Pulmonary Drug Delivery Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

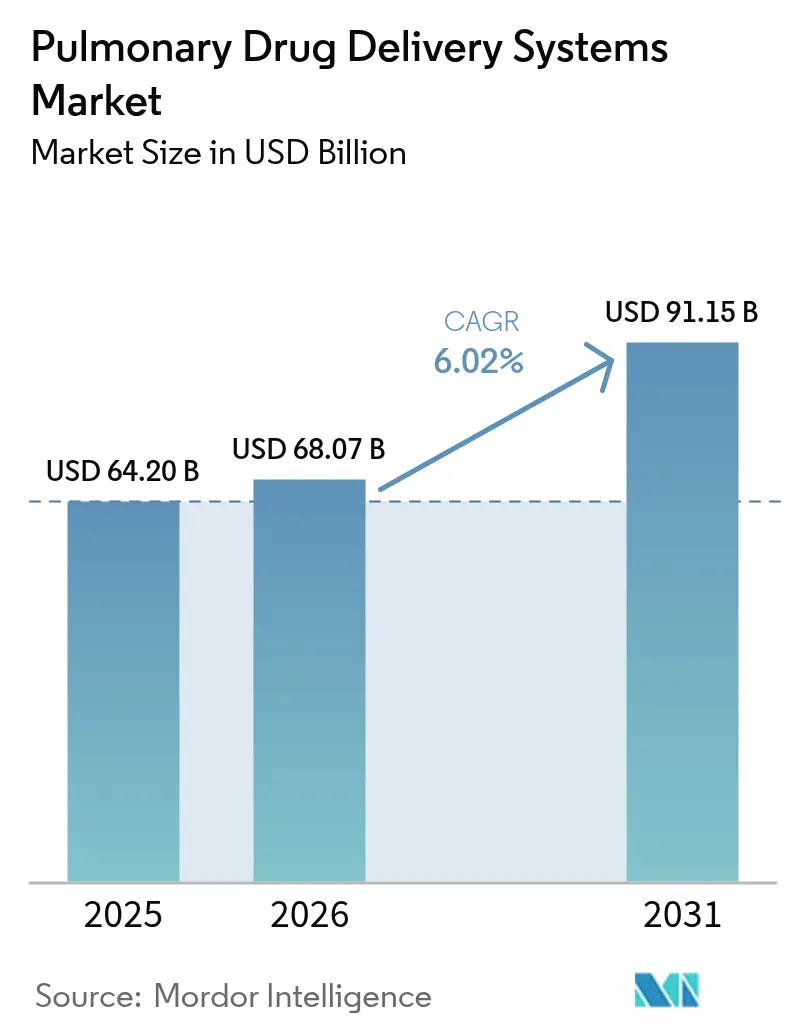

| Market Size (2026) | USD 68.07 Billion |

| Market Size (2031) | USD 91.15 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

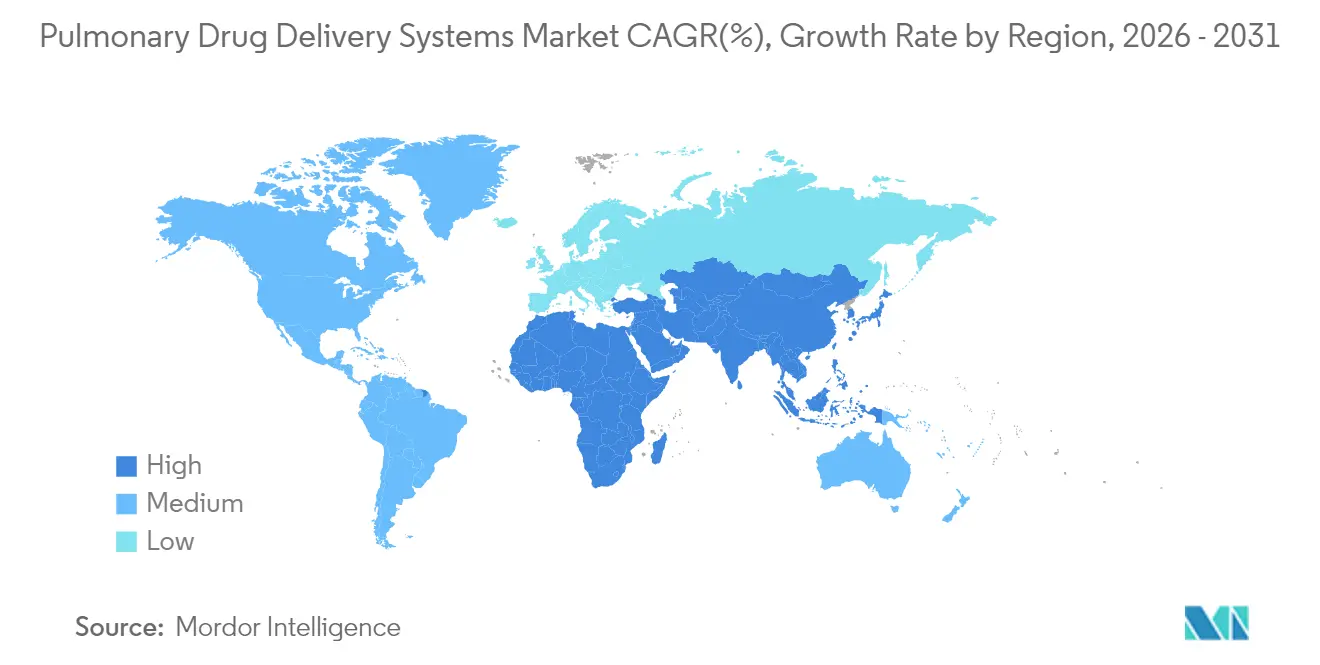

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pulmonary Drug Delivery Systems Market Analysis by Mordor Intelligence

The pulmonary drug delivery system market size was valued at USD 64.20 billion in 2025 and estimated to grow from USD 68.07 billion in 2026 to reach USD 91.15 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). This pulmonary drug delivery system market size expansion reflects steady technology gains, demographic aging, and a global shift toward at-home respiratory care. Device makers are embedding sensors, AI-powered dose counters, and cloud dashboards into familiar inhalers, enabling physicians to track adherence in real time. Environmental rules that mandate low-GWP propellants are catalyzing rapid reformulation programs, creating a multi-billion-dollar pipeline for climate-friendly inhalers. Breakthroughs in mRNA and gene-therapy aerosols are widening the therapeutic canvas, opening possibilities that go well beyond conventional asthma and COPD management. Asia Pacific’s fast-expanding patient base and supportive procurement policies keep the region on a double-digit growth path, while North America retains leadership through sizeable R&D budgets and early digital adoption.[1]American Lung Association, "COPD Trends Brief - Burden," lung.org

Key Report Takeaways

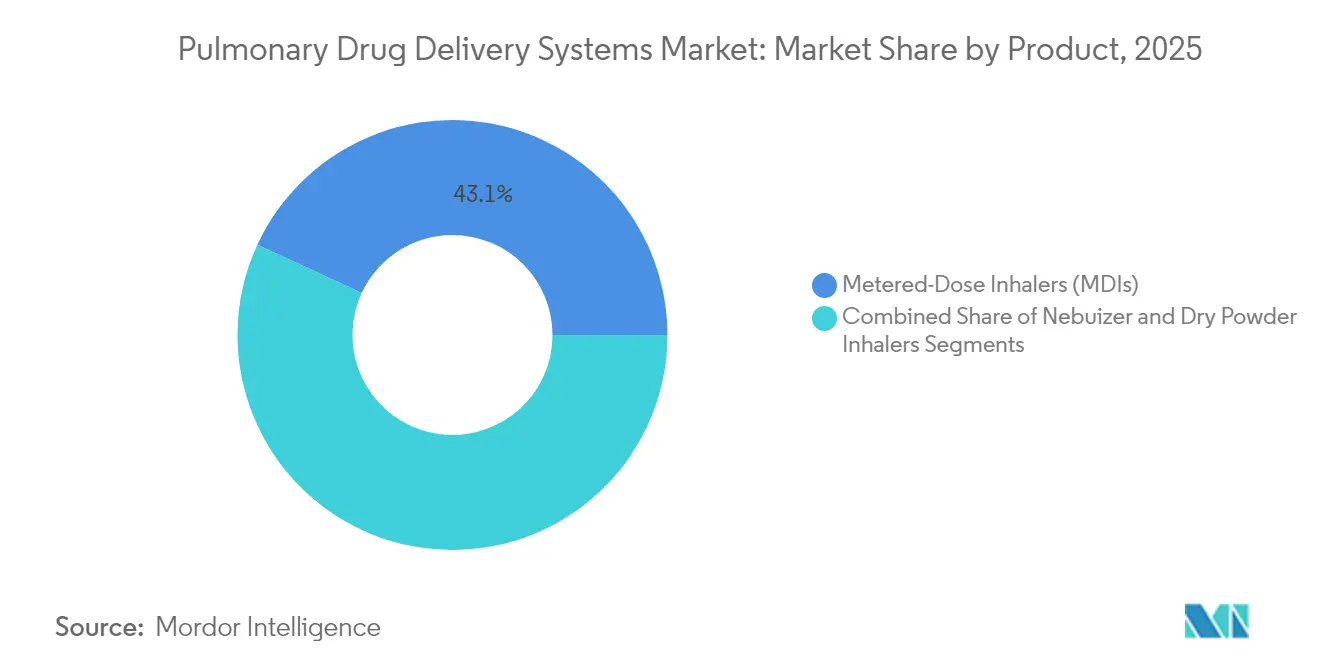

- By product type, metered-dose inhalers led with 43.10% of the pulmonary drug delivery system market share in 2025, whereas dry-powder inhalers are set to post the fastest 9.12% CAGR through 2031.

- By application, asthma captured 39.05% share of the pulmonary drug delivery system market size in 2025; cystic fibrosis is forecast to expand at an 8.31% CAGR to 2031.

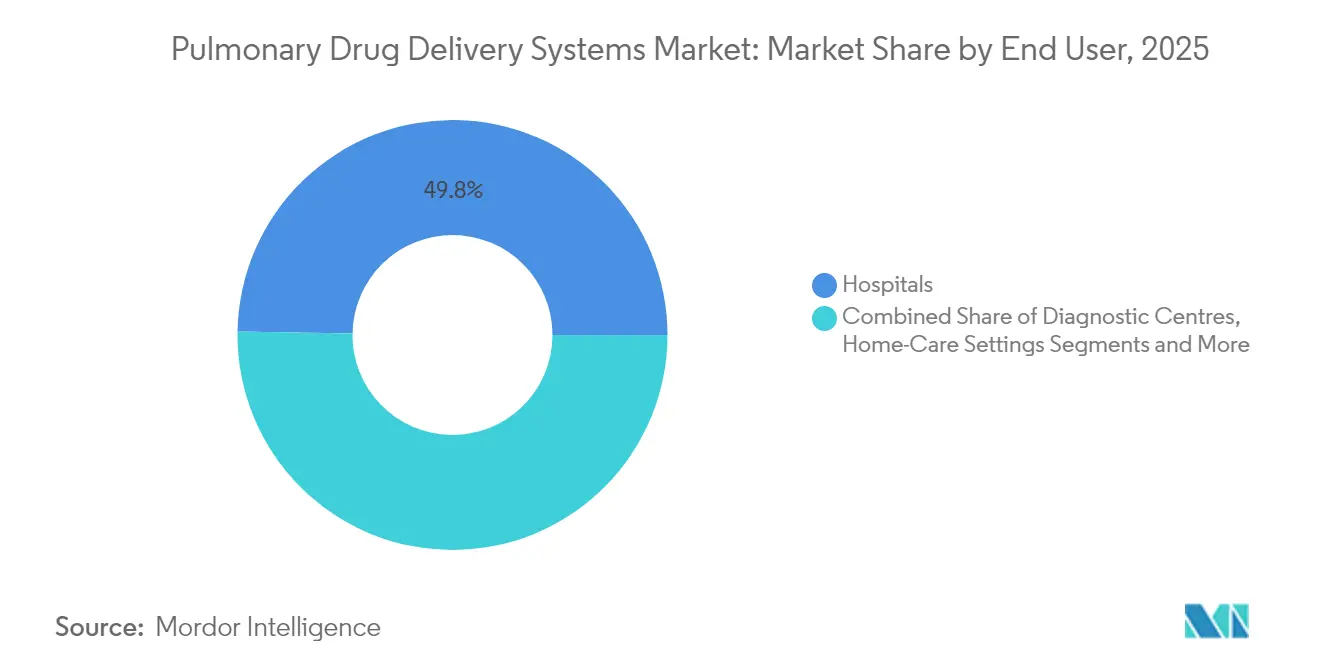

- By end user, hospitals held the largest portion with 49.75% of the pulmonary drug delivery system market in 2025, while home care is projected to accelerate at 10.05% CAGR by 2031.

- By technology, manually-operated devices controlled 67.60% revenue in 2025; digitally enabled smart devices will grow at 10.42% CAGR to 2031.

- By geography, North America commanded 45.10% share of the pulmonary drug delivery system market in 2025; Asia Pacific is the fastest-growing region at a 9.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pulmonary Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in device engineering | +1.2% | Global, early uptake in North America & EU | Medium term (2-4 years) |

| Rising respiratory-disease burden & shift to inhalation route | +1.8% | Global, high in APAC and emerging markets | Long term (≥ 4 years) |

| Ageing population & chronic-care adherence push | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Environmental regulations spurring propellant-free inhalers | +0.7% | EU & UK leading, North America following | Medium term (2-4 years) |

| mRNA / gene-therapy pipelines targeting lung delivery | +0.5% | North America & EU | Long term (≥ 4 years) |

| Home-based smart, prefillable inhalers for connected care | +0.8% | Global, highest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Device Engineering

Smart actuators, breath-actuated triggers, and vibrating mesh nebulizers now deliver more drug into the small airways than earlier jet models, improving the sub-5 µm particle fraction from 54.6% to 59.25%. The FDA clearance of Adherium’s Smartinhaler adds real-time adherence feeds for Airsupra and Breztri, giving clinicians objective dose data. Meta-analysis confirms that vibrating mesh systems outperform jet nebulizers in COPD care, lowering exacerbations and treatment time.[2]Feng Zhouzhou, "Comparison of the Application of Vibrating Mesh Nebulizer and Jet Nebulizer in Chronic Obstructive Pulmonary Disease: A Systematic Review and Meta-analysis," pubmed.ncbi.nlm.nih.gov Manufacturers are testing AI modules that adjust flow rates in response to a patient’s inspiratory profile, a feature that improves pediatric and geriatric outcomes. These engineering gains make inhalers easier to train on, reducing technique errors and hospital readmissions.

Rising Respiratory-Disease Burden & Shift to Inhalation Route

COPD affected 213.39 million people in 2021 and accounted for 4.0 million deaths, solidifying inhalation as the preferred route for both symptom relief and preventive care. China alone reports 45.7 million asthma and 99.9 million COPD patients, a volume that strains clinical capacity and lifts demand for devices that deliver drug directly to the lungs. Air pollution contributes 41.79% of COPD burden among young adults, pushing governments to subsidize inhaled therapies. Benralizumab, the first major asthma-COPD advance in five decades, demonstrated a 30% drop in treatment failures versus steroid regimens, reinforcing the relevance of targeted pulmonary delivery. Payers see inhaled formulations as a path to fewer systemic side effects and shorter hospital stays, underpinning formulary shifts toward aerosol products.

Ageing Population & Chronic-Care Medication Adherence Push

Only 40.9% of surveyed COPD patients exhibit high adherence, with older age a key predictor of missed doses. Digital inhalers have shown a three-point gain in asthma-control scores and lowered severe flare-ups, proving that feedback loops can reshape behavior. The albuterol Digihaler study confirmed that 78% of at-home inhalations generated analyzable flow data, letting physicians coach users remotely.[3]Nature Editorial Team, "Uncovering patterns of inhaler technique and reliever use: the value of objective, personalized data from a digital inhaler," nature.comHome nebulization now ranks high in patient satisfaction surveys among elderly COPD cohorts, especially those unable to coordinate pMDI use.[4]Talwar Deepak, "The Emerging Role of Nebulization for Maintenance Treatment of Chronic Obstructive Pulmonary Disease at Home," journals.lww.com These shifts align with value-based care models that reward outcomes, turning simple adherence tools into powerful market differentiators.

Environmental Regulations Spurring Propellant-Free Inhalers

The EU’s F-gas rulebook is forcing industry to replace hydrofluoroalkanes with low-GWP options such as HFC-152a and HFO-1234ze(E), slashing carbon footprints by up to 99%. AstraZeneca’s Trixeo Aerosphere won UK approval with the new propellant, setting a template for global filings. Dry-powder inhalers and reusable soft-mist devices already meet carbon goals without pressurized gases and could sidestep costly valving redesigns. Early movers enjoy positive brand equity and faster regulatory pathways, though reformulation programs often exceed USD 100 million per molecule. Hospitals and payers are adding sustainability metrics to tenders, accelerating demand for green inhalers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdiction device & drug-combo approvals | -0.8% | Global, complex in EU & US | Medium term (2-4 years) |

| Propellant phase-out costs & supply bottlenecks | -0.6% | Global, highest in EU | Short term (≤ 2 years) |

| Reimbursement uncertainty for digital add-on sensors | -0.4% | North America & EU | Medium term (2-4 years) |

| Micro-plastic & lithium-ion waste scrutiny on disposables | -0.3% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Jurisdiction Device & Drug-Combo Approvals

Combination inhalers must satisfy both drug efficacy and device-performance tests, prolonging development cycles by years and inflating trial budgets. Intellectual-property overlaps around actuator geometries complicate generic entry, limiting price relief in many regions. Digital add-ons invite an additional layer of software validation, often triggering separate submissions under medical-device directives. Smaller firms lack capital to navigate dual pathways, risking innovation attrition and narrowing patient choice.

Propellant Phase-Out Costs & Supply Bottlenecks

Europe has already experienced salbutamol shortages in 21 member states as manufacturers re-tool pMDI lines for new propell ants. The Flovent phase-out lifted patient out-of-pocket costs from USD 14 to USD 25 per month, a jump that could depress adherence in price-sensitive segments. Reformulation costs range from USD 100–200 million per product, including stability tests and bioequivalence studies. Manufacturers face a race to secure HFC-152a and HFO-1234ze(E) allocations, with early movers gaining supply-chain advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Innovation Drives Competitive Dynamics

Metered-dose inhalers claimed 43.10% of the pulmonary drug delivery system market share in 2025 but face mounting environmental pressure to replace high-GWP propellants with sustainable alternatives. Dry-powder inhalers are gaining ground at 9.12% CAGR through 2031, appealing to elderly patients who struggle with MDI coordination and environmentally conscious consumers seeking propellant-free options. Nebulizers remain essential for acute care and patients with limited dexterity, though the segment is shifting from traditional jet models toward advanced vibrating mesh and soft-mist technologies that deliver medication more efficiently.

AstraZeneca's AIRSUPRA launch as the first FDA-approved anti-inflammatory rescue inhaler demonstrates how product innovation can reshape treatment protocols and create new market segments. Soft-mist nebulizers are gaining traction due to their reusable design and reduced environmental impact, with studies confirming 57-71% carbon footprint reduction compared to traditional pMDIs. Ultrasonic nebulizers are experiencing renewed interest as technological advances improve droplet formation control and reduce treatment times, making them particularly valuable for pediatric applications where patient compliance presents challenges. The pulmonary drug delivery system market size for dry-powder inhalers is projected to expand at 9.12% CAGR between 2026-2031, reflecting growing preference for coordination-free devices.

By Application: Therapeutic Breakthroughs Reshape Treatment Paradigms

Asthma applications dominated with 39.05% of the pulmonary drug delivery system market in 2025, reflecting high disease prevalence and established treatment protocols across global healthcare systems. Cystic fibrosis emerges as the fastest-growing application segment with 8.31% CAGR through 2031, driven by breakthrough gene therapy developments including the LENTICLAIR 1 trial testing BI 3720931 inhalable gene therapy across multiple European countries. COPD applications are benefiting from innovative treatments like ensifentrine (Ohtuvayre), which represents the first novel mechanism of action for COPD in over two decades by combining bronchodilator and anti-inflammatory effects. Allergic rhinitis applications are expanding with needle-free delivery systems like Neffy nasal spray for severe allergic reactions, broadening the addressable patient population beyond traditional inhaler users.

The application landscape is undergoing transformation through mRNA and gene therapy innovations, with multiple clinical trials demonstrating the potential for lung-targeted genetic interventions that could fundamentally change treatment paradigms. BioNTech's BNT116 lung cancer vaccine trials across seven countries represent a significant expansion of pulmonary delivery beyond respiratory diseases into oncology applications. Other applications are advancing through specialized formulations, such as novel hyaluronic acid-vancomycin complex powders for pulmonary infections in cystic fibrosis patients, which demonstrate extended release profiles exceeding 24 hours. The pulmonary drug delivery system market size for cystic fibrosis applications is forecast to grow at 8.31% CAGR through 2031, reflecting the impact of these therapeutic innovations.

By End User: Care Setting Evolution Drives Adoption Patterns

Home care settings are advancing at 10.05% CAGR through 2031, outpacing other end-user segments as healthcare systems embrace decentralized care models and patients prioritize treatment convenience. This shift accelerated during the COVID-19 pandemic, which fundamentally altered healthcare delivery preferences by encouraging remote monitoring and telehealth adoption for respiratory disease management. Hospitals maintain their position as the largest end-user segment with 49.75%, leveraging advanced nebulization systems and staff expertise to manage acute exacerbations and initiate treatment protocols. Diagnostic centers are experiencing steady growth as respiratory disease screening becomes more prevalent, particularly in emerging markets where early detection programs are expanding access to care.

The end-user landscape is being reshaped by technological innovations that enable effective home-based therapy management without compromising clinical outcomes. Smart nebulizers and connected inhalers facilitate remote patient monitoring, allowing healthcare providers to track medication adherence and adjust treatment protocols without requiring in-person visits. Home nebulization therapy is gaining acceptance among elderly COPD patients who cannot effectively use handheld inhalers, with studies showing high patient satisfaction rates and improved quality of life outcomes. The transition to home care is supported by reimbursement policy changes that favor cost-effective treatment settings, though challenges remain in ensuring proper device maintenance and patient education in non-clinical environments.

By Technology: Digital Integration Transforms Patient Engagement

Manually-operated devices held 67.60% of the pulmonary drug delivery system market share in 2025, reflecting their established presence and reliability in emergency situations and resource-constrained settings. Digitally-operated smart devices are experiencing rapid adoption with 10.42% CAGR through 2031, driven by healthcare's digital transformation and growing demand for connected health solutions that improve treatment outcomes. This technology shift reflects fundamental changes in patient care expectations, with digital inhalers providing objective data on medication adherence and inhalation technique that enables personalized treatment optimization. Despite clinical guidelines supporting their use, smart inhaler adoption remains low with only 14.5% of adults with moderate to severe asthma prescribed SMART therapy regimens, indicating significant growth potential as awareness and reimbursement improve.

Digital health integration is creating new competitive dynamics within the pulmonary drug delivery system market, with companies developing connected devices such as the Enerzair Breezhaler digital companion for asthma treatment. The technology evolution extends beyond simple connectivity to include artificial intelligence-powered dose optimization and predictive analytics for exacerbation prevention, creating value beyond basic medication delivery. The integration of sensors and connectivity features adds USD 50-100 per device to manufacturing costs, creating pricing pressures that may limit adoption in price-sensitive markets. However, the long-term value proposition of improved adherence and reduced hospitalizations is driving payer interest in covering digital device premiums, supporting continued growth in this segment.

Geography Analysis

North America commanded45.10% of the pulmonary drug delivery system market in2025, benefiting from robust insurance coverage, early uptake of smart inhalers, and swift FDA approvals for breakthrough devices. Recent launches such as AIRSUPRA and Yutrepia sustain demand while public–private R&D programs speed next-generation propellant transitions. Canada and Mexico expand steadily on the back of aging populations and broader access to maintenance therapies, though premium-device use trails the United States.

Asia Pacific is advancing at a9.29% CAGR through2031, propelled by large asthma and COPD pools, widening reimbursement, and local manufacturing that trims device costs. China alone counts45.7million asthma and99.9million COPD patients, driving bulk tenders for dry-powder and mesh-nebulizer systems. India is preparing for Afrezza inhaled insulin, signalling openness to innovative aerosols. Japan, Australia, and South Korea lead regional adoption of connected inhalers as governments push telehealth.

Europe focuses on sustainability, with the UK’s approval of HFO-1234ze(E) propellant inhalers setting a low-carbon benchmark. Germany and France supply critical valve and actuator technology, while EU-wide shortages of salbutamol expose supply-chain risk during propellant changeovers. Eastern Europe, the Middle East & Africa, and South America register rising volumes as funding flows toward air-quality initiatives and local assembly plants.

Competitive Landscape

The pulmonary drug delivery system market is moderately fragmented. AstraZeneca, GlaxoSmithKline, and Boehringer Ingelheim dominate branded therapies and control critical patent estates on propellants and actuator geometries. Philips, PARI, and Omron lead device engineering, pushing vibrating-mesh and soft-mist platforms that cut drug waste and carbon load.

Competition now hinges on two themes: climate-friendly propellants and digital add-ons. Early movers like AstraZeneca finished clinical work for next-generation HFO-based MDIs, gaining a regulatory head start and brand goodwill. Smart-sensor suppliers such as Adherium secure FDA clearances that transform legacy inhalers into connected care tools, creating sticky software-as-a-service revenue.

M&A and licensing remain active as pharma firms seek device know-how and tech companies pursue therapeutic payloads. Regional manufacturers in China and India scale low-cost DPIs, challenging multinationals on price-sensitive tenders. Emerging mRNA and gene-therapy entrants court partners with aerosol expertise to reach distal airways. The result is dynamic rivalry where sustainability credentials, data analytics, and rapid reformulation capacity decide pulmonary drug delivery system market share.

Pulmonary Drug Delivery Systems Industry Leaders

-

Novartis AG

-

Boehringer Ingelheim International GmbH

-

GlaxoSmithKline plc.

-

Cipla

-

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AstraZeneca received UK approval for Trixeo Aerosphere as the first inhaled respiratory medicine using next-generation propellant HFO-1234ze(E) with 99.9% reduction in Global Warming Potential, marking a significant milestone in sustainable inhaler technology and positioning the company as a leader in environmentally friendly respiratory care.

- May 2025: The FDA approved Yutrepia (treprostinil) inhalation powder for treating pulmonary arterial hypertension and pulmonary hypertension associated with interstitial lung disease, utilizing Liquidia's PRINT technology for enhanced deep-lung delivery through a low-effort inhalation device.

- February 2025: Penn Medicine researchers demonstrated breakthrough mRNA therapy for lung repair using ionizable amphiphilic Janus dendrimers, showing potential for healing damaged lungs in lower regions where traditional inhaled medications are ineffective.

- May 2024: DevPro Biopharma and Bespak completed early feasibility studies for DP007, a climate-friendly albuterol inhaler using Honeywell's Solstice Air propellant with 99.9% less global warming potential than current HFAs, with clinical studies planned for late 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the pulmonary drug delivery system market as the global sales value of devices that deposit active pharmaceutical ingredients directly into the lung, namely metered-dose inhalers, dry-powder inhalers, soft-mist inhalers, jet, mesh, ultrasonic nebulizers, and related smart-enabled formats. Products used solely for intranasal, injectable, or oral administration are not included.

Scope exclusion: Stand-alone formulation excipients and single-use spacers without an integrated dose-delivery mechanism are outside the study scope.

Segmentation Overview

-

By Product

- Dry Powder Inhalers

- Metered Dose Inhalers

-

Nebulizers

- Jet Nebulizers

- Soft-Mist Nebulizers

- Ultrasonic Nebulizers

-

By Application

- Asthma

- COPD

- Cystic Fibrosis

- Allergic Rhinitis

- Other Applications

-

By End User

- Hospitals

- Diagnostic Centres

- Home-Care Settings

- Other End Users

-

By Technology

- Manually-Operated Devices

- Digitally-Operated / Smart Devices

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We then interview respiratory physicians, hospital procurement managers, device engineers, and payor advisors across North America, Europe, Asia-Pacific, and Latin America. Their insights refine treated-patient ratios, average selling prices, DPI-pMDI conversion rates, and smart-inhaler adoption curves, allowing us to reconcile desk findings with ground realities.

Desk Research

Our analysts first map the patient and device landscape through tier-1 public sources such as the World Health Organization, the Global Burden of Disease database, the American Lung Association, and regulatory filings from the US FDA and the European Medicines Agency. Trade data from Volza, patent trends extracted via Questel, and company financials on D&B Hoovers complement this foundation, while Dow Jones Factiva tracks product launches and recalls. These sources, among many others, clarify epidemiology, unit production, regulatory shifts, and price points that anchor the model.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-case framework converts COPD, asthma, cystic fibrosis, and allergic rhinitis populations into annual inhaler or nebulizer demand, which is then multiplied by region-specific average device prices. Select bottom-up checks, sampled production volumes, channel audits, and distributor ASPs calibrate totals before final sign-off. Key variables tracked include (1) regional COPD and asthma prevalence, (2) smart-device penetration share, (3) propellant phase-out timelines, (4) average inhaler replacement cycles, and (5) respiratory health care spending per capita. Forecasts employ multivariate regression supplemented by scenario analysis to reflect policy or technology shocks, with gap-filled segments benchmarked against historical shipment patterns.

Data Validation & Update Cycle

Outputs pass a multi-step review: automated anomaly flags, analyst peer checks, and manager approval. Models are refreshed every twelve months, with interim revisions triggered by material events such as major regulatory approvals or pricing shifts, ensuring users always receive the latest vetted view.

Why Our Pulmonary Drug Delivery Systems Baseline Commands Reliability

Published estimates often differ because firms choose dissimilar device lists, pricing anchors, and refresh calendars. Mordor's disciplined scope alignment, dual-path modeling, and annual patient-level refresh mitigate these discrepancies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 64.20 B (2025) | Mordor Intelligence | - |

| USD 55.24 B (2024) | Global Consultancy A | Older base year and exclusion of smart-enabled devices reduces value |

| USD 55.74 B (2024) | Industry Association B | Relies on retail pharmacy sell-through, omitting hospital tender volumes |

The comparison shows that when year alignment, device breadth, and multi-channel volumes are harmonized, Mordor's figure offers the most transparent and decision-ready baseline. Buyers can therefore rely on our numbers to benchmark strategy, allocate R&D budgets, and size investment opportunities with confidence.

Key Questions Answered in the Report

What is driving growth in the pulmonary drug delivery system market?

The market is primarily driven by rising respiratory disease prevalence, technological advancements in device engineering, environmental regulations promoting sustainable inhalers, and increasing adoption of home-based care models that require user-friendly delivery systems.

Which pulmonary drug delivery device type is growing fastest?

Dry-powder inhalers are experiencing the highest growth at 9.12% CAGR through 2031, driven by their propellant-free design, environmental benefits, and ease of use for patients who struggle with coordination requirements of traditional metered-dose inhalers.

How are environmental regulations affecting inhaler technologies?

Environmental regulations are accelerating the transition from high-GWP propellants to sustainable alternatives like HFC-152a and HFO-1234ze(E), which reduce carbon footprint by 85-99% compared to traditional HFA propellants, creating both challenges and opportunities for manufacturers.

Which region leads the pulmonary drug delivery system market?

North America leads with 45.10% market share in 2025, driven by advanced healthcare infrastructure, favorable reimbursement policies, and early adoption of digital health technologies, while Asia Pacific is the fastest-growing region at 9.29% CAGR through 2031.

Page last updated on: