Pharmacy Repackaging Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

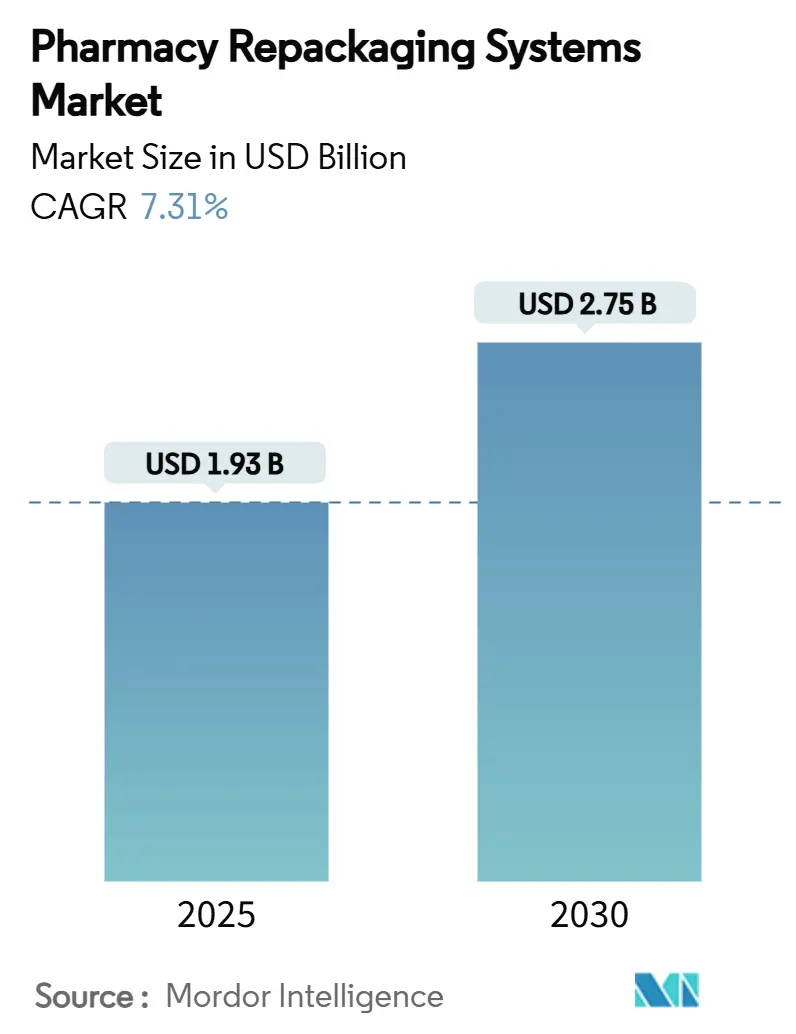

| Market Size (2025) | USD 1.93 Billion |

| Market Size (2030) | USD 2.75 Billion |

| Growth Rate (2025 - 2030) | 7.31% CAGR |

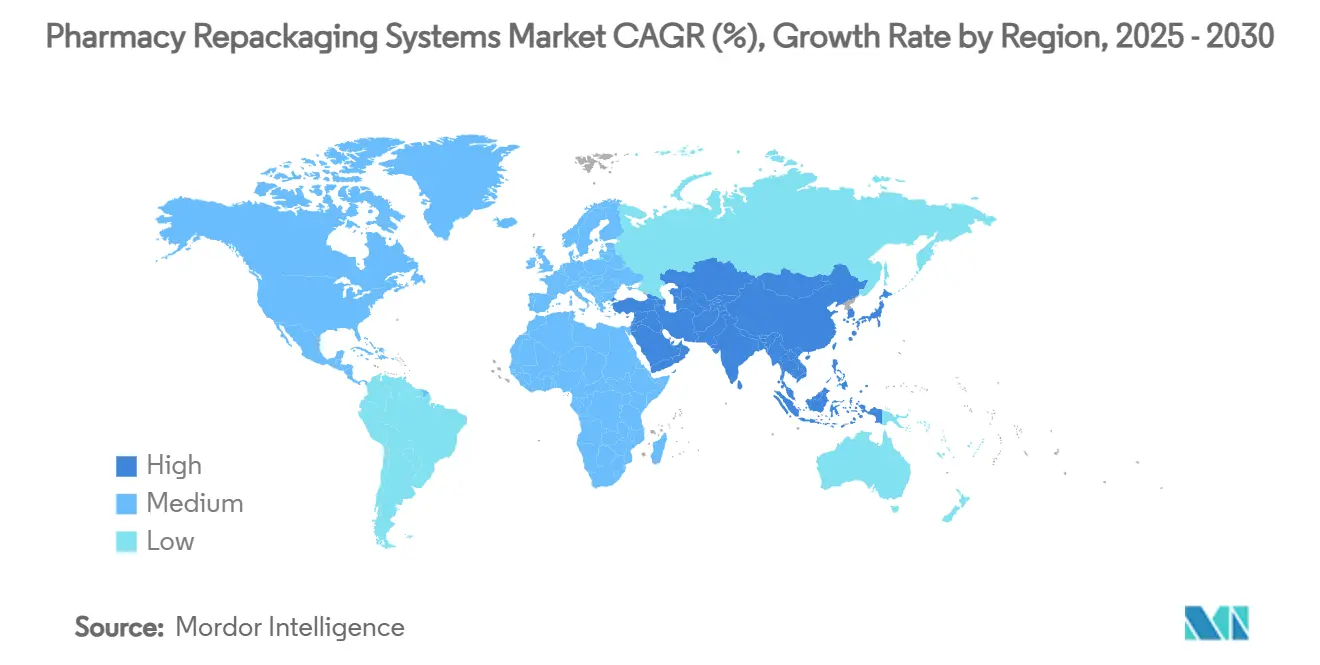

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmacy Repackaging Systems Market Analysis by Mordor Intelligence

The pharmacy repackaging systems market size stands at USD 1.93 billion in 2025 and is forecast to reach USD 2.75 billion by 2030, reflecting a 7.31% CAGR over the period. Demand is being propelled by automation that offsets persistent labor shortages, growing adoption of medication-adherence formats for older patients, and serialization software that satisfies Drug Supply Chain Security Act checkpoints.[1]Food and Drug Administration, “Standards for Securing the Drug Supply Chain,” fda.gov Hospital networks in North America continue to drive early adoption, while Asia-Pacific gains momentum through regulatory harmonization and fresh investment in drug manufacturing capacity.[2]International Society for Pharmaceutical Engineering, “Navigating the Asia-Pacific Pharmaceutical Landscape for Global Impact,” ispe.org In parallel, cloud-native orchestration platforms such as OmniSphere are turning isolated packaging equipment into integrated, data-rich ecosystems. Finally, sustainability goals are encouraging hybrid and recyclable materials that offer barrier protection without raising carbon footprints.

Key Report Takeaways

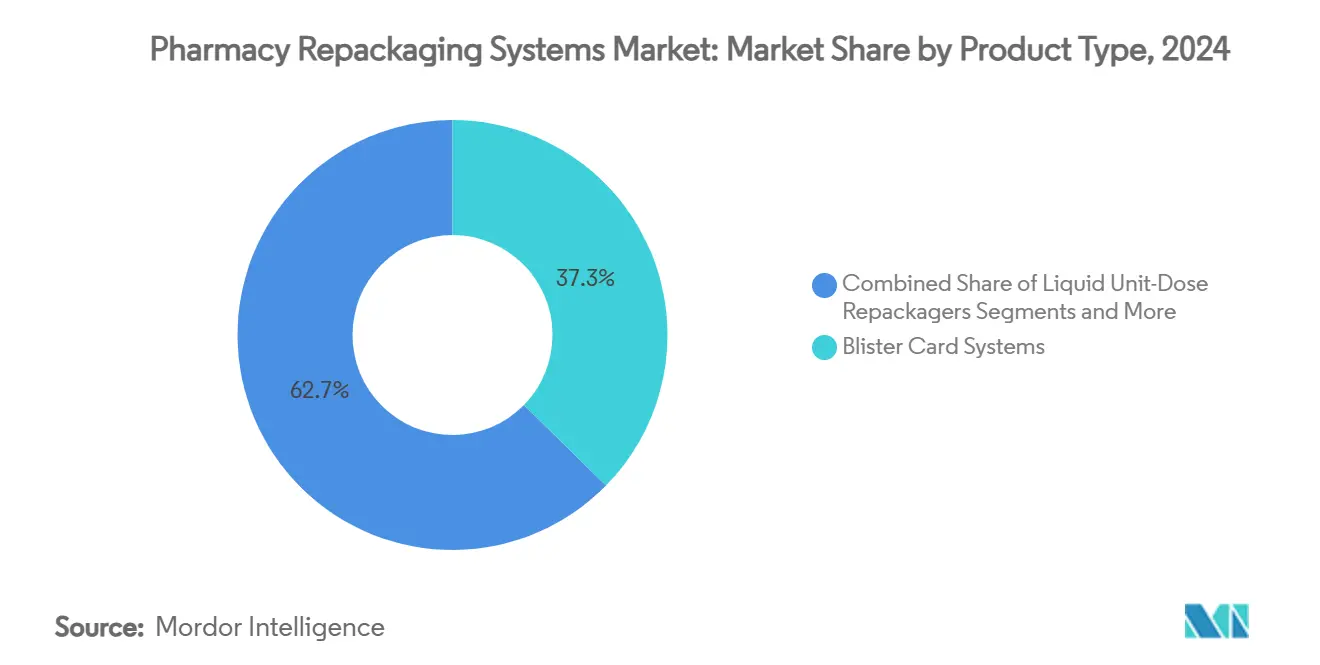

- By product type, unit-dose blister card systems held 37.34% of the pharmacy repackaging systems market share in 2024, while unit-dose pouch solutions are projected to advance at 10.63% CAGR to 2030.

- By automation level, semi-automated carousel platforms commanded 49.53% share of the pharmacy repackaging systems market size in 2024 and fully-automated robotics are expanding at 11.24% CAGR through 2030.

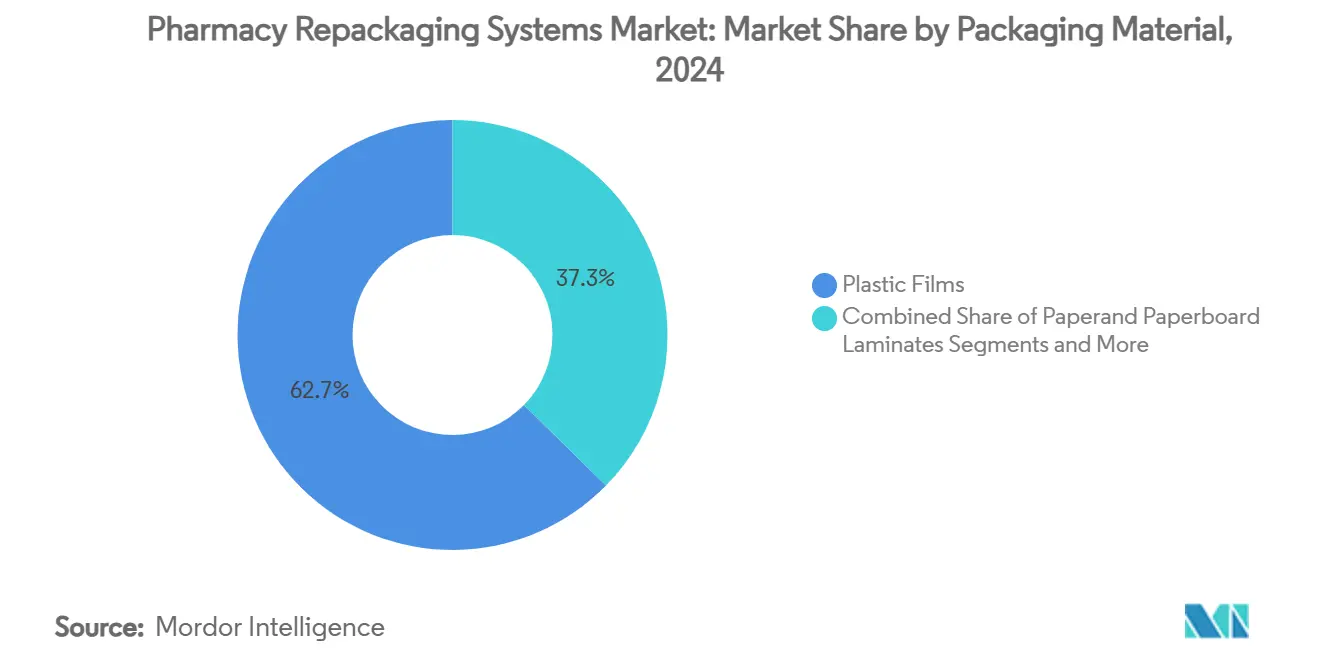

- By packaging material, plastic films dominated with 62.66% revenue share in 2024; hybrid sustainable films represent the fastest trajectory at 9.36% CAGR.

- By end user, hospital pharmacies retained 45.24% share in 2024, whereas mail-order channels are growing at 11.79% CAGR to 2030.

- By geography, North America led with 38.45% share of the pharmacy repackaging systems market in 2024 and Asia-Pacific is forecast to climb at 9.36% CAGR during the outlook window.

Global Pharmacy Repackaging Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medication-adherence packs for ageing societies | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Dose-level bar-coding & serialization | +2.1% | North America, EU, expanding Asia-Pacific | Medium term (2-4 years) |

| Labor shortages in pharmacy workforce | +1.5% | Global; acute in North America & Western Europe | Short term (≤ 2 years) |

| Expansion of mail-order e-pharmacies | +1.2% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| AI-based micro-batching & inventory | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Value-based care incentives for synchronization | +0.6% | North America, pilot Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Medication-adherence packs for ageing societies

Longer life expectancy is placing multiple chronic therapies into the same patient routine, elevating adherence from a convenience to a clinical metric. Automated blister cabinets shorten drug retrieval time by 71% and cut unscheduled deliveries by 96%, saving USD 8,900 per long-term-care facility in BD’s field trial. Hardware makers are consequently launching multi-dose cards that keep compounds stable while simplifying administration schedules. Payers welcome the format because fewer missed doses reduce readmission penalties, especially in capitated reimbursement models. Regions with higher median ages, such as Japan and Northern Europe, have started to write adherence packaging requirements into reimbursement policies, reinforcing sustained demand. Forward-looking pharmacies therefore view adherence packaging as a quality-of-care investment rather than a discretionary expense.

Dose-level bar-coding & serialization

The final DSCSA enforcement milestones in 2025 oblige repackagers to verify, store, and transmit unique product identifiers for each package, a requirement that leaps beyond lot-level tracking. Engineering teams must integrate high-resolution printers, vision inspection, and secure data brokers able to manage large verification volumes. European Falsified Medicines Directive rules are similar, pushing global device makers toward common technical stacks that can be validated across continents. Providers that upgrade early avoid production bottlenecks once wholesalers refuse non-serialized items. Consequently, serialization modules now ship as standard on mid-range carousel lines and are bundled into cloud monitoring suites that flag mismatch errors in real time.

Labor shortages in pharmacy workforce

Vacancy rates for licensed pharmacists and technicians remain elevated, leading hospitals to redeploy personnel toward clinical counseling and away from repetitive filling. Robotic picking arms inside Omnicell’s OmniSphere framework can run through the night, replacing up to three technician shifts while maintaining 0.002% dispensing error rates. Cost savings scale rapidly in urban centers, where wage inflation outpaces automation leasing costs. For independent operators, equipment suppliers have introduced subscription models that convert capital expenditure into operating expense. The shift aligns with workforce planners who prefer reallocating scarce clinicians to vaccination and medication therapy management programs without compromising dispensing throughput.

Expansion of mail-order e-pharmacies

Centralized fulfillment centers rely on high-speed pouch form-fill-seal lines that deliver uniform, tamper-evident sachets ready for shipment. RightHand Robotics reports that its item-handling systems help Apotea lift order capacity by 50,000 parcels per day while sustaining cold-chain integrity for biologics.[3]RightHand Robotics, “Apotea Expands Agreement to Deploy RightPick,” righthandrobotics.com U.S. retail chains mirror this hub-and-spoke model so local pharmacists can focus on patient-facing services. Growth is strongest in rural zones where brick-and-mortar access is limited, making home delivery the default option. Fulfillment operations therefore demand software that synchronizes prescription intake, dynamic batching, and carrier documentation inside a single workflow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & maintenance for automated lines | -1.4% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Stringent validation & GMP documentation | -0.9% | Global | Medium term (2-4 years) |

| Consumable substrate supply volatility | -0.7% | Import-dependent regions | Short term (≤ 2 years) |

| Interoperability gaps with legacy IT | -0.8% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & maintenance for automated lines

Fully robotic fillers often exceed USD 1 million in purchase price, and annual service contracts consume up to 20% of acquisition cost. Smaller community outlets frequently run thin gross margins and cannot spread depreciation over high script volumes. Vendors mitigate the hurdle by offering usage-based rentals that fold hardware, software, and preventive service into a per-dose fee, yet adoption in low-income economies remains limited. Subsidy schemes, where government procurement pools negotiate framework prices, have begun in South Korea and parts of the Gulf region, but coverage is not universal. As a result, the pharmacy repackaging systems market grows unevenly across income tiers.

Stringent validation & GMP documentation

Every software upgrade triggers re-qualification under Good Manufacturing Practice rules, including installation, operational, and performance protocols. The administrative burden stalls system go-live dates by several months and absorbs scarce quality-assurance staff time. Documentation must show complete data integrity, audit trails, and secure user authentication, with FDA guidance warning of warning letters for gaps. Multisite chains handle the process with centralized validation teams, but standalone providers often defer upgrades to avoid paperwork, slowing diffusion of the latest functionality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Blister Leadership Meets Pouch Momentum

Unit-dose blister card equipment generated the largest slice of the pharmacy repackaging systems market in 2024, reflecting 37.34% share as hospitals value its visual verification and barrier strength. Multi-dose configurations extend the same tooling to long-term-care schedules, while vial and bottle lines serve high-volume generics. Hybrid stations now toggle between blisters and bottles without tool changes, ensuring line flexibility. The pharmacy repackaging systems market size for unit-dose pouch machines is forecast to extend at 10.63% CAGR as e-pharmacies standardize on rolls of pouches compatible with sorter conveyors.

Innovations focus on accuracy and speed: TM Robotics’ QPack-1 delivers up to 7,200 vials per hour, a threefold improvement over manual alternatives. Liquid unit-dose repackagers open pediatric and geriatric use cases, though volumes remain niche. Injectable and IV systems require ISO-class cleanrooms, limiting supply to specialized contract service providers. Despite differentiated features, all product categories face the common mandate of unit-level serialization, reshaping hardware and software roadmaps throughout the pharmacy repackaging systems market.

By Automation Level: Semi-Automated Anchors and Robotic Upswings

Semi-automated carousel counters retained 49.53% of the pharmacy repackaging systems market share in 2024, balancing throughput and capital cost. Operators appreciate manageable change-over times, web-based dashboards, and incremental upgrade paths. In contrast, fully robotic cells draw 11.24% CAGR through 2030 as high-volume sites adopt 24/7 lights-out filling modes to offset technician shortages. Predictive maintenance sensors inside these machines alert service teams before mechanical wear slows output, keeping uptime above 99.5%.

Manual benchtop systems still ship into newly founded independent stores or into clinical trial depots where batch size is small. Yet even these units now bundle vision inspection or low-cost serialization printers because DSCSA compliance is non-negotiable. Software orchestration layers such as OmniSphere unify disparate automation tiers under one compliance screen, positioning the pharmacy repackaging systems market for a gradual migration toward full autonomy.

By Packaging Material: Plastic Prevalence and Sustainable Advances

Plastic films captured 62.66% revenue in 2024 thanks to formability and cost-effective sealing temperatures. Cold-form aluminum laminates protect hygroscopic oncology drugs and limit oxygen ingress below 0.01 cc/m², albeit at higher material costs. Paper-based laminates, while eco-friendly, carry moisture-barrier penalties that restrict penetration to vitamins and over-the-counter lines. Hybrid sustainable films, integrating 30% recycled content, record the sharpest 9.36% CAGR as pharma brand owners commit to net-zero goals.

Material choice increasingly intertwines with robotics because seal strength and web tension affect gripper reliability and vision calibration. The pharmacy repackaging systems market therefore sees joint development projects between film suppliers and equipment builders to pre-qualify rollstock. Regulatory agencies in the European Union request life-cycle assessments with product filings, further motivating a switch toward recyclable structures.

By End User: Hospital Core and E-Commerce Rise

Hospital systems owned 45.24% of revenue in 2024 as inpatient medication programs demand multiple dose forms. Integration with electronic health records ensures closed-loop data for dispensing and administration. Specialty oncology centers add sterile repackaging to handle personalized regimens under USP <800> rules. Mail-order and online pharmacies represent the fastest group at 11.79% CAGR, using centralized hubs that feed nationwide distribution grids.

Long-term-care operators adopt synchronization blister cards that simplify nurse rounds and improve inspection compliance. Retail chains rely on micro-fulfillment hubs that feed 3,000–5,000 stores, enabling local pharmacists to deliver vaccinations and medication therapy management. Walgreens reported USD 500 million annual savings after deploying robotic hubs that now service 40% of network scripts. As similar programs multiply, the pharmacy repackaging systems market size for centralized dispensing infrastructure widens.

Geography Analysis

North America contributed 38.45% of global revenue in 2024 on the back of stringent serialization laws and established hospital automation budgets. Cloud platforms allow corporate pharmacy chains to roll software updates across thousands of endpoints overnight, keeping compliance costs predictable. Canada’s single-payer system finances multi-dose programs to reduce hospital readmissions, sustaining unit-dose demand.

Europe ranks second, benefiting from the European Medicines Verification System that pushes pharmacies to scan every pack at patient hand-over. Germany accelerates regional funding for hospital digitization, allocating EUR 4.3 billion, part of which is earmarked for robotics and repackaging. Scandinavian countries pioneer green procurement, preferring sustainable films and pushing local distributors to certify carbon audits, influencing global supplier portfolios.

Asia-Pacific exhibits the highest regional 9.36% CAGR for the pharmacy repackaging systems market through 2030. Korea’s Ministry of Food and Drug Safety subsidizes serialization printers for small pharmacies, while Singapore’s public hospitals standardize carousel systems in new campus builds. NeoX’s AI-OCR prescription reader in Japan illustrates how software overlays are leapfrogging older platforms, achieving 99% transcription accuracy and lifting pharmacist productivity.

Middle East and Africa add smaller but accelerating volumes. Gulf states finance flagship cancer centers that require sterile IV repackagers, whereas Sub-Saharan expansions hinge on donor programs that bundle equipment grants with workforce training. South America sees private hospital networks retro-fitting automation to cut labor costs amid aging urban populations. Across these diverse settings, the pharmacy repackaging systems market continues to tie growth to both public policy and private investment cycles.

Competitive Landscape

The environment is moderately consolidated; the five largest vendors hold a combined share near 60%, placing concentration at a 6 out of 10 score. BD deepened its reach by absorbing Parata Systems and quickly integrated predictive analytics that monitor controlled-substance divergence. Omnicell maintained organic innovation pace with its cloud-native OmniSphere, linking robots, cabinets, and vision inspection under one compliance dashboard.

McKesson broadened automation services by acquiring 80% of PRISM Vision Holdings for USD 850 million, adding retina-focused specialty integration that complements high-speed oral-solid packaging lines. Cardinal Health opened a robotics-powered distribution hub in Fort Worth to support at-home care medication kits, positioning logistics as a differentiator.

New entrants focus on software; Asepha secured USD 4 million to commercialize AI-first pharmacy-operations code that overlays legacy machines without replacing hardware. Itoki’s compact DAP system, recently installed at a regional Japanese chain, proves demand for space-saving pickers that fit tight urban footprints. Such innovations raise competitive pressure on incumbents to refresh portfolios quickly.

Pharmacy Repackaging Systems Industry Leaders

BD

Omnicell Inc.

Swisslog Healthcare

ARxIUM

McKesson Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Itoki Corporation delivered its automated drug-picking system “DAP with MediMonitor” to Kusuri no Fukutaro pharmacy, integrating weight-verified transport to boost accuracy.

- May 2025: Walgreens expanded robotic micro-fulfillment centers to cover 5,000 stores, handling 40% of prescription volume and realizing USD 500 million in annual savings.

- April 2025: McKesson agreed to acquire 80% control of PRISM Vision Holdings for USD 850 million, adding retina and ophthalmology specialty capabilities.

Global Pharmacy Repackaging Systems Market Report Scope

| Unit-Dose Blister Card Systems |

| Unit-Dose Pouch / Strip Packaging Systems |

| Multi-Dose Blister Card Systems |

| Vial / Bottle Repackaging Lines |

| Liquid Unit-Dose Repackagers |

| Injectable / IV Repackagers |

| Manual & Table-top Systems |

| Semi-Automated Carousel & Counter Systems |

| Fully-Automated & Robotic Systems |

| Plastic Films |

| Aluminum Foil / Cold-Form ALU-ALU |

| Paper & Paperboard Laminates |

| Hybrid / Sustainable Films |

| Hospital Pharmacies |

| Retail / Community Pharmacies |

| Long-Term-Care & Assisted-Living Facilities |

| Mail-Order & Online Pharmacies |

| Specialty Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Unit-Dose Blister Card Systems | |

| Unit-Dose Pouch / Strip Packaging Systems | ||

| Multi-Dose Blister Card Systems | ||

| Vial / Bottle Repackaging Lines | ||

| Liquid Unit-Dose Repackagers | ||

| Injectable / IV Repackagers | ||

| By Automation Level | Manual & Table-top Systems | |

| Semi-Automated Carousel & Counter Systems | ||

| Fully-Automated & Robotic Systems | ||

| By Packaging Material | Plastic Films | |

| Aluminum Foil / Cold-Form ALU-ALU | ||

| Paper & Paperboard Laminates | ||

| Hybrid / Sustainable Films | ||

| By End-User | Hospital Pharmacies | |

| Retail / Community Pharmacies | ||

| Long-Term-Care & Assisted-Living Facilities | ||

| Mail-Order & Online Pharmacies | ||

| Specialty Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the pharmacy repackaging systems market in 2025?

The pharmacy repackaging systems market size is USD 1.93 billion in 2025.

What is the growth outlook through 2030?

Revenue is projected to reach USD 2.75 billion by 2030, advancing at a 7.31% CAGR.

Which product format leads global demand?

Unit-dose blister card lines hold the largest 37.34% share of global spending.

Which end-user segment is growing fastest?

Mail-order and online pharmacies show the highest 11.79% CAGR through 2030.

What region exhibits the quickest expansion?

Asia-Pacific records the steepest 9.36% regional CAGR owing to regulatory harmonization and fresh manufacturing investment.

Page last updated on: