GCC Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.99 Billion |

| Market Size (2026) | USD 16.68 Billion |

| Market Size (2031) | USD 20.45 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Low |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Packaging Market Analysis by Mordor Intelligence

The GCC packaging market size is expected to increase from USD 15.99 billion in 2025 to USD 16.68 billion in 2026 and reach USD 20.45 billion by 2031, growing at a CAGR of 4.16% over 2026-2031. Robust petrochemical integration provides the region long-term resin cost leadership, while non-oil diversification agendas channel fresh capital toward consumer goods, pharmaceuticals, and industrial exports, each of which relies on reliable, higher-performance packs. Brand owners are responding to single-use plastic bans, cold-chain food security targets, and e-commerce fulfilment pressures by demanding lighter, smarter, and easier-to-recycle formats, thereby lifting both volume and value intensity across the GCC packaging market. Rising utilities tariffs and adoption of Extended Producer Responsibility in the United Arab Emirates are nudging converters to invest in recycled-content capability, automation, and design-for-circularity, changes that will gradually narrow the cost gap between virgin plastic and alternative substrates. Competitive intensity remains moderate; multinationals supply high-speed carton and flexible-film systems, while regional rigid-plastic and corrugated converters leverage feedstock proximity and lower labour costs to defend margins.

Key Report Takeaways

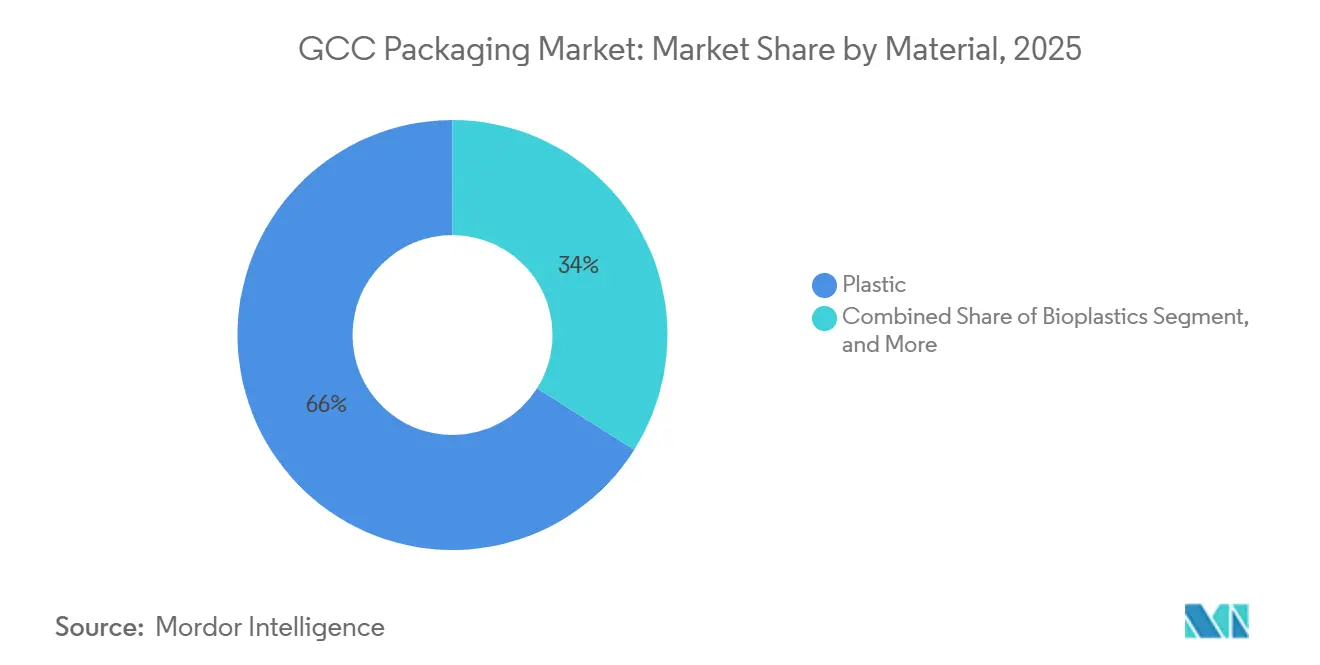

- Plastic captured 66.04% of GCC packaging market share in 2025, whereas bioplastics are projected to expand at a 4.98% CAGR through 2031.

- Rigid formats held 48.19% of the GCC packaging market in 2025, yet flexible packaging is forecast to advance at a 4.56% CAGR during 2026-2031.

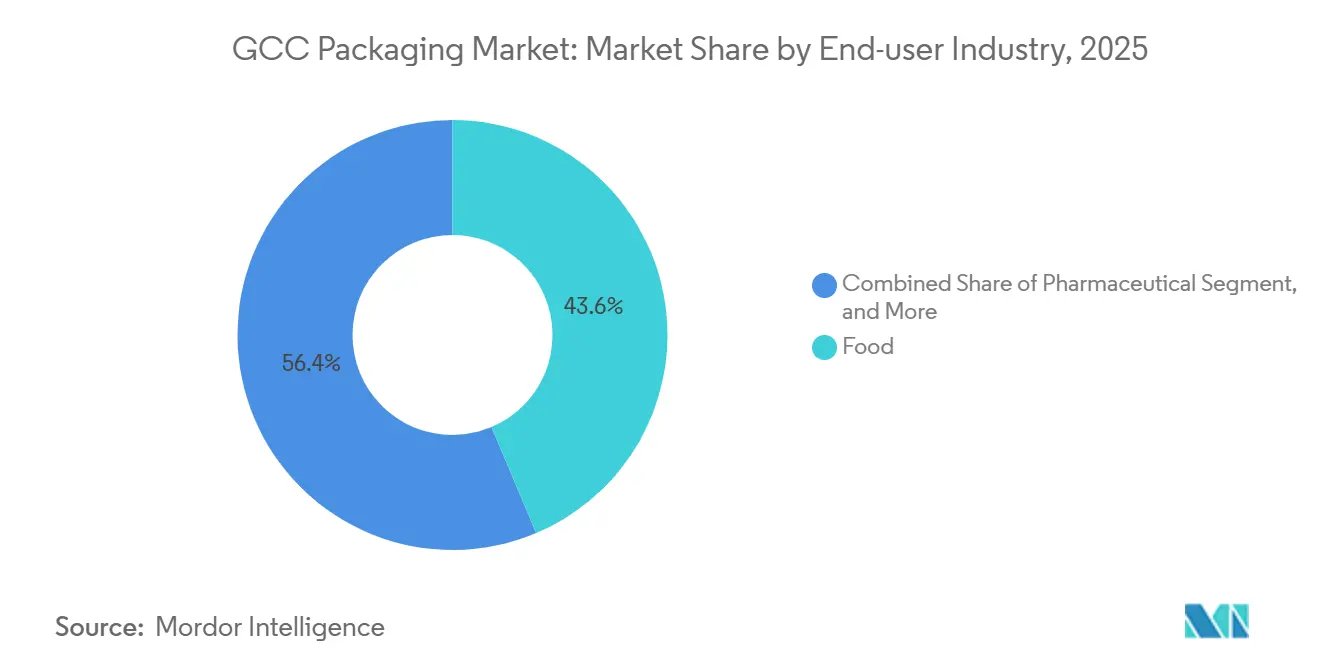

- Food applications accounted for 43.64% of GCC packaging demand in 2025, while pharmaceutical packaging is expected to grow at a 4.88% CAGR over the same period.

- Injection moulding commanded 46.93% of technology uptake in 2025, but injection stretch blow moulding is poised to grow at a 5.12% CAGR, the fastest among all methods.

- Saudi Arabia contributed 54.37% of GCC packaging demand in 2025, whereas Oman is projected to record the highest country-level CAGR at 4.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth in E-commerce Fulfilment Packaging | +0.90% | UAE and Saudi Arabia core; spillover to Qatar and Kuwait | Short term (≤ 2 years) |

| Government Bans on Single-use Plastics Spurring Alternative Materials | +0.70% | UAE leading; Saudi Arabia and Oman phased rollout | Medium term (2-4 years) |

| Food Security Investments Driving Cold-chain Packaging Demand | +0.60% | GCC-wide, with Saudi Arabia and UAE anchor investments | Medium term (2-4 years) |

| GCC Petrochemical Capacity Providing Low-cost Resin Advantage | +0.50% | Saudi Arabia and UAE production hubs; regional supply | Long term (≥ 4 years) |

| Mega-events Catalysing Retail Packaging Upgrades | +0.40% | Saudi Arabia (Vision 2030 events); Qatar (FIFA legacy); UAE (Expo continuation) | Short term (≤ 2 years) |

| AI-driven Packaging Automation Adoption at Converters | +0.30% | UAE and Saudi Arabia early adopters; gradual GCC diffusion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in E-commerce Fulfilment Packaging

Double-digit growth in home delivery is reshaping secondary and tertiary packaging needs across the GCC packaging market. Online orders typically require corrugated outers, cushioning void fill, and tamper-evident seals, formats that carry greater material intensity than in-store retail.[1]Consultancy-me editorial team, “MENA’s consumer packaged goods industry in a high-growth phase,” Consultancy-me.com, consultancy-me.com Retail sales are projected to hit USD 390 billion by 2028, with omnichannel share continuing to climb, a shift that magnifies demand for printable graphics that enhance the unboxing experience and for carrier-optimized pack dimensions that lower last-mile costs.[2]Nivetha Dayanand, “UAE to build world’s largest PLA bioplastic plant,” Zawya, zawya.com Saudi Arabia’s large-scale investments in logistics zones and fulfilment robotics will compress delivery lead times, encouraging frequent but smaller basket sizes, further elevating packaging unit requirements. Converters that add digital printing, right-sized corrugation, and biodegradable cushioning stand to capture premium margins as brand owners seek cost-effective differentiation. E-commerce therefore injects sustained incremental volume into the GCC packaging market and accelerates innovation in structural design.

Government Bans on Single-Use Plastics Spurring Alternative Materials

Implementation of the UAE’s Executive Council Resolution No. 124 of 2023 eliminated single-use plastic bags, cups, plates, and cutlery beginning June 2024, triggering wholesale substrate swaps toward moulded fiber, coated paper, and certified-compostable biopolymers.[3]Government of Dubai, “Executive Council Resolution No. 124 of 2023,” dubai.gov.ae The policy horizon has widened, with Saudi Arabia and Oman unveiling phased bans that prompt regional fast-food chains and retailers to redesign disposable service ware well before the 2028 compliance deadlines. However, GCC paper and board capacity is constrained by water scarcity and high energy costs, creating short-term shortages that inflate import bills and extend lead times. Emirates Biotech aims to address supply gaps through its 160,000-tonne-per-annum polylactic-acid complex, slated for mechanical completion in 2028, thereby positioning the UAE as a renewable-polymer hub. Brand owners now routinely request ISO 14855 or ASTM D6400 certification, and failure to comply risks shelf delisting, making alternative-material agility a competitive prerequisite across the GCC packaging market.

Food Security Investments Driving Cold-Chain Packaging Demand

More than 85% of the region’s caloric intake arrives through imports, exposing governments to external shocks that were amplified during the 2020 pandemic. In response, public investment funds and sovereign vehicles in Saudi Arabia and the UAE are expanding refrigerated logistics corridors, vertical farms, and protein-processing plants, each of which raises adoption of barrier films, modified-atmosphere trays, and aseptic cartons that preserve freshness across long distances. New dairy, juice, and ready-meal lines rely on Tetra Pak’s Factory OS, whose predictive-maintenance suite reduces downtime and cuts material waste, supporting an estimated 6.5% CAGR for Gulf food and beverage output through 2031. Cold-chain expansion also accelerates demand for temperature-indicator labels and data-logging smart tags that verify compliance during cross-desert haulage. Consequently, cold-chain investments strengthen medium-term demand visibility for the GCC packaging market and reward converters capable of advanced multilayer and aseptic structures.

GCC Petrochemical Capacity Providing Low-Cost Resin Advantage

Saudi Arabia’s 800,000-tonne polypropylene addition and Borouge 4’s 1.4 million-tonne polyethylene increment, both commissioned in 2024, underscore the Gulf’s feedstock strength. Natural-gas-linked utilities confer durable cost advantages to film extruders, blow molders, and injection molders that secure long-term offtake agreements, allowing them to price finished goods below import-parity alternatives in Asia or Europe. Yet spot resin volatility remains a profit-risk for smaller converters that buy monthly; polypropylene rose SAR 60 per tonne while polyethylene declined SAR 37 per tonne during 2024-2025. Major producers now explore chemical recycling and bio-feedstock integration to meet future carbon-border-adjustment levies and brand sustainability pledges. Sustained resin competitiveness cements the GCC packaging market’s role as an export-ready supply base, although converters must keep upgrading formulations to align with evolving circularity frameworks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Volatility in Polymer Feedstock Prices | -0.60% | GCC-wide, with Saudi Arabia and UAE production volatility transmitting regionally | Short term (≤ 2 years) |

| Limited Post-consumer Recycling Infrastructure | -0.40% | GCC-wide, with UAE pilot EPR as early exception | Medium term (2-4 years) |

| Water Scarcity Increasing Paper and Board Processing Costs | -0.30% | Saudi Arabia, UAE, and Oman most exposed; Kuwait and Bahrain moderate impact | Long term (≥ 4 years) |

| Skills Gap for Industry 4.0 Packaging Operations | -0.20% | UAE and Saudi Arabia automation leaders; broader GCC lag | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Volatility in Polymer Feedstock Prices

Crude-oil fluctuations, scheduled cracker turnarounds, and shifting Asian demand drove a SAR 60 per tonne rise in polypropylene while polyethylene dropped SAR 37 per tonne during 2024-2025, compressing gross margins for converters locked into quarterly price caps. Although recent capacity additions aim to smooth regional supply, global freight swings and arbitrage windows still transmit sharp resin price gyrations into the GCC packaging market. Smaller family-owned converters lack the hedging instruments that multinational peers wield, forcing them either to hold costly buffer stocks or accept spot-exposure risk. Emerging recycled-content mandates further destabilize price planning, because recycled PET and HDPE command premiums over virgin material in the Gulf due to tight local collection volumes. Without more transparent futures mechanisms or contract indexation, resin volatility will continue to temper near-term investment appetites.

Limited Post-Consumer Recycling Infrastructure

Current GCC recycling rates hover near 10%, well below the 40-50% performance achieved in the European Union and Japan, revealing an infrastructure gap valued between USD 12 billion and USD 25 billion for collection and re-processing capacity. The UAE’s 2025 pilot Extended Producer Responsibility scheme is the only mandatory program in the region, and its limited scope means most post-consumer packaging still lands in municipal dumps or is baled and shipped to Southeast Asia, a route threatened by tightening import restrictions. Lack of automated sorting hampers feedstock quality, making domestic recycled pellets costlier than imported alternatives and impeding brand commitments to 25-30% recycled content. Large beverage producers have funded pilot bottle-to-bottle projects, yet without deposit-return schemes or curb side pickup, volumes remain insufficient to reach scale. Converters therefore face a circularity paradox: customers ask for recycled content, but local supply does not yet exist at competitive prices, slowing sustainable packaging penetration in the GCC packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material - Plastic Strength Prevails While Bioplastics Accelerate

Plastic controlled 66.04% of the GCC packaging market in 2025, and the segment’s absolute tonnage continues to climb even as light-weighting trims gram-per-pack intensity. The dominance reflects resin availability, integrated feedstock economics, and established conversion assets. Within this hierarchy, polyethylene grades feed most films and liners, polypropylene secures closures and rigid tubs, and PET leads beverage bottles, together underpinning a multi-billion-dollar plastics economy inside the broader GCC packaging market size benchmark.

Bioplastics, although holding a single-digit share, are forecast to expand at a 4.98% CAGR as policy bans and multinational sustainability scorecards sharpen substrate choices. Emirates Biotech’s coming PLA complex will anchor regional biopolymer supply, encouraging converters to retrofit extrusion and thermoforming lines for compostable goods. Glass remains niche in pharmaceuticals and premium beverages because of weight and breakage liability, while metal persists in canned drinks and aerosols, buoyed by near-perfect recycling loops. Paper and board growth is moderated by desalinated-water input costs, a structural issue that limits capex for new mills despite rising e-commerce corrugate demand. Overall, material substitution dynamics promise gradual diversification of the GCC packaging market, yet plastics will retain center stage through 2031.

By Packaging Type - Flexible Formats Gain Momentum

Rigid packaging captured 48.19% of spending in 2025, upheld by bottles, jars, and industrial drums that satisfy barrier, stacking, and regulatory demands. However, flexible structures are logging a 4.56% CAGR through 2031 as pouches, sachets, and stretch wraps unlock cost, freight, and shelf-space advantages across food, personal-care, and e-commerce channels. Vacuum pouches extend protein shelf lives, while stand-up spouted pouches replace HDPE bottles in detergents, each substitution elevating the GCC packaging market’s innovation cycle.

E-commerce imposes extra corrugated outers, but brand owners increasingly pair them with lightweight mailer films and molded-fiber inserts to minimize dimensional weight. Semi-rigid blister packs and tubes straddle both camps, finding traction in pharmaceutical dosing compliance and premium cosmetics presentation. SIG’s aluminium-free full-barrier carton further blurs lines by delivering 12-month oxygen protection at a fraction of aluminium’s carbon load, a pivotal lever as corporate climate targets tighten. The convergence of lightweighting economics and sustainability imperatives will keep flexible formats siphoning share from rigid incumbents inside the GCC packaging market.

By End-User Industry - Pharma Leads Growth, Food Holds Scale

Food applications supplied 43.64% of 2025 consumption, reflecting the Gulf’s import dependency and growing domestic processing footprint. Ready meals, confectionery, and bakery products intensify pack counts through single-serve portions calibrated for smaller family sizes and on-the-go lifestyles. Yet the pharmaceutical vertical, while starting from a lower base, is predicted to outpace all peers at a 4.88% CAGR, lifted by localization incentives under Vision 2030 and the UAE’s industrial strategy. The resulting demand stimulates bespoke blister films, desiccant-lined bottles, and serialized labels that meet stringent traceability mandates, thereby enlarging the value share of the GCC packaging market.

Beverage lines rely on aseptic cartons, lightweight PET bottles, and aluminium cans, and they maintain steady growth in tandem with hospitality and tourism rebounds. Personal and home-care packs capture premiumization upside, as consumers shift toward branded beauty and hygiene offerings that often opt for intricate closures and multi-layer tubes. Industrial chemical and lubricant drums are sensitive to oil-price cycles but still represent a sizeable niche that values product integrity over aesthetics. Differentiated growth trajectories among end users therefore diversify revenue streams for converters across the GCC packaging market.

By Packaging Technology - Lightweighting Drives ISBM Adoption

Injection moulding retained 46.93% of technology share in 2025 thanks to its precision and repeatability for closures, tubs, and technical parts. Nonetheless, injection stretch blow moulding is on course for a 5.12% CAGR to 2031 because it unlocks thinner-wall PET bottles that shave up to 25% of resin mass without compromising strength, an irresistible proposition amid resin cost fluctuations. Rigid ISBM capacity expansions in Saudi Arabia and the UAE align with brand owner mandates for 25-30% recycled PET, creating a twin pull for lightweight and circular bottles inside the GCC packaging market share narrative.

Thermoforming sustains demand for transparent produce trays and dual-oven-ready meal dishes, offering speed and moderate tooling costs, whereas extrusion blow moulding remains the workhorse for opaque HDPE jerrycans. Extrusion film lines meet ballooning e-commerce wrap volumes, and converters pursue in-line MDO (machine-direction orientation) upgrades that improve mono-material recyclability. Automation overlays such as AI-guided vision systems and predictive maintenance modules, already live in Tetra Pak’s Factory OS, are migrating across the machinery spectrum, improving OEE and lowering scrap. As capital goods import statistics confirm, the technology mix is trending toward faster, smarter, and lighter solutions that reinforce competitiveness of the GCC packaging market.

Geography Analysis

Saudi Arabia delivered 54.37% of 2025 demand, a scale underpinned by its USD 65 billion consumer-goods economy, integrated resin supply, and a population topping 35 million. Vision 2030’s localization targets stipulate minimum domestic content for every fast-moving consumer product, forcing multinational brand owners to partner with local converters or invest in greenfield assets. Capital goods imports validate this pivot, with machinery shipments climbing 44.2% to EUR 381 million (USD 407 million) in 2024. Mega-event spending on sports and entertainment further spikes single-serve beverage and food-service packaging, pulling forward demand for premium graphics and quick-turn digital print runs.

Oman, despite a smaller population, is projected to outpace its neighbours with a 4.93% CAGR. The Ladayn Polymer Park, backed by USD 155 million across 16 plants, positions the Sultanate as an export-oriented hub for corrugate, film, and caps, augmented by Duqm Port’s deep-water terminals and favourable tax regimes. Manufacturing GDP rose 8.6% in 2024 and foreign direct investment touched RO 2.489 billion (USD 6.5 billion) as firms tapped lower labour costs and proximity to East African trade lanes. Although domestic consumption is modest, outward shipments of industrial goods, seafood, and dates keep converting lines humming and diversify the GCC packaging market.

The United Arab Emirates commands technology leadership, evidenced by EUR 266 million (USD 284 million) in 2024 machinery imports, a 24.5% jump that funds automation, robotics, and circular-material upgrades. Dubai’s Gulfood 2026, spanning 280,000 square meters across two venues, cements the emirate as a trade and innovation node influencing substrate choices and print aesthetics across the broader GCC packaging market. Qatar, Kuwait, and Bahrain add niche pull factors: Qatar’s post-World-Cup retail network favours premium presentation; Kuwait’s 447-liter daily per-capita water use drives PET bottle demand; Bahrain’s re-export logistics hinge on durable corrugate and pallet wrap. Water scarcity, highlighted by the World Bank, pushes paper mills to optimize closed-loop systems, slightly curbing paper’s long-term growth yet unlocking opportunities for water-efficient plastics.

Competitive Landscape

Market structure is moderately concentrated, with global laminate-carton and aseptic-film giants coexisting beside agile regional converters. Tetra Pak shipped 178 billion packs worldwide in FY24, and SIG Combibloc booked EUR 3.3 billion (USD 3.53 billion) revenue that same year, together supplying most dairy, juice, and alternative-milk lines in the GCC. Local rigid-plastic suppliers benefit from feedstock proximity, translating to resin procurement spreads of USD 80-120 per tonne against Asian rivals, a delta that underwrites margins even during oil downturns. Corrugated specialists in Saudi Arabia cluster around Jubail and Dammam to serve petrochemical exports, while Emirati label and tube printers tap Dubai’s free-zone logistics for just-in-time shipments.

Sustainability differentiation is the current battleground. SIG’s Dry-Moulded-Fiber closure, co-developed with Pulpac, targets 90% paper content for full cartons by 2030 and reduces water inputs by up to 70% compared with injection-moulded HDPE caps. Tetra Pak has allocated USD 42 million globally for collection and recycling pilots and an additional USD 107 million for low-carbon material R&D, a commitment echoed in local partnerships with waste-management firms. Emirates Biotech’s forthcoming PLA complex introduces competitive tension in food-service disposables and supermarket produce trays, potentially displacing imports from Europe and Asia once commercial volumes flow.

Technology race momentum is clear. Tetra Pak’s Factory OS and SIG’s NEO filling machine integrate AI-driven predictive maintenance and energy dashboards that cut carbon per filled liter by up to 25%. Regional converters with access to subsidized energy but limited skilled labour are fast-tracking robotics and vision systems to maintain uptime and quality under tighter hygiene codes. Extended Producer Responsibility in the UAE adds compliance cost layers that will reward early adopters of design-for-recycling as fee schedules escalate. Overall, strategic moves indicate a gradual but decisive tilt toward circularity, automation, and lightweighting that will redefine competitive advantages inside the GCC packaging market.

GCC Packaging Industry Leaders

Tetra Pak International SA

Mondi plc

AptarGroup Inc.

Arabian Packaging LLC

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Saudi Arabia mandated recyclable, food-grade compliant packaging for fruits and vegetables, effective immediately.

- August 2025: Arla Foods approved a EUR 50.9 million (USD 56.0 million) expansion for glass cheese jars in Bahrain, which will boost output by 30%.

- July 2025: Oman enforced a ban on single-use plastic bags across all retail outlets.

- May 2025: Hotpack invested USD 100 million to open its first U.S. plant in New Jersey.

GCC Packaging Market Report Scope

The GCC Packaging Market Report is Segmented by Material (Plastic, Metal, Glass, Paper and Paperboard, Bioplastics), Packaging Type (Rigid, Flexible, Semi-rigid), End-user Industry (Food, Beverage, Pharmaceutical, Personal and Homecare, Industrial), Packaging Technology (Thermoforming, Blow Molding, Injection Molding, Vacuum Forming), and Geography (UAE, Saudi Arabia, Qatar, Kuwait, Oman, Bahrain). Market Forecasts are Provided in Value (USD).

| Plastic | LDPE |

| HDPE | |

| PET | |

| PP | |

| PS | |

| PVC | |

| Other Plastics | |

| Metal | Aluminum |

| Steel / Tinplate | |

| Glass | Flint (Clear) |

| Amber | |

| Green | |

| Paper and Paperboard | Corrugated Board |

| Folding Cartons | |

| Liquid Packaging Board | |

| Molded Fiber | |

| Bioplastics | PLA |

| PHA | |

| Starch-based | |

| Bio-PET / Bio-PE |

| Rigid | Bottles and Jars |

| Cans and Drums | |

| Trays and Containers | |

| Caps and Closures | |

| Flexible | Pouches |

| Bags and Sacks | |

| Films and Wraps | |

| Sachets and Stick Packs | |

| Lidding | |

| Semi-rigid | Blister Packs |

| Tubes | |

| Clamshells | |

| Cups and Bowls |

| Food | Processed Food |

| Fresh Produce | |

| Bakery and Confectionery | |

| Meat, Poultry and Seafood | |

| Ready Meals | |

| Beverage | Bottled Water |

| Carbonated Soft Drinks | |

| Dairy Beverages | |

| Juices and Nectars | |

| Alcoholic Beverages | |

| Pharmaceutical | Prescription Drugs |

| OTC Medicines | |

| Nutraceuticals | |

| Personal and Homecare | Personal Care |

| Home Care and Cleaning | |

| Cosmetics | |

| Industrial | Chemicals and Lubricants |

| Building and Construction | |

| Automotive Components |

| Thermoforming | |

| Blow Molding | Extrusion Blow Molding |

| Injection Stretch Blow Molding | |

| Injection Blow Molding | |

| Injection Molding | |

| Vacuum Forming |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Material | Plastic | LDPE |

| HDPE | ||

| PET | ||

| PP | ||

| PS | ||

| PVC | ||

| Other Plastics | ||

| Metal | Aluminum | |

| Steel / Tinplate | ||

| Glass | Flint (Clear) | |

| Amber | ||

| Green | ||

| Paper and Paperboard | Corrugated Board | |

| Folding Cartons | ||

| Liquid Packaging Board | ||

| Molded Fiber | ||

| Bioplastics | PLA | |

| PHA | ||

| Starch-based | ||

| Bio-PET / Bio-PE | ||

| By Packaging Type | Rigid | Bottles and Jars |

| Cans and Drums | ||

| Trays and Containers | ||

| Caps and Closures | ||

| Flexible | Pouches | |

| Bags and Sacks | ||

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Lidding | ||

| Semi-rigid | Blister Packs | |

| Tubes | ||

| Clamshells | ||

| Cups and Bowls | ||

| By End-user Industry | Food | Processed Food |

| Fresh Produce | ||

| Bakery and Confectionery | ||

| Meat, Poultry and Seafood | ||

| Ready Meals | ||

| Beverage | Bottled Water | |

| Carbonated Soft Drinks | ||

| Dairy Beverages | ||

| Juices and Nectars | ||

| Alcoholic Beverages | ||

| Pharmaceutical | Prescription Drugs | |

| OTC Medicines | ||

| Nutraceuticals | ||

| Personal and Homecare | Personal Care | |

| Home Care and Cleaning | ||

| Cosmetics | ||

| Industrial | Chemicals and Lubricants | |

| Building and Construction | ||

| Automotive Components | ||

| By Packaging Technology | Thermoforming | |

| Blow Molding | Extrusion Blow Molding | |

| Injection Stretch Blow Molding | ||

| Injection Blow Molding | ||

| Injection Molding | ||

| Vacuum Forming | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

Key Questions Answered in the Report

How large is the GCC packaging market in 2026 and what is its projected growth?

It is valued at USD 16.68 billion in 2026 and is projected to reach USD 20.45 billion by 2031 at a 4.16% CAGR.

Which material dominates current demand across the Gulf?

Conventional plastics account for 66.04% of 2025 sales because of integrated petrochemical feedstock economics.

What segment is growing fastest within the GCC packaging market?

Injection stretch blow molding technology leads with a 5.12% CAGR due to demand for lightweight PET bottles.

Why is Oman forecast to outpace its neighbors in packaging demand?

Government-backed investments in Ladayn Polymer Park and rising industrial exports push Oman toward a 4.93% CAGR through 2031.

How are single-use plastic bans influencing material choices?

Retailers and food-service chains are pivoting to molded fiber, coated paper, and PLA bioplastics to comply with phased bans in the UAE, Saudi Arabia, and Oman.

What is the main challenge impeding recycled-content adoption?

Limited post-consumer collection and sorting capacity keeps local recycled resin scarce and costlier than virgin alternatives.

Page last updated on: