-track evolution suggests the Microprinting market will continue blending vivid overt features with covert monochrome data at line speeds suited to mass issuance.

Note: Segment shares of all individual segments available upon report purchase

By Print Type: Single-Sided Solutions Meet Efficiency Demands

Single-sided configurations accounted for 54.35% of the Microprinting market in 2025 thanks to simpler web paths and shorter make-ready times. Banks, pharmacies and licensing bodies often need authentication on only one face of cheques, blister packs or permits, aligning well with single-pass engines. Low substrate waste and the ability to retrofit onto existing offset lines further support dominance. However, brand-protection programmes in luxury goods and passports now require microsecurity coverage on both surfaces, lifting double-sided solutions at a robust 3.28% CAGR.

Xerox’s Beyond Secure platform demonstrates in-line duplex capability without special paper, meeting customer demand for full-bleed variable data while trimming process steps. Double-sided systems also accommodate tamper-evident VOID patterns that appear when either side is altered, increasing deterrence. As algorithms detect microspacing irregularities, duplex lines can issue near-real-time reject signals, preventing downstream packaging jams. Therefore, equipment suppliers focusing on modular upgrades that convert single-sided assets into duplex will capture expansion spend while retaining the install base.

By Substrate: Paper Foundation Supports Digital Transition

Paper retained 66.50% of microprinting market share in 2025, anchored by its entrenched use in cheques, certificates and unit-dose pharma cartons. Regulatory familiarity and compatibility with high-volume flexographic presses keep adoption high even as electronic workflows advance. Paper also enables chemically reactive inks that reveal colour shifts under specific solvents, adding covert security. Plastic substrates, however, satisfy durability needs for ID cards, fare media and warehouse labels, growing 2.78% CAGR through 2031.

Suppliers such as Telesis Technologies use laser-etch stations to micro-mark plastic medical parts, guaranteeing permanence under sterilisation. Metals serve micro-trace codes in aerospace and defence where tamper-proof compliance certificates are mandatory. Smart substrates embedding mechano-chromic photonic crystals present long-term avenues by providing reversible colour shifts when bent, offering dynamic authenticity checks at point of use. The interplay of legacy paper and engineered plastics ensures the Microprinting market remains rooted in proven materials while diversifying into high-performance films.

Note: Segment shares of all individual segments available upon report purchase

By Application: BFSI Leadership Faces Pharmaceutical Challenge

The BFSI vertical controlled 36.62% of 2025 revenue owing to mandated MICR lines on cheques and micro-numeric fields in bank drafts. Stringent audit trails and central-bank certifications make switching costs high, entrenching the segment. Yet pharmaceutical packaging is advancing at 3.92% CAGR as global serialisation directives stipulate microprinted random codes at item level. SICPA’s GENESIS line modules now bundle vision inspection with inkjet heads, enabling sub-10 µm lot data that satisfies EU and US track-and-trace.

Government projects remain sizable through e-passport and voter-ID card rollouts. Corporate brand-protection solutions gain traction as luxury houses combat grey-market diversion via blockchain-paired microtext. Transportation and logistics adopt tamper-proof waybills, while the IT-telecom sector embeds micro QR tags on server boards for warranty validation. The widening field ensures the Microprinting market continues to address both legacy cheque volumes and emerging healthcare-driven growth.

Geography Analysis

North America held 35.05% of revenue in 2025 owing to the Drug Supply Chain Security Act’s serialization mandate and enduring MICR standards in banking. The U.S. Homeland Security innovation hub collaborates with domestic press builders to insert micro-security layers that resist photocopying and alter detection. Canada mirrors DSCSA-style rules, while Mexico’s generics industry upgrades blister printing to meet FDA export norms. Ongoing cheque usage, despite mobile options, stabilises demand.

Asia-Pacific posts the highest regional CAGR at 3.67% through 2031. India’s USD 1 billion RFID passport tender, combined with rising e-commerce returns that need secure labels, scales volumes quickly China’s installation of Domino’s N730i digital label press shows converter appetite for 1,200 dpi security engines adapted to domestic compliance needs. Pakistan, Nepal and Indonesia fast-track national identification programmes, each embedding polycarbonate pages with micro-text.

Europe remains significant as the Falsified Medicines Directive and stringent eco-ink laws address counterfeit medicines and sustainability. France’s mineral-oil ban compels ink reformulation, and early-compliant converters gain an edge in tenders. The region’s luxury goods sector further drives colour-shift threads in banknotes. South America and the Middle East invest steadily in e-visa and excise-stamp upgrades, while Africa’s mobile money ecosystem adopts micro-text vouchers to curb agent fraud, indicating new footprints for vendors.

Competitive Landscape

Market Concentration

Competition is moderately fragmented. Legacy OEMs such as Canon, Xerox, HP, Heidelberger and Konica Minolta compete with focused security providers including Domino Printing Sciences, SICPA and Giesecke+Devrient. BFSI and central-bank contracts remain concentrated among a handful of certified suppliers due to audit thresholds, but packaging and ID segments are more open to challengers who offer modular inline hybrids. Patent filings in nanoparticle inks and blockchain-anchored verification rise, pointing to capability races rather than pure scale.

Two strategic paths dominate: scale through merger or technology-led product cycles. Xerox’s USD 1.5 billion Lexmark acquisition expands managed print services and cross-sells document security to an enlarged client list. Domino opts for RandD differentiation, unveiling 30% faster CO₂ laser coders and 1,200 dpi engines suited for variable QR coding. Environmental compliance also shapes portfolios; Orion S.A.’s bio-circular black pigment offers a low-VOC alternative that secures European contracts.

Future competition will pivot on integrating edge-devices with cloud authentication. Vendors that bundle handheld scanners, cryptographic key chains and microprinted tags can monetize verification services beyond the substrate. Early movers in AI-assisted inspection systems win productivity gains by slashing false rejects in ultra-fine text.

Microprinting Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Xerox closed its USD 1.5 billion purchase of Lexmark International, targeting USD 200 million in cost synergies within two years.

- December 2024: Domino Printing Sciences rolled out the Dx-Series CO₂ laser coders, delivering 30% faster processing at FACHPACK 2024.

- November 2024: Giesecke+Devrient launched the RollingStar Venus micro-mirror security thread for banknotes.

- October 2024: Orion S.A. introduced bio-circular PRINTEX Nature 35 to meet French mineral-oil regulations.

Table of Contents for Microprinting Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Escalating demand for anti-counterfeit document security

- 4.2.2Stricter pharma serialization and packaging mandates

- 4.2.3Rapid MICR adoption in banking cheque processing

- 4.2.4Surge in e-passport and national-ID roll-outs

- 4.2.5Nanoparticle functional inks enabling ultra-durable microtext

- 4.2.6Blockchain-linked on-pack microtext for consumer authentication

- 4.3Market Restraints

- 4.3.1High capex for less than 10 micron resolution press lines

- 4.3.2Digitisation reducing paper-based transactions

- 4.3.3Vision-system readability rejects for ultra-fine text

- 4.3.4Environmental limits on heavy-metal and nano-pigment inks

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Consumers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Assessment Impact of Macroeconomic Factors on the Market

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Type

- 5.1.1Color

- 5.1.2Monochrome

- 5.2By Print Type

- 5.2.1Single-Sided

- 5.2.2Double-Sided

- 5.3By Substrate

- 5.3.1Paper

- 5.3.2Plastic

- 5.3.3Metal

- 5.4By Application

- 5.4.1BFSI

- 5.4.2Government

- 5.4.3Corporate

- 5.4.4Packaging

- 5.4.5Healthcare and Pharmaceuticals

- 5.4.6Transportation and Logistics

- 5.4.7IT and Telecom

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2South America

- 5.5.2.1Brazil

- 5.5.2.2Argentina

- 5.5.2.3Rest of South America

- 5.5.3Europe

- 5.5.3.1Germany

- 5.5.3.2United Kingdom

- 5.5.3.3France

- 5.5.3.4Italy

- 5.5.3.5Spain

- 5.5.3.6Rest of Europe

- 5.5.4Asia-Pacific

- 5.5.4.1China

- 5.5.4.2Japan

- 5.5.4.3South Korea

- 5.5.4.4India

- 5.5.4.5Indonesia

- 5.5.4.6Australia

- 5.5.4.7Rest of Asia-Pacific

- 5.5.5Middle East and Africa

- 5.5.5.1Middle East

- 5.5.5.1.1UAE

- 5.5.5.1.2Saudi Arabia

- 5.5.5.1.3Turkey

- 5.5.5.1.4Rest of Middle East

- 5.5.5.2Africa

- 5.5.5.2.1South Africa

- 5.5.5.2.2Egypt

- 5.5.5.2.3Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Xerox Holdings Corporation

- 6.4.2Canon Finetech Nisca Inc.

- 6.4.3Zebra Technologies Corporation

- 6.4.4HP Inc.

- 6.4.5Domino Printing Sciences plc

- 6.4.6Boston Micro Fabrication

- 6.4.7Matica Technologies AG

- 6.4.8Control Print Limited

- 6.4.9Brady Corporation

- 6.4.10Printegra

- 6.4.11Ricoh Company Ltd.

- 6.4.12MICRO FORMAT Inc.

- 6.4.13De La Rue plc

- 6.4.14Giesecke + Devrient GmbH

- 6.4.15SICPA SA

- 6.4.16Microtrace LLC

- 6.4.17AlpVision SA

- 6.4.18Authentix Inc.

- 6.4.19Document Security Systems Inc.

- 6.4.20Nanografix Corporation

- 6.4.21Smithers Pira

- 6.4.22SwiftPro Printer (Hayakawa)

- 6.4.233M (Anti-Counterfeit Solutions)

- 6.4.24Avery Dennison Corporation

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Microprinting Market Report Scope

Microprinting creates identifiable patterns or words in a printed medium at a small scale for human vision to read without a magnifying glass. The text may look like a solid line to the unaided eye. Unless the replication method can recognize and duplicate patterns to such scale, attempts to reproduce through photocopy, image scanning, or pantograph often translate as a dotted or solid line. Microprint is mainly utilized as an anti-counterfeiting technology because it can't be easily duplicated using standard digital techniques.

The microprinting market is segmented by type (color and monochrome), by print type (single-sided and double sided), by substrate (paper, plastic, and metal), by application (BFSI, government, corporate, packaging, healthcare, and pharmaceuticals, transportation & logistic) and by geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the segments mentioned above.