Gastroretentive Drug Delivery Systems Outsourcing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

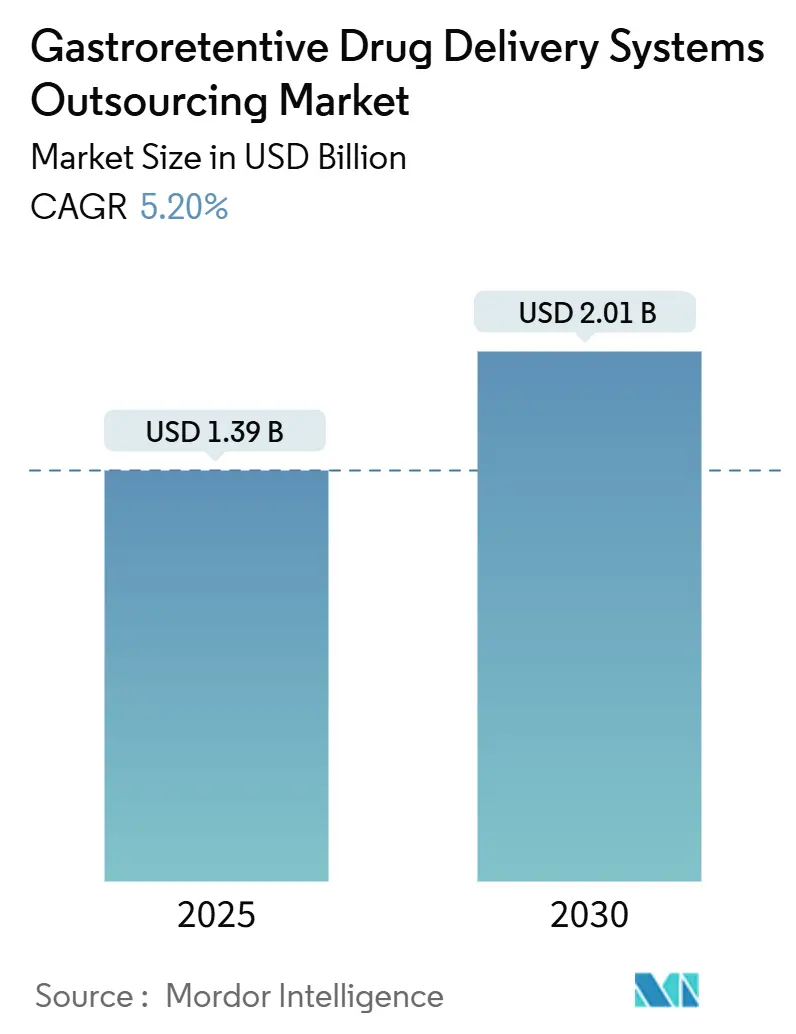

| Market Size (2025) | USD 1.39 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

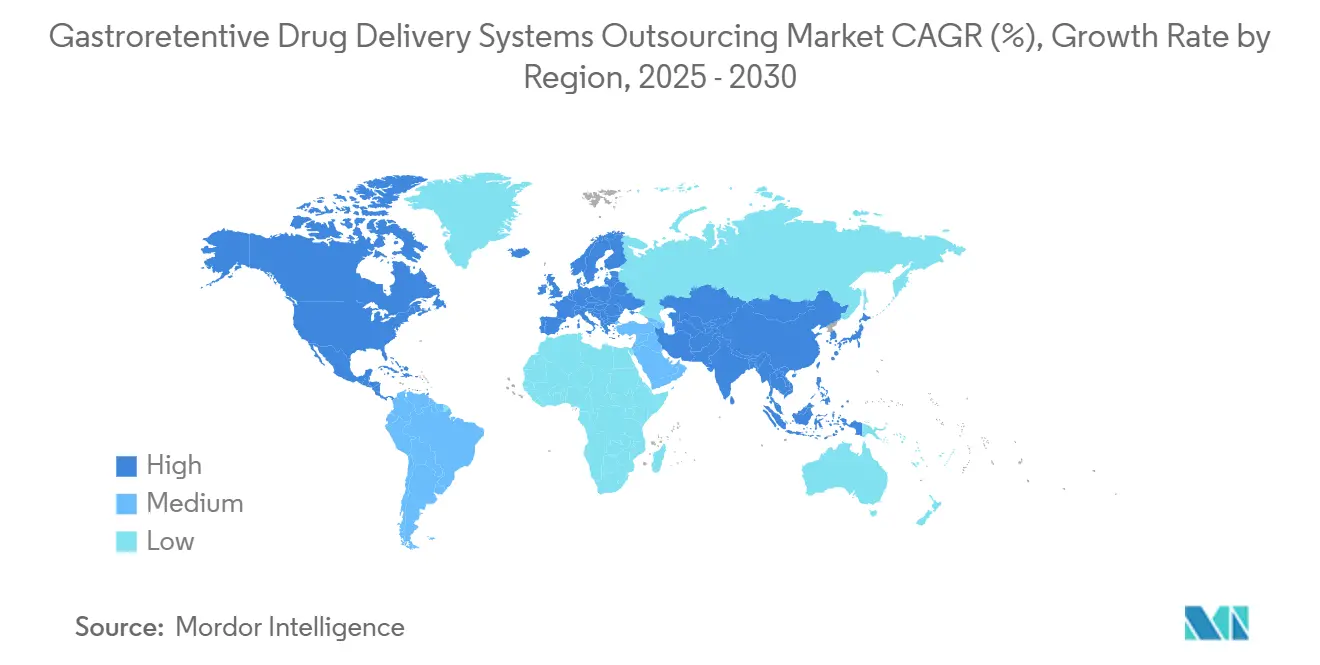

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastroretentive Drug Delivery Systems Outsourcing Market Analysis by Mordor Intelligence

The gastroretentive drug delivery systems outsourcing market size stood at USD 1.39 billion in 2025 and is forecast to reach USD 2.01 billion by 2030, advancing at a 5.20% CAGR. This rise reflects a transition from volume-driven expansion to value creation led by technology, notably AI-guided formulation design and hybrid retention mechanisms. Patent-expiration risk on blockbuster molecules is steering large pharmaceutical companies toward lifecycle-management programs that rely on gastric-retentive formats to preserve exclusivity. At the same time, biotechnology firms view these platforms as a gateway to unlock oral administration for peptides and proteins, reshaping therapeutic economics. Regional performance diverges: North America captures 38.9% 2024 revenue through deep CDMO networks and favorable regulation, while Asia-Pacific is scaling fastest at a 12.4% CAGR as domestic innovators close capability gaps.

Key Report Takeaways

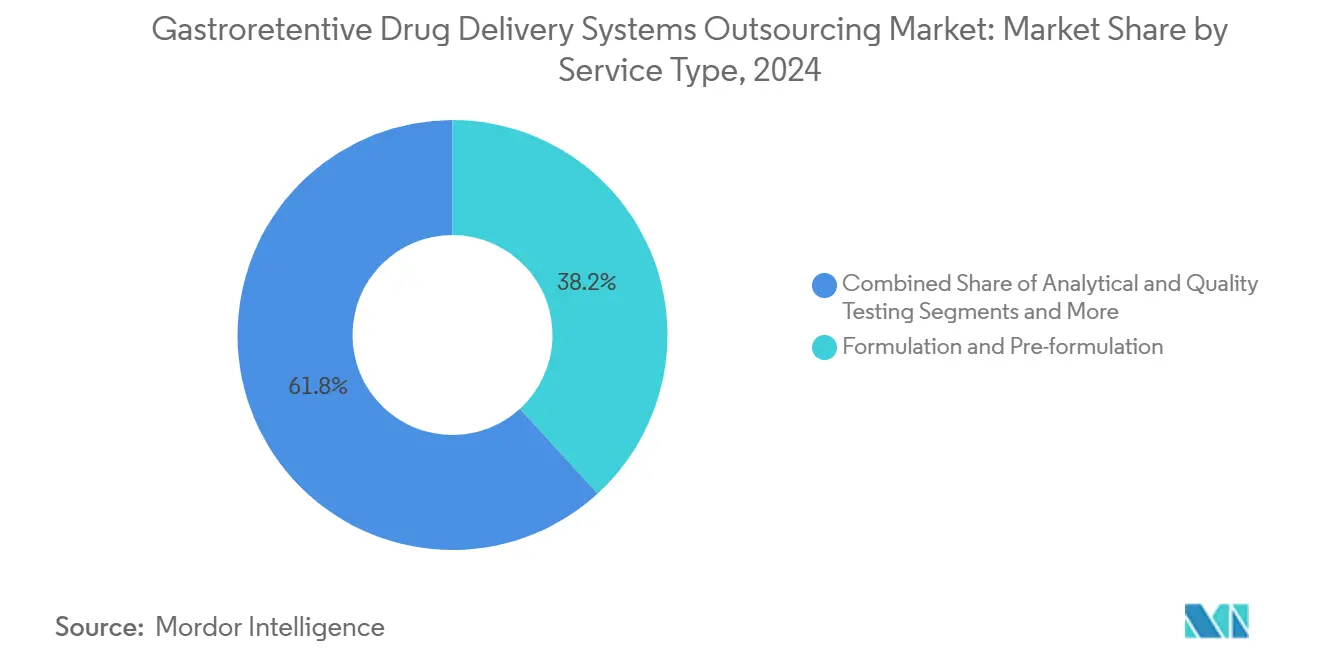

- By service type, Formulation & Pre-formulation held 38.2% of gastroretentive drug delivery systems outsourcing market share in 2024; Clinical-Trial Manufacturing is projected to grow at 12.8% CAGR to 2030.

- By dosage-form approach, Floating Systems led with 42.5% share of the gastroretentive drug delivery systems outsourcing market size in 2024, whereas Dual-Mechanism/Hybrid platforms are set to expand at 14.6% CAGR through 2030.

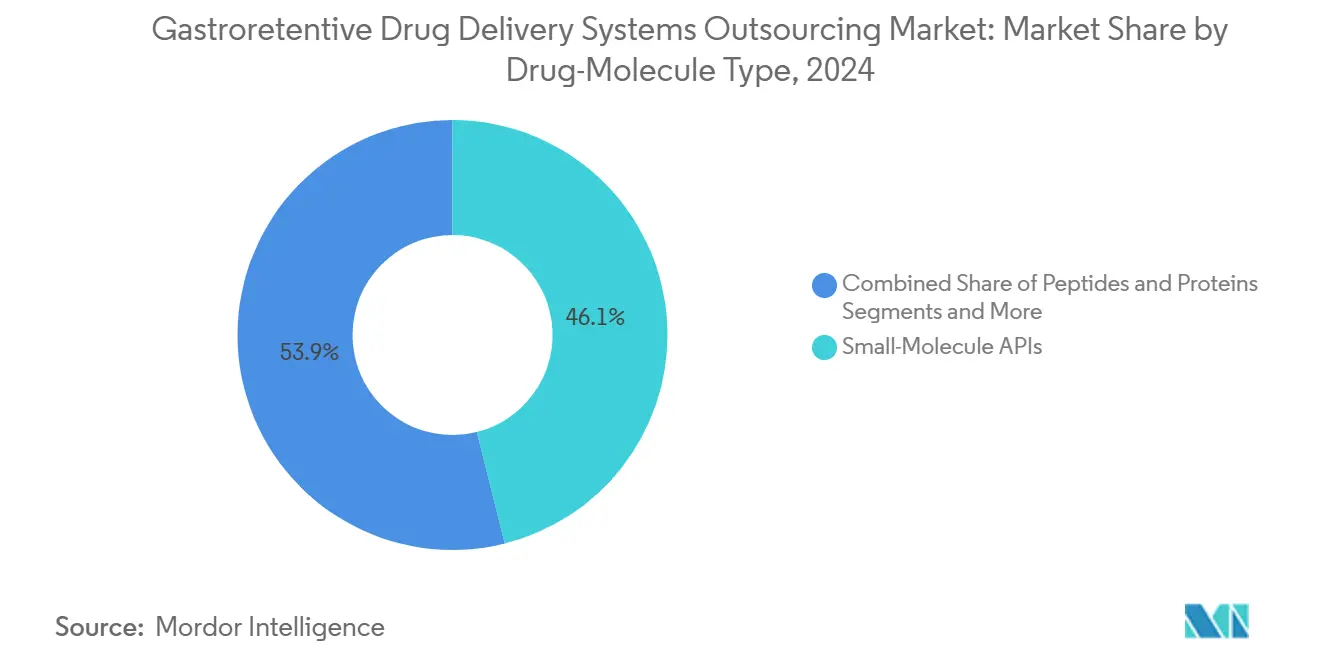

- By drug-molecule type, Small-Molecule APIs commanded 46.1% of 2024 revenue, but Peptides & Proteins exhibit the highest 13.9% CAGR outlook.

- By end user, Large Pharmaceutical companies accounted for 54.6% of 2024 demand, while Biotechnology Firms show a 12.3% CAGR and represent the fastest-growing customer base.

- By geography, North America led with 38.9% revenue share in 2024; Asia Pacific is forecast to post a 12.4% CAGR from 2025-2030.

Global Gastroretentive Drug Delivery Systems Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand For Oral Bioavailability Enhancement | +1.30% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Patent-Cliff Lifecycle Management Initiatives | +0.80% | North America & EU primarily | Short term (≤ 2 years) |

| Rising Prevalence Of Gastric Disorders (GERD, H. Pylori) | +0.90% | Global, highest impact in developed markets | Long term (≥ 4 years) |

| Shift Toward Oral Delivery Of Peptides & Proteins | +1.20% | Global, early adoption in North America | Medium term (2-4 years) |

| 3-D Printing Enabling Personalised GRDDS Prototypes | +0.80% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| AI-Led In-Silico Formulation Screening Lowering Outsourcing Barriers | +0.90% | Global, technology hubs leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Oral Bioavailability Enhancement

Pharmaceutical developers increasingly view controlled gastric residence as a route to salvage compounds with narrow absorption windows or pH-sensitive stability. A 13.98% global prevalence of GERD highlights the scale of patient need for formulations that perform in challenging gastric conditions.[1]World Journal of Gastrointestinal Pharmacology and Therapeutics, “Insight into Global Burden of Gastroesophageal Reflux Disease: Understanding Its Reach and Impact,” wjgnet.com By pairing pH-responsive polymers with buoyant matrices, modern systems boost dissolution rates without exacerbating systemic adverse effects. These advances lower attrition risk in development pipelines and convert shelved molecules into viable assets, reinforcing the gastroretentive drug delivery systems outsourcing market as a strategic tool for portfolio optimization.

Patent-Cliff Lifecycle-Management Initiatives

An estimated USD 183 billion in prescription sales confront generic erosion by 2030, elevating reformulation as a defense strategy. Gastric retentive dosage forms secure additional patents on release kinetics, gaining faster regulatory review than new chemical entities and sustaining premium pricing. Integration of multiple actives within a single retention platform further complicates generic replication, repositioning the patent cliff as a springboard for differentiated therapy offerings.

Rising Prevalence of Gastric Disorders (GERD, H. pylori)

More than 20% of North Americans live with GERD, and H. pylori infection rates reach 41% in select regions.[2]The Lancet Gastroenterology & Hepatology, “The Global, Regional, and National Burden of Gastro-Oesophageal Reflux Disease in 195 Countries and Territories, 1990–2017,” thelancet.com Both conditions alter pH and mucosal characteristics, undermining conventional dosage performance. Muco-adhesive and pH-independent retention technologies stabilize drug exposure over prolonged residence, underpinning demand for tailored solutions that enhance adherence and outcomes in chronic gastric disease management.

Shift Toward Oral Delivery of Peptides & Proteins

Patient preference and payer cost pressures drive the search for oral biologic alternatives to injections. Retentive platforms that shelter labile peptides from enzymatic degradation, combined with permeation enhancers, have demonstrated clinically meaningful bioavailability, opening billion-dollar prospects for oral versions of therapies once limited to parenteral routes. This trend accelerates the adoption of advanced hybrid systems within the gastroretentive drug delivery systems outsourcing market.

3-D Printing Enabling Personalized GRDDS Prototypes

Additive manufacturing allows rapid iteration of geometry and density, producing patient-specific buoyancy profiles and multi-compartment tablets without costly tooling changes. North American and European tech hubs spearhead these pilots, and APAC facilities are beginning to scale powder-bed fusion lines, signaling a new era of personalized drug delivery economics.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Inter-Patient Gastric-Physiology Variability | -0.70% | Global, particularly challenging in diverse populations | Long term (≥ 4 years) |

| Complex, Country-Specific Controlled-Release Regulations | -0.50% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Weak IVIVC Models For Next-Gen GRDDS | -0.40% | Global, concentrated in advanced pharmaceutical markets | Medium term (2-4 years) |

| Supply Bottlenecks For Speciality Low-Density Polymers | -0.30% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Inter-Patient Gastric-Physiology Variability

Gastric emptying can span 30 minutes to 4 hours, complicating prediction of retention time and drug release. Elderly patients, polypharmacy regimens, and gastrointestinal pathologies amplify variability, forcing sponsors to run larger clinical cohorts and driving up costs. Weak in-vitro/in-vivo correlation (IVIVC) models increase regulatory uncertainty and elongate development cycles, tempering investment appetite.

Complex, Country-Specific Controlled-Release Regulations

Divergent FDA, EMA, and emerging-market guidelines oblige sponsors to customize dossiers and occasionally reformulate products, expanding timelines by quarters or years. Combination products and novel polymer classes face prolonged review, deterring SMEs with limited regulatory budgets and delaying global launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Formulation Services Drive Early-Stage Innovation

Early-stage formulation and pre-formulation accounted for 38.2% of 2024 revenue, underscoring their pivotal role in defining downstream manufacturing strategy. The gastroretentive drug delivery systems outsourcing market size for this service group is projected to advance steadily as sponsors leverage AI-guided polymer selection to reduce bench iterations. Rising complexity of peptide payloads heightens demand for sophisticated excipient screening, stimulating outsourcing to CDMOs with niche know-how.

Clinical-Trial Manufacturing, though smaller in absolute value, shows a 12.8% CAGR as precision-dosage trials multiply. Sponsors increasingly execute adaptive designs that require small, staggered batch production, favoring facilities with flexible containment and rapid changeover capabilities. Analytical & Quality Testing grows in lockstep with regulatory scrutiny, while Process Development & Scale-Up providers refine geometrics and buoyancy profiles for commercial batches.

By Dosage-Form Approach: Hybrid Systems Reshape Technology Landscape

Floating tablets maintained 42.5% of 2024 revenue owing to proven design rules and lower regulatory friction. Yet dual-mechanism hybrids, integrating buoyancy with muco-adhesion or expandable matrices, are rising at a 14.6% CAGR, capturing unmet clinical niches that need extended release beyond 12 hours. This surge distributes adoption across cardiometabolic and anti-infective therapies, widening the gastroretentive drug delivery systems outsourcing market footprint.

Muco-adhesive systems serve localized gastric disorders by anchoring actives at the mucosal interface, while swellable formats meet high-dose requirements through volume expansion. High-density tablets remain a niche for geriatric use where motility is reduced. Manufacturers seek 3-D printed architectures to combine these mechanisms, foreshadowing next-generation adaptive release devices.

By Drug-Molecule Type: Peptide Delivery Transforms Market Dynamics

Small-molecule APIs still dominate value with 46.1% share, primarily as reformulated blockbusters nearing patent loss. The gastroretentive drug delivery systems outsourcing market share for peptides & proteins is small today but expanding rapidly: a 13.9% CAGR reflects a pipeline shift in endocrine and rare-disease indications. Successes in protecting GLP-1 analogs inside buoyant enteric microspheres validate commercial potential.

Antibiotics leverage local gastric targeting to eradicate H. pylori with lower systemic exposure, while narrow-absorption-window cardiovascular agents gain therapeutic windows through extended residence. Other high-value molecules—including oncology and immunology biologics—are entering preclinical programs that aim to marry oral convenience with controlled exposure profiles.

By End-User: Biotechnology Firms Accelerate Innovation Adoption

Large Pharmaceutical companies represented 54.6% of 2024 orders, concentrating on lifecycle defense of legacy franchises. The gastroretentive drug delivery systems outsourcing market size attached to biotechnology firms, however, is expanding fastest; their 12.3% CAGR aligns with a surge in orally dosed biologic trials. The gastroretentive drug delivery systems outsourcing industry is, therefore, witnessing a power shift toward emergent innovators that co-develop delivery technology and novel modalities.

Specialty pharma players target niche indications with premium pricing, and generics manufacturers position for complex-generic opportunities as first-generation patents lapse. Academic institutes feed early-stage breakthroughs—such as MIT’s pulsatile depot—into commercial pipelines via licensing, deepening collaboration networks.

Geography Analysis

North America generated 38.9% of 2024 revenue thanks to established clinical infrastructure and strict yet predictable FDA pathways. Investments such as Eli Lilly’s USD 50 billion multi-site expansion and Novo Nordisk’s USD 4.1 billion fill-finish plant underscore commitment to localized, resilient supply chains. The gastroretentive drug delivery systems outsourcing market benefits from adjacent AI and 3-D printing clusters that accelerate formulation cycles.

Asia-Pacific is the fastest mover at a 12.4% CAGR through 2030, fueled by contract research hubs in India and regulatory modernization in China. Economies of scale in polymer production and a growing domestic biotech scene make the region a pivotal outsourcing destination. Regional governments are harmonizing standards with ICH guidelines, easing entry barriers and magnifying the gastroretentive drug delivery systems outsourcing market presence across APAC.

Europe remains technologically mature, channeling investment into high-value biologics and sustainability-focused manufacturing such as Sanofi’s EUR 1.3 billion insulin site. EMA guidance on modified release provides clarity, but environmental regulations spur adoption of greener polymers and solventless processes. South America and Middle East & Africa show nascent yet improving uptake, primarily via multinational pharma tenders and local generics that license older gastric retentive designs.

Competitive Landscape

The gastroretentive drug delivery systems outsourcing market exhibits moderate consolidation: the top five CDMOs and formulation specialists collectively hold roughly 55% revenue, reflecting significant but not prohibitive barriers to entry. Novo Nordisk’s USD 16.5 billion acquisition of Catalent in 2025 illustrates the strategic imperative to internalize advanced delivery capabilities.

Firms now compete on AI-enabled formulation suites, regulatory depth across multiple jurisdictions, and hybrid-mechanism patent portfolios. Material innovation—such as cellulose-nanocrystal microspheres from the University of Arkansas—feeds proprietary platforms that anchor client relationships.[3]Eindhoven University of Technology, “New Method Enables Gradual Release of Protein Drugs into the Body,” phys.org

White-space opportunities center on personalized medicine, oral biologics, and combination regimens within a single retentive shell. Entrants leverage modular 3-D printing and cloud-linked in-silico tools to sidestep large capital expenditure, gradually lowering concentration and intensifying rivalry.

Gastroretentive Drug Delivery Systems Outsourcing Industry Leaders

Catalent

Lonza

Thermo Fisher Inc. (Patheon)

Recipharm

Evonik Health Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LGM Pharma invested USD 6 million to expand U.S. capacity in advanced gastric retentive formulations.

- December 2024: Lonza activated new capsule plants in India and China to meet modified-release demand.

- April 2024: Amneal Pharmaceuticals secured a grant to create an extended-release pyridostigmine gastric retentive tablet.

Global Gastroretentive Drug Delivery Systems Outsourcing Market Report Scope

| Formulation & Pre-formulation Services |

| Analytical & Quality Testing |

| Process Development & Scale-Up |

| Clinical-Trial Manufacturing |

| Commercial Manufacturing |

| Floating Systems |

| Muco-adhesive Systems |

| Expandable / Swellable Systems |

| High-Density Systems |

| Dual-Mechanism / Hybrid Systems |

| Small-Molecule APIs |

| Peptides & Proteins |

| Antibiotics |

| Narrow Absorption-Window Drugs |

| Other High-Value Molecules |

| Large Pharmaceutical Companies |

| Specialty Pharma |

| Biotechnology Firms |

| Generics Manufacturers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Formulation & Pre-formulation Services | |

| Analytical & Quality Testing | ||

| Process Development & Scale-Up | ||

| Clinical-Trial Manufacturing | ||

| Commercial Manufacturing | ||

| By Dosage-Form Approach | Floating Systems | |

| Muco-adhesive Systems | ||

| Expandable / Swellable Systems | ||

| High-Density Systems | ||

| Dual-Mechanism / Hybrid Systems | ||

| By Drug-Molecule Type | Small-Molecule APIs | |

| Peptides & Proteins | ||

| Antibiotics | ||

| Narrow Absorption-Window Drugs | ||

| Other High-Value Molecules | ||

| By End-User | Large Pharmaceutical Companies | |

| Specialty Pharma | ||

| Biotechnology Firms | ||

| Generics Manufacturers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the gastroretentive drug delivery systems outsourcing market?

It was valued at USD 1.39 billion in 2025 and is forecast to reach USD 2.01 billion by 2030.

Which region is growing fastest for gastric retentive technologies?

Asia-Pacific is expanding at a 12.4% CAGR due to rising CDMO capacity and regulatory reforms.

Which dosage-form approach is expected to lead future growth?

Dual-Mechanism/Hybrid systems are forecast to grow at 14.6% CAGR through 2030.

Why are biotechnology firms investing in gastric retentive platforms?

They aim to enable oral delivery of peptides and proteins, improving patient compliance and unlocking new revenue.

What is the main hurdle in global commercialization of GRDDS?

Differing country-specific controlled-release regulations that prolong development timelines and raise costs.

Page last updated on: