Security Awareness Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

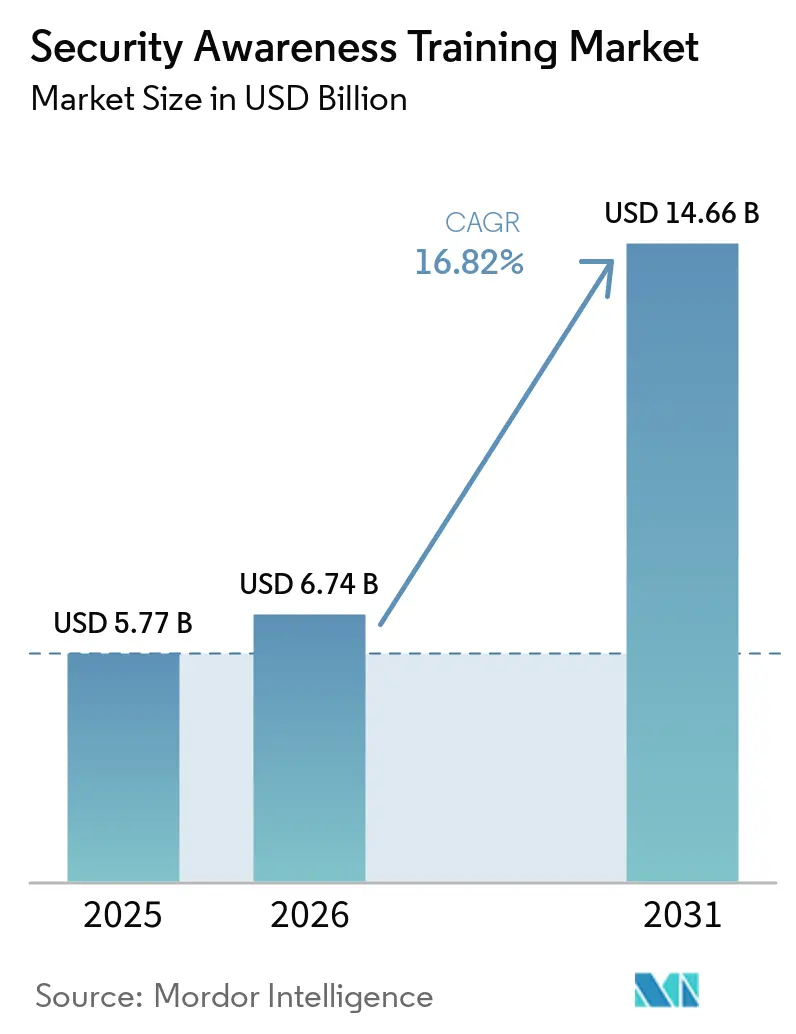

| Market Size (2026) | USD 6.74 Billion |

| Market Size (2031) | USD 14.66 Billion |

| Growth Rate (2026 - 2031) | 16.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

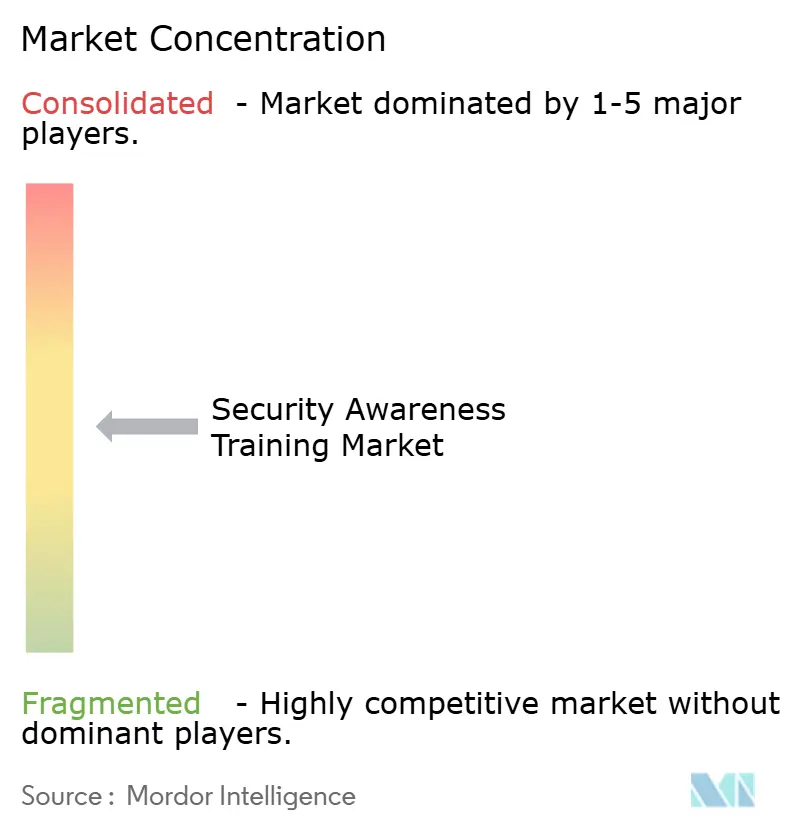

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Awareness Training Market Analysis by Mordor Intelligence

security awareness training market size in 2026 is estimated at USD 6.74 billion, growing from 2025 value of USD 5.77 billion with 2031 projections showing USD 14.66 billion, growing at 16.82% CAGR over 2026-2031. The uptrend reflects intensifying ransomware losses, cyber-insurance mandates that require proof of employee education, and a rapid rise in generative-AI phishing toolkits. Enterprises account for the bulk of current spending, yet small and mid-sized businesses (SMBs) are adopting at elevated rates as cloud delivery removes cost and deployment barriers. Cloud-based courses, micro-learning, and real-time phishing simulations are displacing linear slide decks, while integrated analytics help security leaders quantify risk reduction. Competition is shifting toward full-suite platforms that blend content management, phishing simulation, and behavioral analytics, reinforcing demand for interoperable, API-ready products that slot into broader security stacks.

Key Report Takeaways

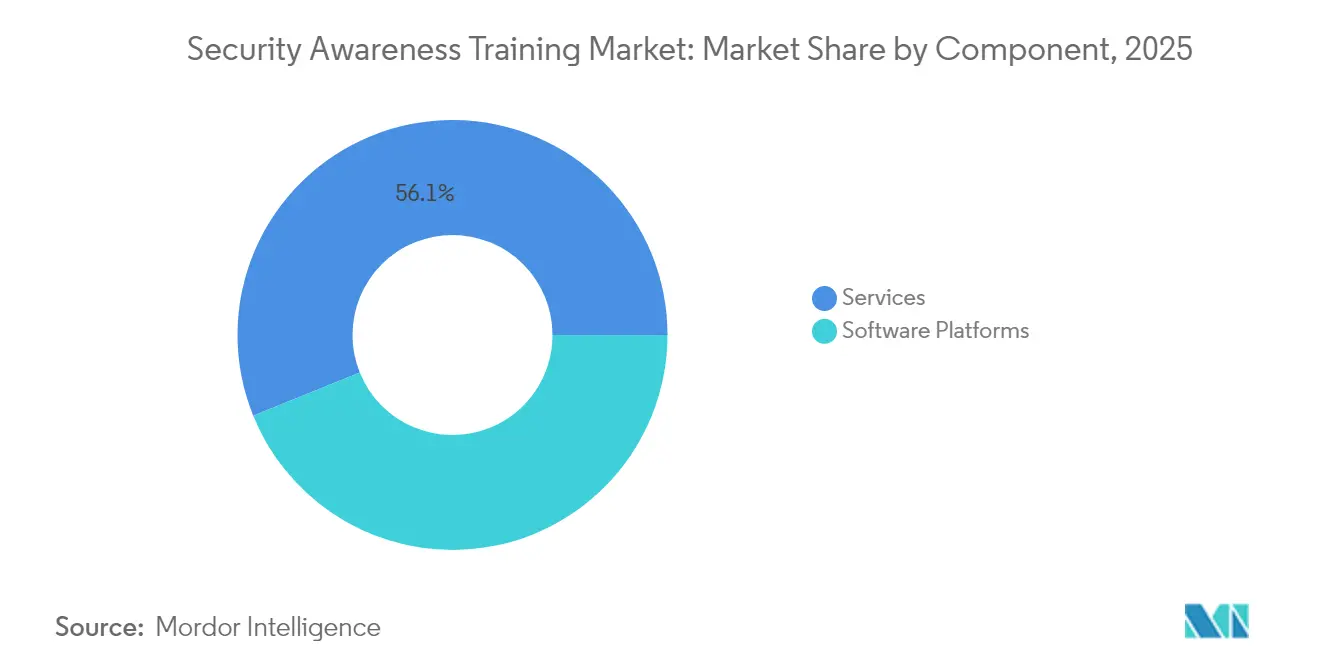

- By component, services led with 56.12% of the security awareness training market share in 2025, while software platforms are expanding at a 19.14% CAGR through 2031.

- By delivery mode, cloud-based offerings captured 73.65% of the security awareness training market size in 2025 and are projected to rise at a 18.72% CAGR.

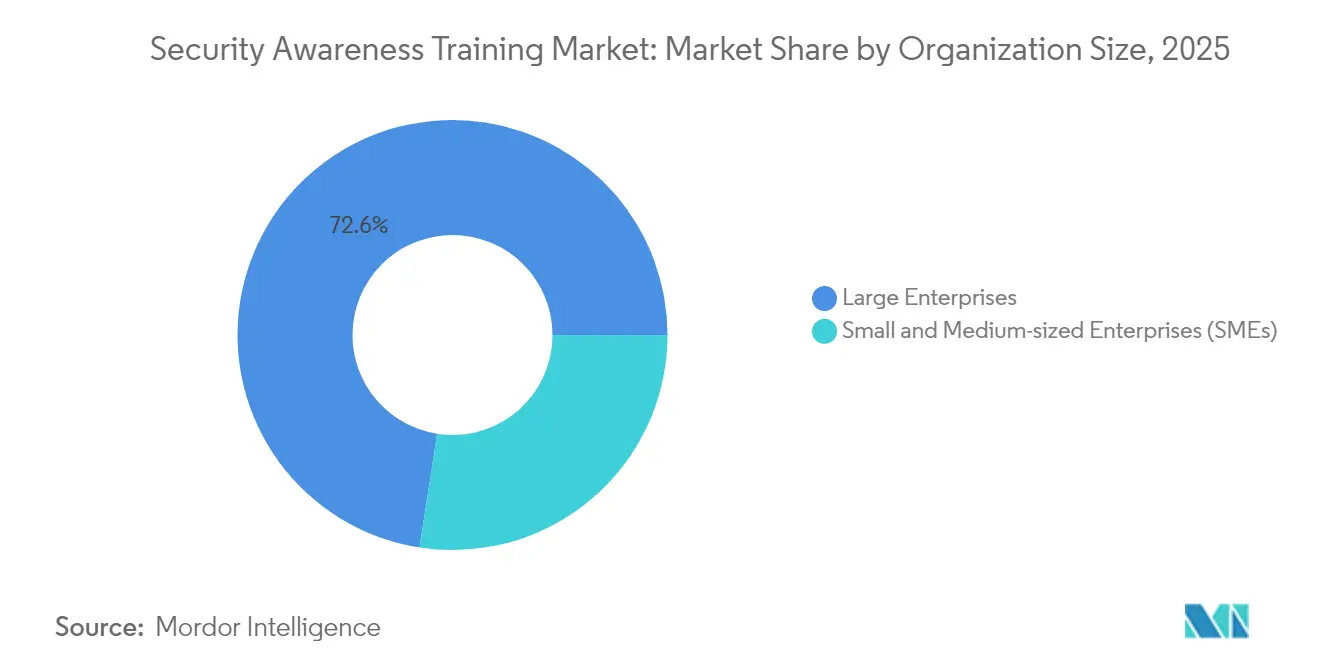

- By organization size, large enterprises retained a 72.55% share of the security awareness training market size in 2025, whereas the SME segment is progressing at a 19.64% CAGR.

- By industry vertical, BFSI generated 28.15% of the security awareness training market share in 2025; healthcare and life sciences represent the fastest growth, advancing at a 18.83% CAGR to 2031.

- By geography, North America held 37.78% of the security awareness training market in 2025, while Asia-Pacific is forecast to log a 18.61% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Awareness Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ransomware and business-email-compromise (BEC) losses | +4.2% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Accelerating cyber-insurance premium hikes requiring employee training proof | +3.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Rapid SaaS adoption by SMBs pushing cloud-native security tools | +3.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of zero-trust architecture programs across enterprises | +2.7% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| ISO/IEC 27001:2022 updates adding people-centric controls | +2.4% | Global, with EU leading compliance adoption | Medium term (2-4 years) |

| Generative-AI-powered phishing kits lowering attack barriers | +4.1% | Global, with sophisticated attacks targeting developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Ransomware and Business-Email-Compromise (BEC) Losses

Ransomware payouts averaged USD 2.73 million in 2024, and manufacturing firms absorbed 68% of industrial incidents in Q1 2025. [1]Manufacturing.net, “Wave of Ransomware Groups Targeting Manufacturing,” manufacturing.net The FBI records BEC losses of USD 43 billion between 2016-2021, driving urgent board-level focus on employee vigilance programs. Healthcare providers lose an estimated USD 2 million daily to cyberattacks, with human error responsible for most breaches. A single click on a malicious link at Evolve Bank and Trust exposed 33 TB of data, underscoring the cost of inattentive staff. Organizations running year-long, high-frequency training saw phish-prone rates fall from 34.3% to 4.6%, validating budget shifts toward human-risk-management platforms.

Accelerating Cyber-Insurance Premium Hikes Requiring Employee Training Proof

Premiums climbed rapidly over the past decade, and insurers now run deep posture checks before issuing coverage. Policies routinely demand quarterly phishing-simulation metrics and certificates of completion, rewarding firms that can verify program engagement with premium discounts that reach 20%. SMB adoption is pushed by underwriters as 82% faced ransomware in 2024. Those meeting minimum awareness standards accessed broader coverage limits while cutting breach-related losses by USD 5.4 million on average. Providers able to integrate loss-data reporting tools enhance their value to both clients and carriers, carving out a secure revenue stream within the security awareness training market.

Rapid SaaS Adoption by SMBs Pushing Cloud-Native Security Tools

More than half of SMB executives cite cybersecurity as their top IT priority, and 81.8% expect higher technology budgets for 2025. [2]Cisco Systems, “Why SMBs Put Security First,” cisco.com Cloud-first application stacks widen the attack surface, so SMBs look for browser-based awareness suites that plug directly into collaboration and email services. Pay-as-you-go subscription models make enterprise-grade phishing simulation and AI-driven micro-learning financially viable, facilitating 67% mobile-learning uptake and boosting completion rates by 50%. Vendors that pre-integrate with popular SaaS ecosystems broaden addressable demand and elevate retention rates inside the security awareness training industry.

Expansion of Zero-Trust Architecture Programs Across Enterprises

NIST’s reference architecture stresses that technical controls alone cannot secure identities without parallel behavior change. The U.S. Department of Defense now runs a structured curriculum covering graduated levels of zero-trust know-how, reaffirming culture as a core pillar of projects worth billions. Adoption across healthcare is particularly visible because 93% of organizations reported past breaches, and patient safety implications bring training under clinical governance rather than IT alone. As enterprises convert to continuous-verification workflows, awareness programs shift from annual slides to just-in-time nudges embedded in daily activity, increasing stickiness for platform providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| End-user fatigue from excessive mandatory trainings | -2.8% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Budget reallocations toward XDR and SASE platforms | -3.4% | North America and EU core, emerging in APAC | Medium term (2-4 years) |

| Inconsistent global privacy regulations limiting data analytics | -2.1% | Global, with varying intensity across EU, North America, and APAC | Long term (≥ 4 years) |

| Talent shortage in content-localization and cultural-nuance design | -1.9% | Global, most acute in APAC and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

End-User Fatigue from Excessive Mandatory Trainings

Proofpoint research shows 68% of workers knowingly break policy despite being aware of the risk, illustrating a saturation point where more modules no longer translate into safer conduct. [3]Proofpoint Inc., “Proofpoint’s 2024 State of the Phish Report,” proofpoint.com Over-frequent sessions can induce a checkbox mentality, and generic content that lacks job relevance erodes engagement. Security teams must rethink cadence and personalize scenarios to sustain attention; otherwise, adoption metrics slip, and ROI diminishes. Gamified simulations, micro-lessons, and role-specific stories have proven effective in restoring impact while trimming total screen time.

Budget Reallocations Toward XDR and SASE Platforms

A growing share of 2025 security budgets is flowing toward automated detection suites that promise measurable MTTR gains. Thirty-six percent of CISOs report cuts to training funds, often to finance converged XDR stacks. Although 95% of breaches still involve human error, board-level appetite for tool consolidation is high, squeezing discretionary spend on employee education. Awareness providers now counter this dynamic by bundling API connectors and shared dashboards to demonstrate direct input into SOC metrics, helping justify their slice of the security wallet inside the security awareness training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Maintain Primacy as Platforms Accelerate

Services captured 56.12% of the security awareness training market in 2025, buoyed by enterprises that outsource content localization, campaign orchestration, and behavioral analytics to specialist partners. Managed programs continuously refresh modules against live threat intel, a requirement that many internal teams cannot scale. Yet software platforms are climbing at a 19.14% CAGR as organizations standardize on centralized consoles to reduce administrative overhead. KnowBe4 now supports 65,000 customers with AI-suggested modules and automated scheduling that frees up security staff. Hybrid consumption is maturing: firms launch with managed packages, then shift workload to internal administrators once competence grows, sustaining dual-track demand in the security awareness training market.

The services cohort differentiates on the depth of localization, industry-specific scenario design, and threat intelligence feeds from mail-security telemetry. Platform vendors, by contrast, compete on user-experience metrics and breadth of integrations from identity systems to HR records. Both models increasingly offer REST APIs so risk scores can feed GRC dashboards. This interoperability imperative reinforces a platform-centric future, even as content and professional-services lines remain vital for nuanced cultural adaptation.

By Delivery Mode: Cloud Centricity Reshapes Access

Cloud products represented 73.65% of the security awareness training market size in 2025 and are projected to rise at a 18.72% CAGR as hybrid work persists. Automatic content updates, single sign-on, and mobile apps raise completion rates compared with legacy on-premise learning-management systems. Corporate e-learning studies show 67% of firms integrate mobile delivery and achieve 50% higher pass-through rates. On-premise implementations still occupy niches where data-sovereignty laws or air-gapped networks prevail, notably in defense and certain public-sector agencies.

Vendors now offer split-deployment modes: sensitive payloads remain behind firewalls while front-end portals run in the vendor’s multitenant cloud. Such architectures let governments meet residency mandates yet still exploit global content pipelines. The mix of SaaS ease and regulated-host controls sustains momentum, reinforcing the cloud’s central role in the security awareness training market.

By Organization Size: SMEs Close the Gap

Large enterprises owned 72.55% of the security awareness training market share in 2025, underscoring compliance-driven procurement cycles and multi-geography rollouts. Nevertheless, SMEs are the fastest-growing cohort at 19.64% CAGR as cyber insurers demand proof of employee education before issuing policies. SMB leaders increasingly cite cybersecurity as their top IT line item, and browser-based suites are price at levels aligned with constrained budgets. AI-driven phishing simulators that auto-generate role-specific lures lower the operational overhead traditionally associated with awareness programs.

Platform providers craft “starter” SKUs restricted to 250 seats with one-click campaign templates, easing first-time adoption. Partnerships with cyber-insurance brokers further accelerate channel traction by embedding training in policy onboarding checklists. The democratization of feature sets shrinks capability gaps across organization sizes, broadening total addressable demand for the security awareness training industry.

By Industry Vertical: Healthcare Momentum Narrows BFSI Lead

BFSI contributed 28.15% of the security awareness training market size in 2025 due to stringent operating regulations such as PCI DSS and the EU Digital Operational Resilience Act, both of which oblige routine staff training. Healthcare now logs the quickest uptake at a 18.83% CAGR after successive headline breaches, including a 13.4 million-record exposure at Kaiser Permanente. Patient-care disruptions sharpen executive focus on staff behavior, turning awareness spending from discretionary to mission-critical outlay.

Manufacturing follows closely because ransomware can halt production lines, with phishing still the primary infection vector. Public-sector, IT-telecom, and retail chains also escalate investments to meet data-privacy mandates and mitigate supply-chain risks. Content customization for operational-technology environments and point-of-sale systems is a growing differentiator among providers eager to court vertical niches within the security awareness training market.

Geography Analysis

North America held 37.78% of the security awareness training market in 2025, thanks to early adoption and dense vendor presence. Phish-prone levels fell from 34.3% to 4.6% in many U.S. deployments that maintained frequent simulations. Cyber-insurance discounts reinforce program continuation, yet user fatigue threatens efficacy if content cadence is not optimized. Canada and Mexico exhibit mid-teen growth as regulatory frameworks tighten around critical-infrastructure operators.

Asia-Pacific is expanding at a 18.61% CAGR on the back of digital-government pushes and high incident volume; the region absorbed 31% of global cyberattacks in 2024. Hong Kong saw phishing complaints more than double, with AI-generated lures raising risk awareness among enterprises. Localization, bilingual modules, and regional compliance content propel sales momentum for both global and domestic vendors.

Europe grows steadily, anchored by GDPR, NIS2, and DORA mandates that set minimum training standards across finance and critical infrastructure. ENISA notes that firms allocate 9% of IT budgets to information security, supporting stable investment pipelines. Strict data-privacy constraints do require adaptations; analytics tied to individual behavior must anonymize or aggregate data to comply, influencing feature roadmaps of providers active in the security awareness training market.

Competitive Landscape

Moderate fragmentation characterizes the sector. KnowBe4, Proofpoint, and Cofense occupy leadership tiers with integrated suites that combine phishing simulation, adaptive micro-learning, and risk scoring. Vista Equity’s 2024 buyout of KnowBe4 infused capital for accelerated R&D and subsequent Egress acquisition, layering cloud email security onto its awareness stack. Proofpoint leverages threat-intelligence feeds from its email-security sensors to tailor attack themes and timing, while Cofense positions its managed phishing-incident-response service as a differentiator for regulated clients.

Market consolidation continues: Mimecast purchased Elevate Security to incorporate behavioral analytics, and partnerships such as KnowBe4-Harmonic Security blend GenAI models to automate risk-based content assignment. Start-ups like Hoxhunt and SoSafe deploy gamification and behavioral science to combat user fatigue, eroding incumbent mindshare in pockets such as Europe. Providers focused on SMB value propositions, including Ninjio, capitalize on simplified price points and cartoon-style narratives that resonate with resource-constrained buyers.

Vendors face rising due diligence scrutiny after a 2024 incident in which a North Korean operative was hired as an AI engineer at KnowBe4, illustrating the importance of internal controls even inside specialist firms. Strategic roadmaps now emphasize transparent supply-chain security and in-house vetting protocols, both as a risk-management necessity and a marketing credential.

Security Awareness Training Industry Leaders

KnowBe4 Inc.

Proofpoint Inc.

Cofense Inc.

Terranova Security (Terranova WW Corp.)

SANS Institute (Escal Institute of Advanced Technologies Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: KnowBe4 and Harmonic Security formed a partnership to trigger dynamic GenAI-powered training aligned with live data-privacy risks.

- April 2025: KnowBe4’s Q1 2025 phishing report found 60.7% of successful lures impersonated internal departments.

- January 2025: The EU Digital Operational Resilience Act went live, obliging financial institutions to roll out specialized staff training.

- January 2025: HKCERT reported a 108% surge in phishing incidents for 2024, prompting local enterprises to expand awareness budgets.

Global Security Awareness Training Market Report Scope

| Software Platforms |

| Services (Content Creation, Managed Programs, etc.) |

| Cloud-Based |

| On-Premise |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| IT and Telecom |

| Retail and E-commerce |

| Manufacturing |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software Platforms | ||

| Services (Content Creation, Managed Programs, etc.) | |||

| By Delivery Mode | Cloud-Based | ||

| On-Premise | |||

| By Organization Size | Small and Medium-sized Enterprises | ||

| Large Enterprises | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the security awareness training market in 2026?

It is valued at USD 6.74 billion in 2026, with a 16.82% CAGR projected through 2031.

Which segment grows fastest within security awareness programs?

Software platforms are advancing at a 19.14% CAGR as firms automate campaign management and reporting.

Why are cyber-insurance firms influencing training adoption?

Underwriters increasingly require proof of quarterly phishing simulations and completion metrics, rewarding compliant clients with premium discounts as high as 20%.

Which region leads spending on staff-focused cybersecurity education?

North America holds 37.78% share today, driven by regulatory obligations and mature vendor ecosystems.

How is zero-trust architecture impacting awareness curricula?

Organizations deploying zero-trust frameworks are shifting from annual slide decks to continuous, context-aware micro-learning aligned with least-privilege principles, making training indispensable for both IT and business users.

Page last updated on: