Education And Research Institutions Cybersecurity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.42 Billion |

| Market Size (2030) | USD 11.07 Billion |

| Growth Rate (2025 - 2030) | 15.35% CAGR |

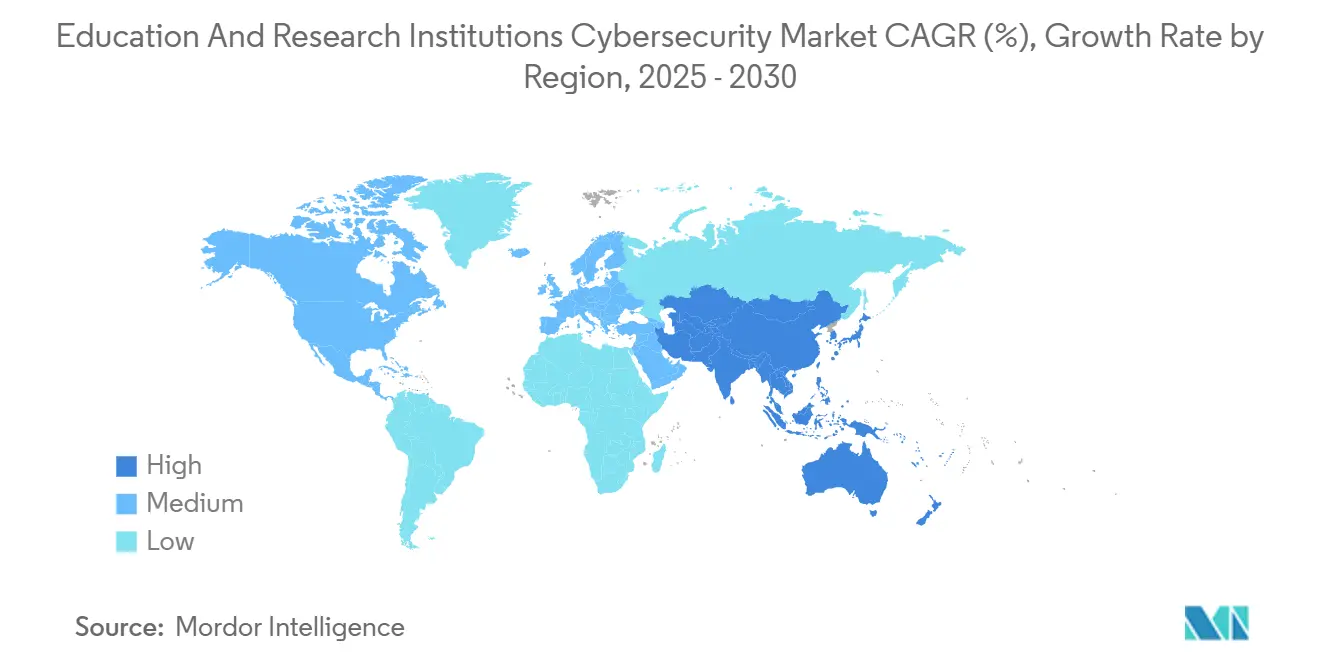

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Education And Research Institutions Cybersecurity Market Analysis by Mordor Intelligence

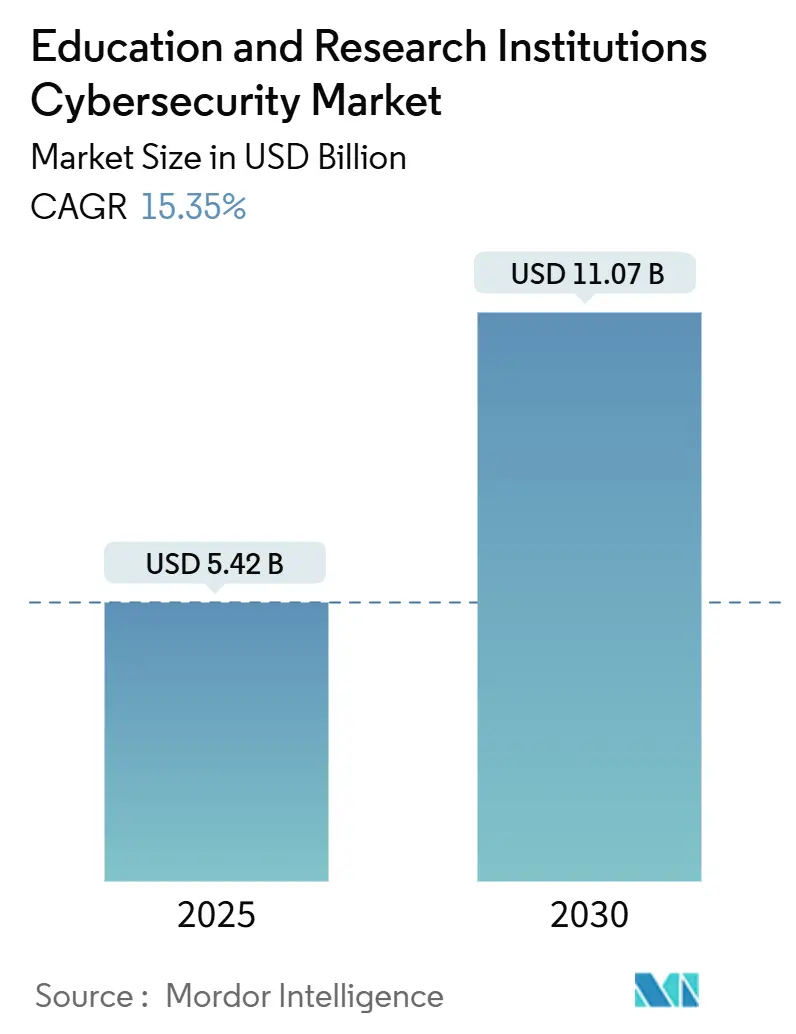

The Education and Research Institutions Cybersecurity market size reached USD 5.42 billion in 2025 and is forecast to rise to USD 11.07 billion by 2030, reflecting a 15.35% CAGR over the period. The surge aligns with a 70% year-on-year jump in ransomware incidents against schools and universities in 2023, prompting institutions to modernize security architectures. Universities now face an average of 2,507 attempted attacks every week, further highlighting the need for layered defenses.[1]EDUCAUSE, “2024 EDUCAUSE Horizon Report,” educause.edu Rapid cloud adoption, with 92% of campuses using cloud services, expands the threat surface and accelerates investment in encryption and key-management solutions.[2]SURF, “Encryption in Microsoft Azure and Amazon AWS Cloud,” surf.nl Identity governance, IoT security, and managed detection are emerging as core budget priorities as institutions balance compliance mandates such as FERPA, GDPR, and CCPA with constrained funding environments.

Key Report Takeaways

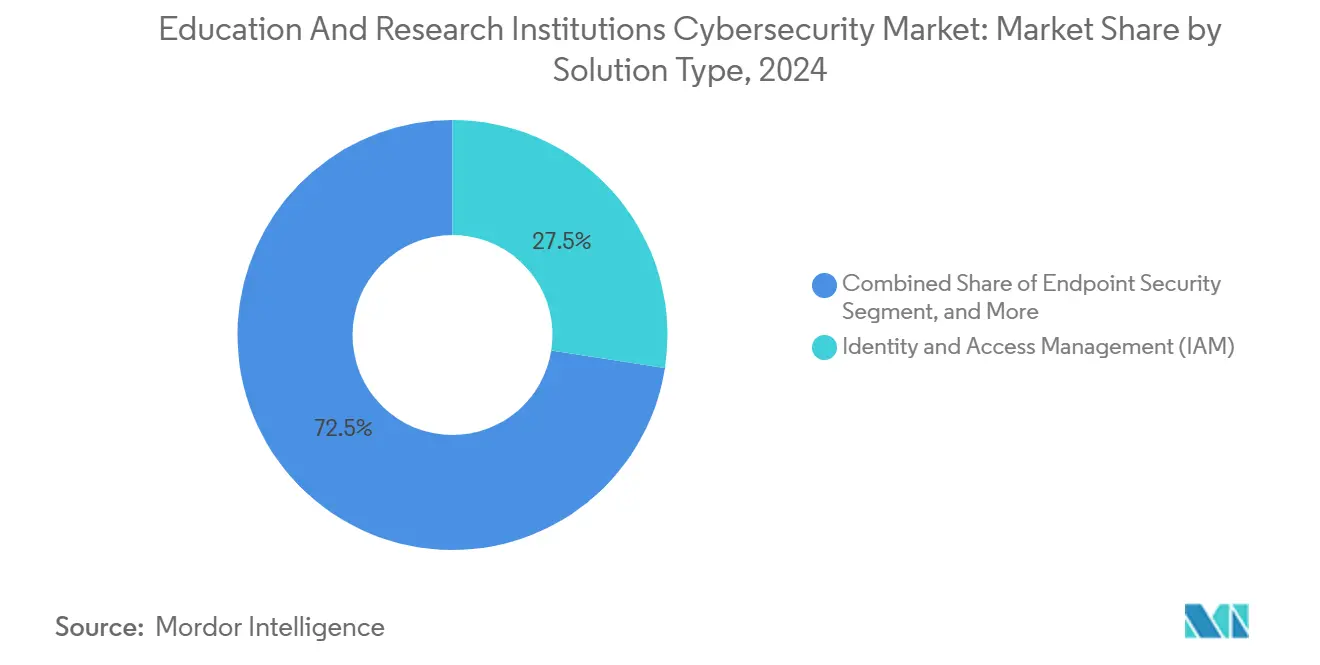

- By solution type, Identity and Access Management commanded 27.46% of Education & Research Institutions Cybersecurity market share in 2024, whereas Security Awareness Training is projected to expand at a 16.83% CAGR through 2030.

- By deployment mode, On-premises deployments accounted for 52.69% of the Education & Research Institutions Cybersecurity market size in 2024, while cloud-based solutions are set to register a 17.05% CAGR between 2025 and 2030.

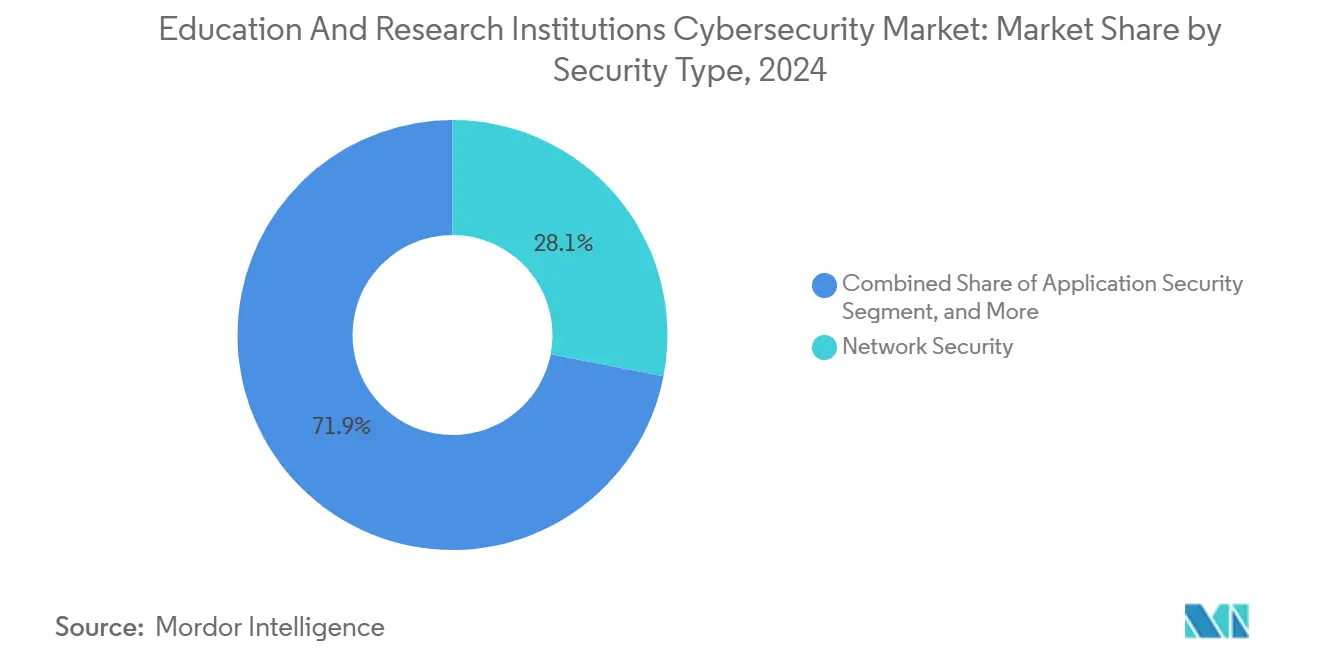

- By security type, Network Security held 28.07% of the Education & Research Institutions Cybersecurity market share in 2024 and Cloud Security is forecast to advance at a 16.04% CAGR to 2030.

- By institution type, Universities and Colleges represented 39.61% of the Education & Research Institutions Cybersecurity market size in 2024, whereas MOOC providers are expected to grow at a 19.52% CAGR during 2025-2030.

- By geography, North America led with 35.85% market share in 2024, while Asia-Pacific is poised for the fastest regional growth at an 18.61% CAGR through 2030.

Global Education And Research Institutions Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating ransomware attacks targeting university networks | +3.2% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Mandatory data-privacy compliance (FERPA, GDPR, CCPA) in education sector | +2.8% | North America & EU primary, APAC emerging | Medium term (2-4 years) |

| Rapid shift to cloud-hosted learning platforms | +2.5% | Global, accelerated in APAC and North America | Short term (≤ 2 years) |

| Proliferation of IoT/OT devices on campus (smart classrooms and labs) | +1.9% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Shortage of skilled cyber talent driving managed-security adoption | +2.1% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Quantum-ready encryption research funding in academia | +1.0% | North America & EU, with emerging activity in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Ransomware Attacks Targeting University Networks

Ransomware volumes rose 70% in 2023, pushing average breach remediation costs to USD 1.42 million per incident. Incidents such as Stanford University’s four-month infiltration and the shutdown of Lincoln College underscore institutional fragility. The FOG ransomware group now pursues higher-education targets using double extortion, exploiting VPN misconfigurations to move laterally. Decentralized network topologies and limited security staff mean 40% of victims require more than a month to restore operations, accelerating zero-trust adoption and advanced endpoint detection procurement.

Mandatory Data-Privacy Compliance in Education Sector

FERPA, GDPR, and CCPA convergence forces institutions to unify policies for student data, research information, and cross-border collaboration. Updated GLBA rules now mandate 24-hour breach notification and demonstrable service-provider oversight, triggering investments in integrated policy management tools. Cloud suppliers such as Microsoft position themselves as “school officials,” offering turnkey compliance frameworks that preserve data sovereignty while easing audit burdens. Smaller colleges struggle to meet staffing and documentation requirements, encouraging demand for managed compliance services. As enforcement penalties escalate, leadership teams increasingly link budget approvals to demonstrated compliance gaps, further propelling platform consolidation.

Rapid Shift to Cloud-Hosted Learning Platforms

With 92% of institutions using cloud services, risk profiles now span multi-tenant applications, third-party APIs, and off-premise IAM tools. K-12 districts cite privacy and security as primary adoption hurdles, yet savings in infrastructure and scalability compel migrations. Cloud security solutions therefore exhibit the highest growth trajectory at 16.04% CAGR. Customer-managed encryption keys, continuous compliance scanning, and SaaS posture management are becoming baseline procurement criteria. Integration challenges encourage institutions to select cloud-native providers that embed education-specific controls, while legacy vendors respond with hybrid security modules to protect both on-campus and cloud workloads.

Proliferation of IoT/OT Devices on Campus

Smart-campus programs introduce an average of 1,350 networked sensors, cameras, and lab instruments per institution, many running proprietary protocols and minimal firmware security.[3]Arista, “Top Private School Relies on NG Firewall,” arista.com Traditional firewalls lack contextual visibility, prompting use of network segmentation and AI-powered behavior analytics. Research facilities add OT safety considerations that demand unified monitoring of cyber-physical systems. Vendor ecosystems now market education-specific IoT discovery and policy engines that auto-isolate anomalous devices. Growing adoption of on-campus 5G and Wi-Fi 7 will magnify device density, requiring dynamic micro-segmentation capabilities and real-time risk scoring to protect sensitive research environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly constrained IT budgets in public institutions | -2.1% | Global, most severe in developing regions and public K-12 | Medium term (2-4 years) |

| Fragmented legacy systems complicate security integration | -1.8% | North America & Europe primary, emerging in APAC | Long term (≥ 4 years) |

| Rising cyber-insurance premiums for education vertical | -1.3% | North America & EU primary, emerging in APAC | Short term (≤ 2 years) |

| Limited cybersecurity awareness among faculty and students | -1.1% | Global, with higher impact in developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Highly Constrained IT Budgets in Public Institutions

Eighty-one percent of K-12 districts report inadequate cybersecurity funding, forcing deferral of essential upgrades and continued reliance on outdated equipment. Public universities balance cybersecurity needs with core academic funding, often resorting to reactive incident response instead of proactive hardening. While managed security services offer operational expenditure flexibility, recurring fees still face scrutiny from boards of education. Vendors responding with modular, subscription-based offerings gain traction in price-sensitive markets. Government grants such as E-rate soften barriers yet rarely cover full lifecycle costs, requiring creative co-investment models and consortium purchasing to stretch limited budgets.

Fragmented Legacy Systems Complicate Security Integration

Universities run mix-version ERP suites, home-grown research platforms, and decades-old laboratory controllers that often lack modern API interfaces. Security teams struggle to implement unified monitoring when protocols are proprietary or unsupported by contemporary SIEM platforms. Technical debt expands attack surfaces and slows zero-trust rollouts. Integration complexity inflates implementation timelines and consulting expenses, discouraging rapid platform replacement. Vendors that offer protocol translation, low-code connectors, and backward-compatible agents position themselves favorably. Over the long term, campuses will need phased decommissioning strategies coupled with middleware layers to reconcile modern security policies with aging infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: IAM Dominance Amid Training Surge

Identity and Access Management retained 27.46% Education & Research Institutions Cybersecurity market share in 2024 as campuses tackled transient user lifecycles and multi-role account provisioning. Security Awareness Training exhibits a 16.83% CAGR to 2030, reflecting recognition that 88% of breaches include a human element. SIEM and Data Loss Prevention continue steady adoption to meet rigorous audit trails and research-data safeguarding requirements.

Institutions emphasize adaptive MFA, delegated account recovery, and automated de-provisioning to reduce credential exposure. Tailored training modules that simulate ransomware, BEC, and social-engineering scenarios resonate with faculty and student audiences. Vendors leveraging gamification and micro-learning show higher engagement metrics. Budget allocations now bundle IAM and training in holistic “people-centric” risk programs, enabling single-vendor negotiations and lower total cost of ownership.

By Deployment Mode: Cloud Acceleration Despite Legacy Constraints

On-premises deployments accounted for 52.69% of Education and Research Institutions Cybersecurity market size during 2024, underlining data-residency rules and sunk infrastructure investments. Cloud-based security, however, is forecast at a 17.05% CAGR, propelled by remote-learning demands and administrative scalability.

Institutions now adopt zero-trust network access and SASE frameworks to secure distributed users without expanding VPN infrastructure. Hybrid models prevail as research data often remains on campus HPC clusters while ERP and collaboration suites migrate to SaaS. Procurement teams favor cloud platforms that provide consumption-based billing and continuous feature updates. Legacy appliance vendors respond with virtualized form factors and managed transition services to preserve customer relationships.

By Security Type: Network Security Leadership Faces Cloud Challenge

Network Security held 28.07% Education and Research Institutions Cybersecurity market share in 2024 thanks to perimeter firewalls, IDS, and segmentation appliances guarding sprawling campus LANs. Cloud Security’s 16.04% CAGR reflects migration of LMS, ERP, and research collaboration to public clouds that require posture management and workload isolation.

Next-generation firewalls integrate encrypted-traffic inspection and application awareness, driving refresh cycles as traffic shifts toward TLS-encrypted SaaS. CASB and cloud workload protection platforms differentiate with auto-classification of sensitive data and cross-tenant anomaly detection. Institutions deploy unified policy engines to extend consistent controls from on-premise networks into IaaS and SaaS environments, reducing configuration drift.

By Institution Type: Universities Lead While MOOCs Accelerate

Universities captured 39.61% Education and Research Institutions Cybersecurity market size in 2024, reflecting complex operational footprints that span academic, research, and healthcare verticals. MOOC providers’ 19.52% CAGR demonstrates the scale of fully online learning platforms managing millions of global learners.

Universities prioritize data-centric controls to protect intellectual property and comply with grant agency mandates. MOOC platforms focus on account integrity and content piracy prevention, selecting cloud-native security stacks for rapid global scaling. K-12 schools leverage federal subsidies but remain hampered by budget cuts, elevating demand for integrated content filtering and endpoint protection bundles. Research institutes procure quantum-safe encryption pilots to future-proof sensitive datasets.

Geography Analysis

North America retained 35.85% Education & Research Institutions Cybersecurity market share in 2024 and is projected to grow at a 15.2% CAGR to 2030, supported by E-rate funding and CISA toolkits that standardize baseline controls. Federal taskforces focus on ransomware readiness, while state programs subsidize threat-hunting services for rural districts. Vendor ecosystems benefit from mature channel partners and proven compliance frameworks.

Asia-Pacific posts the highest regional CAGR at 18.61% through 2030 as governments fund digital campuses and national cybersecurity centers. Australia’s USD 10 million Cyber Cooperation Program highlights public-private collaboration on education-sector resilience. China accelerates smart-campus rollouts, Japan invests in quantum-safe research networks, and India emphasizes low-cost cloud security models for emerging universities. Diversity of maturity levels requires modular solution portfolios that scale from basic endpoint hygiene to advanced SOC automation.

Europe balances GDPR stringency with fiscal austerity, resulting in steady but moderate adoption of privacy-centric security suites. The United Kingdom spearheads quantum-internet pilots valued at GBP 160 million (USD 201 million), aiming to protect high-value research collaborations. Smaller EU members leverage regional funding pools for shared SOC services, while cross-border data transfer rules drive strong encryption and key-management spending. Vendor success depends on localized data-hosting options and adherence to Schrems II guidelines.

Competitive Landscape

The Education and Research Institutions Cybersecurity market remains moderately fragmented as global platform vendors compete with niche education specialists. Palo Alto Networks’ acquisition of IBM QRadar cloud assets illustrates consolidation aimed at expanding threat-analytics depth and education customer reach. Cisco, Microsoft, and Fortinet leverage broad portfolios to secure campus networks, while Okta and Identity Automation emphasize role-based access frameworks tuned for transient student populations.

Differentiation hinges on education-specific compliance automation, LMS integrations, and student privacy dashboards. Managed security services gain ground as 61% of institutions report only two or fewer dedicated security staff, prompting outsourcing of 24/7 monitoring. Start-ups focusing on IoT asset discovery, AI-driven phishing simulation, and quantum-safe encryption attract venture funding due to clear sector pain points. Vendor partnerships increasingly pair connectivity providers with security platforms, as seen in the AT&T and Palo Alto Networks SASE alliance that bundles secure access with AI-based threat prevention.

Pricing pressure persists in K-12 and vocational segments, motivating vendors to offer consumption-based licenses and grant-aligned discounts. Universities demand cross-platform analytics that merge firewall telemetry, cloud logs, and IAM events into single data lakes. Vendors demonstrating measurable risk-reduction metrics and insurance premium impact secure multi-year renewals, while product roadmaps featuring quantum-ready modules and ed-tech APIs improve competitive positioning.

Education And Research Institutions Cybersecurity Industry Leaders

Cisco Systems Inc.

Palo Alto Networks Inc.

Check Point Software Technologies Ltd.

Fortinet Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Accenture completed its tenth acquisition of 2025 with TalentSprint and Ascendient Learning, strengthening its LearnVantage platform to help enterprises and universities reskill workforces in AI and cybersecurity.

- July 2025: Heriot-Watt University secured leadership of the UK’s GBP 160 million (USD 201 million) Integrated Quantum Networks Hub, advancing quantum-internet research aimed at mitigating cybercrime costs in education.

- May 2025: VTT Research launched the EUR 6.3 million (USD 6.8 million) BLimPQC project to develop quantum-safe encryption, partnering with Finnish universities and vendors.

- April 2025: AT&T and Palo Alto Networks announced a strategic SASE partnership that combines secure connectivity and AI-powered threat protection for educational institutions.

Global Education And Research Institutions Cybersecurity Market Report Scope

| Identity and Access Management (IAM) |

| Endpoint Security |

| Network Security/Firewall |

| Security Information and Event Management (SIEM) |

| Data Loss Prevention (DLP) |

| On-premises |

| Cloud-based |

| Network Security |

| Application Security |

| Cloud Security |

| Content Security |

| Endpoint Security |

| K-12 Schools |

| Universities and Colleges |

| Research Institutes and Labs |

| Massive Open Online Course (MOOC) Providers |

| Other Institution Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Identity and Access Management (IAM) | ||

| Endpoint Security | |||

| Network Security/Firewall | |||

| Security Information and Event Management (SIEM) | |||

| Data Loss Prevention (DLP) | |||

| By Deployment Mode | On-premises | ||

| Cloud-based | |||

| By Security Type | Network Security | ||

| Application Security | |||

| Cloud Security | |||

| Content Security | |||

| Endpoint Security | |||

| By Institution Type | K-12 Schools | ||

| Universities and Colleges | |||

| Research Institutes and Labs | |||

| Massive Open Online Course (MOOC) Providers | |||

| Other Institution Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will spending on cybersecurity reach in education and research by 2030?

Spending is projected to rise to USD 11.07 billion by 2030, supported by a 15.35% CAGR driven by cloud adoption, compliance mandates, and ransomware risk.

Which solution category leads current purchasing decisions in higher education?

Identity and Access Management leads, holding 27.46% share in 2024, as campuses prioritize robust credential governance.

Which deployment model is growing fastest among universities and K-12 districts?

Cloud-based security tools are expanding at a 17.05% CAGR because they simplify remote-learning support and lower maintenance overhead.

Which geographic region is showing the strongest growth momentum?

Asia-Pacific is advancing at an 18.61% CAGR thanks to government-backed digital-campus programs and large-scale cloud migrations.

Why are managed security services gaining traction in academic environments?

With 61% of institutions reporting two or fewer dedicated security staff, outsourcing 24/7 monitoring helps close talent gaps and meet insurance prerequisites.

What is the fastest-growing solution type through 2030?

Security Awareness Training is forecast to rise at a 16.83% CAGR as schools address the human factors behind most breaches.

Page last updated on: